Electrically Conductive Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

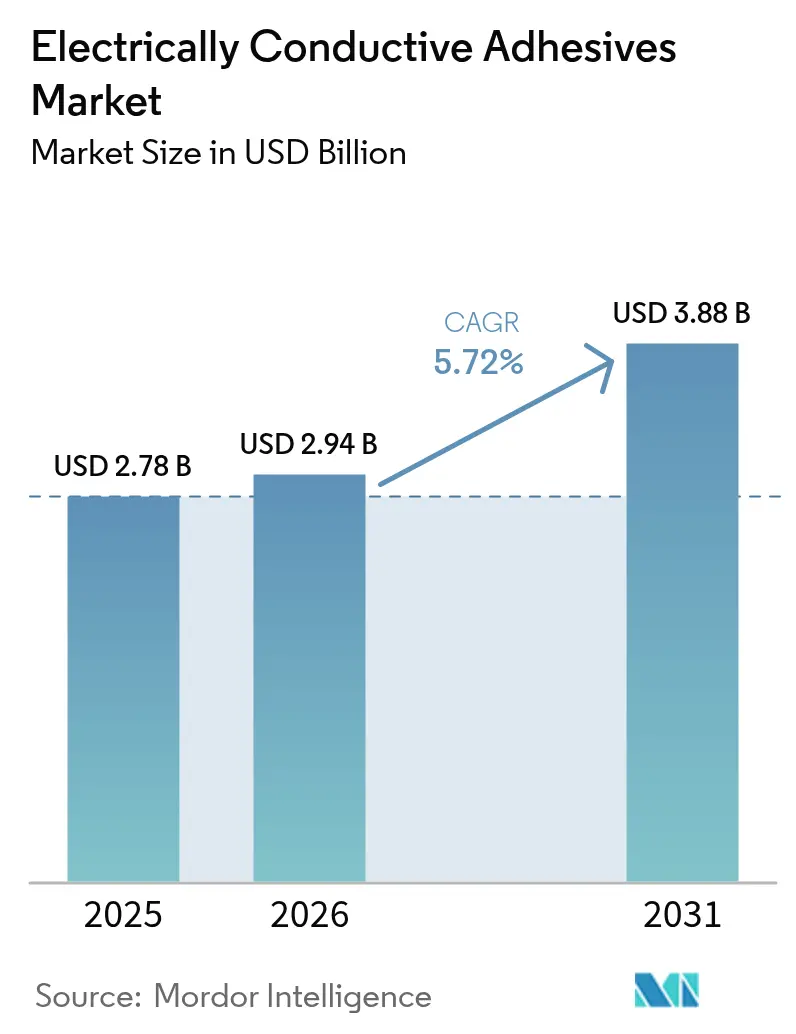

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 3.88 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

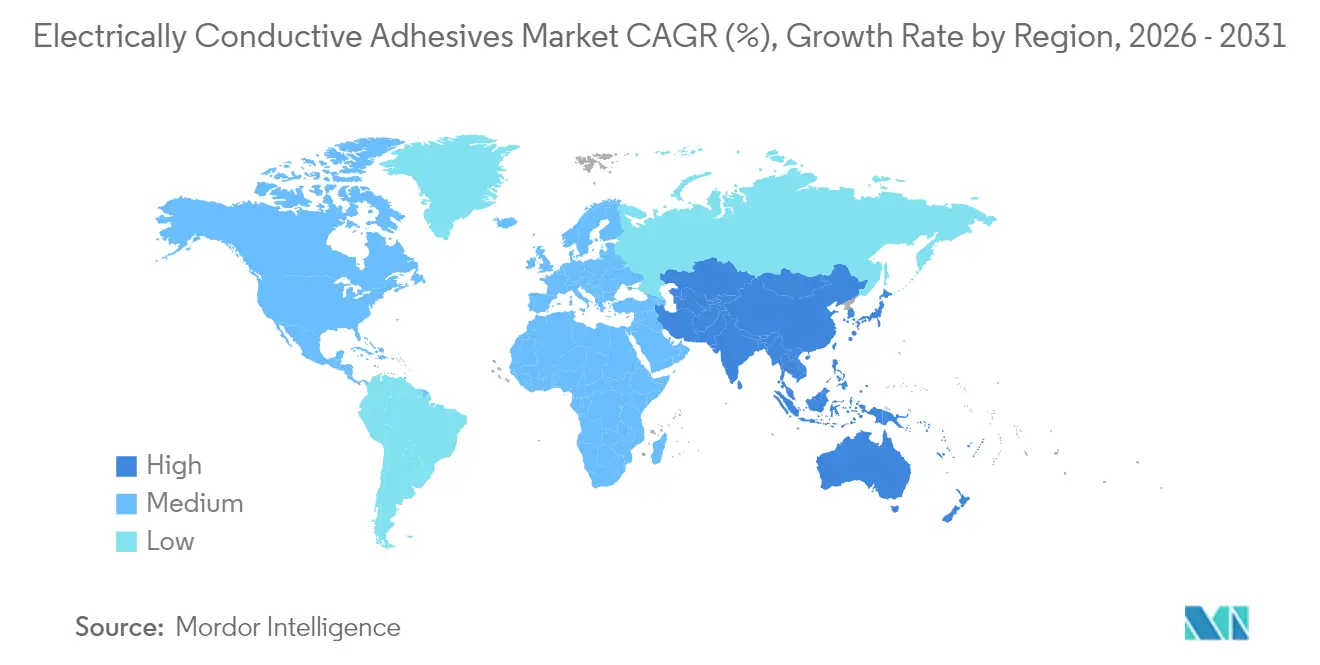

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrically Conductive Adhesives Market Analysis by Mordor Intelligence

The Electrically Conductive Adhesives Market size was valued at USD 2.78 billion in 2025 and estimated to grow from USD 2.94 billion in 2026 to reach USD 3.88 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). The sector’s growth hinges on the electronics industry’s transition to lead-free, low-temperature interconnection methods that safeguard ever-smaller components from thermal damage while complying with global environmental directives. Demand accelerates as power-dense semiconductor devices, high-frequency modules, and battery-centric electric vehicles outstrip the performance window of traditional tin-lead solders, opening a broad runway for epoxy, silicone, and hybrid chemistries that bond, conduct, and dissipate heat in a single step. Silver-filled isotropic grades dominate standard printed circuit assembly, yet anisotropic, carbon-reinforced and graphene-enhanced variants are scaling quickly where ultra-fine pitches, weight constraints and flex cycles dictate directional conductivity and mechanical damping. Regionally, the electrically conductive adhesives market gains most momentum in East Asia where policy-backed semiconductor foundries, photovoltaic gigafactories and accelerating EV adoption anchor the value chain. Parallel growth avenues emerge in aerospace, defense and bio-electronics, where extreme temperature swings, radiation exposure, and biocompatibility demands call for purpose-engineered formulations that pass stringent qualification standards.

Key Report Takeaways

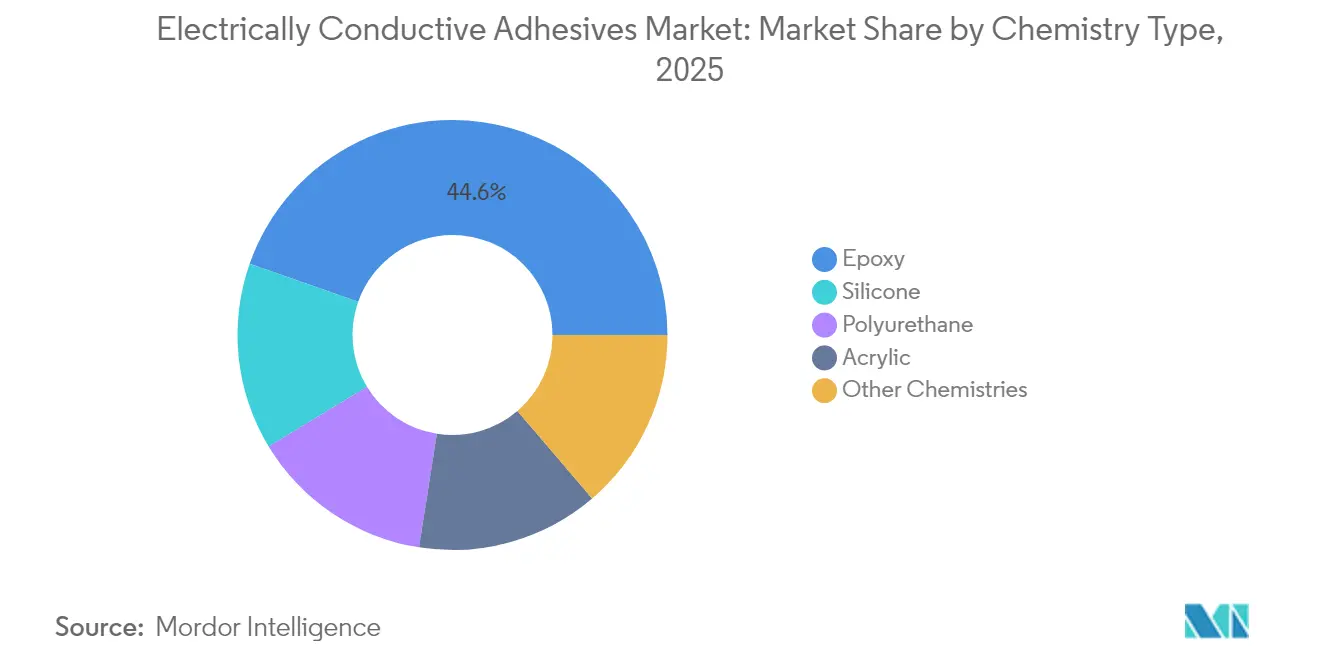

- By chemistry type, epoxy formulations led with 44.62% of the electrically conductive adhesives market share in 2025, while silicone-based systems record the fastest 6.42% CAGR to 2031.

- By type, isotropic grades commanded 66.72% share of the electrically conductive adhesives market size in 2025; anisotropic variants are projected to grow at a 6.78% CAGR through 2031.

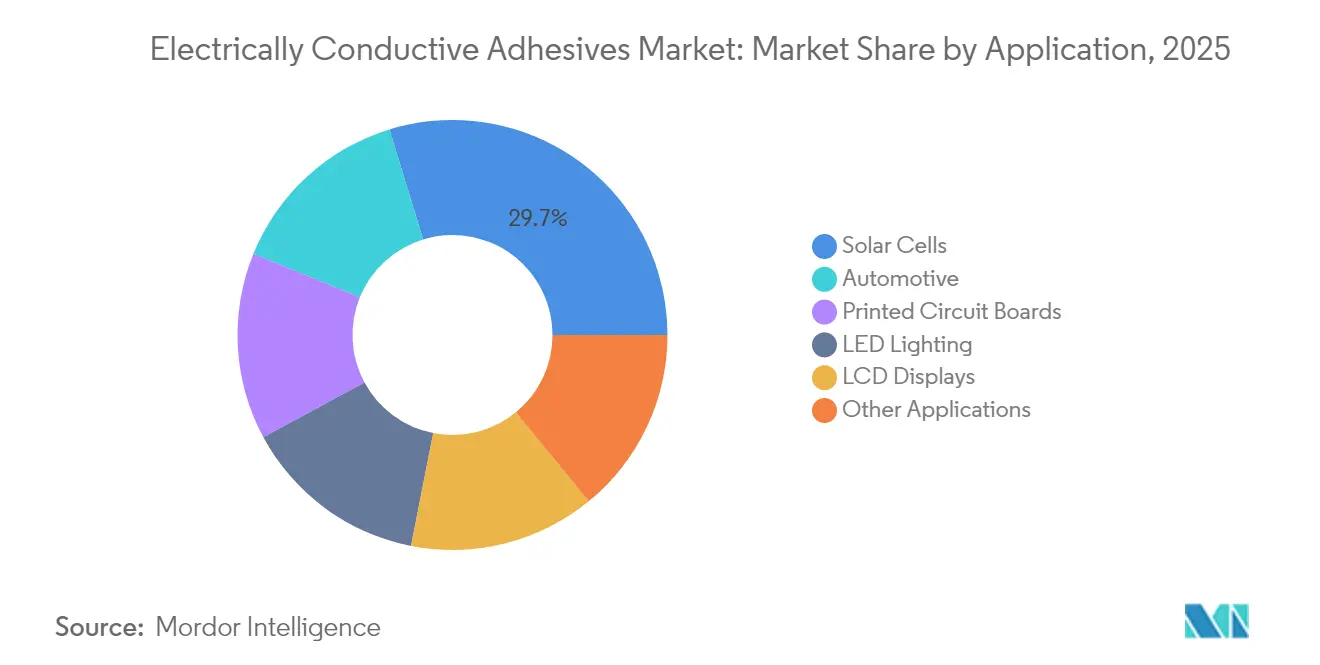

- By application, solar cells and photovoltaic modules captured 29.74% of the electrically conductive adhesives market size in 2025, whereas the “Other Applications” cluster—medical implants, aerospace electronics, and energy storage—expands at a 6.85% CAGR to 2031.

- By geography, Asia-Pacific accounted for 54.83% revenue share in 2025, and the region is forecast to surge at a 6.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrically Conductive Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing application in power electronics | +1.20% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing utilization in electric vehicles | +1.50% | Global, led by China, EU, and North America | Long term (≥ 4 years) |

| Incraesing usage in aerospace and defense applications | +0.80% | North America, Europe, with emerging demand in Asia-Pacific | Long term (≥ 4 years) |

| Growing demand from renewable energy systems | +1.10% | Global, with strong growth in Asia-Pacific and Europe | Medium term (2-4 years) |

| Bio-compatible conductive bio-adhesives for implants | +0.40% | North America and Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Application in Power Electronics

Next-generation power converters incorporating silicon-carbide and gallium-nitride devices run at junction temperatures above 200 °C, a regime that invalidates tin-lead and low-silver solders. Epoxy and silicone adhesives filled with high-purity silver, silver-coated copper, or hybrid graphene networks maintain conductivity under high current densities while buffering thermal shock, enabling miniaturized power modules that deliver higher switching frequencies with lower parasitics. The formulations also double as thermal interface materials, reducing junction-to-case resistance in traction inverters. Material scientists are dispersing carbon-nanotube strands in three-dimensional architectures to unlock parallel electrical and thermal pathways, pushing the electrically conductive adhesives market to the forefront of wide-bandgap power design.

Increasing Utilization in Electric Vehicles

Cell-to-pack battery strategies eliminate module housings, transferring load-bearing and thermal duties to the adhesive layer. Conductive epoxies with shear strengths above 20 MPa withstand vibration and crash pulses while equalizing current across 3,000-plus cylindrical or prismatic cells per pack. Hybrid systems that marry metallic fillers with ceramic spheres form a compliant lattice that absorbs differential expansion between aluminum busbars and copper tabs, extending service life over thousands of high-rate charge-discharge cycles. The 48-V architecture adopted for auxiliary electrification in light vehicles introduces dense power distribution boards where fine-pitch anisotropic joints prevent short circuits, adding fresh volume to the electrically conductive adhesives market.

Growing Demand from Renewable Energy Systems

Shingled and heterojunction photovoltaic cells rely exclusively on conductive adhesives to bridge ultra-thin busbars, boosting active area and raising module power by 5.1% compared with soldered ribbon designs[1]Journal of Nanoscience and Nanotechnology, “Performance of Shingled HJT Cells Using Conductive Adhesives,” nanoscienceworld.org . Low-temperature curing protects passivated contacts and perovskite layers, preserving 25-year field reliability. In wind energy, blade-integrated lightning diverter grids fabricated with carbon-nanotube-rich pastes route strike currents without galvanic corrosion, and the same circuitry doubles as a structural health monitoring network. These cross-functional roles intensify demand, enlarging the electrically conductive adhesives market beyond pure electronics assembly.

Bio-Compatible Conductive Bio-Adhesives for Implants

Flexible neural probes and cardiac telemetry patches require bonds that conduct micro-ampere signals yet remain cytocompatible. Hydrogel-based systems loaded with PEDOT: PSS and silver nanowires achieve sub-5 kΩ contact resistance while passing ISO 10993 cytotoxicity tests[2]Royal Society of Chemistry, “Biocompatible Conductive Hydrogel Adhesives,” rsc.org . Tissue-mimicking modulus prevents foreign-body inflammation, enabling decade-long implantation horizons. Although volumes are modest, profit margins exceed commodity consumer-electronics grades, adding a premium tier to the electrically conductive adhesives market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silver-filler price volatility | -0.90% | Global, with higher impact in cost-sensitive applications | Short term (≤ 2 years) |

| Reliability limits under high current & thermal cycling | -0.70% | Global, particularly affecting automotive and industrial applications | Medium term (2-4 years) |

| Longer curing times and process complexity | -0.50% | Global, with higher impact in high-volume manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Silver-Filler Price Volatility

Silver powders account for 60-80 wt% of typical isotropic adhesives, exposing formulators to bullion swings that can exceed 25% within a quarter. While copper, nickel, and carbon nanotubes promise cost relief, oxidation, diffusion, and percolation thresholds curb their ability to fully replace silver. Hybrid particle architectures that coat copper cores with 300-nm silver shells cut precious-metal content by 30-40% without compromising bulk conductivity, yet the supply chain remains vulnerable to geopolitical mining disruptions. Price pass-through mechanisms are standard in aerospace and medical contracts, but consumer electronics OEMs resist surcharges, trimming near-term expansion of the electrically conductive adhesives market.

Reliability Limits Under High Current & Thermal Cycling

Polymer matrices expand 30-80 ppm /°C against 16-18 ppm /°C for copper substrates, generating shear stress that triggers micro-voids at the filler-matrix interface. Elevated current densities create localized Joule heating; combined thermal-mechanical fatigue can raise joint resistance by 50% after 1,000 h at 85 °C/85% RH. Formulators introduce core-shell rubber particles and silane coupling agents to toughen interfaces, yet an inescapable trade-off remains: softer matrices relieve stress but reduce filler loading, increasing bulk resistivity. These reliability constraints temper electrified powertrain applications and influence the electrified conductive adhesives market adoption curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemistry Type: Epoxy Dominance Faces Silicone Challenge

Epoxy-based grades comprised 44.62% of the electrically conductive adhesives market in 2025 and remain a mainstay where high lap-shear strength and easy dispensing outweigh flexibility concerns. Formulators exploit bisphenol-A, bisphenol-F and novolac backbones to tailor viscosity, glass-transition temperature and modulus, covering everything from rigid board attach to die-attach in power modules. The electrically conductive adhesives market size for epoxy chemistries is projected to grow steadily even as competition intensifies. Their state-of-cure can be accelerated with latent imidazole catalysts, trimming oven time without compromising shelf life. For high-temperature silicon-carbide devices, imide-modified epoxies withstand 200 °C junction environments while keeping thermal cycling stability within 5% resistance drift over 2,000 cycles. On the environmental front, halogen-free formulations satisfy RoHS directives and end-of-life recycling mandates.

Silicone-based systems, recording a 6.42% CAGR to 2031, are closing the market-share gap by delivering elongation over 70% and sustained conductivity after 1,000 salt-spray hours—attributes prized in under-hood automotive controls and offshore wind converters. Polydimethylsiloxane networks absorb shock loads and seal against moisture ingress, addressing failure modes that epoxy cannot. Room-temperature-vulcanizing silicones with platinum catalysts reduce thermal stress on sensitive lens assemblies in LED lighting. Hybrid epoxy-silicone chemistries combine a rigid inner phase for bondline integrity with a compliant outer domain that relieves CTE mismatch. Such synergies reveal how the electrically conductive adhesives market evolves through compositional innovation rather than one-chemistry-wins-all convergence.

By Type: Isotropic Leadership Challenged by Anisotropic Innovation

Isotropic grades commanded 66.72% share of the electrically conductive adhesives market size in 2025, favored for their straightforward process windows and ability to replace reflow solder on through-hole and surface-mount joints. Standard systems maintain volume resistivity under 1 × 10⁻³ Ω·cm using silver flakes optimized for aspect ratio and oxide content. Dispense-and-cure simplicity captures design wins across smartphones, wearables, and consumer appliances where component counts exceed one thousand per board. Yet the omnidirectional conductive network poses a risk of shorts on sub-200 µm pad spacing unless dams or underfills are added, escalating process complexity and cost.

Anisotropic formulations address that pain point with particle designs that conduct solely in the Z-axis. Nickel-plated polymer spheres embedded at 10–15 vol% create vertical percolation paths when compressed, while remaining isolated laterally. In flexible OLED displays, pitch requirements of 40 µm render traditional solders unusable, propelling a 6.78% CAGR for anisotropic adhesives through 2031. High-frequency telecommunications modules employ anisotropic materials to bond flip-chip GaAs dies onto alumina carriers, maintaining 50 Ω impedance without ground-plane coupling. Dual-phase systems that embed anisotropic micro-spheres in an isotropic matrix deliver hybrid benefits, highlighting how the electrically conductive adhesives market reframes the binary type classification into a continuum.

By Application: Solar Dominance Amid Diversification

Solar photovoltaics absorbed 29.74% of market revenue in 2025, driven by giga-factory scale-up and design shifts to ribbon-free shingled architectures. Conductive adhesives eliminate hot-bar soldering steps, trimming cell breakage rates below 0.1% and raising throughput in heterojunction lines. The electrically conductive adhesives market share from solar will stay dominant but edge downward as other segments scale faster. Automotive battery packs trail close behind, capitalizing on conductive epoxies that double as structural fillers to bolster torsional rigidity in skateboard platforms. Printed circuit boards, LED dies and display driver interconnects form a mature demand core, stabilizing volume even as unit prices trend downward.

The “Other Applications” basket—medical implants, aerospace telemetry and energy storage sensors—registers the highest 6.85% CAGR. Biocompatible grades bring USD 2,000–3,000 per kg price points, cushioning margin compression elsewhere. In grid-scale battery racks, adhesives serve as current collectors and thermal spreaders, improving cell uniformity and state-of-health algorithms. Aerospace growth hinges on conductive films that attach radar-absorbing metamaterials to composite fuselages without galvanic mismatch. Each niche may represent a small sliver today, yet collectively they reinforce the electrically conductive adhesives market as a platform technology underpinning converging electronics-mechanical systems.

Geography Analysis

Asia-Pacific retained 54.83% of 2025 revenue and continues as both volume and value leader due to semiconductor powerhouse ecosystems in China, South Korea and Taiwan. Local policy mandates for new-energy vehicles and photovoltaic rollouts funnel sustained demand, translating to a 6.31% CAGR for the electrically conductive adhesives market across the region. National subsidy programs for domestic electric passenger cars anchor long-term offtake contracts with major adhesive suppliers, reducing currency-exchange risk and ensuring steady plant utilization. Start-up clusters in Shenzhen, Suzhou, and Bangalore complement entrenched multinationals by launching flexible, wearable, and printed-electronics products, widening the customer base for niche formulations.

North America demonstrates significant consumption, driven by defense avionics, space exploration initiatives, and the reshoring of power-semiconductor fabs. The region’s qualification standards—NASA outgassing, IPC-CC-830C, UL-94V0—elevate entry barriers, allowing suppliers of premium epoxy-silver pastes and thermally conductive films to command healthy gross margins. Recent capital expansions by DELO and Henkel in Texas and Ohio underscore confidence in long-term demand. Government incentives under the CHIPS and Science Act draw advanced-packaging projects that further enlarge the electrically conductive adhesives market footprint.

Europe maintains a stronghold in automotive, medical and renewable segments. Germany spearheads EV battery pack integration, France and the Nordic nations ramp offshore wind farms, and the Netherlands leads in flexible OLED R&D. These trends converge to sustain steady purchasing volumes despite macroeconomic headwinds. Stringent REACH and RoHS compliance pushes formulators toward halogen-free, lead-free, and solvent-reduced systems, awarding first-mover advantage to innovators capable of aligning performance with sustainability. With corporate average CO₂ targets tightening, OEMs view conductive adhesives as enablers for lighter wiring harnesses and higher-efficiency modules, reinforcing their long-run importance within the electrically conductive adhesives market.

Competitive Landscape

The electrically conductive adhesives market is moderately consolidated: the top five suppliers account for roughly 51% of global sales, leaving ample room for mid-tier specialists and regional champions. Scale economies pivot on silver paste compounding, filler surface treatment, and high-precision dispensing equipment, yet the broad spectrum of application-specific performance envelopes curbs the emergence of a single dominant supplier. Global players such as Henkel, 3M, H.B. Fuller, and Panacol leverage multi-chemistry portfolios, vertical integration into silver-flake production, and global technical-service laboratories to secure design wins in consumer and industrial electronics. Meanwhile, niche innovators concentrate on bio-compatible hydrogels, carbon-nanotube hybrids, or ultra-fast UV cure systems.

Strategic maneuvers revolve around three levers. First, R&D intensity: several leading firms reinvest 10-15% of sales into advanced material programs, racing to co-develop formulations that marry electrical, thermal, structural, and environmental functions in a single bond line. Second, regional proximity: facility expansions in Shanghai, Penang, and Guadalajara position suppliers adjacent to high-volume assembly clusters, reducing lead times and tailoring support to local process windows. Third, sustainability: recycled-silver ink lines introduced in 2025 demonstrate circular-economy credentials and mitigate raw-material volatility. Collectively, these tactics aim to strengthen stickiness with OEMs and stretch competitive moats, steering the long-term direction of the electrically conductive adhesives market.

Competitive pressure varies by vertical. In the price-elastic consumer-electronics arena, commoditized isotropic pastes face annual contract repricing, compelling suppliers to differentiate through dispensability and reworkability rather than pure resistivity numbers. Conversely, aerospace, medical, and defense programs certify a single approved source per platform, locking in multi-decade revenue streams once qualification hurdles are cleared. Custom chemistries that pass cytotoxicity or outgassing tests can earn margins above 35%. Start-ups exploring sintered nano-silver joints or graphene-networked elastomers may up-end incumbent market splits if they scale production and meet reliability proof points, keeping the evolution of the electrically conductive adhesives market fluid and innovation-driven.

Electrically Conductive Adhesives Industry Leaders

3M

Dow

H.B. Fuller Company

Henkel AG & Co. KGaA

Panacol-Elosol GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Henkel has launched a new Adhesive Technologies Application Engineering Center in Shanghai to strengthen localized R&D and industrial applications for the electronics and EV sectors. This development is expected to drive innovation and growth in the electrically conductive adhesives market by addressing evolving industry demands.

- February 2025: Henkel introduced the first silver inks made from recycled silver at LOPEC 2025, enabling the development of highly conductive printed circuits for smart surfaces. This innovation is expected to drive advancements in the electrically conductive adhesives market by promoting sustainable and efficient solutions.

Global Electrically Conductive Adhesives Market Report Scope

Electrically conductive adhesive products are primarily used for electronics applications where components need to be held in place, and electrical currents can be passed between them. The electrically conductive adhesives market is segmented by chemistry type, type, and application. The chemistry type segmentation includes epoxy, silicone, polyurethane, acrylic, and other chemical types, the by type segmentation includes isotropic and anisotropic, and by application, the market segmentation includes solar cells, automotive electronics, LED lighting, printed circuit board, LCD displays, and other applications. The report also covers the size and forecasts for the electrically conductive adhesives market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Epoxy |

| Silicone |

| Polyurethane |

| Acrylic |

| Other Chemistries |

| Isotropic |

| Anisotropic |

| Solar Cells |

| Automotive |

| LED Lighting |

| Printed Circuit Boards |

| LCD Displays |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Chemistry Type | Epoxy | |

| Silicone | ||

| Polyurethane | ||

| Acrylic | ||

| Other Chemistries | ||

| By Type | Isotropic | |

| Anisotropic | ||

| By Application | Solar Cells | |

| Automotive | ||

| LED Lighting | ||

| Printed Circuit Boards | ||

| LCD Displays | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current electrically conductive adhesives market size and growth outlook?

The electrically conductive adhesives market size is USD 2.94 billion in 2026 and is projected to reach USD 3.88 billion by 2031, reflecting a 5.72% CAGR.

Which region contributes the most to electrically conductive adhesive demand?

Asia-Pacific holds 54.83% of global revenue in 2025 and is expanding at a 6.31% CAGR, led by semiconductor manufacturing and aggressive electric-vehicle policies.

Which chemistry type leads the market today?

Epoxy-based formulations account for 44.62% of the 2025 market thanks to their strength and versatility, while silicone grades are the fastest risers at a 6.42% CAGR.

What application segment generates the highest revenue?

Solar photovoltaic modules command 29.74% of 2025 sales because shingled and heterojunction cells rely on conductive adhesives for low-temperature interconnects.

Why are anisotropic conductive adhesives gaining traction?

Anisotropic grades grow at a 6.78% CAGR because they provide Z-axis conductivity that prevents shorts in fine-pitch displays, flexible circuits, and high-density battery boards.

Page last updated on: