Czech Republic ICT Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

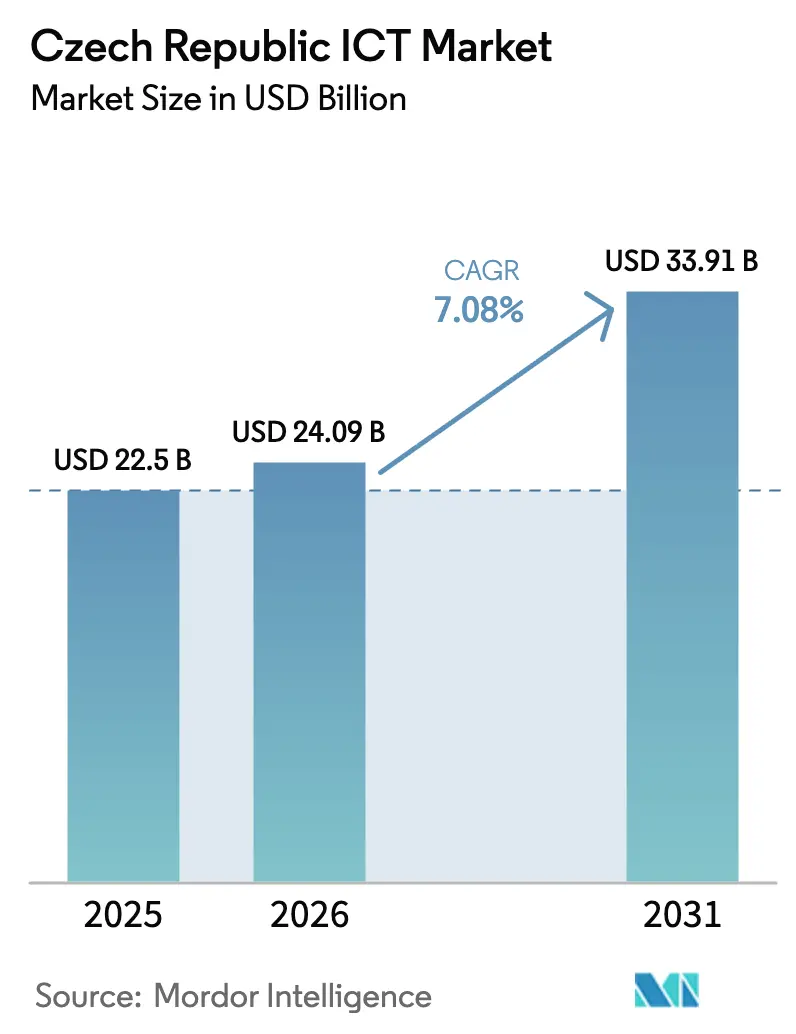

| Base Year Market Size (2025) | USD 22.5 Billion |

| Market Size (2026) | USD 24.09 Billion |

| Market Size (2031) | USD 33.91 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

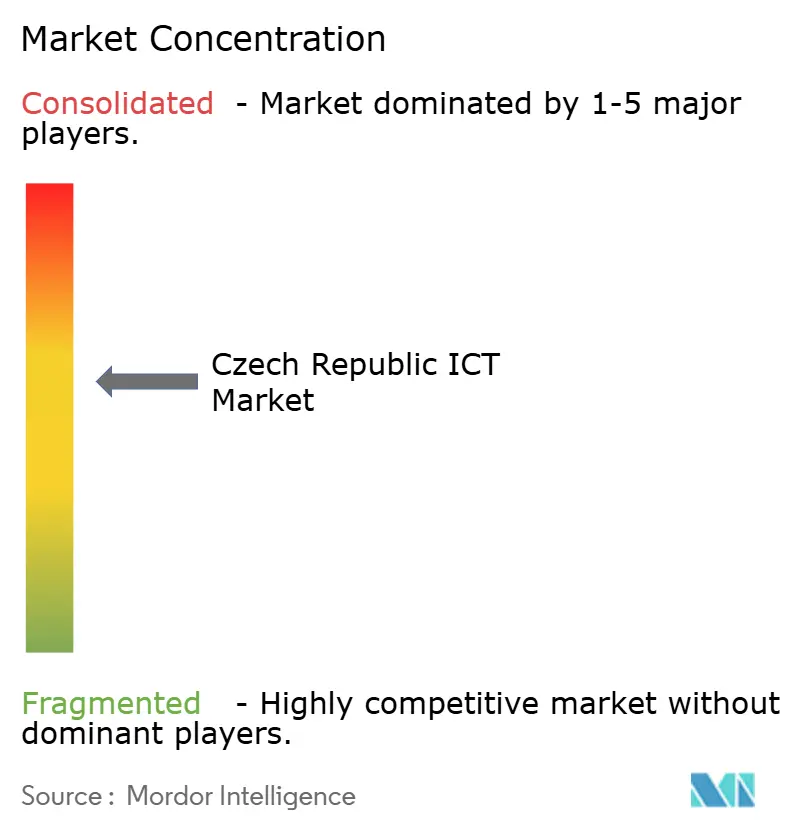

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Czech Republic ICT Market Analysis by Mordor Intelligence

The Czech Republic ICT market size was valued at USD 22.5 billion in 2025 and estimated to grow from USD 24.09 billion in 2026 to reach USD 33.91 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031). The Czech Republic ICT market is expanding on the back of EU recovery funds, accelerated 5G builds, and a vibrant startup scene that positions Prague as a digital gateway to Central Europe. Hardware spending remains the anchor of the Czech Republic ICT market because enterprises are still modernising core data-centre and network layers even as they pivot to cloud consumption. Rapid deployment of gigabit broadband and nationwide 5G is unlocking edge-computing use-cases that favour domestic telecom operators and international hyperscalers. Cyber-security outlays are rising in anticipation of the NIS2 Directive’s full enforcement, while EU-level near-shoring is luring Western European corporates that want both cost efficiency and deep engineering talent. Headwinds persist: senior developer shortages are inflating wages, and hefty spectrum licence fees are straining operator balance sheets even as capital intensity rises.

Key Report Takeaways

- By type, Hardware led with 33.40% of the Czech Republic ICT market share in 2025, whereas Managed Cloud Services are forecast to expand at a 7.05% CAGR through 2031.

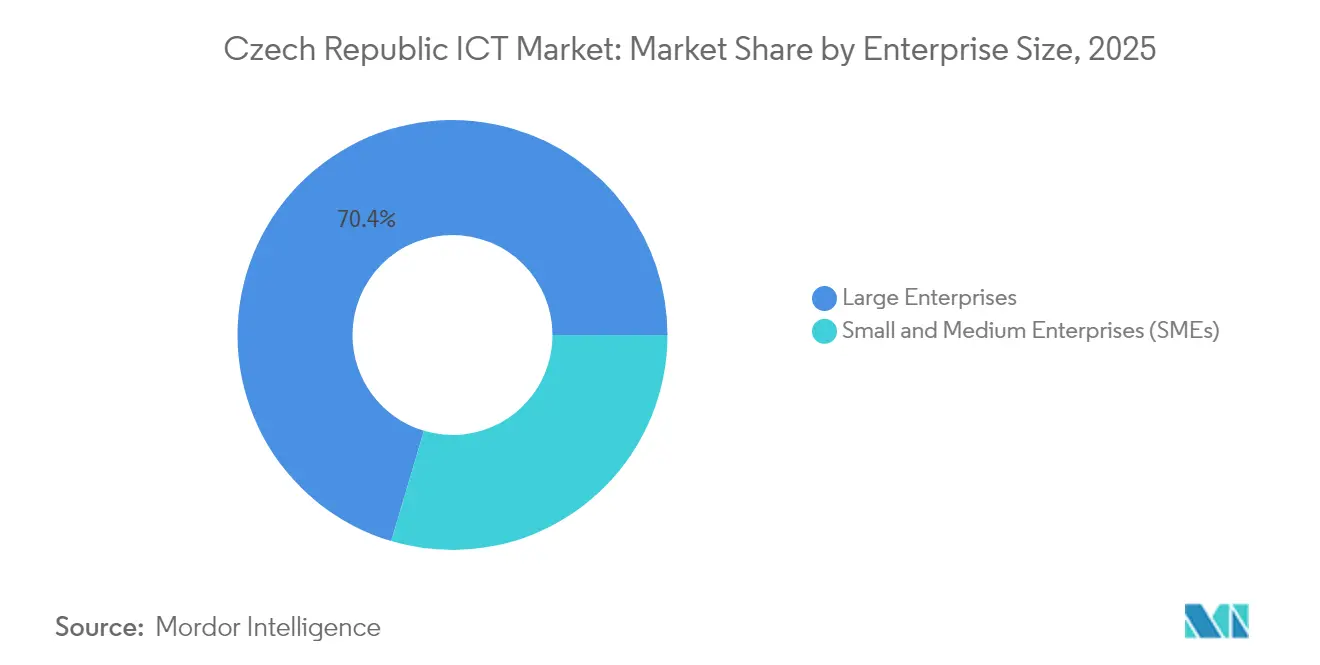

- By enterprise size, Large Enterprises commanded 70.40% of the Czech Republic ICT market size in 2025, but the SME segment is projected to grow at an 8.35% CAGR between 2026-2031.

- By industry vertical, BFSI held an 17.70% share of the Czech Republic ICT market size in 2025, while Smart Factory/Industry 4.0 solutions are advancing at a 8.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Czech Republic ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-funded "Digital Czechia 2030" Accelerating E-Government and Gigabit Connectivity | +2.10% | National, with concentration in Prague, Brno, and regional administrative centers | Medium term (2-4 years) |

| Prague's Start-up Boom Fueling Cloud-Native Infrastructure Demand | +1.80% | Prague and Brno, with spillover effects to smaller tech hubs | Short term (≤ 2 years) |

| Industry 4.0 Incentives for Manufacturing SMEs | +1.50% | Industrial regions, particularly in Moravia-Silesia and Central Bohemia | Medium term (2-4 years) |

| Rapid National 5G Roll-out (O2, CETIN, T-Mobile) Enabling Edge Services | +1.20% | Urban centers initially, expanding to nationwide coverage | Short term (≤ 2 years) |

| Near-shoring of EU Software Development to Czech Talent Hubs | +1.00% | Prague, Brno, and emerging secondary cities like Ostrava and Pilsen | Medium term (2-4 years) |

| Stricter Cyber-Compliance under EU NIS2 Driving Security Spend | +0.90% | National, with emphasis on critical infrastructure sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU-funded “Digital Czechia 2030” Accelerating E-Government & Gigabit Connectivity

The programme channels 22% of Czech Recovery and Resilience funds into digital priorities, which include 100% online public-service availability by 2030. Fixed broadband connections reached 890,000 in 2023, creating fresh demand for systems integrators and identity-management vendors [1]Czech Telecommunication Office, "Annual Report 2023", ctu.gov.cz. Despite progress, fragmented public information systems still need deep integration, an opportunity for middleware specialists.

Prague’s Startup Boom Fueling Cloud-Native Infrastructure Demand

More than 700 startups now operate in Prague, collectively valued at EUR 23 billion (USD 25.0 billion), and they raised EUR 264.5 million (USD 288.0 million) in 2024 alone. New funds such as Soulmates Ventures (EUR 50 million) and Tachles VC keep capital flowing, accelerating adoption of cloud platforms and DevSecOps pipelines [2]SeedBlink, "European VCs That Raised Fresh Funds in Q1 2025", seedblink.com.

Industry 4.0 Incentives for Manufacturing SMEs

More than 71.1% of Czech SMEs report at least a basic level of digital transformation, outpacing the EU average. Financial grants and training vouchers help smaller factories invest in robotics, IIoT sensors, and shop-floor analytics, but limited skillsets and culture gaps still slow advanced AI and VR deployments.

Rapid National 5G Roll-out Enabling Edge Services

Vodafone, O2, and T-Mobile surpassed 93% population coverage by late 2024, under long-dated licences that run to 2044. O2’s new Ericsson network includes RedCap technology for low-power IoT, with commercial launch slated for 2025. This coverage underpins latency-sensitive edge applications in logistics and smart city grids.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Senior IT-Talent Shortage & Rising Wage Inflation | -1.20% | National, most acute in Prague and Brno | Medium term (2-4 years) |

| High Spectrum Fees Constraining Telco CAPEX | -0.70% | National | Short term (≤ 2 years) |

| Fragmented Legacy IT in State Agencies | -0.50% | National, concentrated in government administrative centers | Long term (≥ 4 years) |

| Hardware Import Dependency & Supply-Chain Disruptions | -0.40% | National, with higher impact on manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Senior IT-Talent Shortage & Rising Wage Inflation

About 63% of firms struggle to hire senior developers, with data-science salaries climbing above EUR 60,000 (USD 65,300) a year. Companies counter wage pressure by offering 10%–20% sign-on bonuses and remote-first contracts, yet demographic ageing means the pipeline remains tight.

High Spectrum Fees Constraining Telco CAPEX

The 2020 5G auction cost operators CZK 5.596 billion (USD 254 million). Combined with sector-wide revenue pressure across Europe, operators must now balance licence obligations against fibre-to-the-home build-outs that CETIN targets at 1.3 million premises by 2030. Regulatory relief or further consolidation could ease financing constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardware Maintains Scale as Cloud Services Accelerate

Hardware captured a 33.40% slice of the Czech Republic ICT market in 2025. Telecom equipment demand is buoyant because all three mobile operators pursue aggressive 5G radio upgrades. Servers, storage arrays, and campus switches still underpin private-cloud and edge nodes, keeping capital spending steady even as companies rationalise data centres. The Czech Republic ICT market size for hardware-led deployments is set to expand gradually while infrastructure-as-a-service absorbs workloads that need burst capacity.

The fastest-growing service line is Managed Cloud Services, forecast to post a 7.05% CAGR to 2031. Consumption billing, faster deployment cycles, and compliance support are driving migration away from on-premises stacks. Cyber-security software spend is also surging because NIS2 compels critical-infrastructure entities to harden defences. Enterprise SaaS adoption is widening beyond ERP and CRM into verticalised suites for banking, retail, and healthcare, deepening the Czech Republic ICT market.

By Enterprise Size: SMEs Narrow the Capability Gap

Large Enterprises account for 70.40% of the Czech Republic ICT market, channelling investment into AI-driven automation, multicloud management, and zero-trust security. They are also early adopters of sovereign-cloud zones hosted in domestic data centres to meet EU data-residency obligations.

SMEs, supported by the SME Support Strategy 2021-2027, are projected to grow IT spend at an 8.35% CAGR. These firms leverage voucher schemes and tax subsidies to adopt digital invoicing, e-commerce, and low-code platforms. As a result, the Czech Republic ICT market size attributed to SMEs is expected to climb steadily, shrinking the historical capability gap. The Czech Republic ICT industry nonetheless faces lingering obstacles around digital-skill shortages and financing for advanced analytics, but public-private training initiatives begin to mitigate these barriers.

By Industry Vertical: Financial Services Lead While Manufacturing Digitises

BFSI held an 17.70% share of the Czech Republic ICT market size in 2025. Banks upgrade core banking stacks and embed AI in fraud detection, while insurers roll out telematics for dynamic pricing. Compliance with the Digital Operational Resilience Act further amplifies demand for vendor-risk-management platforms.

Smart Factory and Industry 4.0 solutions register the fastest growth at 8.95% CAGR. Automotive and machinery producers deploy digital twins and predictive-maintenance analytics to raise OEE and energy efficiency. Government grants offset capex, and 5G private networks enable low-latency control loops on the factory floor. Healthcare, retail, and education sectors remain earlier-stage but are ramping up cloud and cyber investments, broadening the Czech Republic ICT market.

Geography Analysis

The Czech Republic ICT market clusters around Prague and Brno, which together house the bulk of engineering and venture-capital talent. Prague alone generates the highest ICT wage levels—CZK 56,000 (USD 2,545) monthly—yet continues to attract both foreign direct investment and local unicorn founders. Access to Charles University and Czech Technical University sustains a robust though insufficient talent pipeline.

Brno emerges as the second pole of the Czech Republic ICT market, supported by Masaryk University’s computer-science faculty and a vibrant R&D scene. Y Soft’s EUR 30 million (USD 32.8 million) EIB funding confirms Brno’s strength in enterprise-software innovation. Secondary hubs such as Ostrava and Pilsen gain momentum as employers seek lower operating costs without compromising workforce quality.

EU digital-decade targets shape nationwide infrastructure plans. Despite 69.1% of citizens having basic digital skills, only 53% of households enjoy very-high-capacity fixed broadband, underscoring a rural connectivity gap. Ongoing FTTH roll-outs and 5G expansion aim to level regional disparities and unlock new opportunities across the Czech Republic ICT industry.

Competitive Landscape

Competition in the Czech Republic ICT market is mixed: telecommunications is highly concentrated, while software and services remain fragmented. O2 Czech Republic, T-Mobile, and Vodafone collectively command a telecom HHI above 3,000, reflecting limited rivalry. To expand service portfolios, O2 acquired Nordic Telecom in 2024, securing extra spectrum and rural wireless assets. Meanwhile, PPF’s divestiture of O2 and CETIN to e& Group in October 2024 reshuffles ownership structures and may unlock cross-border synergies [3]e& PPF Telecom Group B.V., "Annual Accounts 2024", datocms-assets.com.

In software, domestic champions Avast and JetBrains leverage Prague-based engineering to address global markets in cyber-security and developer tooling. Niche specialists target compliance automation, AI model orchestration, and Industry 4.0 middleware, thereby increasing competitive intensity across value pools. The Czech Republic ICT market sees vertical solution integrators partner with telecom operators to co-deliver edge-enabled offerings for manufacturing and smart mobility.

Infrastructure wholesalers such as CETIN Group accelerate fibre and tower roll-outs, creating neutral-host models that lower capital barriers for MVNOs and smaller ISPs. Strategic alliances between connectivity providers and hyperscale cloud operators are forming to meet rising demand for low-latency, in-country zones, reinforcing the Czech Republic ICT market’s attractiveness to foreign investors.

Czech Republic ICT Industry Leaders

-

T-Mobile Czech Republic a.s.

-

Vodafone Czech Republic a.s.

-

Avast Software s.r.o.

-

CETIN a.s.

-

O2 Czech Republic a.s.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CzechInvest launched the DEFENCE HUB to incubate dual-use technologies, aligning start-ups with NATO’s DIANA accelerator and broadening security-tech export potential.

- April 2025: Mplus Group acquired Conectart for EUR 14 million (USD 15.3 million) to deepen CX BPO capabilities and apply automation tools across 42 delivery sites.

- April 2025: PPF Group reported EUR 3.2 billion (USD 3.5 billion) net profit for 2024, fuelled by telecom EBITDA growth and its strategic partnership with e& Group

- March 2025: Y Soft secured EUR 30 million (USD 32.8 million) in EIB venture debt to boost cloud-based office automation R&D in Brno

Czech Republic ICT Market Report Scope

Information and communication technologies or ICT is a broader term for information technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form. The revenue tracks the product offerings provided by the companies.

The Czech ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of enterprises (small and medium enterprises and large enterprises), and industry verticals (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Computing Equipment (Servers, PCs) |

| Networking Equipment | |

| Storage Systems | |

| Peripherals and Others | |

| Software | Enterprise Applications (ERP, CRM) |

| Infrastructure Software (OS, Middleware, DB) | |

| Cyber-security Software | |

| Productivity and Collaboration Software | |

| Vertical-specific Software | |

| IT Services | Consulting and Integration |

| Managed Services | |

| Support and Maintenance | |

| Cloud Services | |

| Telecommunication Services | Mobile Voice |

| Mobile Data | |

| Fixed Voice | |

| Fixed Broadband | |

| Wholesale and Others |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Government and Public Sector |

| Retail and E-Commerce |

| Manufacturing |

| Energy and Utilities |

| Healthcare |

| Transport and Logistics |

| Education |

| Prague (CZ01) | Central Bohemia (CZ02) |

| South-West (CZ03) | |

| North-West (CZ04) | |

| North-East (CZ05) | |

| South-East (CZ06) | |

| Central Moravia (CZ07) | |

| Moravian-Silesia (CZ08) |

| By Type | Hardware | Computing Equipment (Servers, PCs) |

| Networking Equipment | ||

| Storage Systems | ||

| Peripherals and Others | ||

| Software | Enterprise Applications (ERP, CRM) | |

| Infrastructure Software (OS, Middleware, DB) | ||

| Cyber-security Software | ||

| Productivity and Collaboration Software | ||

| Vertical-specific Software | ||

| IT Services | Consulting and Integration | |

| Managed Services | ||

| Support and Maintenance | ||

| Cloud Services | ||

| Telecommunication Services | Mobile Voice | |

| Mobile Data | ||

| Fixed Voice | ||

| Fixed Broadband | ||

| Wholesale and Others | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | BFSI | |

| IT and Telecom | ||

| Government and Public Sector | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Healthcare | ||

| Transport and Logistics | ||

| Education | ||

| By Geography | Prague (CZ01) | Central Bohemia (CZ02) |

| South-West (CZ03) | ||

| North-West (CZ04) | ||

| North-East (CZ05) | ||

| South-East (CZ06) | ||

| Central Moravia (CZ07) | ||

| Moravian-Silesia (CZ08) | ||

Key Questions Answered in the Report

What is the current size of the Czech Republic ICT market?

The Czech Republic ICT market size is USD 24.09 billion in 2026.

How fast will the Czech Republic ICT market grow to 2031?

It is forecast to expand at a 7.08% CAGR to reach USD 33.91 billion by 2031.

Which segment is growing the fastest within the Czech Republic ICT market?

Managed Cloud Services are projected to post a 7.05% CAGR between 2026-2031.

Why is hardware still important in the Czech Republic ICT market?

Enterprises continue to refresh data-centre and network hardware to underpin 5G, edge, and cloud-migration projects.

Page last updated on: