Crawler Camera System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 305.5 Million |

| Market Size (2031) | USD 436.36 Million |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

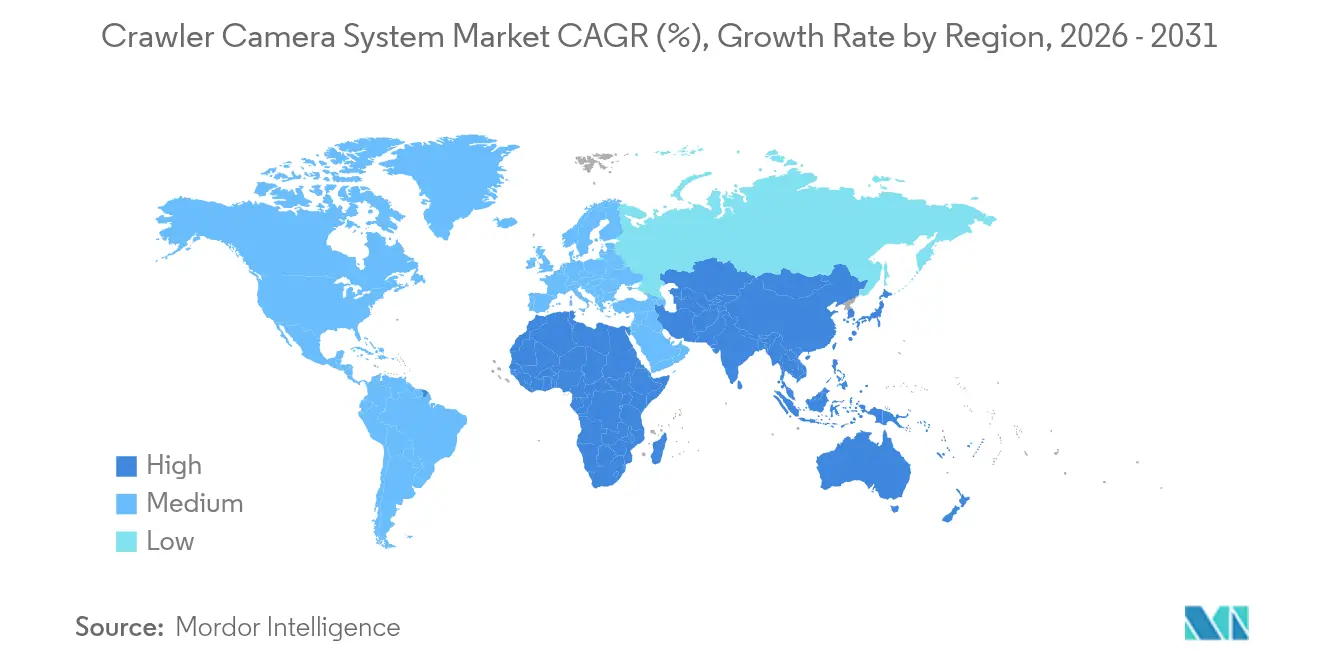

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

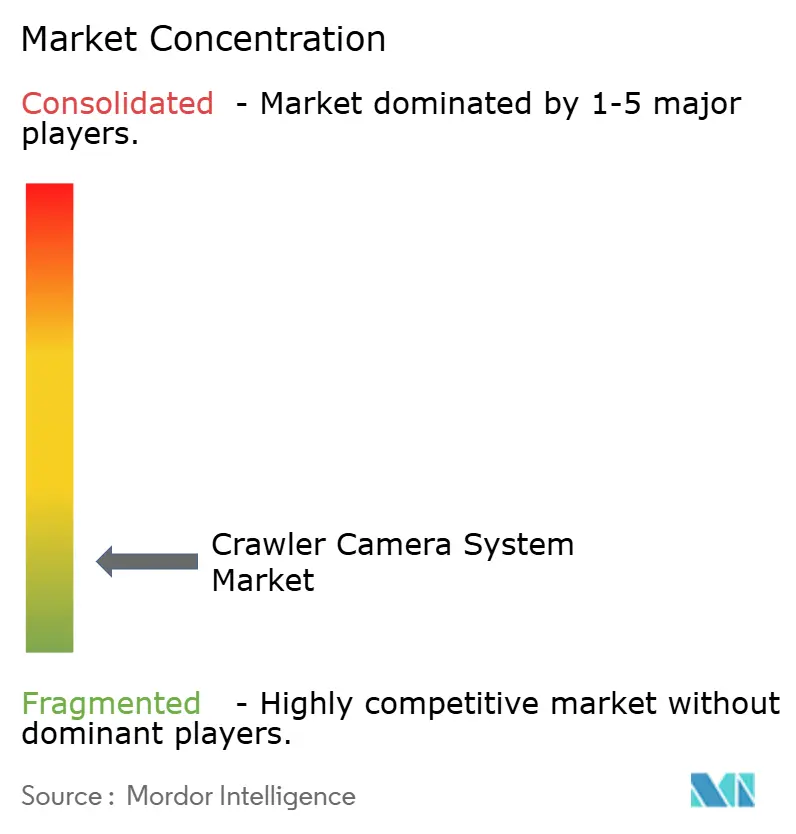

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crawler Camera System Market Analysis by Mordor Intelligence

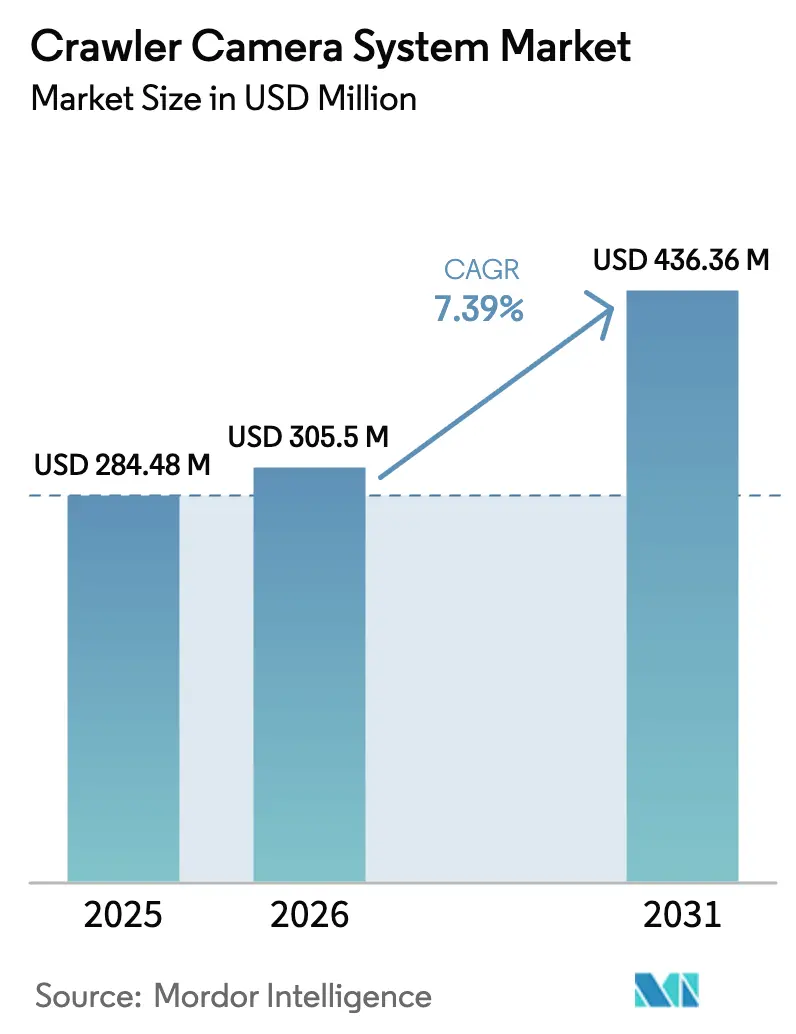

The crawler camera system market size is expected to grow from USD 284.48 million in 2025 to USD 305.5 million in 2026 and is forecast to reach USD 436.36 million by 2031 at 7.39% CAGR over 2026-2031. Growth stemmed from large-scale pipeline rehabilitation programs, stricter inspection mandates under regulations such as the Clean Water Act, and continual advances in high-definition imaging that improve defect detection accuracy. Municipal utilities continued to account for the bulk of demand, yet oil and gas operators accelerated deployments to safeguard remote transmission lines against leaks and third-party damage. Hardware platforms remained the revenue backbone, but software innovation around AI-powered analytics transformed inspection workflows and drove a double-digit expansion in recurring license revenue. Competitive intensity rose as established vendors integrated autonomy and cloud connectivity while start-ups targeted niche use cases in nuclear decommissioning and confined-space asset monitoring.

Key Report Takeaways

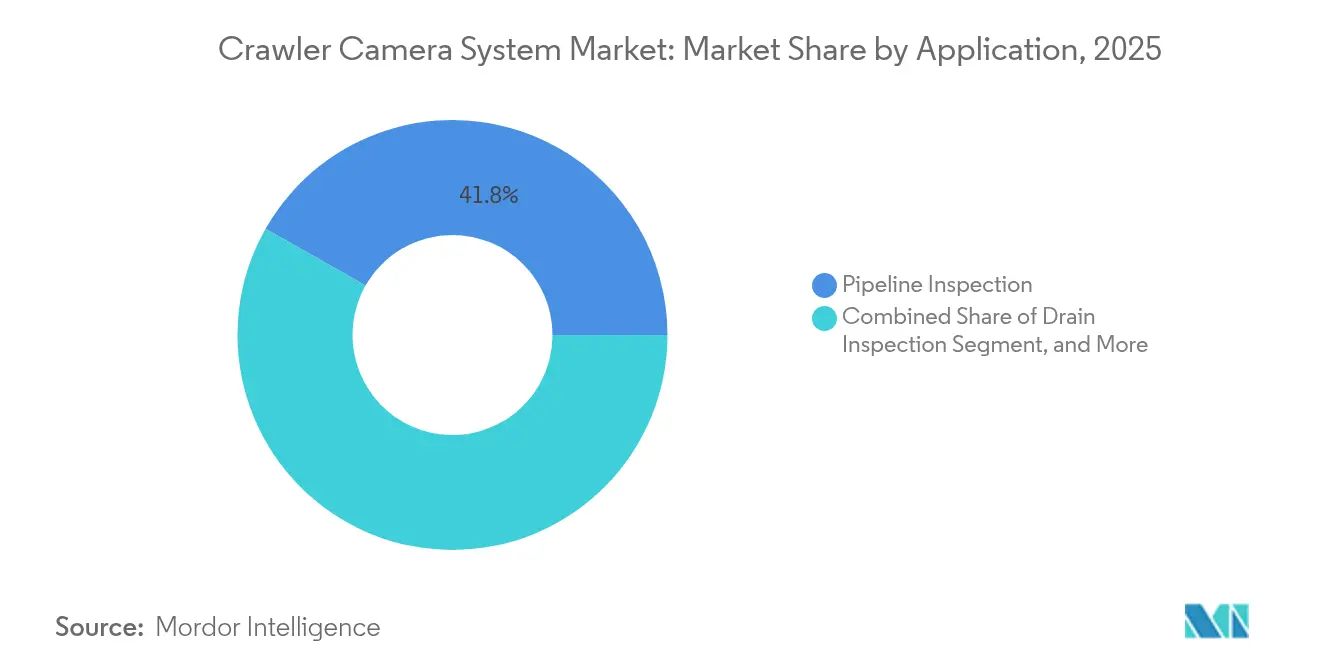

- By application, pipeline inspection commanded 41.78% of crawler camera system market share in 2025, while nuclear power-plant inspection is forecast to advance at a 11.9% CAGR through 2031.

- By end-user, municipal operators held 47.62% share of the crawler camera system market in 2025, whereas oil and gas is projected to expand at an 11.38% CAGR to 2031.

- By component, hardware led with 63.65% revenue share in 2025; software is poised for the fastest growth at 13.95% CAGR through 2031.

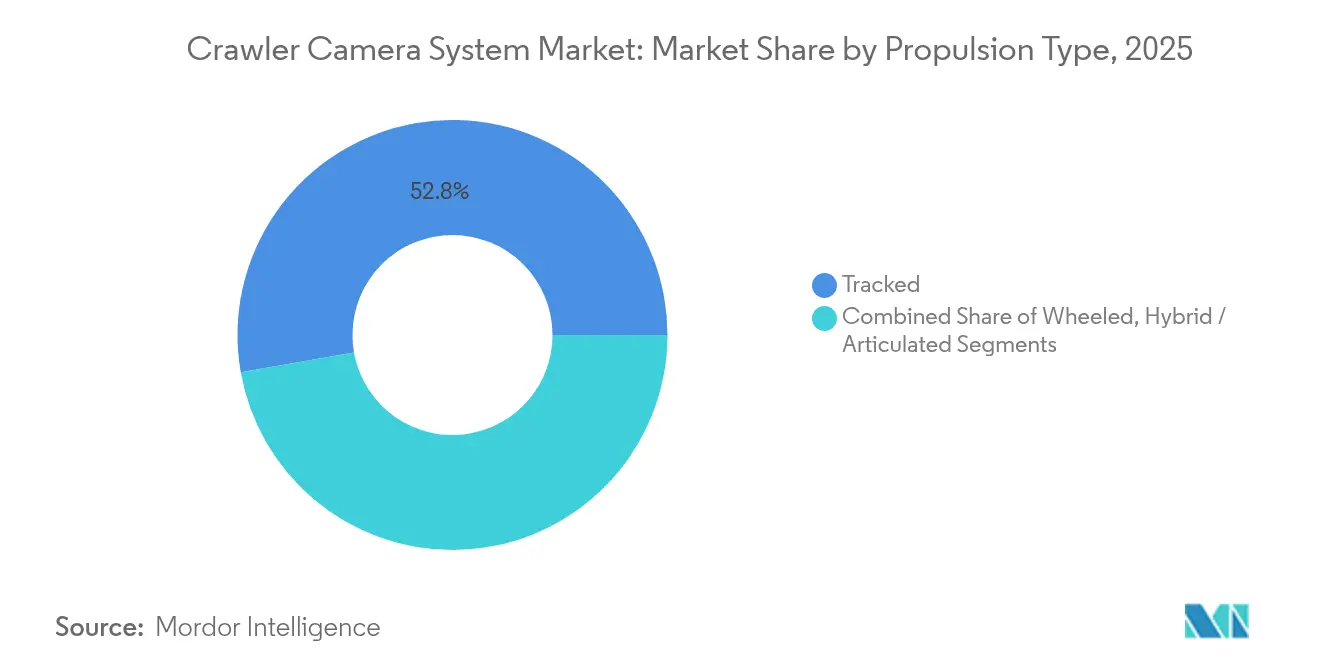

- By propulsion type, tracked systems accounted for 52.78% share of the crawler camera system market in 2025, while hybrid and articulated designs are set to rise at 12.82% CAGR.

- By camera diameter, 101-200 mm solutions retained 45.71% share in 2025; >300 mm systems are projected to grow at a 10.05% CAGR through 2031.

- By geography, North America dominated with 36.88% share in 2025, and Asia-Pacific is anticipated to deliver the highest regional CAGR of 9.86% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Crawler Camera System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating pipeline rehabilitation and replacement projects | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Stringent regulatory mandates for municipal sewer inspections | +1.2% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Growing adoption in oil and gas remote pipeline monitoring | +1.5% | Global, with early gains in North America, Middle East | Short term (≤ 2 years) |

| Advancements in high-definition and 3D imaging for confined spaces | +0.9% | Global | Medium term (2-4 years) |

| Decommissioning of aging nuclear facilities needing RVI | +0.7% | North America, Europe, Japan | Long term (≥ 4 years) |

| AI-based defect classification enabling predictive maintenance | +1.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Pipeline Rehabilitation and Replacement Projects

Pipeline owners in North America and Europe accelerated inspection schedules as mid-20th-century networks neared the end of design life. The American Society of Civil Engineers valued water and wastewater investment needs at USD 434 billion through 2029, a figure that continued to spotlight proactive condition assessment. Utilities therefore expanded crawler fleets to capture high-resolution images that guide asset-life extension decisions. CUES Inc. documented measurable reductions in sanitary sewer overflows after municipalities adopted robotic CCTV for annual programs. [1]CUES Inc., “CCTV Inspection in Municipal Sewer Systems,” cuesinc.com The trend bolstered hardware refresh cycles and spurred demand for multi-sensor payloads that cut field revisit rates. As capital budgets aligned with rehabilitation funding, the crawler camera system market saw steady order pipelines from city agencies and public-private partnerships.

Stringent Regulatory Mandates for Municipal Sewer Inspections

Compliance frameworks such as the National Pollutant Discharge Elimination System compelled U.S. cities to verify pipe integrity on defined cycles. Similar requirements in the European Union’s Urban Waste Water Directive extended the discipline to member states. Vendors highlighted that CCTV evidence formed the backbone of regulatory reporting packages, helping utilities avoid penalties exceeding USD 50,000 per day of violation. Proposed Transportation Security Administration rules on cyber risk management added secure-data-handling benchmarks that favored systems with encrypted telemetry channels. The cumulative effect of these rules enlarged the addressable market for compliant inspection robots capable of authenticated data transfer and tamper-proof audit trails.

Growing Adoption in Oil and Gas Remote Pipeline Monitoring

Midstream operators expanded remote visual inspection to control emissions and maintain throughput on aging long-distance lines. Baker Hughes cited more than 2 million km of pipelines inspected across five decades, underpinning the business case for continuous integrity management. Integration of crawler bots with fiber-optic sensors and unmanned aerial vehicles delivered multi-layer threat detection while containing operational costs. SLB deployed monitoring solutions over 5,500 km of assets, illustrating rising acceptance of automated diagnostics at scale. Early adopters in North America and the Middle East influenced global procurement standards, fostering segment growth that outpaced traditional municipal buying cycles.

Advancements in High-Definition and 3D Imaging for Confined Spaces

Imaging technology underwent rapid refinement as utilities requested survey-grade deliverables. IBAK’s PANORAMO 4K platform produced immersive 3D scans that accelerated desktop condition rating by up to 50%. Videology noted a shift from standard definition to full-HD as contract specifications demanded distortion-free evidence for trenchless rehabilitation design. Sensor convergence introduced thermal, LiDAR, and gas-detection modules, unlocking cross-discipline inspections inside tunnels and chemical plants. Deep-learning algorithms underpinned automatic crack classification, reducing analyst workload and standardizing defect coding across jurisdictions. These imaging breakthroughs elevated end-user expectations and justified premium system pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial procurement cost of robotic crawler platforms | -0.8% | Global, more pronounced in developing markets | Short term (≤ 2 years) |

| Limited maneuverability in complex pipe geometries | -0.6% | Global | Medium term (2-4 years) |

| Shortage of certified robotic inspection operators | -0.4% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Cyber-security risks in remote inspection data transmission | -0.5% | Global, heightened in critical infrastructure sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Procurement Cost of Robotic Crawler Platforms

Acquisition prices for advanced inspection robots ranged from USD 15,000 to USD 200,000 depending on torque, sensor load-out, and cable length. Smaller municipalities and contractors faced capital constraints that delayed system upgrades. Service models evolved as vendors introduced Robots-as-a-Service packages, enabling monthly access fees that bundled maintenance and software updates. Low-cost robotics ecosystems such as igus RBTX broadened entry-level options at USD 2,500, signalling longer-term erosion of price barriers. Yet, short-term budget cycles continued to influence tender timing, marginally tempering overall market growth.

Limited Maneuverability in Complex Pipe Geometries

Conventional tracked or wheeled chassis struggled with 90-degree bends, diameter changes, and heavy debris loads common in legacy sewer networks. Research prototypes based on snake-like articulation navigated 30 mm apertures during UK nuclear clean-up trials, demonstrating a path toward improved mobility. Hybrid propulsion platforms that blended wheels with articulated joints captured a 13.5% CAGR as utilities experimented with more flexible form factors. Advances in path-planning algorithms reduced stall events, but complex geometry still posed a practical limit for mass-market devices, especially when operators lacked robotics expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Nuclear Inspection Drives Specialized Growth

Nuclear power-plant inspection displayed the fastest segment CAGR of 11.9% through 2031 as utilities relied on remote visual inspection robots to cut radiation exposure during outage work. The crawler camera system market size allocation to nuclear assets remained modest in absolute terms, yet the heightened safety value proposition anchored premium pricing and multi-year service contracts. Westinghouse Electric Company’s Gemini Robotic Delivery System shortened reactor vessel head surveys by more than 30%, reinforcing confidence in automated methods.

Pipeline inspection continued to dominate revenue with a 41.78% share in 2025, driven by vast global pipeline mileage and mandatory integrity verification regimes. Multi-sensor crawlers that combined HD video with laser profiling stood out for their ability to quantify ovality and root intrusion in a single pass. Emerging use cases such as industrial boiler tubes, marine ballast tanks, and storage cavities broadened application diversity, signaling sustained demand beyond mainstream water and wastewater networks.

By End-User: Oil and Gas Accelerates Despite Municipal Dominance

Municipal agencies held 47.62% of demand in 2025, reflecting statutory responsibilities to maintain public sewer and stormwater assets. Budgeted capital improvement plans kept replacement cycles predictable, and procurement policies favored vendors with domestic support centers. The crawler camera system market size for municipal utilities is projected to expand steadily alongside infrastructure funding bills.

Oil and gas operators demonstrated the highest end-user growth at 11.38% CAGR. Inline inspection giants such as Baker Hughes validated the performance of robotic crawlers for localized excavation decisions, complementing pigging programs with visual evidence. The sector’s environmental, social, and governance metrics pressured asset owners to document leak prevention, making advanced visual inspection integral to pipeline stewardship strategies.

By Component: Software Innovation Transforms Traditional Hardware Focus

Hardware accounted for 63.65% of revenue in 2025, as cameras, LED lighting arrays, and drivetrain assemblies formed the backbone of each sale. However, the crawler camera system industry pivoted toward analytics platforms that turned raw footage into actionable maintenance schedules. CUES Inc.’s GraniteNet suite integrated defect libraries, GIS maps, and work-order interfaces, setting a template for data-driven asset management.

Software posted a 13.95% CAGR through 2031 as subscription models gained traction. AI classifiers that flag joint offsets or corrosion in real-time reduced video review labor by up to 70%, creating a compelling return on investment. Service revenue also climbed as owners outsourced periodic surveys and relied on vendors to supply crews, hardware, and cloud analysis.

By Propulsion Type: Hybrid Systems Challenge Tracked Dominance

Tracked units maintained 52.78% market share in 2025 thanks to traction consistency across silted, slippery, or egg-shaped conduits. Their simple mechanical design eased maintenance and operator training. Nonetheless, complex interceptor sewers and nuclear steam generator pathways exposed maneuverability limits, sparking interest in hybrid and articulated robots that blended wheel speed with jointed flexibility.

Hybrid platforms, projected to grow at 12.82% CAGR, showed promising field results in pipes with diameter transitions or tight bends. Six-wheel drive chassis with auto-level cameras such as the RX130 improved obstacle negotiation while keeping the system footprint compact. Ongoing R&D in soft-robotics tracks and magnetic adhesion foretells further propulsion diversification.

By Camera Diameter Range: Large Diameter Systems Gain Traction

Systems designed for 101-200 mm pipes retained a dominant 45.71% share in 2025 because most urban sewers fall within that span. They balanced weight, lighting power, and cable drag for long runs under streets without manhole enlargement. Demand rose for >300 mm solutions at a 10.05% CAGR as water utilities, petrochemical plants, and power stations scheduled inspections of high-flow trunk lines.

Manufacturers responded with modular heads that accepted interchangeable lenses, fiber lasers, and gas sensors to suit wide-bore conditions. Smaller ≤100 mm robots supported building laterals and industrial condensate lines, illustrating the market’s broadening diameter coverage.

Geography Analysis

North America accounted for 36.88% of crawler camera system market revenue in 2025. Municipal sewer operators remained the principal buyers, governed by Clean Water Act inspection requirements that mandated periodic CCTV verification. Federal infrastructure programs and proposed cyber-risk mandates for energy pipelines added momentum to procurement budgets. Vendor service networks across the United States and Canada facilitated rapid equipment deployment, fostering long-term service contracts and upgrade paths.

Asia-Pacific delivered the fastest regional CAGR of 9.86% through 2031 as metropolitan expansion and industrial diversification intensified asset monitoring needs. Japan’s launch of the Swimmy Eye water drone showed local ingenuity in adapting robotic inspection to dense sewer grids. Government smart-city schemes in China and India earmarked funds for underground asset digitization, encouraging municipal partnerships with domestic integrators. South Korean component makers such as Samsung Electro-Mechanics and LG Innotek invested in high-resolution robotic camera modules that could spill over into pipe-inspection use cases.

Competitive Landscape

The crawler camera system market remained moderately fragmented in 2025. Established names such as CUES Inc., Deep Trekker, iPEK International, and Envirosight balanced broad portfolios with localized after-sales support. Continuous R&D spending focused on integrating autonomy, multi-sensor payloads, and cloud analytics to defend share against niche disruptors. Rising entrants targeted high-risk environments, including nuclear decommissioning robots capable of teleoperation beyond 100 m and subsea crawlers rated for 1,200 m depth. [4]Ocean Robotics Planet, “Nauticus Robotics Tests Aquanaut Mk2 Vehicle,” oceanroboticsplanet.com

Strategic alliances shaped supplier roadmaps. VideoRay partnered with Sarcos Robotics, Vaarst, and Greensea Systems to pair remotely operated vehicles with machine-vision analytics for offshore structures . Kraken Robotics completed a USD 24.5 million acquisition of 3D at Depth that expanded its subsea 3D imaging capabilities and opened cross-selling avenues to energy clients. Vendors also refined Robots-as-a-Service offerings to meet budget-constrained buyers, bundling hardware, AI software, and certified operators into subscription plans.

Innovation hubs emphasized AI defect libraries that improved with every inspection run. Predictive maintenance dashboards alerted asset owners to emerging risks, shortening repair cycles and underscoring software’s central role in competitive differentiation. Heightened cyber-security expectations from critical-infrastructure operators spurred encryption, user-authentication, and zero-trust architecture adoption, creating new service revenue tied to compliance assurances.

Crawler Camera System Industry Leaders

CUES Inc.

Deep Trekker Inc.

iPEK International GmbH

Envirosight LLC

Rausch Electronics USA LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Samsung Electro-Mechanics and LG Innotek announced plans to mass-produce humanoid robot camera modules by 2026.

- March 2025: Kraken Robotics finalized a USD 24.5 million takeover of 3D at Depth to unify subsea robotics with advanced LiDAR imaging.

- February 2025: Energy Robotics outlined substation inspection pilots that leveraged mobile robots and AI analytics.

- January 2025: NTT DATA, ITOCHU Techno-Solutions, and Mitsubishi Chemical Group validated 120 km real-time robotic inspections over an all-photonics network.

Global Crawler Camera System Market Report Scope

Crawler cameras are robust remotely controlled inspection robots that traverse through a pipe on wheels. These can maneuver inside narrow and rugged pipelines to detect cracks, corrosion or blockages.

The crawler camera system market is segmented by application (drain inspection, pipeline inspection, (tank, void, and conduit/cavity inspection)), by end-user (industrial, commercial, municipal, residential), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Drain Inspection |

| Pipeline Inspection |

| Tank/Void/Cavity Inspection |

| Nuclear Power-Plant Inspection |

| Industrial Boiler Inspection |

| Marine Vessel Ballast-Tank Inspection |

| Industrial |

| Commercial |

| Municipal |

| Residential |

| Oil and Gas |

| Utilities |

| Hardware |

| Software |

| Services |

| Wheeled |

| Tracked |

| Hybrid / Articulated |

| ≤100 mm |

| 101-200 mm |

| 201-300 mm |

| >300 mm |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application | Drain Inspection | ||

| Pipeline Inspection | |||

| Tank/Void/Cavity Inspection | |||

| Nuclear Power-Plant Inspection | |||

| Industrial Boiler Inspection | |||

| Marine Vessel Ballast-Tank Inspection | |||

| By End-user | Industrial | ||

| Commercial | |||

| Municipal | |||

| Residential | |||

| Oil and Gas | |||

| Utilities | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Propulsion Type | Wheeled | ||

| Tracked | |||

| Hybrid / Articulated | |||

| By Camera Diameter Range | ≤100 mm | ||

| 101-200 mm | |||

| 201-300 mm | |||

| >300 mm | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the crawler camera system market?

The crawler camera system market size stood at USD 305.5 million in 2026 and is forecast to reach USD 436.36 million by 2031.

Which application segment grows the fastest?

Nuclear power-plant inspection is projected to register the quickest pace with a 11.9% CAGR through 2031 thanks to strict safety protocols in high-radiation environments.

Why are hybrid propulsion systems gaining popularity?

Hybrid and articulated robots, growing at 12.82% CAGR, offer superior maneuverability in pipes with sharp bends and diameter changes that traditional tracked devices cannot navigate effectively.

How do regulatory mandates influence market adoption?

Rules under the Clean Water Act and similar EU directives require periodic CCTV inspections, compelling municipal agencies to invest in crawler camera systems or face financial penalties for non-compliance.

What role does software play in the market’s future?

AI-enabled inspection platforms that automate defect classification and integrate with GIS systems are expanding at 13.95% CAGR, transforming hardware-only models into data-driven service offerings.

Which region is expected to post the highest growth rate?

Asia-Pacific is poised to record a 9.86% CAGR through 2031, supported by rapid urbanization and government infrastructure initiatives in countries such as Japan, China, and India.

Page last updated on: