Data Discovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.82 Billion |

| Market Size (2031) | USD 41.07 Billion |

| Growth Rate (2026 - 2031) | 16.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

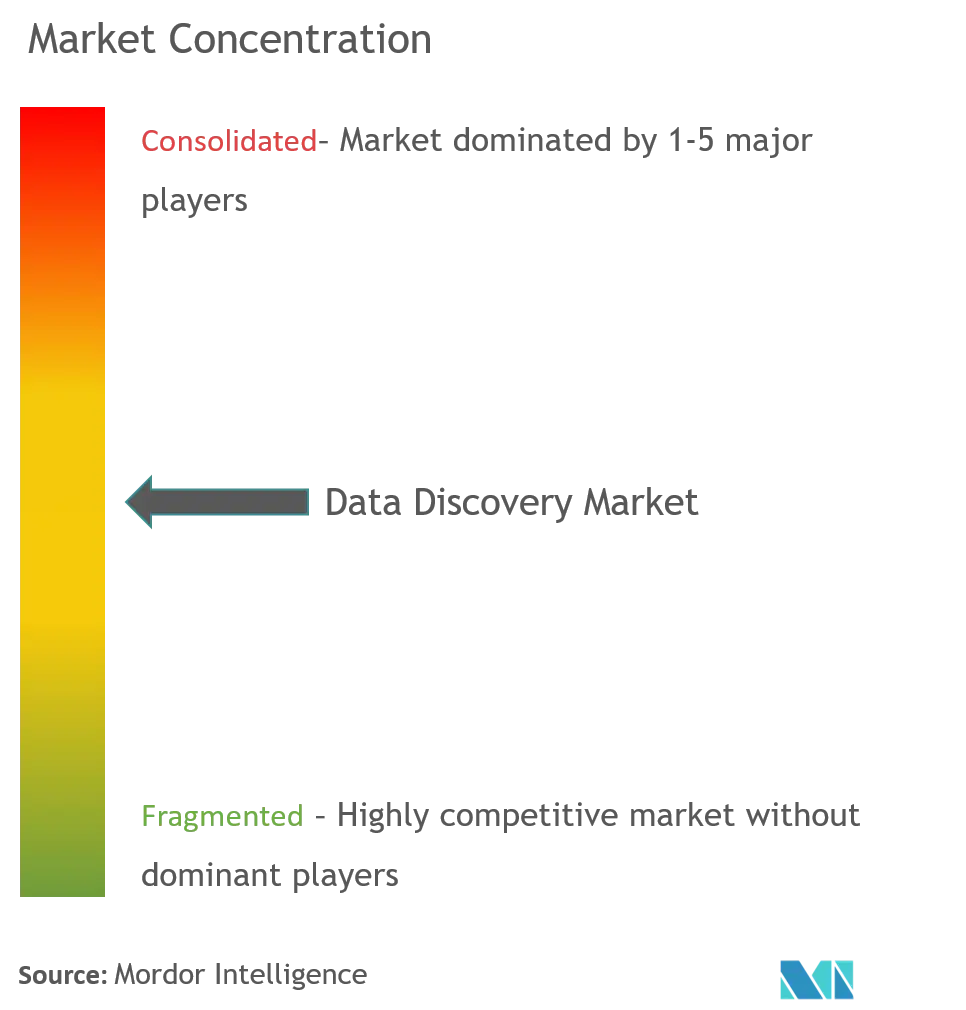

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Discovery Market Analysis by Mordor Intelligence

The data discovery market size is expected to grow from USD 16.1 billion in 2025 to USD 18.82 billion in 2026 and is forecast to reach USD 41.07 billion by 2031 at 16.92% CAGR over 2026-2031. This growth cements the data discovery market as one of the fastest-rising segments of enterprise analytics, fueled by mounting requirements to turn multi-structured data into timely business decisions. Heightened cloud adoption, rapid advances in generative AI, and widening executive mandates for data-driven cultures are accelerating platform demand. At the same time, customers are pivoting from traditional business-intelligence stacks toward intuitive self-service tools that democratize insight generation across departments, boosting platform stickiness and recurring revenue streams. Competitive strategies are increasingly shaped by region-specific regulations—especially sovereign-cloud mandates in APAC and data-governance rules in Europe—that determine deployment choices and vendor partnerships.

Key Report Takeaways

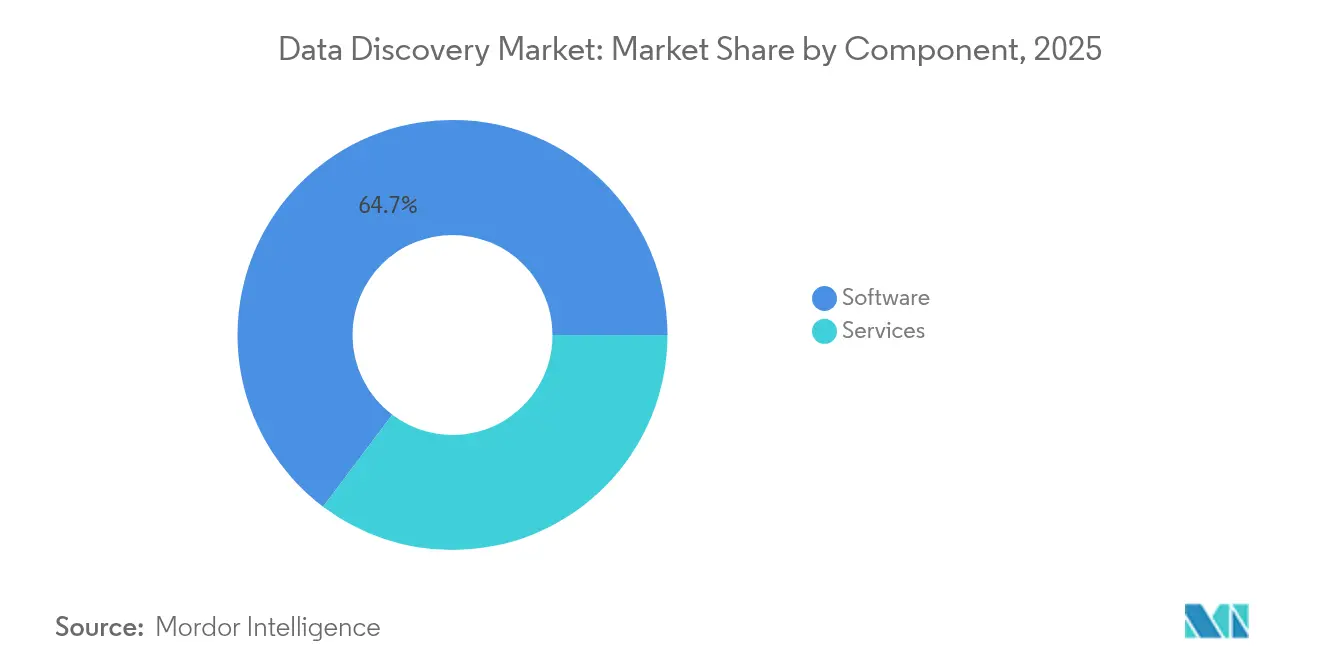

- By component, software solutions retained 64.72% of data discovery market share in 2025, while services are expanding at a 23.12% CAGR through 2031.

- By deployment model, on-premise installations held 54.30% of the data discovery market size in 2025; cloud deployments are set to post a 24.62% CAGR to 2031.

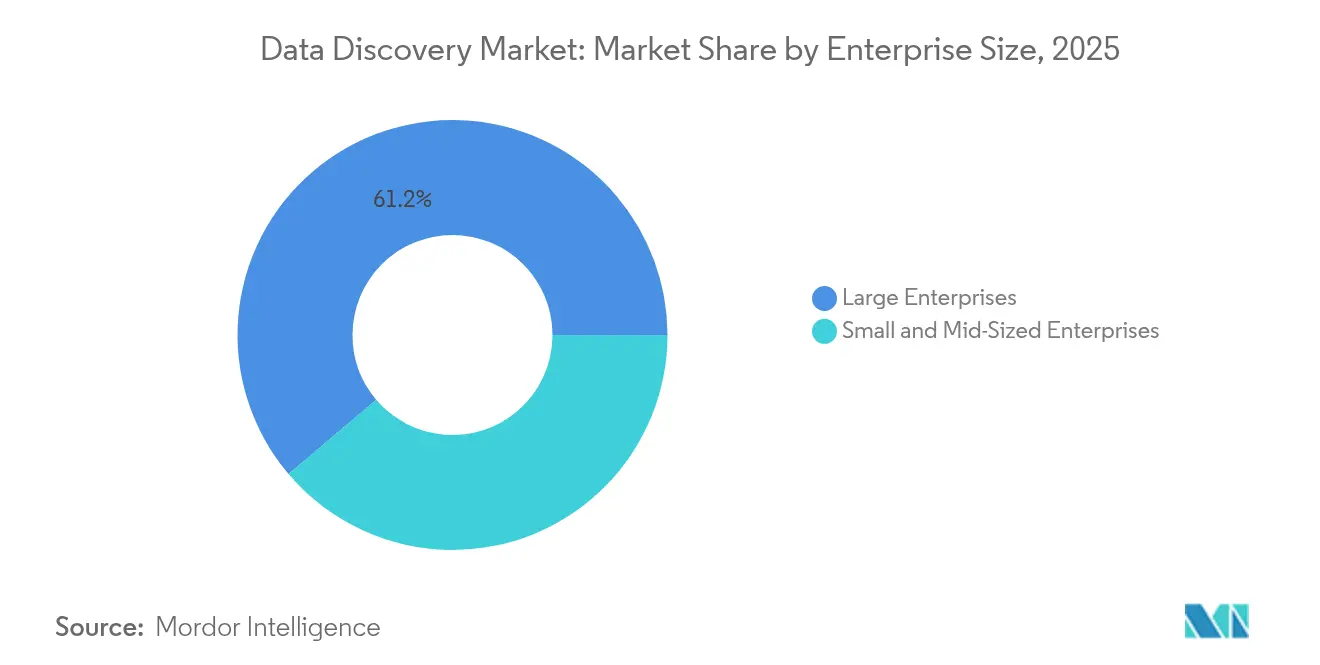

- By enterprise size, large enterprises captured 61.20% of the data discovery market size in 2025; small and mid-sized enterprises will rise at a 24.14% CAGR.

- By vertical, BFSI led with 23.78% of data discovery market share in 2025, whereas healthcare and life sciences is forecast to grow at a 18.92% CAGR.

- By application, risk and compliance management accounted for 27.95% of the data discovery market size in 2025, while customer-experience and personalization applications are projected to advance at a 20.12% CAGR.

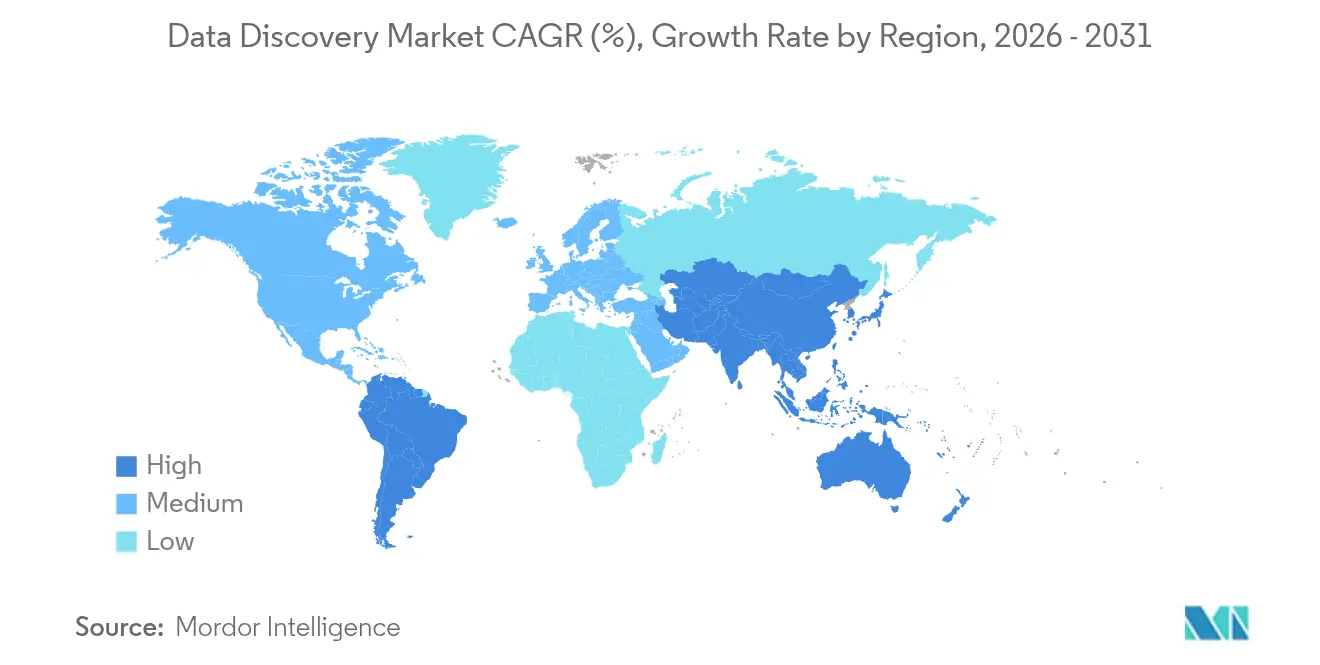

- By geography, North America commanded 39.60% of the data discovery market in 2025; APAC is poised for the fastest expansion at an 18.27% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Data Discovery Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of multi-structured data | +4.2% | Global | Medium term (2-4 years) |

| Push for data-driven decision-making | +3.8% | North America, EU core, APAC expansion | Short term (≤2 years) |

| Rapid uptake of self-service analytics | +3.5% | Global, SME concentration | Medium term (2-4 years) |

| Governance and compliance mandates | +2.9% | EU, North America, emerging APAC | Long term (≥4 years) |

| Generative-AI copilots in workflows | +2.7% | North America, EU, developed APAC | Short term (≤2 years) |

| Falling columnar cloud-warehouse costs | +1.9% | Global cloud-first markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Multi-Structured Data Sources

Enterprises now ingest streams from IoT sensors, social feeds, documents, and edge devices, forcing platforms to unify diverse formats without preprocessing. Vendors embed natural-language processing to auto-catalog assets, reducing the time analysts spend curating data.[1]Io-Tahoe, “Io-Tahoe Files Patent Applications for Its Data Discovery Platforms,” iotahoe.com Edge rollouts amplify this need, and shortages in semiconductors have made cloud elasticity more attractive for scaling discovery workloads. Organizations are concluding that legacy warehouses alone cannot accommodate today’s data velocity, thereby accelerating migrations to cloud-native discovery solutions.

Enterprise Push for Data-Driven Decision-Making

Executive mandates have reframed discovery platforms as strategic assets. HP’s rollout of a conversational BI layer on Databricks enables supply-chain teams to surface anomalies through simple queries instead of heavy engineering efforts.[2]Databricks, “Simplifying Access to Insights with Natural Language,” databricks.com Transparent lineage functions also satisfy auditors, especially in financial services, and successful deployments pair technology rollouts with cultural shifts that place data insights at the heart of day-to-day decisions.

Rapid Uptake of Self-Service Analytics Platforms

Organizations with mature self-service programs report 42% efficiency gains and a 64% rise in data accessibilitys.[3]Rajeev Reddy Chevuri, “The Future of Self-Service Data Science Platforms,” World Journal of Advanced Engineering Technology and Sciences, journalwjaets.com Microsoft’s managed self-service architecture shows how shared semantic models preserve governance while empowering business users. SMEs, previously constrained by IT budgets, now embrace cloud-native delivery that supports unpredictable usage bursts without upfront infrastructure.

Governance and Compliance Mandates

Europe’s Data Act obliges firms to catalog and share data assets on demand, making integrated governance a procurement prerequisite.[4]European Commission, “Data Act—Shaping Europe’s Digital Future,” digital-strategy.ec.europa.eu The European Central Bank’s focus on risk-data aggregation likewise pushes banks toward platforms with robust audit trails. In the United States, the OCC’s 2025 plan reinforces data-classification requirements across third-party ecosystems, while several APAC governments require sovereign storage that further localises deployments.

Restraints Impact Analysis of Data Discovery Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data security and privacy risks | –2.8% | Global, with stronger pressure in EU and highly regulated sectors | Long term (≥4 years) |

| Limited availability of data-engineering and stewardship talent | –2.1% | North America, EU, developed APAC | Medium term (2-4 years) |

| Complex integration with legacy systems | –1.7% | Global, most acute among large enterprises | Medium term (2-4 years) |

| Strict sovereign-cloud data-localization mandates | –1.4% | APAC core, expanding into EU and other emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns

Nearly half of global cyberattacks in 2024 involved data or credential theft, with APAC bearing one-third of incidents. Manufacturers are prime ransomware targets, and broader data access raises regulator scrutiny. Privacy-enhancing technologies exist, yet adoption is hampered by performance trade-offs and cost. Enterprises now demand granular access controls and immutable audit logs that lengthen implementation cycles and inflate budgets.

Shortage of Data-Engineering and Stewardship Talent

Global demand for data specialists eclipses supply, prolonging deployment timelines and elevating service-partner costs. Firms juggling tariff-driven supply-chain disruption alongside platform modernisation cite talent scarcity as a top hurdle. Competition for skilled personnel inflates salaries, pushing some enterprises toward managed-services models to bridge capability gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Data Discovery Market Segment Analysis

By Component:

Services Drive Implementation SuccessSoftware still dominated the data discovery market size with a 64.72% revenue share in 2025. However, services are growing fastest at a 23.12% CAGR as businesses realise successful rollouts require integration, governance, and change-management expertise. Consulting engagements tackle architecture modernisation, while managed services appeal to SMEs lacking internal resources. Over the forecast horizon, services are expected to capture a larger slice of incremental spending as platform complexity rises and talent bottlenecks persist. The shift underscores the transition from tool-centric purchases to outcome-oriented contracts that bundle software with measurable business impact.

Software vendors continue to refine subscription models and embed low-code configuration to curb heavy customisation. Yet enterprise clients frequently augment licences with specialised partners for data onboarding, taxonomy design, and lineage validation. This hybrid buying behaviour aligns with broader market maturation trends in which value is measured by decision-speed improvements rather than feature lists.

By Deployment Mode:

Cloud Economics Override Security ConcernsOn-premise installations retained 54.30% of the data discovery market share in 2025, owing chiefly to banking and public-sector data-localisation mandates. Cloud deployments, however, are projected to climb at a 24.62% CAGR as cost-optimised warehouses and sovereign-cloud frameworks alleviate risk perceptions. Firms now mix local storage for sensitive records with cloud compute for analytical bursts, creating demand for unified control planes that mask underlying complexity.

Fujitsu’s sovereign-cloud launch powered by Oracle Alloy typifies regional responses to localisation rules while still delivering elastic cloud scale. As more regulators publish cloud-security benchmarks, cross-industry confidence grows, and enterprises shift capex toward opex-based consumption models that reduce upgrade cycles.

By Enterprise Size:

SME Democratization Accelerates Market ExpansionLarge enterprises commanded 61.20% of 2025 revenue, but SME adoption is surging at 24.14% CAGR thanks to pay-as-you-go models and intuitive self-service interfaces. Smaller firms, once excluded by infrastructure costs, now consume curated data products through browser-based portals, shrinking time-to-insight. Vendor roadmaps increasingly feature out-of-the-box connectors and auto-governance templates to quick-start SME deployments.

Meanwhile, large organisations remain critical to vendor roadmaps because their complex multi-cloud footprints showcase advanced lineage and security features. Yet even these buyers expect consumer-grade experiences for business users, reinforcing a universal usability bar across customer tiers.

By Industry Vertical:

Healthcare Innovation Outpaces Financial MaturityBFSI led 2025 spending with 23.78% data discovery market share, driven by stringent reporting and audit obligations. Healthcare and life sciences, however, is forecast for the fastest 18.92% CAGR through 2031 as precision-medicine research, clinical-trial analytics, and real-world evidence programs multiply data volume and complexity. Telecommunications, retail, and manufacturing maintain steady investment to optimise customer engagement and shop-floor efficiency, while utilities report expanding interest in predictive maintenance amid decarbonisation drives.

Vertical solutions that pre-package domain ontologies and compliance artefacts are gaining traction, shortening deployment cycles and differentiating vendors in crowded bidding contests.

By Application:

Customer-Experience Transformation Drives GrowthRisk and compliance management held the largest 27.95% slice of 2025 revenues within the data discovery market size, reflecting a regulatory baseline every institution must meet. Looking ahead, customer-experience and personalisation workloads are set for a 20.12% CAGR as firms seek granular insight into omni-channel behaviour. Unifying marketing, support, and product telemetry enables micro-segmentation and real-time offers that lift lifetime value.

Sales and marketing optimisation likewise benefits from consolidated profiles, while operations and supply-chain analytics help organisations mitigate disruptions and improve resilience. Asset-performance management is seeing early adoption in energy and industrial domains where uptime is mission-critical.

Geography Analysis

North America Data Discovery Market

North America retained 39.60% of 2025 revenue, supported by mature governance frameworks, deep cloud penetration, and robust partner ecosystems. Financial-services regulations continue to drive discovery platform renewals, and the U.S. intelligence community’s 2023-2025 data strategy underlines federal commitment to interoperable architectures. Technology-sector RandD labs further expand platform footprints to power AI product development.

APAC Data Discovery Market

APAC is forecast to be the fastest-growing region with an 18.27% CAGR. National digital-government programs and sovereign-AI roadmaps accelerate demand for localised yet scalable discovery environments. Japan exemplifies this trajectory through public-sector shifts to Oracle Cloud Infrastructure, while rising data-centre capacity investments across Southeast Asia lay physical foundations for broader adoption.

EMEA and South America Data Discovery Market

Europe posts steady gains, underpinned by GDPR and the Data Act’s stringent data-sharing and lineage obligations. Banks must align with the European Central Bank’s risk-data guidance, stimulating fresh platform upgrades. Elsewhere, South America and the Middle East and Africa are moving from pilot phases toward enterprise-wide deployments, though infrastructure gaps and talent shortages temper near-term expansion.

Competitive Landscape

The data discovery market is moderately fragmented. Global cloud providers leverage existing IaaS footprints to upsell discovery modules, while best-of-breed vendors differentiate in cataloguing, lineage, or vertical compliance depth. Strategic alliances—such as recent joint database services between leading hyperscalers and database specialists—showcase demand for cross-cloud interoperability maintained under single-pane governance.

Patent trends highlight intensified RandD around natural-language interfaces and automated metadata generation, signalling a race to lower the skill barrier for complex exploration tasks. Vendors bundling advisory services alongside software are gaining traction, particularly where customers grapple with privacy, sovereignty, and talent constraints. Niche players able to certify workloads against regional sovereignty codes are carving defensible beachheads in government and regulated verticals.

Pricing innovation is evident as subscription tiers blend storage, compute, and governance meters to align expenditure with realised business benefits. Overall, competitive intensity remains high, but no single provider dominates mindshare across all regions and verticals.

Data Discovery Industry Leaders

Tableau Software, LLC

Datameer, Inc.

SAP SE.

Tibco Software Inc.

Cloudera, Inc.

- *Disclaimer: Major Players sorted in no particular order

Data Discovery Market Companies Covered in this Report

- Microsoft Corp.

- Tableau Software LLC (Salesforce)

- SAP SE

- QlikTech International AB

- IBM Corp.

- Oracle Corp.

- Amazon Web Services Inc.

- Google LLC (Looker)

- Altair Engineering Inc.

- SAS Institute Inc.

- MicroStrategy Inc.

- Alteryx Inc.

- Datameer Inc.

- Cloudera Inc.

- Talend SA

- Informatica Inc.

- Collibra NV

- Alation Inc.

- Snowflake Inc.

- Tibco Software Inc.

Recent Industry Developments in Data Discovery Market

- June 2025: IBM released its X-Force Threat Intelligence Index 2025, showing data and credential theft comprised nearly 50% of global cyber incidents, underscoring the need for integrated discovery and security functions.

- May 2025: Snowflake reported Q1 2025 revenue of USD 1.04 billion, up 26% year-over-year, and highlighted 451 new customers adopting its cloud data-platform capabilities.

- April 2025: Fujitsu launched a sovereign-cloud service powered by Oracle Alloy, offering 106 locally managed functions to meet Japanese data-sovereignty rules.

- April 2025: The U.S. Patent and Trademark Office issued guidance on AI-assisted patent drafting, encouraging technical safeguards and human oversight to mitigate associated risks.

Data Discovery Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the data discovery market as the total annual revenue from software platforms and related services that let business users explore, profile, visualize, and catalog structured or unstructured data across on-premise, cloud, and hybrid environments.

Scope exclusion: pure-play ETL tools, data warehousing hardware, and standalone visualization packages are not counted.

Segments Covered in This Report

- By Component

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud

- Hybrid

- By Enterprise Size

- Small and Mid-Sized Enterprises

- Large Enterprises

- By Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Telecommunications and IT

- Retail and E-Commerce

- Manufacturing

- Energy and Utilities

- Healthcare and Life Sciences

- Government and Public Sector

- Other Verticals

- By Application

- Risk and Compliance Management

- Sales and Marketing Optimization

- Customer Experience and Personalization

- Operations and Supply-Chain Analytics

- Asset and Performance Management

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with software vendors, system integrators, CIOs, and data-governance leads across North America, Europe, and Asia Pacific. Interviews tested adoption thresholds, price dispersion, and the share of self-service deployments, while short surveys among mid-sized enterprises helped us validate penetration assumptions and upcoming budget intent.

Desk Research

We began with open datasets that gauge enterprise digitization, such as Eurostat's Digital Economy scores, U.S. Census ICT spending tables, and OECD cloud-adoption surveys, which anchor user counts and spending baselines. Company 10-Ks, SEC filings, and investor decks revealed average deal sizes and renewal cycles. Standards bodies and regulators (GDPR texts, NIST privacy framework, ISO 27001 adoption lists) clarified compliance-driven demand pivots. Patent analytics from Questel and news flows on Dow Jones Factiva tracked innovation velocity and product launches. This list is illustrative; many other sources supported data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with global enterprise software spend, filtered by analytics share and then by the specific data-discovery penetration rates we derived from primary calls. Select bottom-up checks, supplier revenue roll-ups and sampled ASP × license counts, stress-test totals. Key variables inside the model include cloud workload mix, average seat price erosion, regulated-industry share, regional data-privacy intensity, and workforce analytics literacy. Multivariate regression links these drivers to historical growth before five-year forecasts are produced. Scenario analysis adjusts for macro shifts like AI-assisted query adoption. Where vendor roll-ups are thin, gaps are bridged with deployment mix proxies confirmed during interviews.

Data Validation and Update Cycle

Outputs pass three layers of analyst review, anomaly flags trigger re-checks with respondents, and variance versus public earnings is logged. Mordor Intelligence refreshes every twelve months and issues interim updates when material events, major regulations, M&A, or pricing resets, occur.

How Mordor Intelligence's Data Discovery Market Size Compares to Other Published Estimates

Published figures often diverge because firms apply different component scopes, base years, and currency conversions. We anchor scope to revenue actually linked to self-service discovery workflows, and we refresh the base year annually, thereby limiting legacy drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.10 Bn (2025) | Mordor Intelligence | - |

| USD 15.35 Bn (2025) | Regional Consultancy A | Narrow component mix; limited SME coverage |

| USD 14.51 Bn (2025) | Trade Journal B | Excludes hybrid deployments; partial regional cut |

| USD 11.67 Bn (2023) | Global Consultancy A | Older base year and linear growth assumption |

These comparisons show that when scope, time frame, and driver selection shift, market value moves materially. By centering on verifiable variables and a clear refresh cadence, Mordor Intelligence delivers a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the data discovery market and how fast is it growing?

The data discovery market is valued at USD 18.82 billion in 2026 and is forecast to reach USD 41.07 billion by 2031, reflecting a 16.92% CAGR.

Which region leads the market today, and which region is expanding the fastest?

North America holds the largest 39.60% revenue share in 2025, while APAC is projected to post the quickest 18.27% CAGR through 2031.

Which industry verticals are the biggest contributors and the fastest risers?

Banking, financial services, and insurance represent the largest 23.78% share, whereas healthcare and life sciences are growing at a 18.92% CAGR.

What deployment model is gaining traction against on-premise systems?

Cloud deployments are set to expand at a 24.62% CAGR, outpacing on-premise installations that still account for 54.30% of 2025 revenue.

What are the top restraints that could slow market growth?

The most significant barriers include data-security and privacy risks (–2.8% impact on CAGR), talent shortages in data stewardship (–2.1%), legacy-system integration complexity (–1.7%), and strict sovereign-cloud data-localization mandates (–1.4%).

Page last updated on: