Thin Client Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

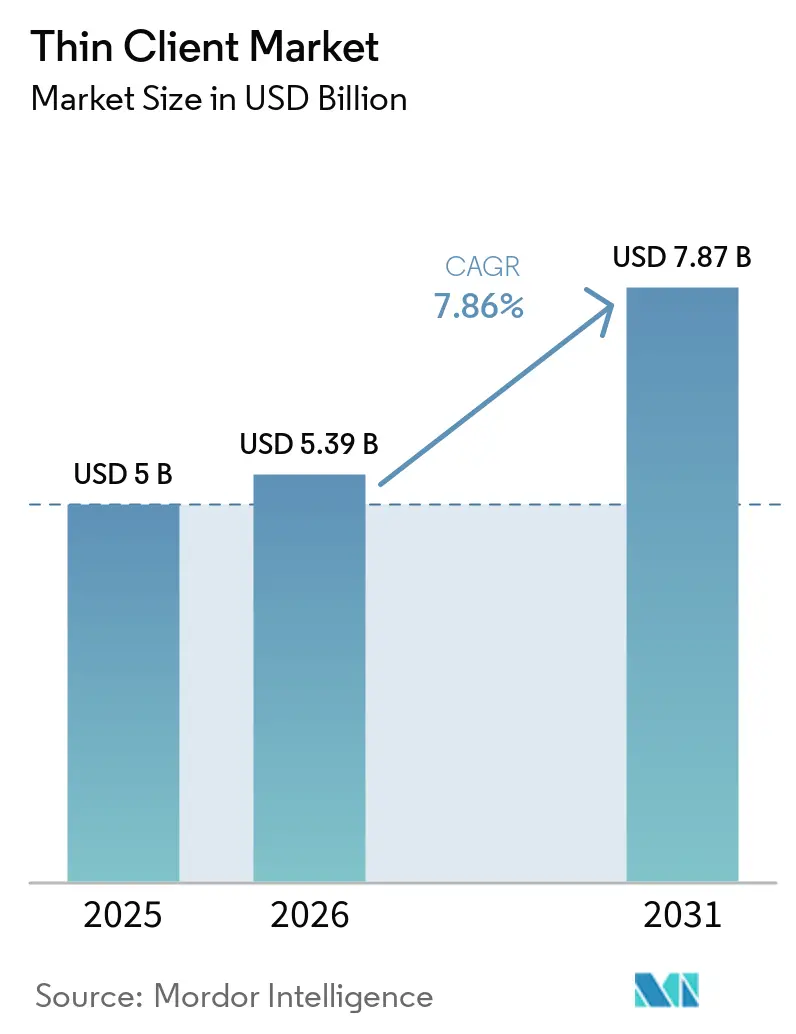

| Market Size (2026) | USD 5.39 Billion |

| Market Size (2031) | USD 7.87 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thin Client Market Analysis by Mordor Intelligence

The Thin Client Market size was valued at USD 5 billion in 2025 and estimated to grow from USD 5.39 billion in 2026 to reach USD 7.87 billion by 2031, at a CAGR of 7.86% during the forecast period (2026-2031). Heightened zero-trust mandates, hybrid-work enablement, and sustainability goals continue to redirect enterprise endpoint budgets toward centrally managed devices. Federal Executive Order 14028, the Department of Homeland Security's zero-trust blueprint, and parallel policies across Europe and Asia elevate secure endpoint procurement within both public and private organizations. Suppliers now blend lightweight hardware with cloud-native operating systems, allowing workers to launch virtual desktops from any location. This combination lowers desk-side support costs while meeting cyber-hygiene targets. Energy-efficiency directives and rising electricity prices add financial urgency, especially as boards commit to scope-2 carbon reporting in 2025 across North America and Europe.

Key Report Takeaways

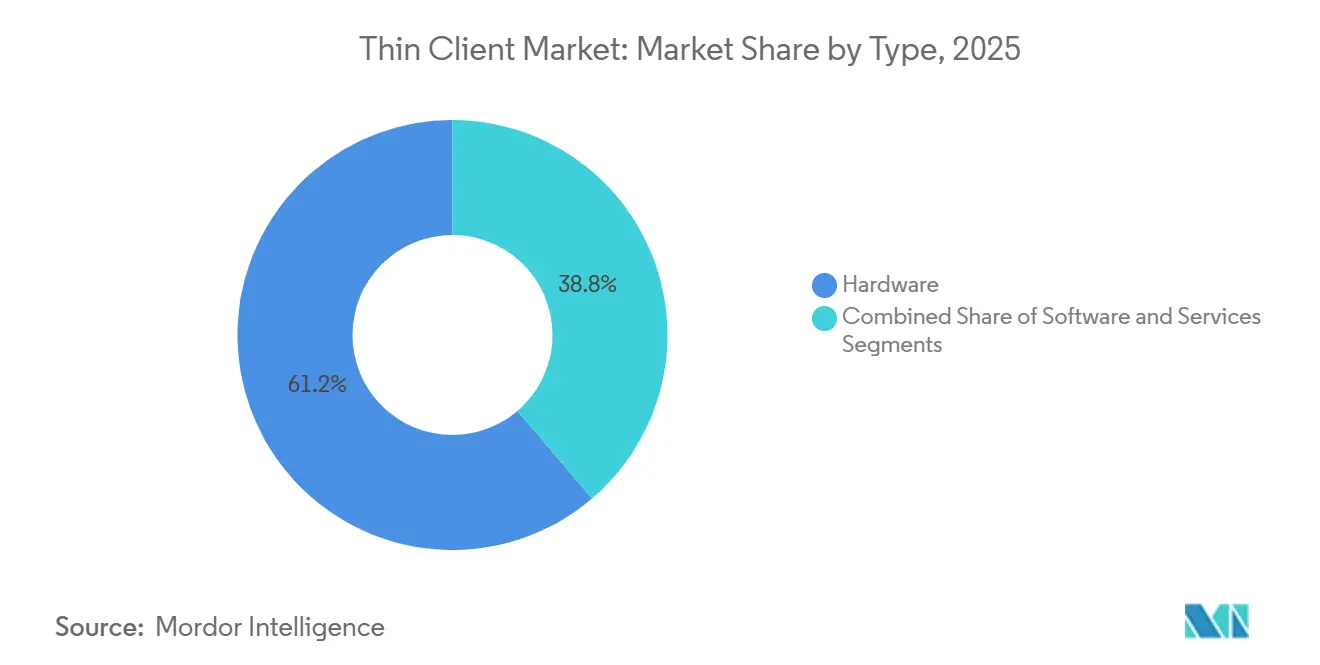

- By type, hardware commanded 61.32% of revenue in 2025; software and services are forecast to grow at a 8.26% CAGR through 2031.

- By end user, IT and telecom held 28.48% of the thin client market share in 2025, while healthcare is advancing at a 9.26% CAGR through 2031.

- By form factor, desktop units accounted for 47.21% of shipments in 2025, and mobile devices are projected to rise at an 8.46% CAGR through 2031.

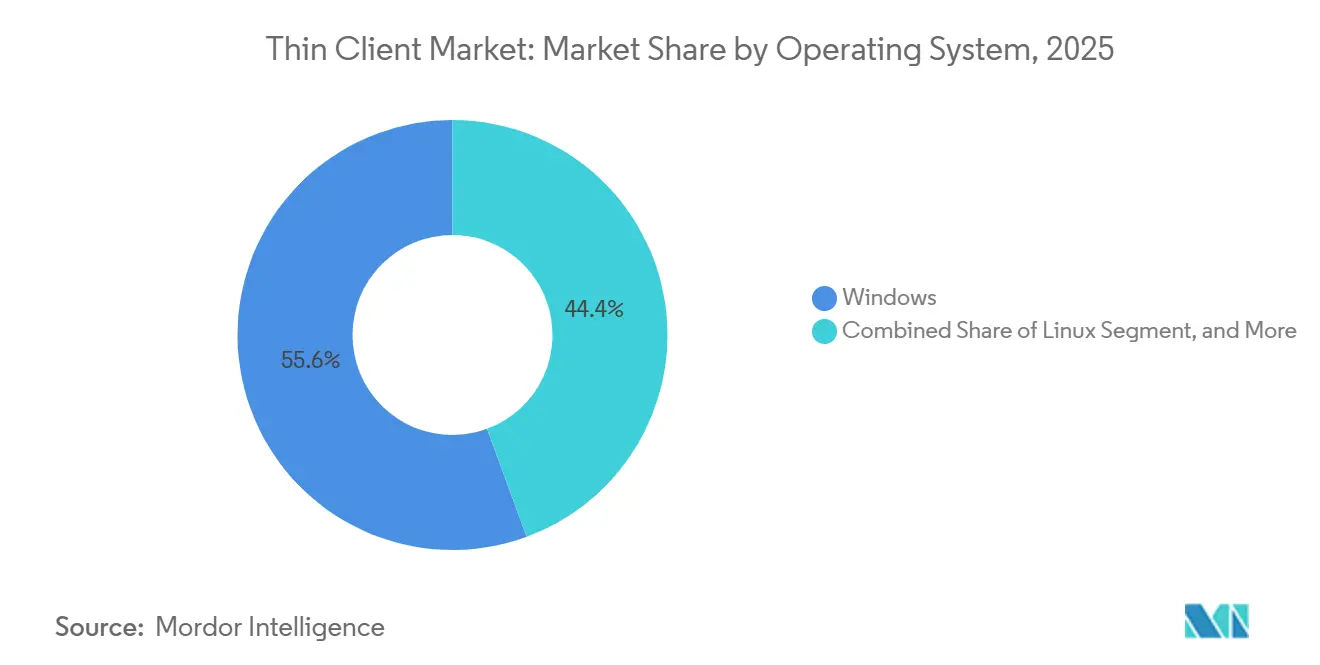

- By operating system, Windows captured 55.62% of the installed base in 2025; Chrome OS is set to expand at an 8.71% CAGR to 2031.

- By deployment model, cloud installations accounted for 44.98% of the thin client market in 2025, and hybrid configurations recorded an 8.34% CAGR through 2031.

- By geography, North America generated 36.21% of revenue in 2025, while Asia-Pacific exhibits the fastest trajectory at an 8.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thin Client Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Pandemic Hybrid-Work VDI Boom | +2.1% | Global, North America and Europe focus | Medium term (2-4 years) |

| Endpoint Cost and Energy-Saving Mandates | +1.8% | Global, especially Europe and North America | Medium term (2-4 years) |

| Rising Cybersecurity and Zero-Trust Roll-Outs | +1.5% | Global, early in BFSI and government | Short term (≤ 2 years) |

| AI-PC Refresh Enables Legacy Conversions | +1.3% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Scope-2 Carbon Reporting Pushes Low Wattage | +0.9% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Edge Workforce Expansion Favors Centralized | +0.7% | Global, manufacturing and retail emphasis | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Hybrid Work VDI Boom

Virtual desktop infrastructure shifted from a niche IT project to a default access layer for distributed staff. General Dynamics Information Technology adopted Zscaler’s zero-trust cloud to secure thousands of remote connections in one month, keeping federal compliance intact. Bolton NHS Foundation Trust trimmed clinician log-on time to three seconds with IGEL OS thin terminals that roam between wards, illustrating workflows beyond knowledge-worker desks. Legal practices and insurers repeat the model to deliver governed access without shipping full PCs to each lawyer or agent. The thin client market, therefore, benefits from a structural redesign in workspace provisioning rather than a temporary pandemic spike.

Endpoint Cost and Energy-Saving Mandates

Thin clients typically draw one-third the power of tower PCs and last 8 years or more, delivering measurable utility savings. Public-sector buyers in Europe increasingly score bids on wattage, putting legacy desktops at a disadvantage. Lenovo’s sub-USD 200 V100 Q, launched in March 2025, shows how vendors strip non-essentials to meet aggressive cost targets.[1]Lenovo Group Ltd, “V100 Q Thin Client Launch,” lenovo.com When paired with centralized management that slashes on-site visits, the total lifecycle bill for mass deployments in retail or government facilities drops sharply. Energy efficiency regulations will tighten after 2027, extending this tailwind.

Rising Cybersecurity and Zero-Trust Roll-Outs

Executive Order 14028 positions zero-trust controls, including multifactor authentication, encrypted DNS, and endpoint detection, as baseline across all federal contracts. The Department of Homeland Security clarified that device inventory and isolation sit at the core of every agency’s roadmap. Private suppliers matching these requirements remain eligible for thousands of government tenders. As a result, Dell, HP, and Lenovo now preload firmware hooks for credential isolation while IGEL wraps its Secure OS with read-only partitions. By substituting legacy PCs with centrally managed stateless terminals, agencies shrink the attack surface and raise compliance scores.

AI-PC Refresh Pushes Legacy PC Conversions

Premium-priced AI-ready laptops put budget pressure on other parts of the fleet, prompting IT managers to repurpose older PCs as thin clients rather than discard them. 10ZiG’s RepurpOS converts Windows 10 systems via a lightweight overlay, extending hardware life and avoiding capital outlays.[2]10ZiG Technology, “RepurpOS Platform,” 10zig.com Google’s remote installer for ChromeOS Flex, introduced in July 2025, lets administrators migrate endpoints without physical touch, cutting labor costs. Organizations staring at the October 2025 Windows 10 end-of-support deadline are accelerating conversions, underpinning steady shipment demand even as new device ASPs decline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unreliable Network Latency in Emerging Markets | -1.2% | Asia-Pacific emerging, Middle East and Africa | Medium term (2-4 years) |

| GPU-Intensive Workload Performance Gaps | -0.9% | Global, design and media sectors | Short term (≤ 2 years) |

| DaaS or VDI Seat-Price Inflation | -0.7% | Global, heavier on small and midsize enterprises | Medium term (2-4 years) |

| Fragmented Peripheral Driver Support | -0.5% | Global, healthcare and manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unreliable Network Latency in Emerging Markets

India’s Digital Public Infrastructure covers millions of citizens, yet 4G coverage gaps in rural areas slow thin client streaming sessions. ERPNext roll-outs for state services work smoothly in urban Maharashtra but struggle in remote districts where throughput drops below 2 Mbps. Bhutan and Saudi Arabia experienced similar constraints outside capital regions. For telehealth or digital classrooms, intermittent latency harms user experience and can prompt fallback to local PCs, hindering broader thin-client deployment until fiber or 5G densification arrives.

GPU-Intensive Workload Performance Gaps

Designers running CAD or media professionals editing 4K footage need constant high-bandwidth GPU rendering. Even though cloud GPU services exist, round-trip delay and data egress fees often push studios to keep local workstations. Semiconductor vendors still prioritize sub-11 nm node production for high-performance clients, sustaining a market niche where thin devices cannot yet compete. Some organizations, therefore, operate mixed fleets, placing thin clients at general office desks while retaining workstations for creatives, limiting the total thin client market size reachable by 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software-defined Platforms Reshape Deployments

The thin client market size for hardware equaled USD 3.06 billion in 2025, giving physical terminals a 61.24% revenue lead. Yet software and services is expanding at 11.62% CAGR, twice the hardware pace, as customers pivot to subscription licenses that unlock multi-vendor devices. IGEL’s 2025 COSMOS platform provides a single control plane for any x86 or Arm client, encouraging reuse of existing PCs rather than outright hardware swaps. Cloud Software Group invested USD 1.65 billion in Microsoft Azure capacity to pre-stage managed desktop sessions, proving that endpoint value is shifting to orchestration software.

Vendors adapt by bundling thin firmware on rebadged mini-PCs while monetizing annual support tiers. Dell’s fiscal 2025 report revealed margin pressure in hardware but strong pull-through on infrastructure services. Under the Windows 10 end-of-support deadline, IT teams license secure OS images that run well on aging processors, deferring capital spend. Over 2026-2031, hardware share is expected to decline gradually as enterprises favor SaaS consoles over proprietary terminals, even though absolute device shipments may still rise.

By End-User Industry: Healthcare Speeds Digital Care

IT and telecom led consumption with 28.48% of the thin client market share in 2025, reflecting long-standing VDI adoption in help desks and NOC environments. Healthcare, however, posts the fastest 9.26% CAGR through 2031 as electronic health record mandates and data-sovereignty statutes elevate secure endpoint demand. India’s ESIC rolled out 31,000 virtual desktops, centralizing patient data and trimming support visits. Pennine Acute Hospitals in the United Kingdom saved GBP 500,000 (USD 630,000) annually after switching to fanless units that cut power and break-fix tickets.[3]National Health Service UK, “Pennine Acute Hospitals Thin Client Savings,” nhs.uk

Retail, manufacturing, and education, while not leading sectors, still derive significant benefits from adopting standardized workflows enabled by thin clients. In the retail sector, point-of-sale stations rely on thin clients' reliability and security to ensure seamless transactions and minimize downtime. Similarly, in manufacturing, shop-floor terminals leverage the durability and efficiency of thin clients to streamline operations and maintain productivity. In the education sector, classroom labs use thin clients for their low failure rates, simplified management, and locked-down software stacks, which help create a secure, controlled learning environment. These advantages collectively contribute to a diversified customer base, providing stability and mitigating the impact of vertical cyclicality across these industries.

By Form Factor: Mobile Gains Traction as Workflows Decentralize

Desktops retained 47.21% of the market share in 2025, yet mobile thin clients are growing at an 8.46% CAGR as clinicians, field engineers, and store associates require portable yet secure devices. Saskatchewan Polytechnic deployed 3,200 ChromeOS units across classrooms and common spaces, mixing clamshells with tablets to support blended learning. Convertible designs with stylus input meet bedside charting needs, while ruggedized shells suit warehouse scanning duties.

Cost remains in favor of desktops for use in cubicles and kiosks due to their affordability and widespread availability. However, advancements in technology, such as falling battery prices and the development of fanless ARM chipsets, are gradually narrowing the cost gap between desktops and alternative devices. These advancements make other options, like thin clients and all-in-one models, increasingly viable for businesses seeking efficiency and modernized setups. All-in-one models, in particular, maintain a stable niche in environments such as reception desks and executive suites, where the emphasis on reducing cable clutter and achieving a sleek, professional aesthetic outweighs concerns about price sensitivity. This trend highlights the growing demand for devices that combine functionality with visual appeal in specific workplace settings.

By Operating System: Chrome OS Squeezes Legacy Windows Dominance

Windows maintained its dominant position, accounting for 55.62% of installations in 2025. However, Chrome OS is rapidly gaining traction, recording an impressive 8.71% CAGR as educational districts and nonprofit organizations increasingly prioritize cost-effective licensing solutions. Google’s remote conversion tool, ChromeOS Flex, enables large-scale deployments without requiring on-site visits, significantly reducing migration-related labor costs. Ayrshire College demonstrated the financial and operational benefits of this approach by integrating Google Workspace into a GBP 53 million (approximately USD 67 million) campus modernization project, which emphasized the importance of low-touch device management for streamlined operations.

Linux-based operating systems continue to play a critical role in regulated sectors due to their flexibility and security features. Citrix’s acquisition of Unicon in January 2025 added the eLux OS to its product portfolio, enabling seamless integration with Citrix Workspace and enhancing its appeal to organizations requiring robust endpoint management solutions. Additionally, niche proprietary platforms remain essential for specific use cases, particularly in kiosk and embedded system deployments. These platforms often feature locked firmware, which simplifies compliance with stringent regulatory requirements and ensures secure, reliable operations in specialized environments.

By Deployment Model: Hybrid Configurations Optimize Cost and Control

Cloud accounts for 44.98% of the thin client market size as of 2025 and is projected to maintain an 8.34% CAGR through 2031. This growth is driven by the increasing adoption of pay-as-you-go Desktop-as-a-Service (DaaS) solutions, which eliminate the need for significant capital expenditure on servers. However, certain latency-sensitive environments, such as trading desks and classified workloads, continue to rely on on-premises infrastructure. This reliance has positioned hybrid architecture as the fastest-growing segment within the market. Hybrid solutions offer the flexibility to combine cloud and on-premise systems, catering to diverse operational needs. Microsoft has responded to this trend by introducing a unified console that integrates Windows 365 with Azure Virtual Desktop and local Active Directory. This integration enables administrators to enforce consistent policies across both cloud-based and on-premise environments, ensuring seamless management.

Small and midsize enterprises are increasingly adopting cloud solutions due to their predictable billing structures, which simplify financial planning. In contrast, Fortune 500 organizations are optimizing mixed deployments to strike a balance between cost efficiency and data sovereignty. This strategic approach to deployment diversity has sustained the demand for integration software, further reinforcing the trend of shifting revenue streams toward subscription-based platforms. The growing reliance on subscription models underscores the evolving preferences of organizations seeking scalable,d flexible solutions to meet their operational requirements.

Geography Analysis

North America accounted for 37.58% of 2025 revenue, driven by the implementation of codified zero-trust regulations and extensive enterprise refresh programs. The Cybersecurity and Infrastructure Security Agency (CISA) confirmed in its January 2025 scorecard that multifactor authentication had been deployed agency-wide. This development significantly boosted orders for stateless devices capable of enforcing a robust endpoint posture. Additionally, private contractors have adopted similar standards to remain eligible for government contracts, thereby aligning security architectures across critical sectors such as defense, healthcare, and financial services ecosystems.

Asia-Pacific is emerging as the primary growth engine, with the market projected to grow at a compound annual growth rate (CAGR) of 10.47% through 2031. Countries like India, Indonesia, and Vietnam are channeling substantial digitization funds into public-service cloud infrastructure. The Account Aggregator framework in these regions enables lenders to securely access citizen data, while administrators increasingly favor centrally managed clients to ensure personal records remain off branch PCs. The industrial sector is also witnessing significant advancements, as demonstrated by Foxconn, which streams virtual machines to shop floors for quality control purposes, effectively reducing plant downtime. To cater to the growing demand, IGEL established a Singapore hub in collaboration with CXA in October 2024, aiming to shorten channel lead times and provide local language support to its customers.

Europe is experiencing steady growth, primarily driven by stringent data-protection compliance requirements and carbon reduction targets that incentivize the adoption of low-wattage endpoints. Meanwhile, South America and the Middle East exhibit selective demand growth, particularly in government and oil-and-gas verticals. A notable development in the region includes Lenovo’s USD 2 billion venture with Alat in 2025, which aims to establish a regional supply base for the Gulf. This move reflects growing confidence in the region's infrastructure readiness and its potential to support future market expansion.

Competitive Landscape

The thin client market shows moderate concentration, with key players leveraging their existing strengths to maintain competitiveness. Dell, HP, and Lenovo capitalize on their established PC supply chains and enterprise contracts to secure bundled refresh deals, which provide them with a consistent revenue stream. IGEL’s acquisition of Stratodesk has significantly bolstered its market position, creating a 5 million-seat software powerhouse. This acquisition enhances IGEL’s ability to offer license subscriptions alongside its white-label hardware, providing customers with a comprehensive solution. Similarly, Citrix’s integration of eLux has extended its control from the data center to the device level, enabling it to deliver a fully curated stack that is particularly appealing to industries with stringent regulatory requirements.

Emerging disruptors are also making their presence felt in the market. For instance, 10ZiG has introduced RepurpOS, a solution specifically designed for cost-sensitive fleets, offering a viable option for organizations with budget constraints.[4]Google LLC, “ChromeOS Flex for Enterprise,” google.com Meanwhile, Google is promoting Chrome OS Flex as a free operating system for converting legacy devices, targeting businesses looking to extend the lifecycle of their existing hardware. Microsoft’s introduction of the Windows 365-optimized Link device signals a move toward deeper vertical integration. This strategy could potentially challenge independent vendors, especially if Microsoft bundles these devices under enterprise agreements, making them more attractive to large-scale organizations.

As hardware margins continue to tighten, vendors are increasingly focusing on differentiation through value-added services. These include remote provisioning capabilities, advanced analytics, and robust security certifications, which are becoming critical factors in purchasing decisions. Despite the dominance of the top five suppliers, who collectively control approximately 60% of the market revenue, there remains a significant opportunity for niche specialists. These smaller players are carving out their space by addressing specific needs in sectors such as healthcare, education, and industrial ruggedization, where tailored solutions are often required.

Thin Client Industry Leaders

Dell Inc.

LG Electronics Inc.

Fujitsu Ltd.

HP Inc.

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Microsoft cut Windows 365 subscription prices by 20%, amplifying competitive pressure on rival DaaS platforms.

- April 2026: Services Australia consolidated its virtual desktop infrastructure to enhance nationwide disaster-recovery readiness.

- April 2026: Tilon entered Japan with an AI-native VDI platform targeting enterprise customers.

- March 2026: 10ZiG released Manager v5.5, adding cloud-based fleet analytics to simplify multi-site administration.

Global Thin Client Market Report Scope

The Thin Client Market refers to the global industry encompassing hardware, software, and services that enable centralized computing architectures in which lightweight client devices depend on remote servers or cloud-based infrastructure for processing, application execution, and data storage. These solutions replace traditional full-featured personal computers with simplified endpoints that connect to virtual desktop environments, improving manageability, security, and cost efficiency for organizations across sectors.

The Thin Client Market Report is Segmented by Type (Hardware, Software, and Services), End-User Industry (BFSI, IT and Telecom, Healthcare, Government, Retail, Manufacturing, and Education), Form Factor (Desktop, All-in-One, and Mobile), Operating System (Windows, Linux, Chrome OS, and Other Operating Systems), Deployment Model (On-Premise, Cloud, and Hybrid), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software and Services |

| BFSI |

| IT and Telecom |

| Healthcare |

| Government |

| Retail |

| Manufacturing |

| Education |

| Desktop Thin Clients |

| All-in-one Thin Clients |

| Mobile Thin Clients |

| Windows |

| Linux |

| Chrome OS |

| Other Operating Systems |

| On-Premise |

| Cloud |

| Hybrid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type | Hardware | ||

| Software and Services | |||

| By End-User Industry | BFSI | ||

| IT and Telecom | |||

| Healthcare | |||

| Government | |||

| Retail | |||

| Manufacturing | |||

| Education | |||

| By Form Factor | Desktop Thin Clients | ||

| All-in-one Thin Clients | |||

| Mobile Thin Clients | |||

| By Operating System | Windows | ||

| Linux | |||

| Chrome OS | |||

| Other Operating Systems | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the thin client market by 2031?

The thin client market size is forecast to reach USD 7.87 billion by 2031, growing at a 7.86% CAGR.

Which end-user industry is expanding the fastest?

Healthcare leads growth with a projected 9.26% CAGR through 2031 as electronic health record mandates drive secure endpoint adoption.

How much revenue did hardware contribute in 2025?

Hardware represented 61.32% of 2025 revenue, underscoring its dominance in the overall spend mix.

Which region is expected to grow quickest?

Asia-Pacific shows the fastest trajectory at an 8.89% CAGR to 2031, propelled by government digitization and manufacturing upgrades.

What is driving the switch from PCs to thin clients?

Lower energy use, centralized security, and reduced total cost of ownership, all reinforced by hybrid-work VDI strategies, are motivating organizations to migrate.

Page last updated on: