Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

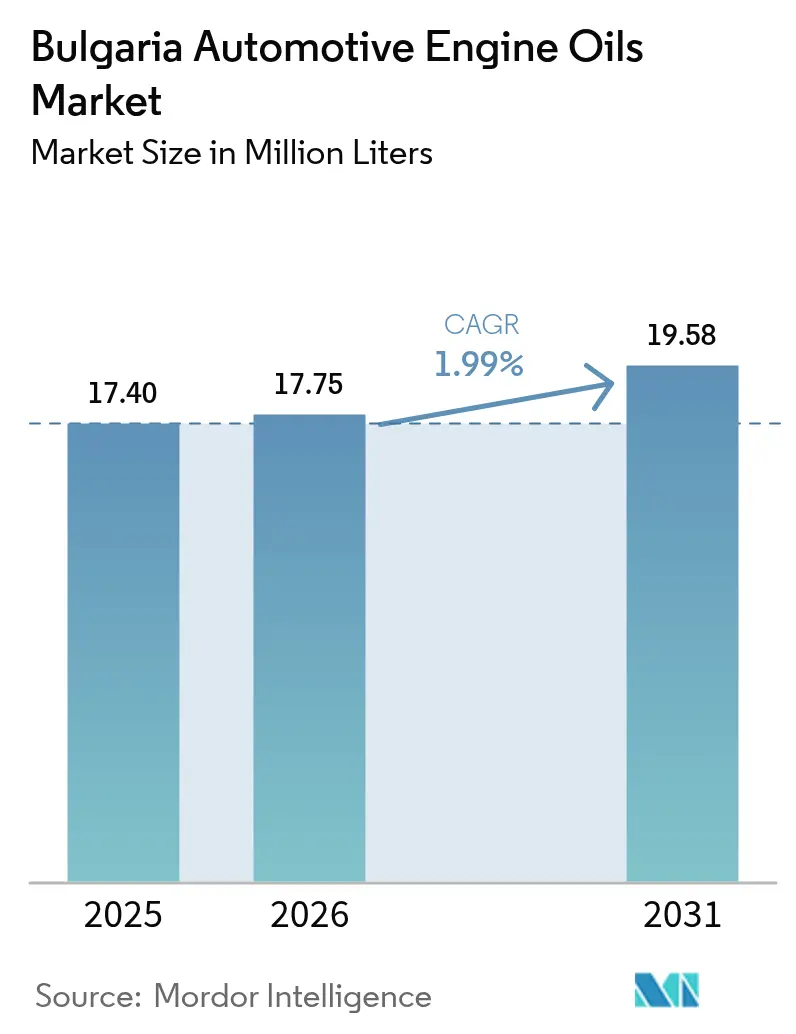

| Base Year Market Size (2025) | 17.40 Million Liters |

| Market Volume (2026) | 17.75 Million Liters |

| Market Volume (2031) | 19.58 Million Liters |

| Growth Rate (2026 - 2031) | 1.99% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bulgaria Automotive Engine Oils Market Analysis by Mordor Intelligence

The Bulgaria Automotive Engine Oils Market size in 2026 is estimated at 17.75 million liters, growing from 2025 value of 17.40 million liters with 2031 projections showing 19.58 million liters, growing at 1.99% CAGR over 2026-2031. An aging national vehicle parc, ongoing adherence to stringent Euro emissions standards, and a gradual consumer pivot toward higher-performance synthetic formulations underpin demand visibility. Steady freight activity along the Orient–East-Med corridor sustains commercial‐vehicle lubricant consumption, while the rebound of tourism and ride-hailing services is lifting two-wheeler and light-duty requirements. Parallel growth in e-commerce is reshaping product availability, empowering do-it-yourself buyers and independent workshops to source a broader range of OEM-approved brands online. At the same time, longer engine oil drain intervals emerging from advanced powertrain designs temper absolute volume potential, placing a premium on value per litre rather than sheer throughput.

Key Report Takeaways

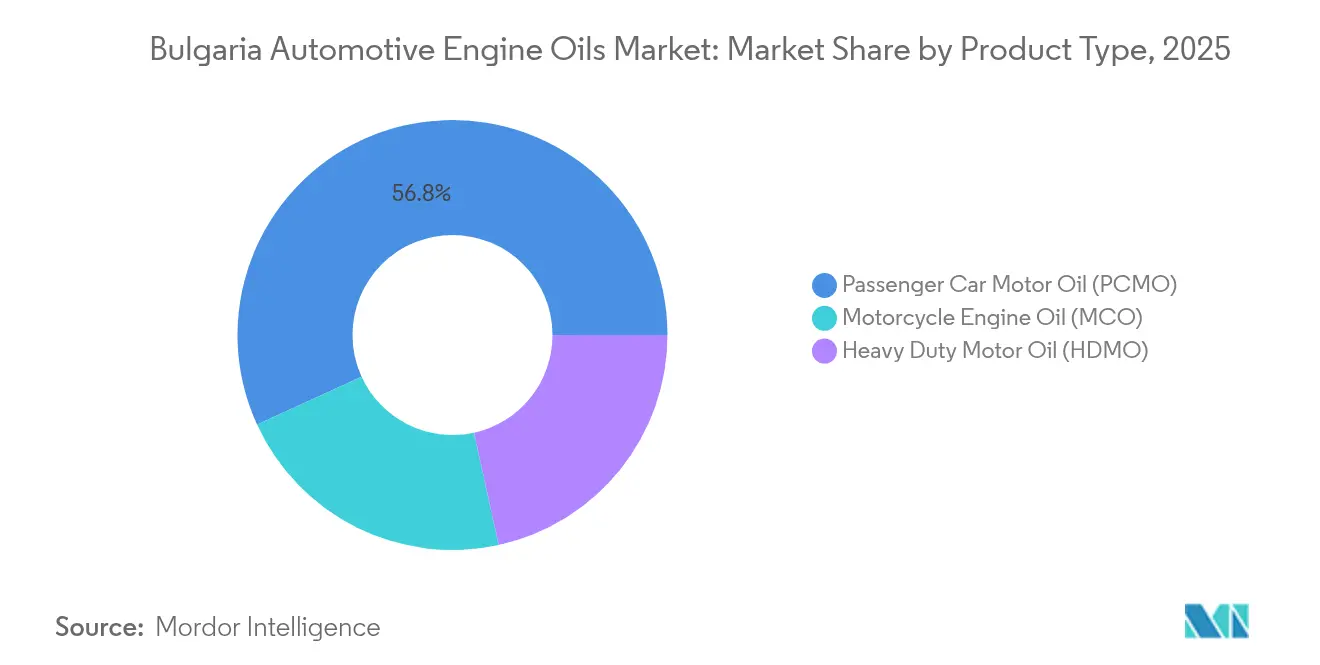

- By product type, Passenger Car Motor Oil held 56.84% share of the Bulgaria automotive engine oils market in 2025, while Motorcycle Engine Oil is forecast to post the fastest 2.17% CAGR through 2031.

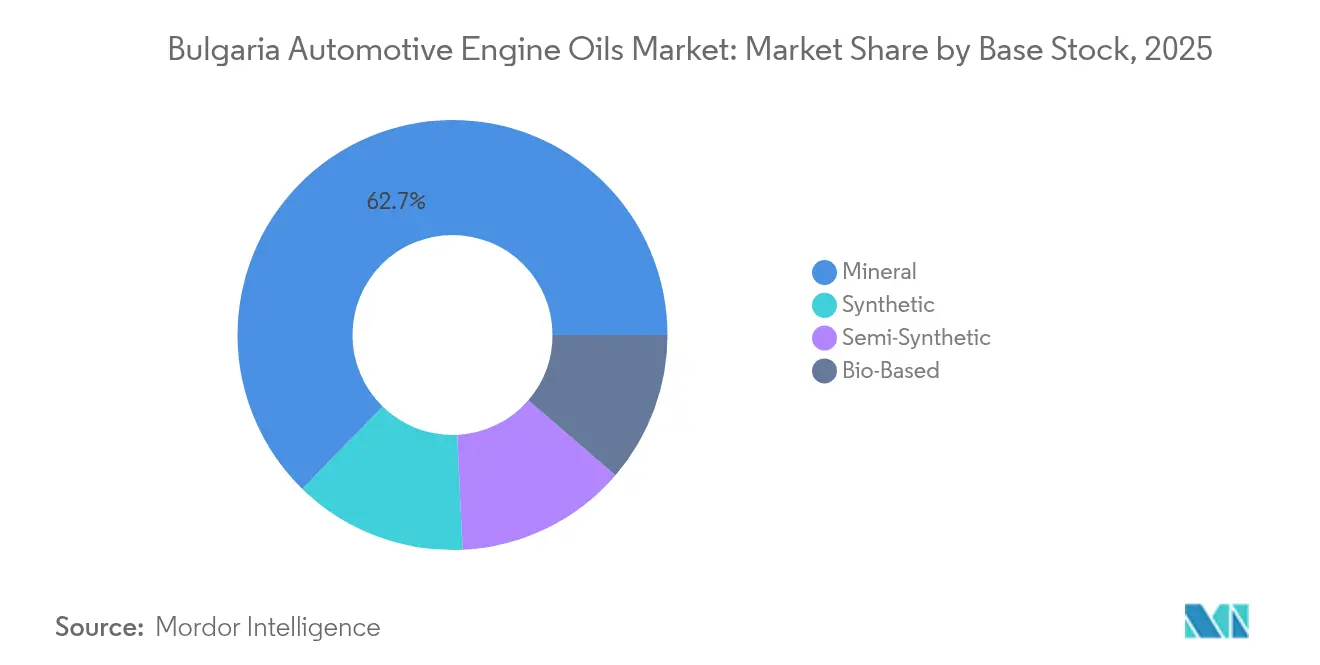

- By base stock, mineral oils accounted for 62.70% of the Bulgaria automotive engine oils market share in 2025, yet synthetic oils are set to grow at a 2.34% CAGR to 2031, signalling an incremental shift toward premium formulations.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bulgaria Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle parc and average fleet age | +0.80% | Sofia, Plovdiv, Varna | Long term (≥ 4 years) |

| Euro 6/VI emissions push toward low-SAPs synthetics | +0.60% | Urban EU-aligned hubs | Medium term (2-4 years) |

| E-commerce boom boosting DIY and after-market sales | +0.50% | National, city-centric | Short term (≤ 2 years) |

| OEM warranty tie-ups with branded oils | +0.40% | Authorized dealer networks | Medium term (2-4 years) |

| Ride-hailing fleet renewal post-tourism rebound | +0.30% | Sofia, Burgas, coastal | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Average Fleet Age

About 70% of Bulgaria’s registered vehicles exceeded 15 years of age in 2024, compared with an EU average of 12.1 years, which drives recurring lubricant demand as mature engines need higher-viscosity or additive-rich oils for wear mitigation[1]European Commission, “Average Age of EU Vehicle Fleet 2024,” europa.eu . Frequent maintenance cycles associated with older cars, vans, and motorcycles anchor a resilient base for the Bulgaria automotive engine oils market. Mineral formulations remain popular among cost-sensitive owners of legacy models, yet premium synthetics are gradually penetrating as motorists seek smoother cold starts and lower fuel consumption. Workshops report consistent turnover in 10W-40 and 5W-30 grades, and rural garages often stock monogrades that align with pre-Euro powertrains. The aging parc also elevates demand for motorcycle lubricants because many older bikes feature air-cooled engines and wet-clutch systems that mandate specialized oils.

Euro 6/VI Emissions Push Toward Low-SAPs Synthetics

Euro 7 rules come into force for new type approvals in November 2026 and tighten limits on particulate mass, ammonia, and crankcase emissions. Bulgarian importers and service centers are therefore expanding stocks of ACEA C1–C3 low-SAP oils designed to protect diesel particulate filters and three-way catalysts. Roughly 25% of the national fleet already complies with Euro 6 standards, bringing a visible uplift in synthetic demand. Brands such as LIQUI MOLY have responded with ultra-low-viscosity 0W-8 formulations that target fuel-economy gains without compromising durability. Truck operators face similar shifts, with Daimler DTFR 15C130 approvals now a prerequisite for warranty claims on latest-generation heavy-duty engines.

E-commerce Boom Boosting DIY/After-Market Sales

Domestic platforms like Vsichki Masla and international marketplaces are accelerating direct-to-consumer lubricant sales, offering transparent pricing and detailed technical sheets that encourage brand comparison. Bulgarian shoppers increasingly research viscosity grades and OEM approvals online, then either perform their own oil changes or schedule services at independent workshops. This omnichannel behavior enlarges the sales footprint for mid-tier and specialty brands that might otherwise lack shelf space at big-box fuel stations. European precedent underscores the opportunity: passenger-car engine oil web sales totaled nearly 30 million litres across leading EU markets in 2021, growing at double-digit rates where digital engagement tools are robust.

OEM Warranty Tie-ups with Branded Oils

Automakers are deepening lubricant alliances to ensure emission system integrity and to mitigate warranty risk. Co-branded bottles, dealership training, and extended-service guarantees help steer motorists toward approved products. Castrol’s warranty‐protection scheme in neighboring Romania illustrates how OEM endorsements translate into aftermarket stickiness[2]Castrol, “Warranty Protection,” castrol.com . Bulgarian dealers replicate the approach, highlighting that failure to use an approved oil may void coverage. The tactic favors global majors whose portfolios already satisfy a wide range of factory specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer oil-drain intervals from engine tech advances | -0.40% | Premium vehicle segments | Long term (≥ 4 years) |

| Stagnant new-vehicle sales amid macro headwinds | -0.30% | National pattern | Medium term (2-4 years) |

| Grey-market bulk imports eroding premium margins | -0.20% | Price-sensitive users | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Longer Oil-Drain Intervals from Engine Tech Advances

Engine downsizing, direct injection, and synthetic base stocks enable intervals of 15,000–30,000 km, far beyond the 10,000 km norm of older models. While per-litre value rises, overall litre consumption per vehicle declines, placing a volume ceiling on the Bulgaria automotive engine oils market. Hybrid powertrains further depress running hours, extending drains even more. Workshops counter by upselling premium blends and ancillary services to offset lower oil turnover, but the restraint remains notable across high-income customer segments that embrace latest technology.

Stagnant New-Vehicle Sales Amid Macro Headwinds

Elevated financing costs and consumer caution curb new-car registrations, limiting factory-fill lubricant demand and dampening early-life service requirements. Many Bulgarians instead import used cars from Western Europe, perpetuating the aging-fleet dynamic. Economic uncertainty ahead of the planned euro changeover in 2026 also postpones large-ticket purchases. The result is subdued uptake of the most advanced low-viscosity oils that new models typically recommend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Car Motor Oil Leads, Motorcycle Oils Rise

Passenger Car Motor Oil contributed 56.84% of the Bulgaria automotive engine oils market in 2025, driven by a 3.1 million-unit passenger-car fleet that skews toward compact B- and C-segment models. Demand centers on 5W-30 and 10W-40 grades because these viscosities meet both Euro 6 after-treatment requirements and older engine tolerances. The Bulgaria automotive engine oils market size for passenger-car oils is projected to expand at a muted pace as longer drain intervals offset parc growth. Nevertheless, the segment remains the anchor for distributor volumes and promotional activity. Traditional fuel‐station forecourts still account for the bulk of quick-top-up sales, while dealership service packages capture higher end of the market through full-synthetic fills.

Motorcycle Engine Oil represents a smaller base yet registers a 2.17% CAGR to 2031, making it the fastest-growing line in the Bulgaria automotive engine oils market. Urban congestion and tourism revival have spurred two-wheeler adoption, especially scooters with displacements under 250 cc. Lubricant requirements include wet-clutch compatibility and heat-resistance additives. LIQUI MOLY’s Motorbike 4T Synth 5W-40 Street Race meets API SP and JASO MA2 and is gaining shelf presence in Sofia and Varna dealerships. Marketing tie-ins such as MotoGP sponsorship reinforce brand recognition and justify premium pricing amid performance-oriented riders.

Heavy-Duty Motor Oil serves roughly 142,000 heavy trucks and buses that move freight between Turkey and Central Europe via the Trakia and Hemus motorways. This application benefits from Euro VI step E engine upgrades that demand low-SAPs 10W-30 synthetics compliant with Daimler DTFR 15C130. While drain intervals reach 80,000 km on modern units, fleet mileages remain high, preserving aggregate volume. Commercial operators favor bulk container deliveries to service hubs in Plovdiv and Ruse, leveraging telematics to schedule oil changes based on real-time soot load measurements.

By Base Stock: Mineral Dominance, Synthetic Momentum

Mineral oils comprised 62.70% of the Bulgaria automotive engine oils market share in 2025 because price awareness remains acute among owners of aging cars and off-warranty imports. Gravity drums and budget 1-litre packs dominate kiosks and rural outlets. However, unit sales of Group III and Group IV synthetics are expanding steadily. The Bulgaria automotive engine oils market size for synthetics reflects a 2.34% CAGR. Performance advantages include lower volatility, superior cold-start lubrication, and compatibility with diesel particulate filters. FUCHS demonstrates these benefits through its XTL Technology, which claims a 30% faster oil flow at engine start and measurable fuel economy gains.

Semi-synthetics bridge the cost–performance gap, targeting taxi fleets and light-duty vans that require higher load capacity than mineral oils can offer. Bio-based formulations remain experimental, accounting for very small share. Yet EU circular-economy financing is expected to accelerate small pilot projects near Burgas refinery complexes, focusing on recycled base stocks blended with renewable esters. Such innovations could create a secondary premium tier aligned with corporate decarbonization goals.

Geography Analysis

Sofia metropolitan area accounts for a significant share of the Bulgaria automotive engine oils market because 1.4 million registered vehicles operate within the capital’s commuting radius. Higher disposable income supports a more rapid shift toward synthetics, and dense dealership networks ensure ready access to OEM-approved brands. Digital platforms offer same-day delivery within the city, making Sofia a bellwether for e-commerce penetration. Plovdiv and Varna follow with clusters of logistics facilities and ports that attract heavy-duty traffic, ensuring consistent throughput of 15W-40 and 10W-30 diesel-engine oils.

The Black Sea coastal corridor experiences distinct seasonality. Summer tourism triggers peaks in motorcycle and rental-car servicing, driving up quarterly lubricant orders as compared with winter months. Service stations along the E87 route stock multi-brand POS displays catering to transient motorists who require top-ups before cross-border trips to Romania or Turkey. Conversely, winter sees elevated consumption of 0W-30 synthetics as temperatures drop and cold-cranking performance becomes critical.

Rural provinces such as Vidin, Montana, and Kardzhali show lower per-vehicle spending. Mineral 20W-50 grades remain popular due to older vehicle demographics and longer oil-change intervals accepted by owners. Distributors deliver via regional wholesalers that maintain buffer inventories to manage occasional road closures in mountainous areas. Notably, cross-border trade with Serbia introduces some grey-market volumes, prompting customs agencies to intensify surveillance at the Kalotina checkpoint. Despite price competition, leading brands maintain visibility through farmer-oriented promotions that bundle engine oil with agricultural lubricant packs, recognizing that many rural households operate both cars and farm machinery.

Competitive Landscape

The Bulgaria automotive engine oils market is consolidated. Shell leverages its Helix Ultra line, formulated with gas-to-liquid base stocks, and offers bundled loyalty rewards at 110 service stations nationwide. BP markets Castrol EDGE for premium cars and Castrol GTX for high-mileage vehicles, capitalizing on co-branding tactics with key automakers.

Specialty suppliers carve out niches. LIQUI MOLY emphasizes German engineering and motorsports partnerships to upsell 0W-8 and motorcycle oils. FUCHS targets fleet managers with TITAN Longlife IV FE 0W-20 that aligns with Volkswagen 508 00/509 00 approvals. Motul appeals to performance enthusiasts through sponsorship of local drift events and a broad racing portfolio. Each challenger banks on technical differentiation to resist price competition.

Distribution innovation is gathering speed. TotalEnergies introduced its Lube Advisor digital platform that matches engine types to correct viscosity grades, improving upsell of Quartz Ineo series in authorized workshops. Meanwhile, local start-ups operate drop-shipping models that connect e-tailers with regional warehouses, reducing inventory risk. Consolidation pressure is evident as smaller importers grapple with Euro 7 conformity certification costs. Analysts expect at least two secondary brands to exit or merge by 2027, tightening supply to mainstream retailers but potentially opening white-label opportunities for supermarket chains.

Bulgaria Automotive Engine Oils Industry Leaders

BP p.l.c.

Exxon Mobil Corporation

Prista Oil

Shell plc

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Esso SAF, the French subsidiary of ExxonMobil, plans to launch a project at its Gravenchon Refinery in northern France to produce re-refined base oils (RRBO) from used oils by the second half of 2025. This development is expected to influence the automotive engine oils market in Bulgaria, as base oils are a key component in engine oil manufacturing.

- March 2024: Alpha Bulgaria, a Bulgarian investment firm, seeks shareholder approval to acquire up to 200,000 shares in Prista Oil Holding by 2025. The investment aims to enhance Alpha Bulgaria's market position while driving Prista Oil's growth, market expansion, and operational upgrades.

Bulgaria Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the current volume size of Bulgaria automotive engine oils?

The Bulgaria automotive engine oils market size reached 17.75 million liters in 2026 and is on track for 19.58 million liters by 2031.

How fast is demand expected to grow?

Volume demand is forecast to rise at a 1.99% CAGR between 2026 and 2031, supported by an aging fleet and regulatory upgrades.

Which product type holds the largest share?

Passenger Car Motor Oil led with 56.84% of the Bulgaria automotive engine oils market share in 2025.

Which segment is expanding the quickest?

Motorcycle Engine Oil shows the fastest growth, projected at a 2.17% CAGR through 2031.

How are synthetics performing versus mineral oils?

Mineral oils still dominate at 62.70% share, yet synthetic oils are growing at 2.34% CAGR as Euro 7 and fuel-economy goals take hold.

What key regulation will shape future demand?

Euro 7 emissions norms, effective for new vehicle types in 2026, will accelerate adoption of low-SAPs synthetic lubricants.

Page last updated on: