Dental Fluoride Treatment Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 13.31 Billion |

| Market Size (2031) | USD 17.29 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

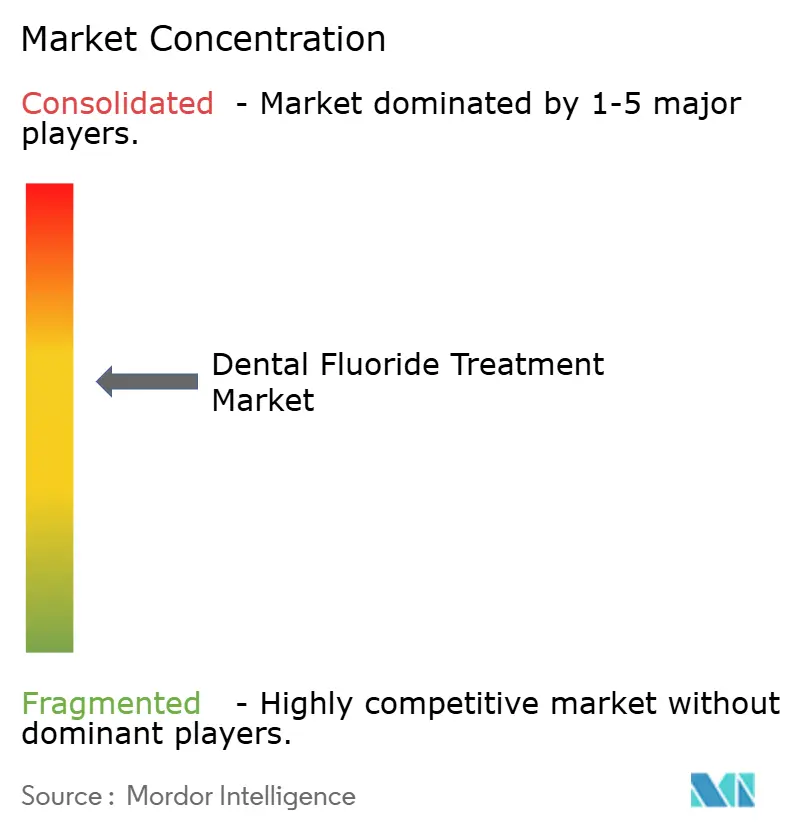

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Fluoride Treatment Market Analysis by Mordor Intelligence

The dental fluoride treatment market size was valued at USD 12.63 billion in 2025 and estimated to grow from USD 13.31 billion in 2026 to reach USD 17.29 billion by 2031, at a CAGR of 5.38% during the forecast period (2026-2031). Europe holds the largest regional share at 32.34% in 2024, sustained by strong preventive-care reimbursement and long-established clinical protocols. Asia-Pacific is advancing at a 7.35% CAGR on the back of rapid urbanization, growing oral-health literacy, and an expanding network of private dental clinics. Toothpaste formulations dominate with 38.23% share, while silver diamine fluoride leads in growth at 6.01% CAGR due to its non-invasive caries-arrest benefits in children and seniors. The May 2025 FDA decision to withdraw ingestible pediatric fluoride supplements is steering innovation toward topical products and bioactive delivery platforms, creating new competitive opportunities[1]Source: U.S. Food and Drug Administration, “FDA Begins Action To Remove Ingestible Fluoride Prescription Drug Products for Children from the Market,” fda.gov .

Key Report Takeaways

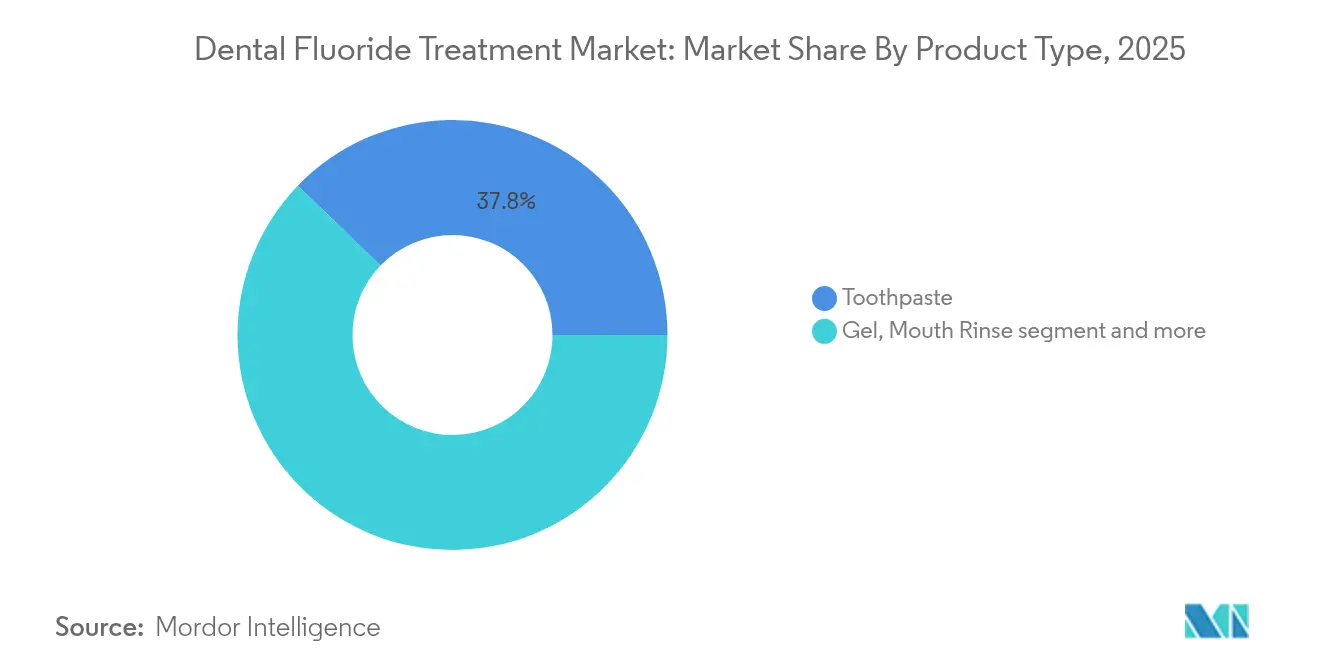

- By product type, toothpaste held 37.78% of the dental fluoride treatment market share in 2025, while silver diamine fluoride is projected to grow at a 5.74% CAGR to 2031.

- By application, caries prevention accounted for 60.84% share of the dental fluoride treatment market size in 2025; dentinal hypersensitivity treatment is forecast to expand at 6.21% CAGR through 2031.

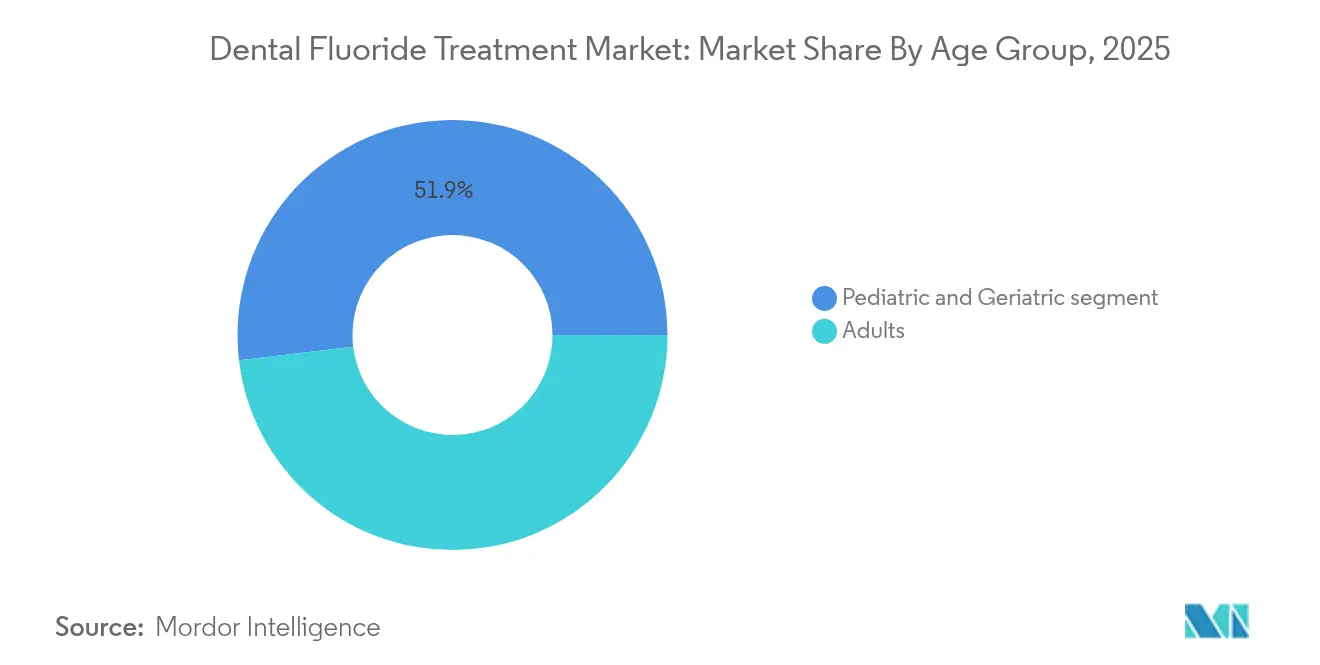

- By age group, adults represented 48.12% share in 2025, whereas the geriatric segment is rising at a 6.78% CAGR over 2026-2031.

- By end user, dental clinics led with 53.86% revenue share in 2025; home-care/OTC use is the fastest-growing channel at 6.6% CAGR.

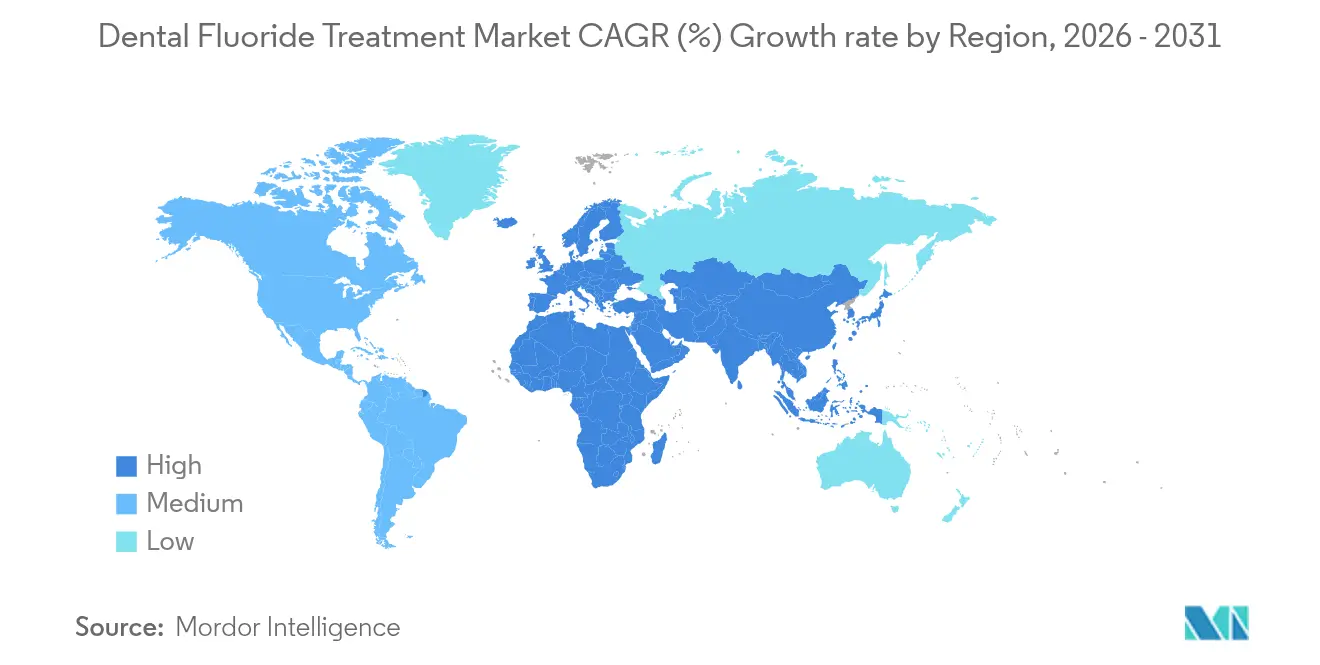

- By geography, Europe commanded 31.95% of the dental fluoride treatment market share in 2025, yet Asia-Pacific is set to climb at 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Dental Fluoride Treatment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries worldwide | +1.2% | Global, strongest in Asia-Pacific & Latin America | Long term (≥ 4 years) |

| Government reimbursement policies for preventive fluoride varnish | +0.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Advances in high-adhesion fluoride delivery systems | +0.6% | Global, led by North America & Europe | Medium term (2-4 years) |

| Growing adoption of minimally-invasive dentistry protocols | +0.5% | Global, early uptake in developed markets | Long term (≥ 4 years) |

| State-level mandates expanding fluoride-varnish coverage | +0.3% | North America (selected states) | Short term (≤ 2 years) |

| Bioactive glass-enhanced varnishes targeting geriatric caries | +0.4% | Global, aging populations in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries Worldwide

Dental caries affects an estimated 2.3 billion individuals, underpinning persistent demand for fluoride-based prevention. Incidence is accelerating in emerging economies where diets high in processed sugars outpace access to professional dental care. The World Health Organization’s 2021 endorsement of silver diamine fluoride highlights its suitability as a scalable, low-cost intervention, especially in resource-constrained settings. Clinical data show 38% silver diamine fluoride can halt roughly 70% of active lesions, reducing the need for restorative procedures. Pediatric and geriatric cohorts benefit most, given their higher caries vulnerability and treatment barriers. Continuous global surveillance of caries prevalence is therefore expected to sustain growth momentum for the dental fluoride treatment market.

Government Reimbursement Policies for Preventive Fluoride Varnish

Shift toward value-based healthcare is broadening insurance coverage for professional fluoride varnish. Integration of varnish application within primary-care workflows allows trained medical staff to deliver interventions cost-effectively, extending reach beyond dental offices. Longitudinal studies indicate varnish use can cut coronal caries by 27% and root caries by 23% in community-dwelling elders. Standardized clinical guidelines from the American Dental Association further streamline provider adoption, encouraging insurers to reimburse evidence-backed preventive care. As Medicaid and private payers scale coverage, varnish utilization is poised to rise, elevating topical fluoride consumption across age groups.

Advances in High-Adhesion Fluoride Delivery Systems

Technological innovation focuses on retention time and sustained release. Chitosan-modified varnish exhibits superior viscosity and prolonged fluoride elution compared with conventional formulas. Nanoscale carriers such as hollow mesoporous silica curb erosive dentin loss by 75% relative to sodium fluoride gels[2]Source: J-M Chen et al., “Enhancing the Inhibition of Dental Erosion With Quercetin-Encapsulated Nanocomposites,” frontiersin.org . Calcium-phosphate-fortified systems extend bioavailable fluoride for up to 24 hours and aid apatite regeneration. These advances create differentiation opportunities, enabling manufacturers to command premium pricing while delivering measurable clinical improvements.

Growing Adoption of Minimally-Invasive Dentistry Protocols

Current treatment paradigms favor remineralization over restoration in early lesions. Regulatory clearance of Curodont Repair Fluoride Plus underscores acceptance of non-operative enamel therapy. AI-enhanced diagnostics identify incipient lesions sooner, allowing tailored fluoride application before cavitation. Cost-effectiveness models demonstrate higher lifetime savings when early fluoride therapy replaces drilling. Adoption of minimally-invasive protocols is therefore expanding the therapeutic addressable market, reinforcing long-term demand for high-performance fluoride products.

Restraints Impact Analysis of Dental Fluoride Treatment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluorosis risk driving stricter dosage guidelines | -0.7% | Global, with highest impact in regions with natural fluoride exposure | Medium term (2-4 years) |

| Consumer shift toward fluoride-free oral-care products | -0.5% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Supply-chain volatility for pharmaceutical-grade sodium fluoride | -0.4% | Global, with highest vulnerability in import-dependent regions | Short term (≤ 2 years) |

| Environmental scrutiny on fluoride effluent from dental offices | -0.3% | North America & Europe, with emerging concerns in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluorosis Risk Driving Stricter Dosage Guidelines

Growing scrutiny of fluoride safety is prompting regulators to tighten pediatric dosage recommendations. The May 2025 FDA action to pull concentrated supplements cited potential gut microbiome disruption and neurodevelopmental concerns. Epidemiological data link high systemic intake during enamel formation to irreversible fluorosis, resulting in mottling and aesthetics-driven quality-of-life impacts. Consequently, producers must invest in precision-dosing formats and transparent labeling to reassure clinicians and consumers. Stricter limits could temper overall volume growth, even while stimulating innovation in safer topical delivery.

Consumer Shift Toward Fluoride-Free Oral-Care Products

Health-conscious shoppers increasingly associate “natural” claims with safety, moving some demand toward fluoride-free pastes and gels. Florida and Utah bans on water fluoridation amplify public debate, reinforcing skepticism despite decades of supportive research. Manufacturers of fluoride products therefore need targeted education campaigns and expanded R&D into biocompatible additives to defend market share against alternative remineralization technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Dental Fluoride Treatment Market Segment Analysis

By Product Type:

Silver Diamine Fluoride Drives InnovationSilver diamine fluoride posted a 5.74% CAGR outlook, outperforming the broader dental fluoride treatment market. Clinical studies showing 70% lesion-arrest efficacy underpin adoption in school-based sealant programs and geriatric facilities. Toothpaste remains the volume anchor with 37.78% of dental fluoride treatment market share in 2025, benefiting from daily-use frequency and established consumer trust. Varnish formulations are gaining ground as professional standards evolve toward quarterly high-fluoride applications, leveraging sustained-release profiles validated by 24-hour elution testing. Gel and foam formats continue serving niche roles in custom trays and chairside prophylaxis but face substitution from high-adhesion varnishes. Mouth rinses enjoy moderate growth, driven by convenience-oriented adults seeking incremental fluoride exposure between hygiene visits. Hydrogel patches and nano-carrier sprays represent pipeline innovations, offering targeted therapy for orthodontic brackets and interproximal sites.

Growing silver diamine fluoride uptake is catalyzing new delivery form factors, including single-dose applicators that limit cross-contamination and simplify billing in community clinics. Retail toothpaste innovation centers on higher-ppm fluoride bands and calcium-phosphate co-formulations, aiming to retain loyal users amid fluoride-free competition. Chewable tablets are declining after the FDA supplement withdrawal, prompting pediatric dentists to shift toward varnish during medical well-child appointments. Overall, toothpaste will likely preserve a dominant revenue role, yet product diversification enlarges the total dental fluoride treatment market, especially in emerging economies adopting evidence-based caries-arrest protocols.

By Application:

Caries Prevention Dominates While Hypersensitivity GrowsCaries prevention held 60.84% of the dental fluoride treatment market size in 2025, reflecting its centrality in public-health dentistry. Professional guidelines advocating biannual varnish for moderate-risk adults assure stable demand across developed regions. Dentinal hypersensitivity treatments, advancing at 6.21% CAGR, leverage fluoride’s tubule-occluding and nerve-calming properties. High-fluoride rinses and bioactive glass pastes are capturing patients dissatisfied with potassium-nitrate alternatives. Enamel remineralization occupies a rising niche as AI imaging detects early white-spot lesions, allowing non-invasive fluoride infiltration therapies such as Curodont Repair Fluoride Plus. Root-caries management gains salience with global aging; fluoride gel trays combined with chlorhexidine rinse show promising root-surface hardening in elders with dexterity limitations.

In hypersensitivity, premium SKU pricing offsets lower unit volumes, encouraging firms to incorporate arginine, calcium silicate, or stannous compounds for faster relief. Early remineralization therapies rely on dentist-led education to shift mindsets from drill-and-fill to preserve-and-protect. Public-sector programs in Latin America increasingly fund high-fluoride gel for schoolchildren, aiming to cut untreated decay prevalence. As preventive-first paradigms consolidate, overlapping indications blur lines among applications, yet the high share of caries prevention ensures continued bulk purchasing of basic fluoride formulations.

By Age Group:

Geriatric Segment Accelerates GrowthAdults accounted for 48.12% revenue in 2025, reflecting routine hygiene visits and over-the-counter purchases. However, seniors aged 65+ form the fastest-growing demographic, expanding at 6.78% CAGR as global life expectancy rises. Only 7% of high-risk elders currently receive fluoride interventions, representing a sizeable untapped pool. Xerostomia-induced caries, root exposure, and institutional-care settings create distinct therapeutic needs addressed by 5,000 ppm toothpaste and high-viscosity varnish. Pediatric demand is reshaping after ingestible supplement withdrawal; topical modalities now dominate, administered by medical providers during immunization visits.

Manufacturers are designing age-tailored packaging with arthritis-friendly caps for seniors and flavor-free low-foam formulas for dysphagia patients. Pediatric product portfolios emphasize taste masking and cartoon branding while ensuring safe fluoride dosing. Adult consumers exhibit brand loyalty but increasingly opt for whitening-plus-fluoride hybrids. Across age brackets, digital reminders and subscription bundles encourage adherence, anchoring recurring revenue streams in the dental fluoride treatment market.

By End User:

Home Care Segment Gains MomentumDental clinics led with 53.86% share in 2025, cemented by professional varnish and in-office gel therapies. Pandemic-era disruptions, however, accelerated home-care demand, which is growing at 6.6% CAGR. OTC rinses, high-ppm toothpaste, and do-it-yourself tray kits empower consumers to extend preventive regimens between visits. Hospitals and specialty centers continue delivering fluoride for medically complex cases, yet account for a modest portion of volume.

Scale-up of e-commerce and subscription models enables direct-to-consumer distribution at favorable margins. Dental-service organizations use bundled varnish-plus-AI-diagnostics packages to upsell preventive plans. Government oral-health campaigns distribute fluoride varnish in schools and maternal clinics, broadening reach among underserved groups. Integration of fluoride into non-dental retail—such as pharmacy immunization kiosks—further diversifies channel exposure, enhancing overall resilience of the dental fluoride treatment market.

Geography Analysis

Europe Dental Fluoride Treatment Market

Europe remains the largest regional contributor with a 31.95% share thanks to entrenched preventive protocols, mandatory insurance coverage, and strict product-safety regulation. High awareness translates into routine professional varnish every six months and near-universal toothpaste penetration. Growth is comparatively modest yet stable, supported by incremental upgrades to sustained-release formulations and expanding senior-care initiatives.

APAC Dental Fluoride Treatment Market

Asia-Pacific leads in growth rate at 6.98% CAGR, propelled by urban middle-class expansion and aggressive public-health programs in China and India. Government subsidies for school-based varnish, domestic manufacturing incentives, and the proliferation of private clinics are key drivers. However, rural-urban disparities and dentist shortages temper full potential. Multinationals are partnering with local producers to navigate price-sensitive segments while complying with divergent regulatory standards.

North America, LATAM and MEA Dental Fluoride Treatment Market

North America shows mixed dynamics. Robust evidence-based practice supports premium product uptake, but state-level fluoridation bans in Florida and Utah introduce policy uncertainty, prompting municipalities to explore alternative topical delivery. Medicaid expansion of fluoride-varnish coverage in medical offices mitigates risks by sustaining public-sector demand. Latin America and the Middle East & Africa collectively represent emerging opportunities, characterized by low baseline penetration yet high disease burden. International NGOs and multilaterals financing school sealant programs are seeding demand, setting the stage for gradual uptake of professional fluoride products.

Competitive Landscape

The dental fluoride treatment market shows moderate concentration, with diversified personal-care multinationals vying alongside dental-focused specialists. Procter & Gamble, Johnson & Johnson, and Colgate-Palmolive leverage global distribution and brand equity in toothpaste, jointly controlling a sizable share of consumer channels. Professional segments are led by 3M, GC, and Dentsply Sirona, whose R&D emphasizes varnish adhesion, nano-carrier gels, and calcium-phosphate synergy.

Strategic collaborations are a defining trend. Henry Schein’s exclusive deal with vVARDIS aligns AI diagnostics from VideaHealth with drill-free fluoride therapy, producing a vertically integrated caries-management offering. Similar alliances pair manufacturers with imaging-software vendors to bundle early-detection tools and targeted fluoride delivery, enhancing practice revenue while improving clinical outcomes. Patent filings at the USPTO reveal growing focus on sustained-release fluoride matrices and fluoride-plus-bioactive-glass composites, signaling sustained innovation spending despite regulatory headwinds.

Supply-chain vulnerability remains a shared concern. Roughly 63% of fluorosilicic acid, a key precursor, derives from phosphate fertilizer by-product streams in Florida, making manufacturers susceptible to hurricane-season disruptions. Companies diversify sourcing through shipments from Morocco and China, yet logistics costs and purity variance affect margins. Meanwhile, natural-care disruptors such as ORALPEACE market fluoride-free lines to capture wellness consumers, nudging incumbents to expand biocompatible portfolios. Competitive positioning therefore hinges on balanced investment in next-generation fluoride innovation and credible alternatives that hedge against shifting consumer attitudes.

Dental Fluoride Treatment Industry Leaders

Philips

Colgate

DMG Dental

VOCO GmbH

Dentsply Sirona

- *Disclaimer: Major Players sorted in no particular order

Dental Fluoride Treatment Market Companies Covered in this Report

- 3M

- Colgate-Palmolive Company

- Dentsply Sirona

- GC Corporation

- Ivoclar Vivadent

- Ultradent Products

- Centrix Inc.

- Henry Schein

- Preventech

- Young Innovations

- VOCO

- Pulpdent Corporation

- Premier Dental Products

- Kuraray Noritake Dental

- Keystone Industries

- Medicom

- Darby Dental Supply

- Crosstex International

- Elevate Oral Care

- Oral BioTech

- SDI

- Church & Dwight (Arm & Hammer)

- Sunstar Group

- DSI Dental Solutions Israel

- Rising Pharma Holdings

- Benco Dental

- PureLife Dental

- Patterson Dental

Recent Industry Developments in Dental Fluoride Treatment Market

- June 2025: FDA opens public docket and schedules July 23, 2025 hybrid meeting to discuss orally ingestible fluoride use in children, aiming to refine clinical guidelines

- May 2025: FDA removes concentrated ingestible pediatric fluoride products, setting October 31, 2025 deadline for comprehensive safety review.

Dental Fluoride Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the dental fluoride treatment market as all professional-grade and consumer fluoride preparations, such as varnishes, gels, foams, rinses, toothpastes, silver diamine fluoride, and chewable tablets, that are formulated to remineralize enamel, curb dentinal hypersensitivity, or prevent primary and root caries in children and adults. Measurements are provided in US-dollar value at manufacturer selling price, covering retail, e-commerce, dental-office, and institutional channels across 25 countries.

Exclusions: Bulk fluoride feedstocks used for municipal water-fluoridation schemes and generic toothbrushes or floss are outside our scope.

Segments Covered in This Report

- By Product Type

- Toothpaste

- Gel

- Mouth Rinse

- Varnish

- Silver Diamine Fluoride

- Chewable Tablets

- Novel Hydrogel & Other Delivery Systems

- By Application

- Caries Prevention

- Dentinal Hypersensitivity Treatment

- Enamel Remineralization

- Root-caries Management

- By Age Group

- Pediatric

- Adult

- Geriatric

- By End User

- Dental Clinics

- Hospitals

- Home-care / OTC Use

- Other Institutional Care (Schools, Public Health)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middel East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed practicing dentists, preventive-care product managers, and public-health officials across North America, Europe, Asia-Pacific, and Latin America. Conversations probed unit consumption per patient group, emerging silver-diamine protocols, reimbursement uptake, and expected average price shifts, which sharpened our assumptions and bridged regional data gaps.

Desk Research

We began by mapping national oral-health surveys and caries prevalence data released by bodies such as the WHO Global Oral Health Data Bank, the CDC's National Health and Nutrition Examination Survey, Eurostat, and Japan's Ministry of Health. Trade flows for HS 330610 (dentifrices) and HS 330690 (mouthrinses) from UN Comtrade helped gauge cross-border supply, while import price trends from Volza clarified average selling prices. Clinical-trial registries, PubMed journals on fluoride efficacy, and filings on Form 10-K gave further volume and pricing clues. Data pulls from D&B Hoovers and Dow Jones Factiva provided company-level revenue splits that anchored channel weights. The sources cited above are illustrative, not exhaustive; many other databases and industry portals fed our desk research.

Market-Sizing & Forecasting

A top-down demand pool was built by pairing country-level caries incidence with treatment penetration and dosing frequency. Select bottom-up checks, supplier roll-ups of fluoride-varnish vials, sampled OTC ASP × units, and clinic inventory audits validated totals and corrected outliers. Key model drivers include: 1) treated-caries prevalence, 2) per-capita toothpaste and varnish consumption, 3) reimbursement coverage ratios, 4) silver-diamine adoption curve, and 5) retail ASP drift. A multivariate regression linked these drivers to historical market value. Forecasts to 2030 extend the equation under three policy-change scenarios agreed upon with expert respondents. Gaps where bottom-up evidence was thin were adjusted to the mid-point of the scenario band.

Data Validation & Update Cycle

Outputs pass through variance checks versus trade, retail-scanner, and payer reimbursement data before senior analyst sign-off. Reports refresh annually, and we trigger interim updates when regulatory, epidemiological, or pricing shifts exceed preset thresholds, ensuring clients receive the latest view.

How Mordor Intelligence's Dental Fluoride Treatment Market Size Compares to Other Published Estimates

Published figures often diverge because firms mix preventive products with water-fluoridation infrastructure, apply different ASP benchmarks, or freeze exchange rates.

Key gap drivers include scope creep into systemic fluoride spend, reliance on press-release pricing, and models updated on multi-year cadences that miss rapid silver-diamine uptake or reimbursement changes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.63 Bn (2025) | Mordor Intelligence | - |

| USD 14.8 Bn (2025) | Global Consultancy A | Adds OTC rinses and floss; single-scenario model; infrequent refresh |

| USD 16.19 Bn (2025) | Trade Journal B | Combines water-fluoridation capital spend; minimal primary validation; 2022 FX rates locked |

The comparison shows that once differing scopes and dated inputs are stripped away, Mordor's disciplined variable selection and yearly review cycle deliver a balanced, transparent baseline that stakeholders can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the projected value of the dental fluoride treatment market by 2031?

The dental fluoride treatment market is forecast to reach USD 17.29 billion by 2031 at a 5.38% CAGR.

Which region will grow the fastest through 2031?

Asia-Pacific is expected to record the highest CAGR of 6.98%, driven by expanding dental infrastructure and rising oral-health awareness.

Why is silver diamine fluoride gaining traction?

Clinical evidence shows it can arrest about 70% of active caries without drilling, making it attractive for pediatric and geriatric care programs.

How are regulatory changes affecting product demand in North America?

State bans on water fluoridation and the FDA withdrawal of ingestible supplements are shifting demand toward topical fluoride varnishes and high-fluoride toothpaste.

Which end-user segment is expanding the quickest?

Home-care and over-the-counter channels are growing at 6.6% CAGR as consumers adopt self-administered preventive products between professional visits.

Page last updated on: