Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

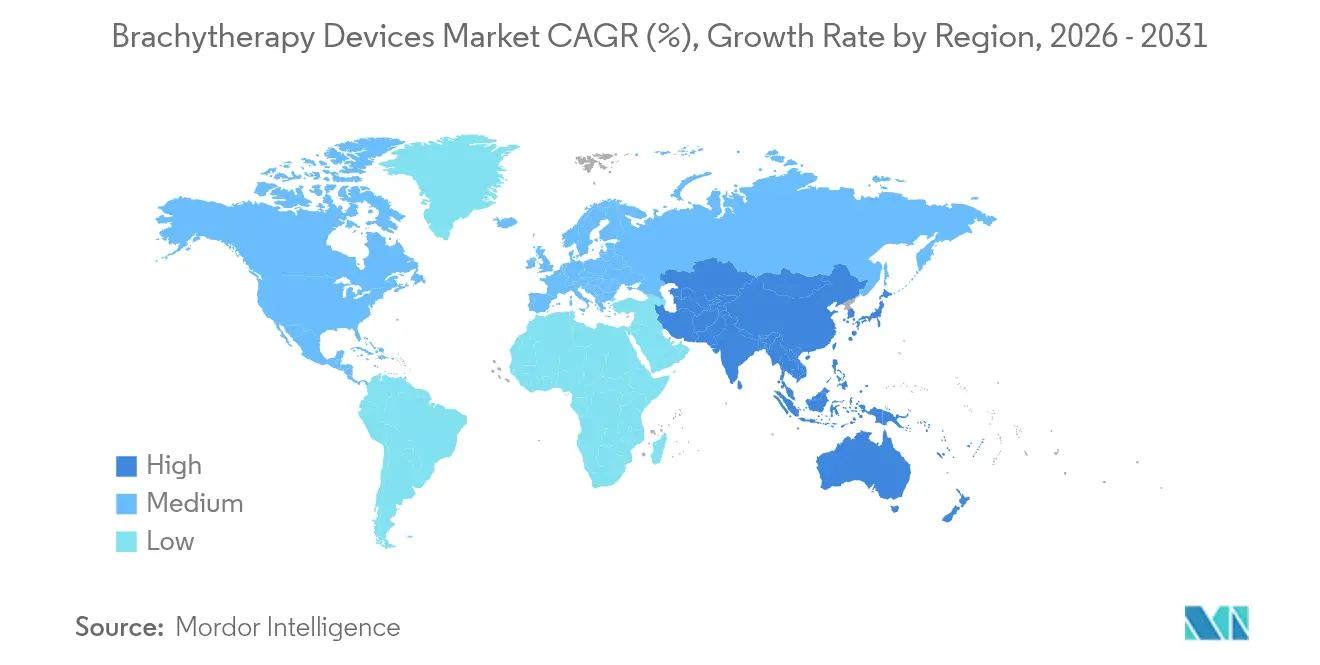

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

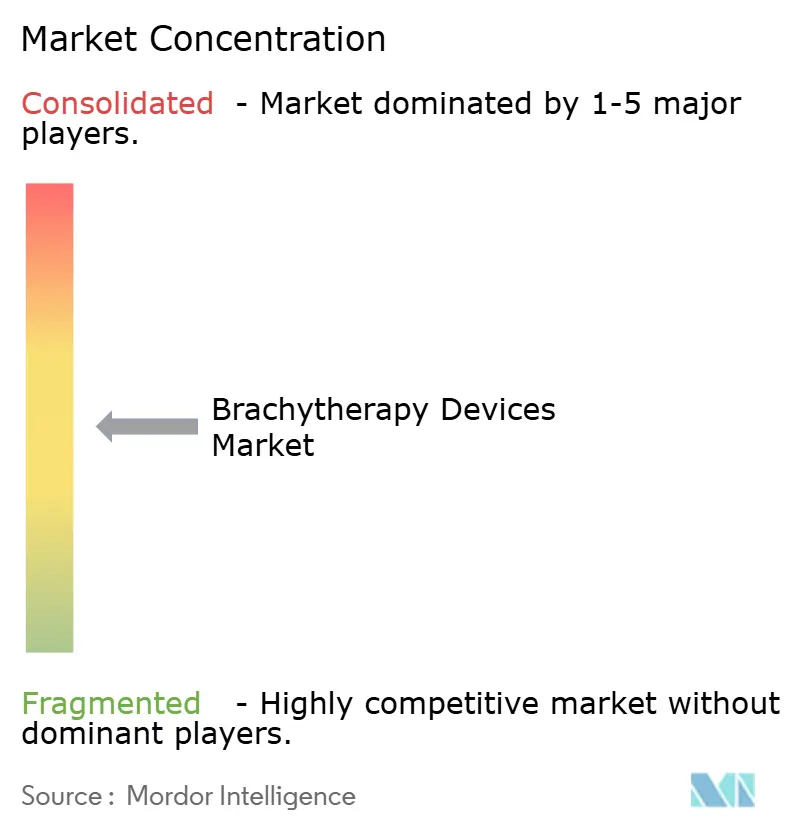

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brachytherapy Devices Market Analysis by Mordor Intelligence

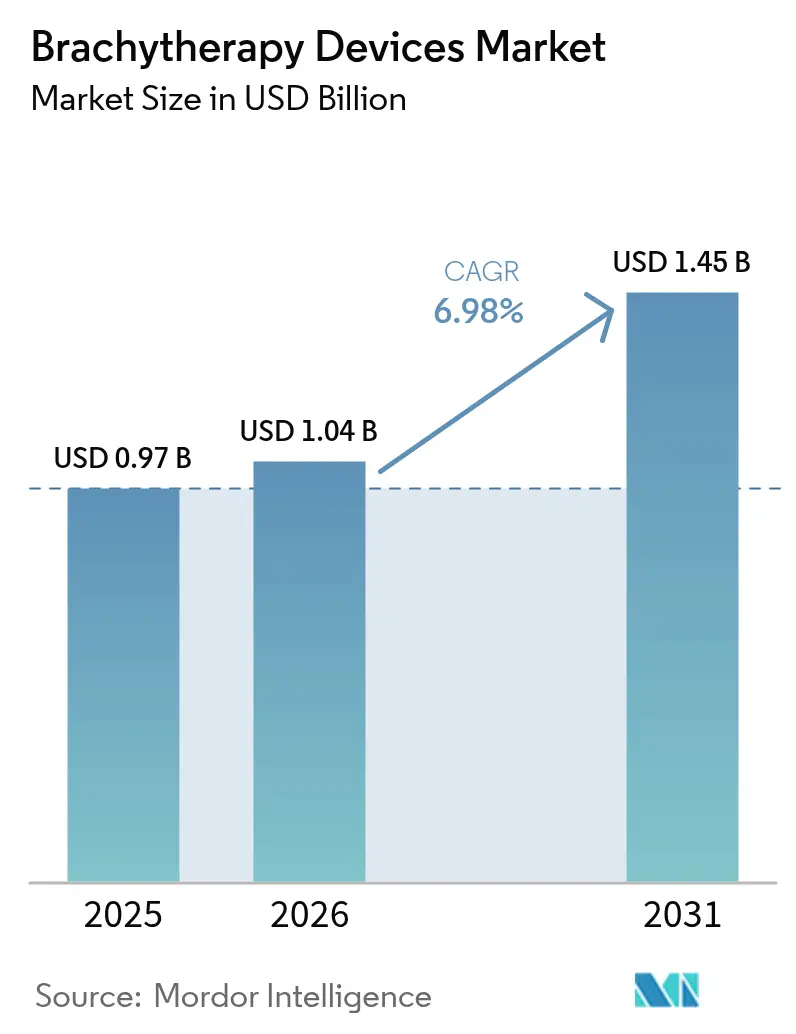

The Global brachytherapy devices market size was valued at USD 0.97 billion in 2025 and estimated to grow from USD 1.04 billion in 2026 to reach USD 1.45 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031). Intensifying cancer incidence, favorable reimbursement for outpatient high-dose-rate (HDR) procedures, and rapid adoption of electronic systems anchor the demand outlook. Government and payer programs that accelerate radiotherapy access, especially in Asia-Pacific and Latin America, further support uptake. Parallel advances in artificial intelligence (AI) for treatment planning and electronic after-loading technologies shorten procedure times, expand deployment to community settings, and safeguard the isotope supply chain. Emerging nano-scale radionuclide carriers could unlock organ-sparing salvage options, broadening the therapeutic window and lengthening device replacement cycles for the Global brachytherapy devices market.

Key Report Takeaways

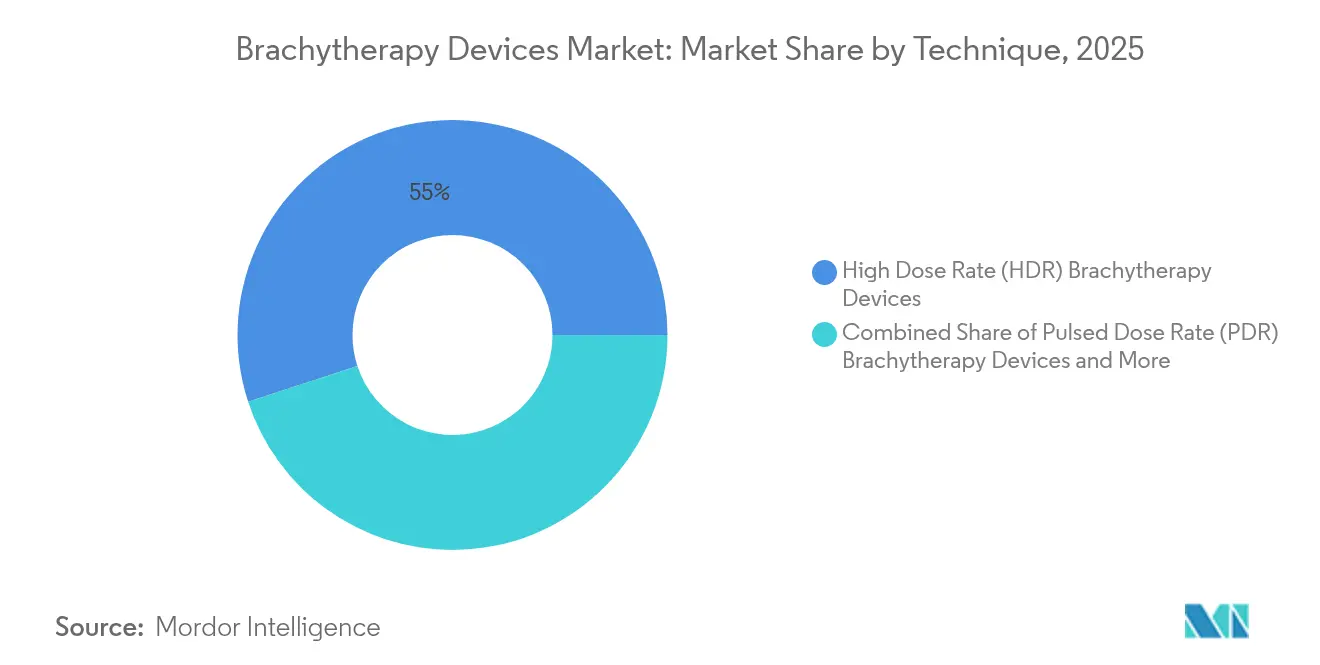

- By technique, HDR held 55.02% of the Global brachytherapy devices market share in 2025, while pulsed-dose-rate (PDR) is forecast to expand at 8.88% CAGR through 2031.

- By product type, seeds accounted for 43.05% share of the Global brachytherapy devices market size in 2025; electronic brachytherapy systems are poised for 14.39% CAGR to 2031.

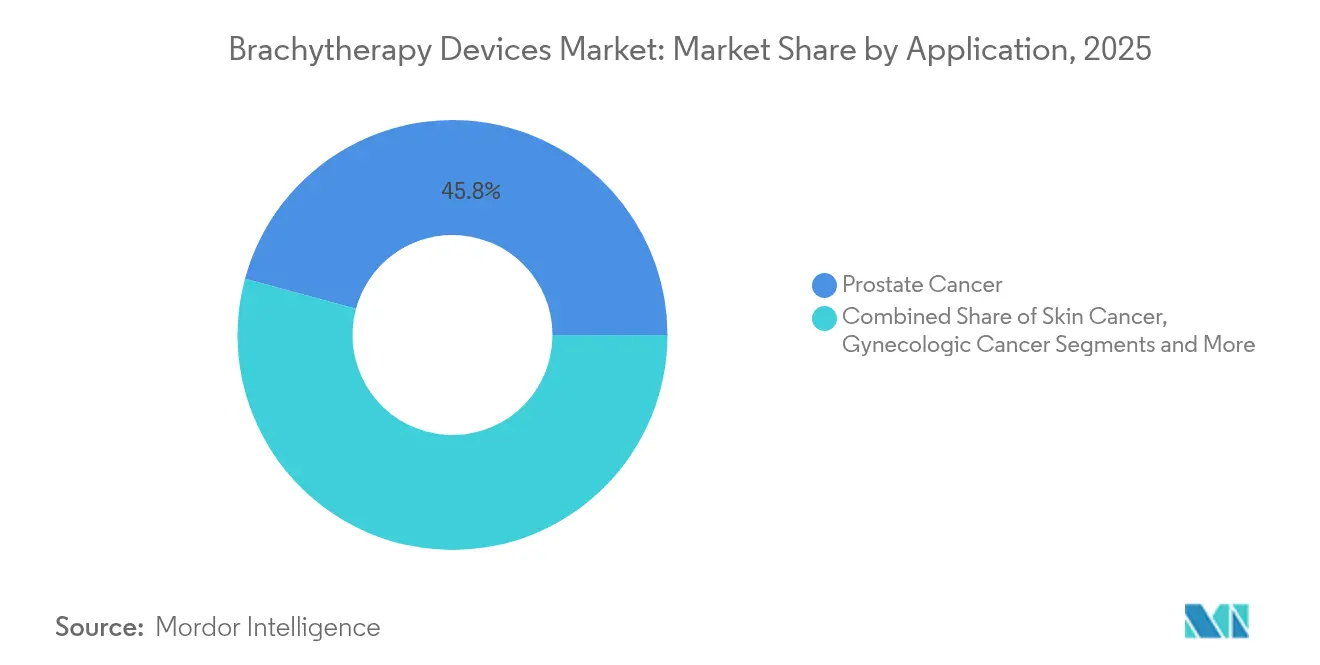

- By application, prostate cancer led with 45.78% revenue share in 2025; skin cancer treatments are projected to grow at a 10.32% CAGR to 2031.

- By end user, hospitals captured 59.35% share of the Global brachytherapy devices market size in 2025, whereas ambulatory surgical centers are set for a 9.24% CAGR over the outlook period.

- By geography, North America dominated with 44.90% share in 2025, while Asia-Pacific is projected to log the fastest 9.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Brachytherapy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Cancer Incidence | +1.8% | Global, with highest impact in aging populations of North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Rising Government & Payer Initiatives To Expand Radiotherapy Access | +1.2% | Global, particularly emerging markets in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Technological Shift Toward HDR & Electronic Brachytherapy Systems | +1.5% | North America & Europe leading, APAC adoption accelerating | Medium term (2-4 years) |

| Reimbursement Tail-Winds For Outpatient HDR Procedures | +0.9% | North America & Europe, with selective coverage in developed APAC markets | Short term (≤ 2 years) |

| AI-Driven Treatment-Planning Improving Workflow Efficiency | +0.8% | North America & Europe initially, global expansion expected | Medium term (2-4 years) |

| Nano-Scale Radionuclide Carriers Enabling Organ-Sparing Salvage Therapy | +0.6% | Research centers in North America & Europe, clinical translation pending | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Cancer Incidence

Persistent growth in global cancer diagnoses underpins a structural need for precise, localized radiation. The American Cancer Society projects 2,041,910 new U.S. cases in 2025, with prostate, breast, and gynecologic cancers forming the core clinical settings for brachytherapy. As aging populations swell, oncologists value brachytherapy’s high conformality and organ preservation advantages. Clinical data in hepatocellular carcinoma cite 98.5% overall response rates using high-dose-rate protocols, signaling opportunity for disease-site expansion. Together, epidemiology and outcome evidence reinforce long-run demand in the Global brachytherapy devices market.

Rising Government & Payer Initiatives to Expand Radiotherapy Access

Policy makers view radiotherapy equity as public-health priority. India’s National Cancer Grid is closing a national shortfall of 53 brachytherapy units through indigenous HDR platforms, such as the ‘Karknidon’ remote after-loader, lowering acquisition costs. In the United States, Medicare’s Transitional Coverage for Emerging Technologies (TCET) pathway accelerates breakthrough device coverage decisions, potentially welcoming five brachytherapy candidates each year[1]Centers for Medicare & Medicaid Services, “Medicare Program; Transitional Coverage for Emerging Technologies,” Federal Register, federalregister.gov. These moves broaden patient pools and de-risk innovation for the Global brachytherapy devices market.

Technological Shift Toward HDR & Electronic Brachytherapy Systems

Cancer centers increasingly migrate from permanent low-dose-rate implants to HDR and electronic modalities that support outpatient care, reduce shielding needs, and streamline workflows. The U.S. FDA regulates electronic brachytherapy as Class II with special controls, expediting approvals while safeguarding safety. With Elekta’s acquisition of Xoft, global portfolios now encompass eBx for facilities where isotope logistics are prohibitive. This pivot enhances throughput and underpins recurring hardware and software revenues in the Global brachytherapy devices market.

Reimbursement Tail-Winds for Outpatient HDR Procedures

Under the 2025 U.S. Hospital Outpatient Prospective Payment System, brachytherapy source C2645 reimburses at USD 4.69 per mm², sustaining favorable economics versus inpatient stays. Value-based-care emphasis on cost-effective protocols promotes HDR in ambulatory surgical centers, catalyzing double-digit growth pockets across the Global brachytherapy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Trained Brachy-Oncologists & Medical Physicists | -1.4% | Global, most acute in emerging markets and rural areas | Long term (≥ 4 years) |

| Uneven Isotope Supply Chain (Ir-192, I-125) & Export Controls | -0.9% | Global, with supply concentration in few countries creating vulnerability | Medium term (2-4 years) |

| Declining Utilization Amid Competition From SBRT & Robotic Surgery | -0.7% | North America & Europe primarily, emerging in developed APAC markets | Medium term (2-4 years) |

| Regulatory Uncertainty Around Electronic Brachytherapy Devices (Class III) | -0.5% | North America & Europe, affecting global product development strategies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Trained Brachy-Oncologists & Medical Physicists

Fifteen percent of U.S. medical physicists signal retirement intentions within 10 years, while cancer incidence climbs 2% annually, magnifying staffing gaps[2]American Society for Radiation Oncology, “Medical Physicist Workforce,” astro.org. Residency directors cite limited caseloads as barriers to braid practical exposure, curtailing future competencies. Australian and New Zealand trainees echo concerns over shrinking seed-implant volumes, foreshadowing skills attrition. While simulation workshops raise proficiency, the talent pipeline remains a rate-limiter for the Global brachytherapy devices market.

Uneven Isotope Supply Chain & Export Controls

Most Ir-192 and I-125 sources originate from a handful of reactors subject to maintenance outages and export restrictions, exposing cancer centers to schedule disruptions and premium pricing. The United States imports roughly 90% of raw isotopes for nuclear medicine, underscoring geopolitical dependencies. Accelerator-based production offers diversification, yet commercial scale remains nascent. Supply insecurity restrains procurement decisions across the Global brachytherapy devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: HDR Dominance Drives Workflow Evolution

High-dose-rate systems secured 55.02% share of the Global brachytherapy devices market in 2025, reflecting their capacity to condense treatment into few fractions and fit modern outpatient economics. Peer-reviewed data at ASTRO 2024 confirmed dose escalation benefits without overall-survival trade-offs across HDR and low-dose-rate (LDR) arms. The segment’s leadership remains anchored in prostate and gynecologic workflows, yet lung, liver, and head-and-neck indications show acceptance, sustaining hardware refresh cycles in the Global brachytherapy devices market.

Pulsed-dose-rate (PDR) technology is projected to record 8.88% CAGR through 2031, blending LDR radiobiology with HDR infrastructure to expand case mix flexibility. AI-enabled planning equalizes quality between modalities, flattening the learning curve for new adopters. LDR retains relevance in permanent seed implants where single-session convenience aligns with patient preference. Technique diversification ensures clinicians match dose kinetics to tumor biology, reinforcing clinical confidence and mitigating modality substitution risk.

By Product Type: Electronic Systems Reshape Market Dynamics

Seeds captured 43.05% share of the Global brachytherapy devices market in 2025, bolstered by decades of urology familiarity and streamlined inventory models. Yet electronic brachytherapy (eBx) systems—free of radioactive source handling—are on track for a 14.39% CAGR through 2031. The Global brachytherapy devices market size for eBx is projected to climb as unshielded-room operation invites smaller hospitals and ambulatory centers into the modality, especially for skin and breast protocols.

Applicators and after-loaders represent the mechanical backbone of HDR and PDR workflows, sustaining steady replacement demand as caseloads and dose-rate innovations evolve. Treatment-planning software, increasingly bundled in subscription models, embeds reinforcement learning scripts that cut plan iterations from hours to minutes, driving stickiness for integrated vendors and elevating switching costs across the Global brachytherapy devices market.

By Application: Prostate Cancer Leadership Amid Diversification

Prostate cancer procedures held 45.78% share in 2025, continuing to anchor volumes for seeds and HDR boosts. Favorable reimbursement, robust long-term biochemical control data, and rising active-surveillance transitions to focal salvage underpin its base. Skin cancer registers the swiftest 10.32% CAGR to 2031, leveraging eBx portability and a growing elderly demographic with non-melanoma lesions. The Global brachytherapy devices market size for skin applications remains comparatively small today but offers scaling runway as dermatology practices embrace office-based radiotherapy.

Gynecologic oncology strengthens through MRI-guided hybrid interstitial-intracavitary techniques, while accelerated partial-breast irradiation consolidates outpatient gains. Novel alpha-emitter intratumoral devices, such as Alpha DaRT, create footholds in challenging head-and-neck and glioblastoma recurrences. Application breadth reduces reliance on a single disease site, engineering resilience into the Global brachytherapy devices market.

By End User: Ambulatory Centers Drive Access Expansion

Hospitals commanded 59.35% of 2025 demand owing to full-service oncology infrastructure, in-house physics teams, and capital budgets. Yet ambulatory surgical centers (ASCs) will post a 9.24% CAGR through 2031, propelled by payer preference for lower-cost sites and HDR’s single-visit convenience. The Global brachytherapy devices market share held by ASCs is supported by Medicare’s standalone payment rates that offset equipment amortization.

Specialty oncology clinics and academic centers remain technology vanguards, piloting AI-guided workflows and nanoparticle trials that later cascade into community practice. As electronic systems sidestep vault requirements, new entrants can expand service lines with moderate capital, growing the distributed footprint of the Global brachytherapy devices market.

Geography Analysis

North America retained 44.90% share in 2025 as mature reimbursement, early AI adoption, and a dense cancer-care network sustain procedure volumes. Federal programs such as TCET speed market access for breakthrough brachytherapy devices, while a looming 15% physicist retirement rate challenges workforce capacity. Partnerships like Varian-Ballad Health illustrate efforts to bridge rural access gaps via long-term equipment and service contracts. Vendor service revenues from these deals underpin regional resilience for the Global brachytherapy devices market.

Europe delivers steady growth through evidence-based adoption and cross-border research collaborations. Germany, France, and the United Kingdom pioneer MRI-guided adaptive brachytherapy, while CE-marked innovations such as AngioDynamics’ AlphaVac F18 85 gain rapid uptake, reinforcing regulatory predictability. EU-backed training exchanges with Asia bolster best-practice dissemination and support consistent utilization across the continent. The Global brachytherapy devices market benefits from Europe’s early-phase clinical trial density, informing global purchasing decisions.

Asia-Pacific will chart the highest 9.08% CAGR through 2031 as oncology infrastructure scales. India records nearly 1 million new cancer cases annually and addresses a 53-unit brachytherapy gap through indigenous HDR platforms. Japan hosts 129 Ir-192 remote after-loaders and reports 48% of centers employing 3D planning, underscoring advanced practice penetration. China’s provincial equipment procurement programs and central reimbursement reforms are expanding patient access, but physics staffing remains constrained. Regional collaboration via the Federation of Asian Organizations for Radiation Oncology aims to elevate treatment quality, sustaining momentum for the Global brachytherapy devices market.

Competitive Landscape

The Global brachytherapy devices industry is moderately fragmented, with multinationals balancing hardware breadth, software integration, and service wrap to secure account stickiness. Elekta, Varian, Isoray, and Eckert & Ziegler leverage multi-modal portfolios, while regional innovators such as BRIT/-BARC compete on cost-optimized HDR systems for emerging markets. Competitive intensity centers on AI-enhanced planning suites, electronic after-loading platforms, and isotope supply reliability.

Strategic alliances dominate differentiation. Elekta integrates GE HealthCare’s MIM Software to streamline contouring and plan-optimization pipelines. Azra AI collaboration automates registry abstraction, unlocking outcomes-based contracting opportunities. Eckert & Ziegler’s Actinium-225 ramp diversifies revenue into alpha-therapy precursor supply, creating synergies with brachytherapy source manufacturing.

Mergers and acquisitions align with expansion into adjacent oncology verticals. Elekta’s purchase of Xoft adds electronic brachytherapy, while BD’s planned separation of its Biosciences division could spin out radiotherapy assets into sharper growth vehicles. Vendor strategies increasingly pair capital equipment with managed-service models, locking multi-year refresh pipelines and underpinning revenue visibility across the Global brachytherapy devices market.

Brachytherapy Devices Industry Leaders

Carl Zeiss Meditec AG

Elekta AB

Becton, Dickinson and Company

Eckert & Ziegler BEBIG

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Dr. Kamakshi Memorial Hospital inaugurated a new Flexitron HDR brachytherapy unit, expanding precision cancer treatment capacity.

- May 2024: Artemis Hospital, Delhi NCR, launched a dedicated brachytherapy program providing minimally invasive radiation options for diverse tumor sites.

Global Brachytherapy Devices Market Report Scope

As per the scope of the report, Brachytherapy is a type of internal radiation therapy that involves the placement of radioactive material inside the patient body to treat cancer. The brachytherapy devices market is segmented by technique (high dose rate brachytherapy devices and low dose rate brachytherapy devices), application (gynecologic cancer, prostate cancer, breast cancer, and others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

By Technique

| High Dose Rate (HDR) Brachytherapy Devices |

| Low Dose Rate (LDR) Brachytherapy Devices |

| Pulsed Dose Rate (PDR) Brachytherapy Devices |

By Product Type

| Seeds |

| Applicators & Afterloaders |

| Electronic Brachytherapy Systems |

| Software & Treatment-Planning Solutions |

By Application

| Prostate Cancer |

| Gynecologic Cancer |

| Breast Cancer |

| Skin Cancer |

| Head & Neck Cancer |

| Others |

By End User

| Hospitals |

| Oncology Centers & Specialty Clinics |

| Ambulatory Surgical Centers |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technique | High Dose Rate (HDR) Brachytherapy Devices | |

| Low Dose Rate (LDR) Brachytherapy Devices | ||

| Pulsed Dose Rate (PDR) Brachytherapy Devices | ||

| By Product Type | Seeds | |

| Applicators & Afterloaders | ||

| Electronic Brachytherapy Systems | ||

| Software & Treatment-Planning Solutions | ||

| By Application | Prostate Cancer | |

| Gynecologic Cancer | ||

| Breast Cancer | ||

| Skin Cancer | ||

| Head & Neck Cancer | ||

| Others | ||

| By End User | Hospitals | |

| Oncology Centers & Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Global brachytherapy devices market in 2026?

The market is valued at USD 1.04 billion in 2026 and is projected to reach USD 1.45 billion by 2031, reflecting a 6.98% CAGR.

Which technique segment is growing fastest?

Pulsed-dose-rate devices are set to grow at a 8.88% CAGR through 2031 as they blend HDR precision with LDR radiobiology.

What drives adoption in ambulatory surgical centers?

Favorable outpatient reimbursement, HDR’s single-visit protocols, and electronic systems that operate without shielded vaults underpin a 9.24% CAGR for ASCs.

How is AI influencing brachytherapy workflows?

Reinforcement-learning and large-language-model tools cut planning time from hours to minutes while maintaining plan quality, easing workforce pressure and standardizing care.

Which region will post the highest growth?

Asia-Pacific will record a 9.08% CAGR to 2031, propelled by expanding infrastructure, indigenous HDR technology, and government initiatives to bridge treatment gaps.

Page last updated on: