Market Overview

| Study Period | 2020 - 2031 |

|---|---|

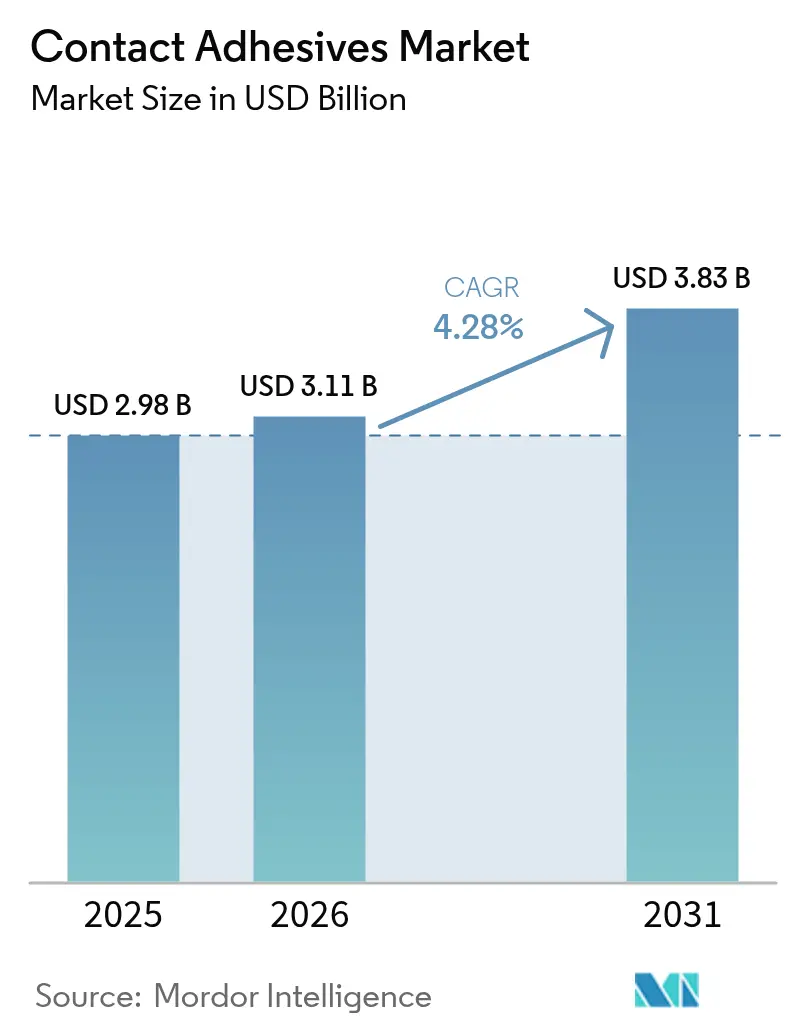

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 3.83 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contact Adhesives Market Analysis by Mordor Intelligence

The Contact Adhesives Market size in 2026 is estimated at USD 3.11 billion, growing from 2025 value of USD 2.98 billion with 2031 projections showing USD 3.83 billion, growing at 4.28% CAGR over 2026-2031. This growth path shows a maturing core business now supported by new demand in electric-vehicle battery packs and renewable-energy maintenance. Immediate-bond applications such as footwear assembly, modular furniture, and on-site construction keep the contact adhesives market firmly rooted in traditional sectors where instant tack and repositioning resistance remain critical. Meanwhile, regulatory pressure to lower volatile-organic-compound (VOC) emissions is accelerating the shift toward waterborne formulations, opening room for innovation without compromising bonding performance. Supply-chain resilience, especially in Asia-Pacific, underpins price stability even as chloroprene monomer shortages and raw-material volatility periodically challenge manufacturers. Finally, automation in Asian footwear plants and rising repair work on wind-turbine blades are creating white-space opportunities that allow premium pricing for specialized grades.

Key Report Takeaways

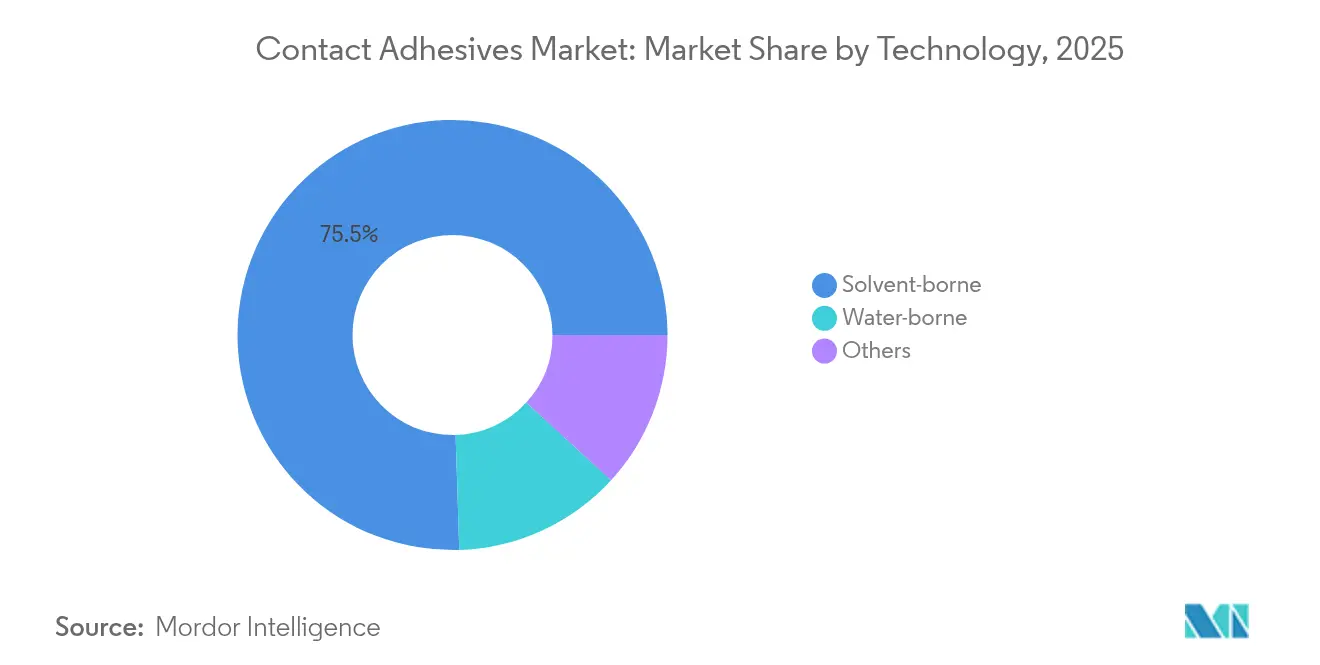

- By technology, solvent-borne systems led with 75.50% revenue share in 2025, while water-borne systems are projected to expand at a 4.85% CAGR to 2031.

- By polymer, polychloroprene held 59.65% of the contact adhesives market share in 2025 and is growing at a 4.8% CAGR through 2031.

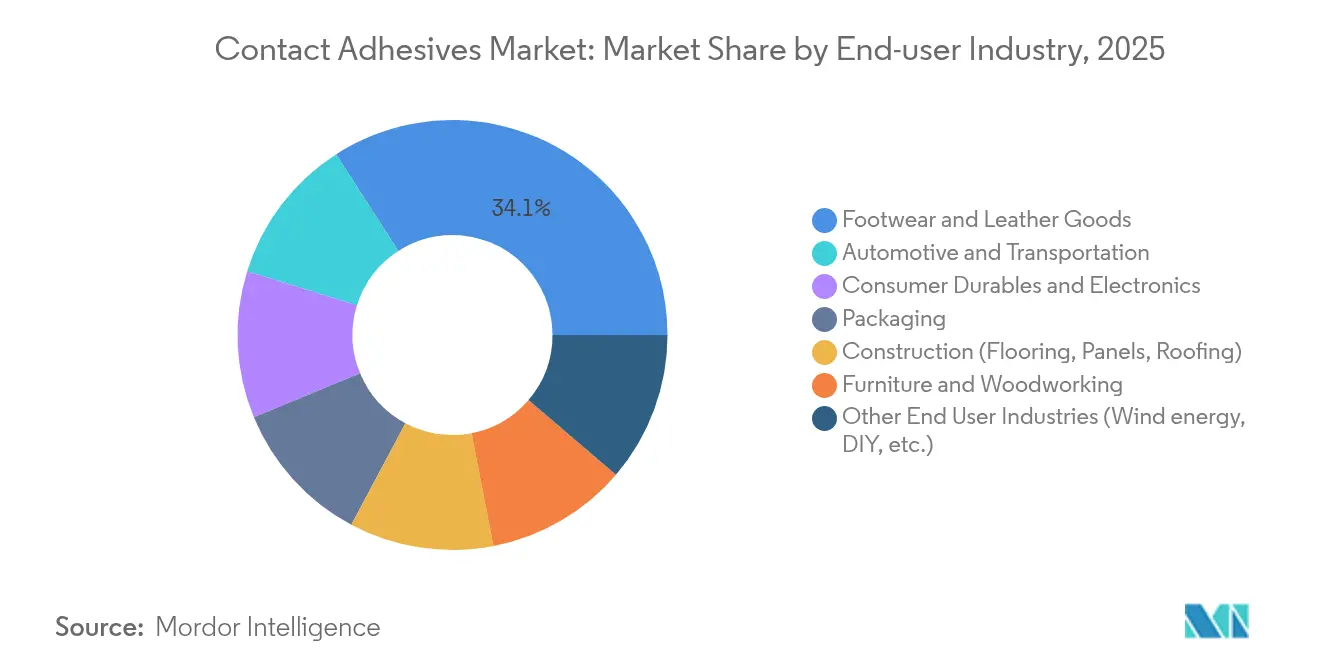

- By end-user industry, footwear and leather goods accounted for 34.10% of the contact adhesives market size in 2025 and are advancing at a 4.75% CAGR to 2031.

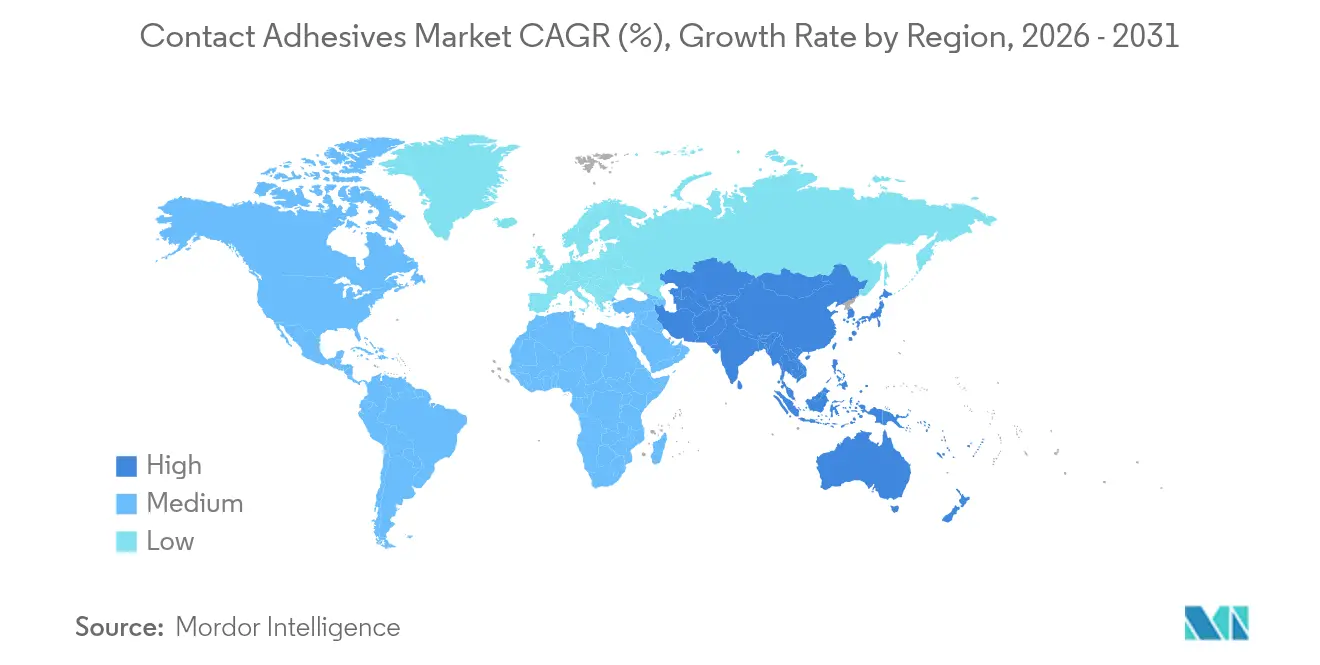

- By geography, Asia-Pacific commanded 59.10% of the contact adhesives market size in 2025 and is forecast to grow at a 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contact Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to low-VOC waterborne systems | +1.2% | Global, strongest in North America and the EU | Medium term (2-4 years) |

| Booming modular furniture and interior fitouts | +0.8% | Global, high in APAC urban centers | Short term (≤ 2 years) |

| Integration of robotic adhesive-dispensing lines in Asian footwear plants | +0.6% | APAC core, spill-over to Latin America | Medium term (2-4 years) |

| Repair demand for wind-turbine blades | +0.4% | Global, early gains in Europe, North America, and China | Long term (≥ 4 years) |

| Thermal-insulation bonding inside EV battery packs | +0.7% | Global, strongest in China, North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Low-VOC Water-Borne Systems

Regulatory momentum is reshaping formulation strategies as tougher VOC caps in California and Canada’s 2024 national limits push manufacturers toward waterborne products[1]Government of Canada, “Volatile Organic Compound Concentration Limits for Certain Products Regulations,” canada.ca. The economics now favor the scale production of solvent-free grades that meet multiple jurisdictions with a single recipe. Proposed United States restrictions on N-Methylpyrrolidone at 45% concentration for consumer adhesives narrow the solvent palette further, driving research and development toward completely water-based chemistries. Product launches such as 3M Fastbond 1049 show that the contact adhesives market can meet performance benchmarks without solvent carriers. As a result, suppliers anticipate incremental price premiums for compliant grades and broader uptake in cost-sensitive Asian factories as formulations reach parity on open time and green strength.

Booming Modular Furniture and Interior Fitouts

Urban densification and hybrid workspaces are fueling modular construction techniques that favour adhesive-based assembly over mechanical fasteners. Adhesive solutions trim weight, enhance aesthetics, and cut installation time, aligning with Asia-Pacific’s fast-track residential and commercial build cycles. Projects that rely on pre-finished panels and lightweight composites often specify contact adhesives for their high initial tack, enabling vertical mounting without clamping. The modular trend also improves circularity because glued components can be removed cleanly for reuse or recycling. Together, these factors lift short-term demand in the contact adhesives market by an estimated 0.8 percentage points.

Integration of Robotic Adhesive-Dispensing Lines in Asian Footwear Plants

Automation delivers consistent bead geometry, cuts reject rates by 40%, and drops labor expenses by half in Vietnam, Thailand, and Indonesia, which collectively produce more than half the world’s athletic shoes. Henkel’s Bien Hoa Application Center demonstrates how suppliers now bundle robots, vision systems, and adhesives to offer turnkey packages. Robots also accommodate waterborne grades whose viscosity and open time differ markedly from solvent variants, reducing the learning curve for regulatory-driven transitions. This technology upgrade adds 0.6 percentage points to the medium-term CAGR of the contact adhesives market.

Repair Demand for Wind-Turbine Blades

First-generation wind farms are exiting warranty and require leading-edge bond repairs that must withstand freeze–thaw cycles, salt spray, and UV exposure. Adhesive degradation has become a primary failure mode, creating demand for high-modulus, moisture-tolerant products such as SikaPower 830. Research suggests that controlled moisture uptake can accelerate cure kinetics, shortening repair downtime.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.9% | Global, strongest in cost-sensitive APAC markets | Short term (≤ 2 years) |

| Stringent VOC and flammability rules | -0.6% | North America and EU, spill-over to export-oriented APAC | Medium term (2-4 years) |

| Global chloroprene monomer supply disruptions | -0.7% | Global, acute in neoprene-dependent applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Polymer-grade propylene, chloroprene, and natural rubber prices have swung sharply on supply cuts, weather events, and logistics bottlenecks. Small producers are hit hardest because they lack leverage to secure long-term supply contracts. Ethylene and propylene profitability remains weak in Asia, discouraging reinvestment and heightening the risk of further cost spikes. Inventory buffers and dual sourcing offer partial relief but capex decisions for new contact adhesives market capacity are delayed amid uncertainty.

Stringent VOC and Flammability Rules

Europe’s upcoming broad per- and polyfluoroalkyl substances (PFAS) restrictions and formaldehyde limits under REACH Annex XVII, effective August 2026, mandate extensive reformulation and extra testing[2]TÜV SÜD, “Formaldehyde Emission Limits under REACH Annex XVII,” tuvsud.com. The United States Environmental Protection Agency ban on trichloroethylene and perchloroethylene compounds imposes these obligations. Compliance favors multinationals with dedicated regulatory teams, widening the competitive gap and trimming 0.6 percentage points from the contact adhesives market CAGR during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solvent-Borne Dominance Faces Water-Borne Challenge

Solvent-borne systems retained 75.50% of the contact adhesives market in 2025, thanks to unmatched open-time flexibility and high initial tack. Footwear production lines, for instance, rely on rapid grab that keeps assembly throughput high. Yet waterborne grades are growing at a 4.85% CAGR due to VOC rules and advancements in resin emulsification that narrow the performance gap. California’s latest consumer-products rule and Canada’s 2024 VOC cap accelerate global standardization efforts toward solvent-free solutions.

Hot-melt and reactive chemistries play niche roles where temperature resistance or instant set outweigh cost. Suppliers such as 3M now advertise entirely solvent-free lines that equal older chloroprene formulations in peel strength, proving technology convergence is feasible. Over the forecast period, the contact adhesives market size for water-borne formulations is expected to reach USD 520 million, reflecting steady substitution in regulated regions.

By Polymer: Polychloroprene Resilience Despite Supply Challenges

Polychloroprene commanded 59.65% of the contact adhesives market in 2025 due to its chemical resistance and balanced elasticity. Growth of 4.8% through 2031 underscores the polymer’s staying power despite episodic supply shocks. Styrene-butadiene rubber caters to lower-cost applications with less demanding performance, while acrylic copolymers gain ground for UV-exposed surfaces. Polyurethane grades offer superior impact resistance that suits structural laminations in wind-turbine blades and electric-vehicle battery trays. Henkel’s recent pilot runs of bio-based neoprene alternatives indicate the first serious commercial exploration of greener drop-ins.

By End-User Industry: Footwear Leadership Drives Asian Manufacturing

The footwear and leather segment retained 34.10% of the contact adhesives market in 2025, expanding at 4.75% through 2031. Asian contract manufacturers ramp up robotic adhesive-dispensing lines that boost quality by 40% and reduce material waste. Consumer electronics follow, thanks to rising unit volumes of tablets, laptops, and foldable devices that demand thin-film bonding with controlled thermal dissipation. Packaging applications turn to solvent-free grades that align with brand-owner sustainability pledges. Automotive adoption centers on battery-pack thermal insulation and interior light-weighting, two areas set to raise per-vehicle adhesive usage above 2 kg by 2030. Construction remains a steady consumer of contact adhesives in flooring, partition panels, and roofing membranes, especially in fast-urbanizing economies.

Geography Analysis

Asia-Pacific held 59.10% of the contact adhesives market in 2025 and is projected to post a 4.92% CAGR, driven by China’s diversified manufacturing base and India’s government-led push for import substitution. Vietnam, Thailand, and Indonesia invest heavily in smart factories for athletic shoes, pushing regional demand for precise, low-VOC formulations. Despite periodic raw-material volatility, proximity to resin producers keeps landed costs favorable compared with imports into Europe or North America.

North America maintains a robust demand anchored in electric-vehicle production and stringent environmental standards. Automakers increasingly specify waterborne adhesives to secure credits under the United States Advanced Clean Transportation program, raising North American uptake for compliant grades. Regional suppliers leverage strong intellectual-property positions to command price premiums, boosting margins even as sales volumes grow at a moderate pace.

Europe’s mature market is notable for regulatory leadership. Broad PFAS and formaldehyde restrictions under REACH prompt accelerated reformulation cycles. Europe also hosts a large installed base of wind-turbine blades now entering their repair life phase, placing specialized contact adhesives in steady demand.

South America and the Middle East, and Africa offer frontier opportunities tied to residential construction and light manufacturing. Currency volatility remains a headwind, yet regional governments are rolling out industrial parks with tax incentives that could attract adhesive converters.

Competitive Landscape

The market shows moderate fragmentation. Product portfolios are shifting toward waterborne and bio-based technologies to pre-empt tightening VOC and PFAS rules. Large players capitalize on scale to roll out globally harmonized formulations that simplify qualification for multinational customers. Regional challengers focus on niche opportunities such as low-cost neoprene alternatives or climate-specific grades for equatorial markets. Some Chinese suppliers have begun exporting turnkey robotic dispensing systems bundled with proprietary adhesives, thus competing on total cost of ownership.

Contact Adhesives Industry Leaders

Henkel AG & Co. KGaA

Sika AG

3M

H.B. Fuller Company

Arkema (Bostik)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Henkel and Celanese collaborated to produce water-based adhesives using carbon-capture vinyl acetate monomer for sustainable packaging applications in paper and board, e-commerce, and labeling.

- June 2024: Saint-Gobain acquired Dubai-based FOSROC for USD 1.025 billion, expanding its construction chemicals footprint across 73 countries

Global Contact Adhesives Market Report Scope

The scope of the contact adhesives market report includes:

By Technology

| Water-borne |

| Solvent-borne |

| Others |

By Polymer

| Polychloroprene (Neoprene) |

| Styrene-Butadiene Rubber (SBR) |

| Acrylic Copolymers |

| Polyurethane |

| Nitrile and Others |

By End-user Industry

| Consumer Durables and Electronics |

| Packaging |

| Automotive and Transportation |

| Furniture and Woodworking |

| Footwear and Leather Goods |

| Construction (Flooring, Panels, Roofing) |

| Other End User Industries (Wind energy, DIY, etc.) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Technology | Water-borne | |

| Solvent-borne | ||

| Others | ||

| By Polymer | Polychloroprene (Neoprene) | |

| Styrene-Butadiene Rubber (SBR) | ||

| Acrylic Copolymers | ||

| Polyurethane | ||

| Nitrile and Others | ||

| By End-user Industry | Consumer Durables and Electronics | |

| Packaging | ||

| Automotive and Transportation | ||

| Furniture and Woodworking | ||

| Footwear and Leather Goods | ||

| Construction (Flooring, Panels, Roofing) | ||

| Other End User Industries (Wind energy, DIY, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global contact adhesives market?

The market is valued at USD 3.11 billion in 2026 and is projected to reach USD 3.83 billion by 2031.

What is the expected growth rate of the contact adhesives market through 2031?

The market is forecast to grow at a 4.28% compound annual growth rate (CAGR) from 2026 to 2031.

Which technology segment leads the contact adhesives market?

Solvent-borne systems held 75.50% revenue share in 2025, remaining the dominant technology despite rising demand for low-VOC water-borne alternatives.

Why are water-borne contact adhesives gaining traction?

Stricter VOC regulations in regions such as North America and the EU are accelerating adoption of water-borne formulations that reduce emissions without sacrificing performance.

Which end-user industry accounts for the largest market share?

Footwear and leather goods lead with 34.10% share in 2025, supported by rising automation in Asian manufacturing plants.

Page last updated on: