Compound Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

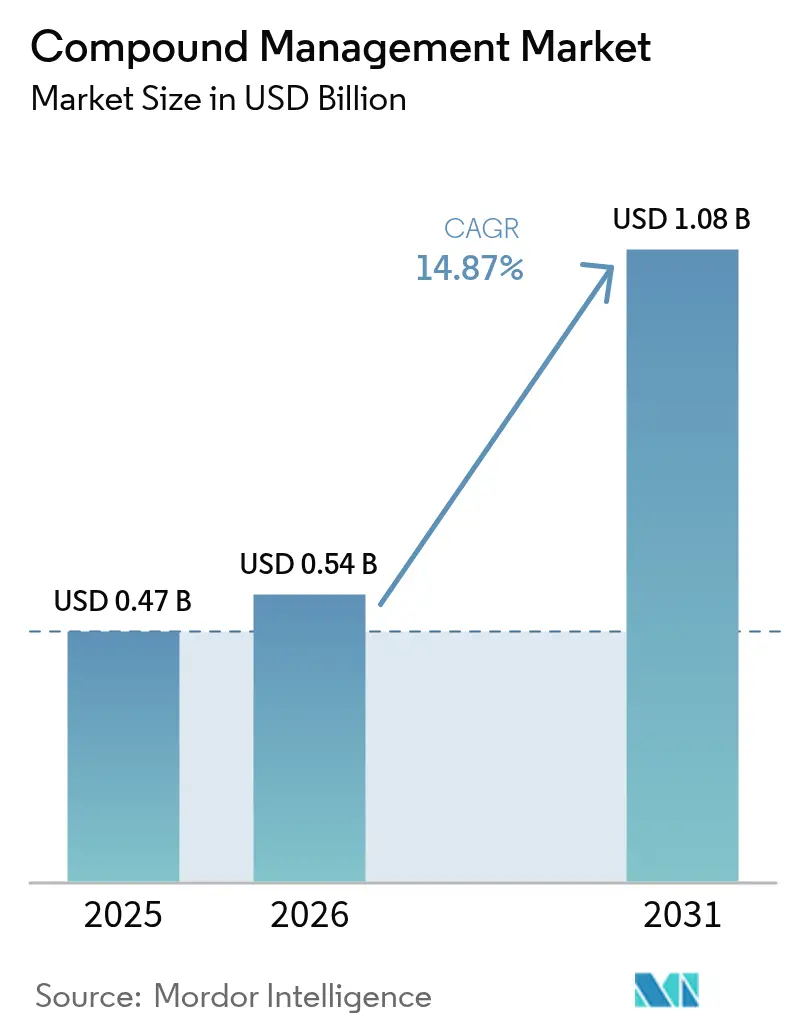

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 14.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compound Management Market Analysis by Mordor Intelligence

The compound management market size is projected to be USD 0.47 billion in 2025, USD 0.54 billion in 2026, and reach USD 1.08 billion by 2031, growing at a CAGR of 14.87% from 2026 to 2031. Robust expansion reflects pharmaceutical and biotech companies’ push to shorten discovery cycles by outsourcing physical libraries, adopting AI-enabled high-content screening, and automating cold-chain logistics. Suppliers that combine robotic freezers with imaging analytics are securing long-term framework agreements, while venture investors channel more than USD 150 million into start-ups that promise modular, software-defined infrastructure. Regulatory updates—such as the FDA’s tighter temperature-excursion guidance and the European Union’s revised data requirements—are turning compliance into a buying trigger, accelerating the replacement of manual systems with audit-ready platforms. At the same time, ESG commitments are steering buyers toward energy-efficient freezers and pay-per-vial storage models that lower Scope 1 and 2 emissions. Moderate concentration among the top five vendors leaves space for niche players in enzymatic DNA synthesis, microfluidics, and low-carbon storage.

Key Report Takeaways

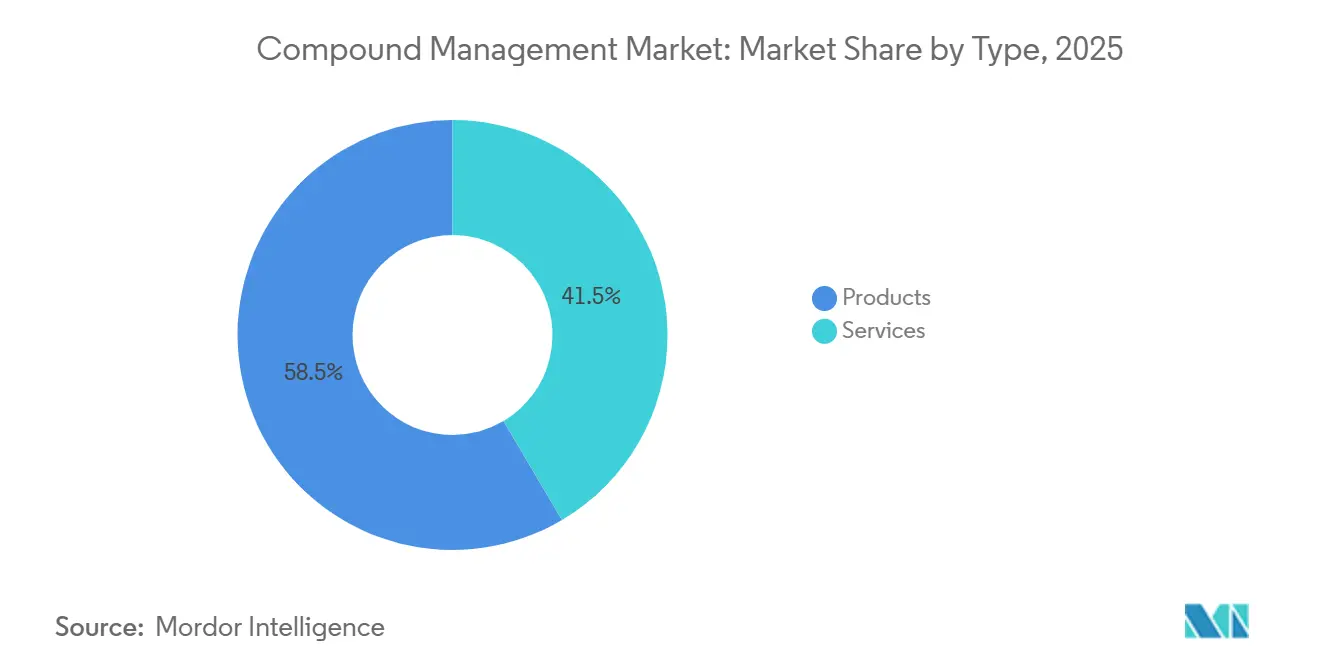

- By type, products led with 58.55% revenue share in 2025; services are forecast to advance at a 16.25% CAGR through 2031.

- By sample type, chemical compounds accounted for 52.53% of the compound management market share in 2025, while biosamples are set to expand at a 17.75% CAGR to 2031.

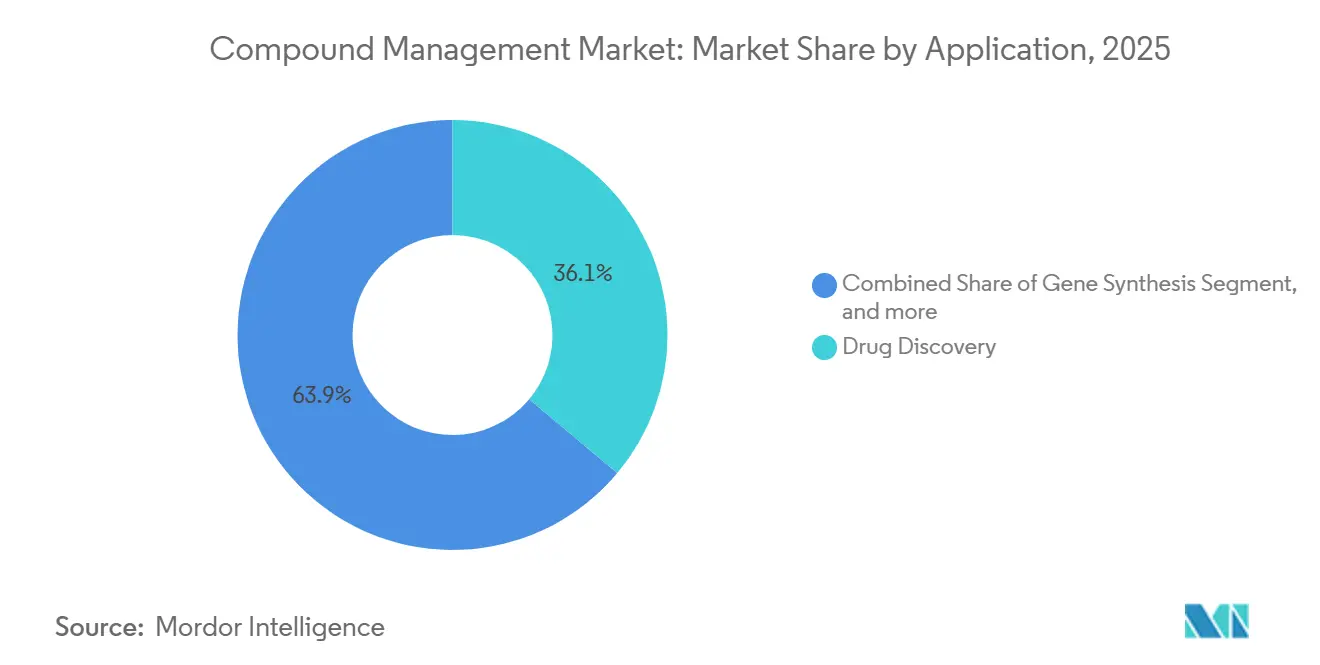

- By application, drug discovery captured 36.15% of 2025 revenue; biobanking is projected to grow at a 17.82% CAGR through 2031.

- By end user, pharmaceutical companies contributed 35.65% of 2025 sales, whereas contract research organizations are poised for a 15.32% CAGR by 2031.

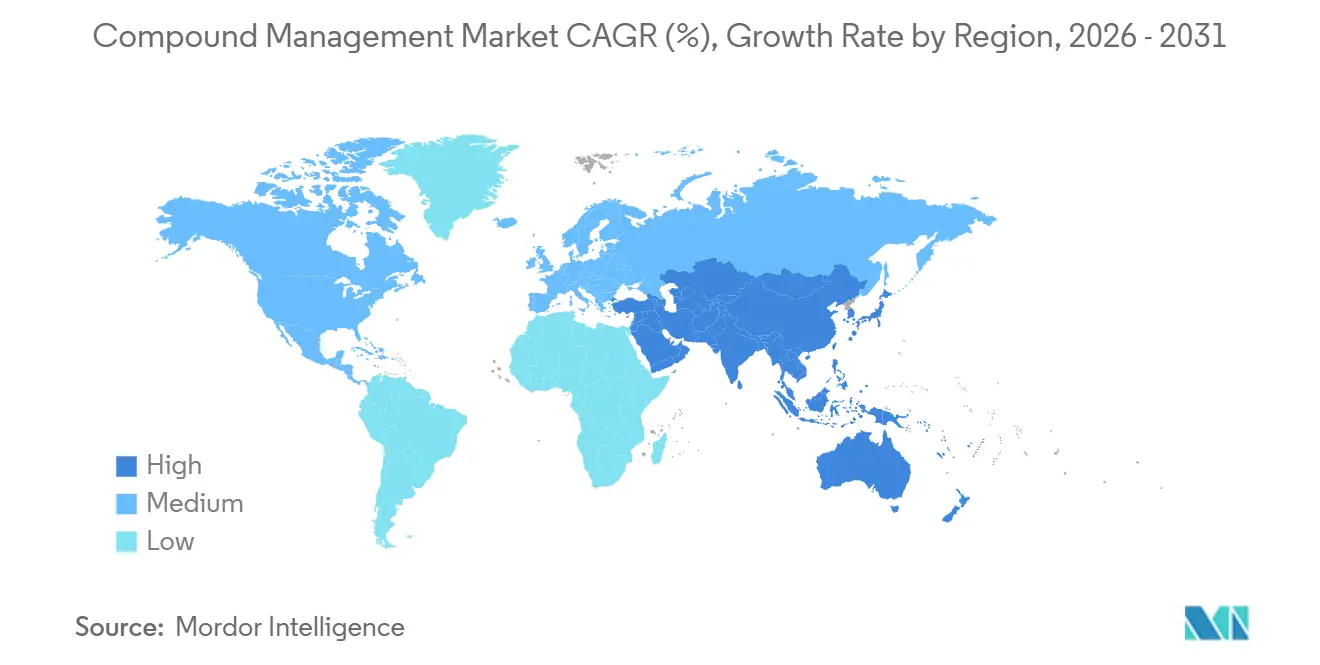

- By geography, North America held 38.23% in 2025, and Asia-Pacific is expected to post the fastest 16.42% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compound Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding AI-enabled high-content screening platforms | +3.2% | Global, North America & Europe | Medium term (2-4 years) |

| Surging biologics & cell-/gene-therapy pipelines | +4.1% | Global, led by North America, rising in Asia-Pacific | Long term (≥ 4 years) |

| Outsourcing of sample libraries to specialized biorepositories | +2.8% | North America & Europe core, Asia-Pacific emerging | Medium term (2-4 years) |

| Cold-chain automation mandates in regulated markets | +2.3% | North America & EU, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Venture-capital inflows into robotic infrastructure | +1.9% | North America primary, Europe secondary | Short term (≤ 2 years) |

| ESG-driven decarbonized laboratory operations | +1.4% | Europe & North America, early in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding AI-Enabled High-Content Screening Platforms

Advanced imaging systems that embed machine-learning models now cut hit-to-lead timelines by up to 40%, fueling demand for robotic freezers that can deliver 384-well plates within minutes. Molecular Devices’ ImageXpress HCS.ai, introduced in 2024, enabled an oncology screen of 1.2 million compounds in six weeks. ZEISS followed with the arivis Cloud in 2025, linking 3-D analytics to compound databases via RESTful APIs for real-time structure-activity insights[1]ZEISS, “arivis Cloud Announcement,” zeiss.com. Open-source pipelines such as PhenoProfiler validate AI triage by predicting bioactivity with 82% accuracy, halving reagent consumption. Start-ups like Automata integrate schedulers that reduce manual transfers by 70%. Together these advances redirect spending from static storage toward integrated discovery suites.

Surging Biologics & Cell-/Gene-Therapy Pipelines

The American Society of Gene and Cell Therapy counted 4,418 active programs in Q1 2025, up 12% year on year[2]American Society of Gene and Cell Therapy, “Q1 2025 Landscape,” asgct.org. Cryogenic precision is critical: WuXi Biologics added three automated vial-thaw suites in 2024 to curb contamination during master-cell-bank expansion. Evotec’s EUR 15 million partnership with Halozyme targets high-concentration biologics that demand inert storage conditions. Novartis collaborates with Isomorphic Labs to rapidly archive thousands of AI-designed antibody sequences. Rising construct volumes therefore elevate the need for scalable, barcode-driven compound management market solutions.

Outsourcing of Sample Libraries to Specialized Biorepositories

Sponsors increasingly transfer stewardship to third-party facilities to convert capex into service fees. BioAscent invested EUR 20 million in its Edinburgh hub in 2024, adding 12 million vial positions and four-hour turnaround. Charles River manages 1.4 million unique compounds across three continents with FDA-compliant chain-of-custody. Syngene’s Bangalore biorepository provides 40% cheaper storage than North American peers. Azenta secured contracts from four top-20 pharma companies using its BioStore III automated freezers. This bifurcation lets sponsors retain core chemistry while outsourcing archiving and plate reformatting.

Cold-Chain Automation Mandates in Regulated Markets

Regulators now insist on continuous monitoring and electronic audit trails. The FDA’s January 2025 guidance fixes deviation thresholds at ±2°C, beyond manual log capabilities. The EU’s Annex 11 revision, effective June 2025, extends similar controls to computerized systems. Vendors respond with sensor-rich incubators like LiCONiC’s STX series that stream data every 30 seconds. SPT Labtech’s RFID-enabled arktic units cut temperature spikes 85%. Mandatory validation is therefore accelerating upgrades across the compound management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx for −80°C & LN₂ automated stores | −1.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Data-integrity & cybersecurity exposure of cloud LIMS | −1.3% | North America & Europe primary, Asia-Pacific secondary | Medium term (2-4 years) |

| Shortage of compound-management skillsets | −0.9% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Volatile supply of lab-grade CO₂/N₂ | −0.7% | Global, episodic regional shortages | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CapEx for −80°C & LN₂ Automated Stores

Fully robotic cryogenic systems cost USD 1.5–3 million each, a hurdle for CROs with revenue below USD 50 million. Azenta’s BioStore III lists near USD 2.5 million before validation, while Brooks’ legacy SampleStore demands clean-room retrofits adding 30–40% to project totals. Six-tank LN₂ arrays can push redundancy budgets beyond USD 2 million[3]Nexus Cryogenic Solutions, “Pricing Guide 2024,” nexuscryo.com . Lease-to-own models from Heraeus offer relief yet struggle for uptake because sponsors want ownership over IP-sensitive libraries. Capital intensity therefore concentrates demand among cash-rich enterprises.

Data-Integrity & Cybersecurity Exposure of Cloud LIMS

A 2025 survey found 38% of IT managers cite ransomware fears as the top barrier to cloud migration. Annex 11 now obliges cloud systems to maintain audit trails and role-based controls, increasing compliance spend for small vendors. Titian’s Mosaic 2025 brings end-to-end encryption and MFA, but roll-out requires staff versed in GxP and cybersecurity, scarce in developing regions. FDA 21 CFR Part 11 audits can extend validation by up to 12 months, slowing adoption. As a result, only 28% of pharma firms had moved more than half their libraries to cloud by late 2024.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Gain Speed as Sponsors Outsource

Products delivered 58.55% of 2025 revenue, anchored by robotic freezers, liquid handlers, and inventory scanners. However, services will outpace hardware with a 16.25% CAGR through 2031 as CROs absorb stewardship duties that once resided in-house. Automated storage systems—typified by Tecan’s Fluent and Hamilton’s Microlab STAR—reduce manual errors 95%, sustaining demand even while commoditization narrows margins. Sponsors refocus capital on AI analytics, letting external biorepositories finance cold-chain infrastructure.

Sample-archiving contracts convert fixed depreciation into variable fees and guarantee four-hour fulfillment. BioAscent’s Edinburgh upgrade added 12 million vial slots, while Syngene’s Bangalore facility undercuts U.S. pricing by 40%. Such models expand the compound management market size for services even as hardware sales plateau.

By Sample Type: Biosamples Accelerate on Advanced Therapies

Chemical compounds held 52.53% in 2025, yet biosamples will climb at 17.75% CAGR as cell and gene therapies proliferate. Each investigational product spawns thousands of cryovials that must remain at −80°C or in LN₂ with chain-of-custody metadata. WuXi Biologics added automated vial-thaw suites that cut contamination in master-cell banks. Enzymatic gene-synthesis start-ups also swell demand for plasmid storage.

Virtual catalogs such as Enamine’s REAL reduce physical small-molecule footprints, slowing chemical growth. Conversely, population cohorts and rare-disease registries extend biosample retention horizons to 50 years, elevating freezer capacity planning across the compound management industry.

By Application: Biobanking Races Ahead, Drug Discovery Remains Core

Drug discovery retained 36.15% of 2025 sales thanks to high-throughput screening and AI triage. Yet biobanking will post a 17.82% CAGR through 2031 as genomics consortia scale to millions of biospecimens. SPT Labtech’s arktic platform reduces door openings 85%, preserving sample integrity for decades. Long-term storage fees and consent-management software push the compound management market size higher in this segment.

Gene-synthesis workflows, though smaller, gain from enzymatic DNA writers that deliver constructs same-day for CRISPR screens. Other niches—materials science or chemical synthesis—adopt similar plate-handling robotics, benefiting from spillover innovation.

By End User: CROs Capture Incremental Spend

Pharmaceutical companies generated 35.65% of 2025 turnover, running centralized libraries for IP security. However, CROs will achieve a 15.32% CAGR as sponsors outsource plate reformatting and long-term archiving. Charles River already supervises 1.4 million compounds globally, shipping under temperature-monitored logistics compliant with FDA audits. Contract developers in India and China leverage labor arbitrage to deliver 24/7 retrieval at lower cost, swelling their share of compound management market revenue.

Academic institutes like UK Biobank contribute steady baseline demand yet operate under capped grants, favoring open-source inventory systems. Biopharma companies pursuing RNA and cell therapies require LN₂ precision, driving premium freezer sales and service contracts.

Geography Analysis

North America led with 38.23% of 2025 revenue, propelled by FDA guidance that mandates real-time temperature alerts and by deep venture funding for lab-automation start-ups such as Automata. Large players like Thermo Fisher, which bought Olink for USD 3.1 billion in 2024, integrate spatial-biology assays with storage workflows, reinforcing the region’s dominance. Canada and Mexico grow as satellite CRO hubs; BioAscent plans a 5 million-vial Toronto site by 2027.

Europe benefits from a unified Annex 11 framework effective June 2025, spurring multi-country biorepository networks. Evotec and Lonza illustrate regional momentum, the latter posting a 12% emission reduction after freezer upgrades. Germany, the UK, and France remain flagship markets, while Switzerland and the Nordics specialize in gene synthesis and precision biobanking.

Asia-Pacific will record the fastest 16.42% CAGR through 2031. Chinese CDMOs like WuXi AppTec reported USD 3.89 billion revenue in 2024 and are deploying automated vial-thaw suites to serve global sponsors. India’s Syngene offers FDA-compliant storage at 40% lower cost, attracting multinational trials. Yokogawa’s RAPID-Lab system aligns with Japan’s legacy ERP frameworks, easing adoption. Emerging clusters in Singapore and Taiwan court investment with modular automation and favorable regulation.

The Middle East, Africa, and South America together represent a smaller but rising share. Brazil’s National Cancer Institute modernized its biobank in 2024, and South Africa’s CSIR opened a gene-synthesis unit in 2025. Supply-chain fragility and skills shortages limit near-term growth yet create long-run catch-up potential.

Competitive Landscape

The compound management market is moderately concentrated: Thermo Fisher, Azenta, Tecan, Hamilton, and Beckman Coulter together command a significant share, but dozens of mid-tier specialists compete on niche innovation. Thermo Fisher’s Olink acquisition links proteomic readouts to freezer fleets, offering a cradle-to-insight platform. Tecan spent USD 576 million on Paramit and EUR 75 million on Cellenion to merge liquid handling with single-cell dispensing. Azenta leverages ISO 9001-certified BioStore III units to win multi-year archiving contracts from four top-20 pharma sponsors.

Disruptors attract venture funding: Ansa’s USD 65 million round advances enzymatic DNA synthesis, removing phosphoramidite waste. Automata’s LINQ orchestrates mixed-vendor robots through a single scheduler, raising USD 45 million. Trilobio’s microfluidic chips promise disposable dilution, cutting cross-contamination. Competitive differentiation is shifting from hardware robustness to software interoperability and cybersecurity readiness; Titian’s Mosaic 2025 adds MFA and encryption in response to 38% of IT managers fearing ransomware.

Compliance expertise becomes a protective moat: Annex 11’s audit-trail mandate strains small vendors lacking dedicated quality teams, while large multinationals build in-house regulatory affairs. Geographical arbitrage also influences strategy; Syngene’s Bangalore site offers compliant storage at 40% savings, and WuXi AppTec’s Shanghai hub provides Asia-Pacific proximity under China’s biosecurity rules.

Compound Management Industry Leaders

Hamilton Company

Azenta Life Sciences

Danaher (Beckman Coulter Life Sciences)

Thermo Fisher Scientific

Tecan Trading AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nanyang Biologics partners with Equinix and HPE to launch Vecura, an AI-driven discovery platform, and plans to build the world’s largest natural compound library in Singapore within a year.

- August 2025: Ginkgo Bioworks forms a strategic alliance with Inductive Bio and Tangible Scientific to pair high-throughput workflows, streamlined compound management, and predictive chemistry AI models for broader drug-discovery access.

Global Compound Management Market Report Scope

Compound management, also referred to as compound control, is defined as the management of chemical libraries, including renewal of outdated chemicals, databases containing the information, robotics often involved in fetching chemicals, and quality control of the storage environment.

The compound management market is segmented by type into products, including automated systems for compound/sample storage, automated systems for liquid handling, and other storage and handling systems, as well as services. By sample type, the market is categorized into chemical compounds and biosamples. By application, it is divided into drug discovery, gene synthesis, biobanking, and other applications. By end user, the market is segmented into pharmaceutical firms, biopharmaceutical firms, contract research organizations, and academic and government institutions. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The study also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value in USD for the above segments.

| Products | Automated Compound/Sample Storage Systems |

| Automated Liquid-Handling Systems | |

| Other Storage/Handling Systems | |

| Services |

| Chemical Compounds |

| Biosamples |

| Drug Discovery |

| Gene Synthesis |

| Biobanking |

| Other Applications |

| Pharmaceutical Companies |

| Biopharmaceutical Companies |

| Contract Research Organisations |

| Academic & Government Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Products | Automated Compound/Sample Storage Systems |

| Automated Liquid-Handling Systems | ||

| Other Storage/Handling Systems | ||

| Services | ||

| By Sample Type | Chemical Compounds | |

| Biosamples | ||

| By Application | Drug Discovery | |

| Gene Synthesis | ||

| Biobanking | ||

| Other Applications | ||

| By End User | Pharmaceutical Companies | |

| Biopharmaceutical Companies | ||

| Contract Research Organisations | ||

| Academic & Government Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What does compound management cover and why is it increasingly vital for drug discovery?

It brings together robotic freezers, liquid handlers, and inventory software to store and retrieve chemicals or biosamples on demand, trimming hit-to-lead timelines by up to 40% through seamless integration with AI imaging systems.

How rapidly is spending on outsourced sample libraries expanding?

Services that archive, reformat, and ship samples for sponsors are projected to climb at a 16.25% CAGR between 2026 and 2031 as companies convert fixed storage costs into pay-as-you-go fees.

Which sample type is growing the quickest and what is driving the surge?

Biosamples are forecast to rise at a 17.75% CAGR through 2031 because cell and gene therapy pipelines demand cryogenic precision for cell banks, viral vectors, and plasmids.

How do regulations such as the FDA's temperature guidance and the EU's Annex 11 affect adoption?

These rules require continuous temperature monitoring, audit trails, and electronic signatures, pushing labs to replace manual freezers and paper logs with automated, software-controlled systems.

In what ways are laboratories reducing the energy footprint of ultra-low-temperature storage?

Measures such as raising set points from -80 °C to -70 °C and fitting variable-speed compressors cut freezer electricity use by 15-28%, helping firms like Lonza lower Scope 1 and 2 emissions by 12% in 2024.

Page last updated on: