Europe Pharmaceutical Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

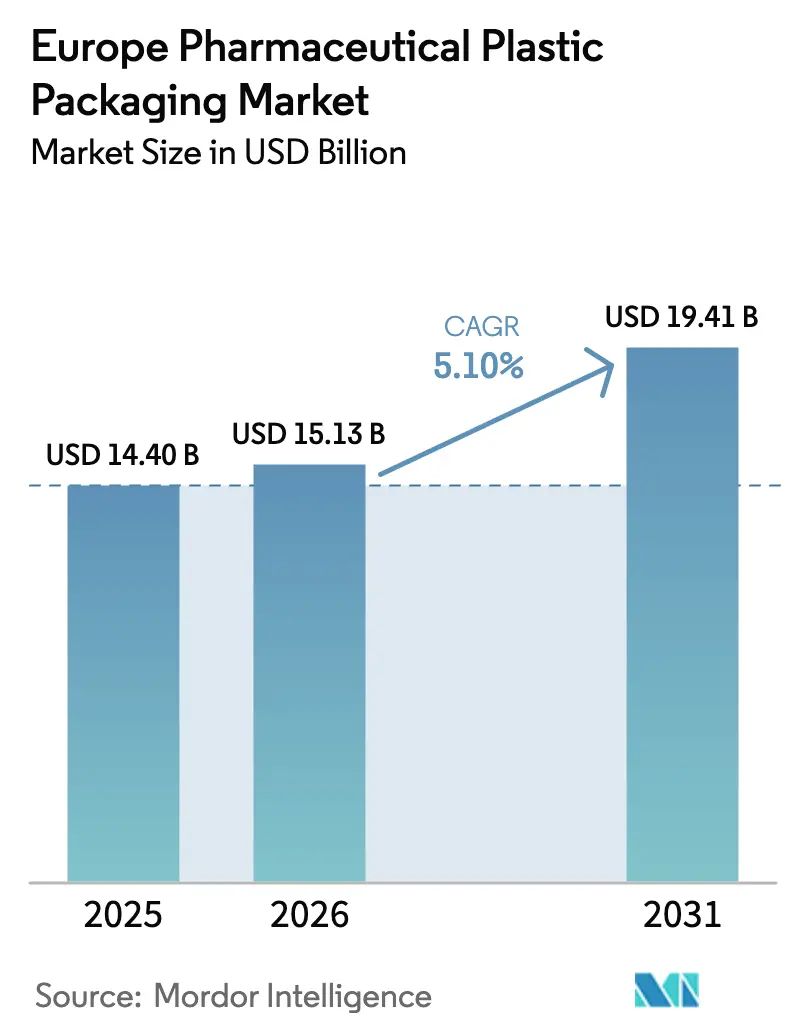

| Base Year Market Size (2025) | USD 14.40 Billion |

| Market Size (2026) | USD 15.13 Billion |

| Market Size (2031) | USD 19.41 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

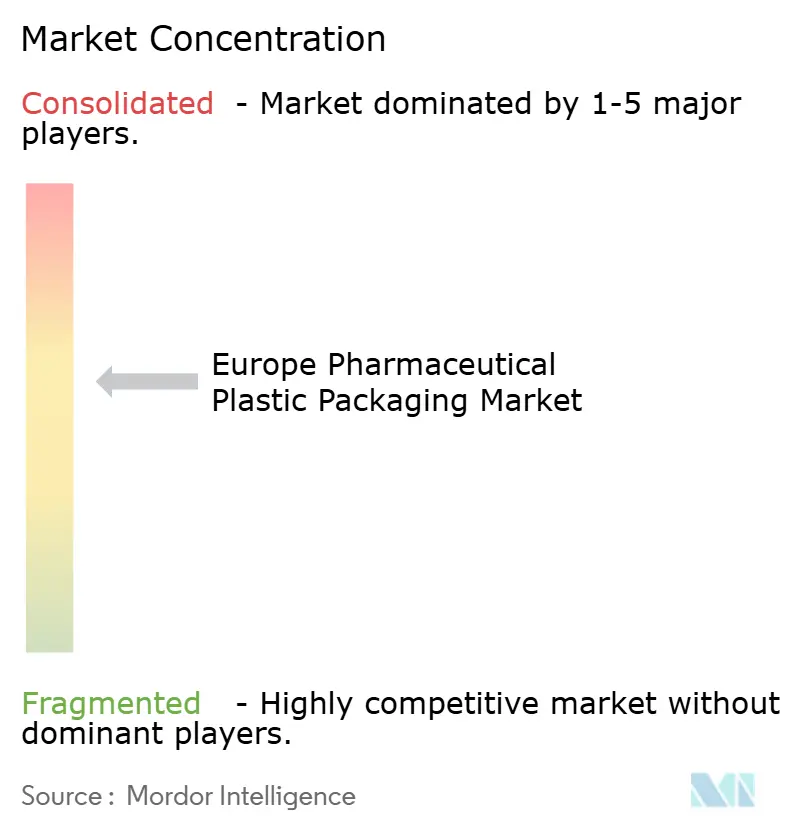

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pharmaceutical Plastic Packaging Market Analysis by Mordor Intelligence

The pharmaceutical plastic packaging market size is projected to expand from USD 14.39 billion in 2025 and USD 15.13 billion in 2026 to USD 19.41 billion by 2031, registering a CAGR of 5.11% between 2026 to 2031. Robust biologics pipelines, e-commerce drug distribution, and the European Union’s circular-economy mandates are simultaneously widening demand for performance plastics and driving converters toward recycled-content solutions. Vertically integrated suppliers that co-locate resin compounding, injection molding, and ISO 15378-certified assembly continue to consolidate volume as mid-tier firms struggle to fund both sustainability retrofits and expanded clean-room capacity. At the same time, regulatory scrutiny of extractables, leachables, and per- and polyfluoroalkyl substances is accelerating the shift toward ultra-high-purity cyclic-olefin polymers in prefilled syringes and polymer vials. These crosscurrents are reshaping capital allocation across the pharmaceutical plastic packaging market, rewarding scale, technical differentiation, and cradle-to-cradle design expertise.

Key Report Takeaways

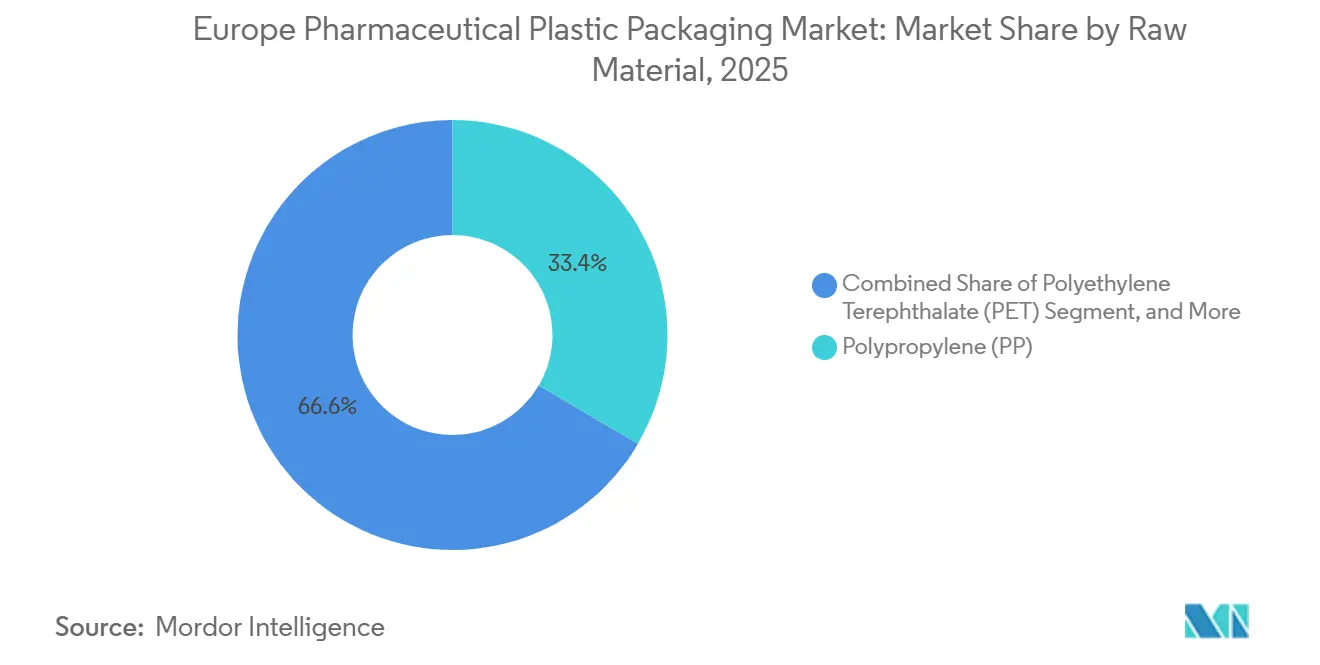

- By raw material, polypropylene led with 33.44% of the pharmaceutical plastic packaging market share in 2025, while bio-polymers are forecast to expand at a 6.08% CAGR through 2031.

- By product type, solid containers accounted for 38.76% of 2025 revenue, yet prefilled syringes are projected to post a 7.98% CAGR through 2031, the fastest growth rate in the pharmaceutical plastic packaging market.

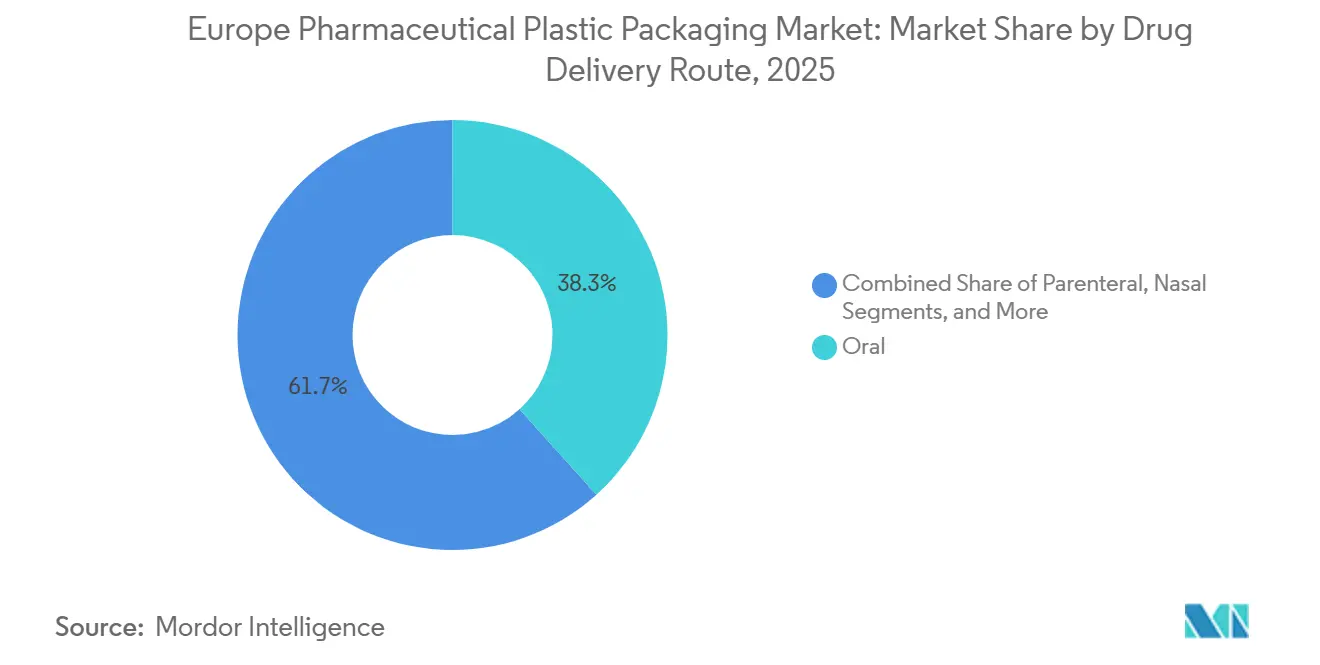

- By drug-delivery route, oral packaging accounted for 38.32% of 2025 demand, whereas parenteral formats are advancing at a 6.03% CAGR through 2031, driven by biologics approvals.

- By country, Germany accounted for the largest share of 2025 revenue at 20.93%, while Spain is poised to record the highest country-level growth at 6.53% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Pharmaceutical Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Child-Resistant and Senior-Friendly Packs | +0.8% | Germany, France, United Kingdom, Sweden | Medium term (2-4 years) |

| Surge in Biologics Needing Advanced Parenteral Plastics | +1.2% | Germany, Belgium, France, United Kingdom | Long term (≥ 4 years) |

| EU Circular-Economy Rules Accelerating Recyclable Plastics | +1.0% | All Europe, strongest in Germany, France, Sweden | Long term (≥ 4 years) |

| E-Commerce Pharma Boosting Protective Secondary Packaging | +0.7% | United Kingdom, Germany, Spain, Italy | Short term (≤ 2 years) |

| Home-Injection Therapies Driving Small PP Prefilled Syringes | +0.9% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Robotics-Ready RFID Blister Packs for Hospital Automation | +0.5% | Germany, Belgium, Sweden, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Child-Resistant and Senior-Friendly Packs

Germany’s 2025 mandate requiring child-resistant packaging for prescription opioids ignited a retrofit wave across central-European filling lines, lengthening development cycles by up to 12 weeks. An aging European population exceeding 130 million individuals over 65 is simultaneously pressuring designers to lower opening torque and enhance tactile cues.[1]Eurostat, “Demographic Projections for Europe 2030,” ec.europa.eu Dual-certified closures now command 15%-20% price premiums that converters typically recoup within 18 months of launch. Specialty suppliers such as AptarGroup and Weener Plastics, owners of one-handed opening patents, have captured early share as pharmaceutical plastic packaging market customers migrate to ISO 8317-compliant systems. National authorities in France and Sweden are following Germany’s lead, expanding addressable volume for certified closures across Western Europe.

Surge in Biologics Needing Advanced Parenteral Plastics

European Medicines Agency approvals for biologics climbed to 47 new entities in 2025, up 24% in two years, with large-molecule drugs now comprising 62% of the centralized-procedure pipeline. These sensitive formulations favor cyclic-olefin polymer and cyclic-olefin copolymer containers that exhibit vapor-transmission rates below 0.1 g m⁻² day⁻¹. West Pharmaceutical Services’ Daikyo Crystal Zenith syringe captured 28% of regional prefilled-syringe volume for high-concentration biologics after demonstrating silicon migration under 5 ppb. Contract manufacturers in Belgium and Germany have installed polymer-vial handling robots, reducing manual inspection and shortening time-to-market by up to six weeks. This biologics wave is expected to underpin the long-term upward trajectory of the pharmaceutical plastic packaging market.

EU Circular-Economy Rules Accelerating Recyclable Plastics

Regulation 2025/40 obliges 30% recycled content in pharmaceutical packaging by 2030 and lifts collection targets to 65% by 2028. Even though direct-contact primary packs are temporarily exempt, rising eco-taxes such as Germany’s EUR 0.42 kg levy (USD 0.47 kg) are nudging brand owners toward mono-material high-density polyethylene bottles, reclaiming fee reductions. Amcor’s AmLite Ultra bottle, containing 60% post-consumer recycled high-density polyethylene, cleared ISO 15378 validation in January 2026, signaling that regulatory pull is now matched by supply-side readiness. Sweden’s deposit-return pilots further expand post-consumer feedstock availability, lowering recycled-resin cost differentials that historically discouraged adoption.

E-Commerce Pharma Boosting Protective Secondary Packaging

Online drug sales reached EUR 38 billion (USD 43 billion) in 2025, expanding 19% year-over-year and intensifying last-mile handling risks. The United Kingdom’s Good Distribution Practice update now requires temperature-excursion indicators on all direct-to-patient biologic shipments, fueling demand for polyethylene foam liners that hold 2 °C-8 °C for 48 hours. Automated lines in Spanish fulfillment centers integrate RFID tagging and void-fill dispensing, slicing labor costs by up to 40%. Berry Global’s SecureShip pouch, launched February 2025, combines peelable PET windows with moisture-barrier laminates, resonating with mail-order pharmacies processing more than 10,000 daily parcels. These developments reinforce the short-term upside for protective formats within the pharmaceutical plastic packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile PP and PET Resin Prices | -0.6% | All Europe, acute in Italy, Spain | Short term (≤ 2 years) |

| Stricter Extractables and Leachables Limits | -0.4% | Germany, Belgium, France, United Kingdom | Medium term (2-4 years) |

| Glass and Aluminum Substitution in Injectables | -0.3% | Germany, France, Italy | Long term (≥ 4 years) |

| Short Supply of Medical-Grade Recycled Resin | -0.5% | Germany, France, Sweden, Belgium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile PP and PET Resin Prices

Spot polypropylene and polyethylene terephthalate prices fluctuated between EUR 1,050 and EUR 1,420 per ton in 2025, reflecting cracker outages and tariff shifts. Southern European converters, reliant on imports from Northern Europe, absorbed Q2 2025 spikes of 18% when BASF’s Ludwigshafen and TotalEnergies’ Antwerp facilities experienced unplanned shutdowns. Forty-two percent of pharmaceutical packaging suppliers have since moved to quarterly price-index clauses, but smaller firms still lack hedging capacity, exposing margins to 200-300 bp erosion during peaks.[2]European Plastics Converters, “Quarterly Price Adjustment Mechanisms Survey 2025,” plasticsconverters.eu Persistent volatility adds near-term cost pressure across the pharmaceutical plastic packaging market.

Stricter Extractables and Leachables Limits

The European Medicines Agency now aligns with United States Pharmacopeia chapters 661, 1663, and 1664, demanding detection thresholds below 1 µg day⁻¹ for parenteral applications.[3]European Medicines Agency, “Centralized Procedure and Biologics Approvals,” ema.europa.eu Borealis Bormed grades, guaranteeing extractables under 50 ppb, carry 25%-35% premiums. Validation programs have stretched to 18 months as sponsors run accelerated aging at 40 °C and 75% relative humidity, adding EUR 150,000-300,000 (USD 170,000-340,000) per container system. Eleven German prefilled-syringe dossiers were rejected in 2025 for insufficient data, underlining compliance barriers facing new entrants and tempering growth in the pharmaceutical plastic packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Bio-Polymers Extend Momentum Amid Circular Mandates

Polypropylene retained the largest slice of 2025 demand at 33.44%, anchoring child-resistant caps, solid containers, and prefilled-syringe barrels. Polyethylene terephthalate followed at roughly 22%, prized for oxygen-barrier clarity in liquid bottles and blister backing. Yet the “Others” bucket, where cyclic-olefin polymers and bio-polymers reside, already contributes up to 17% of revenue and is expanding fastest. The pharmaceutical plastic packaging market size for cyclic-olefin copolymer vials is forecast to expand well above the overall growth trajectory as biologics manufacturers prize ultra-low extractables. Bio-polymer adoption is presently confined to secondary packs, but Alpla’s 2025 polylactic-acid cough-syrup bottle illustrated how renewable resins can meet 18-month shelf-life targets without sacrificing drop-impact performance.

Converters face a dual challenge of validating post-consumer recycled polyethylene terephthalate that clears ISO 15378 sterility thresholds and sourcing medical-grade recycled high-density polyethylene, volumes of which remain scarce at fewer than five certified European compounders. High-density polyethylene is nonetheless gaining share in child-resistant applications where stiffness reduces torque variability. Polyvinyl-chloride-free laminates are displacing legacy blister films in Scandinavia as hospital systems ban dioxin-emitting materials. Overall, raw-material diversification is set to intensify, reinforcing competitive moats for suppliers that control resin purification and polymer science expertise within the broader pharmaceutical plastic packaging market.

By Product Type: Prefilled Syringes Leapfrog as Home-Care Grows

Solid containers withheld 38.76% revenue in 2025, yet prefilled syringes are charting the steepest climb with a 7.98% CAGR to 2031. Cartridge-based pens and polymer vials also ride the biologics wave, together lifting the parenteral cluster’s share of the pharmaceutical plastic packaging market size. Liquid-dropper bottles and nasal-spray packs maintain relevance in pediatrics and allergy care, but flexible pouches are absorbing over-the-counter analgesic volume because a laminated polyethylene structure shaves 40%-50% of pack weight. West’s silicon-free polymer syringe platform, now specified in 18 European Medicines Agency-approved molecules, evidences how technical innovation can convert premium unit economics into market penetration.

Blister packs are evolving into data carriers as near-field-communication tags enable hospital automation pilots in Belgium and Sweden, although cost premiums keep penetration below 5% of blister volume. Meanwhile, AptarGroup’s SimpliSqueeze closure, certified in September 2025, illustrates that even mature solid-dose formats can gain share through ergonomic upgrades. These shifts collectively advance the pharmaceutical plastic packaging market toward higher-value, device-integrated formats.

By Drug Delivery Route: Parenteral Platforms Rise on Biologic Self-Injection

Oral formats still dominate at 38.32%, but parenteral packaging is expanding 6.03% annually as hospital-based intravenous therapies migrate to home-care subcutaneous regimens. Novo Nordisk’s switch to FlexTouch pens lifted European self-injection volume by 22% between 2024 and 2025. Nasal delivery holds about 8% share, fueled by migraine and allergy treatments, while pulmonary formats stand near 6% on persistent asthma prevalence. Transdermal patches remain a niche below 3% because limited molecules cross the skin barrier efficiently.

The pharmaceutical plastic packaging market share for parenteral devices will keep widening as regulators promote patient-centric care and biosimilar uptake intensifies. Serialization rules under the Falsified Medicines Directive continue to pressure oral packaging lines to integrate vision inspection and two-dimensional barcoding, cementing investments even in slower-growing segments.

Geography Analysis

Germany contributed 20.93% of 2025 revenue, underpinned by a EUR 53 billion (USD 60 billion) pharmaceutical production base and 40-plus ISO 15378 plants clustered in Baden-Württemberg, Bavaria, and North Rhine-Westphalia. Growth prospects track just below the regional mean at 5.0% as mature oral-solid portfolios cap domestic volume, though polymer vials and prefilled syringes are expanding 7%-8%. Spain posts the fastest trajectory at 6.53% through 2031 as Lonza, Recipharm, and Faes Farma build secondary-packaging lines near Barcelona and Madrid to serve Iberian and North African exports.

France, the United Kingdom, and Italy together roughly 36% of market value display divergent dynamics. Paris-Lyon consolidation is narrowing France’s vendor lists, while post-Brexit trade friction nudges some United Kingdom filling operations into EU jurisdictions, even as the country emerges as a cold-chain packaging hub. Italy counters higher labor costs with automation, installing robotic inspection cells that drive defect rates below 50 ppm at Bormioli Pharma’s Parma plant.

Belgium and Sweden, small in absolute terms, punch above their weight in innovation, piloting RFID-enabled blister packs and bio-polymer bottles. The rest-of-Europe cohort Poland, Netherlands, Switzerland, Austria, Nordics matches the regional growth average. Poland’s cost base 40%-50% below Germany’s draws rigid-container production, while Switzerland’s biologics cluster sustains premium polymer vial demand. Dutch logistics corridors around Schiphol and Rotterdam boost secondary-pack procurement that embeds real-time temperature monitoring, illustrating how infrastructure advantages convert into packaging pull within the pharmaceutical plastic packaging market.

Competitive Landscape

The top five suppliers Gerresheimer, Amcor, Berry Global, West Pharmaceutical Services, and AptarGroup command roughly 40% of 2025 revenue, confirming moderate concentration. Integrated players combine glass, plastic, and closure expertise on single campuses to streamline validation. Gerresheimer’s Wackersdorf and Horsovsky Tyn complexes illustrate the end-to-end model that drug sponsors prefer for cyclic-olefin polymer and glass vials alike. Berry Global and Amcor parlay flexible-pack know-how into child-resistant pouches and sachets, stealing share from rigid polypropylene bottles in over-the-counter categories.

Technical specialists such as Stevanato Group and Bormioli Pharma carve niches in cyclic-olefin copolymer processing, defending price premiums with <10 ppb extractables. White-space plays cluster around renewable polymers and smart packaging. Alpla’s polylactic-acid bottles demonstrated commercial readiness for renewable resins, while RFID blister pilots target hospital automation despite per-unit cost premiums.

Patent races focus on leachables mitigation. West holds 14 European patents on fluoropolymer-coated seals, whereas AptarGroup owns nine on silicone-free nasal-valve designs.[4]European Patent Office, “Extractables-Mitigation Technology Patents,” epo.org Smaller disruptors like Origin Pharma Packaging and Comar leverage digital-twin modeling to slash prototyping cycles to four weeks, positioning themselves as agile partners for clinical trial supply in the pharmaceutical plastic packaging market.

Europe Pharmaceutical Plastic Packaging Industry Leaders

Gerresheimer AG

Amcor PLC

AptarGroup Inc.

Origin Pharma Packaging

Pretium Packaging

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Gerresheimer AG completed a EUR 60 million (USD 68 million) expansion at Wackersdorf, Germany, adding two injection-molding lines for cyclic-olefin polymer vials, boosting annual capacity to 120 million units.

- January 2026: Amcor PLC rolled out AmLite Ultra bottles with 60% post-consumer recycled high-density polyethylene at its Ghent facility, targeting 50 million units in 2026.

- December 2025: Stevanato Group finalized a EUR 45 million (USD 51 million) capacity expansion at Pioltello, Italy, lifting EZ-fill polymer-vial output by 40%.

- November 2025: Berry Global opened a 15,000 m² plant in Zaragoza, Spain, featuring six blow-molding lines for high-density polyethylene bottles and child-resistant closures.

Europe Pharmaceutical Plastic Packaging Market Report Scope

The Europe Pharmaceutical Plastic Packaging Market is witnessing significant growth due to the increasing demand for lightweight, durable, and cost-effective packaging solutions in the pharmaceutical industry. Factors such as the rising prevalence of chronic diseases, advancements in drug delivery systems, and stringent regulatory requirements for safe and secure packaging are driving the market's expansion.

The Europe Pharmaceutical Plastic Packaging Market Report is Segmented by Raw Material (Polypropylene, Polyethylene Terephthalate, Low-Density Polyethylene, High-Density Polyethylene, Others), Product Type (Solid Containers, Liquid and Dropper Bottles, Nasal Spray Bottles, Oral-Care Packs, Pouches/Sachets, Vials and Ampoules, Cartridges, Prefilled Syringes, Caps and Closures, Others), Drug Delivery Route (Oral, Parenteral, Nasal, Pulmonary, Transdermal), and Geography (United Kingdom, Germany, France, Spain, Italy, Belgium, Sweden, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Low-Density Polyethylene (LDPE) |

| High-Density Polyethylene (HDPE) |

| Others, Raw Material (COP, COC, PVC-Free Blends, Bio-Polymers) |

| Solid Containers |

| Liquid and Dropper Bottles |

| Nasal Spray Bottles |

| Oral-Care Packs |

| Pouches / Sachets |

| Vials and Ampoules (Polymer) |

| Cartridges |

| Prefilled Syringes |

| Caps and Closures |

| Others, Product Type (Unit-Dose Strips, Inhaler Canisters) |

| Oral |

| Parenteral |

| Nasal |

| Pulmonary |

| Transdermal |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Belgium |

| Sweden |

| Rest of Europe |

| By Raw Material | Polypropylene (PP) |

| Polyethylene Terephthalate (PET) | |

| Low-Density Polyethylene (LDPE) | |

| High-Density Polyethylene (HDPE) | |

| Others, Raw Material (COP, COC, PVC-Free Blends, Bio-Polymers) | |

| By Product Type | Solid Containers |

| Liquid and Dropper Bottles | |

| Nasal Spray Bottles | |

| Oral-Care Packs | |

| Pouches / Sachets | |

| Vials and Ampoules (Polymer) | |

| Cartridges | |

| Prefilled Syringes | |

| Caps and Closures | |

| Others, Product Type (Unit-Dose Strips, Inhaler Canisters) | |

| By Drug Delivery Route | Oral |

| Parenteral | |

| Nasal | |

| Pulmonary | |

| Transdermal | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large will European demand for plastic packs in pharma be by 2031?

Value is forecast to reach USD 19.41 billion by 2031, reflecting a 5.11% CAGR from 2026.

Which plastic pack format is growing fastest?

Prefilled syringes lead, advancing at a 7.98% CAGR on the back of at-home biologic injections.

Why is Spain outpacing other countries in growth?

Contract manufacturers are adding secondary-packaging lines near Barcelona and Madrid, lifting Spain’s forecast CAGR to 6.53%.

What sustainability rules affect pharmaceutical plastic packs?

EU Regulation 2025/40 mandates 30% recycled content by 2030 and raises collection-rate targets to 65%.

Which resin family faces the strongest demand in parenterals?

Cyclic-olefin polymers are gaining share because they minimize protein adsorption and resist delamination.

How concentrated is the supplier landscape?

The top five players account for around 40% of revenue, signaling moderate concentration.

Page last updated on: