Bulgaria ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.55 Billion |

| Market Size (2026) | USD 8.77 Billion |

| Market Size (2031) | USD 9.93 Billion |

| Growth Rate (2026 - 2031) | 2.53% CAGR |

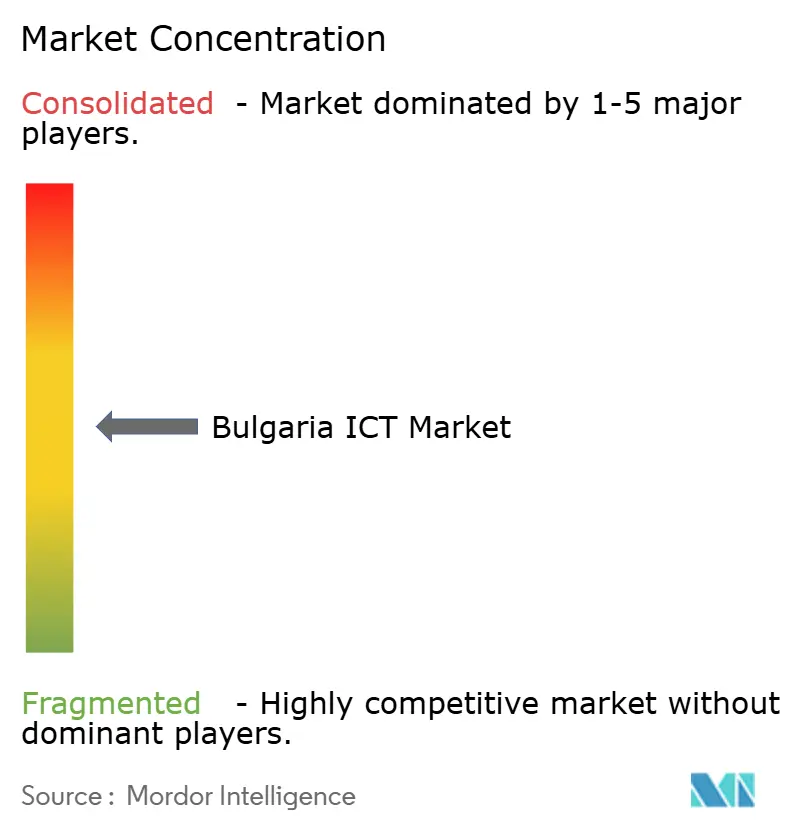

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bulgaria ICT Market Analysis by Mordor Intelligence

The Bulgaria ICT market size is expected to grow from USD 8.55 billion in 2025 to USD 8.77 billion in 2026 and is forecast to reach USD 9.93 billion by 2031 at 2.53% CAGR over 2026-2031. Infrastructure upgrades funded through the Digital Bulgaria 2025 program, nationwide 5G deployment, and steadily rising enterprise cloud adoption anchor long-term growth. Large enterprises keep directing the bulk of spending toward managed services, cybersecurity, and hybrid-cloud architectures, while EU cohesion funds and the Just Transition mechanism broaden demand in energy-transition regions. Competitive intensity is deepening as global majors expand local footprints and Bulgarian champions such as Lace AI attract venture funding, reinforcing Sofia’s role as a regional R&D hub. Persistent skills shortages, rural connectivity gaps, and energy-linked data-center costs temper the otherwise favorable outlook.

Key Report Takeaways

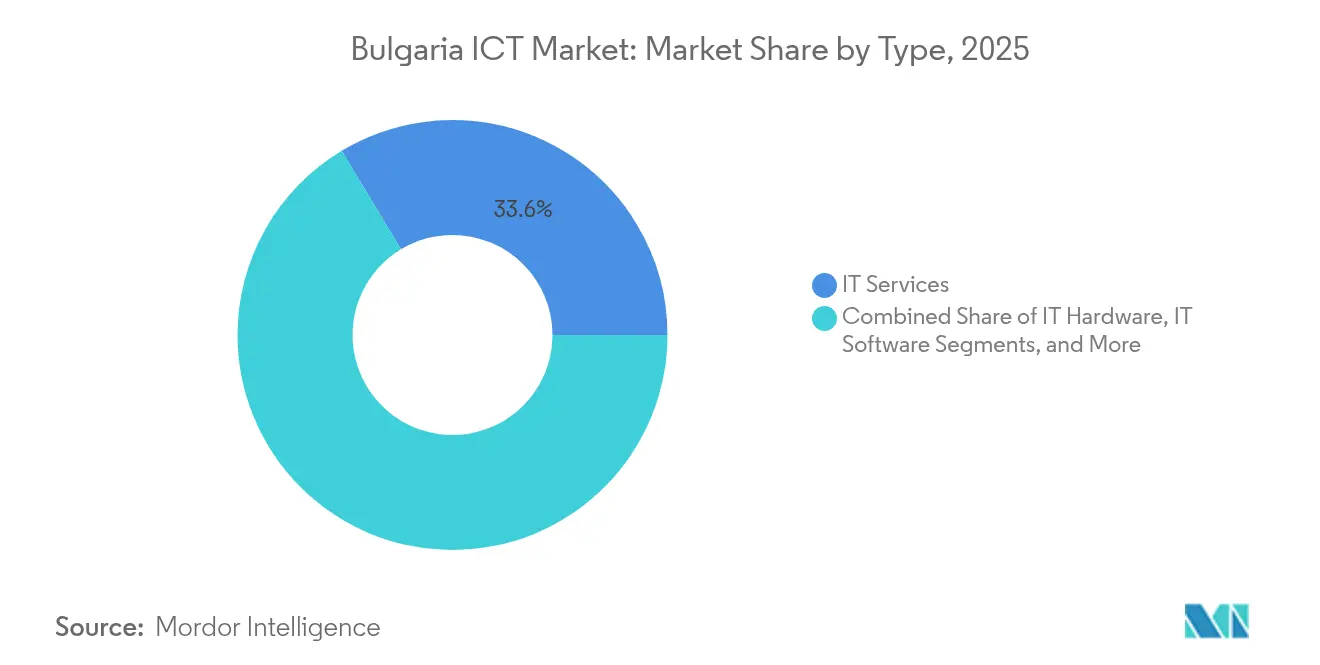

- By type, IT Services led with 33.62% of Bulgaria ICT market share in 2025; IT Security is forecast to expand at a 2.79% CAGR through 2031.

- By enterprise size, Large Enterprises captured 57.15% share of the Bulgaria ICT market size in 2025, while SMEs are projected to grow at 2.92% CAGR to 2031.

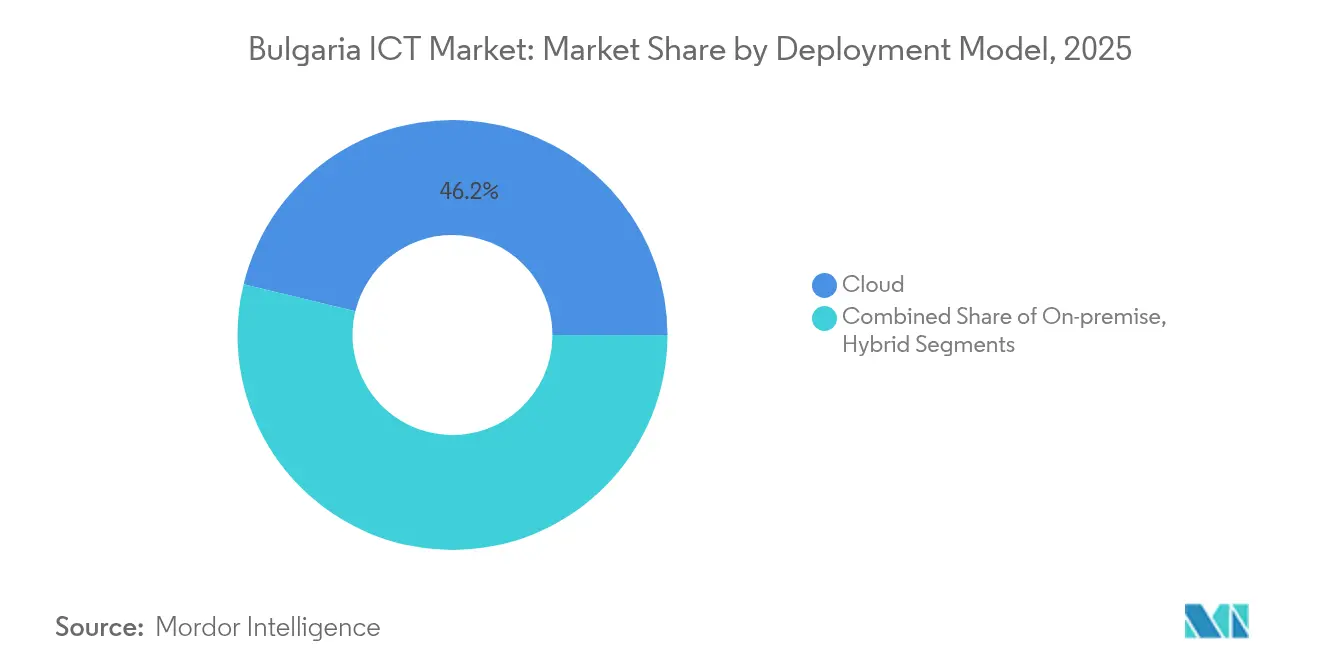

- By deployment model, cloud solutions commanded 46.20% share of the Bulgaria ICT market size in 2025 and are advancing at 2.85% CAGR through 2031.

- By end-user vertical, Government and Public Administration held 17.70% share of the Bulgaria ICT market in 2025; Gaming and Esports is the fastest-growing vertical at 3.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bulgaria ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Digital Bulgaria 2025 + EU funding | +0.8% | National, Sofia and regional centers | Medium term (2–4 years) |

| National 5G rollout | +0.6% | Urban first, rural expansion | Medium term (2–4 years) |

| Enterprise cloud and XaaS uptake | +0.5% | Nationwide, Sofia-centric | Long term (≥ 4 years) |

| Escalating cybersecurity threats | +0.4% | Critical infrastructure | Short term (≤ 2 years) |

| Near-shoring of Western-EU R&D | +0.3% | Sofia, Plovdiv, Varna | Long term (≥ 4 years) |

| Sofia Tech Park HPC demand | +0.2% | Sofia metro | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government Digital Bulgaria 2025 and EU Funding Propel Infrastructure Modernization

Digital Bulgaria 2025 allocates EUR 690 million (USD 808.66 million) to help SMEs and mid-caps digitize operations, mandates e-government services across ministries, and funds a national digital-skills platform serving 500,000 citizens by 2026. [1]European Commission, “Bulgaria’s Recovery and Resilience – Supported projects,” EC.EUROPA.EU The Fund Manager of Financial Instruments in Bulgaria (FMFIB) channels EUR 548.9 million (USD 643.30 million) from ESIF into thirteen blended-finance vehicles, triggering EUR 645.8 million (USD 756.86 million) in co-investment for innovation projects. Together, these instruments expand addressable demand for enterprise software, cybersecurity suites, and cloud infrastructure. Local vendors gain a springboard to export services into neighboring EU markets pursuing similar cohesion-fund programs, reinforcing long-run growth prospects for the Bulgaria ICT market.

Nation-Wide 5G Rollout Accelerates Enterprise Transformation

Telecom operators have earmarked BGN 1.1 billion (USD 0.66 billion) for 5G, with Vivacom targeting 90% population coverage by 2026 and A1 ranking fourth globally for network speed. Ultra-low-latency connectivity is already supporting predictive-maintenance pilots in automotive parts plants and real-time logistics visibility in Black-Sea ports. Parallel fiber upgrades under Vivacom’s 10GIGA program will pass 1.8 million addresses, enabling bandwidth-heavy AI applications. Although Bulgaria missed the October 2024 NIS2 transposition deadline, enterprises are pre-investing in edge-security solutions to mitigate compliance risk, further driving managed-service demand within the Bulgaria ICT market.

Cloud Adoption Rises Despite SME Lag

Cloud penetration among Bulgarian enterprises climbed to 14.2% in 2024 yet still trails the 38.9% EU average. Large corporations, compelled by governance and cost-efficiency mandates, anchor demand for hybrid architectures, while Microsoft forecasts Eastern-European cloud revenue to quadruple by 2029. Managed-service providers capture value as firms outsource migration and security tasks, explaining why IT Services holds 33.98% share of the Bulgaria ICT market. Government grant schemes now reimburse up to 50% of SME cloud-migration costs, signaling upside once administrative hurdles ease.

Escalating Cyber-Threat Landscape Spurs Security Spend

E-mail attacks on Bulgarian companies surged 197% in H2 2024. Penalties up to EUR 10 million (USD 11.72 million) under eventual NIS2 enforcement push boards to elevate cybersecurity budgets, catalyzing a 2.87% CAGR for the security segment-well above the broader Bulgaria ICT market. Investments include zero-trust frameworks among financial institutions and encrypted mobile communications for emergency-response agencies, supported by a EUR 63.7 million (USD 38.20 million) digital TETRA roll-out.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High digitalization cost for SMEs | −0.4% | Nationwide, rural focus | Medium term (2–4 years) |

| IT-skills shortage & out-migration | −0.3% | Sofia brain drain | Long term (≥ 4 years) |

| Fragmented rural broadband | −0.2% | Mountain & border areas | Medium term (2–4 years) |

| Energy-price volatility on data centers | −0.1% | Data-center clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Digitalization Costs Constrain SME Uptake

Full-scale digital adoption can exceed 20% of annual revenue for many SMEs, discouraging cloud migration even where grant funding is available. Rural firms struggle with patchy broadband, forcing them to rely on lower-cost, on-premise solutions and limiting revenue upside for the Bulgaria ICT market.

Persistent Skills Gaps Limit Market Velocity

Fewer than 3% of Bulgarian workers are ICT specialists, and just 31.2% of adults possess basic digital skills, widening the talent deficit as Western-EU employers lure engineers abroad. [2]European Bank for Reconstruction and Development, “Bulgaria Country Diagnostic,” EBRD.COM Despite initiatives such as the Women in Tech program training 500+ unemployed women, near-term supply constraints hold back advanced-technology adoption rates in the Bulgaria ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: IT Services Anchor Market Transformation

IT Services account for 33.62% of Bulgaria ICT market share in 2025 on the strength of cloud migration, security outsourcing, and business-process automation contracts. The Bulgaria ICT market size attributable to IT Security is expanding at a 2.79% CAGR through 2031, supported by NIS2-driven compliance projects. Hardware demand remains stable as carriers pour BGN 1.1 billion (USD 0.66 billion) into 5G infrastructure, sustaining orders for networking gear and edge servers. Software sales benefit from public-sector digitization; ministries are integrating e-signature, document-management, and citizen-ID modules to meet Digital Bulgaria 2025 milestones. Communication Services gain momentum from Vivacom’s 10GIGA fiber and smart-city pilots across 130 municipalities.

Second-order effects reinforce service revenue: complex hybrid-cloud environments require ongoing optimization, and rising cyber-insurance premiums incentivize managed-detection and response contracts. Domestic suppliers differentiate through language skills and EU regulatory expertise, while global integrators leverage economies of scale to win nationwide roll-outs. Over the forecast horizon, converged IT-OT solutions for Industry 4.0 are expected to lift demand for analytics-driven managed services in manufacturing hubs such as Plovdiv and Stara Zagora.

By Enterprise Size: Large Enterprises Dominate Spending

Large corporations captured 57.15% of Bulgaria ICT market outlays in 2025, reflecting capital resources to implement ERP modernization, zero-trust security, and AI-enabled customer analytics. Yet SMEs, aided by EUR 690 million (USD 810.98 million) in Economic Transformation grants, will drive incremental volume, growing at 2.92% CAGR to 2031. SME adoption concentrates on SaaS collaboration suites and affordable cyber-hygiene bundles as threats intensify. Micro-enterprises in rural areas still rely on on-premise solutions or mobile hotspots, underscoring the importance of ongoing broadband programs.

Large enterprises increasingly outsource to Bulgarian R&D centers as part of near-shoring strategies, boosting project pipelines for domestic service firms. Meanwhile, SME cloud-migration remains sensitive to subscription pricing and the availability of local language support. Vendors offering usage-based billing and bundled training stand to acquire share once digital-skills programs raise baseline capabilities across the workforce.

By Deployment Model: Cloud Momentum Builds

Cloud accounted for 46.20% of Bulgaria ICT market size in 2025 and is forecast to post the highest 2.85% CAGR through 2031. Hybrid deployments dominate among banks and utilities balancing data-residency mandates with elasticity benefits. On-premise systems persist in regions lacking reliable high-speed links; roughly 15% of households still lack fixed broadband, limiting full cloud offload potential. The planned NIS2 law may boost private-cloud adoption as firms prioritize data-sovereignty controls.

New data-center investments cluster around Sofia, Varna, and Burgas, taking advantage of submarine-cable access and free-cooling climates. Edge sites tied to 5G macro towers will support low-latency workloads such as machine-vision in logistics parks. CSPs partner with local ISPs to offer managed Wi-Fi and SD-WAN services to SMEs, translating connectivity upgrades directly into platform revenue for the Bulgaria ICT market.

By End-user Vertical: Government Leads Digital Spend

Government and Public Administration absorbed 17.70% of Bulgaria ICT market value in 2025 on compulsory e-government projects and cybersecurity modernization. BFSI maintains steady demand for AML analytics and secure mobile banking, while manufacturing taps 5G and IoT to automate production lines. Gaming and Esports, propelled by Bulgaria’s strong software talent pool, is the fastest-growing vertical at 3.36% CAGR, reflected in Lace AI’s 1,000% revenue surge in 2024.

Energy-sector digitalization accelerates as utilities deploy smart-metering and predictive-maintenance systems funded under the Just Transition mechanism. Healthcare invests in telemedicine platforms such as Healee, which integrates with national e-health records to expand specialist access beyond Sofia. Retail and logistics players are overhauling supply-chain visibility using SaaS inventory modules, positioning the sector for stronger e-commerce penetration once rural broadband gaps narrow.

Geography Analysis

Sofia generates roughly 87.60% of Bulgaria’s ICT value-added, employing about 105,000 tech specialists at an average monthly wage of BGN 4,700. The capital’s dense fiber grid-85% coverage-coupled with Sofia Tech Park’s Discoverer supercomputer and EUR 90 million (USD 105.48 million) BRAIN++ AI factory attracts multinationals such as Progress Software and IBM. Venture investment surpassed EUR 3.1 billion between 2021 and 2024, with Lace AI and EnduroSat exemplifying deep-tech scale-ups. This critical mass cements Sofia as the principal node of the Bulgaria ICT market and a magnet for near-shored R&D work from Western-EU clients.

Secondary hubs are emerging in Plovdiv, Varna, and Burgas, aided by local universities and cost advantages over the capital. Telelink Business Services targets USD 100-150 million in Western-EU contracts to be executed from these cities, diversifying geographic exposure of the Bulgaria ICT market. Regional authorities leverage EU cohesion funds to build incubators and fiber rings, seeking to replicate Sofia’s clustering effects. Still, broadband black spots in mountainous districts inhibit wider SME participation in cloud commerce.

The rural digital divide remains pronounced: about 15% of households in border zones lack reliable internet, curbing e-commerce and telework adoption. Just Transition programs earmark more than EUR 1 billion (USD 1.17 billion) for coal-region diversification into digital services, funding reskilling and micro-data-center pilots in Stara Zagora, Pernik, and Kyustendil. Over time, these efforts should broaden the revenue base and temper Sofia’s dominance, fostering a more balanced Bulgaria ICT market.

Competitive Landscape

Global incumbents-including Microsoft, IBM, SAP, Cisco, and Oracle-vie with dynamic local players such as Sirma Group, Evrotrust, and Progress Software for projects spanning e-government, cybersecurity, and cloud integration. International providers leverage scale and product depth, while domestic specialists win on regulatory insight and Bulgarian-language support. For example, Evrotrust now pilots Digital ID wallet scenarios within an EU consortium, showcasing compliance-ready solutions that resonate with public-sector buyers. [4]Investor.bg, “Vivacom ordered to reverse price indexation,” INVESTOR.BG

Strategic plays center on partnerships and ecosystem positioning. Huawei supports the Women in Tech program to bolster talent pipelines, whereas Vivacom commits BGN 3 billion (USD 1.80 billion) to network modernization to secure municipal smart-city contracts. Start-ups such as AMPECO and Lace AI raise eight-figure rounds, validating Bulgaria as a launchpad for export-oriented SaaS and deep-tech ventures. These dynamics intensify competition for scarce specialists, pushing wages upward and prompting firms to establish satellite sites in Plovdiv and Varna.

White-space opportunities persist in managed cybersecurity, rural connectivity solutions, and SME-tailored cloud bundles. Only 14.2% of enterprises have moved to cloud platforms, signaling room for growth. Vendors that combine pricing flexibility with turnkey training could unlock latent demand and gain share in the Bulgaria ICT market. Overall, the top five providers control around 35% of spending, indicating a moderately fragmented environment that favors specialists capable of meeting EU-grade compliance requirements.

Bulgaria ICT Industry Leaders

IBM Corporation

Hewlett Packard Enterprise Company

Cisco Systems Inc.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lace AI closed a USD 19 million seed round led by Bek Ventures, citing 1,000% revenue growth in 2024 and designating Sofia as its primary R&D base.

- February 2025: EnduroSat secured USD 21 million Series A funding to expand its cloud-based nanosatellite platform.

- February 2025: Bulgaria’s Supreme Administrative Court blocked Vivacom’s attempt to index mobile-service prices, ordering refunds to consumers.

- January 2025: Codery and Devision merged to create a broader technology-services player focused on export markets.

Bulgaria ICT Market Report Scope

ICT, an umbrella term encompassing Information Technology (IT), covers a wide array of communication technologies. These include wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and various media applications. Collectively, these technologies empower users to store, access, transmit, retrieve, and manipulate information in digital formats.

The Bulgarian ICT market is segmented by type (hardware, software, services, and telecommunication services), size of enterprise (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals).

The market sizes and forecasts are provided for a value of USD for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

What is the current value of the Bulgaria ICT market?

The market stands at USD 8.77 billion in 2026 and is set to reach USD 9.93 billion by 2031.

How fast is cloud adoption growing among Bulgarian enterprises?

Cloud deployments hold 46.20% share and are expanding at a 2.85% CAGR, faster than on-premise systems.

Which segment leads the Bulgaria ICT market by type?

IT Services dominate with 33.62% share due to demand for managed services and cloud migration.

Why is cybersecurity spending rising in Bulgaria?

E-mail attacks jumped 197% in H2 2024 and impending NIS2 compliance is driving investment in security solutions.

Which geographic area attracts the most ICT investment in Bulgaria?

Sofia accounts for 87.60% of ICT value-added, supported by dense fiber coverage and the Sofia Tech Park ecosystem.

How are SMEs being supported in their digital transformation?

The Economic Transformation Program provides EUR 690 million in grants and guarantees to help SMEs fund digital upgrades.

Page last updated on: