Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

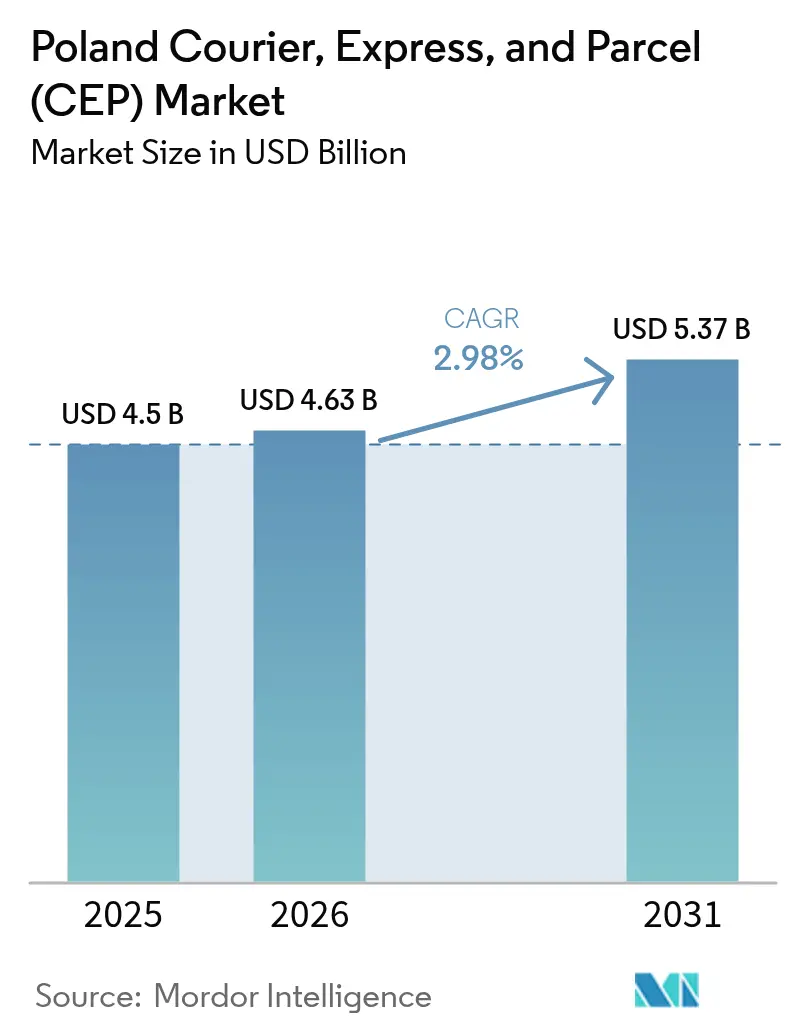

| Base Year Market Size (2025) | USD 4.5 Billion |

| Market Size (2026) | USD 4.63 Billion |

| Market Size (2031) | USD 5.37 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

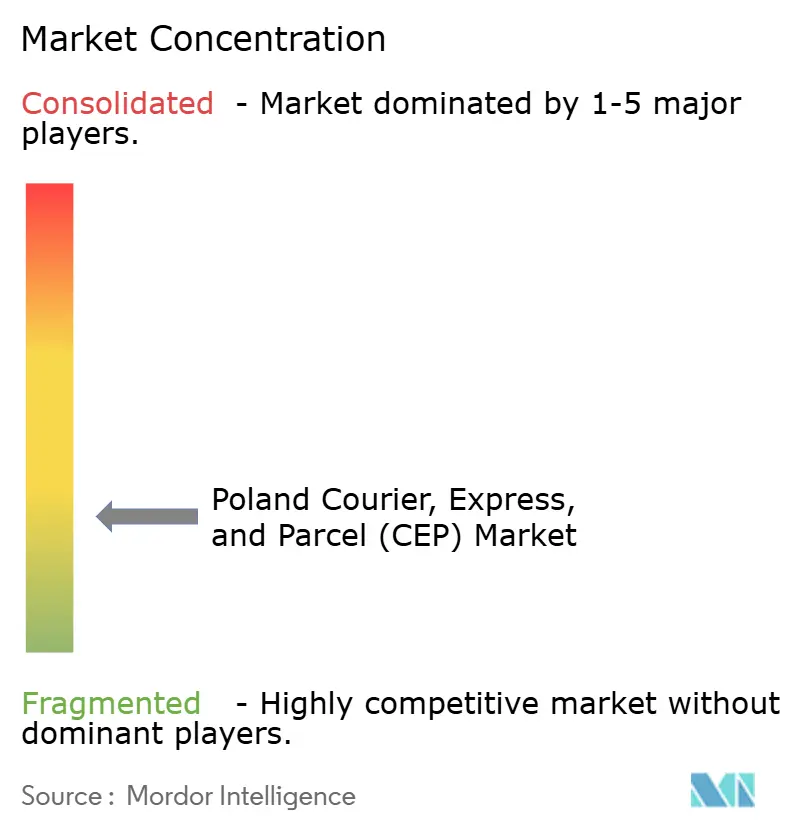

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Courier, Express, And Parcel (CEP) Market Analysis by Mordor Intelligence

The Poland courier, express, and parcel market size is expected to grow from USD 4.5 billion in 2025 to USD 4.63 billion in 2026 and is forecast to reach USD 5.37 billion by 2031 at 2.98% CAGR over 2026-2031.

Robust e-commerce spending, expanding cross-border trade, and sustained infrastructure upgrades funded by European programs are reinforcing parcel flows across the nation. Automated parcel lockers continue to lift delivery density and lower unit costs, while technology-enabled route planning helps operators counter rising labor expenses. Regulatory stimuli that encourage zero-emission fleets support modal shifts toward rail and electric road vehicles, further shaping competitive positioning. Taken together, these drivers signal steady yet disciplined growth as the Poland courier, express, and parcel market approaches structural maturity.

Key Report Takeaways

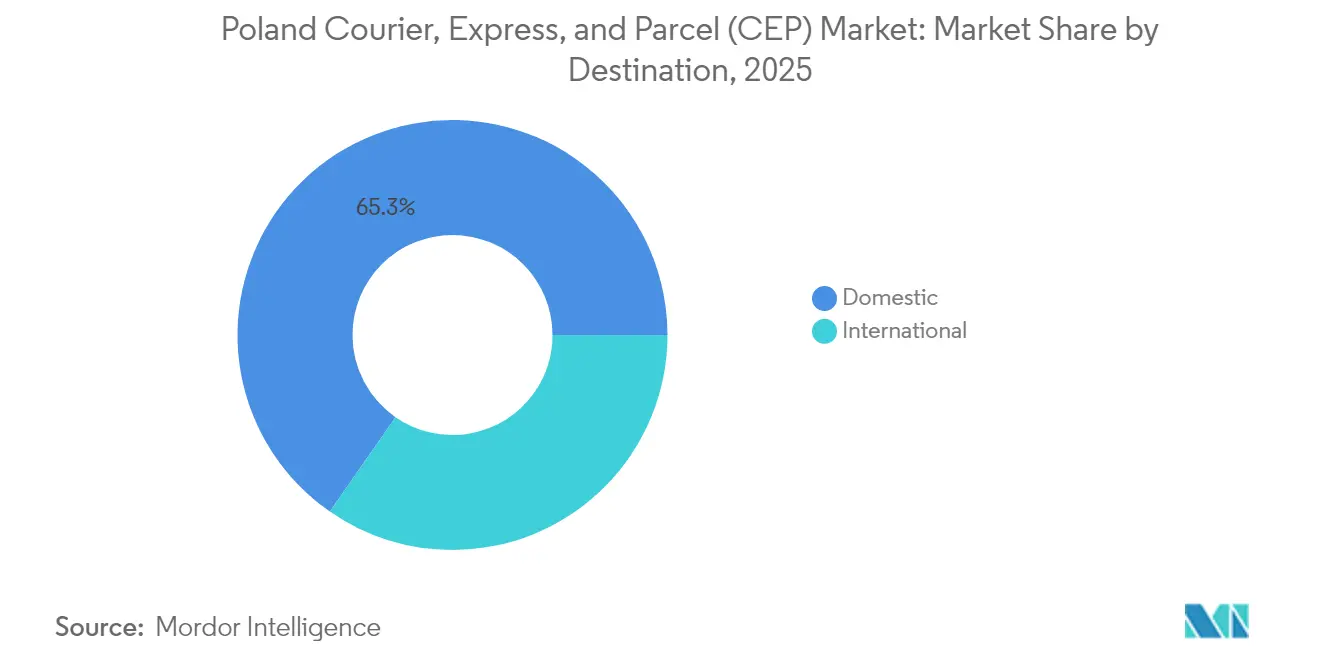

- By destination, domestic shipments led with 65.34% of the Poland courier, express, and parcel market share in 2025, while international parcels are projected to expand at a 3.18% CAGR through 2031.

- By speed of delivery, non-express services accounted for 76.05% share of the Poland courier, express, and parcel market size in 2025; express shipments post the fastest 3.52% CAGR through 2031.

- By model, Business-to-Consumer held 51.84% revenue share in 2025 and is advancing at a 3.96% CAGR to 2031, reflecting the strength of e-commerce fulfillment.

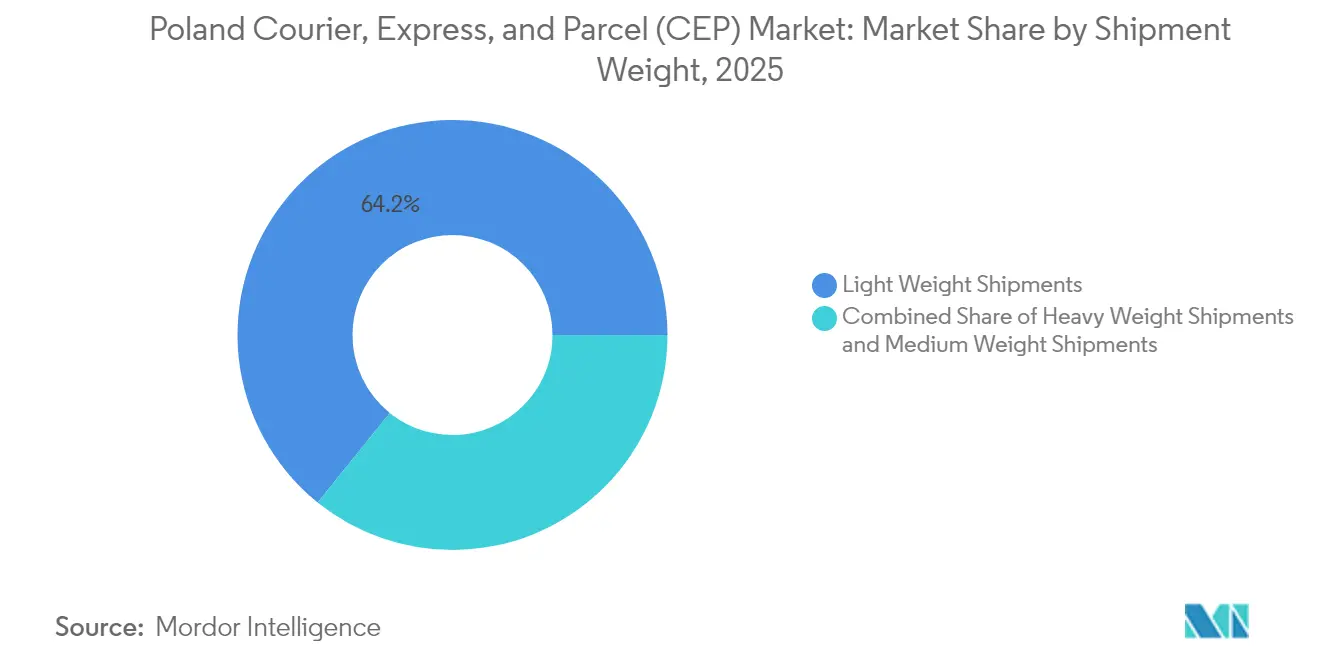

- By shipment weight, light parcels captured 64.21% of volume in 2025 and are forecast to grow at a 3.34% CAGR, mirroring the shift toward smaller, higher-value items.

- By mode of transport, road commanded a 50.87% share in 2025, whereas rail-based and other multimodal routes are projected to rise at a 3.79% CAGR on cost and sustainability advantages.

- By end-user industry, e-commerce contributed 41.65% of demand in 2025 and is expanding at a 3.31% CAGR, signaling continued penetration in rural regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Courier, Express, And Parcel (CEP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce volume growth post-COVID | +0.8% | Warsaw, Kraków, Gdańsk metro areas | Medium term (2-4 years) |

| Rapid adoption of parcel-locker networks | +0.6% | Urban cores spreading to suburbs and rural towns | Short term (≤ 2 years) |

| SME cross-border export surge via marketplaces | +0.4% | Border zones with Germany, Czech Republic; Warsaw logistics hub | Long term (≥ 4 years) |

| EU Fit-for-55 incentives for zero-emission fleets | +0.3% | Low-Emission Zones in Warsaw, Kraków, Wrocław | Long term (≥ 4 years) |

| AI-driven dynamic routing and micro-fulfillment | +0.2% | Nationwide, early uptake in core hubs | Medium term (2-4 years) |

| Government-funded postal infrastructure modernization | +0.2% | Nationwide with rural emphasis | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive E-Commerce Volume Growth Post-COVID

The pandemic jump-started digital retail, and online penetration is projected to hit 25% by 2032[1]AEW Research, “Logistics Remains Favorite As Take-Up And Values Are Projected To Recover,” aew.com. Allegro’s cross-border expansion and Amazon’s deeper Polish footprint enlarge the total addressable parcel pool, especially for next-day international fulfillment. Shoppers now treat same-day and next-day delivery as a standard inclusion, forcing carriers to redesign networks for speed rather than cost. Cashier-less convenience stores such as Żabka’s AiFi trial create micro-fulfillment nodes that shorten last-mile distances and demand near-real-time inventory updates. Rural areas remain underserved, offering sizable upside once locker density and road upgrades unlock reliable access. Overall, e-commerce keeps parcel volumes on a durable uptrend even as urban markets near saturation.

Rapid Adoption of Parcel-Locker (APM/PUDO) Networks

InPost operates Poland’s largest parcel-locker grid, lowering failed-delivery rates and mitigating labor shortages compared with door-to-door drops. Competitors such as Orlen Paczka and GLS race to match coverage, yet first-mover habit formation grants InPost stickiness. Lockers reduce unit delivery cost by clustering stops and enable 24-hour self-service, an advantage amplified during COVID-era distancing norms. Smaller couriers integrate with the network through API links, gaining nationwide reach without building costly last-mile fleets. Consumer surveys show a strong preference for contactless pickup, suggesting further diffusion into suburban and rural districts. As density rises, network effects reinforce the moat that large locker operators enjoy, reshaping market expectations for convenience.

SME Cross-Border Export Surge Via Marketplaces

Marketplace platforms empower Polish SMEs to ship globally without mastering customs procedures. Meest Post’s 2025 launch of direct services to the United States, Canada, and the United Kingdom exemplifies demand for long-haul lanes[2]Meest Post, “Ship Parcels from Poland to USA, Canada, and United Kingdom,” meestpost.com. EU trade facilitation and digital documentation tools simplify regulatory compliance, compressing delivery cycle time. Friend-shoring trends drive Western buyers toward Polish manufacturing capacity, increasing outbound parcel flows on B2B and B2C models. Currency stability inside the euro-pegged region reduces transaction risk, encouraging merchants to scale exports. This export momentum lifts the international share of Poland courier, express, and parcel market volume despite higher labor costs on West-bound routes.

EU Fit-for-55 Incentives for Zero-Emission Last-Mile Fleets

The EU’s Fit-for-55 climate package channels grants toward electric vans, depot chargers, and renewable energy hubs, directly lowering the cost of fleet transition. Municipal Low-Emission Zones provide access benefits for zero-emission vehicles, cutting detour times for compliant carriers. DHL’s new Poznań hub incorporates large-scale EV charging, signaling readiness for regulatory carbon caps. The KPO program earmarks PLN 40 billion (USD 12.2 billion) for green urban transport, unlocking co-investment with private couriers[3]Gov.pl, “KPO: 40 mld zł na projekty wspierające zieloną transformację miast,” gov.pl. As battery prices fall, the total cost of ownership converges with diesel vans, further accelerating uptake. Zero-emission fleets also support ESG disclosures required by the Corporate Sustainability Reporting Directive, offering brand upside in a competitive field.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute courier-driver shortage and wage inflation | -0.7% | Nationwide, severe in large cities | Short term (≤ 2 years) |

| EU Mobility Package wage parity | -0.4% | Cross-border routes to Western Europe | Medium term (2-4 years) |

| Urban Low-Emission-Zone surcharges | -0.3% | Warsaw, Kraków, Wrocław, Gdańsk | Medium term (2-4 years) |

| Parcel-locker vandalism and cyber-fraud | -0.1% | Areas with dense locker installation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Courier-Driver Shortage and Wage Inflation

Record-low jobless rates in Poland, coupled with competing industrial demand for labor, have intensified the battle for qualified drivers. Logistics wages now outpace headline inflation, squeezing margins for small carriers that cannot amortize costs via automation. Some courier firms experiment with signing bonuses and flexible schedules, but attrition remains high. Automation vendors report surging inquiries for robotic sorters, driven more by labor scarcity than by ROI calculations. Demographic aging further limits the driver pipeline, pushing operators toward electric cargo bikes and locker deliveries that require fewer licensed drivers. Wage pressure directly lowers profitability, curtailing fleet expansion plans.

EU Mobility Package Wage Parity Raising Line-Haul Costs

The posted-workers rules mandate Western wage scales for Polish drivers operating abroad, removing a key cost advantage on Frankfurt, Paris, and Amsterdam lanes[4]ING Think, “Polish Data Signals a Softer Fourth Quarter but a Brighter Outlook for 2025,” ing.com. Carriers must install tachograph telematics to prove time spent in each jurisdiction, adding compliance overhead. Some operators shift to relay models where a Western-based partner handles the final leg, fragmenting control over service quality. Small firms face existential stress as higher payroll costs coincide with elevated diesel prices. While larger integrators absorb the hit via scale, the regulation arguably accelerates consolidation within the Poland courier, express, and parcel industry. The rule is phased in over two years, keeping cross-border pricing in flux until full adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Destination: International Parcels Capture Momentum

Domestic traffic retained 65.34% of Poland courier, express, and parcel market share in 2025, benefiting from mature urban consumption patterns and widespread locker networks. International shipments, however, are expected to record the quicker 3.18% CAGR through 2031 as SMEs embrace cross-border marketplaces and Poland’s central location enables gateway operations into Eastern Europe. Inbound e-commerce flows from Germany and the Czech Republic rise alongside outbound exports to the United States, Canada, and the United Kingdom, underpinning a balanced volume mix. Operators hedge currency and duty risks through digital customs platforms that cut clearance times to under two hours on priority lanes. Domestic growth now depends on rural penetration, where public funding improves road links and broadband connectivity, potentially unlocking new parcel volumes. International logistics remains sensitive to EU Mobility Package wage rules, yet increased value density permits premium pricing that partially offsets cost.

A growing share of cross-border parcels rides direct rail links through the Łódź–Chengdu corridor, shortening transit by five days relative to ocean transport and offering an attractive alternative amid Red Sea disruptions. Marketplace sellers employ fulfillment centers near border crossings, allowing them to localize inventories for same-day dispatch into Germany. Enhanced trade digitization positions Poland as a distribution hub for Central-Eastern Europe, further tilting growth toward international parcels despite persistent domestic dominance.

By Speed of Delivery: Express Demands Premium Service Levels

Non-express services still command 76.05% in 2025 due to competitive pricing and consumer willingness to wait 48–72 hours when fees are low. Express deliveries, though smaller in share, is expected to book the fastest 3.52% CAGR (2026-2031), propelled by rising expectations for next-day arrival and the growth of high-value verticals such as healthcare. E-commerce giants bundle expedited shipping into membership programs, shifting customer mindsets toward speed as a default feature. The Poland courier, express, and parcel market size for express shipments improves on the back of AI-powered sorting that raises throughput. Non-express networks adopt dynamic cut-off times and off-peak locker drop-offs to emulate some express attributes at lower costs.

Traffic segmentation blurs as InPost lockers provide parcel retrieval within hours, undermining the distinctiveness of legacy express services. However, sectors like pharma and automotive components still rely on guaranteed time windows, offering resilient revenue streams. Express margins widen slightly as shippers accept accessorial fees linked to carbon-neutral delivery options, reflecting broader ESG priorities.

By Model: B2C Parcel Flow Defines Network Design

B2C volume represented 51.84% in 2025, driven by double-digit growth in marketplace transactions and omnichannel retail. The segment’s 3.96% CAGR through 2031 necessitates dense pick-up and drop-off points, real-time tracking, and seamless return logistics. Locker architectures and flexible evening deliveries cater to consumer demand, pushing carriers to redesign routes around retail precincts and residential clusters. B2B remains vital for industrial replenishment, yet grows more slowly as digitized procurement reduces emergency shipment frequency.

C2C traffic edges up via social-commerce platforms that integrate shipping labels at checkout, providing end-to-end visibility once reserved for enterprises. For the Poland courier, express, and parcel industry, the surge in B2C parcels accelerates investment in customer-facing apps, chatbots, and loyalty programs, reinforcing market stickiness while raising service benchmarks across all models.

By Shipment Weight: Lightweight Parcels Dominate Network Economics

Light parcels held 64.21% in 2025 and are estimated to clock a 3.34% CAGR through 2031, as fashion, electronics, accessories, and health supplements dominate online carts. Standardized dimensions flow efficiently through automated sorters without manual intervention, cutting per-piece costs. Medium-weight categories maintain relevance for B2B spares and bulk e-grocery orders, yet growth lags. Heavy shipments gravitate toward specialized forwarders equipped with lift-gate vehicles and white-glove crews, narrowing their share within the Poland courier, express, and parcel market.

The prevalence of lightweight parcels enables pilot rollouts of cargo drones for remote village deliveries, reducing transit times. Parcel density per route rises, supporting electric van adoption despite shorter range limits. AI algorithms leverage uniform parcel data to improve cube utilization, trimming wasted truck space and thereby lowering emissions per kilogram.

By Mode of Transport: Rail and Multimodal Solutions Advance

Road retained a 50.87% share in 2025, underpinning first-mile and last-mile coverage. Rail and other multimodal options, however, outpace with a 3.79% CAGR (2026-2031), fueled by emissions regulations and rising highway tolls. Integrators deploy “rail-air” corridors—rail to central hubs and air for the final leg—to balance cost and time. The Poland courier, express, and parcel market size linked to rail trunking benefits from CEF Transport grants that modernize intermodal yards and cut cargo dwell times.

Electric line-haul trucks see test programs on Warsaw–Wrocław lanes, but charging infrastructure remains nascent. Waterway usage is minimal yet receives exploratory funding for containerized barge services on the Vistula River, a long-term sustainability play. Overall, multimodal flexibility emerges as a hedge against fuel volatility and driver scarcity.

By End User Industry: E-Commerce Retains Prime Position

E-commerce generated 41.65% of parcel demand in 2025 and is expected to grow at a 3.31% CAGR (2026-2031), cementing its lead. Saturation in metropolitan markets shifts carrier focus toward smaller cities where locker roll-outs unlock new segments. Healthcare logistics accelerate on temperature-controlled pharmaceutical deliveries and direct-to-patient services, prompting investments in validated cold-chain packaging. Financial services hold steady as regulatory mailings persist, yet digital signatures slow physical envelope volumes.

Manufacturing parcels stabilize as just-in-time systems mature, yet opportunities arise in spare-parts distribution linked to Poland’s thriving automotive cluster. Renewable-energy component shipping shows early promise as wind-farm installation ramps up in the Baltic region. Collectively, vertical specialization pressures parcel operators to diversify service portfolios beyond generic transport.

Geography Analysis

Poland’s domestic network benefits from an extensive highway grid and central European positioning, enabling overnight coverage for 85% of the population. Warsaw remains the single largest origin-destination pair, while Kraków and Wrocław add critical regional heft. Rural districts, historically underserved, receive targeted KPO grants that finance depot automation and road resurfacing, reducing delivery lead times by one day on average. Driver shortages tighten capacity in top metros, spurring experiments with autonomous mobile robots inside urban micro-hubs.

Internationally, parcel flows to Germany dominate outbound lanes, leveraging open border crossings and harmonized EU customs codes. Meest Post’s direct lanes to North America diversify risk and capture higher yield shipments motivated by Polish diaspora demand. The EU Mobility Package raises costs on West-bound trucking, nudging some traffic to rail intermodal links. Poland’s eastern frontier with Ukraine experiences sporadic spikes in humanitarian goods, showcasing the network’s agility. Overall, geography confers gateway advantages yet subjects operators to divergent regulatory regimes that complicate pricing.

Competitive Landscape

Competition clusters around technology leadership, network density, and regulatory readiness. InPost’s parcel-locker ecosystem delivers a formidable moat by locking in consumer habits and offering drop-point proximity within a 7-minute walk for 60% of urban dwellers. State-owned Poczta Polska leverages universal-service obligations to preserve rural reach, yet modernizes slowly relative to private rivals.

International integrators—DHL, UPS, FedEx—compete on cross-border reliability, embedding Poland into pan-European delivery meshes. Strategic moves underscore the race for scale. DHL inaugurated a 32,000 sqm hub near Poznań and EV charging stations, boosting throughput to 45,000 parcels per hour. GLS joined forces with Orlen to overlay parcel machines onto Orlen’s fuel-station network, extending out-of-home delivery to 15,000 lockers.

Smaller couriers form alliances with locker operators to remain relevant in the Poland courier, express, and parcel market. Rising compliance costs under EU wage parity drive a wave of M&A as under-capitalized firms seek exit options. Consolidation lifts the combined share of top-five carriers, signaling a gradual shift from fragmented to moderately concentrated structure.

Poland Courier, Express, And Parcel (CEP) Industry Leaders

InPost

DPD (Part of Geopost)

Poczta Polska

GLS Poland

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Meest Post expanded long-haul parcel lanes from Poland to the United Kingdom, Canada, and the United States to serve SME exporters.

- July 2024: GLS Poland and ORLEN announced a partnership, adding 15,000 parcel lockers to GLS’s out-of-home network.

- March 2024: DHL Group opened an international logistics center in Robakowo near Poznań, spanning 32,000 sqm with a sorting capacity of 45,000 parcels per hour.

- February 2024: Hermes Fulfilment Group confirmed that it will take over bonprix returns processing in Łódź from Mar 2025, deepening its footprint in Poland.

Poland Courier, Express, And Parcel (CEP) Market Report Scope

The CEP market covers the services offered by the logistics service providers related to courier, express, and parcel delivery.

The report offers a complete background analysis of the courier, express, and parcel (CEP) market, including market overview, market size estimation for key segments, emerging trends by segment, and market dynamics. The report also offers a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across key points in the industry's value chain.

Poland's Courier, Express, and Parcel (CEP) Market is Segmented by Business (B2B and B2C), Destination (Domestic and International), and End User (Services, Wholesale and Retail Trade, Manufacturing, Construction and Utilities, and Primary Industries). The report offers market size and forecasts in value (USD billion) for all the above segments.

By Destination

| Domestic |

| International |

By Speed of Delivery

| Express |

| Non-Express |

By Model

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

By Shipment Weight

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

By Mode Of Transport

| Air |

| Road |

| Others |

By End User Industry

| E-Commerce |

| Healthcare |

| Financial Services (BFSI) |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| By Destination | Domestic |

| International | |

| By Speed of Delivery | Express |

| Non-Express | |

| By Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| By Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| By Mode Of Transport | Air |

| Road | |

| Others | |

| By End User Industry | E-Commerce |

| Healthcare | |

| Financial Services (BFSI) | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others |

Key Questions Answered in the Report

What is the current value of the Poland courier, express, and parcel market?

The market reached a value of USD 4.63 billion in 2026 and is projected to hit USD 5.37 billion by 2031.

How fast is parcel demand growing in Poland?

Parcel volume is forecast to grow at a 2.98% CAGR through 2031, supported by e-commerce and cross-border exports.

Which delivery model holds the largest share in Poland?

Business-to-Consumer shipments lead with 51.84% share in 2025 and are expanding at a 3.96% CAGR.

How significant are parcel lockers in Polish logistics?

Parcel-locker networks now account for a growing share of last-mile deliveries, improving success rates and cutting unit costs.

What segments will grow fastest over the next five years?

International parcels, express deliveries, and healthcare logistics are expected to post above-market CAGRs through 2031.

How is regulation shaping fleet strategy?

EU Fit-for-55 incentives and Low-Emission Zones are accelerating the shift toward electric and multimodal transport options.

Page last updated on: