Single Tooth Implants And Dental Bridges Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

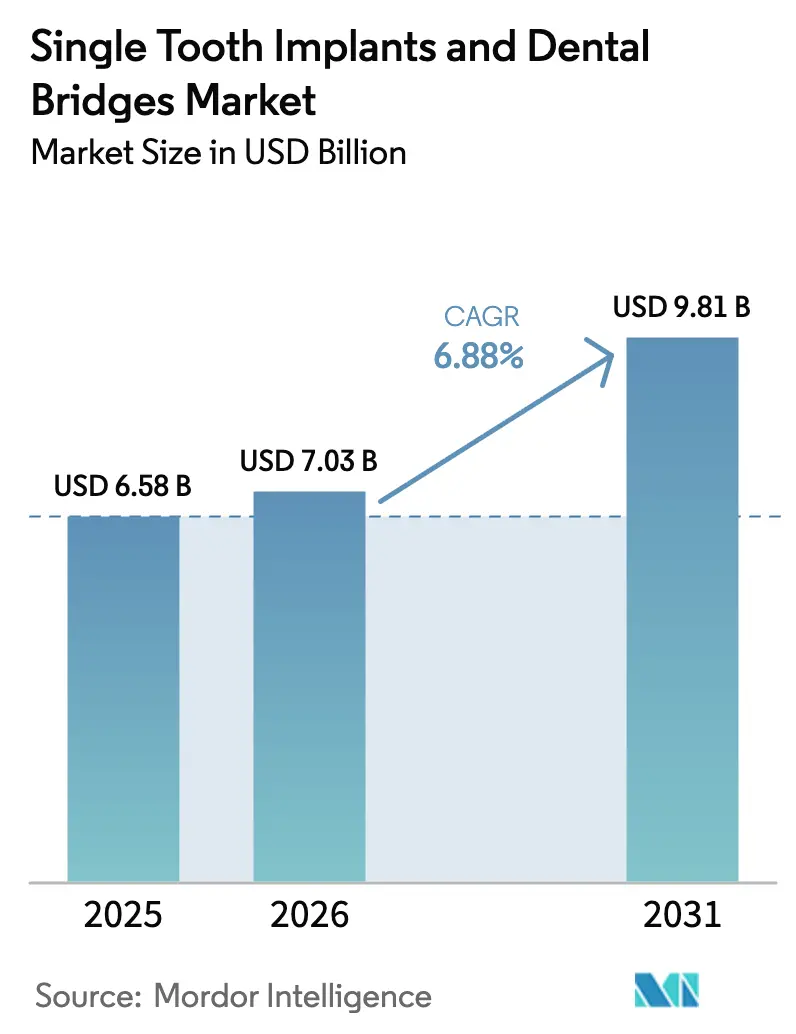

| Market Size (2026) | USD 7.03 Billion |

| Market Size (2031) | USD 9.81 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

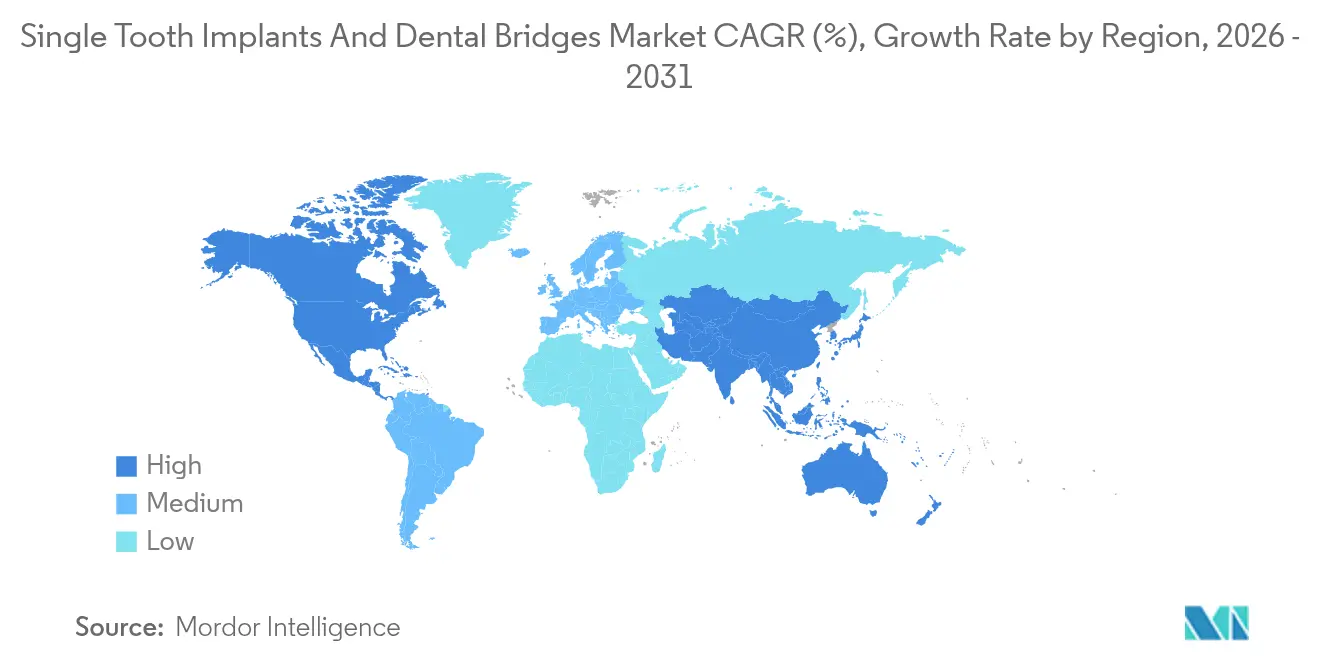

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Single Tooth Implants And Dental Bridges Market Analysis by Mordor Intelligence

The single tooth implants and dental bridges market size was valued at USD 6.58 billion in 2025 and estimated to grow from USD 7.03 billion in 2026 to reach USD 9.81 billion by 2031, at a CAGR of 6.88% during the forecast period (2026-2031). A confluence of population aging, expanding aesthetic expectations, and digitally enabled chairside production methods underpins this trajectory, with metal-based systems still dominant yet ceramic alternatives gaining traction [1]Institut Straumann AG, “Annual Report 2024,” straumann.com . North America retains scale leadership, while Asia-Pacific records the sharpest uptake thanks to disposable-income growth and medical-tourism accords. Top manufacturers emphasize integrated CAD/CAM ecosystems that allow same-day restorations, reshaping practice economics and lifting case-acceptance rates. On the supply side, titanium and zirconia sourcing risks, along with a shortage of certified implantologists in emerging economies, temper the otherwise optimistic outlook.

Key Report Takeaways

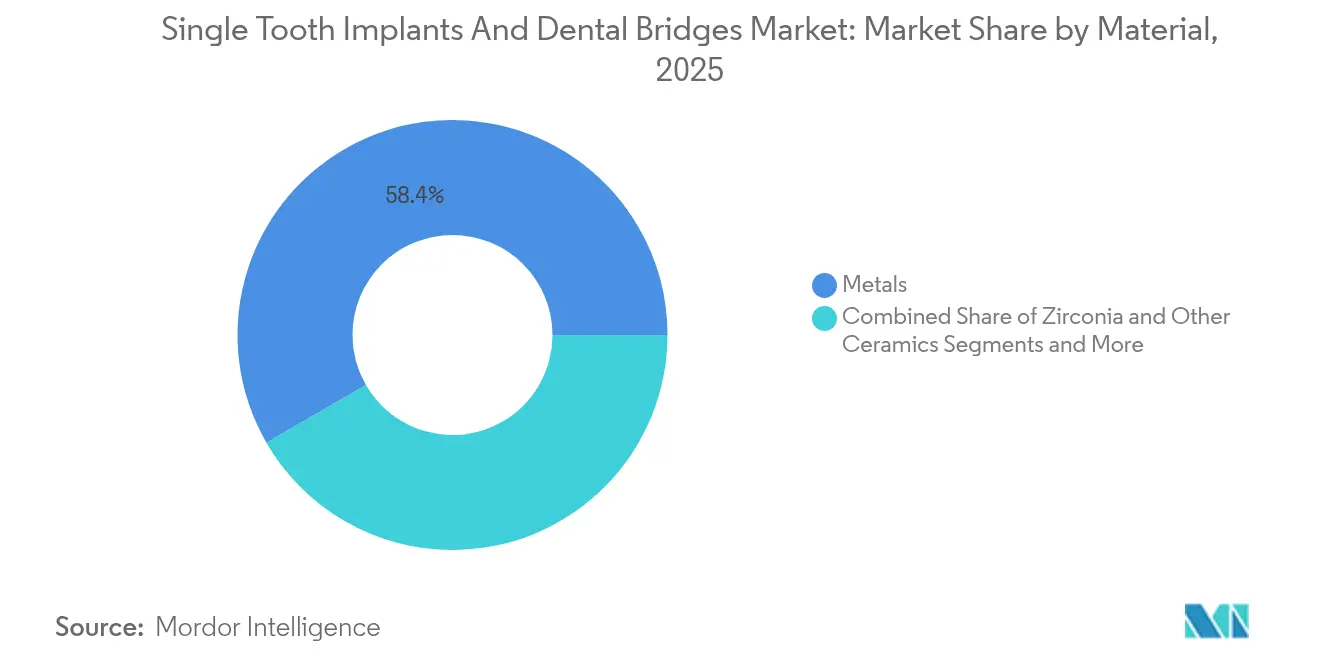

- By material, metals led with 58.35% revenue share in 2025; zirconia and other ceramics are projected to expand at a 7.22% CAGR to 2031.

- By product, single tooth implants captured 62.60% of the single tooth implants and dental bridges market share in 2025, while dental bridges are forecast to grow at 7.31% CAGR through 2031.

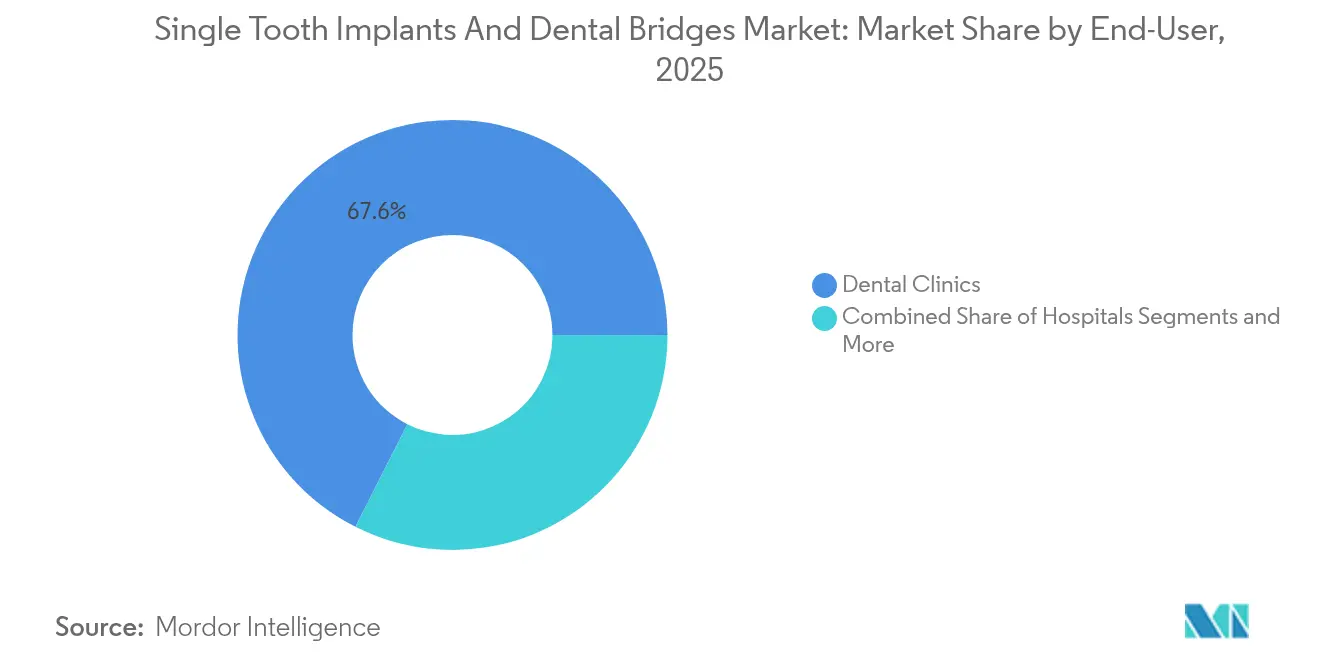

- By end-user, dental clinics commanded 67.55% share of the single tooth implants and dental bridges market size in 2025, whereas hospitals post the highest projected CAGR at 7.46% for 2026-2031.

- By geography, North America accounted for 40.78% revenue share in 2025; Asia-Pacific is advancing at a 7.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single Tooth Implants And Dental Bridges Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for preventive & cosmetic dentistry | +1.2% | Global, with premium segments in North America & Europe | Medium term (2-4 years) |

| Increasing prevalence of edentulous & geriatric population | +1.8% | Global, concentrated in aging societies of Japan, Germany, Italy | Long term (≥ 4 years) |

| Rapid adoption of digital workflows | +1.4% | North America & Europe leading, APAC catching up | Short term (≤ 2 years) |

| Growing insurance coverage & value-based dental care models | +0.9% | North America primarily, expanding to Europe | Medium term (2-4 years) |

| Proliferation of chair-side milling enabling same-day bridges | +0.8% | Global, concentrated in developed markets with digital infrastructure | Short term (≤ 2 years) |

| Expansion of dental-tourism clusters via bilateral health accords | +0.6% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Preventive & Cosmetic Dentistry

Urban consumers prioritize early intervention that preserves natural tooth structure and delivers high-end esthetics. The American Dental Association recorded 23% growth in cosmetic procedures in 2024, and single-unit implants are increasingly preferred over tooth-supported bridges because they leave adjacent teeth untouched [2]American Dental Association, “Cosmetic Dentistry Trends Report 2024,” ada.org . Digital smile-design tools align clinical and esthetic goals, while intraoral scanners combined with chairside mills reduce chair time, spurring same-day delivery and higher patient satisfaction. Premium implant materials, especially zirconia, meet esthetic demands in anterior zones and command pricing power. Practices that bundle preventive services with implant therapy achieve stronger lifetime patient value, reinforcing the single tooth implants and dental bridges market’s upward curve.

Increasing Prevalence of Edentulous & Geriatric Population

Global longevity keeps demand robust, as 23% of adults aged 65-74 were fully edentulous in 2024 [3]World Health Organization, “Global Health Observatory – Oral Health,” who.int . Immediate-loading protocols show >96% success when comorbidities are controlled, positioning implants as the preferred solution for aging patients. Hydrophilic and bioactive surface technologies improve outcomes in osteoporotic bone, while minimally invasive, outpatient-ready procedures dovetail with aging-in-place care models. Consequently, the single tooth implants and dental bridges market receives a structural tailwind from demographic momentum.

Rapid Adoption of Digital Workflows

Clinics using fully integrated CAD/CAM systems recorded 34% higher case-acceptance rates in 2024. Sub-50 µm scanner accuracy underpins reliable restorative fits, and AI-driven design modules shave design cycles by 60%. Open-architecture platforms let clinicians source affordable blanks without compromising quality, expanding access in cost-sensitive markets. Same-day bridges created via chairside milling reshape patient expectations, keeping the single tooth implants and dental bridges market on its digital fast track.

Growing Insurance Coverage & Value-Based Dental Care Models

Seventy-eight percent of Medicare Advantage plans covered implants in 2024, elevating volumes among older adults. Private insurers view implants’ lower lifetime maintenance cost as economically sound, fostering bundled-payment pilots that favor multi-unit implant bridges. Digital documentation platforms provide outcome data that supports value-based contracting, anchoring reimbursement expansion and stimulating the single tooth implants and dental bridges market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost & limited reimbursement | -1.1% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Shortage of skilled implantologists in emerging economies | -0.7% | APAC, Latin America, parts of MEA | Long term (≥ 4 years) |

| Titanium & zirconia supply-chain volatility from geo-political tensions | -0.5% | Global, with acute impact on European and North American manufacturers | Short term (≤ 2 years) |

| Stricter ESG limits on precious-metal use in PFM restorations | -0.3% | Europe and North America primarily, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost & Limited Reimbursement

Implant therapy costs USD 3,000–6,000 per tooth, far exceeding typical annual dental-benefit caps of USD 1,500, leaving a funding shortfall that curbs adoption. Financing plans fill gaps but carry 17.9% average interest, making them less appealing to middle-income patients. Although value-based care models propose bundled payment structures, uptake remains confined to large, integrated health systems. As long as out-of-pocket exposure stays high, demand elasticity will cap upside in price-sensitive regions.

Shortage of Skilled Implantologists in Emerging Economies

Low- and middle-income countries report an implantologist density below 8% of the dental workforce, creating service bottlenecks. Training programs demand 12-24 months, a commitment many dentists cannot accommodate. While simplified kits and guided-surgery sleeves shorten learning curves, complex full-arch reconstructions still require specialist expertise. Workforce scarcity therefore slows procedure ramp-up in high-growth geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Biocompatible Innovation Drives Differentiation

Metals retained 58.35% of the single tooth implants and dental bridges market share in 2025 thanks to titanium’s four-decade safety record and cost-effective machining. The single tooth implants and dental bridges market size for metals reached USD 3.84 billion that year, reflecting their entrenched clinical acceptance. In contrast, zirconia and other ceramics logged a 7.22% CAGR outlook through 2031, propelled by demand for metal-free esthetics in anterior restorations and growing evidence of favorable soft-tissue response.

Proprietary modifications, such as Nobel Biocare’s hydrophilic surface, narrow survival-rate gaps between zirconia and titanium, with five-year rates approaching 97.3%. Regulatory pathways eased when the FDA broadened 510(k) routes in 2024, unlocking faster market entry for ceramic systems. ESG scrutiny over precious-metal use in porcelain-fused-to-metal crowns further tilts momentum toward ceramics, reinforcing the premium-pricing corridor and elevating brand differentiation strategies inside the single tooth implants and dental bridges market.

By Product: Bridge Configurations Gain Clinical Momentum

Single tooth implants dominated 62.60% of 2025 revenue, equal to USD 4.12 billion of the single tooth implants and dental bridges market size. Their popularity stems from the ability to preserve adjacent tooth structure while delivering long-term durability. Yet implant-supported bridges hold the speed advantage, with a 7.31% CAGR forecast through 2031. Evidence from Institut Straumann’s PRO Arch registry cites 98.2% survival at 3 years for immediate-load full-arch cases.

Digital workflow advances allow pre-surgical virtual wax-ups that streamline guide fabrication, tighten implant parallelism, and support screw-retained prostheses that eliminate cement risks. Such efficiencies resonate with high-volume practices and reinforce bridges as the growth engine within the single tooth implants and dental bridges market.

By End-User: Hospital Integration Accelerates Adoption

Dental clinics held 67.55% revenue share in 2025, equivalent to USD 4.45 billion of the single tooth implants and dental bridges market size. Clinics benefit from specialized staff and flexible pricing, but growth momentum is shifting toward hospitals that post a 7.46% CAGR forecast to 2031. Hospital programs integrate oral-surgery suites with imaging departments, enabling complex grafting and oncology-related reconstructions under one roof.

University-affiliated centers push translational research; Penn Dental Medicine, for instance, shortened osseointegration timelines by 40% using bioactive coatings. Institutional settings also facilitate bundled insurance contracts that couple implant therapy with systemic-care pathways, enlarging patient access and deepening the single tooth implants and dental bridges market penetration inside integrated-delivery networks.

Geography Analysis

North America led with 40.78% of 2025 revenues, supported by Medicare Advantage expansions that unlocked implant coverage for 12.4 million seniors. Well-established digital infrastructures speed adoption of chairside workflows, and private insurers increasingly reimburse implant-supported bridges under value-based contracts. U.S. regulatory rigor favors incumbents with the scale to fund clinical trials, thereby concentrating market power.

Europe follows with harmonized EU MDR rules that cut compliance redundancy. Germany reported 847,000 implant procedures in 2024, underpinned by statutory insurance co-payments that offset patient costs. The United Kingdom’s MHRA accelerated ceramic-implant approvals post-Brexit, making it an attractive pilot market for innovative materials. Scandinavian countries, buoyed by state dental benefits, posted the world’s highest per-capita implant placements, reinforcing premium demand for zirconia solutions.

Asia-Pacific is the fastest riser at a 7.54% CAGR forecast, with China’s enhanced insurance plan covering 340 million citizens for restorative dental care. Japan’s geriatric needs spur protocols adapted to osteoporotic bone, while South Korea capitalizes on medical tourism that blends esthetics and competitive pricing. India’s low implantologist density tempers near-term uptake, yet expanding dental-school capacity and public-private training initiatives suggest an inflection point later in the decade. These dynamics collectively enlarge the single tooth implants and dental bridges market footprint across diverse economic contexts.

Competitive Landscape

The single tooth implants and dental bridges market features moderate concentration, with top firms combining proprietary surfaces, digital ecosystems, and extensive clinical proof. Straumann’s 14.3% organic revenue growth in 2024 stems from its seamless scanner-to-mill workflow, positioning the group firmly in the premium implant tier. Dentsply Sirona’s CEREC Primemill processes zirconia crowns in under 15 minutes, enhancing chairside immediacy and nudging share gains in integrated practices. Nobel Biocare broke ground with its FDA-cleared NobelPearl ceramic system, delivering faster osseointegration and satisfying esthetic-zone demand.

Asian entrants such as Osstem and Neobiotech pursue value strategies, leveraging regional manufacturing to price 20-30% below Western peers. Their CE-marked guided-surgery kits shorten chair time by 18 minutes, appealing to volume-driven clinics. Nonetheless, limited long-term data constrains premium adoption in risk-averse markets. ZimVie invests USD 45 million to enlarge Indiana production, focusing on automated quality checks that improve consistency and support North American growth targets.

Single Tooth Implants And Dental Bridges Industry Leaders

-

ZimVie Inc

-

Dentsply Sirona

-

Solventum

-

Ivoclar Vivadent AG

-

Institut Straumann AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Institut Straumann AG acquired Anthogyr SAS for EUR 193 million (USD 205 million), adding the Axiom implant line and digital solutions to its European portfolio.

- September 2024: Dentsply Sirona unveiled the CEREC Primemill, reducing zirconia-milling cycles to <15 minutes for same-day crowns.

- August 2024: Nobel Biocare gained FDA 510(k) clearance for NobelPearl, the first zirconia implant approved for immediate loading in the U.S.

Global Single Tooth Implants And Dental Bridges Market Report Scope

As per the scope of this report, single-tooth dental implants are permanent fixtures rooted in the jawbone and act as long-term treatments for tooth loss. While dental bridges are fixed prosthetics devices that are used to restore tooth size, strength, and shape to improve tooth appearance. In addition, dental bridges are used to maintain the shape of the face and restore the ability to chew and speak, which are used to prevent remaining teeth from shifting out of position. The Single Tooth Implants and Dental Bridges Market is segmented by Material (Ceramic materials, Metals, Porcelain-Fused-to-Metal (PFM)), Product (Single Tooth Implants and Dental Bridges), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Metals |

| Zirconia & other ceramics |

| Porcelain-Fused-to-Metal (PFM) |

| Single Tooth Implants |

| Dental Bridges |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Metals | |

| Zirconia & other ceramics | ||

| Porcelain-Fused-to-Metal (PFM) | ||

| By Product | Single Tooth Implants | |

| Dental Bridges | ||

| By End-User | Dental Clinics | |

| Hospitals | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the single tooth implants and dental bridges market in 2026?

The sector generated USD 7.03 billion in 2026, reflecting strong demand across restorative and esthetic applications.

What is the expected CAGR for the single tooth implants and dental bridges market through 2031?

The market is projected to grow at a 6.88% CAGR between 2026 and 2031, powered by digital workflow adoption and demographic aging.

Which material segment is growing the fastest?

Zirconia and other ceramics are advancing at a 7.22% CAGR due to superior esthetics and favorable soft-tissue response.

Which region shows the highest growth momentum?

Asia-Pacific posts the strongest outlook with a 7.54% CAGR, fueled by rising incomes and medical-tourism inflows.

Which product type is expanding more rapidly?

Implant-supported dental bridges outpace single units with a 7.31% CAGR, aided by immediate-loading protocols.

Who are the leading companies in this space?

Institut Straumann AG, Dentsply Sirona, Nobel Biocare, ZimVie, and Ivoclar Vivadent collectively account for over half of global revenues.

Page last updated on: