China Copper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

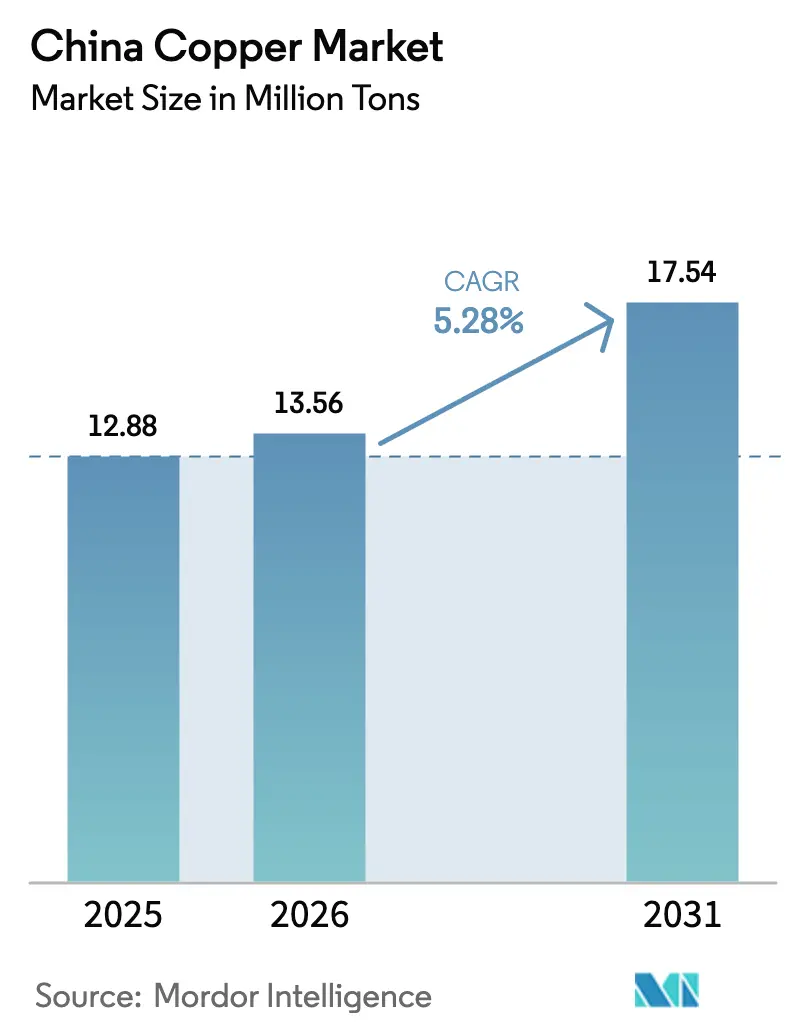

| Base Year Market Size (2025) | 12.88 Million tons |

| Market Volume (2026) | 13.56 Million tons |

| Market Volume (2031) | 17.54 Million tons |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Copper Market Analysis by Mordor Intelligence

China Copper Market size in 2026 is estimated at 13.56 Million tons, growing from 2025 value of 12.88 Million tons with 2031 projections showing 17.54 Million tons, growing at 5.28% CAGR over 2026-2031. Robust renewable-energy build-outs, grid modernization, and vehicle electrification anchor this expansion. State-backed investments in ultra-high-voltage (UHV) transmission lines, worth USD 89 Billion for 2025, channel copper into long-distance infrastructure while cushioning the market from cyclical swings. Demand also gathers pace from electric-vehicle (EV) manufacturing hubs, where battery, traction-motor, and charging-station build-outs intensify copper use. Industrial automation in coastal factories and the mushrooming of artificial intelligence (AI)-ready data centers reinforce a consumption pattern far less sensitive to traditional construction cycles. On the supply side, capacity additions by state-owned smelters reshuffle market power even as tighter emission caps squeeze operating margins.

Key Report Takeaways

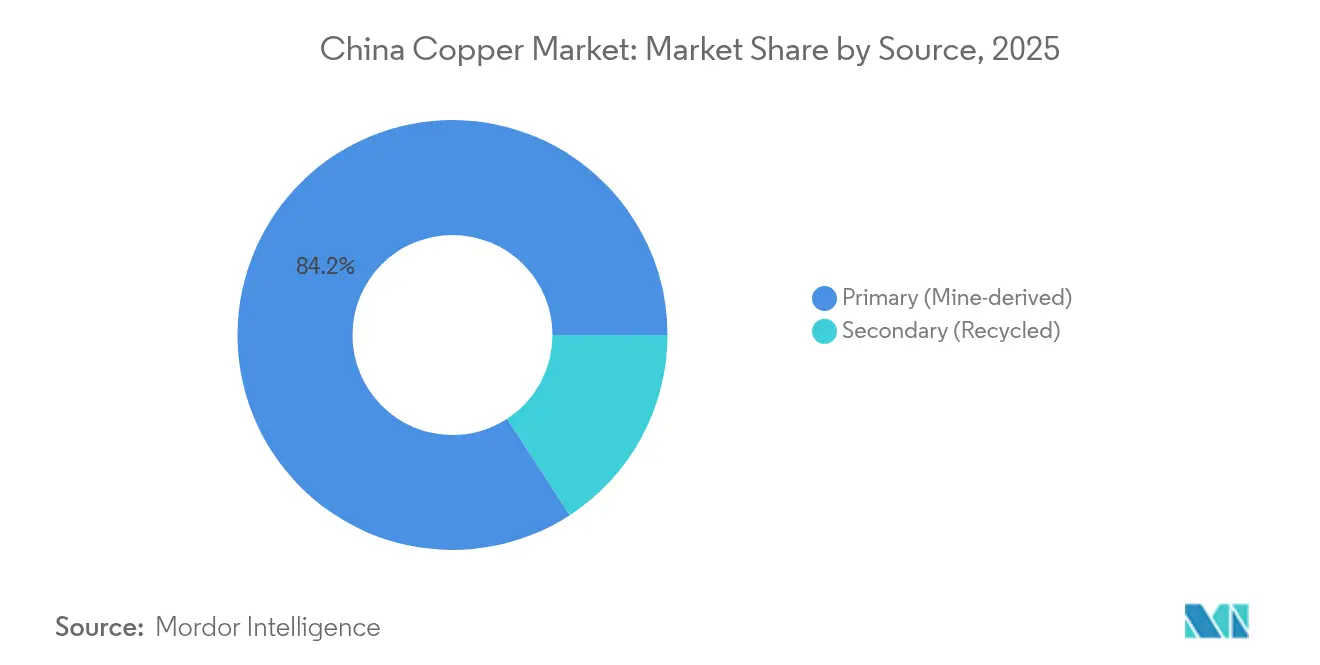

- By source, primary copper retained an 84.19% share of the China Copper market in 2025. However, secondary copper is forecasted to expand at the fastest CAGR of 6.35% through 2031.

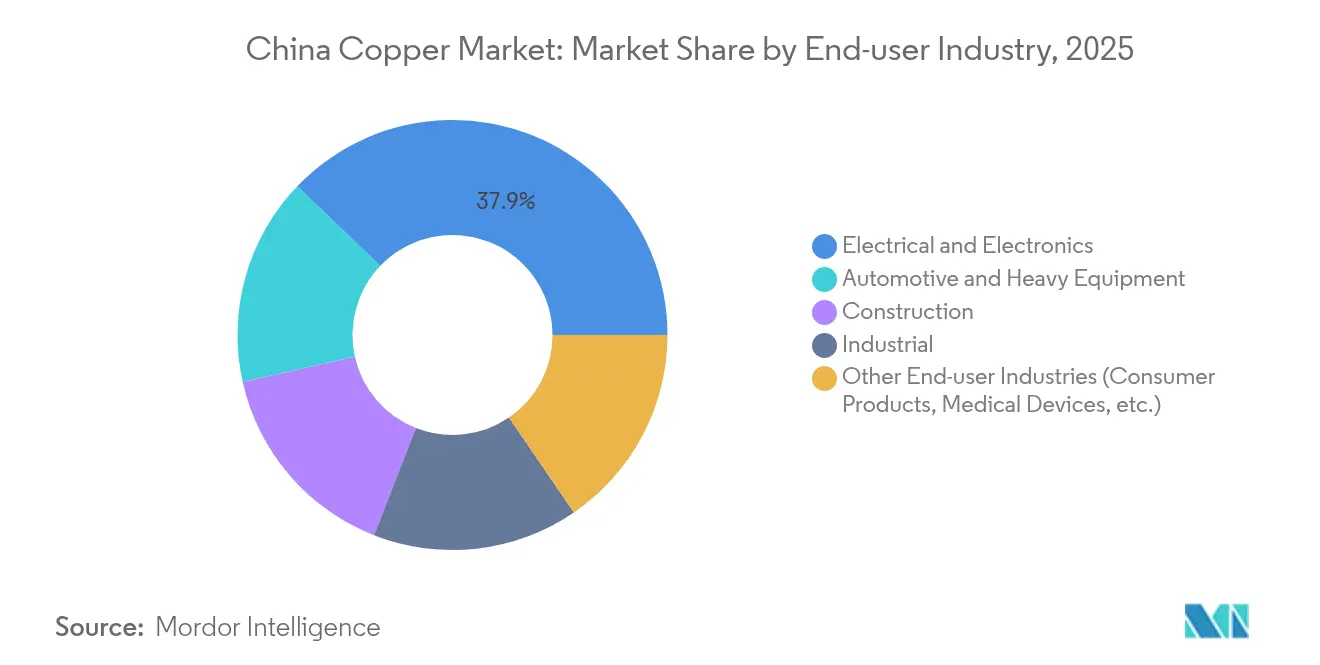

- By end-user industry, electrical and electronics captured 37.85% of the China Copper market share in 2025. Whereas, automotive and heavy equipment is projected to register the highest growth at 6.59% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on copper market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Copper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand From Renewable Energy and Grid Expansion | +1.8% | National focus, Western renewable bases | Long term (≥ 4 years) |

| Rapid Build-out of Domestic EV and Battery Manufacturing | +1.5% | Coastal production hubs, nationwide adoption | Medium term (2-4 years) |

| Accelerating Deployment of AI-ready Data-centres | +0.9% | Eastern economic corridors, Tier-2 city clusters | Medium term (2-4 years) |

| Government-backed Western Region Infrastructure Push | +0.7% | Western provinces, Belt and Road corridors | Long term (≥ 4 years) |

| Upscaling of Smart Factory Automation in Coastal Provinces | +0.6% | Guangdong, Jiangsu, Zhejiang manufacturing zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand From Renewable Energy and Grid Expansion

A nationwide pivot toward clean-energy generation is placing copper at the heart of China’s electrical-infrastructure rollout. Each kilometer of a new ultra high voltage (UHV) line embeds about 6 tons of refined copper, and 38 such lines were already in service by April 2024, linking renewable-rich western deserts to coastal load centers. The ongoing Gansu–Zhejiang ±800 kV link alone consumes over 14,000 tons of copper and transmits 36 Billion kWh annually, more than half stemming from wind and solar plants. Solar and onshore wind capacity, which together target 1,200 GW by 2030, require copper-heavy cabling, inverters, transformers, and switchgear that extend well beyond classical demand models. Because grid investments are locked in through multi-year state plans, they shelter the China Copper market from short-term construction slumps while anchoring floor prices for refined metal.

Rapid Build-out of Domestic EV and Battery Manufacturing

Battery-electric vehicles average close to 70 kg of copper per unit, covering wiring harnesses, rotors, and battery-pack connectors. Even if industry roadmaps halve intensity to 38 kg by 2030 through design efficiencies, absolute tonnage will still rise on surging output. China manufactured 958.7 Million vehicles in 2023, up 35.8% yearly, and continues to scale dedicated assembly lines in Shanghai, Guangzhou, and Changzhou. Charging networks amplify demand: every additional megawatt of charging capacity deploys 20 to 40 tons of copper in conductors, switchgear, and thermal-management loops. Vertical integration inside automakers’ supply chains ensures that a large portion of copper sourcing and processing remains domestic, lending visibility to long-term offtake agreements for smelters.

Accelerating Deployment of AI-ready Data-centres

AI workloads raise power-density thresholds and cooling complexity, both of which intensify copper intensity per megawatt of IT load. Chinese data-center energy consumption reached 140 Billion kWh in 2024 and could triple by 2035, implying more than 2.6 Million tons of refined copper per year for server racks, busbars, and chilled-water loops. Large hyperscalers are adopting high-current copper interconnects in preference to fiber for short-reach, latency-sensitive switching, amplifying near-term orders for wire-rod producers. The resulting demand nodes emerge in Jiangsu, Zhejiang, and Hebei, where land, grid access, and cold-climate advantage converge, reshaping regional flows of refined metal.

Government-backed Western Region Infrastructure Push

The Western Development Strategy funnels capital into railways, highways, and industrial parks across Xinjiang, Tibet, and Inner Mongolia. Projects along the China–Pakistan Economic Corridor, valued at USD 60 Billion, incorporate copper-rich power plants and transmission assets. Recent geological surveys on the Qinghai-Xizang Plateau identified more than 20 Million tons of copper resources, prompting rapid mine-site electrification and haul-road construction that lift local refined-copper use. Because UHV lines bridge western generators with eastern consumers, copper moves through extended project pipelines that span exploration, beneficiation, smelting, and final fabrication.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Sulphur-dioxide and Carbon-emission Caps on Smelters | -1.2% | National, with severe impact on industrial provinces | Short term (≤ 2 years) |

| Persistent Copper-concentrate Deficit and Low TC/RCs | -0.8% | Global supply chains affecting domestic smelters | Medium term (2-4 years) |

| Rising Competition from Aluminum Substitution in 1 kV Cabling | -0.6% | National, with focus on construction and electrical sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Sulphur-dioxide and Carbon-emission Caps on Smelters

Updated environmental standards restrict SO₂ to 6.3 lb/h and tighten particulate and lead limits for primary smelters, obliging operators to retrofit scrubbers and electrostatic precipitators at high capital cost [1]Federal Register, “National Emission Standards for Primary Copper Smelting,” federalregister.gov. Provincial regulators have also curbed petroleum-coke firing, eliminating 12 Million tons of annual fuel imports and forcing a switch to cleaner natural gas. Compliance timelines of two years risk near-term output cuts among mid-tier smelters, lowering domestic cathode supply just as consumption scales. Government quotas on new capacity now require applicants to hold equity stakes in upstream mines, slowing project approvals and concentrating market power among existing state-owned incumbents.

Persistent Copper-concentrate Deficit and Low TC/RCs

Global concentrate tightness collapsed spot treatment charges to single-digit USD per tonne in late-2024, a 90% contraction from prior-year averages. Chinese smelting additions of 1.25 Million tons per year outstrip new mine supply, binding domestic refiners to unfavorable benchmark negotiations with suppliers from Chile and Peru. Import tariffs of 34% on selected US-sourced scrap further constrain feedstock diversity, leaving refineries vulnerable to price spikes and relogistics costs. Prolonged margin pressure may shutter less efficient converters and contribute to structural refined-copper shortfalls, tempering the otherwise strong growth trajectory of the China copper market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Primary Dominance Amid Secondary Acceleration

Primary copper commanded 84.19% of the China Copper market in 2025 as smelters leveraged consistent ore flows from Jiangxi Copper and Zijin Mining as well as long-term offtake agreements with Chilean and Peruvian producers. The China Copper market size for primary material is expected to track a 5.04% CAGR through 2031, supported by UHV grid projects and electric vehicle (EV) battery-foil expansions. Although smaller, secondary copper is set to gain share at a 6.35% CAGR, helped by a January 2025 tariff cut on recycled-copper imports to 0% and city-level scrap-collection pilots targeting 400,000 tons of annual recycled output by 2025 . Growing circular-economy mandates and rising treatment-charge stress encourage smelters to substitute concentrates with scrap, allowing secondary flows to dilute overall feedstock risk. Recyclers have invested in automated dismantling lines that lift recovery rates on wire harnesses and air-conditioner coils, narrowing the quality gap with virgin cathode.

By End-user Industry: Electronics Leadership with Automotive Momentum

Electrical and electronics held 37.85% of the China Copper market share in 2025 on the back of extensive consumer-electronics assembly, telecommunication-equipment production, and data-center build-outs. Segment sales are projected to grow at 4.05% CAGR, underpinned by rising server-grade cable demand and network-edge device upgrades. Automotive and heavy equipment, although smaller in base, is forecast to outpace peers at a 6.59% CAGR through 2031 as pure EVs keep more than 60% of national auto sales and each charging pile deploys up to 8 kg of copper in busbars and cooling coils. Construction contributes steady baseline demand through smart-grid meters and elevator modernization, while industrial automation adds episodic spikes that sync with factory-upgrade cycles. Collectively these consumption avenues reinforce the structural uptrend in the China Copper market size even when single sectors face cyclical pauses.

Geography Analysis

Eastern coastal provinces, Guangdong, Jiangsu, and Zhejiang, absorbed the largest slice of refined metal in 2025 owing to export-oriented electronics clusters and well-developed logistics. The China copper market size attached to these three provinces surpassed 5.24 Million tons in 2026, equal to nearly 40% of national demand. Beijing–Tianjin–Hebei registers the quickest advance, recording a forecast 6.84% CAGR as AI-ready data-center campuses mushroom around Zhangbei and Langfang, both linked to renewable energy corridors. Central provinces such as Hubei and Hunan serve as trans-shipment and fabrication hubs, supporting wire-rod, alloy-tube, and transformer makers that supply the coast. Western China brings emerging volume aided by resource-driven infrastructure spending and the commissioning of large solar-plus-storage parks. Ultra-high-voltage corridors like the 2,370 km Gansu–Zhejiang line knit western generation with eastern consumption, knitting regional price convergence and deepening copper flows across inland logistic routes

Competitive Landscape

The China Copper market possesses moderate concentration. Top state-owned groups benefit from policy support, home-based smelting capacity, and dedicated ore pipelines. For instance, Jiangxi Copper Corporation controls a domestic mining-to-refining chain exceeding 1.2 Million tons, while Zijin Mining produced 1.01 Million tons of copper in 2024 after ramping the Qulong mine and Serbian acquisitions. CMOC Group is expanding overseas exposure through a USD 420 Million buyout of Ecuador’s Cangarejos project, gaining an eventual 41 Million lb annual copper stream. Private entrants focus on scrap-based refining and high-value copper-foil lines, hedging against concentrate scarcity and regulatory hurdles. Recycling alliances between smelters and appliance manufacturers illustrate vertical integration aimed at securing steady scrap inflows. Cross-border joint ventures with Belt and Road partners continue as Chinese groups lock in off-shore ore sources to buffer domestic supply deficits.

China Copper Industry Leaders

Jiangxi Copper Corporation

Zijin Mining Group Co., Ltd.

CMOC

Tongling Non-ferrous Metals Group Holding Co., Ltd.

Jinchuan Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: China has tightened rules for new copper smelters, requiring firms to secure mine supply through ownership or equity stakes, as per its 2025-2027 copper industry plan. This move is expected to limit new smelters to a few major Chinese companies.

- January 2024: Jiangxi Copper Company announced to expand its Nanchang plant with Danieli Fröhling's technology, adding 15,000 tons of annual capacity for copper and copper-alloy products. The upgrade includes a 20-high reversing mill to roll copper from 0.8 mm to 0.03 mm thickness, targeting foil and thin-strip markets.

China Copper Market Report Scope

Copper, a reddish-brown colored metal, is primarily known for its good electrical conductivity, excellent thermal conductivity, corrosion resistance, high ductility, recyclability, and non-magnetic nature. The compatible properties of copper make it a primary metal for cables and wiring in the electrical and electronics industry.

The China copper market is segmented by end-user industry (automotive and heavy equipment, construction, electrical and electronics, industrial, and other end-user industries (Consumer Products, Medical Devices, etc.). The report covers the market size and forecast for the studied market in terms of volume (tons).

| Primary (Mine-derived) |

| Secondary (Recycled) |

| Automotive and Heavy Equipment |

| Construction |

| Electrical and Electronics |

| Industrial |

| Other End-user Industries (Consumer Products, Medical Devices, etc.) |

| By Source | Primary (Mine-derived) |

| Secondary (Recycled) | |

| By End-user Industry | Automotive and Heavy Equipment |

| Construction | |

| Electrical and Electronics | |

| Industrial | |

| Other End-user Industries (Consumer Products, Medical Devices, etc.) |

Key Questions Answered in the Report

What is the current size and projected CAGR of the China Copper market?

The market stands at 13.56 Million tons in 2026 and is forecast to reach 17.54 Million tons by 2031, reflecting a 5.28% CAGR.

Which end-user segment holds the largest share of China’s copper demand?

Electrical and electronics leads with 37.85% of national consumption in 2025.

Which copper source segment is growing the fastest?

Secondary (recycled) copper is projected to expand at a 6.35% CAGR between 2026 and 2031.

How does China’s renewable-energy build-out affect copper usage?

Each kilometer of UHV transmission line embeds 6 tons of copper, and grid projects tied to the 1,200 GW wind-plus-solar target underpin long-term demand.

What supply-side constraints could limit copper availability in China?

Tight sulphur-dioxide and carbon-emission caps on smelters and a global concentrate deficit that has pushed treatment charges to single-digit USD levels both weigh on domestic output.

Page last updated on: