Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

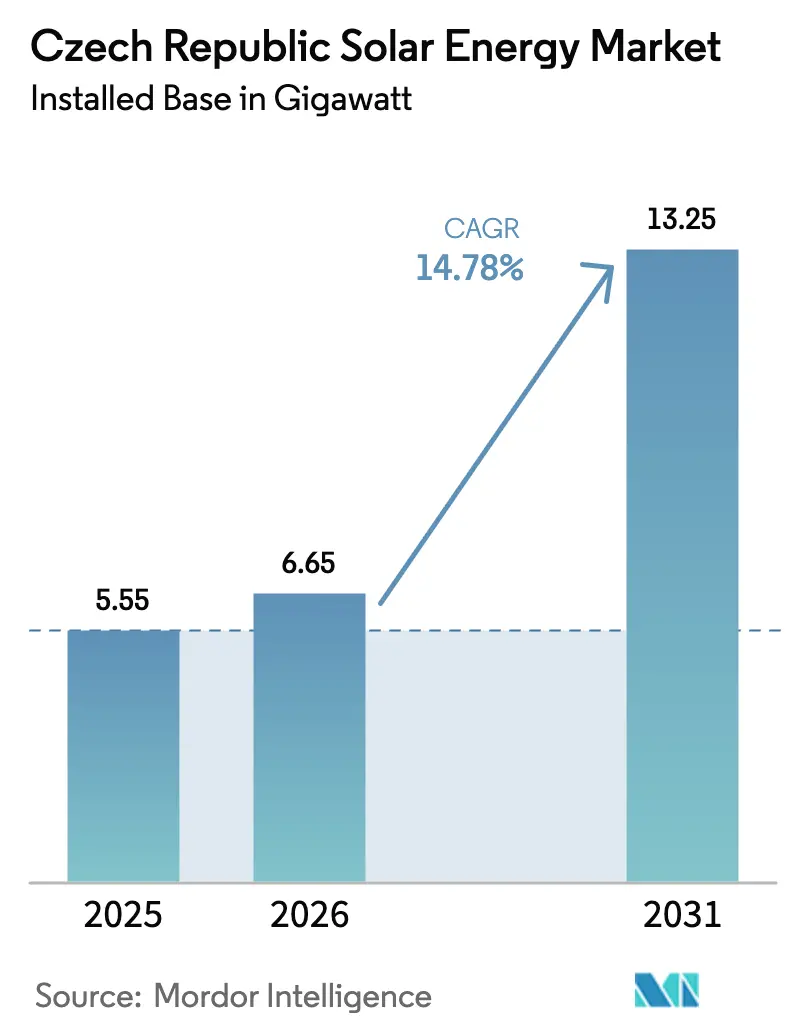

| Base Year Market Size (2025) | 5.55 gigawatt |

| Market Volume (2026) | 6.65 gigawatt |

| Market Volume (2031) | 13.25 gigawatt |

| Growth Rate (2026 - 2031) | 14.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Solar Energy Market Analysis by Mordor Intelligence

The Czech Republic Solar Energy Market size in terms of installed base is expected to grow from 5.55 gigawatt in 2025 to 6.65 gigawatt in 2026 and is forecast to reach 13.25 gigawatt by 2031 at 14.78% CAGR over 2026-2031.

Rising corporate demand for long-term price certainty, the National Energy and Climate Plan’s 10 GW target for 2030, and Modernisation Fund grants worth CZK 76.7 billion (USD 3.2 billion) are the core forces lifting the Czech Republic's Solar Energy market. Utility developers are redeploying former coal sites to bypass greenfield permitting, while engineering-procurement-construction specialists fight for rooftop contracts amid tightening grid-connection queues in South Moravia. Falling auction strike prices are steering projects toward merchant and corporate offtake models, and a wave of battery-ready designs is emerging as installers prepare for intraday arbitrage opportunities. Competitive intensity is moderate: ČEZ, Photon Energy, and Solek lead utility pipelines, but more than twenty smaller firms crowd the commercial rooftop arena.

Key Report Takeaways

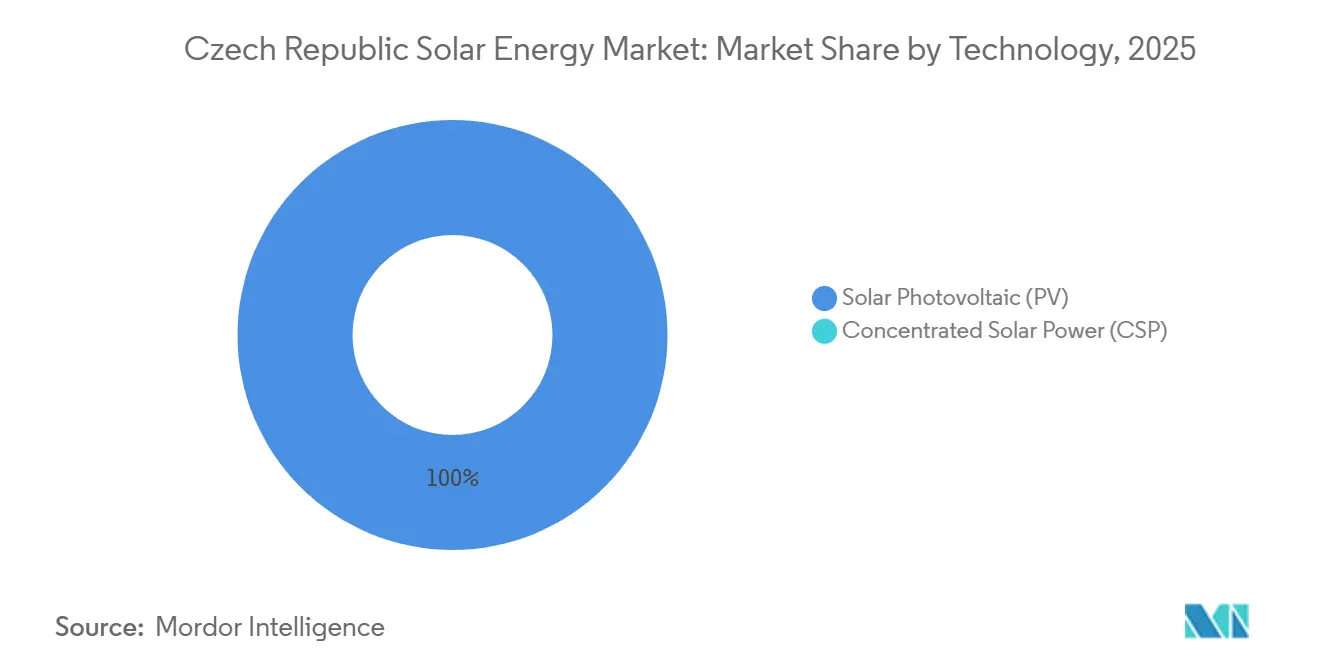

- By technology, photovoltaic systems held 100% of the Czech Republic's Solar Energy market share in 2025 and are set to mirror the overall 14.8% CAGR through 2031.

- By grid type, on-grid systems commanded 98.4% of the Czech Republic Solar Energy market size in 2025, whereas the off-grid segment will rise at a 24.9% CAGR to 2031.

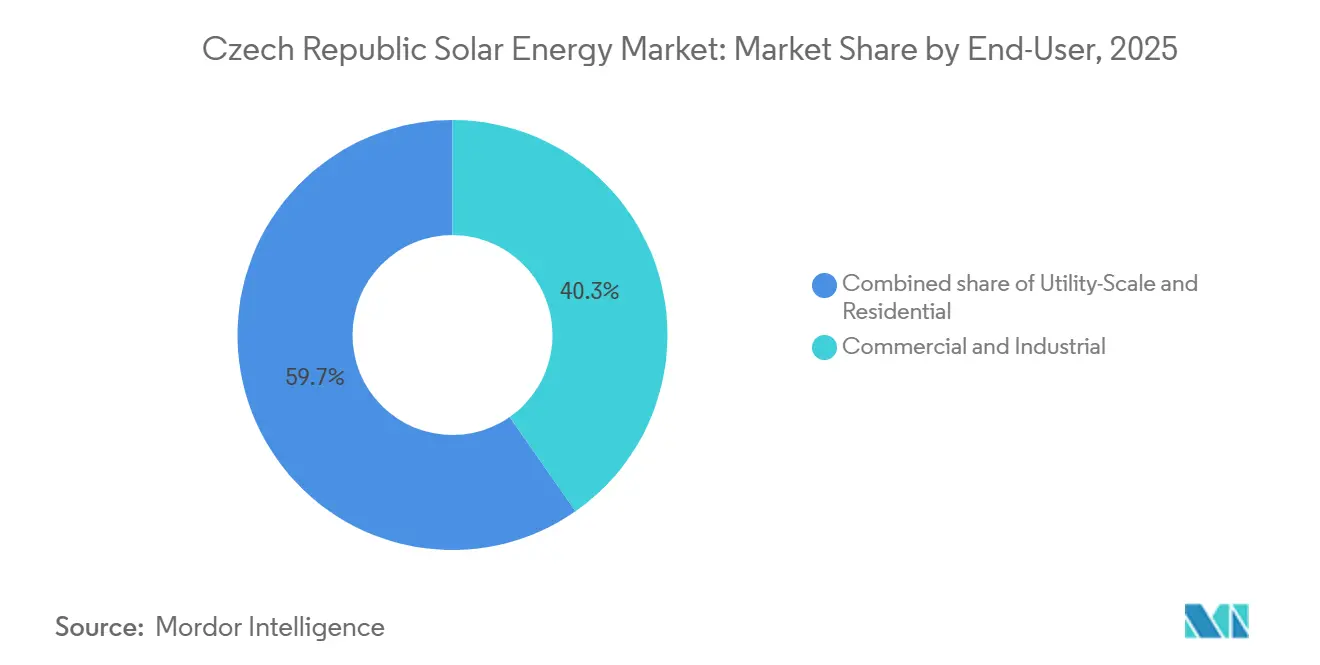

- By end user, the commercial and industrial segment led with 40.3% revenue share in 2025; residential installations are projected to post the fastest 27.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Czech Republic Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambitious NECP Target of 10 GW Solar by 2030 | 3.5% | National, with concentration in South Moravia, Central Bohemia, and Moravian-Silesian regions | Long term (≥ 4 years) |

| Declining Auction Strike Prices for Feed-in Premiums | 2.8% | National, utility-scale projects across all regions | Medium term (2-4 years) |

| Industrial-Power-Price Hedging by C&I Off-takers | 2.2% | National, strongest in industrial zones (Brno, Ostrava, Prague periphery) | Medium term (2-4 years) |

| EU Recovery & Resilience Funding for Rooftop PV | 2.0% | National, preferential allocation to Karlovy Vary, Moravian-Silesian, Ústí nad Labem | Short term (≤ 2 years) |

| ČEPS Grid-Upgrade Program 2025-27 | 1.8% | National transmission backbone, enabling capacity in South Moravia and North Bohemia | Medium term (2-4 years) |

| 2024 Community-Energy Law for Collective Self-Consumption | 1.5% | National, urban multi-tenant buildings and municipal cooperatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ambitious NECP Target of 10 GW Solar by 2030

The National Energy and Climate Plan anchors a floor for auction volumes and Modernisation Fund allocations, doubling installed capacity within five years and giving developers pipeline certainty. ČEZ’s 126.7 MW Tusimice and 115.7 MW Vysocany-Plato projects typify brownfield coal-site conversions that slash permitting risk. The target also intensifies land-lease competition in South Moravia and Central Bohemia, where agricultural landlords charge premiums for grid-proximate plots. International EPC contractors now view the Czech Republic Solar Energy market as a scale opportunity rather than a niche play. The Ministry of Industry and Trade cemented the goal in its 2023 State Energy Concept update, integrating it with nuclear and biomass plans.[1]Ministry of Industry and Trade, “State Energy Concept 2023,” renewablemarketwatch.com

Declining Auction Strike Prices for Feed-in Premiums

Clearing prices have neared grid parity since 2021, shifting project economics toward corporate PPA structures that lock 10-year fixed rates below spot forecasts.[2]KPMG Česká Republika, “RES+ Funding Note,” kpmg.com The RES+ program caps subsidies at 30% of the eligible cost, forcing developers to absorb merchant risk. Hybrid solar-plus-storage bids are materializing to monetize intraday volatility. Retroactive tariff cuts for 2009–2010 plants, passed in December 2024, underline the pivot to competitive support and deter reliance on legacy feed-in schemes.

Industrial Power-Price Hedging by C&I Off-takers

Rooftop arrays on logistics parks near Brno demonstrate how tenants use on-site generation to lock in tariffs below grid rates for 15 years. ČEZ ESCO finances construction, bearing balance-sheet risk, while tenants avoid capex. Public entities such as the Prague Congress Centre have copied the template, realizing CZK 5.5 million (USD 230,000) annual savings. Virtual PPAs remain scarce, leaving space for aggregators to bundle off-site solar with demand-response services.

EU Recovery & Resilience Funding for Rooftop PV

The RRF funnels EUR 7 billion into Czech green upgrades, with CZK 500 million (USD 21 million) ring-fenced for rooftop PV in lagging regions. ČEZ ESCO’s “PV for 1 CZK” model wraps grant administration into turnkey packages, but the need for a building permit at application slows smaller installers. The 70% self-financed portion screens out rooftops with sub-optimal orientation, nudging installers toward prime urban surfaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy above 1 MWp Permitting Timelines | -1.2% | National, acute in greenfield sites lacking prior industrial use | Medium term (2-4 years) |

| Distribution-Grid Congestion in South Moravia | -0.9% | South Moravia, localized in Brno periphery and Hodonín district | Short term (≤ 2 years) |

| Module Import Dependence & Logistics Tariffs Risk | -0.7% | National, supply-chain exposure to Asian manufacturers | Medium term (2-4 years) |

| Conservative Debt Tenors Squeezing IRRs | -0.5% | National, affecting independent power producers more than balance-sheet developers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy above 1 MWp Permitting Timelines

Projects over 1 MWp often spend more than a year in municipal and environmental approval queues, discouraging speculative pipelines and privileging incumbents with in-house legal teams. ČEZ mitigates the pain by reusing coal-plant land that carries existing industrial zoning, compressing lead times to eight months. New entrants increasingly pay premium leases to landowners holding pre-approved parcels.

Distribution-Grid Congestion in South Moravia

Transformer shortfalls near Brno create 6–12-month connection delays, nudging developers toward Central Bohemia despite lower isolation. Firms lacking legacy industrial feeders must either self-fund CZK 10 million (USD 420,000) upgrades or queue for distributor reinforcement, tilting the field toward large balance-sheet players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Monopoly Reflects Temperate Climate

Photovoltaics represented 100% of the Czech Republic's Solar Energy market in 2025 and will shadow the overall 14.8% CAGR through 2031 as CSP remains uncompetitive at Czech latitudes. The Prague Congress Centre chose SolarEdge inverters and ballast mounts to comply with urban safety codes, revealing how inverter topology has become a differentiator. Brownfield coal-site projects such as Mělník harness existing grid hookups, shaving both capex and timelines.

Module efficiencies exceeding 22% for tier-1 suppliers and cheaper ballast structures trim rooftop installation costs by up to 15%. Less than 5% of utility plants employ trackers because the 8–12% yield uplift cannot offset a 20–25% cost premium under frequent cloud cover. Integration of battery storage is accelerating, with ČEZ planning cells at Mělník to arbitrage intraday spreads. Residential experiments like the Kyselov Self-sufficient House achieve 90% self-reliance but face 10-year payback horizons that limit mass adoption.[3]Lifetree Project, “Self-sufficient House Performance,” lifetree.cz

By Grid Type: Off-Grid Surge Driven by Storage Economics

On-grid systems held 98.4% of the Czech Republic Solar Energy market share in 2025, yet off-grid arrays will post a 24.9% CAGR to 2031 as LiFePO4 batteries cheapen and Lex OZE 3 eases licensing for sub-100 kW plants. Rural households prioritize autonomy amid grid outages, while hybrid designs blur boundaries between grid-tied and island modes.

ČEZ ESCO’s Battery Box lets users scale storage from 5 kWh to 25 kWh, and all-in-one kits such as the MUST HBP1800 retail below CZK 94,000 (USD 3,930) for 10.24 kWh capacity.[4]mivvyENERGY, “HBP1800 Datasheet,” mivvyenergy.cz Industrial bidders, including CTP’s Eurologis tender, now stipulate battery-ready rooftops to secure backup power. Domestic suppliers like AERS employ second-life EV cells to win on warranty terms and local servicing.

By End-User: Residential Acceleration Outpaces C&I Maturity

Commercial and industrial buyers accounted for 40.3% of the Czech Republic Solar Energy market in 2025, leveraging power-price hedges and third-party finance. The residential segment will expand by 27.5% CAGR to 2031, catalyzed by RES+ subsidies and collective self-consumption rules.

Affluent Prague households install 5–10 kWp arrays with storage to reach 80% self-consumption, while lower-income homes in Karlovy Vary fit 3–5 kWp panels without batteries. Utility-scale developments, dominated by ČEZ, Photon Energy, and Solek, exploit Modernisation Fund grants that cover over half of capex, cushioning merchant-price exposure.

Geography Analysis

South Moravia, Central Bohemia, and the Moravian-Silesian region together hold roughly 65% of installed capacity, with South Moravia topping 1,100 kWh/m² annual insolation. Brno’s logistics parks host the nation’s largest rooftop portfolio at 5.5 MW, yet distribution bottlenecks delay further grid-tied additions. Central Bohemia attracts utility capital through reused coal sites such as Tusimice and Vysocany-Plato that already possess high-voltage hookups.

The Moravian-Silesian region is pivoting from coal, with ČEZ preparing 37 PV projects totaling 798 MWp alongside wind farms in Bruntál and Opava. Prague lacks ground-mount acreage but leads in complex rooftops like the 936 kWp Congress Centre installation that saves CZK 5.5 million (USD 230,000) a year. RES+ earmarked CZK 500 million (USD 21 million) for Karlovy Vary, Moravian-Silesian, and Ústí nad Labem to stimulate household adoption, where penetration trailed 2% in 2024.

A EUR 400 million ČEPS upgrade will erase transmission limits by 2026, after which distribution grids, especially in South Moravia, will become the chokepoint. Municipalities differ sharply: South Moravia fast-tracks zoning, North Bohemia guards farmland. Growing cross-border interconnection with Slovakia and Austria lets developers arbitrage regional price spreads, further integrating the Czech Republic Solar Energy market into Central European dispatch.

Regulatory Landscape

The Czech solar market operates under a policy framework led by the Ministry of Industry and Trade (MPO) for renewables support and the Energy Regulatory Office (ERU) for network regulation and connection rules. A key 2025-2026 inflection is the move to the VI regulatory period: ERU implemented its price control methodology for 2026-2030 effective January 1, 2026, bringing incentive regulation and flexibility-oriented elements that affect how TSOs and DSOs recover costs and prioritize grid upgrades relevant to PV connection queues.

On project development and grid access, Act No. 249/2025 Coll. (ZOZE), effective August 1, 2025, introduced acceleration concepts through defined areas intended to streamline permitting for renewables. Grid-connection rules were updated via Decree No. 302/2025 Coll., effective October 1, 2025, which also included definitions for energy storage facilities, supporting hybrid PV-plus-storage interconnection. Separately, Decree No. 248/2024 Coll. sets grid-connection parameters with selected provisions taking effect from April 1, 2026, reinforcing technical compliance expectations for new and modified plants.

Competitive Landscape

Market concentration is moderate. ČEZ, Photon Energy, and Solek held an estimated 55–60% of utility-scale capacity under development in 2025, while more than twenty EPC specialists divided the commercial rooftop space. ČEZ dominates brownfield conversions; its 126.7 MW Tusimice and 115.7 MW Vysocany-Plato units achieve sub-eight-month build cycles by reusing coal-plant permits and grid links. Photon Energy manages a 1.2 GWp regional pipeline and 130.4 MWp of operating assets, favoring cross-border scale to dilute Czech regulatory risk.

Solek’s 95.2 MW Leyda project in Chile, financed by BNP Paribas and BlackRock, signals how Czech players tap international debt when domestic lenders limit tenors to 10 years. Technology rivalry hinges on inverter architecture and storage coupling; tender documents now require battery readiness, pushing suppliers to bundle energy-management software. Emerging disruptors such as Greenbuddies specialise in ballast-mounted urban rooftops that demand stringent fire-safety compliance.

White-space opportunities include collective self-consumption schemes in Prague high-rises, hybrid solar-plus-storage for industrial redundancy, and virtual PPAs, virtually unused despite popularity in Western Europe. December 2024 tariff clawbacks destabilised vintage assets but inadvertently levelled the field for post-2020 entrants operating under auction mechanisms.

Czech Republic Solar Energy Industry Leaders

ČEZ Group

Photon Energy NV

Solar Global a.s.

Solartec Holding a.s.

Ekotechnik Czech s.r.o.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Corporate self-consumption and complex rooftop portfolios are emerging as a near-term whitespace where permitting and site-use rules are being simplified. Building Act amendments effective in early 2026 are geared toward PV deployment on existing roofs, parking areas, and operational spaces, with less zoning-plan friction in many cases, which aligns with the market shift toward corporate offtake and on-site generation. The pace of recent additions also provides a deployment benchmark for EPC capacity and supply chains, with 696 MW of solar added during 2025 taking cumulative installed capacity to around 5.5 GW by end-2025.

Acceleration and grid-integration reforms also broaden room for larger projects, repowering, and flexibility-linked business models. Act No. 249/2025 Sb. set out acceleration zones intended to simplify permitting, and 15 MW-plus PV projects are treated as energy security structures under the 2025 legislative amendments, improving administrative priority for utility-scale builds and brownfield conversions. At the same time, formal rules for battery energy storage systems (including differentiated treatment by system size) and updated connection rules that recognize storage-focused configurations make PV-plus-storage projects more bankable, and they can be paired with intraday optimization and emerging aggregation concepts under the Lex OZE framework.

Recent Industry Developments

- May 2026: ČEZ ESCO completed a 725 kWp rooftop solar installation at the EUROPARK Štěrboholy shopping center in Prague. The project adds another high-visibility commercial site to the distributed PV base and reinforces turnkey rooftop delivery as a growth lane in dense urban areas with limited ground-mount options.

- November 2025: CTP and ČEZ ESCO launched a 5.5 MW rooftop solar project in Brno and Blučina, described as the largest industrial rooftop installation in South Moravia. The footprint (nearly 86,000 m2) and planned output (around 5.2 GWh annually) highlight how logistics and industrial parks are converting roof area into generation capacity, despite local grid-connection constraints.

- August 2024: KGAL acquired a 50 MW Czech solar project (PVPP Saxonie) via its KGAL ESPF 5 impact fund, with the site planned near Most close to the German border. The transaction indicates continued appetite from non-domestic asset managers for Czech utility-scale pipelines, supporting liquidity for developers and recycling capital into new build activity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the total installed solar power capacity in the Czech Republic, counted in gigawatts, covering operating solar PV systems that deliver electricity either to the grid or behind the meter.

Coverage exclusions: We exclude solar thermal heating, concentrating solar power, and small unregistered off-grid kits that are not captured in official capacity reporting.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base of the model, especially around installed capacity history, annual additions, and the types of policy or permitting signals that typically move commissioning timelines in the Czech Republic. We relied on public energy statistics and power system reporting such as national energy regulators and grid operators, Eurostat energy balances, the IEA renewables statistics, and IRENA renewable capacity series, which help cross-check capacity totals and definitions.

To tighten assumptions, we also reviewed items like project announcements, press releases, company presentations, and audited annual reports where they clearly state commissioned MW and pipeline status. In a few cases, paid company financials and intelligence subscription content, and a paid news and financials subscription, were used to verify ownership changes and commissioning dates, which then fed into our consistency checks. These examples are not exhaustive, and many other public sources were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on checking what is actually getting connected and when, because official capacity numbers can lag project activity. We spoke with developers, EPC participants, equipment distributors, utilities, and large commercial buyers, and then used their feedback to confirm pipeline realism, typical build timelines, and the share of rooftop versus ground-mounted systems that reaches commissioning.

Coverage was kept Czech Republic specific, but viewpoints were balanced across investor-backed projects and smaller local installers, so assumptions on commissioning pace and repowering did not lean on one cohort.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 19% | APAC: 53% |

| Mid tier: 43% | Functional/Unit leaders: 28% | EMEA: 29% |

| Smaller Players: 20% | Managers: 53% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where national capacity time series and annual additions are reconstructed, then adjusted using commissioning signals from permitting and grid-connection progress in the Czech Republic. The totals are corroborated with selective bottom-up approximations, like sampling announced project MW, checking rooftop activity through installer channel feedback, and sanity-testing implied annual additions against observed connection constraints.

Inputs used in the model include the installed base in GW, yearly capacity additions, grid-connection lead times, typical project size mix (rooftop versus ground-mounted), repowering and lifetime assumptions, and policy triggers that affect economics (such as support scheme changes and connection rules). Where gaps existed in public reporting for smaller installations, the missing portion was filled using bounded ranges from interviews and then stress-tested, so the final number stayed consistent with official aggregates.

For forecasting, scenario analysis was used because growth can shift quickly with permitting bottlenecks, connection queues, and financing conditions. Assumptions for each scenario were anchored to expert consensus from primary discussions, and then translated into capacity-addition paths that roll forward into the installed base.

Data Validation & Update Cycle

Validation was done by triangulating model outputs against independent signals such as grid connection updates, regulator capacity registers, and the pace of new project commissioning communicated by market participants. When a year showed a sharp deviation, the drivers were rechecked, and follow-up calls were triggered to confirm whether the change came from delayed commissioning, reporting timing, or one-off large project starts.

Before sign-off, the model goes through a multi-step analyst review that includes unit checks, year-on-year variance checks, and consistency checks between additions and total installed base. Reports are refreshed annually, and interim updates are made when material events occur. Right before delivery, a final review pass is completed so clients receive the most current view.

Mordor Intelligence's Czech Republic Solar Energy Market Size Measured Against Other Published Estimates

Published estimates for the Czech Republic solar energy market often diverge because some sources size revenue while others size installed capacity, and because timing choices can shift the number that lands in a given year. Differences also show up when forecasts assume faster or slower grid connections, or when currency conversion is applied to local project costs at different points in the year.

A refresh-led difference is common here because equipment pricing and project economics move quickly, which can change implied ASPs and revenue-style totals even if the same MW is installed. The table reflects that spread, and the discipline comes from using the most recent capacity registers and reconciling them with commissioning checks, a cadence kept current in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.55 B (2025) | |

| Industry Research Publisher A | USD 1.80 B (2024) | This figure is value-based and expands scope beyond installed capacity by folding in services and adjacent infrastructure (including storage and digital layers), which raises definitional mismatch versus a capacity-led view and also shifts results with local currency and equipment price timing. |

| Global Research Publisher B | USD 1.94 B (2025) | This estimate is reported in USD value terms and is sensitive to assumed system prices, module mix, and the split across rooftop and utility projects. If ASP decline or commissioning timing is treated differently, the same underlying MW pipeline can produce a lower or higher USD total. |

Overall, the widest gaps come from mixing capacity and revenue concepts, plus how quickly price assumptions and connection progress are refreshed. By keeping the inputs tied to observable capacity movements and then checking them with market participants, the final view stays transparent and repeatable year to year.

Key Questions Answered in the Report

How large is the Czech Republic Solar Energy market in 2026?

Installed capacity reaches 6.65 GW in 2026 and is projected to climb to 13.25 GW by 2031 at a 14.78% CAGR.

Which segment grows fastest within Czech solar?

Residential systems are set to post a 24.9% CAGR to 2031, outpacing on-grid growth.

Who are the leading utility-scale developers?

ČEZ, Photon Energy, and Solek collectively control about 55–60% of utility-scale capacity under development.

What policy supports rooftop PV uptake?

RES+ grants, Lex OZE 2 and 3 licensing simplifications, and EU Recovery Facility funds collectively incentivize rooftop projects.

Why do investors favor brownfield coal sites?

Existing grid connections and industrial zoning shorten permitting to eight months and cut capex tied to new infrastructure.

Page last updated on: