Cryogenic Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 27.59 Billion |

| Market Size (2031) | USD 37.64 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cryogenic Equipment Market Analysis by Mordor Intelligence

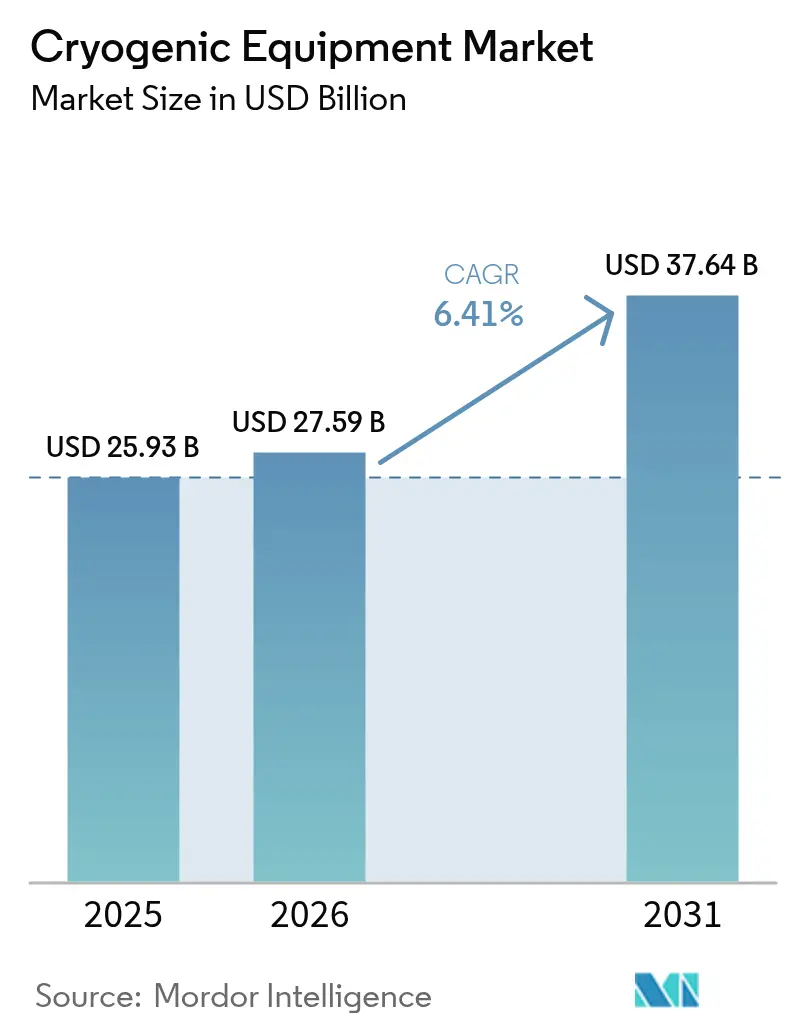

The Cryogenic Equipment market size is expected to grow from USD 25.93 billion in 2025 to USD 27.59 billion in 2026 and is forecast to reach USD 37.64 billion by 2031 at 6.41% CAGR over 2026-2031.

The current momentum reflects the impact of LNG infrastructure expansion, semiconductor-grade gas demand, quantum-computing breakthroughs, and accelerating investments in green-hydrogen liquefaction. Project pipelines in North America and Asia-Pacific anchor near-term growth, while long-haul applications in space exploration and hydrogen mobility broaden the medium-term outlook. Supply-side realignment continues as new helium, argon, and hydrogen capacities mitigate recent shortages. Strategic mergers, notably the pending Chart Industries–Flowserve transaction, strengthen vertical integration and aftermarket capabilities, reinforcing the competitive landscape. Safety-related regulation and high capital intensity still hinder first-time entrants, yet established manufacturers benefit from rising compliance barriers and long maintenance cycles that underpin service revenues.

Key Report Takeaways

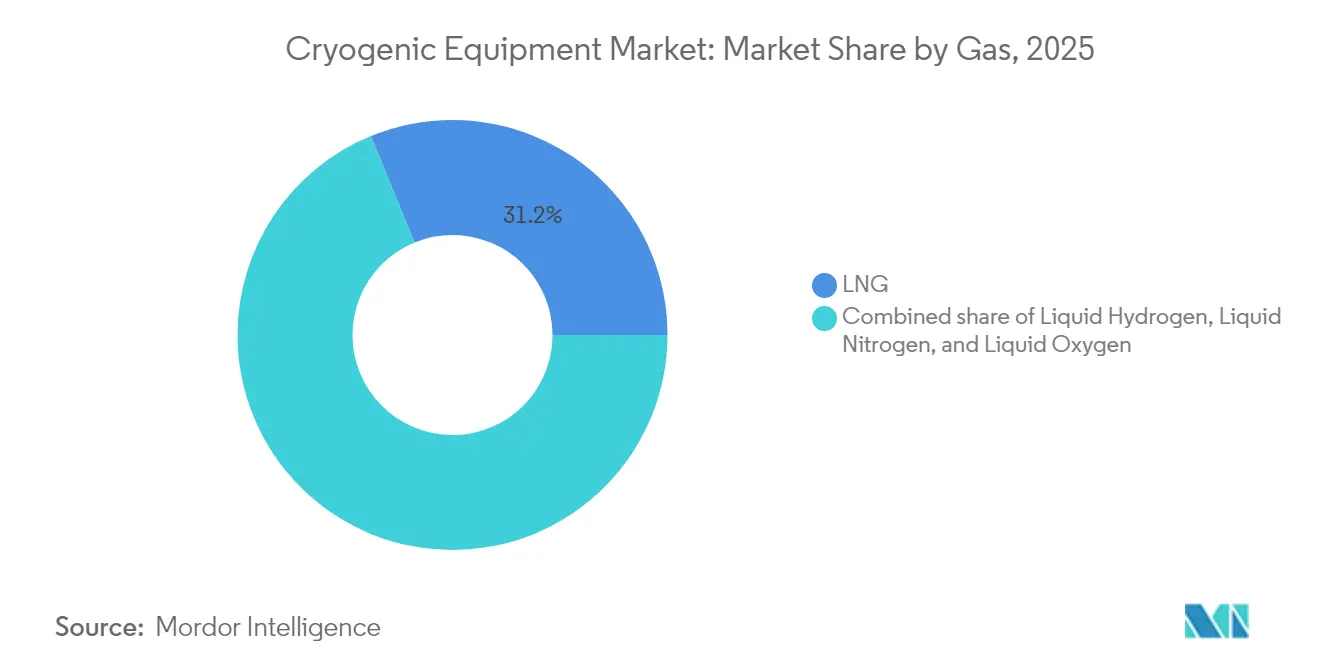

- By gas, LNG led with 31.20% of the global cryogenic equipment market share in 2025. Liquid hydrogen is projected to expand at a 9.95% CAGR to 2031.

- By equipment, tanks commanded a 33.25% share of the global cryogenic equipment market in 2025. Pumps are forecast to advance at an 8.18% CAGR between 2026-2031.

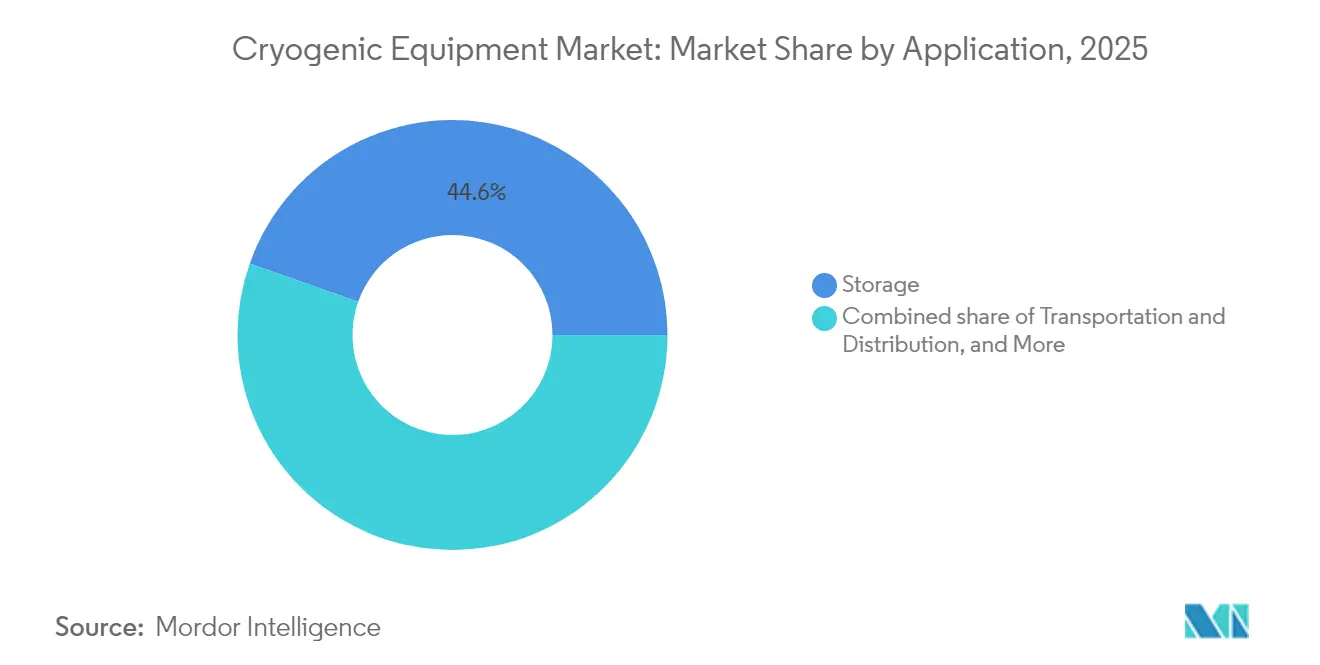

- By application, storage accounted for 44.60% of the global cryogenic equipment market size in 2025. Transportation and distribution exhibit the fastest growth at a 7.69% CAGR to 2031.

- By end-user, oil & gas contributed 27.55% revenue in 2025, while electronics and semiconductors registered a 9.26% CAGR through 2031.

- Asia-Pacific held 42.30% of the global cryogenic equipment market share in 2025, and the region is expanding at a 7.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cryogenic Equipment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging LNG trade & small-scale LNG infrastructure | +1.80% | Global; strongest in APAC & North America | Medium term (2-4 years) |

| Expansion of semiconductor fabs requiring ultra-pure cryogens | +1.50% | North America, APAC | Short term (≤ 2 years) |

| Growth of space-launch demand for cryogenic propellants | +0.90% | North America, Europe, emerging APAC | Long term (≥ 4 years) |

| Emergence of quantum-computing & superconducting use-cases | +0.70% | North America, Europe, selective APAC hubs | Long term (≥ 4 years) |

| Growth in medical cryotherapy & biologics cold-chain logistics | +0.60% | Global; developed markets | Medium term (2-4 years) |

| Investments in green-hydrogen liquefaction plants | +1.20% | Europe, North America, expanding MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging LNG trade & small-scale LNG infrastructure

New liquefaction trains entering service across the United States, Qatar, and East Africa elevate demand for tanks, heat exchangers, and boil-off reliquefaction systems. Venture Global’s Plaquemines plant shipped its first cargo in 2024, demonstrating mid-scale technology that compresses build schedules. Qatar’s North Field expansion to 142 million tpa by 2030 positions the country for 25% of global LNG trade. Modular systems, typified by Linde’s OPTI-LNG™ plants, support niche off-grid consumption in Latin America and sub-Saharan Africa.(1)Linde AG, “OPTI-LNG™ Technology Brief,” linde.com Record orders for Turbo-Brayton units illustrate shipping-sector investments in methane capture that cut voyage losses. Utilization below 50% at some European regasification terminals cautions against blanket capacity additions and may spur retrofit rather than greenfield spending.

Expansion of semiconductor fabs requiring ultra-pure cryogens

The CHIPS Act’s USD 30 billion incentives stimulate multiple U.S. mega-fabs, quadrupling domestic helium needs within a decade. Air Liquide is building a USD 250 million ultra-pure nitrogen complex in Idaho to serve Micron’s 1-beta DRAM line, integrating renewable electricity to lower Scope 2 emissions. Chinese import pivots, now sourcing nearly 90% of helium from Qatar, reshape maritime logistics for ISO tanks and liquid liners. At node sizes below 5 nm, permissible impurity levels decline to parts-per-trillion, lifting demand for high-spec cryogenic purification skids. Localized gas ecosystems could see 60% of semiconductor material inputs produced within U.S. borders by 2030, accelerating procurement of Global Cryogenic Equipment market offerings.

Growth of space-launch demand for cryogenic propellants

Commercial constellations and Artemis lunar logistics multiply liquid hydrogen, oxygen, and methane storage requirements. NASA experiments show zero-boil-off tanks can save 42% propellant annually using active mixing and cryocoolers. ESA validations of vapor-shield cooling give European suppliers an entry path for interplanetary missions. Graham Corporation’s new Florida test site will characterize pumps and valves to 20 K, strengthening domestic qualification infrastructure. Permanent-magnet levitated transfer lines slash conductive heat ingress, prolonging stage-time windows critical for reusable launch vehicles. Terrestrial spin-offs include hydrogen storage for hybrid-electric aviation, broadening the addressable Global Cryogenic Equipment market.

Investments in green-hydrogen liquefaction plants

Air Liquide’s Nevada site delivers 30 t/d and supports more than 40,000 fuel-cell vehicles across California.(2)Air Liquide, “Turbo-Brayton Order Intake Sets New Record,” airliquide.com Plug Power’s Louisiana plant, launched in April 2025, lifts its North American output to 40 t/d and validates electrolytic hydrogen economics at sub-USD 3/kg. Chart Industries supplies liquefiers to Element Resources’ Lancaster hub targeting 20,000 t/y, underscoring OEM opportunity diversity. Europe plans 10 million t/y domestic hydrogen by 2030, implying at least 310 GW of electrolyzer build and widespread demand for 1-3 t/d satellite liquefiers. Emerging hybrid LNG-hydrogen jetties require dual-service tanks and valves, widening the Global Cryogenic Equipment market potential for retrofittable designs.

Restraints Impact Analysis of Cryogenic Equipment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost & complex installation | -1.20% | Global; pronounced in emerging markets | Short term (≤ 2 years) |

| Helium supply shortages & price volatility | -0.80% | Global; APAC & North America | Medium term (2-4 years) |

| Safety risks causing regulatory delays | -0.60% | Global; stricter in developed markets | Medium term (2-4 years) |

| Scarcity of cryogenics-skilled workforce | -0.40% | Global; acute in emerging economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital cost & complex installation

Large-scale LNG or air-separation units entail USD 5 billion-plus annual capex for market leaders, deterring smaller entrants. Heat-exchanger manufacture alone can form 30% of plant budgets, yet each 1% efficiency boost saves 5% compressor energy. ADNOC’s Ruwais project illustrates the financing barrier, with a USD 5.5 billion EPC value before commissioning. Compliance with NFPA 59A and ASME codes extends schedules by months and demands specialist inspection. European gas-association guidelines further increase design complexity and curricula for operators. Consequently, retrofit optimization often supersedes greenfield builds, moderating immediate Global Cryogenic Equipment market orders.

Helium supply shortages & price volatility

Prices peaked at USD 14/m³ in 2023 following the U.S. reserve phase-out, pressuring MRI suites and semiconductor fabs. Qatar became the largest supplier, covering 90% of China’s imports. Russia’s Amur Gas Processing Plant adds new volumes, but geopolitical risk persists. Closed-loop recovery kiosks and small-scale purification skids help fabs curb consumption up to 30%. Exploration in North America and Tanzania signals future diversification, yet pipelines to market remain expensive. Volatility, therefore, injects procurement uncertainty into the Global Cryogenic Equipment market, contracting cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cryogenic Equipment Market Segment Analysis

By Gas:

LNG dominance challenged by hydrogen accelerationLNG represented 31.20 of % Global Cryogenic Equipment market share in 2025, anchored by 2.6 bcf/d capacity at Plaquemines and Qatar’s expansion trajectory. Liquid hydrogen, however, grows at a 9.95% CAGR underpinned by Plug Power’s Louisiana line and Air Liquide’s Nevada unit. Global Cryogenic Equipment market size for hydrogen liquefiers could exceed USD 3.18 billion by 2031 if Europe hits the 10 million t annual target. Helium and argon remain niche but strategic: semiconductor-grade argon rides lithography growth, while helium shortages intensify focus on recycling skids. Diversified order books now include methane tanks for reusable launch vehicles and nitrogen freezers for plant-based protein processors, underscoring widening end-use diversity.

The segment’s competitive focus shifts toward modular, high-flexibility plants capable of switching between gas species. Chart Industries’ plug-and-play hydrogen modules exemplify this convergence, allowing LNG-trained fabricators to pivot into hydrogen with minimal retooling. North America and APAC dominate the market, yet Europe’s green-deal funding anchors demand for mid-scale green-hydrogen liquefiers. Suppliers demonstrating contamination control to single-digit ppt levels gain pricing premiums in microelectronics contracts.

By Equipment:

Tank stability meets pump innovationTanks held 33.25% share of Global Cryogenic Equipment market size in 2025, supported by demand for full-containment LNG storage nearing 250 m³ and high-pressure composite cylinders in aviation prototypes. Pump revenues expand fastest at 8.18% CAGR, boosted by Dover’s Cryogenic Machinery Corp acquisition that brings low-NPSH centrifugal designs into its portfolio.

Heat-exchanger upgrades dominate refinery retrofits, where 1% thermodynamic gains translate to 5% compressor energy savings. Valve makers leverage digital twins for predictive-maintenance offerings, capturing sticky aftermarket revenue even as unit sales plateau. Instrumentation demand rises in tandem with safety automation, with SIL-3 certified sensors becoming baseline in tenders. Emerging magnetic-levitation transfer lines, eliminating friction losses, position ancillary component specialists for long-cycle orders in space-grade pipelines.

By Application:

Storage leadership faces transport disruptionStorage contributed 44.60% of Global Cryogenic Equipment market size in 2025, reflecting the universality of bulk tanks across LNG, oxygen and nitrogen supply chains. Transportation equipment accelerates at 7.69% CAGR as hydrogen mobility and ISO LNG container trade expand. The U.S. west-coast trucking corridor expects over 40,000 fuel-cell vehicles by 2030, requiring polyurethane-insulated trailers rated below 20 K.

Processing and liquefaction equipment grows alongside green-hydrogen electrolyzer roll-outs, while regasification demand lags in Europe amid sub-50% terminal utilization. R&D applications, though niche in volume, generate premium margins; dilution refrigerators for quantum chips can price above USD 1 million per set. Maritime boil-off reliquefiers, led by Turbo-Brayton orders, demonstrate how specific application pain points foster rapid equipment adoption.

By End-User Industry:

Oil & gas maturity contrasts electronics surgeOil & gas still delivered 27.55% revenue in 2025, yet forward growth tilts toward the electronics cluster expanding at 9.26% CAGR. Micron, Samsung and SK Hynix ramps necessitate on-site air-separation and point-of-use purification, locking in multiyear gas-supply and equipment contracts. Energy-transition verticals adopt hydrogen and LNG for power generation and heavy transport, bringing new peak-shaving and satellite regasification projects. Food-processing uses liquid nitrogen flash-freezing to protect plant-protein textures, while healthcare upgrades cryobanks to support autologous cell therapies under stringent FDA rules. Aerospace demand multiplies with space-tourism flights, where ground support requires rapid-chill fill-stands and zero-boil-off pads.

Geography Analysis

APAC Cryogenic Equipment Market

Asia-Pacific maintained 42.30% Global Cryogenic Equipment market share in 2025, owing to China’s 29 operating LNG terminals and 39 builds underway. Regional CAGR of 7.38% remains intact as India lifts regas capacity and South Korea deepens U.S. chip-supply alliances. By volume, China’s capacity utilization could slip to 43% by 2030, yet tank revamps and safety retrofits sustain aftermarket demand.

North America Cryogenic Equipment Market

North America benefits from CHIPS-Act fabs and LNG exports. By 2028, the United States projects 21.2 bcf/d liquefaction capacity, underpinning large storage-tank and cold-box orders. Simultaneously, Louisiana’s hydrogen corridor positions local OEMs to supply twin-service valves viable for both methane and hydrogen. Canada’s emerging helium projects amplify cryogenic separation skid procurement.

EMEA and South America Cryogenic Equipment Market

Europe wrestles with declining gas demand—20% year-on-year drop in H1 2024—yet continues to commission terminals, raising under-utilization risk. The continent’s hydrogen strategy, targeting 10 million t/y output, channels capex toward electrolyzer-coupled liquefiers. Regulations such as the EU Pressure Equipment Directive elevate compliance costs but protect incumbents. The Middle East & Africa leverages low-carbon LNG at ADNOC’s Ruwais and QatarEnergy projects, while South America adds floating regasification units in Brazil. Each geography channels distinctive stimuli and constraints into the Global Cryogenic Equipment market growth arc.

Competitive Landscape

The Global Cryogenic Equipment market shows moderate concentration but rising consolidation velocity. The all-stock merger between Chart Industries and Flowserve will create a USD 19 billion value entity capturing roughly 20% of combined pumps, valves, and storage-vessel revenues, with USD 300 million cost synergies targeted by 2027. Dover’s acquisition of Cryogenic Machinery Corp augments its pump segment and secures long-term supply into air-gas majors. Alfa Laval’s EUR 200 million purchase of Fives Energy Cryogenics expands into hydrogen and CO₂ capture lines.

Technology differentiation emerges as a prime lever. Air Liquide’s Turbo-Brayton reliquefiers dominate maritime retrofits, while HeLIUM Cryogenics’ Stirling micro-coolers win quantum-lab tenders. Nikkiso’s plan to double German manufacturing capacity shows OEMs expanding regional footprints to navigate trade frictions and cut lead times. Service revenues climb as operators outsource predictive maintenance; Chart’s Nordic service center acquisition echoes this trajectory.

New entrants gravitate to niche segments—quantum, micro-LNG,, and medical cryotherapy—where legacy economies of scale matter less than time-to-market and IP agility. Incumbents respond with venture investments and co-development pacts, seeking to pre-empt disruption.Aa blend of consolidation and specialization characterizes the competitive chessboard of the Global Cryogenic Equipment market.

Cryogenic Equipment Industry Leaders

Linde plc

Emerson Electric Co.

Beijing Tianhai Industry Co Ltd

Cryofab Inc

Chart Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Cryogenic Equipment Market Companies Covered in this Report

- Linde plc

- Air Liquide

- Chart Industries Inc.

- Air Products & Chemicals Inc.

- Cryofab Inc.

- Beijing Tianhai Industry Co. Ltd.

- Emerson Electric Co.

- Honeywell International Inc.

- Sumitomo Heavy Industries Ltd.

- McDermott International Ltd.

- Flowserve Corporation

- HEROSE GmbH

- Wessington Cryogenics

- Cryostar SAS

- IHI Corporation

- Kawasaki Heavy Industries Ltd.

- INOXCVA

- Taylor-Wharton

- Fives Group

- Peters Shipyards

Recent Industry Developments in Cryogenic Equipment Market

- June 2025: Chart Industries and Flowserve are merging in an all-stock deal, creating a combined entity valued at approximately USD19 billion with a target of USD 300 million in annual synergies.

- April 2025: Plug Power and Olin's joint venture, Hidrogenii, has commissioned a 15 t/d hydrogen liquefaction plant in St. Gabriel, Louisiana, significantly increasing Plug Power's total hydrogen production capacity to 40 t/d.

- January 2025: Dover's PSG division has acquired Cryogenic Machinery Corp (Cryo-Mach), expanding its presence in the cryogenic pump market. Cryo-Mach specializes in cryogenic centrifugal pumps, mechanical seals, and accessories, particularly for industrial gases.

- August 2024: Nikkiso Clean Energy & Industrial Gases Group is expanding its manufacturing operations in Wurzen, Germany, to double its European capacity.

Global Cryogenic Equipment Market Report Scope

The cryogenic equipment market report includes:

Segmentation Overview

| Liquid Nitrogen (LIN) |

| Liquid Oxygen (LOX) |

| Liquid Argon |

| Liquid Helium |

| Liquid Hydrogen (LH₂) |

| LNG (Methane) |

| Tanks (Cryogenic storage tanks, Dewars and cylinders, ISO and road tank containers) |

| Pumps |

| Heat Exchangers |

| Valves and Regulators |

| Instrumentation and Controls |

| Ancillary Equipment (transfer lines, cold boxes, etc.) |

| Storage |

| Transportation and Distribution |

| Processing and Liquefaction |

| Regasification |

| R&D/Laboratory |

| Oil and Gas (upstream, midstream, LNG) |

| Energy and Power (grid-scale storage, SMR, H₂) |

| Chemicals and Petrochemicals |

| Food and Beverage |

| Healthcare and Life-Sciences |

| Electronics and Semiconductors |

| Aerospace and Defense |

| Others (Marine, Metallurgy and Metal-processing) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Gas | Liquid Nitrogen (LIN) | |

| Liquid Oxygen (LOX) | ||

| Liquid Argon | ||

| Liquid Helium | ||

| Liquid Hydrogen (LH₂) | ||

| LNG (Methane) | ||

| By Equipment | Tanks (Cryogenic storage tanks, Dewars and cylinders, ISO and road tank containers) | |

| Pumps | ||

| Heat Exchangers | ||

| Valves and Regulators | ||

| Instrumentation and Controls | ||

| Ancillary Equipment (transfer lines, cold boxes, etc.) | ||

| By Application | Storage | |

| Transportation and Distribution | ||

| Processing and Liquefaction | ||

| Regasification | ||

| R&D/Laboratory | ||

| By End-user Industry | Oil and Gas (upstream, midstream, LNG) | |

| Energy and Power (grid-scale storage, SMR, H₂) | ||

| Chemicals and Petrochemicals | ||

| Food and Beverage | ||

| Healthcare and Life-Sciences | ||

| Electronics and Semiconductors | ||

| Aerospace and Defense | ||

| Others (Marine, Metallurgy and Metal-processing) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Global Cryogenic Equipment market?

The Global Cryogenic Equipment market size reached USD 27.59 billion in 2026 and is projected to grow to USD 37.64 billion by 2031.

Which gas segment is growing fastest?

Liquid hydrogen records the fastest expansion, advancing at a 9.95% CAGR through 2031 as large-scale green-hydrogen liquefiers come onstream.

Why are pumps growing quicker than other equipment categories?

Specialized cryogenic pumps benefit from efficiency upgrades and consolidation moves like Dover’s acquisition of Cryogenic Machinery Corp, resulting in an 8.18% CAGR forecast.

Which region dominates demand?

Asia-Pacific leads, holding 42.30% Global Cryogenic Equipment market share in 2025 due to aggressive LNG terminal builds and semiconductor manufacturing investments.

How will safety regulations affect future projects?

Stringent codes such as NFPA 59A and EU pressure-equipment rules extend approval timelines and raise compliance costs, reinforcing the advantage of experienced suppliers.

Page last updated on: