Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.63 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cryogenic Pump Market Analysis by Mordor Intelligence

Cryogenic Pump Market size in 2026 is estimated at USD 2.63 billion, growing from 2025 value of USD 2.5 billion with 2031 projections showing USD 3.37 billion, growing at 5.10% CAGR over 2026-2031.

Accelerated LNG terminal build-outs, hydrogen economy infrastructure, and deep-tech applications such as quantum computing and commercial spaceflight reinforce equipment demand. Rising policy support for cleaner fuels and technology improvements that lower boil-off and raise flow efficiency are prompting end users to replace legacy pumps ahead of scheduled life cycles. Suppliers respond through larger impeller designs, integrated condition-monitoring, and modular skids positioned for rapid installation at brownfield and greenfield sites. Concurrently, corporate acquisitions are concentrating intellectual property, helping global vendors offer complete cryogenic fluid-handling packages across LNG, liquid hydrogen, and specialty gas value chains.

Key Report Takeaways

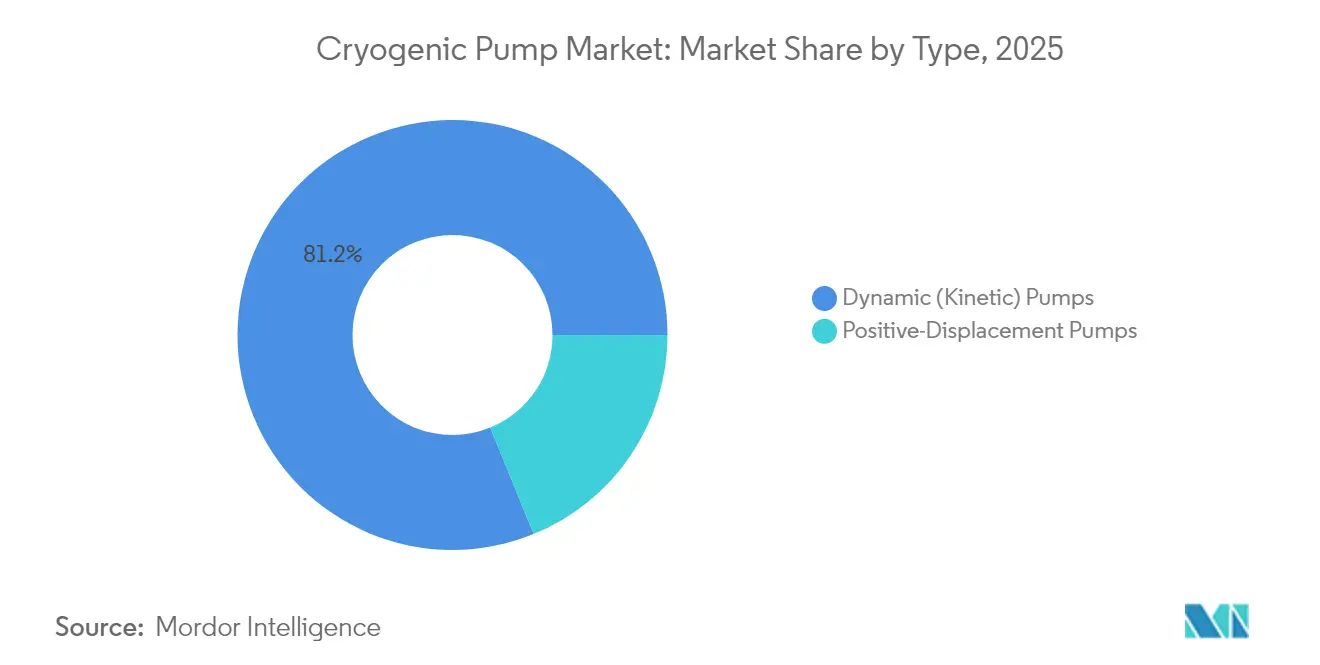

- By type, dynamic kinetic designs held 81.16% of the cryogenic pump market share in 2025, while positive-displacement units are pacing at a 5.62% CAGR through 2031.

- By cryogenic gas, LNG accounted for 26.95% of the cryogenic pump market size in 2025; hydrogen is projected to expand at an 8.55% CAGR to 2031.

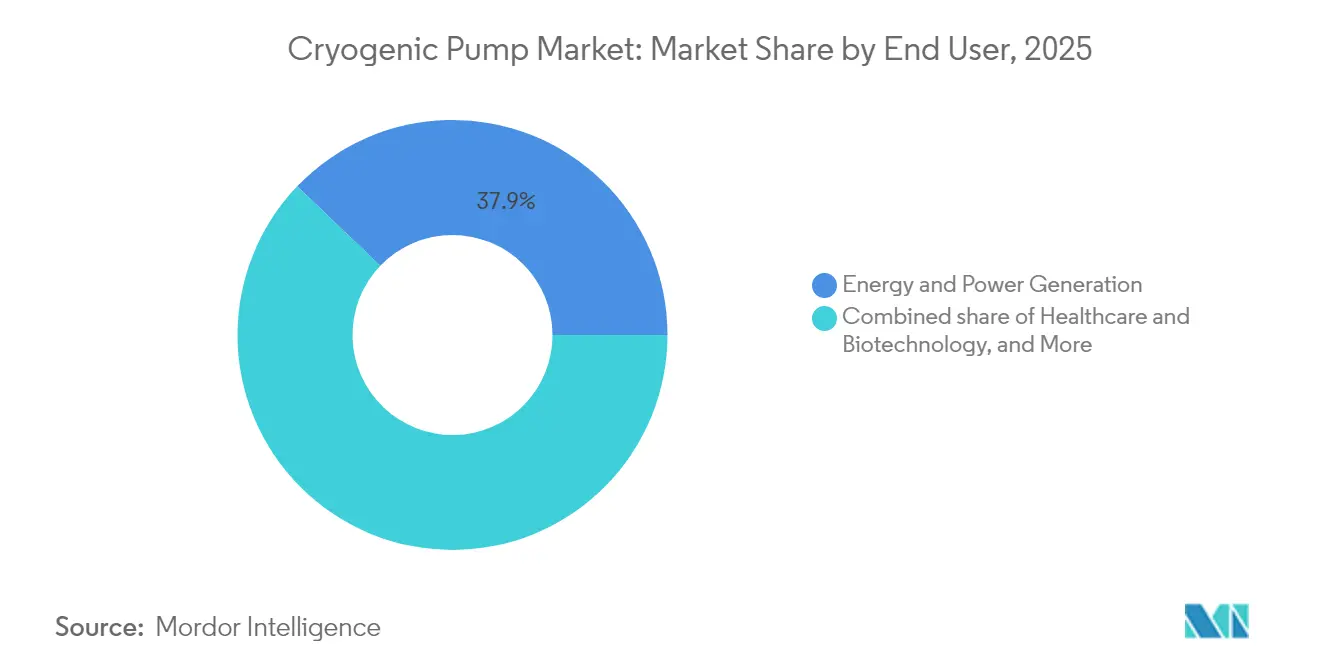

- By end user, energy and power generation led with 37.85% revenue share in 2025; healthcare and biotechnology are set to climb at a 6.32% CAGR through 2031.

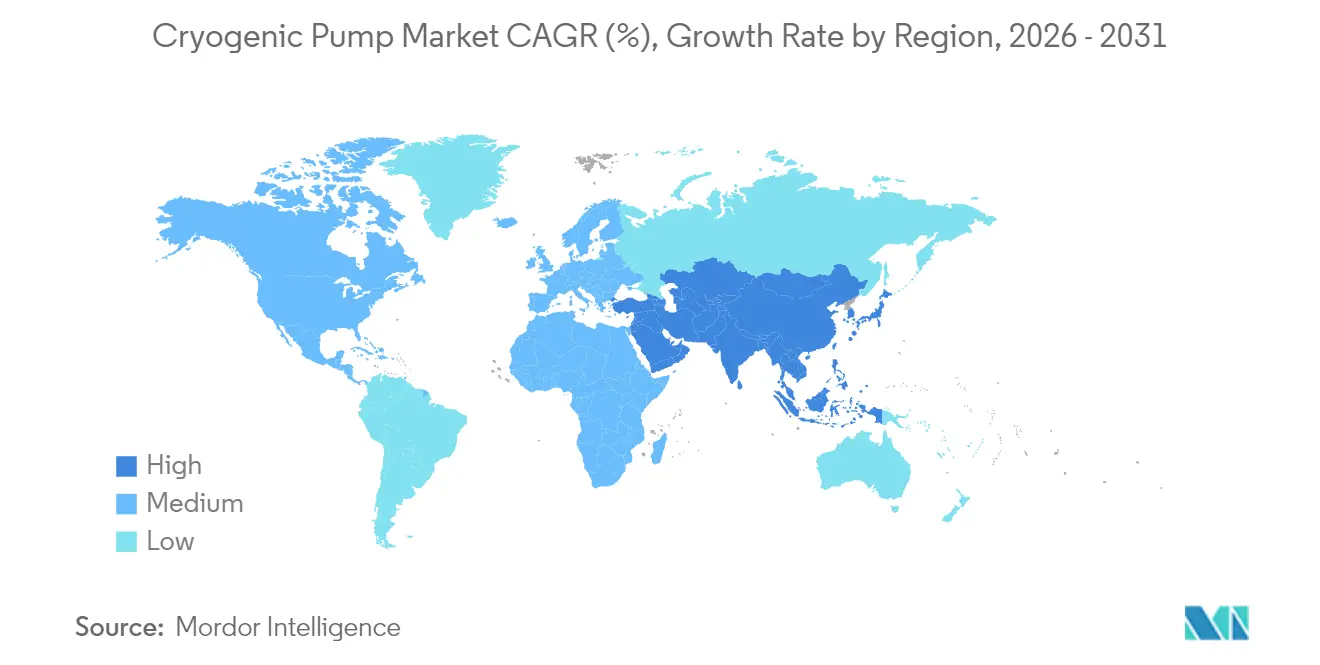

- By geography, Asia Pacific commanded 37.92% of the cryogenic pump market share in 2025 and is advancing at a 5.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cryogenic Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in LNG infrastructure investments | 1.2% | Global, with early gains in Asia Pacific, North America | Medium term (2-4 years) |

| Rising industrial-gas demand from healthcare & semiconductor fabs | 0.9% | APAC core, spill-over to North America & EU | Short term (≤ 2 years) |

| Expansion of the global hydrogen economy | 1.1% | Global, with concentration in EU, Japan, South Korea | Long term (≥ 4 years) |

| Replacement of ageing ASUs in OECD countries | 0.7% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Cryogenic pumps for hyperscale quantum-computing data centers | 0.6% | North America, EU, China | Long term (≥ 4 years) |

| Commercial space-launch propellant handling requirements | 0.5% | North America, EU, India, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in LNG Infrastructure Investments

Nearly 290 billion m³ per year of new LNG export capacity is slated to come online between 2025 and 2030, the largest wave in industry history. Projects such as Plaquemines, Corpus Christi Stage 3, and Qatar’s North Field East underpin bulk demand for pumps rated down to −162 °C. In Europe, the Stade terminal hosts two 240,000 m³ storage tanks that require multi-stage centrifugal units sized for rapid ship-to-shore transfer. Vendors, including Nikkiso, have opened European service hubs to shorten overhaul cycles, while process licensors integrate variable-speed drives to trim power consumption by up to 7%. Contract backlogs are being locked in under long-term service agreements that guarantee availability thresholds exceeding 99% [1]International Energy Agency, “Gas Market Report—Q1 2025,” iea.org.

Rising Industrial-Gas Demand from Healthcare & Semiconductor Fabs

Helium demand is forecast to double by 2035, propelled by MRI installations and 2 nm semiconductor node transitions that need ultra-high-purity environments. The U.S. CHIPS Act channels USD 30 billion into new fabs, motivating EPC firms to bundle nitrogen, argon, and helium supply systems with turnkey cryogenic pump skids. Precision diaphragm pumps ensure oil-free delivery that meets ISO 14644-1 Class 1 cleanroom standards. In Asia, wafer capacity additions in Taiwan, South Korea, and mainland China are driving orders for high-head reciprocating pumps that recycle helium at 25 bar discharge pressure, cutting gas losses by 15% versus legacy loops [2]Cryogenic Society of America, “Helium Outlook 2025,” cryogenicsociety.org.

Expansion of the Global Hydrogen Economy

Liquid hydrogen’s density advantage over compressed gas is attracting heavy-duty mobility and long-duration energy storage developers. Global liquefaction capacity reached 358.9 t/day in 2024, with the U.S. and Canada holding 85% of output. Japan’s Ebara is investing USD 16 billion in the world’s first full-scale LH₂ pump test center, validating components at −253 °C to ISO 21013-1 standards. Simultaneously, China has issued three national LH₂ standards since 2020 and deployed 128 fueling stations, accelerating local demand for small-footprint vertical inline pumps that fit within dense urban forecourts. Government-backed hydrogen hubs in the U.S. earmark USD 7 billion for infrastructure, guaranteeing multi-year offtake that derisks pump capital expenditure [3]EBARA Corporation, “Ebara Opens Liquid Hydrogen Test Center,” ebara.co.jp.

Replacement of Ageing ASUs in OECD Countries

More than 40% of air separation units in Europe and North America were commissioned before 2005. Retrofit programs like Germany’s FLEXASU demonstrate how thicker pipeline walls, upgraded insulation, and additional cryogenic pumps can trim specific power by 8%. Variable-pricing electricity markets reward flexible plants, so operators install two-speed motor drives and predictive maintenance software to shift production toward off-peak hours. Linde’s recent EUR 100 million China ASU mirrors this approach, embedding digital twins that cut unplanned downtime by 30% and lengthen mean-time-between-overhauls for submerged pumps to 60,000 hours [4]Linde Engineering, “FLEXASU Retrofit Project Factsheet,” linde.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & maintenance complexity | -0.8% | Global | Short term (≤ 2 years) |

| LNG price volatility delaying projects | -0.6% | Global, with concentration in Asia Pacific, Middle East | Short term (≤ 2 years) |

| Supply-chain shortages of specialty alloys | -0.4% | Global, with acute impact in North America, EU | Medium term (2-4 years) |

| Regulatory uncertainty on ammonia as marine fuel | -0.3% | Global, with focus on major shipping routes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & Maintenance Complexity

A submerged cryogenic pump skid can represent 4–6% of an LNG train’s installed cost, while welders certified to American Society of Mechanical Engineers Section IX have commanded wage premiums surpassing 20% since 2021. The Golden Pass LNG project’s delays, triggered by contractor insolvency, highlight budget exposure. Furthermore, pump repair windows require specialist tooling held by only a handful of service centers worldwide, extending turnaround intervals. Tariffs on cryogenic steel and Inconel exacerbated by geopolitical tensions inflate bills of material, prompting operators to negotiate vendor-managed inventory programs that amortize supply risk.

LNG Price Volatility Delaying Projects

Asian spot LNG exceeded USD 52/MMBtu during 2024 peaks, stalling final investment decisions for new liquefaction in the U.S. Gulf Coast. Europe’s pause on non-FTA export approvals introduces scheduling uncertainty that undercuts pump order visibility, pushing prospective buyers to defer procurement until market signals stabilize. Similar hesitancy affects Middle East mega-projects, where offtake contracts now include price-reopeners disincentivizing early EPC mobilization. Pump manufacturers are lengthening quotation validity and adding currency-hedge clauses to safeguard margins, yet booking cycles remain elongated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dynamic Pumps Dominate Through Efficiency Advantages

Dynamic kinetic designs, primarily centrifugal models, controlled 81.16% of the cryogenic pump market in 2025 because they deliver high volumetric flow with limited moving parts. LNG terminals favor between-bearings centrifugal pumps whose open-volute architecture minimizes NPSH requirements at −162 °C. The segment is forecast to maintain leadership as regasification capacity accelerates across Asia and Europe. Positive-displacement technology, by contrast, caters to precision dosing and high-pressure hydrogen service where flow stability outweighs capacity. These units are projected to post a 5.62% CAGR, buoyed by growth in liquid hydrogen distribution networks for mobility and distributed power.

Centrifugal models integrate vapor-return lines that reduce cavitation, extending overhaul intervals beyond 60,000 hours. Axial-flow variants target peak-shaving peak load LNG send-out, where differential pressures remain modest. Mixed-flow pumps provide hybrid performance for floating storage regasification units. Reciprocating pumps within the positive-displacement category employ oil-free piston rings that limit hydrocarbon contamination, a key metric for fuel-cell-grade hydrogen. Screw pumps support continuous duty in metallurgical argon service, whereas diaphragm pumps deliver particle-free flow for 3 nm semiconductor wet benches. Diversifying duty points ensures that every modality finds its niche, sustaining healthy competition across design paradigms. The segment’s split also underpins after-market revenues, as different architectures require distinct seal kits and spare rotors, reinforcing OEM lifecycle engagement with plant operators.

By Cryogenic Gas: Hydrogen Emerges as Growth Driver

LNG retained 26.95% of the cryogenic pump market size in 2025, anchored by installed liquefaction and regasification assets that integrate multi-stage pumps. However, the hydrogen segment is projected to expand at an 8.55% CAGR, catapulted by national road maps targeting net-zero objectives. Liquid hydrogen’s gravimetric energy density advantages foster adoption in heavy transport and aviation test beds, stimulating orders for pumps capable of 120 bar discharge. Meanwhile, nitrogen and oxygen maintain stable demand for steelmaking and medical applications, necessitating standard-duty submerged centrifugals.

Helium’s niche yet fast-growing role in quantum computing and MRI scanning propels demand for specialized low-loss pumps that withstand sub-2 K operation. Recovery units engineered with regenerative braking recapture up to 14% of motor energy, demonstrating efficiency gains baked into new designs. Argon continues to serve additive manufacturing and high-purity welding markets, where contamination control trumps volumetric throughput. Across gas types, multipurpose package offerings—combining pump, vaporizer, and controls—enable suppliers to tailor configurations swiftly, aligning with varied thermodynamic properties and end-user purity specifications.

By End User: Healthcare & Biotechnology Drives Innovation

Energy and power generation commanded 37.85% of the cryogenic pump market size 2025, reflecting entrenched LNG trade flows and industrial gas consumption in refineries and integrated steel plants. However, healthcare and biotechnology are the fastest-growing verticals at 6.32% CAGR through 2031. MRI fleet expansion, proton-therapy rollouts, and cryoablation devices are proliferating, requiring pumps that maintain constant helium or nitrogen supply with minimal vibration to protect imaging resolution. Equipment suppliers are collaborating with OEMs of medical devices to integrate compact pumps into turnkey cooling loops that fit hospital infrastructure.

Petrochemical clusters continue deploying oxygen and nitrogen pumps for oxidative cracking and inert blanketing, yet growth is moderate. Metallurgical sites, particularly direct-reduced iron plants, demand oxygen boosted by cryogenic pumps to reach reactor stoichiometry, supporting conversion to greener steelmaking. Electronics fabs depend on argon and nitrogen for lithography, and here leak-tight diaphragm pumps ensure no oil contamination compromises wafer yield. Aerospace launch complexes and propulsion test stand out in the customer base, sourcing large-bore LH₂ and LOX pumps certified to ASME B31.3 piping codes for stringent reliability. Diversification across segments cushions suppliers from cyclicality in any single end use, reinforcing resilience in the broader cryogenic pump market.

Geography Analysis

Asia Pacific led the cryogenic pump market in 2025 with 37.92% revenue share, anchored by China’s 27 ongoing LNG terminals and aggressive hydrogen station rollouts. Regional CAGR is projected at 5.38% to 2031 as India, Japan, and South Korea accelerate clean-fuel imports and semiconductor capacity. Indigenous OEMs are scaling local assembly to cut logistics costs, while multinationals license IP to joint-venture partners to comply with procurement rules. China’s Tangshan II terminal, featuring 584.4 bcf storage, typifies the massive duty points driving multi-stage pump demand. Simultaneously, the Xi’an small-scale LNG hub adds 1,400 ktpa liquefaction, boosting orders for skid-mounted pumps deployable in remote industrial parks.

North America maintains robust momentum backed by an 11.4 Bcf/d LNG export base forecast to reach 24.4 Bcf/d by 2028. Liquid hydrogen leadership, with 15 facilities producing 326 t/day, positions the region as a technology incubator. U.S. vendors leverage proximity to aerospace primes and hydrogen hub grants, embedding advanced vibration diagnostic analytics into pump offerings. Canada’s emerging LH₂ corridors link Prince Rupert to inland trucking fleets, spurring demand for mid-scale pumps optimized for trailer offloading. Mexico’s industrial gas expansion in aerospace clusters further broadens regional opportunities.

Europe is pivoting toward import infrastructure to counter Russian gas shortfalls. Germany’s Stade terminal integrates ammonia-ready baseload pumps, future-proofing against fuel transition. Scandinavian shipyards are trialing LH₂ bunkering, requiring portable pump modules with rapid disconnect couplings. Middle East exporters continue capitalizing on cost-advantaged feedgas, but newer blue-hydrogen plants in Saudi Arabia and the UAE are incorporating LH₂ logistics chains that necessitate ultra-low-temperature pumps. Africa and South America remain nascent yet are advancing small-scale LNG for off-grid power, laying the groundwork for incremental pump demand.

Competitive Landscape

The industry exhibits moderate concentration owing to high technical barriers and long qualification cycles. Nikkiso controls roughly a 50% share in select LNG send-out niches, capitalizing on patented spiral inducer designs that suppress cavitation under high flow. The 2025 all-stock merger between Chart Industries and Flowserve creates a USD 19 billion entity with 42% sales from aftermarket services, signalling a pivot toward lifecycle revenue models that lock in customers. Alfa Laval’s EUR 200 million acquisition of Fives Energy Cryogenics broadens its heat-transfer-plus-pump bundle, while Dover’s PSG division integrates Cryogenic Machinery Corp. to deepen centrifugal pump capability.

Competitors differentiate through metallurgy, digital twins, and packaged skid engineering. Ebara’s USD 16 billion LH₂ test center validates components for 10,000-hour duty at −253 °C, conferring first-mover advantage. Flowserve leverages global service hubs that shorten overhaul cycles to less than 14 days, a competitive edge where downtime is punitive. Start-ups target white-space in quantum computing, offering magnetically levitated micro-pumps tailored for dilution refrigerators. Strategic emphasis is shifting from component sales to platform solutions that couple pumps with vaporizers, controls, and predictive analytics, fostering stickier customer relationships and recurring revenue.

Cryogenic Pump Industry Leaders

Nikkiso Co., Ltd.

Ebara Corporation

Flowserve Corporation

Cryostar SAS

Sumitomo Heavy Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Alfa Laval finalized the EUR 200 million purchase of Fives Energy Cryogenics, expanding into advanced cryogenic heat-transfer and pump systems.

- January 2025: PSG (Dover) acquired Cryogenic Machinery Corp., bolstering its centrifugal pump line for industrial gases.

- December 2024: ArianeGroup and Fives entered an MoU to co-develop LH₂ pumps for heavy-duty mobility

- June 2024: The ITER fusion project received its first full-scale cryopump, marking a milestone for fusion-energy infrastructure.

Global Cryogenic Pump Market Report Scope

The cryogenic pump market report includes:

By Type

| Dynamic (Kinetic) Pumps | Centrifugal |

| Axial Flow | |

| Mixed Flow | |

| Positive-Displacement Pumps | Reciprocating |

| Screw | |

| Diaphragm |

By Cryogenic Gas

| Nitrogen |

| Oxygen |

| Argon |

| LNG |

| Hydrogen |

| Helium |

By End User

| Energy and Power Generation |

| Chemicals and Petrochemicals |

| Healthcare and Biotechnology |

| Metallurgy and Metal Processing |

| Semiconductor and Electronics |

| Aerospace and Space Launch Services |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Dynamic (Kinetic) Pumps | Centrifugal |

| Axial Flow | ||

| Mixed Flow | ||

| Positive-Displacement Pumps | Reciprocating | |

| Screw | ||

| Diaphragm | ||

| By Cryogenic Gas | Nitrogen | |

| Oxygen | ||

| Argon | ||

| LNG | ||

| Hydrogen | ||

| Helium | ||

| By End User | Energy and Power Generation | |

| Chemicals and Petrochemicals | ||

| Healthcare and Biotechnology | ||

| Metallurgy and Metal Processing | ||

| Semiconductor and Electronics | ||

| Aerospace and Space Launch Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What will the cryogenic pump market be worth by 2031?

The cryogenic pump market size is projected to reach USD 3.37 billion by 2031, growing at a 5.10% CAGR.

The cryogenic pump market size is projected to reach USD 3.37 billion by 2031, growing at a 5.10% CAGR.

Asia Pacific holds the largest share at 37.92% and is also the fastest-growing region with a 5.38% CAGR.

Why are cryogenic pumps important for the hydrogen economy?

Liquid hydrogen must be transported at −253 °C, and specialized cryogenic pumps enable safe, efficient transfer at the high pressures required for mobility and industrial applications.

Which pump type dominates LNG service?

Dynamic centrifugal pumps dominate due to their high flow capacity and low maintenance, securing 81.16% of overall market share in 2025.

How is healthcare influencing demand for cryogenic pumps?

Expanding MRI installations and proton-therapy centers drive the healthcare and biotechnology segment, expected to grow at 6.32% CAGR through 2031.

What impact will the Chart Industries-Flowserve merger have on the market?

The USD 19 billion merger creates a full-line provider with extensive service coverage, likely intensifying competition and accelerating technology integration across product lines.

Page last updated on: