Plastic Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 72.53 Billion |

| Market Size (2031) | USD 84.67 Billion |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

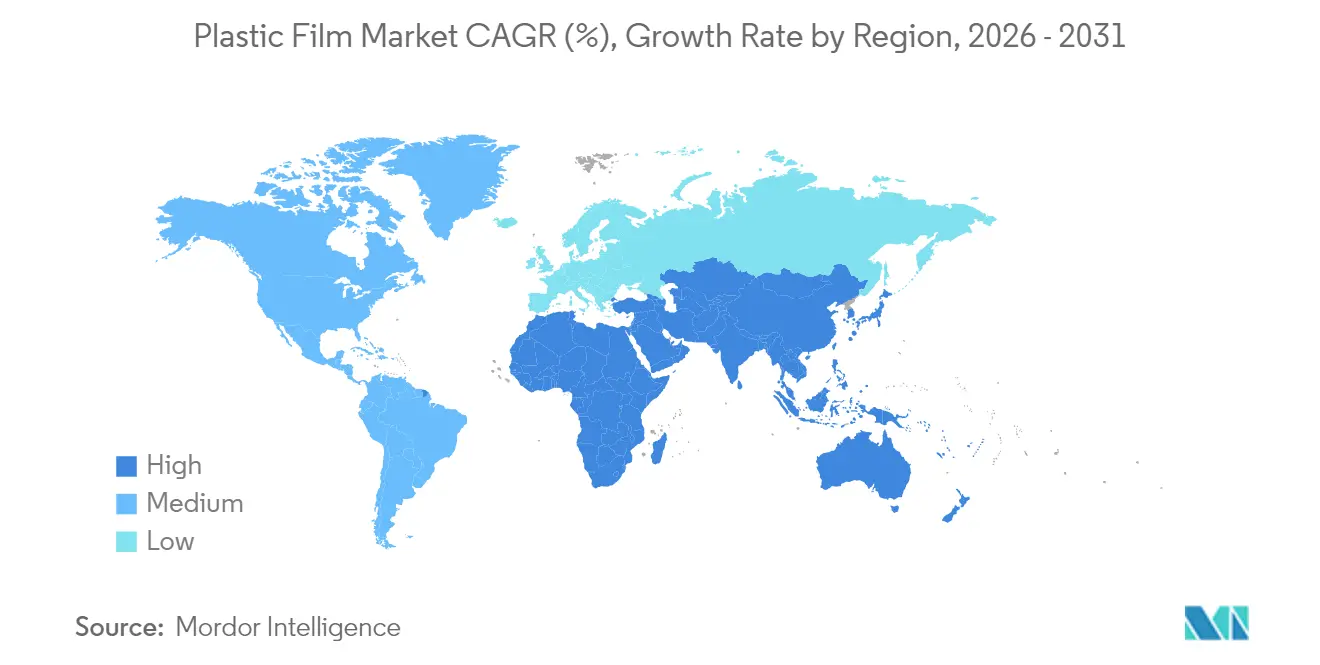

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Film Market Analysis by Mordor Intelligence

The plastic film market size is expected to grow from USD 70.30 billion in 2025 to USD 72.53 billion in 2026 and is forecast to reach USD 84.67 billion by 2031 at 3.18% CAGR over 2026-2031. This performance underscores a maturing landscape where incremental value now arises from specialty, high-barrier films sold into medical, electronics, and e-commerce channels. Heightened regulatory attention to circular-economy goals is accelerating a pivot toward recyclable mono-material structures and certified compostable grades, while persistent raw-material price swings continue to test converter margins. Integrated producers with vertical control over resin and film assets are mitigating volatility and capturing premium spreads through downgauging, barrier-coating, and recycling initiatives.

Key Report Takeaways

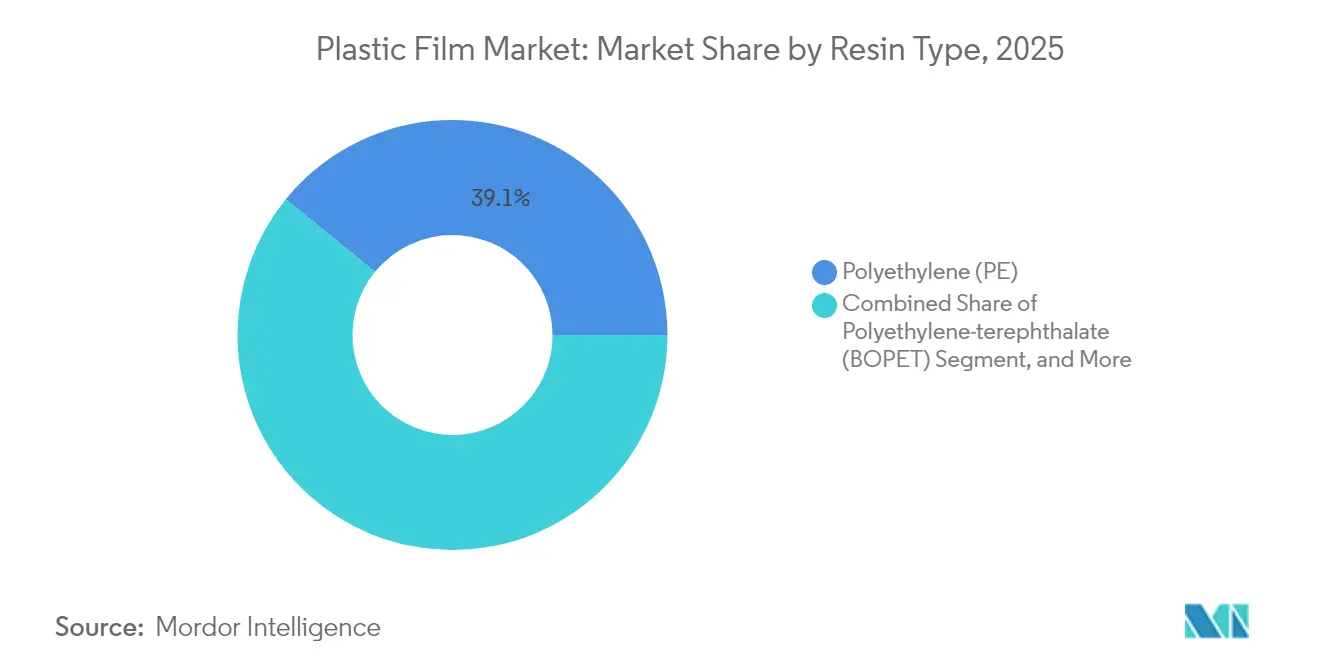

- By resin type, polyethylene retained 39.12% of plastic film market share in 2025, while bioplastics recorded the highest CAGR at 5.87% through 2031.

- By application, pouches accounted for 47.95% of 2025 revenue; wraps and overwraps are forecast to grow at 4.56% CAGR to 2031.

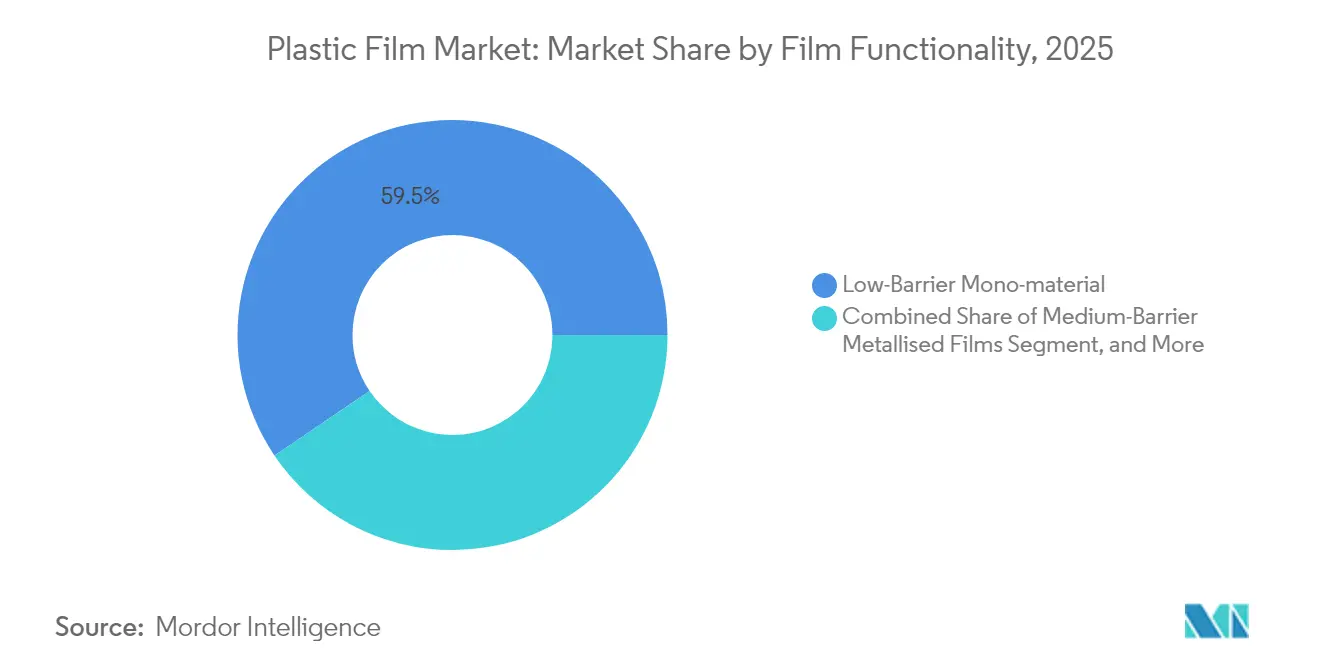

- By film functionality, low-barrier mono-material products led with 59.46% share in 2025; high-barrier multilayer films will expand at 5.86% CAGR.

- By end-use industry, food packaging commanded 31.89% of the plastic film market size in 2025, whereas healthcare and pharmaceuticals are advancing at 4.83% CAGR.

- By Asia-Pacific dominated with 37.98% share in 2025; the Middle East and Africa region is projected to post a 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastic Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward mono-material recyclable film structures | +0.8% | EU, North America, global spillover | Medium term (2-4 years) |

| Growing adoption of biodegradable and compostable films amid regulations | +0.6% | EU, North America, select APAC markets | Long term (≥ 4 years) |

| Rising demand for high-barrier films in medical and electronics packaging | +0.5% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Expansion of agri-film usage in vertical farming and greenhouse automation | +0.3% | APAC core, MEA and Latin America | Medium term (2-4 years) |

| Film downgauging enabled by advanced metallocene catalysts | +0.4% | Global, led by major polymer producers | Short term (≤ 2 years) |

| Surge in regional e-commerce cold-chain requiring specialty films | +0.7% | Asia-Pacific, North America, MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer Shift Toward Mono-Material Recyclable Film Structures

Circular-economy policies are swiftly converting legacy multilayer formats into mono-material films that meet recyclability thresholds without sacrificing performance. European regulations mandating full recyclability by 2030 have already spurred converters such as Uzel Plastik to roll out polyethylene pet-food films that eliminate tie-layer adhesives while preserving oxygen barriers.[3]Uzel Plastik, “Recyclable PE Films for Pet Food,” uzelplastik.com Brand owners are rewarding early adopters with multi-year supply contracts linked to sustainability metrics, yet initial capital outlays for new extrusion and adhesive systems are trimming near-term margins. Pharmaceutical players are also transitioning; Klöckner Pentaplast introduced a mono-material blister film that meets stringent medical compliance while simplifying downstream recycling. This momentum is expected to lift mono-material share from 60% in 2024 toward two-thirds of the plastic film market by 2030.

Growing Adoption of Biodegradable and Compostable Films Amid Regulations

A mosaic of state and national mandates is fueling demand for certified compostable films, particularly in food service and produce packaging. Washington State’s labeling and facility-certification rules set a technical benchmark that global suppliers must now match. Minnesota’s legislation requiring industrial-composting compatibility is influencing private-label specifications for supermarket chains. Suppliers with robust R&D budgets, such as DNP Group, are commercializing multilayer compostable structures capable of 90-day degradation while sustaining gas-barrier properties that protect snack foods. Lack of harmonized global standards remains a hurdle, forcing converters to produce country-specific SKUs and inflating compliance costs.

Rising Demand for High-Barrier Films in Medical and Electronics Packaging

Device sterilization protocols and low-moisture requirements for flexible displays are elevating the bar for barrier films. SÜDPACK’s co-extruded medical laminates now guarantee sub-1 cm³/m²/day oxygen transmission rates, fetching premium price points that cushion raw-material volatility. Concurrently, ProAmpac’s investment in USD 50 million metallization assets targets electronics customers seeking water-vapor transmission rates below 0.1 g/m²/day. Participation from upstream chemical firms such as Honeywell, which launched a fluoropolymer-based barrier layer for OLED devices, underscores vertical integration’s role in capturing these high-margin niches.

Expansion of Agri-Film Usage in Vertical Farming and Greenhouse Automation

Urban agriculture and controlled-environment practices are enlarging the addressable pool for agri-films that block near-infrared radiation and endure automated handling. Hyma Plastic’s NIR-blocking greenhouse covers sell at triple the price of commodity mulch films but deliver energy savings by lowering inside temperatures 2-3 °C. Integrated sensor networks from industrial-automation players like ifm require films with consistent optical properties, fusing packaging-grade polymers with precision-ag-equipment standards. As Asian megacities embrace vertical farming, the agri-film subset is set to outpace overall plastic film market growth through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in polyolefin and PET feedstock prices | -0.9% | Global, import-dependent regions | Short term (≤ 2 years) |

| Stringent single-use plastic bans in emerging economies | -0.6% | Africa, Latin America, Asia | Medium term (2-4 years) |

| Supply tightness of medical-grade PVC resin | -0.4% | Developed healthcare markets | Short term (≤ 2 years) |

| Capital intensity of synchronous biax orientation lines | -0.3% | Global, major film producers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polyolefin and PET Feedstock Prices

Quarterly swings of 15-20% in PET and LDPE spot prices have compressed converter spreads, particularly among non-integrated players. ChemOrbis data show PET values oscillating between USD 1,200 and USD 1,450 per ton in 2024, making long-term contracts risky for suppliers dependent on spot resin. Overcapacity in Asia’s BOPET segment has driven realizations to historical lows; Firsta Group recorded instances where margins dipped below INR 15/kg, triggering temporary plant shutdowns. Inventory management is further complicated by lengthy transit times, causing small converters to absorb losses during price retracements.

Stringent Single-Use Plastic Bans in Emerging Economies

Accelerated policy rollouts in Africa and Latin America are shrinking demand for conventional carry bags and sachets. Nigeria’s plan to outlaw single-use films by 2026 jeopardizes roughly 200,000 t of annual flexible demand. Similar moves in Tanzania and Kenya have forced local converters to either invest swiftly in biodegradable lines or cease operations. Jamaica’s 2025 progress report validating waste-reduction success has emboldened neighboring Caribbean states to consider analogous bans, expanding the regulatory ripple effect.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Bioplastics Drive Innovation Despite PE Dominance

Polyethylene retained 39.12% of 2025 volume, underpinned by metallocene catalyst technology that slashed film gauge by up to 20% without surrendering stiffness or clarity. This dominance supplied predictable cash flows even when oil-linked feedstock costs spiked. In contrast, bioplastics, though representing a modest baseline, are set to post a 5.87% CAGR as brand owners deploy compostable packaging pilots to meet ESG targets. Rising supply of second-generation feedstock, including sugarcane bagasse and algae oils, has clipped the cost premium to conventional resins. Still, high-barrier medical and electronics uses remain out of reach for most bioplastics due to hydrolytic-stability constraints.

Converters courting the bioplastic subsector are negotiating multi-year off-take pacts with resin start-ups to hedge price-volatility risk. Regional clustering around EU and North-American compost facilities also influences plant-location decisions. Polypropylene continues expanding within retort pouch applications, benefiting from heat-resistance and grease-barrier traits, while BOPET producers seek anti-dumping shelters in markets like the United States to escape Asian oversupply. Specialty polymers such as cyclic olefin copolymers fill niche roles in medical diagnostics, emphasizing the value of performance-led differentiation within the plastic film market.

By Application: E-commerce Elevates Wraps as Pouch Leadership Holds

The pouch format delivered 47.95% of 2025 sales thanks to portion-control convenience and seal-integrity that reduces food waste. Automated form-fill-seal lines, common in snack and pet-food factories, favor its geometry, while digital printing allows hyper-customized graphics for short campaigns. However, wraps and overwraps are forecast to grow at 4.56% CAGR as omnichannel grocery and meal-kit services demand puncture-resistant films compatible with high-speed bagging robots. Cold-chain compliance amplifies the need for moisture barriers that stay ductile at sub-zero temperatures, an area where BOPP-based laminates have recently gained traction.

Converters are integrating data-matrix codes into secondary wraps to track last-mile delivery conditions, creating analytics revenue streams beyond the material sale itself. Linerless label films and shrink-bundling for multipacks remain important, though growth is slower due to maturation in carbonated-drink markets. Across applications, film formats enabling resource efficiency such as perforated produce wraps that modulate respiration align with retailer sustainability pledges and thus secure shelf space despite premium pricing.

By Film Functionality: Mono-Material Shift Challenges Multilayer Dominance

Low-barrier mono-material films accounted for 59.46% of 2025 shipments as FMCG brands responded to consumer pressure for drop-in recyclable alternatives. Targeted seal-layer engineering and reactive-extrusion tie-layers have narrowed the performance gap with complex laminates, making the cost of switching viable for mid-shelf-life goods. High-barrier multilayer films are still on track for a 5.86% CAGR through 2031, propelled by pharmaceuticals and flexible displays where oxygen or moisture ingress can trigger recalls.

Early commercialization of reactive-extrusion nano-clay masterbatches promises to lift oxygen-barrier performance in mono-material PE films by 40-60%, though scale-up has been slow due to compounding-line abrasion. Metallized films stay relevant for coffee and infant-formula packaging where brand heritage demands foil-like optics. Meanwhile, antimicrobial additives and controlled-release ethylene absorbers create white-space opportunities that command unit prices several multiples above commodity grades. Bostik’s collaboration with Brückner on solvent-free lidding adhesives illustrates how machine suppliers influence the transition to single-polymer options by synchronizing screw profiles, die designs, and adhesive rheology

By End-Use Industry: Healthcare Growth Outpaces Food Segment Leadership

Food packaging generated 31.89% of the plastic film market size in 2025, propelled by single-serve snacks, frozen convenience meals, and pet foods that benefit from downgauged high-clarity PE/PP blends. Retailers are also piloting pouch-to-pouch collection schemes that elevate consumer loyalty. Healthcare and pharmaceuticals, while smaller, are set to expand 4.83% annually on aging-population dynamics and surgical-kit standardization. Sterile-barrier film makers enjoy margins two-to-three times higher than food-grade counterparts due to clean-room processing and ISO-certification prerequisites. Investments such as Caesar Pack’s USD 48.4 million recycling facility in Egypt underscore the vertical-integration trend linking reclaimed PET flakes to medical-grade films.

Personal-care segments are transitioning to monomaterial pump sleeves and refill-pouch formats, while household-care brands trial solvent-resistant PE/PA blends to replace rigid bottles. Industrial film users remain sensitive to macro-economic cycles; however, electronics assembly lines now specify ultra-low ion-contamination films, an attribute that filters through to specialized clean-room grades.

Geography Analysis

Asia-Pacific secured a 37.98% share of the plastic film market in 2025 by pairing scale economies with burgeoning domestic consumption. China maintains dominance in BOPET and BOPP, though capacity additions have outstripped local demand by roughly 260,000 t a year, pressing margins and catalyzing M&A among mid-tier converters. India leverages metallocene-catalyst technology to serve upgraded pouch formats and is onboarding new BOPP lines at a brisk pace. Japan’s mature yet highly technical ecosystem sustains innovation in optical and battery-separator films.

North America’s demand is steadier, buoyed by on-shoring trends and sustainability mandates that push recyclable PE wraps for e-commerce. Polyplex’s USD 100 million PET-film expansion in Alabama illustrates the pull of regional supply chains aligned with trade-policy certainty. Converters increasingly co-locate with logistics hubs to shrink lead times, a factor critical for meal-kit and pharmaceutical shipments.

Europe continues to act as a policy bellwether; extended-producer-responsibility (EPR) fees penalize non-recyclable formats, driving R&D dollars into mono-material upgrades. Mechanical-recycling capacity additions are ramping, and venture funds are backing chemical-recycling pilots aimed at rigid-flexible feedstock mixes.

The Middle East and Africa is poised for a 7.86% CAGR through 2031 on the back of import-substitution plans and regulatory incentives. Egypt’s joint venture to build a recycled-polyester fiber line worth USD 54.8 million signals rising local appetite for circular solutions. Gulf Cooperation Council members leverage hydrocarbon integration to supply competitively priced PE, spawning downstream film clusters that aim to capture regional food-security programs. Sub-Saharan Africa’s demand growth is driven by population expansion and fast-moving consumer-goods uptake, though infrastructure gaps in waste management may moderate adoption of premium sustainable films.

South America delivers mid-single-digit growth as branded food and personal-care multinationals widen rural retail penetration, creating incremental packaging needs. Currency volatility and regulatory divergence between Mercosur nations complicate capacity planning, yet rising household incomes sustain baseline consumption.

Competitive Landscape

The global scene remains moderately fragmented. Larger groups capitalize on backward-linked resin assets and multimodal logistics to tame feedstock swings. Revolution Sustainable Solutions’ acquisition of Island Plastics expands its post-consumer-recycled (PCR) film stream, guaranteeing supply of PCR-rich feedstock for brand owner mandates.[1]Revolution Sustainable Solutions, “Island Plastics Acquisition,” revolutionsustainablesolutions.com Coveris’ twin acquisitions S and K Label and Hadepol Flexo illustrate roll-up strategies aimed at consolidating Eastern-European converting capacity while cross-selling bakery and confectionery films.[2]Plasticker, “Coveris Acquires Hadepol Flexo,” plasticker.de

Capacity investment continues even amid regional oversupply; Polyplex’s Indian and U.S. expansions reflect confidence in premium BOPET niches for electronics and pharmaceuticals. Berry Global’s tie-up with VOID Technologies targets mono-material pet-food structures offering barrier performance once achievable only via EVOH or aluminum deposition, validating technology partnerships as a path to leapfrog rivals. Equipment suppliers such as Brückner Maschinenbau are embedding inline-recycling modules in orientation lines, enabling off-spec film to be reincorporated instantly, slashing scrap rates from 8% to under 3% in pilot installations. Patents concentrate around solvent-free adhesives, nano-coatings, and enzymatic degradation accelerators, signaling R&D focus on sustainability enablers.

A cadre of disruptors is emerging in chemical recycling, promising to depolymerize mixed-color post-consumer film back to virgin-grade feedstock that circumvents mechanical-recycling limitations. Should scale and economics mature, resin suppliers may find their feedstock oligopoly challenged, adding a new competitive dimension beyond conventional extrusion and orientation prowess.

Plastic Film Industry Leaders

Amcor plc

Taghleef Industries LLC

Toray Industries, Inc.

Jindal Poly Films Limited

Oben Holding Group S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Coveris announced the acquisition of Poland’s Hadepol Flexo, extending bakery-film reach across Central and Eastern Europe.

- January 2025: Polyplex Corporation invested INR 558 crore (USD 66.4 million) to add a specialty BOPET line targeting high-barrier electronics applications.

- December 2024: Berry Global partnered with VOID Technologies to launch recyclable PE pet-food films that retain premium oxygen-barrier properties.

- December 2024: Revolution Sustainable Solutions purchased Island Plastics, enriching its PCR-film capacity and collection network.

Global Plastic Film Market Report Scope

Plastic film is a flexible packaging solution which is a continuous form of thin plastic material usually wound on a core or cut into sheets. The plastic film is made from different plastic resins based on the requirements and end-user industries.

The plastic film market is segmented by PP films, BOPET films, PE films, PVC films, and other plastic film types, end-user Industries, and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyethylene-terephthalate (BOPET) |

| Polystyrene (OPS) |

| Bioplastics |

| Other Material Types |

| Wraps and Overwraps |

| Bags and Linings |

| Pouches |

| Other Applications |

| Low-Barrier Mono-material Films |

| Medium-Barrier Metallised Films |

| High-Barrier Multilayer Films |

| Specialty Active and Antimicrobial Films |

| Food | Candy and Confectionery |

| Frozen Foods | |

| Fresh Produce | |

| Dairy Products | |

| Meat, Poultry and Seafood | |

| Pet Food | |

| Other Food Products | |

| Beverages | |

| Healthcare and Pharmaceutical | |

| Personal Care and Home Care | |

| Industrial Packaging | |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Resin Type | Polypropylene (PP) | ||

| Polyethylene (PE) | |||

| Polyethylene-terephthalate (BOPET) | |||

| Polystyrene (OPS) | |||

| Bioplastics | |||

| Other Material Types | |||

| By Application | Wraps and Overwraps | ||

| Bags and Linings | |||

| Pouches | |||

| Other Applications | |||

| By Film Functionality | Low-Barrier Mono-material Films | ||

| Medium-Barrier Metallised Films | |||

| High-Barrier Multilayer Films | |||

| Specialty Active and Antimicrobial Films | |||

| By End-use Industry | Food | Candy and Confectionery | |

| Frozen Foods | |||

| Fresh Produce | |||

| Dairy Products | |||

| Meat, Poultry and Seafood | |||

| Pet Food | |||

| Other Food Products | |||

| Beverages | |||

| Healthcare and Pharmaceutical | |||

| Personal Care and Home Care | |||

| Industrial Packaging | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the plastic film market in 2031?

It is forecast to reach USD 84.67 billion by 2031 based on a 3.18% CAGR.

Which region is expected to grow the fastest through 2031?

The Middle East and Africa region, supported by infrastructure expansion, is projected to grow at a 7.86% CAGR.

Which resin type holds the largest share today?

Polyethylene leads with 39.12% of market revenue in 2025.

Why are mono-material films gaining popularity?

They meet recyclability mandates while narrowing performance gaps with multilayer structures, aligning with brand-owner sustainability goals.

Which application segment is expanding fastest?

Wraps and overwraps, driven by e-commerce logistics, are advancing at 4.56% CAGR.

What factor most pressures converter margins?

Volatility in polyolefin and PET feedstock prices erodes spreads for non-integrated players.

Page last updated on: