Medical Device Adhesive Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

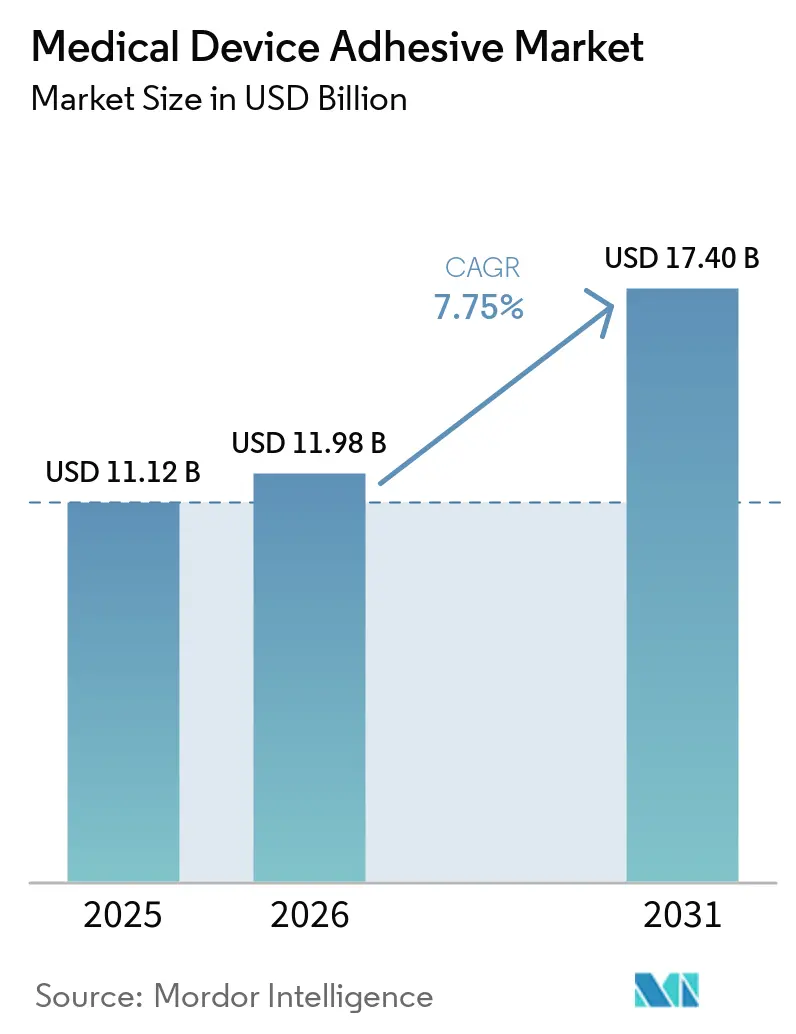

| Market Size (2026) | USD 11.98 Billion |

| Market Size (2031) | USD 17.40 Billion |

| Growth Rate (2026 - 2031) | 7.75% CAGR |

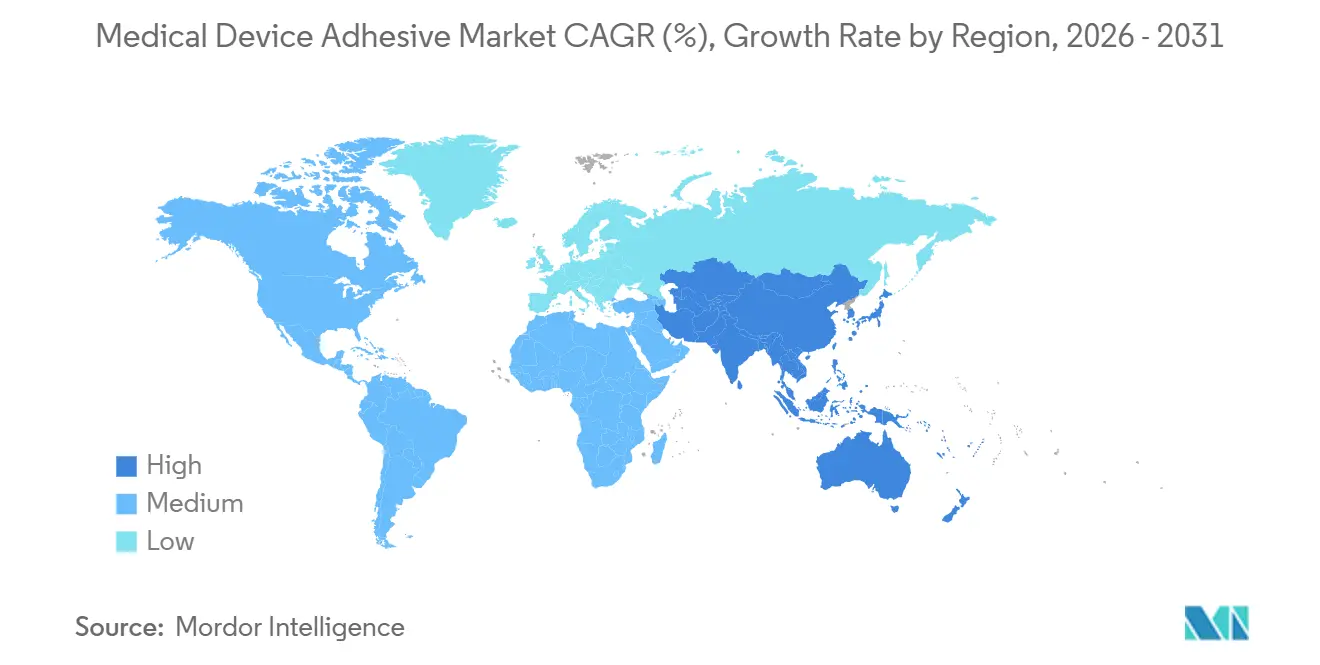

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Adhesive Market Analysis by Mordor Intelligence

The Medical Device Adhesive Market size is expected to grow from USD 11.12 billion in 2025 to USD 11.98 billion in 2026 and is forecast to reach USD 17.40 billion by 2031 at 7.75% CAGR over 2026-2031. Regulatory mandates for ISO 10993 biocompatibility testing, the acceleration of home-based care, and AI-guided optical-curing systems that shorten production cycles by 20-30% have combined to lift demand. Silicone chemistries that retain peel strength after 25-kGy gamma sterilization are displacing acrylics despite their higher raw-material cost, while water-based formulations continue to benefit from European VOC (volatile organic compounds) limits of 50 mg/m³. Pressure-sensitive films dominate wearable glucose monitors, yet hydrocolloid patches are gaining traction as chronic-wound care shifts to the home. Regionally, North America remains the largest buyer thanks to concentrated Class III device manufacturing and the FDA (Food and Drug Administration)’s streamlined 510(k) route, whereas Asia-Pacific is the fastest-growing arena as China and Japan harmonize with ISO 10993.

Key Report Takeaways

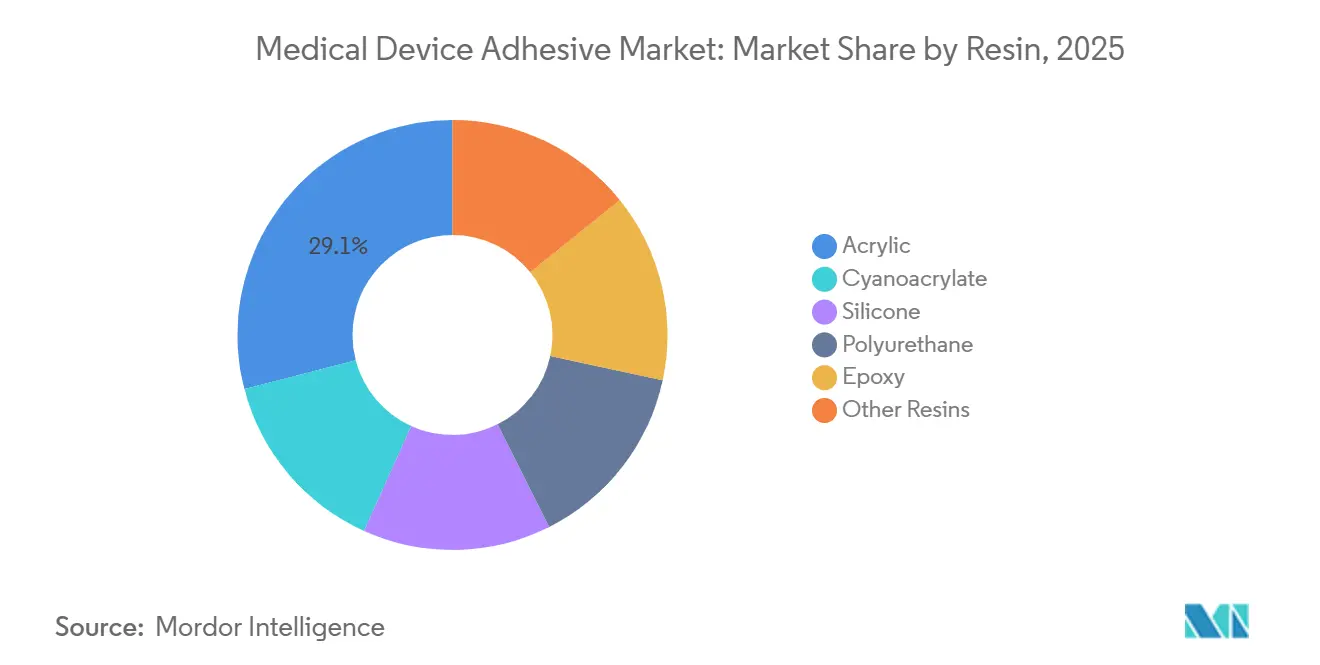

- By resin, acrylic led with 29.05% of the medical device adhesive market share in 2025, while silicones are projected to expand at a 8.11% CAGR during the forecast period (2026-2031).

- By technology, water-based systems held 34.82% of the medical device adhesive market size in 2025; UV/radiation-curable systems record the highest forecast CAGR at 8.35% during the forecast period (2026-2031).

- By adhesive form, pressure-sensitive films and tapes accounted for 37.02% of the medical device adhesive market size in 2025; gels and hydrocolloid patches are expected to advance at a 8.27% CAGR during the forecast period (2026-2031).

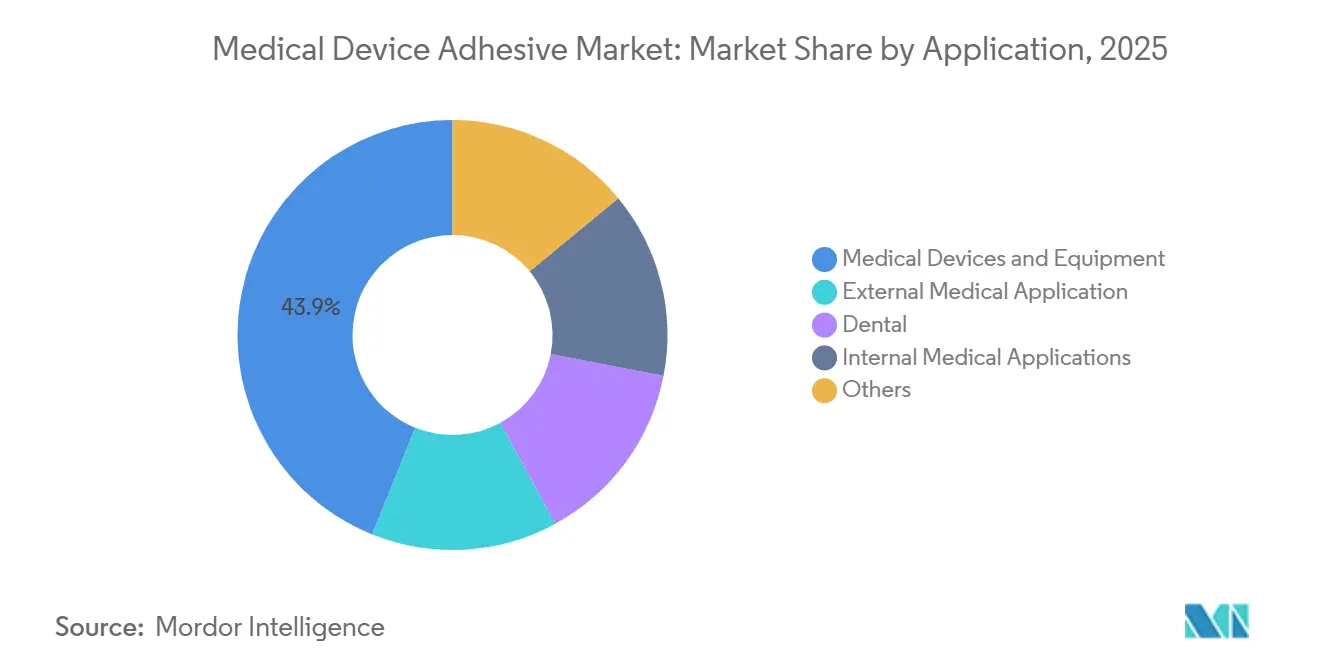

- By application, medical devices and equipment captured 43.92% of the medical device adhesive market share in 2025, and the share of the internal medical applications is expected to grow at a 8.54% CAGR during the forecast period (2026-2031).

- By geography, North America remained the largest regional contributor with 38.11% revenue share in 2025; Asia-Pacific is anticipated to post the fastest CAGR of 8.46% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device Adhesive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in remote-monitoring and wearable therapeutic devices | +1.4% | Global, with North America and Asia-Pacific leading adoption | Medium term (2-4 years) |

| Expansion of single-use and minimally-invasive catheter platforms | +1.2% | North America, Europe, and Japan core markets | Medium term (2-4 years) |

| Growth in home-infusion pumps requiring long-wear PSAs | +1.0% | North America and Western Europe | Short term (≤ 2 years) |

| Wider adoption of hydrogel and bio-resorbable adhesive chemistries | +0.9% | Global, with early traction in EU and US | Long term (≥ 4 years) |

| Emergence of printed self-powered biosensor patches needing stretchable conductive adhesives | +0.8% | Asia-Pacific manufacturing hubs, North America R&D centers | Long term (≥ 4 years) |

| AI-driven inline optical-curing QA boosting assembly line throughput | +0.7% | Global, concentrated in high-volume manufacturing sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Remote-Monitoring and Wearable Therapeutic Devices

Wearable devices now demand skin adhesion for 7-14 days without sensitization. Medtronic showed silicone-acrylate hybrids cut erythema scores 35% versus standard acrylics in 2025 trials, thanks to silicone surface energies near 20 dynes/cm that limit protein adsorption[1]Medtronic, “Extended-Wear Infusion Set Clinical Results,” medtronic.com. The FDA cleared 14 new adhesive-backed insulin-delivery systems during 2025, each passing ISO 10993-10 and -23 protocols. Co-development of tapes at the design stage has replaced retrofit approaches, optimizing peel strengths of 400-600 g/inch and moisture-vapor transmission above 800 g/m²/24 h.

Expansion of Single-Use and Minimally-Invasive Catheter Platforms

EU MDR 2017/745 tightened re-use rules in 2024, prompting rapid growth of disposable catheters. Boston Scientific reported 28% sales growth in single-use ureteroscopes aided by UV-curable balloon bonds with 5-second cure times[2]Boston Scientific, “Investor Presentation 2025,” bostonscientific.com. Stryker applies low-viscosity cyanoacrylates that wick into less than100-µm gaps on neurovascular devices, meeting ISO 10993-18 extractables thresholds under 0.1 ppm. The quick cure slashes work-in-process inventories by 40%.

Growth in Home-Infusion Pumps Requiring Long-Wear PSAs

CMS broadened reimbursement in January 2025, lifting ambulatory pump placements 22% in H1. Baxter’s Novum IQ uses a hydrocolloid-bordered patch absorbing 3 g exudate per 10 cm², preventing tack loss of up to 40% over 4 days. ISO 15621 adaptation for wound-contact absorbency is now an informal payer prerequisite.

Wider Adoption of Hydrogel and Bio-Resorbable Adhesive Chemistries

Catechol-functionalized PEG adhesives lost 80% mass in 14 days yet delivered 150 kPa lap-shear on porcine skin, according to an Advanced Healthcare Materials 2025 study. Johnson & Johnson disclosed a thermosensitive hydrogel that gels at 32°C, enabling cold-chain storage and body-heat activation. FDA draft guidance (March 2025) recommends full ISO 10993 testing plus chronic-toxicity data for bio-resorbables exceeding 30-day wear.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex ISO-10993 biocompatibility and extractables testing burden | -0.8% | Global, with heightened scrutiny in EU and US | Medium term (2-4 years) |

| Cost volatility of medical-grade silicone and specialty acrylates | -1.1% | Global, acute in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Sterilization-induced crosslink-density drift reducing shelf-life of advanced PSAs | -0.6% | North America and Europe, where gamma sterilization dominates | Medium term (2-4 years) |

| Supply risk of pharma-grade tackifier resins due to SE-US pine-blight | -0.4% | North America, with ripple effects in global supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex ISO-10993 Biocompatibility and Extractables Testing Burden

ISO 10993-1:2018 now mandates chemical characterization before biological tests, adding 18-24 months and USD 200,000-500,000 per new formulation. Contract-lab backlogs stretched to 16 weeks in 2025, delaying launches. REACH Annex XVII phthalate bans, effective June 2024, forced re-qualification of legacy tapes throughout Europe.

Cost Volatility of Medical-Grade Silicone and Specialty Acrylates

Silicone raw-material prices climbed 18-22% between Q1 2024 and Q2 2025 after supply disruptions at key Asian siloxane plants, squeezing margins by roughly 280 basis points at Wacker Chemie. Parallel 15-20% swings in 2-ethylhexyl acrylate spot pricing destabilized fixed-price OEM contracts, pushing smaller buyers toward water-based emulsions that carry 25-30% lower feedstock costs but give up 10-15% peel strength on silicone-coated liners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Silicone Chemistries Lead Sterilization-Tolerant Growth

Acrylics held 29.05% of the medical device adhesive market share in 2025 because of their USD 4.50-6.00/kg cost and 200-m/min coating speeds. Silicone resins are on track for an 8.11% CAGR between 2026 and 2031 as device makers favor adhesives that maintain greater than or equal to 400 g/in peel after 25-kGy gamma cycles. Yet ISO 10993-5 cytotoxicity scores below 1 for silicones are steering long-wear CGM and insulin-pump platforms their way. Niche cyanoacrylates, as seen in Ethicon’s Dermabond Prineo 2.0, cut closure time 30% in a 450-patient trial.

Polyurethane chemistries underpin structural bonds in implantable pulse generators that require greater than or equal to 2,500 psi lap-shear, while epoxies dominate catheter-tip assembly. FDA clearance of six cyanoacrylate surgical sealants during 2025 confirms regulatory comfort when formaldehyde release stays under 2 ppm.

By Technology: UV-Curing Systems Outpace Solvent and Water Alternatives

Water-based chemistries retained 34.82% share of the medical device adhesive market size in 2025 under tight EU VOC caps, yet their 15-30 minute dry times limit throughput. Dymax’s 405-nm LED line cures to 75 Shore D in 3s, trimming energy use 85% versus mercury lamps. UV/radiation-curable adhesives will post an 8.35% CAGR through 2031, propelled by zero-VOC processing and sub-5-second cures that align with injection-molding tact times.

Solvent-based systems endure where gap filling or long open times are needed, and hot-melts are growing in surgical-drape attachment with 120-140°C melt points. Hybrid dual-cure epoxies that photopolymerize surfaces and dark-cure hidden joints over 24 h eliminate voids in complex geometries.

By Adhesive Form: Hydrocolloid Patches Gain in Home-Based Wound Care

Pressure-sensitive films and tapes led with 37.02% of 2025 revenue, yet gels and hydrocolloid patches are expected to grow at an 8.27% CAGR during the forecast period (2026-2031) as diabetic ulcer care shifts homeward. Smith & Nephew’s Allevyn Life absorbed 40% more exudate and cut dressing changes 18% year-on-year. Hydrocolloids swell 150-200%, distributing shear and keeping bacterial barriers intact for up to 7 days.

Structural liquids, epoxies, urethanes, cyanoacrylates, anchor catheter components with tensile strengths more than 3,000 psi at service temperatures to 150°C. Sprayable cyanoacrylates with 10s tack-free times are entering surgical skin prep, while polyurethane foams expand 300-400% for negative-pressure therapy cavities.

By Application: Internal Uses Grow Fastest on Minimally Invasive Surgery

Medical devices and equipment represented 43.92% of 2025 sales, yet internal medical uses, surgical sealants, balloon bonds, and implantable assemblies will grow at an 8.54% CAGR through 2031. Baxter’s Tisseel reformulation shortened liver-resection hemostasis by 35%, saving 12 OR minutes per case. Regulatory pathways for fibrin and cyanoacrylate sealants now demand viral inactivation log-reductions greater than or equal to 6.

External applications, wound dressings, transdermals, wearables, lean on silicone-acrylate hybrids that strip at less than 100 g/inch yet survive 5-day wear, while universal dental systems remove separate etch and prime steps, cutting restoration chair time by 5 minutes.

Geography Analysis

North America held 38.11% of global revenue in 2025, sustained by FDA 510(k) clearances that can close in 120 days and a critical mass of CGM and insulin-pump production. Abbott, Dexcom, and Medtronic shipped 8.2 million sensors in 2025, all using silicone-acrylate hybrids qualified to ISO 10993-10 for 14-day wear. Solventum’s spin-off unlocked USD 180 million for new ISO-10993 labs, while Henkel added 8,000 tons of UV-curable capacity in Mexico to meet near-shoring demand.

Asia-Pacific is the fastest-growing region at an 8.46% CAGR from 2026 to 2031. China’s NMPA aligned with ISO 10993 and saw a 12% device-market jump in 2025; Mindray and United Imaging integrated structural adhesives in new imaging gear. Japan okayed 18 adhesive-containing devices during 2025, and Dow opened a 3,500-ton silicone plant in Pune under India’s PLI scheme. South Korea’s MFDS approval of Samsung’s Galaxy Watch 6 Medical Edition showcased conductive polyurethane adhesives delivering 0.8 Ω/square sheet resistance during 20% wrist flex.

In Europe, MDR enforcement tightened evidence demands. Germany’s Lohmann converted 68% of its catalog to bio-based acrylates, lowering CO₂ footprints 22%. The U.K. introduced a fast-track path for FDA-cleared adhesives, France prioritized diabetic wound-care reimbursement, and Urgo’s hydrocolloid–silver dressing cut healing times 25%. Russia’s import-substitution policy spurred domestic cyanoacrylate launches at a 30-35% price edge.

Competitive Landscape

The Medical Device Adhesive market is moderately fragmented. AI-driven QC is a new differentiator. Coherix’s Predator3D trimmed bead-placement defects 50-60%, lifting first-pass yields to 98% and saving about USD 1.2 million per line annually for Henkel clients. Start-ups are also encroaching. UC-San Diego spin-outs commercialized laser-induced graphene adhesives that cost 40% less than silver-filled benchmarks while hitting 5-10 Ω/square, appealing to low-current heart monitors.

Medical Device Adhesive Industry Leaders

3M

Arkema

Henkel AG & Co. KGaA

DuPont

Avery Dennison Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Henkel Adhesive Technologies launched a new range of flexible and rigid LED-curable adhesives under its Loctite brand, including Loctite AA 3951/AA 3953 and Loctite AA 3961/AA 3963, developed to meet the stringent demands of modern medical device assembly.

- July 2025: Researchers at Texas A&M University's Department of Mechanical Engineering created an innovative adhesive, potentially revolutionizing comfort in wearable healthcare devices, including glucose and heart monitors, by providing a superior alternative to traditional hydrophobic, pressure-sensitive adhesives.

Global Medical Device Adhesive Market Report Scope

Medical device adhesives are specialized, biocompatible materials (ISO 10993 compliant) used to bond, seal, and assemble devices like catheters, syringes, and wearables.

The medical device adhesive market is segmented by resin, technology, adhesive form, application, and geography. By resin, the market is segmented into acrylic, cyanoacrylate, silicone, polyurethane, epoxy, and other resins. By technology, the market is segmented into water-based, solvent-based, hot-melt, and UV/radiation-curable. By adhesive form, the market is segmented into pressure-sensitive films and tapes, structural/semi-structural liquids, gels and hydrocolloid patches, and sprayable/foam adhesives. By application, the market is segmented into medical devices and equipment, external medical applications, dental, internal medical applications, and others. The report also covers the market size and forecasts for medical device adhesives in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Acrylic |

| Cyanoacrylate |

| Silicone |

| Polyurethane |

| Epoxy |

| Other Resins |

| Water-based |

| Solvent-based |

| Hot-melt |

| UV/Radiation-curable |

| Pressure-Sensitive Films and Tapes |

| Structural/Semi-Structural Liquids |

| Gels and Hydrocolloid Patches |

| Sprayable/Foam Adhesives |

| Medical Devices and Equipment |

| External Medical Application |

| Dental |

| Internal Medical Applications |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin | Acrylic | |

| Cyanoacrylate | ||

| Silicone | ||

| Polyurethane | ||

| Epoxy | ||

| Other Resins | ||

| By Technology | Water-based | |

| Solvent-based | ||

| Hot-melt | ||

| UV/Radiation-curable | ||

| By Adhesive Form | Pressure-Sensitive Films and Tapes | |

| Structural/Semi-Structural Liquids | ||

| Gels and Hydrocolloid Patches | ||

| Sprayable/Foam Adhesives | ||

| By Application | Medical Devices and Equipment | |

| External Medical Application | ||

| Dental | ||

| Internal Medical Applications | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will global sales of medical device adhesives be by 2031?

The Medical Device Adhesive Market size is expected to grow from USD 11.12 billion in 2025 to USD 11.98 billion in 2026 and is forecast to reach USD 17.40 billion by 2031 at 7.75% CAGR over 2026-2031.

Which resin type is growing fastest?

Silicone chemistries are projected to register the highest 8.11% CAGR during the forecast period (2026-2031) because they retain peel strength after gamma sterilization and meet stricter biocompatibility standards.

Why are UV-curable formulations gaining share?

They cure in under 5 seconds, cut energy use up to 85%, and avoid VOC emissions, helping manufacturers boost line speeds without adding solvent-recovery systems.

Which region shows the strongest future growth?

Asia-Pacific is expected to post an 8.46% CAGR through 2031 as China, Japan, and India harmonize standards and expand production capacity.

Page last updated on: