Payment Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

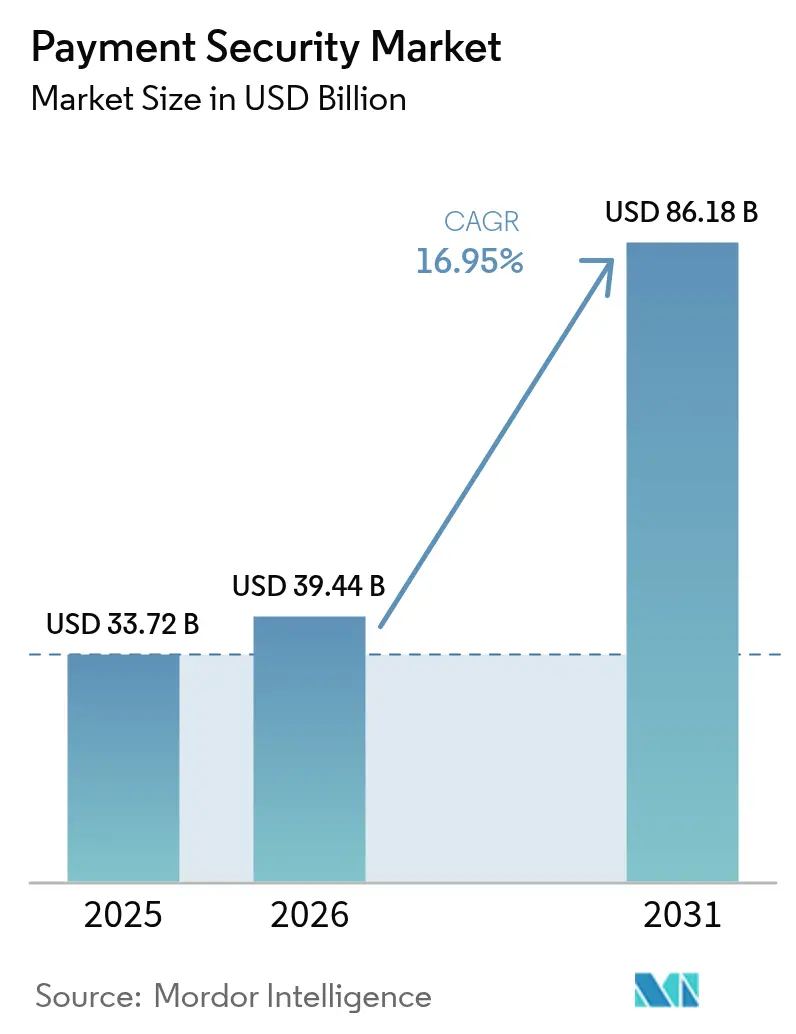

| Market Size (2026) | USD 39.44 Billion |

| Market Size (2031) | USD 86.18 Billion |

| Growth Rate (2026 - 2031) | 16.95% CAGR |

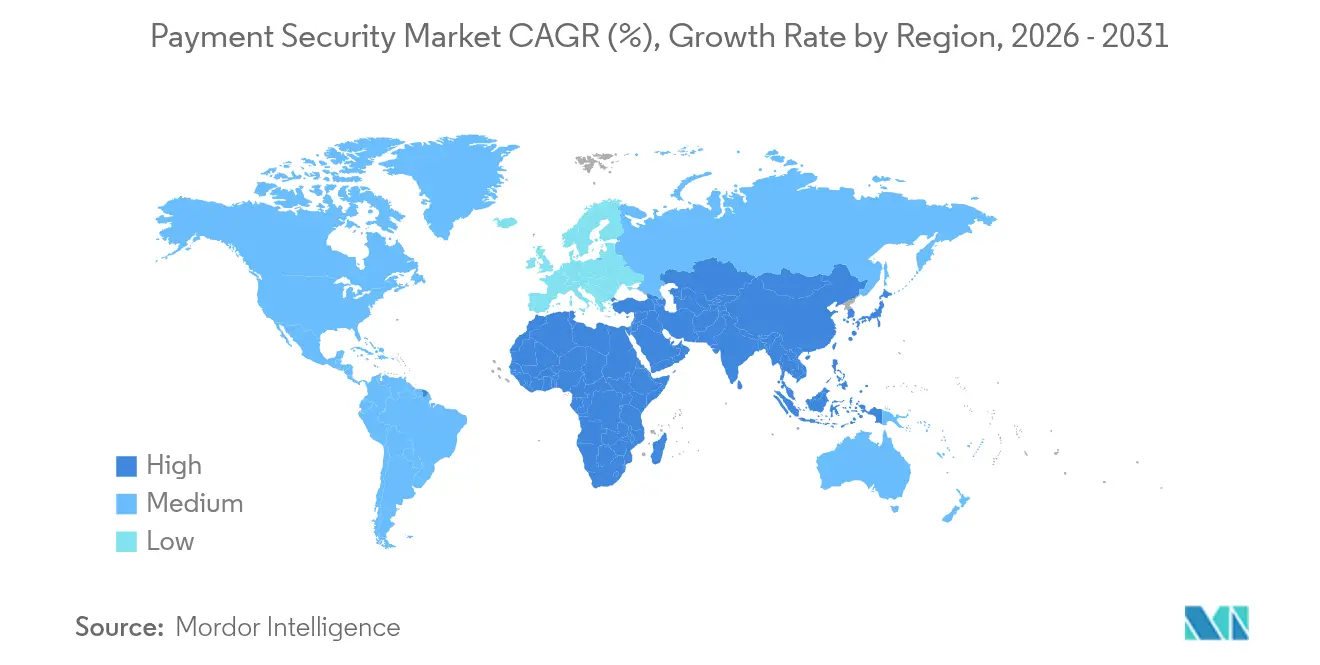

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payment Security Market Analysis by Mordor Intelligence

The payment security market size was valued at USD 33.72 billion in 2025 and estimated to grow from USD 39.44 billion in 2026 to reach USD 86.18 billion by 2031, at a CAGR of 16.95% during the forecast period (2026-2031). This solid trajectory aligns with tightening regulatory mandates, rising transaction volumes across digital channels, and continued innovation in detection technologies. Continuous compliance investments linked with the final PCI DSS 4.0 deadline, wide-scale application of artificial intelligence in fraud analytics, and the proliferation of mobile-first wallets are shaping enterprise spending priorities. Tokenization and encryption remain foundational, yet real-time behavioral analytics and multi-factor authentication are taking a larger budget share as issuers and merchants confront synthetic identity attacks. Parallel to technology upgrades, competitive consolidation among networks and processors is accelerating as firms integrate threat-intelligence platforms and expand global merchant bases to defend share in the payment security market

Key Report Takeaways

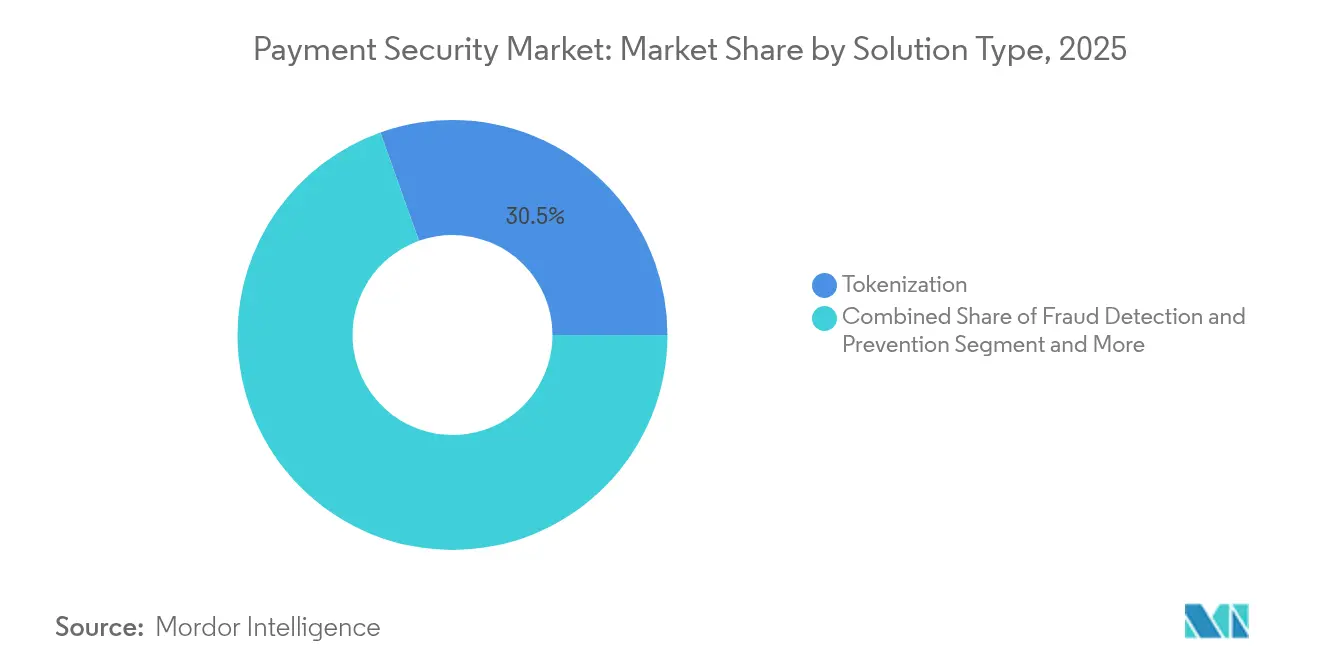

- By solution type, tokenization captured 30.45% of payment security market share in 2025, while AI-enabled fraud detection solutions are projected to expand at a 20.4% CAGR from 2026 to 2031.

- By platform, web-based deployments led with 46.20% revenue share in 2025; mobile platforms are forecast to record a 22.3% CAGR through 2031.

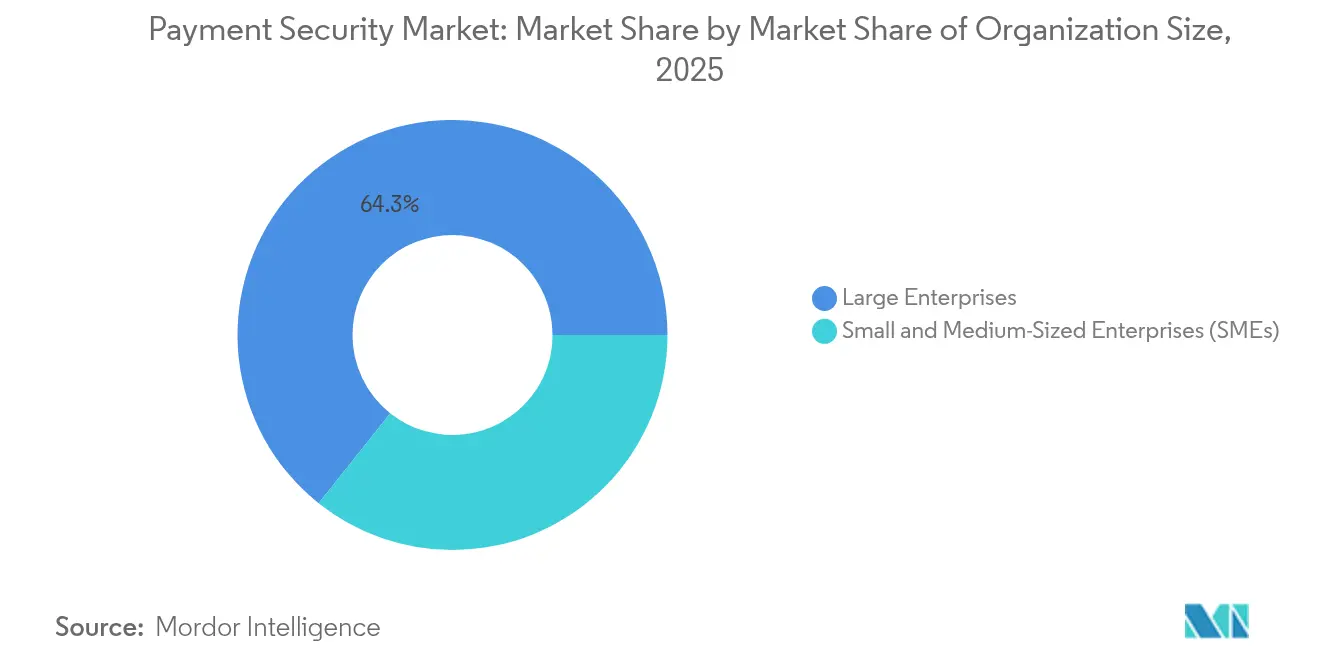

- By organization size, large enterprises commanded 64.30% of the payment security market size in 2025, whereas the SME segment exhibits a 21.9% CAGR to 2031.

- By end-user industry, retail and e-commerce held 36.40% of the payment security market size in 2025, while healthcare is advancing at a 18.7% CAGR through 2031.

- By geography, North America contributed 29.60% to the global payment security market in 2025, whereas the Middle East and Africa region is rising at a 19.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Payment Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Push for PCI-DSS 4.0 Compliance in North America | +4.2% | North America, EU spillover | Short term (≤ 2 years) |

| Surge in AI-based Fraud Analytics among Cloud Payment Processors | +3.8% | Global, concentrated in APAC & North America | Medium term (2-4 years) |

| Expansion of Buy-Now-Pay-Later (BNPL) Requiring Secure Token Vaults | +2.9% | North America, EU, emerging APAC markets | Medium term (2-4 years) |

| Rapid Growth of IoT-Enabled POS Terminals in Europe | +2.1% | Europe, North America adoption following | Medium term (2-4 years) |

| Mobile-First Wallet Boom across Emerging Asian Markets | +3.4% | APAC core, spillover to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory push for PCI DSS 4.0 compliance

Mandatory adherence to PCI DSS 4.0 beginning in March 2025 is reshaping security budgets across North America. Enterprises face annual outlays that climb to USD 250,000 at Level 1, reflecting the standard’s 64 new requirements covering continuous log analysis and payment-page script integrity. Non-compliance fines of up to USD 500,000 per month sharpen the focus on immediate remediation, prompting rapid adoption of tokenization and automated encryption services. European acquirers are already mapping PSD3 provisions to PCI controls, creating a spill-over effect that sustains investment momentum through 2027.

Surge in AI-based fraud analytics

Financial institutions increasingly pivot from rule-based engines to adaptive machine-learning models that inspect more than 100 contextual signals in real time. Visa reports that AI applications blocked USD 40 billion in fraudulent transactions during 2024, cutting false positives by 85% and improving authorization rates. Cloud processors embed these models as micro-services, allowing merchants to fine-tune risk thresholds without lengthy integrations. Emerging markets benefit from cloud scale because it removes the need for legacy on-premise infrastructure, a dynamic that supports uniform global deployment of next-generation fraud analytics.

Expansion of BNPL requiring secure token vaults

The growing use of buy-now-pay-later in sectors such as groceries and housing introduces longer exposure windows to synthetic identity fraud. Providers now deploy multilayered defenses that combine device fingerprinting with real-time biometric checks and hardened token vaults to reduce PCI scope. Heightened regulatory attention in Europe drives providers to certify vault designs that support installment splits without storing raw card data. In North America, rapid consumer uptake offsets underwriting risks, incentivizing specialized vendors to offer BNPL-specific analytics engines that flag anomalies across recurrent installment flows.

Rapid growth of IoT-enabled POS terminals

European retailers continue to roll out cellular-enabled POS terminals that self-switch across carrier networks for uninterrupted processing, mitigating Wi-Fi outages common in legacy architectures. PCI MPoC rules, covering 192 conditions for commercial off-the-shelf devices, require developers to embed cryptographic isolation zones and tamper-resistant hardware. Integrated remote-management dashboards allow acquirers to push over-the-air patches, cutting service downtime and supporting tighter key-rotation cycles. North American deployments follow as price points decline and merchants aim for uniform omnichannel experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-front Integration Costs for Small & Mid-Sized Merchants | -2.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Transaction-Latency Issues in 3-D Secure 2.2 Roll-outs | -1.9% | North America, selective EU markets | Medium term (2-4 years) |

| Fragmented & Overlapping Data-Protection Statutes in Emerging Nations | -1.6% | Emerging markets, APAC & MEA focus | Medium term (2-4 years) |

| Consumer Privacy Concerns over Behavioral Biometrics | -1.3% | Global, heightened in EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront integration costs for SMEs

Typical annual security spend for a small merchant can range from USD 5,000 to USD 50,000, an amount that strains cash flows in emerging economies where total IT budgets are modest. Complex scoping exercises push many SMEs toward bundled cloud subscriptions, yet concerns around data residency and vendor lock-in slow conversions. As a result, low-cost plug-in solutions dominate lower-volume web stores, leaving gaps in advanced risk analytics. Security vendors that can tier services according to volume thresholds are expected to capture latent SME demand once cost curves decline.

Transaction-latency issues in 3-D Secure 2.2 roll-outs

The requirement to exchange richer data fields during 3DS 2.2 challenges acquirers seeking to keep checkout times below critical drop-off thresholds. Tests in North America show added network hops increasing average authorization time by 200 milliseconds, resulting in measurable revenue leakage for high-traffic merchants. Issuer behavior further complicates roll-outs because inconsistent 3DS interpretation can lower approval ratios. Optimization efforts now focus on risk-based step-up models that reduce challenges for trusted devices while routing higher-risk sessions through biometric flows endorsed by card networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Tokenization leadership coupled with analytics acceleration

Tokenization accounted for 30.45% of payment security market share in 2025, underscoring its role in removing primary account numbers from merchant systems and shrinking audit scope. Visa processed 10 billion tokenized transactions in 2024, up 45% from the prior year, proving scalability in both in-store and e-commerce settings. Encryption remains mandatory for data-in-transit, particularly in banking and healthcare where breach disclosure rules impose heavy penalties. Fraud detection platforms that embed machine-learning pipelines are projected to expand at 20.4% CAGR, reflecting demand for adaptive controls that self-learn from evolving attack vectors. Other emerging solutions, including quantum-safe cryptography and distributed-ledger verification, currently capture niche use-cases but hold long-term upside as standards mature. Vendors able to interlink token services with AI-driven analytics create combined offerings that minimize manual review costs while keeping false positives in check. This capability supports upsell cycles, positioning integrated platforms for outsized contribution to overall payment security market revenue.

Growth across solution types will influence payment security market size forecasts, specifically by shifting spend from basic compliance tools to intelligent orchestration engines. Vendors competing on breadth rather than point functionality tend to secure longer-term contracts, especially with enterprises that favor consolidated dashboards for audit reporting. As token vault density increases inside acquirer environments, supply-chain chip shortages may hit hardware HSM refresh plans, thereby accelerating interest in virtualized key-management modules.

By Platform: Mobile momentum redefines omnichannel expectations

Web-based deployments led the payment security market in 2025 with a 46.20% share, driven by entrenched desktop shopping patterns and mature gateway integrations. However, mobile platforms are the clear growth engine at 22.3% CAGR through 2031. China already records that 82% of online baskets close via mobile wallets, while India’s UPI system enables sub-second peer-to-merchant transfers that now outpace card usage. These trends elevate requirements for biometric authentication, network-token provisioning, and device attestation directly in the app layer. As a result, security roadmaps center on building SDKs that allow merchants to orchestrate common policies across native mobile, browser, and progressive web-app flows.

Omnichannel strategies are narrowing the historical gap between card-present and card-not-present security standards. In-store tap-to-phone initiatives, enabled by NFC and MPoC guidelines, introduce the same real-time risk insights present in e-commerce. The converging channel architecture is expected to push payment security market size for unified gateway solutions to USD XX billion by 2031, assuming current penetration trajectories. The rise of mobile also acts as a forcing function for web platforms to adopt modern session integrity controls, ensuring that customer experience remains consistent across a retailer’s full engagement cycle.

By Organization Size: Enterprise depth versus SME velocity

Large organizations held 64.30% of the payment security market in 2025 due to deeper budgets and the complexity of multi-region compliance. Enterprises typically prefer integrated platforms that layer tokenization, risk scoring, and orchestration into a single console, simplifying policy rollout across hundreds of merchant identifiers. Vendor selection criteria emphasize global acquirer connectivity, customizable dashboards, and API-level extensibility. In contrast, SMEs propel overall market velocity, expanding at a 21.9% CAGR through 2031 as subscription-based models lower adoption thresholds. Pay-as-you-grow price grids appeal to merchants seeking predictable monthly costs while avoiding capital outlays.

Divergent purchase triggers shape product roadmaps. Enterprises demand granular key-rotation schedules, dedicated hardware security module clusters, and native SIEM integrations. SMEs look for one-click plug-ins, pre-vetted compliance templates, and simplified PCI questionnaires. Providers that segment their catalog accordingly are well placed to capture growth across both cohorts, supporting sustained revenue diversity inside the payment security market.

By End-user Industry: Retail remains pivotal; healthcare accelerates

Retail and e-commerce maintained 36.40% of payment security market size in 2025, largely because card-not-present fraud continues to shadow online volume growth. Investments focus on checkout-page script monitoring, network token rollout, and real-time risk engines that keep approval latency below two seconds. Dynamic routing is gaining traction as merchants look to recover declined authorizations by cascading transactions across multiple acquirers.

Healthcare is the fastest mover, advancing at a 18.7% CAGR as providers digitize billing channels and reconcile PCI obligations with HIPAA mandates. Tokenized patient payment profiles protect stored credentials while facilitating recurring copay billing. Banking, financial services, and insurance players stay aggressive on spend due to direct regulatory oversight and rising account-takeover attempts. Government agencies follow similar paths as treasury departments modernize citizen-services portals, bringing them under PCI and local data-protection umbrellas. Each vertical’s distinct pain points expand addressable revenue pools for niche suppliers specialising in contextual regulations, thereby broadening competitive intensity within the wider payment security industry.

Geography Analysis

North America contributed 29.60% of payment security market revenue in 2025, boosted by early PCI DSS 4.0 migrations and continued upgrades among large omnichannel merchants. Enterprise budgets prioritise AI-powered risk engines, while card networks bundle value-added security services inside processing tariffs. Implementation challenges linked to 3DS 2.2 latency still influence approval ratios, yet the regulatory certainty of defined enforcement timelines underpins steady procurement pipelines. Strategic acquisitions, such as Mastercard’s USD 2.65 billion purchase of Recorded Future in 2024, highlight an ongoing drive to embed native threat-intelligence feeds inside network stacks.

Asia–Pacific remains the growth nucleus. Mobile wallets now drive 70% of total ecommerce volume, supported by government-backed real-time payment rails and aggressive financial inclusion policies. Infrastructure leapfrogging lets merchants skip legacy mag-stripe systems, installing cloud-native gateways from inception. Cross-border QR alliances, typified by the linkage between Singapore’s PayNow and Thailand’s PromptPay, further increase transaction counts that must be secured end-to-end. As a result, regional demand skews toward lightweight SDKs that embed device binding and behavioral biometrics without adding checkout friction.

Europe balances strong consumer-protection norms with rapid POS technology refresh cycles. PCI MPoC and PSD3 create a harmonised compliance backdrop across 27 member states, spurring automotive, hospitality, and transport sectors to adopt contactless and IoT-enabled terminals. Meanwhile, the Middle East and Africa show the highest CAGR at 19.8% through 2031, driven by mobile-money platforms that serve previously unbanked populations. Regional regulators accelerate digital-identity frameworks, supporting cloud token vaults hosted in locally compliant data centres. These initiatives collectively expand regional payment security market size, although SME affordability constraints persist.

Regulatory Landscape

Regulation and standards continue to drive baseline controls in payment security. PCI DSS 3.2.1 was retired on 31 March 2024, and PCI DSS v4.x requirements came into force from 31 March 2025. The change shifts compliance from point-in-time controls to ongoing security operations, including continuous log analysis and payment-page script integrity, and it is pushing spend toward tokenization, encryption, and monitoring across merchants and service providers.

Across major regions, regulators are tightening digital payment security expectations beyond card-scheme requirements. In India, the Reserve Bank of India issued its 2025 Directions on authentication mechanisms for digital payment transactions, effective 1 April 2026, and it also released draft 2026 Directions on digital payment security controls for commercial banks and for non-banking financial companies. In the European Union, the Payment Services package (PSD3 and the Payment Services Regulation, PSR) moved through finalization milestones after a provisional political agreement in November 2025, with compromise texts confirmed by May 2026, reinforcing harmonized requirements for payment service providers along with broader obligations on ICT and fraud-related data sharing.

Value Chain Analysis

The payment security value chain spans standards and rule-setters (PCI SSC, EMVCo), identity and authentication ecosystems (3-D Secure, passkeys, device attestation), and cryptography and key-management infrastructure (HSMs, token vaults, certificate authorities). Enabling software layers, including fraud engines, risk scoring, orchestration, and monitoring, sit on top of this infrastructure and are deployed through gateways, acquirers, processors, and card networks before delivery to merchants via direct enterprise integrations, SaaS platforms, and channel partners such as POS terminal OEMs and ISVs for vertical software (hospitality, healthcare, retail). Threat intelligence and behavioral analytics data providers also connect with chargeback and dispute tooling to complete the prevention-to-recovery loop.

Recent moves show value creation shifting toward network-grade fraud signals, modular integrations, and resilient authorization-path operations. In 2026, Visa partnered with Switch Al Maghrib to integrate Visa Advanced Authorization into Morocco's national switch, bringing AI-driven fraud detection closer to the routing layer. Visa also collaborated with OpenAI and executed live agentic commerce transactions in Europe using tokenized credentials and Payment Passkeys aligned with Strong Customer Authentication. In parallel, ecosystem initiatives such as the Linux Foundation-backed x402 Foundation point to emerging machine-to-machine payment standards, which raises the importance of secure APIs, verified agent identity, and dependency management, including SBOM practices and circuit-breaker patterns, across the processor and gateway supply chain.

Competitive Landscape

Competition in the payment security market is characterised by a blend of established card networks, global processors, and specialised fintech start-ups. Market leaders pursue bolt-on acquisitions to fast-track capability expansion. Visa plans to close its purchase of AI specialist Featurespace by September 2025, adding adaptive behavioural models to its in-house risk stack.[2]Visa, “Visa to Acquire Featurespace,” usa.visa.com Worldpay acquired Ravelin in February 2025 to lift e-commerce authorization rates, then agreed to merge with Global Payments in April 2025 to scale combined coverage to 94 billion transactions annually.[3]Worldpay, “Worldpay Acquires Ravelin,” worldpay.com These moves underscore the strategic significance of embedded fraud analytics and global merchant reach.

Technology differentiation hinges on machine-learning depth, latency management, and token-life-cycle governance. Patent activity remains strong, illustrated by Microsoft’s ledger-independent token patent that allows cross-network portability, a feature that appeals to merchants running multi-acquirer routing. Niche innovators focus on quantum-resistant key exchange, biometric continuous authentication, and blockchain-anchored audit trails. Many target pain points in high-growth segments such as BNPL fraud or cross-border small-ticket commerce.

The competitive field also shows horizontal alliances. Device manufacturers collaborate with gateway providers to preload secure elements, ensuring end-to-end encryption from keypad to acquirer. Processors team up with cloud platforms to push pre-certified sandbox environments that shorten time-to-market for new merchants. Although consolidation is underway, specialised vendors that excel in a single pain point can still capture profitable sub-segments, keeping overall fragmentation at a moderate level.

Payment Security Industry Leaders

CyberSource Corporation (Visa Inc.)

Bluefin Payment Systems LLC

Elavon Inc.

SecurionPay

PayPal Holdings Inc. (Braintree)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is modernization of checkout and authorization security using network-provided intelligence and enriched transaction context, which creates room for vendors that reduce fraud without adding latency. Visa made its Checkout Intelligence Layer commercially available in April 2026, and ecosystem plugins such as the WooCommerce-Stripe update, enabling enriched data fields, show how merchant platforms are adapting to pass higher-quality signals into risk decisions. That, in turn, expands demand for interoperable orchestration across gateways, fraud engines, and network token services, particularly among large merchants running multi-acquirer routing and looking for consistent controls across web, mobile, and in-store channels.

A second whitespace area is securing non-human commerce and automated transactions, where authentication, intent verification, and credential lifecycle management extend beyond traditional cardholder flows. In July 2026, Visa reported live agentic commerce transactions in Europe using Trusted Agent Protocol and Payment Passkeys for SCA-aligned authentication, and the Linux Foundation formally launched the x402 Foundation to standardize internet-native payments between software agents with support from Visa, Mastercard, Ripple, and Stripe. Alongside this, regulatory hardening continues to drive demand for adaptable authentication and monitoring stacks, including the RBI's authentication directions effective 1 April 2026 and ongoing EU PSD3/PSR finalization by May 2026, encouraging vendors to package configurable controls for banks, PSPs, and merchants operating across jurisdictions.

Recent Industry Developments

- July 2026: Elavon and Wix announced an integration of Elavon Business Solutions with Wix unified commerce capabilities to help small businesses manage payments and storefront operations through one platform. The move broadens Elavon's reach through a high-volume merchant creation channel while embedding security and payment acceptance deeper into SMB workflows.

- April 2026: MoneyHash announced a multi-year partnership with Visa to scale Cybersource enablement within MoneyHash's payment orchestration layer across MENA. This expands Cybersource footprint in emerging markets by pairing orchestration-led routing with network-grade security tooling, reducing implementation friction for regional merchants.

- December 2024: Mastercard closed its acquisition of Recorded Future, bringing threat-intelligence feeds into Mastercard's security stack. The combination strengthens detection of compromised cards and fraud infrastructure, supporting faster response cycles for issuers and merchants connected to Mastercard services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the payment security market covers software, services, and security functions used to protect payment transactions and related data across online, mobile, and in-store channels, from authorization through settlement. This includes controls designed to reduce fraud risk and support payment security requirements.

Scope exclusions: Pure payment processing fees, general cybersecurity products not built for payments, and unmanaged hardware-only sales are excluded unless they are sold as part of a payment security solution or service.

Segmentation Overview

- By Solution Type

- Encryption

- Tokenization

- Fraud Detection & Prevention

- Other Solutions

- By Platform

- Mobile-Based

- Web-Based

- In-Store / POS

- By Organization Size

- Small & Medium-Sized Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- Retail and E-commerce

- BFSI

- Healthcare

- IT and Telecom

- Travel and Hospitality

- Government

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base and to keep assumptions tied to measurable signals that move with payment volumes and fraud pressure. We relied on public references such as central bank payment statistics, BIS and IMF macro indicators, PCI Security Standards Council updates, and NIST security guidance, along with open publications from agencies like the FTC and ENISA on fraud and cyber trends.

To translate these signals into market inputs, we also reviewed company filings, investor presentations, audited annual reports, and product documentation, plus credible press coverage and association websites related to digital commerce and cards. Paid subscriptions for company financials and news intelligence, patent databases, and an import-export shipment level database were used selectively to confirm vendor exposure, feature direction, and regional activity. These examples are not exhaustive, and additional sources were checked to collect, validate, and clarify the data.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with payment security solution providers, payment service partners, merchants, and financial institutions, so the model could be adjusted to real buying and deployment patterns. For global coverage, inputs were validated across APAC, EMEA, and the Americas, with follow-ups used when desk research left gaps on pricing logic, adoption timing, and channel mix.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 43% |

| Mid tier: 53% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 21% | Managers: 52% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where transaction growth, channel shift (card present versus card not present), and documented fraud pressure are used to reconstruct the demand pool for payment security spending by region. After that pool is formed, we apply adoption and spend intensity assumptions, which were checked with interview feedback. We then compare the result with selective bottom-up approximations such as sampled price ranges multiplied by likely deployment volumes for key solution categories.

Inputs used in the model include digital payment transaction value and volume trends, e-commerce and mobile wallet usage indicators, reported fraud loss and chargeback direction, PCI DSS and related compliance timelines, and cloud adoption patterns that influence how solutions are deployed and priced. Where a bottom-up check cannot cover smaller vendors or private revenue splits, gaps are handled through conservative share assumptions and then re-tested against regional payment growth and vendor activity signals.

For forecasting, scenario analysis is used around fraud intensity, regulatory enforcement pace, and merchant migration to modern payment rails. This is supported by short-cycle trend fitting on historical growth to reduce sensitivity to one-year spikes. The final forecast path is reviewed to stay consistent with the expected movement in payment volumes and the observed speed of security feature rollouts.

Data Validation & Update Cycle

Validation is carried out by checking whether outputs move logically with independent indicators such as payment transaction expansion, fraud and chargeback direction, and security compliance milestones, then investigating any large variances. When a result looks off, we revisit conversion rates, pricing ranges, and regional splits, and we re-contact relevant respondents if the assumption is sensitive.

Before sign-off, the model and narrative go through multi-step analyst reviews that include consistency checks across years, currency conversion timing checks, and reasonableness tests against adjacent security and payments spend patterns. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Payment Security Market Size Versus Other Published Estimates

Published market sizes for payment security often differ because each publisher draws the market line differently and then applies its own pricing and adoption assumptions. Variation also comes from older base years, different currency timing, and forecast paths that assume faster regulatory enforcement.

Some estimates include broader payment industry revenue pools in the total, such as processing-linked charges and adjacent banking technology spend. In Mordor Intelligence, only payment security solutions and services tied to protecting payment transactions across web, mobile, and in-store channels are counted, while generic cybersecurity and pure processing fees are kept out unless they are sold as part of a payment security engagement.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.44 B (2026) | |

| Global Consultancy A | USD 24.61 B (2024) | Uses a 2024 valuation window and a wider security practices framing, which can shift totals when services and multi-vertical security spend are grouped under payment security without consistent channel-level filters. |

| Industry Publisher B | USD 17.33 B (2024) | Applies a longer 2025-2035 outlook with a lower CAGR and a different starting pool, which can reflect narrower inclusion of advanced authentication and deployment types and more conservative adoption ramp assumptions. |

The spread across sources mainly comes from how far adjacent spend is allowed into the market and which year is treated as the starting point for pricing and adoption. By keeping the demand pool tied to payment transaction protection use cases and checking assumptions against payment volume growth and fraud direction, we arrive at a total that can be traced back to clear levers and repeated as new data is released.

Key Questions Answered in the Report

What is the current value of the payment security market?

The market is valued at USD 39.44 billion in 2026, with a forecast to grow to USD 86.18 billion by 2031 at a 16.95% CAGR.

Which solution type leads by revenue?

Tokenization leads and held 30.45% of payment security market share in 2025, driven by its ability to remove sensitive data from merchant systems.

Which platform shows the fastest growth?

Mobile-based deployments expand at a 22.3% CAGR through 2031, supported by strong digital-wallet adoption across Asia–Pacific.

Why is healthcare the fastest-growing end-user industry?

Healthcare accelerates at a 18.7% CAGR because organizations are digitizing billing channels and aligning PCI controls with stringent HIPAA data-protection rules.

What impact does PCI DSS 4.0 have on merchants?

Merchants must comply with 64 new controls by March 2025, with non-compliance fines up to USD 500,000 per month, triggering substantial investment in tokenization and continuous monitoring solutions.

How fragmented is the competitive landscape?

With the top five vendors controlling about 35% of revenue, the market is moderately fragmented, allowing specialised players to target niches such as BNPL fraud and quantum-safe encryption.

Page last updated on: