Core Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

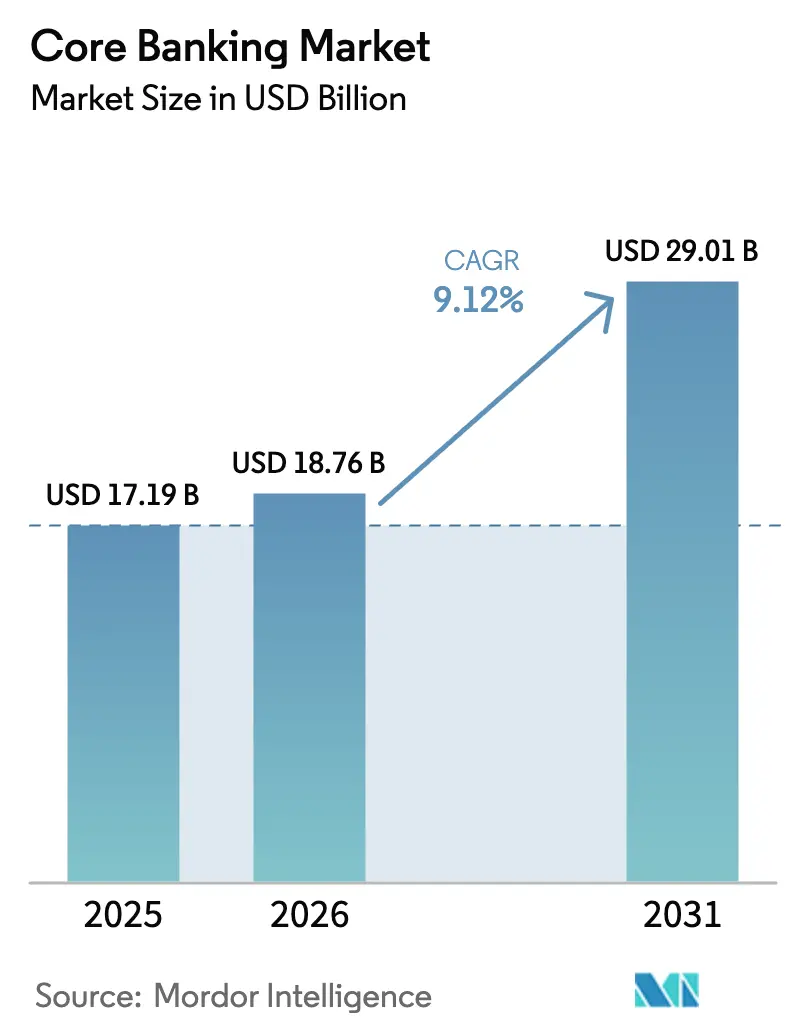

| Market Size (2026) | USD 18.76 Billion |

| Market Size (2031) | USD 29.01 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

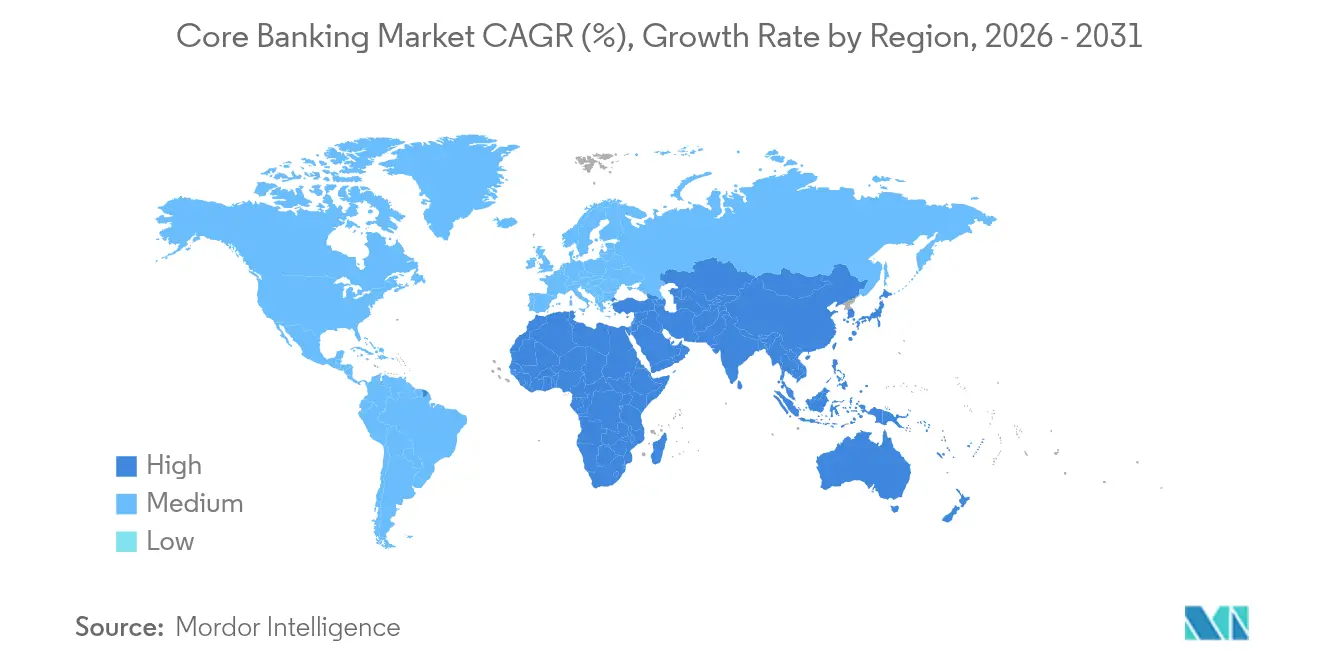

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Core Banking Market Analysis by Mordor Intelligence

The core banking market size is expected to grow from USD 17.19 billion in 2025 to USD 18.76 billion in 2026 and is forecast to reach USD 29.01 billion by 2031 at 9.12% CAGR over 2026-2031. Bank executives see modern, API-driven platforms as critical to competing with digital-first challengers, and many institutions are timing transformation programs around pending mainframe end-of-support deadlines. Asia-Pacific’s double-digit expansion, real-time payment mandates in North America, and hyperscaler incentives worldwide are accelerating demand for cloud-native and micro-services-based cores. At the same time, talent shortages in COBOL-to-Java re-platforming, data-residency requirements, and vendor lock-in concerns are forcing many banks to adopt phased or hybrid modernization strategies. Intensifying rivalry between incumbents and cloud-only providers is widening the solution spectrum but heightening due-diligence requirements for long-term flexibility.

Key Report Takeaways

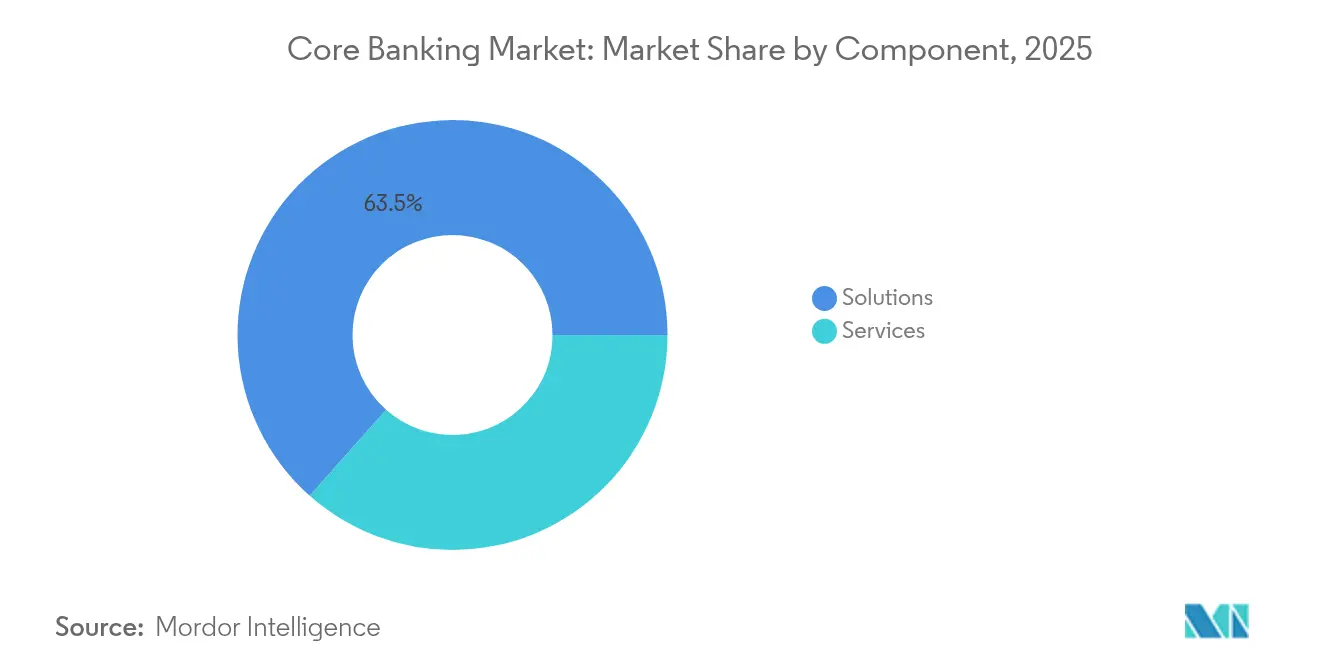

- By component, Solutions commanded 63.45% of core banking market share in 2025, while Services are forecast to expand at a 12.12% CAGR to 2031.

- By deployment mode, on-premise held 70.20% share of the core banking market size in 2025; cloud is projected to grow at a 16.7% CAGR between 2026-2031.

- By solution type, Retail Banking Cores led with 45.30% revenue share in 2025; Corporate/Commercial Banking Cores are advancing at a 12.05% CAGR through 2031.

- By end-user, banks held 73.20% share of the core banking market in 2025, while fintechs and other non-banks are set to expand at a 14.78% CAGR to 2031.

- By geography, North America accounted for 31.70% of the core banking market size in 2025; Asia-Pacific is forecast to register the highest regional CAGR at 13.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Core Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open-API Regulations Accelerating Core Modernisation in Europe and APAC | +2.1% | Europe, Asia-Pacific, with spillover to North America | Medium term (2-4 years) |

| Real-time Payments (ISO 20022, FedNow) Driving Micro-services Adoption in North America | +1.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Neobank Proliferation in Emerging Asia and LatAm Fuelling SaaS Core Demand | +1.5% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Mainframe End-of-Support (2027-29) Prompting Core Replacement in Tier-1 Banks | +1.3% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Hyperscaler Migration Incentives (AWS, Azure) Lowering TCO for Cloud Cores | +1.2% | Global | Short term (≤ 2 years) |

| Expansion of Sharia-Compliant Banking in GCC Requiring Dedicated Core Modules | +0.7% | Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Open-API Regulations Accelerating Core Modernisation in Europe and APAC

Open-banking directives such as PSD2 in Europe and parallel frameworks in Singapore and Australia are compelling 80% of regional institutions to expose services through standardized APIs, pushing legacy cores toward obsolescence. [1] Basel Committee on Banking Supervision, “Report on Open Banking and Application Programming Interfaces,” bis.org Banks are prioritizing API-first replacements to capture ecosystem revenues, yet must also build governance frameworks to mitigate new liability risks around data sharing.

Real-Time Payments Driving Micro-services Adoption in North America

FedNow’s launch and raised transaction ceilings have encouraged 84% of US banks to predict a 23% rise in instant-payment volumes over three years, prompting investment in cores that process ISO 20022 messages 24/7. [2]RedCompass Labs, “RTP and FedNow Limit Increases Surge in Instant Payments,” thepaypers.com Componentized architectures enable faster feature rollouts, positioning innovators to monetize value-add payment services.

Neobank Proliferation in Emerging Asia and LatAm Fuelling SaaS Core Demand

Digital-only banks are scaling rapidly in markets with large unbanked populations. SaaS cores allow these entrants to sidestep heavy capex, and academic research shows efficiency gains accrue over time despite upfront costs. Regulators are monitoring systemic risk, but for vendors, the addressable customer base continues to widen.

Mainframe End-of-Support Prompting Core Replacement in Tier-1 Banks

Support sunsets between 2027-2029 and rising COBOL maintenance costs are forcing global Tier-1 institutions to plot modernization roadmaps now. The shrinking pool of COBOL specialists increases operational risk, intensifying the financial case for migration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity in US Regional Banks | -1.4% | North America, with moderate impact in Europe | Medium term (2-4 years) |

| Scarcity of COBOL-to-Java Re-platforming Skills | -1.2% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Data-Residency Rules Slowing Public-Cloud Roll-outs in Africa | -0.8% | Africa, with spillover to Middle East | Medium term (2-4 years) |

| Proprietary-Architecture Vendor Lock-in Concerns | -1.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity in US Regional Banks

A majority of mid-sized US institutions remain tied to incumbent providers despite sub-par satisfaction scores, delaying modernization because of high integration risk. Opportunity costs mount as outdated systems inflate operating expenses and limit product agility.

Scarcity of COBOL-to-Java Re-platforming Skills

Retirement of veteran programmers has created a bottleneck: 43% of companies still run critical workloads on COBOL codebases. Banks compete for scarce talent or rely on service partners, stretching project timelines and budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Solutions in Growth Race

Services revenue is forecast to rise at 12.12% CAGR as institutions prioritize implementation expertise for complex migrations, while Solutions retain 63.45% of 2025 spend. Managed-services uptake is also fuelled by talent scarcity noted by industry associations. The core banking market size for services is therefore expanding faster than product sales, signalling that execution capability is becoming the primary differentiator. Consultancy-led models reduce project risk, help banks navigate compliance, and free internal staff for higher-value tasks. Simultaneously, software vendors are embedding low-code tools and composable components to shorten deployment cycles, sustaining solution demand even as banks allocate larger budgets to partners. Cost-efficient subscription models and outcome-based contracts further strengthen the services growth trajectory.

By Deployment Mode: Cloud Acceleration Reshapes Banking Infrastructure

On-premise still owns 70.20% of installations in 2025 because mission-critical workloads and regulatory scrutiny favour direct control. Yet cloud’s 16.7% CAGR shows that decision-makers now view elasticity and rapid feature delivery as strategic. Larger institutions increasingly pursue multi-cloud or hybrid strategies to balance data-residency and lock-in risks. Hyperscalers’ sector-specific regions and compliance overlays remove major hurdles for moving core workloads, while containerisation brings cloud-like agility to private data centres. The core banking market share of cloud deployments will therefore continue to climb, although recent workload repatriations highlight a maturing cost–benefit calculus. Going forward, orchestration platforms capable of unifying on-premise and cloud components are set to gain traction.

By Solution Type: Corporate Banking Cores Gain Momentum

Retail cores held 45.30% revenue share in 2025 owing to high consumer transaction volumes, yet the corporate segment’s 12.05% CAGR underscores rising demand for sophisticated treasury and trade-finance capabilities. Commercial clients expect real-time cash-flow analytics, configurable loan products, and seamless cross-border services, driving banks to modernize corporate cores ahead of retail upgrades. Advanced analytics embedded in the new platforms improve risk management and enable personalized advisory propositions. Retail cores are also evolving, integrating AI-driven personal financial management to retain customer loyalty. Overall, solution providers that can harmonize retail and corporate modules within a single architecture are likely to capture disproportionate growth.

By End-User: Non-Bank Entities Disrupt Traditional Paradigm

Banks controlled 73.20% of 2025 deployments, but fintechs, payment processors, and embedded-finance providers are set to register 14.78% CAGR. These firms need robust core capabilities without the overhead of a banking charter, turning to modular SaaS offerings for fast market entry. The Bank for International Settlements observes that partnerships between tech companies and licensed banks are re-defining service delivery. Treasury Prime’s collaboration with KeyBank demonstrates the strategy: embedded-finance specialists tap regulated balance sheets, while banks monetize API infrastructure. As regulation evolves, platform providers offering compliance-ready environments for non-banks will gain competitive advantage.

Geography Analysis

North America generates 31.70% of core banking market revenue, anchored by urgent legacy-modernization programs among regional and community banks. FedNow’s push for instant payments and consumer expectations for continuous service availability are shortening upgrade cycles. Survey data shows that despite mixed satisfaction with existing vendors, most banks plan incremental migrations to mitigate operational risk, boosting services revenue. Talent shortages in legacy languages and escalating mainframe costs further reinforce the modernization mandate.

Asia-Pacific is the fastest-growing region with a 13.02% CAGR to 2031, fuelled by rapid digitisation, financial-inclusion initiatives, and regulatory support for open banking. Regional banks expand into underserved segments using cloud-native cores, while global hyperscalers build local data centres to meet sovereignty requirements. Japanese and South Korean institutions are targeting Southeast Asian markets for growth, often through digital subsidiaries.

The Middle East and Africa is witnessing accelerated digital-bank launches and a surge in Islamic-finance adoption. Banks are investing in Sharia-compliant modules to tap projected USD 7.5 trillion in Islamic assets by 2028. Meanwhile, African institutions navigate strict data-residency frameworks that necessitate hybrid deployment models, gradually expanding to full cloud as local compliance infrastructure matures. Overall, regional diversification of vendor footprints and tailored compliance offerings are unlocking new addressable markets.

Competitive Landscape

The core banking market exhibits moderate concentration. Established vendors such as Temenos, Fiserv, FIS, and Finastra maintain deep product suites and extensive service ecosystems, leveraging incremental componentization to help clients modernize without wholesale replacement. FIS advocates for modular migration as a lower-risk, lower-cost pathway. Cloud-native challengers—Thought Machine, Mambu, and others—differentiate through micro-services architectures and rapid update cycles, winning greenfield neobank deployments and selective brownfield migrations targeting specific product lines.

White-space opportunities are emerging in specialized verticals like Islamic banking and embedded finance. Tuum’s rapid expansion of its Islamic suite illustrates how focused functionality can unlock high-growth niches. Vendor strategy increasingly revolves around platform openness: API marketplaces and pre-integrated fintech connectors are becoming table stakes for large RFPs. Meanwhile, the Kansas City Federal Reserve notes that core providers are pivotal in enabling instant-payment services for community banks. [3]Kansas City Federal Reserve, “The Role of Core Banking Services Providers in Facilitating Instant Payments,” kansascityfed.org

Strategic moves in 2025 further underscore consolidation and partnership themes. Global Payments’ planned USD 22.7 billion acquisition of Worldpay expands processing scale and cross-selling capacity, while Finastra’s tie-up with i2c deepens card-issuance capabilities for mid-tier banks. nCino’s Sandbox Banking purchase enhances integration tooling, reducing time-to-value for clients. These manoeuvres signal a drive toward end-to-end digital platform breadth, positioning suppliers to capture recurring revenue across adjacent banking functions.

Core Banking Industry Leaders

Oracle Corporation

Unisys Corporation

Capgemini SE

SAP SE

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Global Payments Inc. announced agreements to acquire Worldpay for USD 22.7 billion, creating a combined entity that will serve over 6 million customers and process approximately USD 3.7 trillion in payment volume annually.

- March 2025: Finastra and i2c Inc. announced a strategic partnership to provide payment issuance solutions to North American banks and credit unions, enabling features like digital wallet support and enhanced cardholder controls through API connectivity with Finastra's Phoenix core solution.

- February 2025: nCino acquired Sandbox Banking for USD 52.5 million to enhance data connectivity and streamline operations for banks and credit unions through an Integration Platform as a Service (iPaaS), helping financial institutions overcome integration challenges and accelerate project timelines.

- February 2025: Treasury Prime expanded its bank network with KeyBank, enhancing embedded banking solutions for fintechs through a reliable platform for scalable fintech programs, leveraging KeyBank's virtual account management solution.

Global Core Banking Market Report Scope

The core banking encompasses the technological platforms that empower banks and financial institutions to efficiently handle fundamental banking operations, including deposits, withdrawals, loans, account management, payments, and a range of other services.

The study tracks the revenue accrued through the sale of core banking solutions by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The core banking market is segmented by component (solution and services), deployment mode (on-premise and cloud), end-user (banks, financial institutions, and others), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Solutions |

| Services |

| On-premise |

| Cloud |

| Retail Banking Core |

| Corporate / Commercial Banking Core |

| Other Solution Types |

| Banks |

| Non-Bank Financial Institutions |

| Other End-users (FinTechs, Payment Institutions) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Component | Solutions | |

| Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| By Solution Type | Retail Banking Core | |

| Corporate / Commercial Banking Core | ||

| Other Solution Types | ||

| By End-User | Banks | |

| Non-Bank Financial Institutions | ||

| Other End-users (FinTechs, Payment Institutions) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving the rapid shift toward cloud deployment in the core banking market?

Regulatory-compliant hyperscaler regions, lower upfront costs, and the need for continuous feature delivery are pushing banks toward cloud cores, which are forecast to grow at a 16.7% CAGR through 2031.

Why are services growing faster than solutions in the core banking industry?

Complex migrations require external implementation expertise, leading banks to allocate more budget to managed and professional services, which are projected to expand at 12.12% CAGR.

How significant is Asia-Pacific’s influence on future core banking investments?

Asia-Pacific records the highest regional CAGR at 13.02%, driven by digital-bank launches, financial-inclusion mandates, and supportive open-banking regulation.

What challenges slow modernization among US regional banks?

Integration complexity, legacy vendor contracts, and shortages in COBOL-to-Java skills deter many mid-size institutions, subtracting an estimated 1.4 percentage points from market CAGR.

How are vendors addressing Islamic-finance requirements?

Providers such as Tuum and Finastra have launched dedicated Sharia-compliant modules that automate profit-sharing and asset-backed transaction workflows to serve the USD 7.5 trillion Islamic-finance market projected for 2028.

What role do non-bank entities play in core banking market growth?

Fintechs and embedded-finance players are adopting SaaS cores to offer specialized services without full banking licenses, expanding at a 14.78% CAGR and reshaping competitive dynamics.

Page last updated on: