Content Creation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 43.44 Billion |

| Market Size (2031) | USD 73.49 Billion |

| Growth Rate (2026 - 2031) | 11.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Creation Market Analysis by Mordor Intelligence

The content creation market size was valued at USD 39.1 billion in 2025 and estimated to grow from USD 43.44 billion in 2026 to reach USD 73.49 billion by 2031, at a CAGR of 11.09% during the forecast period (2026-2031). Demand is lifted by enterprise-wide digital transformation, the rapid rollout of generative artificial intelligence in everyday authoring workflows, and a decisive shift toward cloud-first deployment. Cloud platforms accelerate collaboration and shorten release cycles, while headless architectures allow content to flow to web, mobile, and social channels without redevelopment. Small and medium-sized enterprises (SMEs) expand faster than large organizations because subscription models reduce the need for heavy upfront investment. Vendors differentiate through embedded AI services that automate tagging, translation, and compliance checks. Competitive momentum intensifies as emerging headless providers challenge full-suite platforms with modular offerings that promise lower lock-in and greater flexibility.

Key Report Takeaways

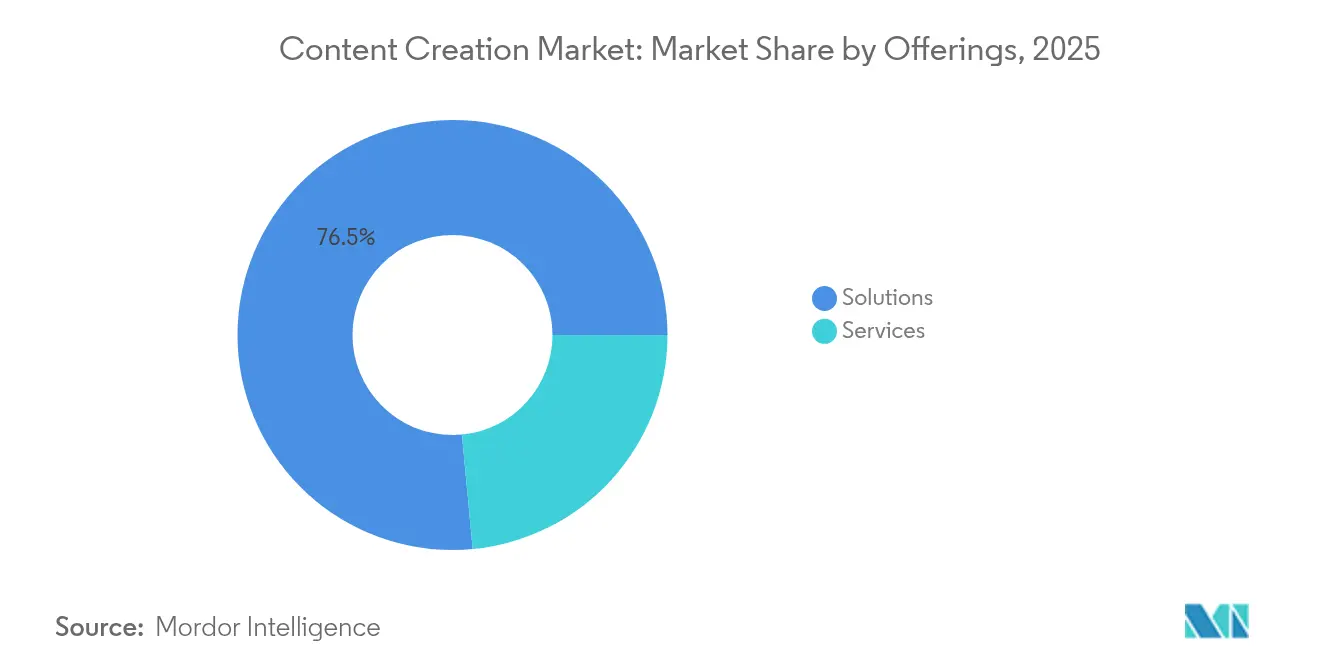

- By offerings, solutions commanded 76.50% of the content creation market share in 2025, while services are forecast to expand at a 16.28% CAGR through 2031.

- By deployment mode, the cloud segment held a 70.15% share of the content creation market in 2025 and is expected to grow at an 18.2% CAGR to 2031.

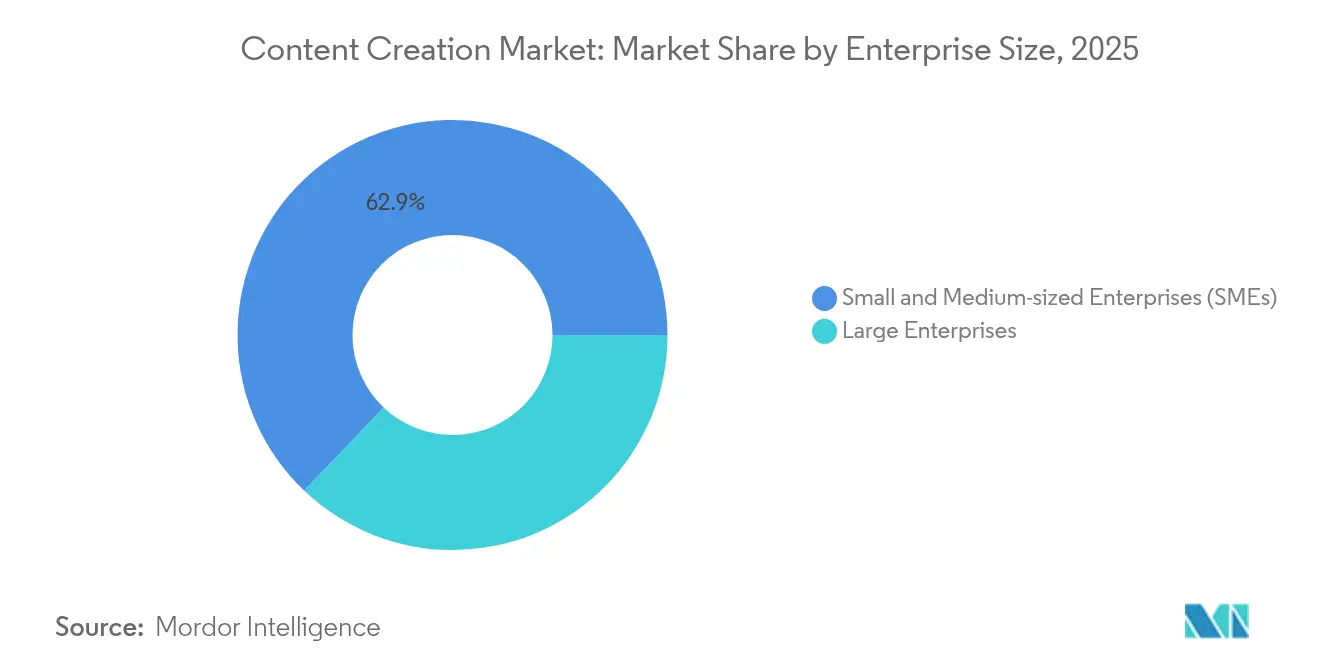

- By enterprise size, SMEs accounted for 62.90% of the market in 2025 and are projected to rise at a 14.05% CAGR through 2031.

- By end-user vertical, media and entertainment led with 29.60% revenue share in 2025; retail and e-commerce are poised for the fastest growth at a 15.52% CAGR to 2031.

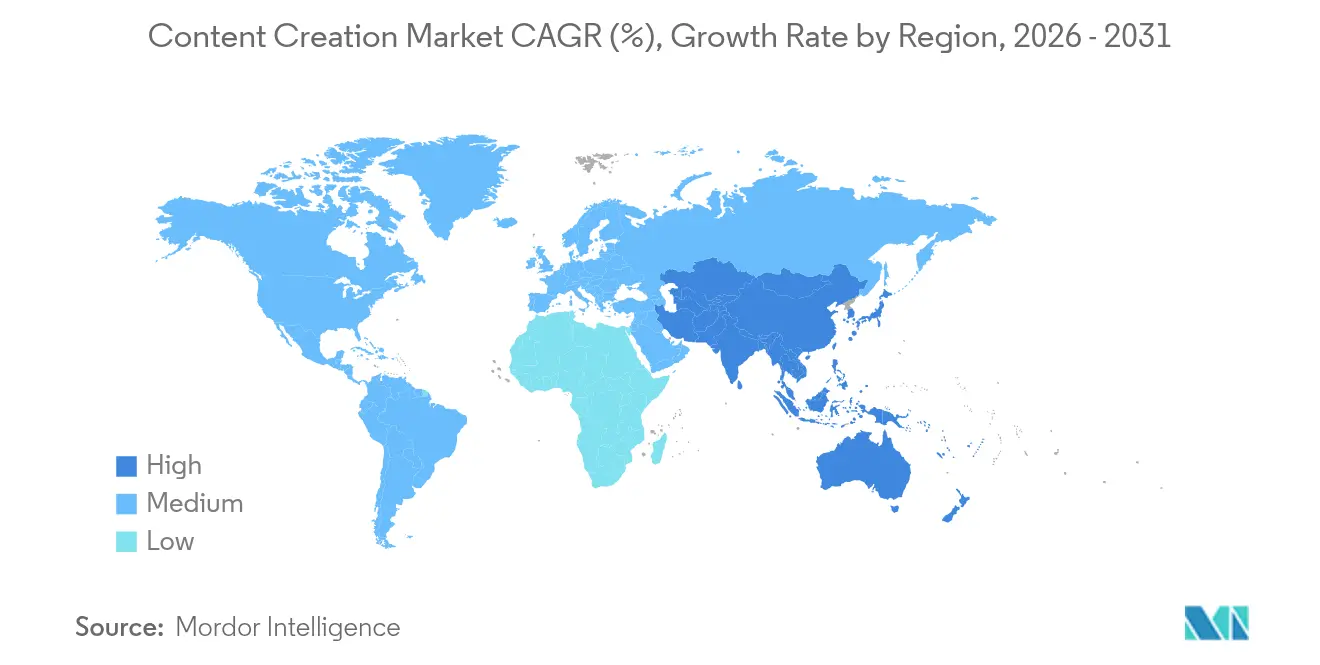

- By geography, North America controlled 34.20% of 2025 revenue, while Asia-Pacific is on track for a 16.88% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Content Creation Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first adoption of content platforms | +2.8% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Generative-AI tools slash production lead times | +3.2% | Global core markets | Short term (≤ 2 years) |

| Social-commerce boom amplifies creator demand | +1.9% | Global, strongest in APAC and North America | Medium term (2–4 years) |

| Micro-personalization via headless and composable CMS | +2.1% | North America, Europe, APAC spillover | Long term (≥ 4 years) |

| Mandatory ESG disclosure fuels sustainability-report content | +1.4% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-first adoption of content platforms

Organizations migrate from on-premise systems to cloud-native suites to gain elasticity and lower maintenance overhead. Microsoft’s cloud revenue reached USD 42.4 billion in Q3 FY25, reflecting steady enterprise consolidation on unified platforms that embed both productivity and CMS capabilities. Retailer TELUS cut its time-to-market in half after embracing a headless, API-first stack. The cloud model also enables instant access to GPU-powered generative AI, letting teams generate assets without local infrastructure.

Generative-AI tools slash production lead times

Adobe’s GenStudio automates variant creation, compliance checks, and distribution, positioning brands to meet a fivefold surge in content demand by 2026.[1]Adobe, “Adobe Expands GenStudio Content Supply Chain Offering for Marketing and Creative Teams to Tackle Skyrocketing Content Demands with AI,” news.adobe.com Japanese integrator Zenken saved 12,500 hours each month by rolling out ChatGPT Enterprise across its workforce. Enterprises combine AI with human review to maintain brand voice while accelerating repetitive tasks.

Social-commerce boom amplifies creator demand

Retailers turn to influencer and user-generated content, requiring CMS platforms that support omnichannel moderation and rapid publishing. INTERSPORT’s Pimcore deployment lifted online revenue by over 80% after unifying product information and content workflows. Headless architectures thrive because they stream content to social apps, web stores, and in-store kiosks from a single repository.

Micro-personalization via headless and composable CMS

MACH-aligned stacks combine microservices, API-first design, and headless delivery to tailor experiences at scale. Tata Digital’s switch to a headless CMS helped its Tata Neu super-app reach 11 million downloads within two months.[2]Sanity, “Tata Digital Customer Story | Sanity,” sanity.io While modularity expands choice, firms must invest in orchestration talent to prevent integration sprawl.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher compliance costs for copyright protection and deep-fake safeguards | -1.8% | Global; enforcement is toughest in North America and Europe | Short term (≤ 2 years) |

| SMEs push back against rising subscription prices | -2.3% | Worldwide, with the strongest effect in price-sensitive Asia-Pacific and other emerging markets | Medium term (2–4 years) |

| Quality suffers when AI automation goes unchecked | -1.2% | Global, hitting content-heavy sectors such as media and entertainment hardest | Medium term (2–4 years) |

| Unclear rules for AI-generated content | -1.5% | Starts in Europe and North America, then extends to Asia-Pacific as regulations spread | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising copyright and deep-fake compliance costs

Automated verification tools become essential as AI-generated media proliferates. IntelligenceBank’s acquisition of Red Marker signals a rush to embed pre-publication compliance filters into CMS workflows.[3]IntelligenceBank, “IntelligenceBank Acquires AI Content Compliance Platform Red Marker,” intelligencebank.com Smaller firms face higher legal exposure and may delay advanced AI adoption.

Subscription fatigue and price sensitivity among SMEs

Annual SaaS price increases and bundled feature “shrinkflation” tighten SME budgets. Google raised Workspace Business Standard from USD 12 to USD 14 per user, prompting customers to reassess platform mix. Vendors counter with tiered editions and consumption-based models to sustain volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offerings: Services scale as AI complexity rises

Services revenue is climbing at a 16.28% CAGR, outpacing the solutions segment that retains an 76.50% share of the content creation market in 2025. Enterprises call on system integrators to stitch together AI, data, and workflow engines, ensuring that automated pipelines deliver measurable speed and compliance gains. Adobe’s expansion of GenStudio with workflow agents underscores the service opportunity anchored in custom orchestration and change management. As adoption spreads, a rising pool of certified partners further fuels the services boom.

At the same time, organizations continue renewing core platform licenses, but growth moderates as baseline capabilities commoditize. Solution vendors now package AI features as premium modules, nudging customers toward service-heavy engagements that shorten payback periods. The interplay of product and services spend sustains overall momentum in the content creation market.

By Deployment Mode: Cloud dominance intensifies

The cloud model captured 70.15% of 2025 revenue and is on track for an 18.2% CAGR to 2031, cementing its role as the default operating environment for the content creation market. Microsoft’s USD 42.4 billion cloud haul signals buyer preference for integrated stacks that bundle storage, distribution, and AI inference in a single SLA. Sitecore’s XM Cloud doubled its revenue during 2024, further validating the approach.

On-premise deployments persist in regulated sectors where data residency is non-negotiable, yet even these clients adopt hybrid models to tap AI services without overhauling core databases. As connectivity improves, latency concerns fade, giving cloud vendors a broader canvas to push edge rendering, real-time personalization, and serverless preview environments.

By Enterprise Size: SMEs widen the user base

SMEs controlled 62.90% of spending in 2025 and are expanding at 14.05% CAGR, making them the volume engine of the content creation market. Cloud SaaS removes hardware hurdles, letting smaller firms publish and personalize at a pace once reserved for large media houses. Japanese survey data shows that 60% of SMEs now self-manage website builds, a jump enabled by intuitive dashboard design and pre-built templates.

Large enterprises remain critical for high-ticket deals that bundle digital asset management, analytics, and multi-brand governance. They lean on advanced permissioning, sandboxing, and audit trails to coordinate global author teams. Both segments converge on AI-driven productivity, but implementation depth scales with wallet size.

By Content Format: Video leads infrastructure investment

Video libraries swell as engagement metrics confirm stronger click-through and conversion performance. Platforms embed automated transcoding, adaptive bitrate streaming, and AI captioning to keep delivery costs predictable while maximizing accessibility. Audio and podcast workflows rise in parallel as voice search and infotainment consumption gain traction.

Static text and image assets remain foundational, but generative AI increasingly repurposes them into multi-format variants for each channel, raising the volume of items a CMS must track. Adobe’s Content Hub highlights this shift, supporting millions of assets with generative renditions to match device context.

By End-user Vertical: Retail’s rapid climb challenges media leadership

Media and entertainment preserved a 29.60% slice of 2025 revenue, relying on high-volume pipelines for streaming and news. Yet retail and e-commerce are sprinting at a 15.52% CAGR as stores blur with social feeds. The National Retail Federation trimmed website build times by 70% through a headless CMS rollout, spotlighting the productivity upside.

Healthcare, government, and BFSI sectors also escalate adoption to improve citizen services, patient portals, and regulatory reporting. Each vertical imposes its own compliance script, steering vendors toward verticalized accelerators and certified templates.

Geography Analysis

North America generated 34.20% of 2025 revenue, supported by deep cloud penetration, mature IT budgets, and a dense ecosystem of implementation partners. Office 365 Commercial seats climbed 16% in the region, underscoring buyers’ appetite for integrated collaboration and content management. Heightened scrutiny over AI-generated media rights, however, lifts compliance costs and may temper growth among smaller publishers.

Asia-Pacific is the fastest-growing territory at a 16.88% CAGR through 2031. Japan serves as a bellwether: 73.7% of companies have digital-transformation programs in play, up from 55.8% in 2021. Awareness of headless CMS reaches 75%, yet implementation lags, suggesting runway for integrators and SaaS providers. China and India add sheer scale, though data residency rules steer multinational vendors toward local cloud regions.

Europe retains a sizeable share thanks to strong regulatory impetus. GDPR, AI Act deliberations, and ESG mandates prompt organizations to seek platforms with built-in governance. Google Cloud’s 35% regional growth reflects confidence in hyperscale infrastructure that meets sovereignty requirements.

The Middle East and Africa, plus South America, offer emerging opportunities. Uptake aligns with rising broadband coverage, but currency volatility and uneven regulatory maturity keep deployments phased. Vendors that bundle financing and localization services hold an edge.

Competitive Landscape

Competition is moderate, with a cluster of full-suite providers—Adobe, Microsoft, and Google—guarding entrenched bases through ecosystem breadth. Adobe’s Creative Cloud added USD 504 million in net-new annualized recurring revenue during FY25, reflecting consistent upsell into adjacent marketing clouds. Microsoft reported USD 13.9 billion in quarterly productivity revenues, bolstered by bundled AI co-pilot features that deepen stickiness.

Headless specialists—Sanity, Contentful, Storyblok—compete on speed, developer ergonomics, and composability. Sanity’s USD 85 million Series C validates investor confidence in data-centric operating systems that treat content as structured objects.[4]Sanity, “The End of CMS Era and Our $85M Series C,” sanity.io Contentful’s purchase of Ninetailed adds in-house personalization, illustrating an arms race to infuse AI at the edge of the experience layer.

M&A accelerates as incumbents scoop niche capabilities: IntelligenceBank bought Red Marker for automated compliance, while Sitecore emphasizes acquisition-led innovation to keep cloud momentum. White-space remains in regulated verticals where domain-specific templates and certifications lower adoption hurdles. Vendors able to quantify gains in asset velocity and campaign lift secure premium pricing despite SaaS inflation.

Content Creation Industry Leaders

Adobe Systems Incorporated

Aptara Inc.

Acrolinx GmbH

Apple, Inc.

Corel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sanity secured USD 85 million in Series C funding to position its Content Operating System as a unified, AI-ready hub.

- March 2025: Adobe embedded workflow agents into GenStudio via Microsoft 365 Copilot integration to speed multichannel content delivery.

- January 2025: Google raised Workspace prices while bundling Gemini AI features at no extra cost, intensifying value comparisons among SaaS suites.

- November 2024: Storyblok helped the National Retail Federation reduce website build time by 70% and integration time by 75% through a headless rollout

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

In our study, Mordor Intelligence defines the global content creation market as the yearly revenue earned by commercial-grade software platforms and cloud services that enable individuals and organizations to conceive, author, edit, publish, manage, and collaborate on digital text, image, audio, and video assets.

Scope Exclusion: We exclude hardware peripherals, influencer sponsorship income, and outsourced creative agency fees.

Segmentation Overview

- By Offerings

- Solutions (Software Tools)

- Services (Managed / Professional)

- By Deployment Mode

- Cloud

- On-premise

- By Enterprise Size

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- By Content Format

- Text

- Video

- Audio/Podcast

- Image/Graphics

- By End-user Vertical

- Media and Entertainment

- Retail and E-commerce

- Hospitality and Travel

- Government and Public Sector

- Education

- BFSI

- Healthcare and Life Sciences

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Several discussions with SaaS product managers, indie creators, studio CTOs, and regional software resellers across North America, Europe, and Asia-Pacific validated price corridors, seat expansion rates, and emerging AI adoption curves. Periodic client surveys reconciled unpaid user cohorts with licensed volumes.

Desk Research

Our analysts began with publicly available baselines from tier-1 sources such as the US Bureau of Labor Statistics' software spending tables, Eurostat's ICT usage survey, OECD Digital Economy Outlook, UNESCO culture statistics, and patent filings retrieved through Questel to map the global pool of professional and prosumer creators. We then layered company filings, IPO prospectuses, app-store revenue dashboards, trade papers from the Content Marketing Institute and the Interactive Advertising Bureau, plus news and financial records mined via Dow Jones Factiva and D&B Hoovers to capture firm-level momentum. This list is illustrative, with many additional sources referenced during validation.

Market-Sizing & Forecasting

We reconstruct global turnover through a top-down lens that marries national accounts, trade data, and creator population estimates. We corroborate outcomes with sampled average selling price multiplied by active seat roll-ups to retain bottom-up realism.

Key drivers in our model include paying-creator growth, cloud-subscription ARPU shifts, generative-AI productivity lifts, smartphone and tablet shipment trends, and regional broadband speeds. These inputs feed a multivariate regression with ARIMA overlays, while gaps in emerging markets are bridged using proxy adoption curves drawn from comparable digital tool rollouts.

Data Validation & Update Cycle

Outputs pass three-layer variance reviews; anomaly flags trigger analyst rework, and every figure is reread before sign-off. The model refreshes each year, with interim updates if material events such as major pricing shifts occur.

Why Mordor's Content Creation Baseline Remains the Most Dependable

Published estimates often diverge because firms choose different scopes, exchange-rate snapshots, or refresh calendars.

Our study reports only platform and software revenue in constant 2025 dollars and adjusts ASP progressions for the fast freemium-to-paid mix shift. Other publishers fold in agency services, use headline local currencies, or extrapolate linear user growth, which expands the gap.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.1 B | Mordor Intelligence | |

| USD 36.4 B | Global Consultancy A | Includes agency service fees and 2024 FX rates |

| USD 36.7 B | Industry Journal B | Treats perpetual licenses and subscriptions identically |

| USD 34.5 B | Regional Consultancy C | Relies on unverified creator counts from social platforms |

The comparison shows that by isolating true software turnover, standardizing currency, and checking seat counts with market voices, Mordor delivers a transparent, repeatable baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the content creation market?

The market is worth USD 43.44 billion in 2026 and is projected to reach USD 73.49 billion by 2031 at an 11.09% CAGR.

Which deployment model is growing fastest?

Cloud deployment leads with an 18.2% CAGR and already represents nearly 70% of global revenue.

Why are services outpacing solutions in growth?

AI integration and composable architectures increase complexity, prompting enterprises to engage professional and managed services that grow at a 16.28% CAGR.

Which region will add the most new revenue?

Asia-Pacific shows the highest regional CAGR at 16.88% due to aggressive digital transformation in markets such as Japan, China, and India.

What vertical is forecast to grow quickest?

Retail and e-commerce are expected to advance at a 15.52% CAGR because omnichannel shopping requires headless CMS and real-time personalization.

Page last updated on: