Market Overview

| Study Period | 2021 - 2031 |

|---|---|

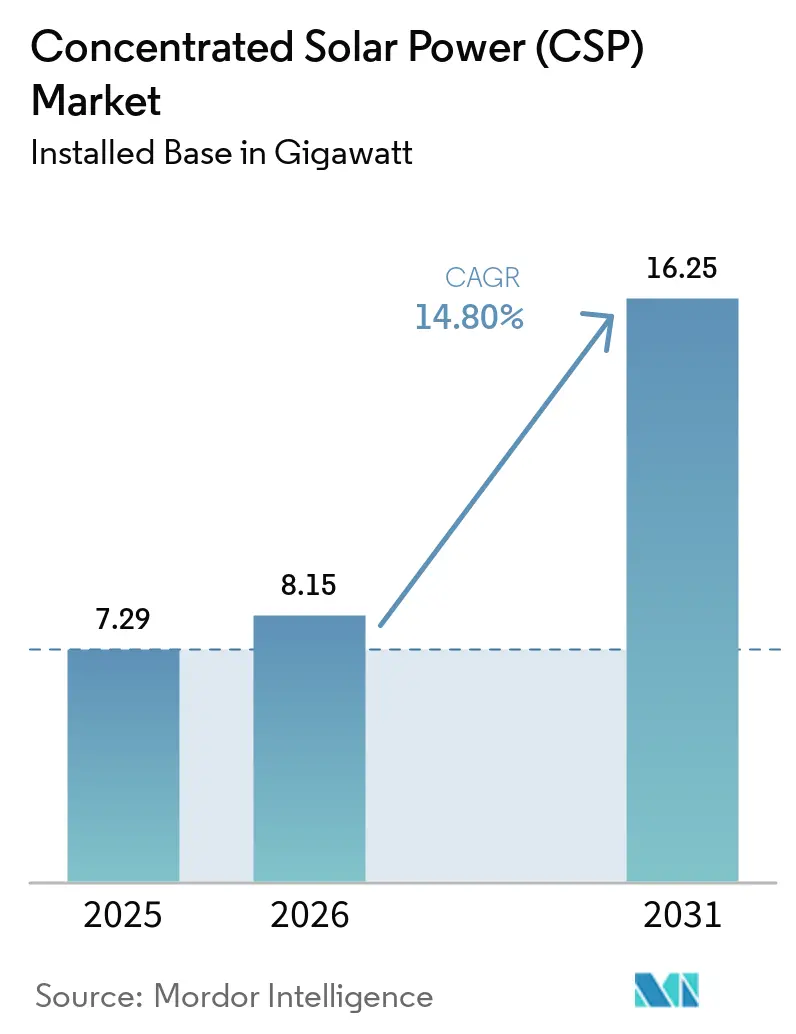

| Market Volume (2026) | 8.15 gigawatt |

| Market Volume (2031) | 16.25 gigawatt |

| Growth Rate (2026 - 2031) | 14.80% CAGR |

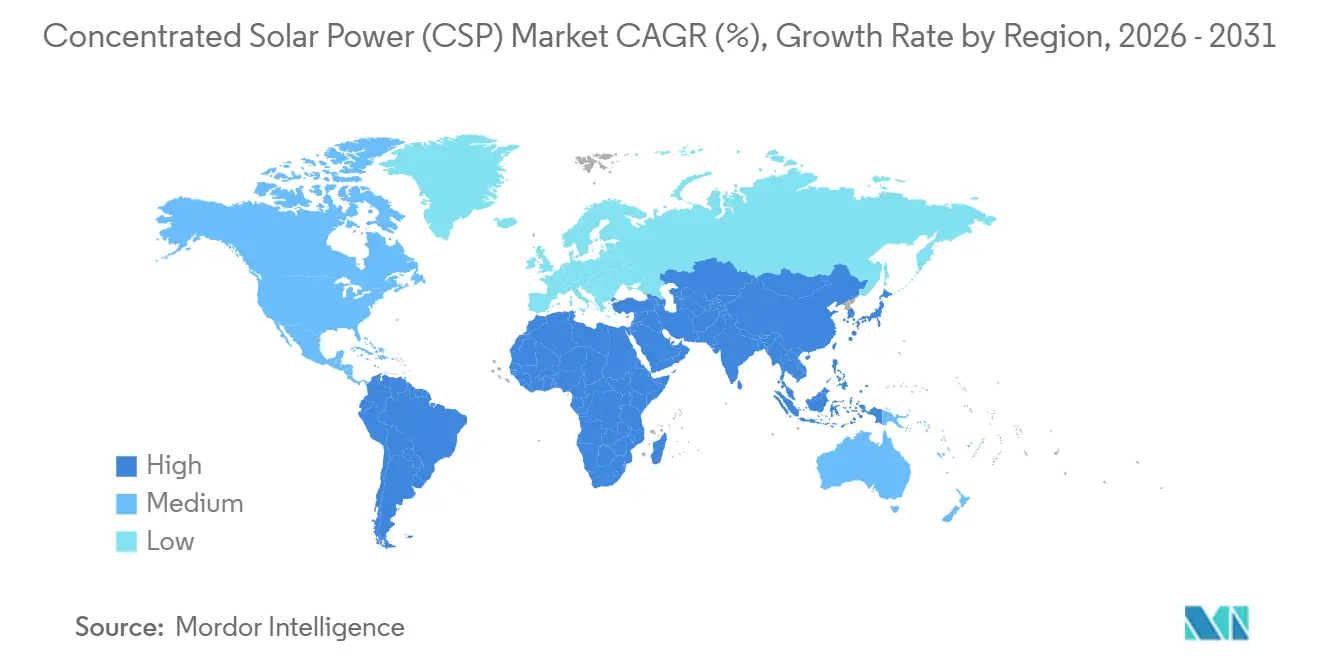

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Concentrated Solar Power (CSP) Market Analysis by Mordor Intelligence

The Concentrated Solar Power Market size in terms of installed base is projected to expand from 7.29 gigawatt in 2025 and 8.15 gigawatt in 2026 to 16.25 gigawatt by 2031, registering a CAGR of 14.80% between 2026 to 2031.

Grid planners are turning to CSP because photovoltaic arrays paired with lithium-ion batteries become uneconomic once discharge horizons exceed eight hours, whereas molten-salt storage can run 15 hours or more at lower marginal cost. Policy momentum is rising in China, Saudi Arabia, and the United Arab Emirates as governments write auction rules that reward long-duration dispatch and capacity credits above 80% of nameplate rating.[1]China Energy Portal, “China 14th Five-Year Renewable Plan,” chinaenergyportal.org Thermal efficiency gains in power-tower designs, steady cost compression of heliostats, and sovereign-backed financing in the Middle East and Africa underpin an accelerated build-out in the CSP market, while industrial process-heat demand and desalination integration open new revenue streams that photovoltaic hybrids struggle to match.[2]Dubai Electricity and Water Authority, “Mohammed bin Rashid Al Maktoum Solar Park Details,” dewa.gov.ae Construction timelines of three to five years and installed costs near USD 3,677 per kW continue to limit the developer pool, yet concessional debt from multilateral banks is widening geographic reach into North and Sub-Saharan Africa.

Key Report Takeaways

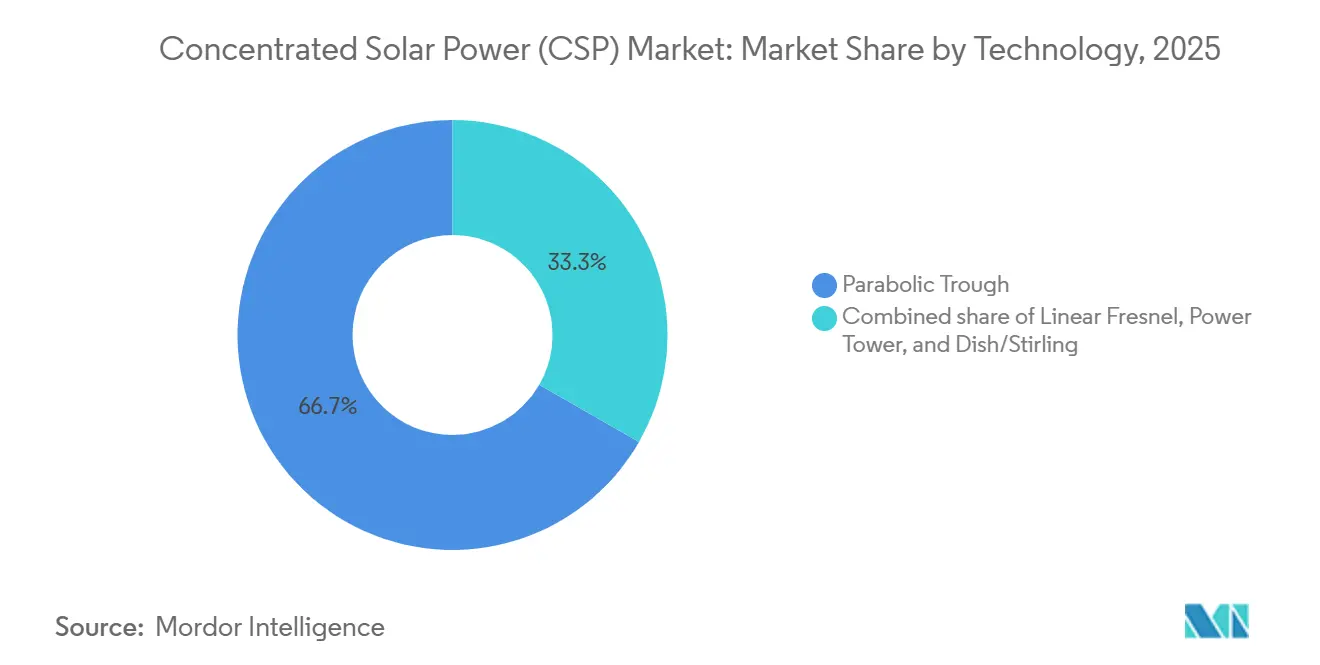

- By technology, parabolic trough systems retained 66.7% capacity share in 2025, while power towers are advancing at a 16.8% CAGR through 2031, the fastest across all technologies in the concentrated solar power market.

- By heat-transfer fluid, molten salt captured 58.5% of 2025 demand and is expanding at a 15.9% CAGR to 2031, outpacing synthetic oils.

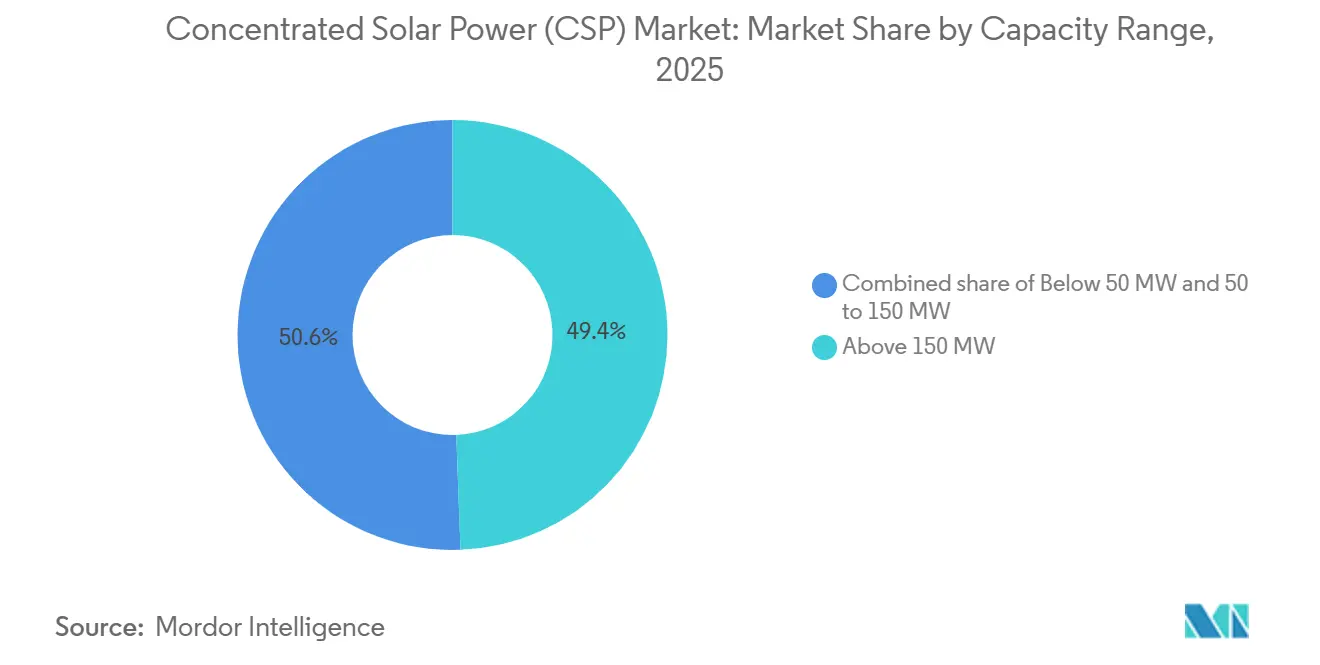

- By capacity, plants sized above 150 MW held 49.4% of 2025 installations, yet the 50 MW to 150 MW class is growing at 19.3% CAGR amid easier project finance in the concentrated solar power market.

- By geography, Europe accounted for 32.1% of cumulative capacity in 2025, but the Middle East and Africa corridor is the fastest region, moving at a 22.5% CAGR through 2031.

- ACWA Power, SENER, Abengoa successor entities, and Shouhang High-Tech control roughly 70% of active pipelines, underscoring moderate concentrated solar power market concentration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Concentrated Solar Power (CSP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining LCOE for CSP With Storage | +3.2% | Global, early gains in China, UAE, Saudi Arabia | Medium term (2-4 years) |

| Grid Need for Long-Duration Dispatchable Renewables | +2.8% | APAC, Middle East & Africa, Southern Europe | Long term (≥ 4 years) |

| MENA & China Policy Auctions Accelerating Build-Out | +2.5% | Middle East & Africa, China | Short term (≤ 2 years) |

| Industrial Process-Heat & Green-Hydrogen Coupling | +1.9% | Middle East, China, Spain, Germany | Medium term (2-4 years) |

| Hybrid CSP-Desalination in Water-Stressed Regions | +1.4% | UAE, Saudi Arabia, Egypt, North Africa | Medium term (2-4 years) |

| 24/7 Clean Heat Demand From Hyperscale Datacenters | +0.8% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining LCOE for CSP With Storage

Levelized-cost curves for CSP combined with molten-salt storage fell 70% between 2010 and 2024, hitting USD 0.092 per kWh worldwide, while Chinese projects landed at USD 0.069 per kWh in late 2024.[3]International Renewable Energy Agency, “Renewable Power Generation Costs 2024,” irena.org Standardized heliostat designs, local manufacturing in China and Gulf states, and auction-driven competition underpin that drop, creating a stronger economic foundation for the csp market. Dubai’s 950 MW Mohammed bin Rashid Al Maktoum Phase 4 locked a record USD 0.073 per kWh tariff in 2023, proving competitiveness against gas turbines in carbon-constrained markets.[4]Dubai Electricity and Water Authority, “Mohammed bin Rashid Al Maktoum Solar Park Details,” dewa.gov.ae Fifteen-hour storage lets utilities defer large battery procurements. Capital markets have started to factor the lower revenue volatility into weighted-average cost of capital models, reducing required equity returns by up to 150 basis points in recent financings. Developers are now underwriting projects assuming a 5% to 7% annual capex decline through 2030, which accelerates pipeline growth in subsidy-light jurisdictions.

Grid Need for Long-Duration Dispatchable Renewables

Global transmission operators report deepening net-load ramps as solar penetration rises. California’s spring 2024 “duck curve” saw a 13 GW three-hour ramp, straining reserves. Lithium-ion batteries excel at four-hour discharge but become uneconomic beyond eight hours, leaving a gap that molten-salt CSP supplies at a lower lifetime cost. CSP turbines can start in under ten minutes, offering inertia and frequency response without cycle-life degradation. Capacity-credit frameworks now assign CSP up to 85% of nameplate rating in Spain, South Africa, and Chile, compared with 30%-50% for photovoltaic-battery hybrids. As grids target 24/7 renewable portfolios, planners are increasingly embedding minimum long-duration storage quotas in resource-adequacy procurements, directly boosting the Concentrated Solar Power market.

MENA & China Policy Auctions Accelerating Build-Out

China’s 14th Five-Year Plan mandates 15 GW of operating CSP by 2030, up from 838 MW in 2024, and provincial auctions in Gansu, Qinghai, and Inner Mongolia attach feed-in premiums tied to storage hours. Saudi Arabia, the UAE, and Egypt launched multi-gigawatt hybrid solar tenders capped below USD 0.08 per kWh, compressing lead times by bundling land rights, grid access, and sovereign guarantees. Shouhang High-Tech’s 100 MW Dunhuang tower demonstrated bankability, catalyzing a 3.3 GW construction wave. Combined, these frameworks pull projects through permitting in under 24 months, sharply faster than legacy European processes, positioning policy auctions as a main catalyst for the Concentrated Solar Power market.

Industrial Process-Heat & Green-Hydrogen Coupling

Industrial heat between 150 °C and 565 °C represents close to 20% of global final energy demand, and CSP can supply that range without combustion emissions, creating new opportunities for the CSP market beyond electricity generation. Heineken España’s 30 MW parabolic trough plant cuts gas imports by 18,000 t annually. Saudi Arabia’s NEOM project couples a 300 MW CSP plant to a 50,000 t-per-year hydrogen facility, using tower heat to raise electrolyzer efficiency. Early pilots in Germany and Australia test thermochemical water-splitting at above 800 °C, which next-generation power towers target. These industrial integrations diversify revenue, shorten offtake tenures, and lower merchant-price exposure, lifting projected internal rates of return by 120 basis points on average.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PV + Battery Cost Declines Undercutting CSP Bids | −2.9% | North America, Europe, Australia | Short term (≤ 2 years) |

| High Upfront CAPEX & Limited Finance Pools | −2.1% | Emerging markets outside China and GCC | Medium term (2-4 years) |

| Hitec-Salt Supply-Chain Price Volatility | −1.2% | Global, acute where no long-term contracts exist | Short term (≤ 2 years) |

| Cooling-Water Scarcity at Desert Sites | −0.9% | Middle East, North Africa, U.S. Southwest, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PV + Battery Cost Declines Undercutting CSP Bids

Photovoltaic modules fell another 12% year-on-year in 2024, while lithium-ion packs are 89% cheaper than in 2010, letting four-hour hybrids clear auctions near USD 0.055 per kWh in high-irradiance markets. Australia’s 2024-2025 tenders awarded no CSP, and the United States has not announced new CSP since 2020, as financiers prefer faster, proven photovoltaic projects. Unless RFPs explicitly demand eight-hour-plus discharge or carbon caps favor CSP, bid competitiveness will keep eroding near-term Concentrated Solar Power market share.

High Upfront CAPEX & Limited Project Finance Pools

Average CSP installed cost stood at USD 3,677 per kW in 2024, around 3.7 times photovoltaic benchmarks. Construction spans up to five years, loading projects with interest-rate and foreign-exchange risk. Only USD 6 billion of the USD 40-50 billion CSP investment that the International Energy Agency deems necessary by 2030 was committed in 2024-2025. Multilateral banks fill some gaps, but their lending caps curb diversification, thereby slowing learning-curve benefits in the Concentrated Solar Power industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology – Power Towers Close the Gap

The Concentrated Solar Power market size for parabolic trough systems stood at 4.86 GW in 2025, equal to 66.7% of total capacity, yet power towers are expanding at a 16.8% CAGR en route to 7.3 GW by 2031. Power towers reach 565 °C, integrate 15-hour storage, and secured 100 MW at Dubai Phase 4 in 2023. Although towers carry a 15%-20% cost premium, Spain’s 2025 auctions awarded them 85% capacity credits against 70% for troughs, tilting new orders. Linear Fresnel and dish-Stirling remain niche, collectively under 3% of 2025 installations, but Fresnel arrays find traction in process-heat projects where land constraints and lower temperature needs dominate economics.

Capex learning rates favor towers as heliostat automation improves and supercritical CO₂ cycles target 50% turbine efficiency by 2030. Troughs continue in hybrid retrofits that reuse turbines and balance-of-plant gear, cutting repower capex by up to 40%. Technology choice now hinges less on optical design and more on dispatch duration and storage integration, a shift that will keep the Concentrated Solar Power market diversified yet tower-weighted through the decade.

By Heat Transfer Fluid – Molten Salt Widens Lead

Molten salt held 58.5% of 2025 installations and is on course to reach 70% by 2031, underpinning 9.6 GW of the projected Concentrated Solar Power market size at the end of the forecast period. Dual use as working fluid and storage medium compresses tank volume, as shown by Dubai’s 5,907 MWh storage system. Synthetic oil continues to lose ground amid thermal degradation above 400 °C, while direct steam generation tests in Spain seek lower capex but face control-system complexity. Supercritical CO₂ pilots in New Mexico validated a 10,000-hour operation in 2024, offering a potential 50% cycle efficiency that could unlock further salt alternatives.

Regulation indirectly favors salt, where environmental rules raise containment costs for synthetic oils. China’s nitrate-production dominance remains a supply risk, yet long-term framework contracts have started to appear, smoothing price swings. The shift toward higher operating temperatures cements molten salt as the reference medium, anchoring cost curves in the Concentrated Solar Power market.

By Capacity Range – Mid-Scale Plants Gain Momentum

Plants above 150 MW dominated capacity in 2025 at 3.6 GW, but 50-150 MW projects exhibit the quickest growth, running at a 19.3% CAGR to 2031. A 100 MW tower with 12-hour storage reached financial close in South Africa’s Redstone project in 2024, relying on blended commercial and development-bank debt. This shift toward mid-sized developments is gaining traction across the CSP market. Sub-150 MW designs fit within single-turbine blocks, simplifying debt sizing and construction schedules under 36 months, attributes that appeal to lenders wary of multi-phase megaprojects.

Below-50 MW plants occupy industrial self-generation and off-grid mining niches, where avoided diesel costs justify higher unit capex. Policy incentives in China’s Qinghai province, including fast-track grid interconnection, made the 100-150 MW tranche a sweet spot for domestic investors. Coupled with modular tower receiver packages, mid-scale projects are set to capture a growing slice of the Concentrated Solar Power market share through 2031.

Geography Analysis

Europe retained 2.34 GW of capacity in 2025, equal to 32.1% of the global base, yet growth is muted as auctions favor PV-battery hybrids. Spain’s Solgest-1, a 110 MW direct-steam trough, is the only new European CSP under construction, slated for 2026 commissioning. Policy uncertainty and ample offshore wind resources in Northern Europe limit further uptake, constraining expansion opportunities in the concentrated solar power market.

The Middle East and Africa posted the fastest expansion at 22.5% CAGR. Saudi Arabia’s 2.6 GW pipeline, the UAE’s operating 950 MW complex, and Egypt’s 600 MW tender underpin that momentum. Morocco’s Noor complex proves CSP viability in North Africa, spurring feasibility studies in Tunisia and Algeria, while a 200 MW expansion at Noor was evaluated in 2024. Auction rules bundle sovereign guarantees, de-risking foreign debt, and helping the Concentrated Solar Power market grow rapidly in the region.

Asia-Pacific growth is China-centric. Operating 838 MW in 2024, China has 3.3 GW under construction and targets 15 GW by 2030, backed by provincial feed-in premiums for ≥10-hour storage. India’s CSP ambitions stalled after only 225 MW out of the original 500 MW Jawaharlal Nehru Mission quota reached completion, and Australia’s Aurora project remains unfunded. North America’s 1.7 GW legacy fleet has seen no new projects since 2014, reflecting investor preference for credit-enhanced photovoltaic storage. South America hosts only Chile’s 110 MW Cerro Dominador, with subsequent CSP proposals sidelined by domestic lithium-battery manufacturing policy, highlighting regional disparities within the concentrated solar power market.

Competitive Landscape

Market structure is moderately concentrated: the top five EPC contractors hold about 70% of the active pipeline, giving the Concentrated Solar Power market a mid-range consolidation profile. Leading concentrated solar power companies, including ACWA Power and DEWA leverage sovereign sponsorship to win Middle East megaprojects at debt costs 200-250 basis points below commercial norms. SENER and successor entities to Abengoa dominate tower receiver design, cutting optical losses 12%-15% versus first-generation systems. Shouhang High-Tech’s vertical integration slashes Chinese project capex by 30%, and the firm is bidding to turnkey exports into Belt and Road markets.

Differentiation hinges on technology packages and financing muscle within the concentrated solar power market. BrightSource’s direct-steam tower at Ivanpah improved land-use efficiency by 30% but faced steam-drum control issues and avian impacts, limiting replication. Aalborg CSP’s integrated biomass-CSP systems open combined heat-and-power niches, securing Jiangsu contracts in 2024. Patent activity in wireless heliostat control, recognized by SolarPACES in 2024, indicates a pivot toward digital O&M that could shave 15%-20% life-cycle costs. Collectively, these moves underscore a competitive field driven by cost, dispatchability, and project-delivery track records.

Concentrated Solar Power (CSP) Industry Leaders

ACWA Power

Brightsource Energy Inc.

Abengoa Solar / Atlantica

Shouhang High-Tech

SENER

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: China General Nuclear (CGN) has begun construction of the 50 MW Wumatang Concentrated Solar Power (CSP) project in Tibet. Situated near Lhasa at an elevation of approximately 4,550 meters, this project is set to become the world's highest-altitude CSP facility. It is part of a hybrid solar energy complex that integrates CSP and photovoltaic generation.

- September 2025: Cosmo Films, based in Mumbai, introduced CSP Dualcoat, a dual-coated synthetic paper for various printing applications. It offers durability, tear resistance, and vibrant prints while addressing sustainability by eliminating wood pulp, reducing deforestation, and ensuring performance in challenging conditions, making it ideal for branding and commercial displays.

- September 2025: Alfa Laval Aalborg Header-Coil A/S, a joint venture between Alfa Laval and Aalborg CSP, launched its first product for large-scale thermal energy storage systems. The header-and-coil heat exchanger offers high thermal efficiency, a compact design, and reliability under cyclic operating conditions.

- March 2024: Aptar CSP Technologies and ProAmpac have launched ProActive Intelligence Moisture Protect (MP1000), combining 3Phase ActivPolymer™ and flexible blown film technologies. This patent-pending packaging solution reduces degradation risks, preserves potency, and enhances product performance, marking the first in a series of active microclimate management innovations.

Global Concentrated Solar Power (CSP) Market Report Scope

Concentrated Solar Power (CSP) is the technology developed to generate electricity by transforming concentrated sunlight into solar thermal energy. Mirrors reflect solar radiation to a thermal receiver. The collected solar energy is then absorbed and used to heat the heat-transfer fluid (HFT). The heat retained in the fluid is accumulated, which powers a turbine to generate electrical energy.

The concentrated solar power market is segmented by technology, heat transfer fluid, capacity range, and geography. By technology, the market is segmented into parabolic trough, linear fresnel, power tower, and dish/stirling. Heat transfer fluid: the market is segmented into molten salt, water-based, oil-based, and other heat transfer fluids. By capacity range, the market is divided into below 50 MW, 50-150 MW, and above 150 MW. The report also covers the market size and forecasts for the concentrated solar power (CSP) market across major regions, such as Asia-Pacific, North America, Europe, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Technology

| Parabolic Trough |

| Linear Fresnel |

| Power Tower |

| Dish/Stirling |

By Heat Transfer Fluid

| Molten Salt |

| Synthetic Oil |

| Direct Steam/Water |

| Other Fluids (CO₂, Nanofluids) |

By Capacity Range

| Below 50 MW |

| 50 to 150 MW |

| Above 150 MW |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Parabolic Trough | |

| Linear Fresnel | ||

| Power Tower | ||

| Dish/Stirling | ||

| By Heat Transfer Fluid | Molten Salt | |

| Synthetic Oil | ||

| Direct Steam/Water | ||

| Other Fluids (CO₂, Nanofluids) | ||

| By Capacity Range | Below 50 MW | |

| 50 to 150 MW | ||

| Above 150 MW | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the installed capacity forecast for global CSP by 2031?

Global capacity is projected to reach 16.25 GW by 2031, advancing at a 14.8% CAGR during the period 2026-2031.

Which region is growing fastest in CSP deployments through 2031?

The Middle East and Africa lead with a 22.5% CAGR, backed by sovereign-supported auctions and record-low tariffs.

Why are power-tower systems gaining share over parabolic troughs?

Towers operate at 565 °C, integrate 15-hour storage, and now receive higher capacity credits, driving a 16.8% CAGR to 2031.

How do CSP costs compare with PV-battery hybrids?

CSP averaged USD 0.092 per kWh in 2024 versus roughly USD 0.055 per kWh for PV plus four-hour batteries; CSP becomes more competitive at storage durations beyond eight hours.

Which companies dominate new CSP project pipelines?

ACWA Power, SENER, Shouhang High-Tech, and Abengoa successor entities together oversee about 70% of gigawatt-scale pipelines worldwide.

What role can CSP play in industrial decarbonization?

CSP supplies continuous heat up to 565 °C for sectors like cement and chemicals and can integrate with electrolysis to lower green-hydrogen costs below USD 2 per kg by 2030.

Page last updated on: