Food Intolerance Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

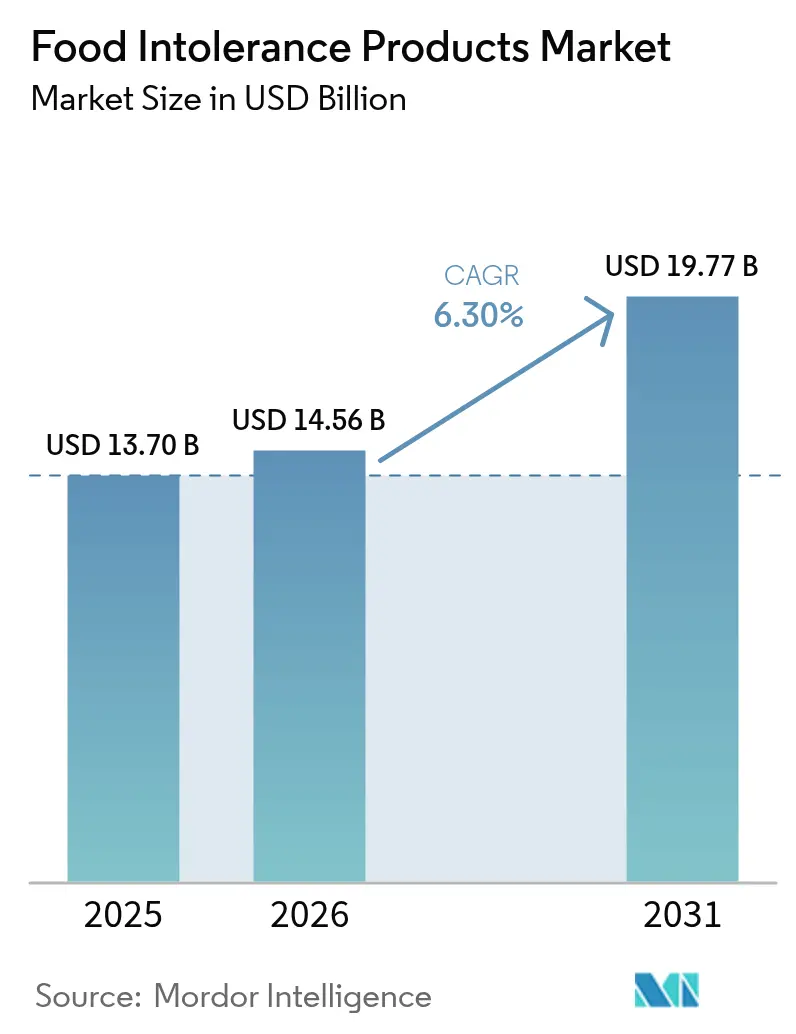

| Market Size (2026) | USD 14.56 Billion |

| Market Size (2031) | USD 19.77 Billion |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Intolerance Products Market Analysis by Mordor Intelligence

The food intolerance products market size in 2026 is estimated at USD 14.56 billion, growing from 2025 value of USD 13.7 billion with 2031 projections showing USD 19.77 billion, growing at 6.30% CAGR over 2026-2031. The growth trajectory is driven by stringent food-safety regulations, increased consumer awareness of diet-related health concerns, and a steady rise in medically diagnosed allergies. The 2024 update to the U.S. gluten-free rule for fermented and hydrolyzed foods has reduced compliance uncertainties, facilitating new product launches and building trust among sensitive consumers. While North America maintains its leadership due to early regulatory clarity and high label literacy, urban households in the Asia-Pacific region are driving the fastest volume growth, supported by rising incomes and expanding e-commerce. Manufacturers are prioritizing investments in cost-efficient plant-based ingredients and precision fermentation technologies to enhance taste parity with conventional foods, a critical factor for ensuring repeat purchases. Retailers are optimizing shelf space by allocating premium end-caps and algorithm-driven search placements to brands that meet clean-label, allergen-free, and organic standards. These strategic adjustments are expected to support long-term volume growth in the free-from foods market.

Key Report Takeaways

- By product type, dairy and dairy alternatives captured 30.10% of the free-from foods market share in 2025, while confectionery products are projected to expand at a 7.68% CAGR through 2031.

- By labeling type, gluten-free dominated with a 57.00% share of the free-from foods market size in 2025; lactose-free foods are advancing at an 8.02% CAGR between 2026-2031.

- By category, conventional lines accounted for 78.10% of the market in 2025, and organic lines are growing the fastest at 8.84% CAGR to 2031, markedly outpacing conventional products.

- By distribution channel, supermarkets and hypermarkets held 62.95% of the free-from foods market share in 2025, while online retail is growing the fastest at 8.98% CAGR.

- By geography, North America led with 35.40% revenue share in 2025; Asia-Pacific is forecast to deliver the highest regional CAGR at 8.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Intolerance Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Premiumization of gluten-free bakery products | +1.2% | North America and Europe; spreading to Asia-Pacific cities | Medium term (2-4 years) |

| Rising prevalence of food intolerances and allergies | +1.8% | Global; highest in developed markets | Long term (≥ 4 years) |

| Increased consumer awareness and demand for label transparency | +0.9% | Global; led by North America and Western Europe | Short term (≤ 2 years) |

| Growth in plant-based and dairy-free diets | +1.4% | Global; early adoption in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expansion of online and specialty retail channels | +0.7% | Global; accelerated in urban markets | Short term (≤ 2 years) |

| Demand for convenient and ready-to-eat products | +0.6% | Global; strongest in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization of gluten-free bakery products

The gluten-free bakery market is transitioning from basic dietary compliance to delivering enhanced sensory experiences and improved nutritional value. For instance, in 2024, General Mills introduced Annie's Super! Mac, featuring 15 grams of protein and 6 grams of fiber per serving through yellow pea integration. This highlights how manufacturers are advancing gluten-free offerings beyond traditional wheat substitutes. Premium positioning enables manufacturers to offset higher production costs while meeting consumer demand for products that match the quality of conventional options. This approach is particularly effective in developed markets, where consumers are willing to pay a premium for perceived health benefits and superior taste. Market analysis indicates that this premiumization strategy is expanding into confectionery and snack segments, unlocking new revenue opportunities for established food manufacturers. However, the sustainability of this trend relies on continuous advancements in ingredient technology and processing methods to deliver conventional-like experiences without compromising 'free-from' attributes.

Rising prevalence of food intolerances and allergies

The market for food allergies and intolerances is experiencing notable growth, driven by evolving consumer lifestyles and health awareness. Factors such as dietary changes, hygiene practices, environmental exposures, and shifts in gut microbiomes are being actively studied as contributors to this trend. In 2024, the Food Standards Agency reported that 12% of consumers in the United Kingdom (excluding Scotland) were affected by food intolerances[1]Source: Food Standards Agency, "Food and You 2: Wave 8', www.food.gov.uk, highlighting the scale of the issue. In response to this growing concern, the FDA implemented updated 2024 regulations for gluten-free labeling of fermented and hydrolyzed foods. These updates aim to address previous regulatory gaps that inadvertently exposed celiac disease patients to gluten, thereby enhancing consumer safety and trust. The prevalence of food intolerances among younger demographics and urban populations underscores a stable and growing demand base, which is expected to evolve into increased purchasing power over time. Furthermore, the healthcare sector's recognition of food allergies as a significant public health challenge is driving regulatory advancements, particularly in the area of transparent labeling standards. This evolving regulatory environment is creating substantial growth opportunities for manufacturers in the 'free-from' food segment, enabling them to cater to the rising demand for allergen-free and intolerance-friendly products.

Increased consumer awareness and demand for label transparency

Driven by high-profile food safety incidents and growing health awareness, consumer demand for label transparency has surged. This shift has prompted regulatory measures, including the FDA's proposed front-of-package nutrition labeling rule announced in January 2025. The regulation focuses on interpretive labeling to enable consumers to quickly assess levels of saturated fat, sodium, and added sugars. This development presents a strategic opportunity for "free-from" products to emphasize the absence of these ingredients. In 2023, the WHO's expert consultation on food allergen risk assessment highlighted the need for more robust precautionary allergen labeling systems, citing inconsistencies and a lack of risk-based approaches that contribute to consumer confusion. Singapore's revised food labeling regulations, effective in 2025, incorporate specific guidelines for gluten-free claims and prohibit misleading statements, reflecting a global shift toward standardized transparency requirements. The alignment of consumer expectations with regulatory frameworks creates a competitive advantage for manufacturers adopting transparent labeling practices. This trend is particularly advantageous for smaller "free-from" food companies, enabling them to differentiate through clear and credible communication about their product attributes and manufacturing processes.

Growth in plant-based and dairy-free diets

Plant-based diets have transitioned from niche health trends to a significant driver of mainstream consumer behavior, supported by institutional endorsements and innovative product developments. In February 2024, Beyond Meat introduced its fourth-generation Beyond IV platform, which reduces saturated fat by 60% through the incorporation of avocado oil and has received certifications from the American Heart Association and American Diabetes Association. This initiative highlights how plant-based manufacturers are addressing longstanding concerns regarding nutritional adequacy. The movement is further validated by advancements in precision fermentation technologies, which produce animal-identical dairy proteins to overcome taste and functionality limitations in traditional plant-based alternatives. Investments in advertising for dairy alternatives are increasing, with the Food Foundation Organization reporting that in the UK, 27% of advertising expenditure was allocated to dairy alternatives, compared to 73% for conventional dairy products[2]Source: Food Foundation Organization, "The Broken Plate 2025", www.foodfoundation.org.uk. Nestlé's investment in precision fermentation for its Cowabunga range exemplifies how multinational food corporations are strategically preparing for potential disruptions in the dairy market. The trend's growth is further supported by heightened environmental awareness among younger demographics and corporate sustainability initiatives that prioritize plant-based ingredients. Additionally, the movement is expanding geographically, particularly in the Asia-Pacific region, where traditional plant-based diets are being adapted into Western-style convenience formats to meet evolving consumer preferences.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Higher manufacturing and certification costs limits the growth | -1.1% | Global; most severe in emerging markets | Medium term (2-4 years) |

| Challenges in achieving taste and texture parity with conventional foods | -0.8% | Global; varies by category | Long term (≥ 4 years) |

| Limited availability in emerging markets | -0.6% | Africa | Medium term (2-4 years) |

| Consumer skepticism and confusion over labeling | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher manufacturing and certification costs limits the growth

Free-from food manufacturers face ongoing cost challenges. Achieving gluten-free certification involves extensive documentation, facility upgrades, and continuous compliance management. According to the FDA's regulatory impact analysis, the annual compliance cost for gluten-free labeling is approximately USD 8.8 million[3]Source: Food and Drug Administration, "Food Labeling", www.fda.gov. These costs disproportionately impact smaller manufacturers that lack economies of scale. The need for specialized ingredient sourcing, dedicated production lines, and stringent testing protocols creates structural cost disadvantages, hindering market entry in price-sensitive segments. This issue is particularly significant in emerging markets, where consumers have limited tolerance for premium pricing and regulatory frameworks for free-from foods are still evolving. However, advancements in manufacturing technologies and ingredient alternatives are gradually narrowing these cost disparities. Innovations such as precision fermentation and alternative protein technologies present opportunities to achieve cost parity.

Challenges in achieving taste and texture parity with conventional foods

Despite notable advancements in ingredient science and processing technologies, sensory experience gaps between free-from and conventional foods continue to limit broader market penetration. Consumer preference studies consistently emphasize taste and texture as critical drivers of purchase decisions, yet many free-from products fail to meet the sensory expectations set by conventional alternatives. This issue is particularly significant in the bakery segment, where replicating gluten's structural functionality with alternative binding agents and proteins remains challenging. Innovations in enzyme technology, fermentation techniques, and protein modification are progressively addressing these gaps. However, achieving full sensory equivalence across all product categories remains a long-term objective, requiring sustained investment in research and development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Alternatives Drive Innovation

Dairy and dairy alternatives command 30.10% market share in 2025, reflecting the segment's maturity and broad consumer acceptance across multiple dietary restriction categories. This segment's success is attributed to its ability to simultaneously address the needs of lactose-intolerant consumers, individuals with dairy allergies, and those following plant-based diets, thereby capturing a broader market compared to single-restriction categories. Confectionery products represent the fastest-growing segment, achieving a 7.68% CAGR through 2031, driven by premiumization trends and innovative product development beyond traditional sugar-free offerings. Meanwhile, the bakery segment demonstrates consistent growth, supported by advancements in gluten-free products. Similarly, the meat and seafood categories benefit from innovations in plant-based proteins and alternative protein technologies.

Rising awareness of lactose intolerance symptoms and diagnoses has significantly increased the demand for lactose-free products across multiple food categories. In response, manufacturers are expanding their product portfolios to include lactose-free options in key categories such as milk, yogurt, cheese, and ice cream. For instance, in January 2023, Califia Farms introduced organic almond milk and oat milk products made with simple ingredients like purified water, sea salt, and almonds, excluding added oils or gums, to cater to lactose-intolerant consumers seeking clean-label alternatives. Additionally, sauces, condiments, and dressings present a growing opportunity as manufacturers develop 'free-from' versions of traditionally challenging categories. Furthermore, specialty products targeting niche dietary requirements contribute to the overall diversification of the market.

By Labeling Type: Lactose-Free Gains Momentum

Gluten-free foods maintain market leadership with a 57.00% share in 2025, supported by established consumer awareness and regulatory standardization. However, lactose-free products are experiencing faster growth, with an 8.02% CAGR forecasted through 2031, reflecting a shift in consumer preferences beyond celiac disease management. The lactose-free segment capitalizes on its broader demographic reach, as lactose intolerance impacts a larger global population compared to gluten sensitivity, presenting a significant market opportunity. The FDA's updated gluten-free labeling requirements for fermented and hydrolyzed foods in 2024 provide manufacturers with clearer compliance pathways, potentially stabilizing growth in the gluten-free segment while reducing regulatory uncertainties.

Labeling categories are expanding to include emerging free-from claims such as sugar-free, preservative-free, and allergen-specific designations, addressing increasingly sophisticated consumer dietary demands. The integration of multiple free-from claims on a single product offers premium market positioning opportunities but also introduces greater manufacturing complexities and higher certification costs. Singapore's 2025 food labeling regulations highlight this regulatory evolution by establishing clear standards for gluten-free claims and prohibiting misleading statements, thereby supporting market standardization and enhancing consumer confidence.

By Category: Organic Segment Accelerates

In 2025, conventional free-from foods continue to dominate the market, holding a significant 78.10% share. This dominance highlights their affordability and widespread availability, making them a preferred choice for a broad consumer base. These products cater to cost-conscious consumers while maintaining a strong presence across various distribution channels. In contrast, organic free-from products are experiencing remarkable growth, with a projected CAGR of 8.84% through 2031. This growth reflects the increasing expansion of the premium market segment, driven by evolving consumer preferences for products that offer dual benefits, such as health and environmental sustainability. The rapid growth of the organic segment aligns with broader trends in the organic market, presenting manufacturers with opportunities to carve out a unique position in an increasingly competitive landscape.

Health-conscious consumers are particularly inclined toward the organic-free-from combination, as they perceive these attributes as complementary and reinforcing each other. This trend is fueled by growing awareness of health and wellness, as well as a shift toward sustainable consumption patterns. However, manufacturers face significant operational challenges in meeting the stringent requirements for both organic certification and free-from compliance. These dual standards demand robust processes and resources, creating high entry barriers for new players. Established companies with advanced supply chain management capabilities are better positioned to navigate these complexities and capitalize on the growing demand. As free-from foods continue to gain mainstream acceptance, the importance of dual certification is expected to rise significantly, becoming a key differentiator for premium positioning in the market.

By Distribution Channel: Digital Commerce Transforms Access

In 2025, supermarkets and hypermarkets maintain their dominance with a substantial 62.95% market share, effectively leveraging their extensive shelf space and aligning with established consumer shopping patterns. These retail formats capitalize on their ability to offer a wide variety of free-from products, ensuring convenience and accessibility for a broad customer base. Simultaneously, online retail channels are witnessing significant momentum, with a robust CAGR of 8.98% projected through 2031. This growth is fundamentally altering how consumers discover and purchase free-from products. The integration of digital technologies has facilitated the fulfillment of specialized dietary requirements across diverse geographic regions, addressing the long-standing challenge of limited local availability for niche free-from items. Health-food stores continue to play a critical role in the market by not only providing products but also offering educational resources and personalized consultations. These stores are particularly indispensable for consumers managing complex dietary restrictions, as they deliver expert guidance and tailored product recommendations to meet specific health needs.

Convenience and grocery stores act as accessible distribution points for mainstream free-from products, catering to consumers seeking quick and easy purchasing options. Additionally, other distribution channels, such as specialty retailers, foodservice providers, and direct-to-consumer models, are strategically positioned to serve distinct market segments. For manufacturers of free-from foods, adopting a comprehensive multi-channel strategy is imperative to maximize market penetration and address the diverse shopping preferences and accessibility requirements of consumers. Online platforms, in particular, provide a competitive advantage by offering detailed product descriptions, ingredient transparency, and customer reviews. These features empower consumers to make informed purchasing decisions while ensuring compliance with their dietary restrictions, thereby enhancing trust and loyalty in the brand.

Geography Analysis

In 2025, North America secured the largest regional revenue share at 35.40%, driven by stringent allergen-label regulations, a high prevalence of medically diagnosed intolerances, and a well-established chilled-chain logistics network. Collaborative efforts between research institutions and ingredient suppliers in the region are advancing texture-enhancing hydrocolloids and enzyme systems, which are rapidly entering commercial markets. The growing emphasis on ESG reporting has elevated the shelf presence of 'free-from' products with organic or sustainably sourced certifications, further strengthening North America's market leadership.

Asia-Pacific is the fastest-growing region, with an anticipated CAGR of 8.33% through 2031. Urban Millennials in key markets such as China, India, and Thailand are increasingly replacing dairy milk with plant-based alternatives, a trend fueled by social media influencer marketing. Singapore's planned alignment of gluten-free standards with Codex by 2025 is expected to streamline cross-border e-commerce for brands exporting from Australia and the United States. Despite disparities in purchasing power across sub-regions, the adoption of mobile payments and the rise of micro-fulfillment centers are enabling 'free-from' brands to overcome traditional distribution challenges, driving the region's significant growth in the free-from foods market.

Europe combines established organic consumption patterns with certain distribution inefficiencies that limit full product availability. Countries like Germany and Sweden benefit from strong health-food store networks. The EU's stringent allergen-label regulations, among the most rigorous globally, provide consumers with high confidence in both domestic and imported 'free-from' products. In contrast, Latin America and the Middle East and Africa are in the early stages of market adoption. However, the expanding middle class and increasing exposure to Western dietary trends in these regions indicate growth potential, particularly as regulatory frameworks advance and cold-chain infrastructure improves.

Competitive Landscape

The food intolerance products market is fragmented, with consolidation gaining momentum as established conglomerates increasingly acquire innovation rather than developing it internally. The market dynamics are driven by a combination of scale efficiencies and advanced research and development capabilities. Companies secure a competitive edge by focusing on three critical factors: achieving sensory equivalence, ensuring transparent sourcing, and building a robust omnichannel presence. The major players operating in the market include General Mills Inc., Danone S.A., Abbott Laboratories, Nestlé S.A., and Arla Foods amba, among others.

Small to mid-sized disruptors sustain their relevance by targeting specific dietary niches, such as keto-friendly, nut-free baking mixes, or by operating certified allergen-free facilities, which larger competitors find challenging to replicate without significant retrofitting investments. The steady increase in patent filings at the USPTO for plant-based emulsions, extrusion technologies, and allergen-detection assays underscores the industry's ongoing efforts to address taste and cost challenges through technical advancements.

Competitive dynamics favor companies that can manage certification costs, operate or lease dedicated production lines, and leverage direct data feedback from e-commerce channels. Strategic collaborations between ingredient specialists and contract manufacturers are accelerating time-to-market for start-ups, driving high category turnover, and ensuring a continuous pipeline of innovation in the free-from foods market.

Food Intolerance Products Industry Leaders

-

General Mills Inc.

-

Danone S.A.

-

Abbott Laboratories

-

Nestlé S.A.

-

Arla Foods amba

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Doughlicious has introduced a new range of vegan and gluten-free gourmet cookies. The product lineup includes flavors such as Double Chocolate Chip, Salted Caramel, Chocolate Chip, and Banana Good Granola.

- February 2025: Flowers Foods completed its USD 795 million acquisition of Simple Mills, a leading natural snack manufacturer specializing in gluten-free crackers, cookies, and baking mixes.

- October 2024: Feel Good Foods has launched gluten-free chicken soup dumplings, strategically designed to cater to consumer demand for convenient meal options, including lunch, light dinners, and afternoon snacks.

- May 2024: Mondelez International has launched its inaugural certified gluten-free cookie under the Chips Ahoy! brand. The company spent years perfecting the new cookie to achieve a texture and decadent taste.

Global Food Intolerance Products Market Report Scope

Food intolerance products refer to free-from products with claims like 'vegan,' 'dairy-free,' and others.

The global food intolerance products market is segmented by product type, labeling type, distribution channel, and geography. Based on the product type, the market is segmented into bakery products, confectionery products, dairy and dairy alternatives, meat and seafood, sauces, condiments and dressings, and others. Based on labeling type, the market is divided into gluten-free food, lactose-free food, and other labeling types. On the basis of distribution channels, the market is divided into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. The study also involves the global level analysis of regions such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Dairy and Dairy Alternatives |

| Bakery Products |

| Confectionery Products |

| Meat and Seafood Products |

| Sauces, Condiments and Dressings |

| Other Product Types |

| Gluten-Free Food |

| Lactose-Free Food |

| Others |

| Conventional |

| Organic |

| Supermarkets/Hypermarkets |

| Health-Food Stores |

| Convenience and Grocery Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Dairy and Dairy Alternatives | |

| Bakery Products | ||

| Confectionery Products | ||

| Meat and Seafood Products | ||

| Sauces, Condiments and Dressings | ||

| Other Product Types | ||

| By Labeling Type | Gluten-Free Food | |

| Lactose-Free Food | ||

| Others | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health-Food Stores | ||

| Convenience and Grocery Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the free-from foods market?

The free-from foods market size stands at USD 14.56 billion in 2026 and is projected to reach USD 19.77 billion by 2031, supported by a 6.30% CAGR.

Which region leads the global free-from foods market?

North America leads with a 35.40% revenue share in 2025, driven by clear labeling regulations and high consumer awareness.

Which product segment is growing the fastest?

Confectionery products, including allergen-friendly chocolates and gummies, are forecast to grow at a 7.68% CAGR through 2031.

How is e-commerce influencing free-from food sales?

Online grocery channels are expanding at a 8.98% CAGR, offering broader assortment filters and direct distribution to consumers with specialized dietary needs.

Page last updated on: