Mist Eliminator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

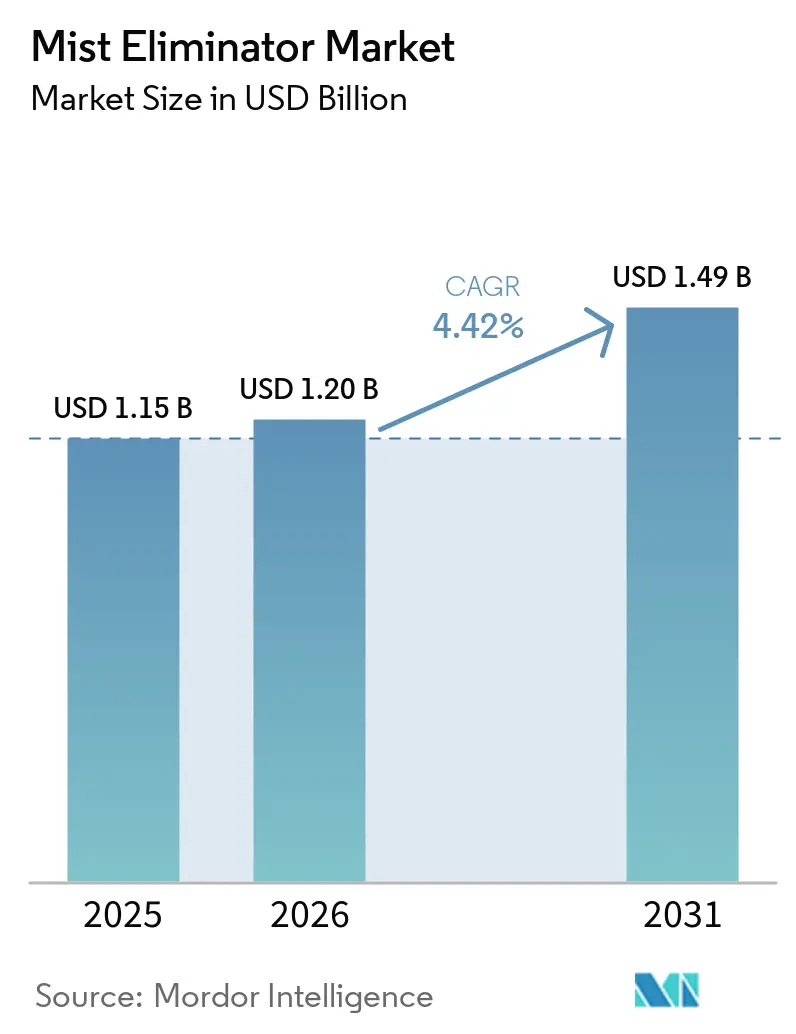

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mist Eliminator Market Analysis by Mordor Intelligence

The Mist Eliminator Market size is projected to be USD 1.15 billion in 2025, USD 1.20 billion in 2026, and reach USD 1.49 billion by 2031, growing at a CAGR of 4.42% from 2026 to 2031. Rising retrofit activity in refinery and gas‐processing columns, the surge of zero-liquid-discharge (ZLD) desalination plants, and the deployment of droplet-management hardware in green-hydrogen electrolyzers are shifting demand from wire-mesh pads to hybrid, fiber-bed, and corrosion-resistant vane designs. Semiconductor fabs require sub-micron acid-mist capture to safeguard expensive ULPA filters, while ZLD projects in the Gulf Cooperation Council (GCC) region handle high-salinity brines and aggressive chemistries, favoring thermoplastic internals. Asia-Pacific, already the largest regional contributor, continues to anchor new capacity with India’s petrochemical developments and China’s integrated refinery expansions. Meanwhile, the Middle-East and Africa are experiencing the fastest regional CAGR, driven by Saudi Arabia’s USD 500 million Ras Mohaisen and USD 272 million Yanbu desalination contracts, along with the nearly completed NEOM green-hydrogen complex. Competitive dynamics remain moderate; however, recent mergers, such as ITT-SPX FLOW and the pending CECO-Thermon tie-up, indicate a shift toward integrated process-equipment platforms that combine mist eliminators with pumps, valves, and aftermarket analytics, raising entry barriers for smaller stand-alone vendors.

Key Report Takeaways

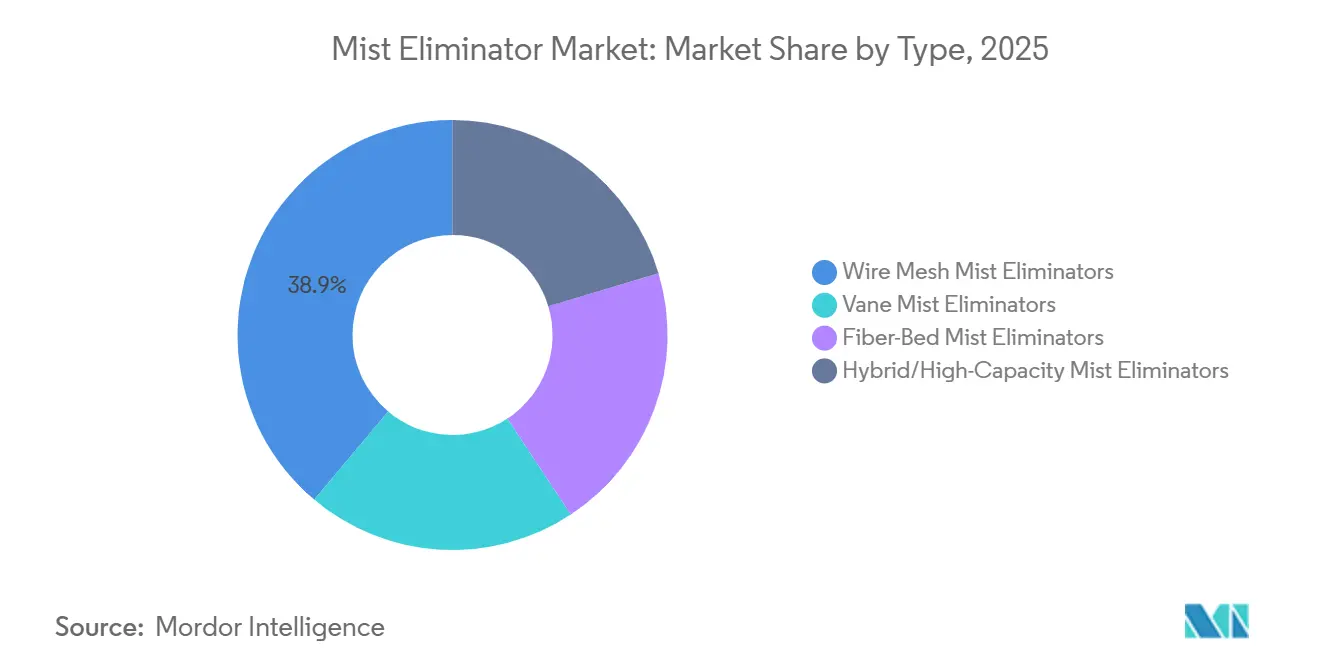

- By type, wire-mesh mist eliminators held 38.88% of the mist eliminator market share in 2025, while hybrid/high-capacity mist eliminators are forecast to grow at a 4.71% CAGR through 2031.

- By material, metal (stainless, duplex, nickel alloys) captured 47.76% of the mist eliminator market share in 2025, yet thermoplastic (PP, PTFE, PVC) is advancing at a 4.59% CAGR through 2031.

- By application, oil and gas production and refining captured 36.22% of the mist eliminator market share in 2025, while desalination and zero-liquid-discharge plants are forecast to grow at a 4.89% CAGR through 2031.

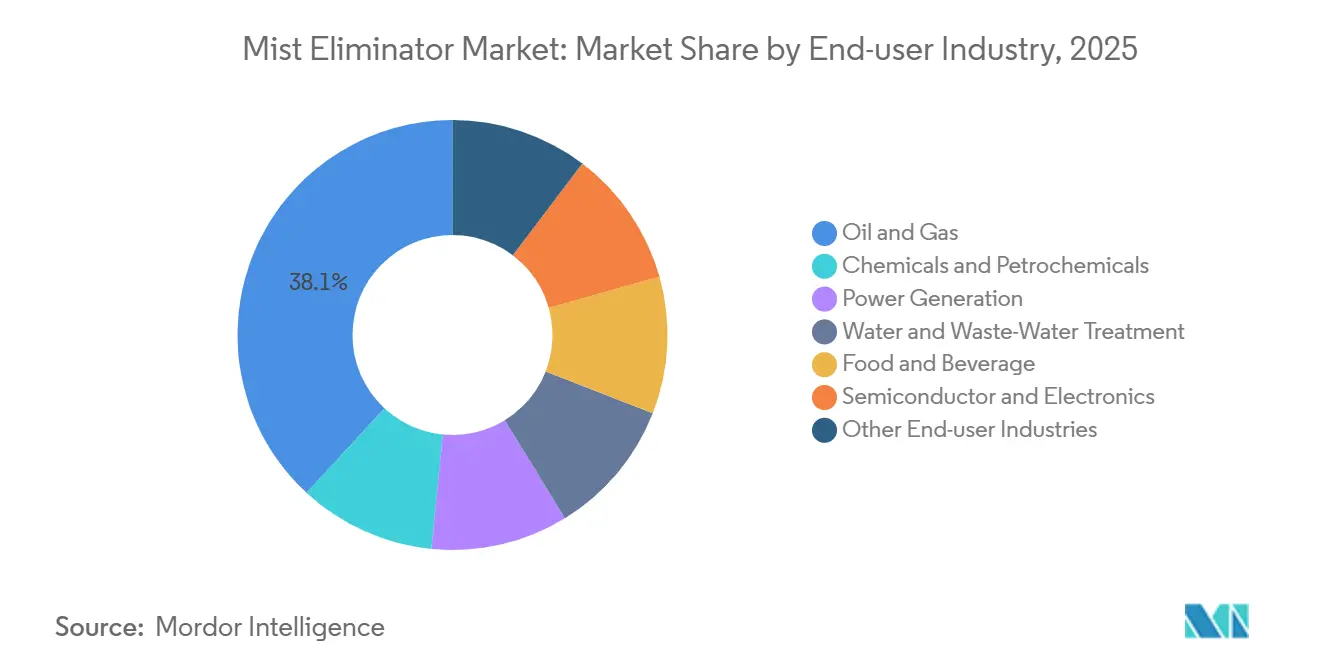

- By end-user industry, oil and gas captured 38.12% of the mist eliminator market share in 2025, while desalination and semiconductor and electronics is forecast to grow at a 4.95% CAGR through 2031.

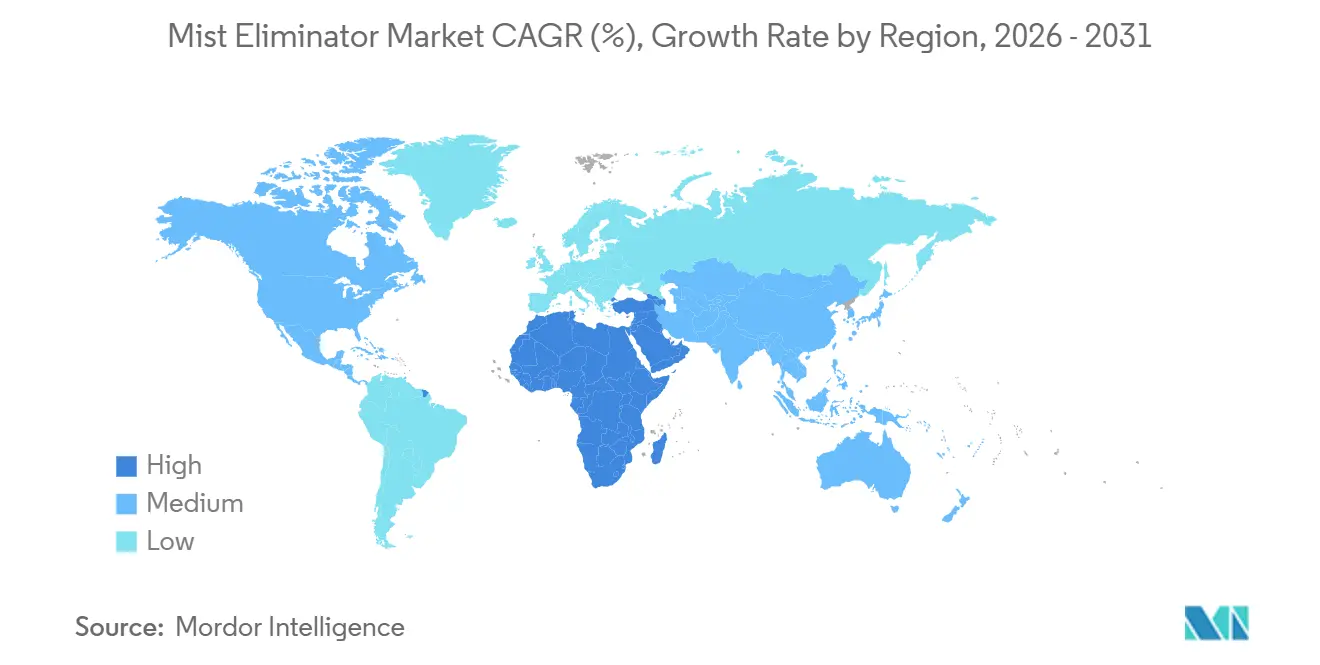

- By geography, Asia-Pacific commanded 38.23% of the mist eliminator market share in 2025, while the Middle-East and Africa is set to record a 5.11% regional CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mist Eliminator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating petrochemical and gas-processing capacity additions in Asia and Middle-East | +1.2% | Asia-Pacific (China, India, ASEAN), Middle-East (Saudi Arabia, UAE) | Medium term (2–4 years) |

| Rapid build-out of zero-liquid-discharge desalination plants in GCC and India | +0.9% | Middle-East and Africa (GCC core), Asia-Pacific (India) | Long term (≥4 years) |

| Rising retrofit demand from IMO-2020 marine scrubber installations | +0.6% | Global, with concentration in Europe and Asia-Pacific shipping hubs | Short term (≤2 years) |

| Sub-micron acid-mist capture for next-gen semiconductor wet-process fabs | +0.7% | Asia-Pacific (Taiwan, South Korea, Japan), North America (United States) | Medium term (2–4 years) |

| Droplet-management in green-hydrogen electrolyzers and e-fuel stack designs | +0.5% | Middle-East (Saudi Arabia, UAE), Europe (Germany, Nordic countries) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Petrochemical and Gas-Processing Capacity Additions in Asia and the Middle-East

India’s USD 45 billion petrochemical pipeline, along with an additional USD 100 billion in proposed projects, is expected to increase annual capacity from 29.62 million tpa to 46 million tpa by 2030, driving demand for distillation, absorption, and scrubbing columns that rely on mist eliminators to reduce solvent loss. China’s Sinopec is upgrading the Tahe complex by adding a new ethylene cracker and increasing crude throughput to 8.5 million tpa, which intensifies the need for compact, high-capacity hybrid internals in congested coastal sites. Regulatory mandates in both countries are leading to the closure of high-emission legacy plants, accelerating replacement cycles. As a result, procurement specifications now frequently require 0.45 m/s gas-load factors and two-stage separation efficiencies above 99%, which hybrid vane-mesh or cyclone-mesh combinations achieve more effectively than legacy pads.

Rapid Build-Out of ZLD Desalination Plants in the GCC and India

Saudi Arabia’s Ras Mohaisen project will produce 300,000 m³/day of potable water, incorporating energy-recovery devices and a 30 MW solar plant, which necessitates low-pressure drops through mist eliminators. Va Tech Wabag’s Yanbu contract adds another 300 million L/day, while Qatar’s Pearl gas-to-liquids complex operates a 45,000 m³/day ZLD loop that relies on vane separators to capture entrained brine aerosols. These large-scale projects treat aggressive, high-TDS streams that corrode stainless steel, increasing demand for polypropylene, PTFE, and PFA-coated meshes. VSEP’s shear-enhanced reverse-osmosis modules reduce evaporator duty by 70%, requiring upstream mist control to prevent carry-over into crystallizers.

Rising Retrofit Demand from IMO-2020 Marine Scrubber Installations

Scrubber penetration in container shipping is projected to reach 42% of the fleet, or 1,543 vessels, by January 2026. Although fuel-price spreads have narrowed, aftermarket pad replacements remain essential to ensure emission compliance and reduce wash-water volumes. Damen Shipyards’ compact damper-scrubber retrofits integrate mist elimination within the housing, reducing the deck footprint and setting a design trend likely to be adopted across other vessel classes.

Sub-Micron Acid-Mist Capture for Next-Generation Semiconductor Fabs

ISO Class 1–5 cleanrooms require upstream separators before ULPA filters to prevent droplet coalescence. A DRAM fab in Hsinchu demonstrated 95% mixed-acid removal with less than 80 Pa pressure drop over 3.5 years, validating the use of honeycomb wet-scrubber modules paired with fine-fiber pads. Europe’s upcoming PFAS restrictions are increasing scrutiny on scrubber blow-down, accelerating the adoption of thermoplastic meshes that emit minimal fluorinated by-products and integrate effectively with VSEP concentration skids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of qualified fabricators for exotic-alloy mesh pads | -0.4% | Global, with acute constraints in North America and Europe | Short term (≤2 years) |

| Competitive threat from low-cost electrostatic alternatives in light-duty VOC control | -0.3% | Asia-Pacific (China, India), emerging markets | Medium term (2–4 years) |

| Integration challenges with AI-enabled "smart" towers in legacy plants | -0.2% | North America, Europe (mature industrial bases with aging infrastructure) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Qualified Fabricators for Exotic-Alloy Mesh Pads

Mesh pads made from Alloy 625 or C-276 require specialized vacuum annealing and welding processes, which are available at only a few vendors. Lead times often exceed 20 weeks, forcing operators to maintain costly spare inventories or opt for lower-quality stainless alternatives that double replacement frequency[1]Sulzer Process Technologies, “KnitMesh XCOAT Datasheet,” sulzer.com. Consolidation within the industry, such as ITT-SPX FLOW and Thermo Fisher’s filtration acquisition, further concentrates supply and may lead to price increases.

Competitive Threat from Low-Cost Electrostatic Alternatives in VOC Control

Wet electrostatic precipitators achieve particulate emissions below 1 mg/Nm³ with minimal pressure loss, making them attractive for paint booths and light chemical VOC streams. A novel dual-plane ionization electrode has achieved over 98.6% capture at only 15.1 kV, offering cost advantages over fiber-bed pads in terms of capital expenditure and consumables. However, ozone generation and poor performance with sticky aerosols limit their applicability in heavy-duty petrochemical operations, where mesh separators remain the preferred choice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hybrid Designs Gain Traction in Offshore Debottlenecking

Wire mesh mist eliminators accounted for 38.88% of 2025 revenue. However, hybrid/high-capacity mist eliminators are expected to grow at the fastest CAGR of 4.71% through 2031, as offshore platforms aim to achieve 25%–40% reductions in vessel diameter and over 300% increases in throughput during revamps. Two-stage systems like DEMISTER-PLUS or VORSOMAX cyclone-mesh combinations maintain 99% efficiency at gas loads of ≥0.45 m/s, aligning with process intensification objectives. The mist eliminator market benefits from Munters’ UltraFlow, which reduces column height by 20% and pump energy consumption by 30%, resulting in savings of approximately USD 150,000 for a 50-MW coal scrubber retrofit.

Hybrid adoption is also driven by stricter space constraints in semiconductor and battery-recycling plants near urban centers. Fabricators now pre-assemble vane decks and fiber pads into cassette frames for quick installation through a single manway, reducing outage windows by 40% and lowering scaffolding costs.

By Material: Thermoplastics Advance in Corrosive Service

Metal materials retained 47.76% of 2025 revenue, but thermoplastics (PP, PTFE, PVC) are projected to grow at the fastest CAGR of 4.59% through 2031. This growth is driven by applications in ZLD desalination, semiconductor processes, and PFAS-laden acid-scrubber streams, where corrosion resistance is prioritized over temperature tolerance. Sulzer’s KnitMesh XCOAT, featuring wire coated with pure PFA, extends service life threefold compared to bare stainless steel in sulfuric-acid dryers. Initial capital expenditure for thermoplastic pads is 30%–50% lower than equivalent stainless steel options, and end-of-life disposal avoids hazardous-waste surcharges associated with alloy metals. Lifecycle analyses indicate a 15-year net present value cost advantage of USD 1.8 million for a 300 m³/h hydrochloric-acid scrubber retrofitted with PTFE mesh.

Heightened focus on PFAS emissions further accelerates the shift to thermoplastics. These materials exhibit minimal fluorine breakdown, reducing downstream adsorbent loading and facilitating compliance with Europe’s upcoming PFAS ban.

By Application: Desalination and Zero-Liquid-Discharge Plants Deliver the Highest Growth Runway

Oil and gas production and refining accounted for 36.22% of 2025 revenue. However, desalination and zero-liquid-discharge (ZLD) plants are projected to grow at a CAGR of 4.89% through 2031. Multi-stage brine concentrators utilize vane sections to remove droplets before evaporators, reducing thermal duty by 70%. A typical 300,000 m³/day desalination plant installs 800–1,000 m² of vane area, representing USD 3 million in hardware.

Semiconductor fabs contribute incremental but high-margin demand. A single 100,000-wafer-per-month foundry requires up to 250 wet-process tools, each needing localized mist capture. Planned giga-scale fabs in the U.S. and Japan are expected to increase semiconductor-related demand.

By End-user Industry: Electronics Surge on Cleanroom Mandates

Oil and gas accounted for 38.12% of end-user industry revenue in 2025, but the semiconductor and electronics segment is projected to grow at a CAGR of 4.95% through 2031. Mist eliminators are increasingly used in CMP rinse, sulfuric-peroxide mix, and HF etch stations, where sub-0.12 µm droplets can impact yield. ACM Research’s Ultra C Tahoe system reports 75% sulfuric-acid savings, reducing scrubber liquid load and downstream pad size by 20%. While power, metals, fertilizer, and pulp industries maintain steady replacement demand, stricter VOC regulations in battery recycling and EV cathode production create niche growth opportunities.

Geography Analysis

Asia-Pacific posted 38.23% of 2025 revenue. India’s petrochemical CAPEX wave and China’s Tahe revamp ensure a robust replacement market for mesh pads. Taiwan and South Korea are driving semiconductor-related demand with ULPA-grade requirements. ASEAN countries, including Vietnam and Thailand, are attracting foreign direct investment in downstream chemicals, though project scales remain modest. North America sees LNG export terminals and data-center cooling towers adopting vane-mesh hybrids, with CECO’s record USD 135 million gas-fired project confirming domestic momentum. Europe focuses on decarbonization, with wet electrostatic retrofits in wood-panel and mineral-wool factories.

The Middle-East and Africa will record the fastest 5.11% CAGR through 2031. Saudi megaprojects alone are projected to require over 3,000 m² of new vane area per desalination site. NEOM’s electrolyzer stacks are incorporating AI-enabled mist-management modules, setting a precedent for future hydrogen clusters in the UAE and Oman. Nigeria’s petrochemical developments and South Africa’s mining-water ZLD trials add incremental demand, though a lack of qualified fabricators limits immediate adoption.

South America offers steady demand for pulp, sugar-ethanol, and mining retrofits. Political risks and currency volatility constrain large greenfield investments, but multinational EPCs like Veolia are piloting closed-loop systems in drought-affected Brazilian states.

Competitive Landscape

The mist eliminator market hosts a mix of specialist and diversified suppliers. Koch-Glitsch leverages a 70-year DEMISTER installed base and emergency-delivery services to defend its share. Sulzer differentiates with PFA-coated KnitMesh XCOAT targeted at sulfuric acid and purified terephthalic acid duties. Munters’ UltraFlow vane series emphasizes 20% height cuts and 30% pump-energy savings for coal scrubbers.

Consolidation is reshaping the field. ITT closed a USD 4.775 billion SPX FLOW buyout, integrating separation tech into a new Flow Technologies division. Thermo Fisher paid USD 4.0 billion for Solventum’s filtration business to push into ultra-pure water and bioprocessing. CECO’s planned merger with Thermon marries emissions control with process heating, creating cross-sell avenues into power, battery recycling, and LNG[2]CECO Environmental Form 10-K 2025, cecoenvironmental.com. These deals elevate cross-portfolio bundling, mist eliminators shipped with valves, pumps, and digital monitoring contracts, which could squeeze smaller fabricators lacking breadth.

Technology trends center on computational fluid dynamics, AI-linked pressure sensors, and modular skid designs shipped fully populated with pads and drainage baffles. Vendors quote 15% faster installation times and 10% longer mean-time-between-cleanings for smart towers calibrated via real-time analytics.

Mist Eliminator Industry Leaders

Koch Engineered Solutions

Sulzer Ltd

Munters Group AB

CECO ENVIRONMENTAL

Elessent Clean Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mass-Vac, Inc. introduced a range of MV Oil Mist Eliminators designed to prevent oil mist, smoke, and residue from vacuum pump exhaust from entering the workplace environment. These eliminators were equipped with microfiber-glass coalescing elements, achieving filtration down to 0.1 microns with an efficiency of 99.9999% for pumps with capacities ranging from 5 to 300 CFM.

- December 2025: Filtermist Limited launched the AW Series, a range of compact, machine-mounted oil mist eliminators designed specifically for high-pressure neat oil machining applications, including Swiss-type sliding head lathes. The AW Series included models tailored to varying pollution levels, based on three primary airflow capacities: 250 m³/hr, 500 m³/hr, and 800 m³/hr.

Global Mist Eliminator Market Report Scope

A mist eliminator is a specialized industrial device designed to remove liquid droplets and mist from gas streams. Its primary purposes are to prevent corrosion, ensure environmental compliance, and protect downstream equipment. Mist eliminators are commonly used in wet scrubbers, cooling towers, and chemical processes. They typically employ wire mesh pads, chevron baffles, or fiber beds to coalesce mist into larger droplets, which then drain by gravity.

The Mist Eliminator Market is segmented into type, material, application, end-user industry, and geography. By type, the market is segmented into wire mesh mist eliminators, vane mist eliminators, fiber-bed mist eliminators, and hybrid/high-capacity mist eliminators. By material, the market is segmented into metal (stainless, duplex, nickel alloys), thermoplastic (PP, PTFE, PVC), fiber glass, and other materials (FRP, exotic alloys). By application, the market is segmented into oil and gas production and refining, gas processing and compression, desalination and zero-liquid-discharge plants, chemical and fertilizer manufacturing, thermal and geo power plants, pharmaceutical, food and beverage, and other applications. By end-user industry, the market is segmented into oil and gas, chemicals and petrochemicals, power generation, water and waste-water treatment, food and beverage, semiconductor and electronics, and other end-user industries. The report also covers the market size and forecasts for mist eliminator in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Wire Mesh Mist Eliminators |

| Vane Mist Eliminators |

| Fiber-Bed Mist Eliminators |

| Hybrid/High-Capacity Mist Eliminators |

| Metal (Stainless, Duplex, Nickel Alloys) |

| Thermoplastic (PP, PTFE, PVC) |

| Fiber Glass |

| Other Materials (FRP, Exotic Alloys) |

| Oil and Gas Production and Refining |

| Gas Processing and Compression |

| Desalination and Zero-Liquid-Discharge Plants |

| Chemical and Fertilizer Manufacturing |

| Thermal and Geo Power Plants |

| Pharmaceutical, Food and Beverage |

| Other Applications |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Power Generation |

| Water and Waste-Water Treatment |

| Food and Beverage |

| Semiconductor and Electronics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Wire Mesh Mist Eliminators | |

| Vane Mist Eliminators | ||

| Fiber-Bed Mist Eliminators | ||

| Hybrid/High-Capacity Mist Eliminators | ||

| By Material | Metal (Stainless, Duplex, Nickel Alloys) | |

| Thermoplastic (PP, PTFE, PVC) | ||

| Fiber Glass | ||

| Other Materials (FRP, Exotic Alloys) | ||

| By Application | Oil and Gas Production and Refining | |

| Gas Processing and Compression | ||

| Desalination and Zero-Liquid-Discharge Plants | ||

| Chemical and Fertilizer Manufacturing | ||

| Thermal and Geo Power Plants | ||

| Pharmaceutical, Food and Beverage | ||

| Other Applications | ||

| By End-user Industry | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Power Generation | ||

| Water and Waste-Water Treatment | ||

| Food and Beverage | ||

| Semiconductor and Electronics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the mist eliminator market?

The mist eliminator market stands at USD 1.20 billion in 2026 and is projected to reach USD 1.49 billion by 2031.

Which regional shows the fastest growth potential through 2031?

The Middle-East and Africa are set to post a 5.11% CAGR through 2031, led by Saudi desalination and hydrogen projects.

Which type is expanding the quickest through 2031?

Hybrid and high-capacity mist eliminators are growing at a 4.71% CAGR through 2031 as offshore and retrofit users seek compact, high-throughput solutions.

Why are thermoplastic meshes gaining popularity?

Polypropylene, PTFE, and PVDF meshes resist corrosion in acidic ZLD and semiconductor streams, cost up to 50% less than stainless, and ease PFAS compliance.

Page last updated on: