Composite Materials In Renewable Energy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.97 Billion |

| Market Size (2031) | USD 16.12 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

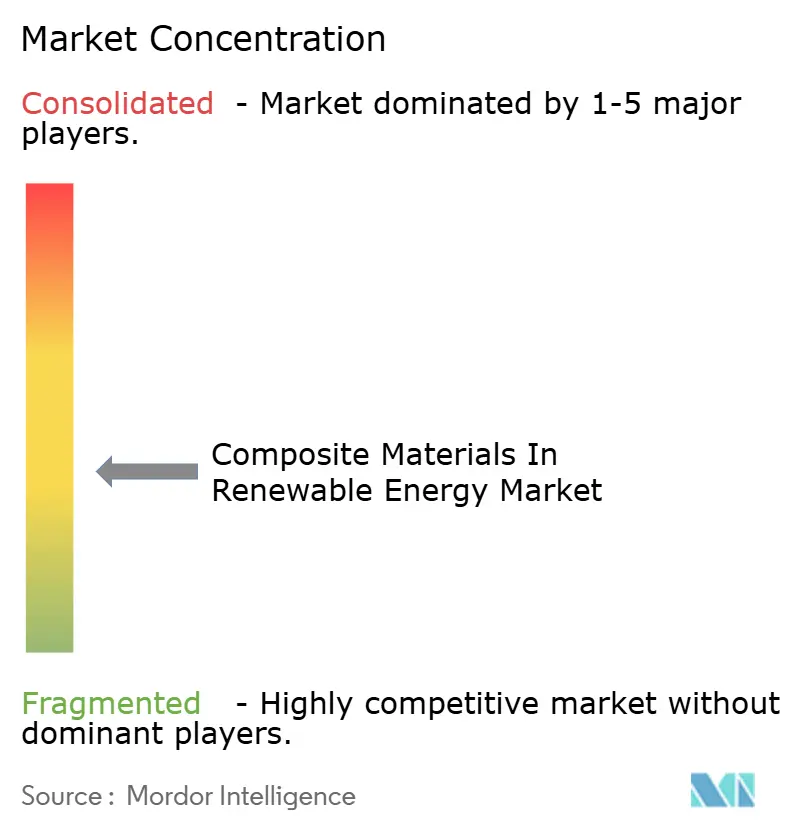

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Composite Materials In Renewable Energy Market Analysis by Mordor Intelligence

The composite materials in the renewable energy market size was valued at USD 10.16 billion in 2025 and estimated to grow from USD 10.97 billion in 2026 to reach USD 16.12 billion by 2031, at a CAGR of 7.99% during the forecast period (2026-2031). Rapid capacity additions in wind, solar, and hydrogen projects demand lighter, stronger structures that extend component lifetimes and shrink carbon footprints. Government clean-energy mandates, breakthroughs in recyclable thermoplastic platforms, and the need for lightweight materials that endure harsh offshore and desert climates combine to accelerate procurement cycles. Automated fibre placement, 3D printing, and other Industry 4.0 processes are compressing production timelines while trimming manufacturing scrap. At the same time, vertically integrated suppliers are consolidating fibre spinning, resin synthesis, and part fabrication to secure critical inputs amid supply-chain tension. These intersecting forces position the composite materials in the renewable energy market for a decade of steady, innovation-driven growth.

Key Report Takeaways

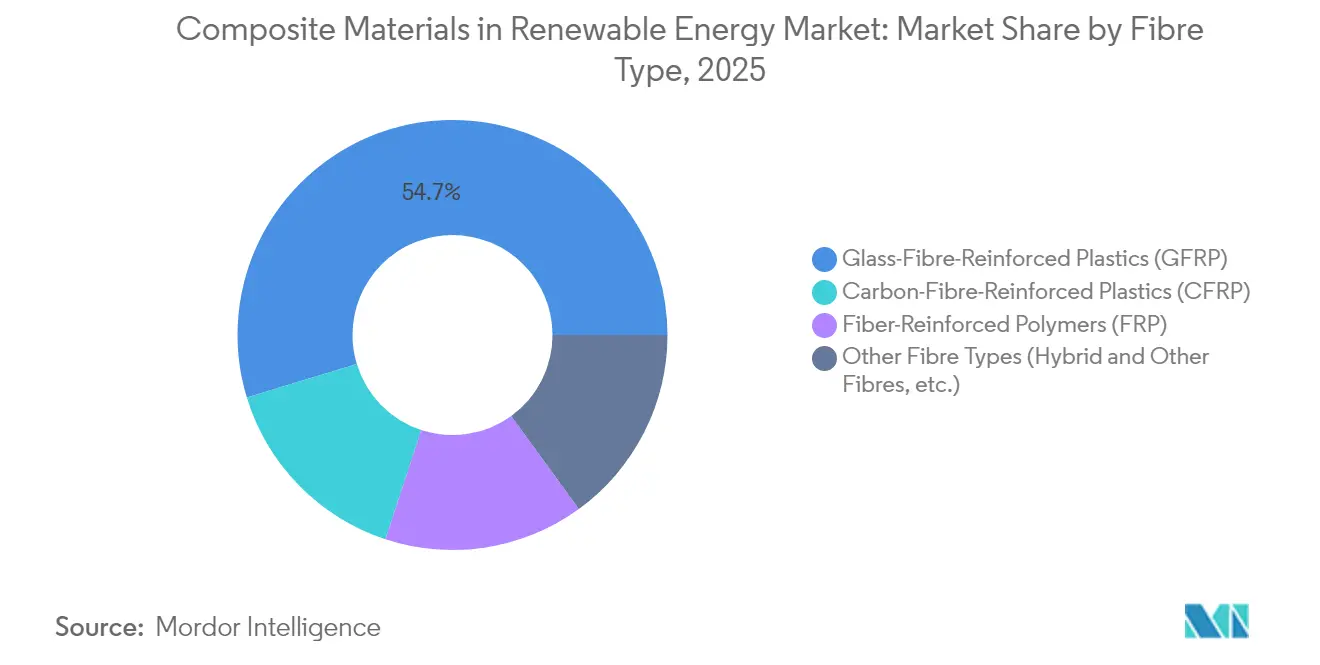

- By fibre type, glass-fibre-reinforced plastics led with 54.70% revenue share in 2025; carbon fibre is projected to grow fastest at 8.39% CAGR to 2031.

- By resin matrix, epoxy accounted for 45.20% revenue share in 2025; bio-resins and recycled resins are projected to grow fastest at 7.88% CAGR through 2031.

- By manufacturing process, vacuum infusion dominated with a 33.75% share in 2025, while automated fibre placement and 3D printing will expand at a 7.75% CAGR to 2031.

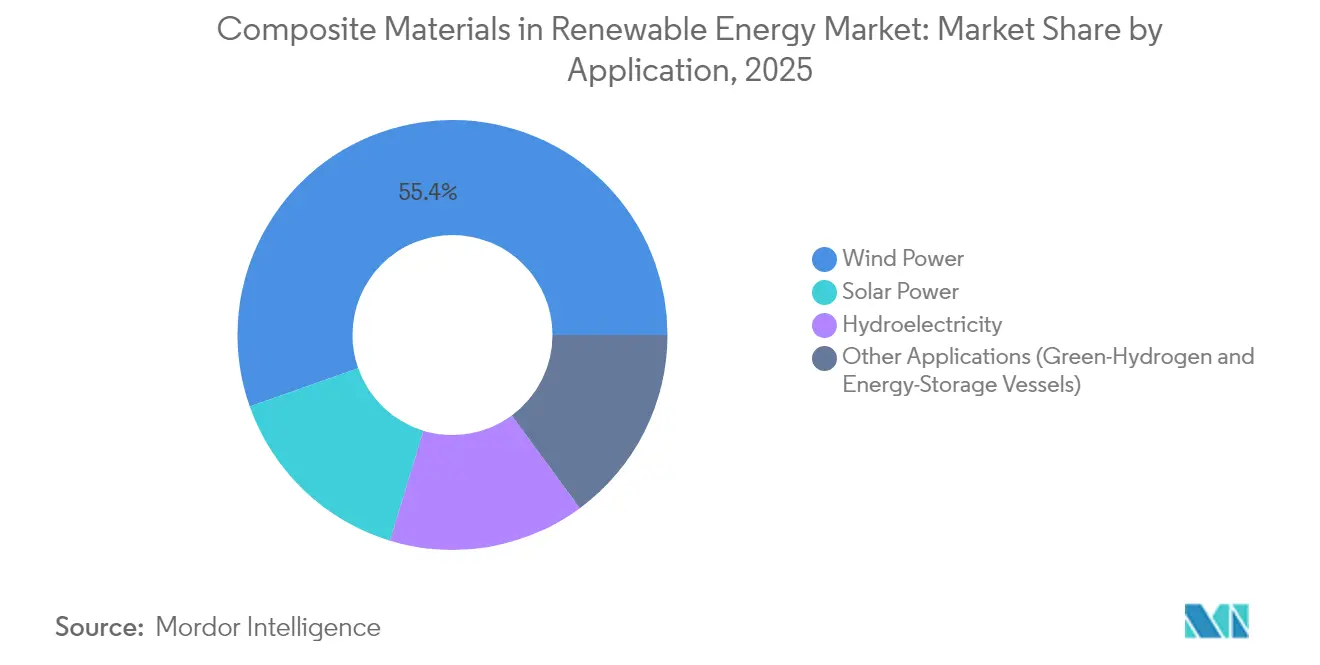

- By application, wind power held 55.40% of composite materials in the renewable energy market share in 2025, whereas other applications, such as green-hydrogen storage and floating solar installations, are projected to advance at the fastest CAGR of 7.60% through 2031.

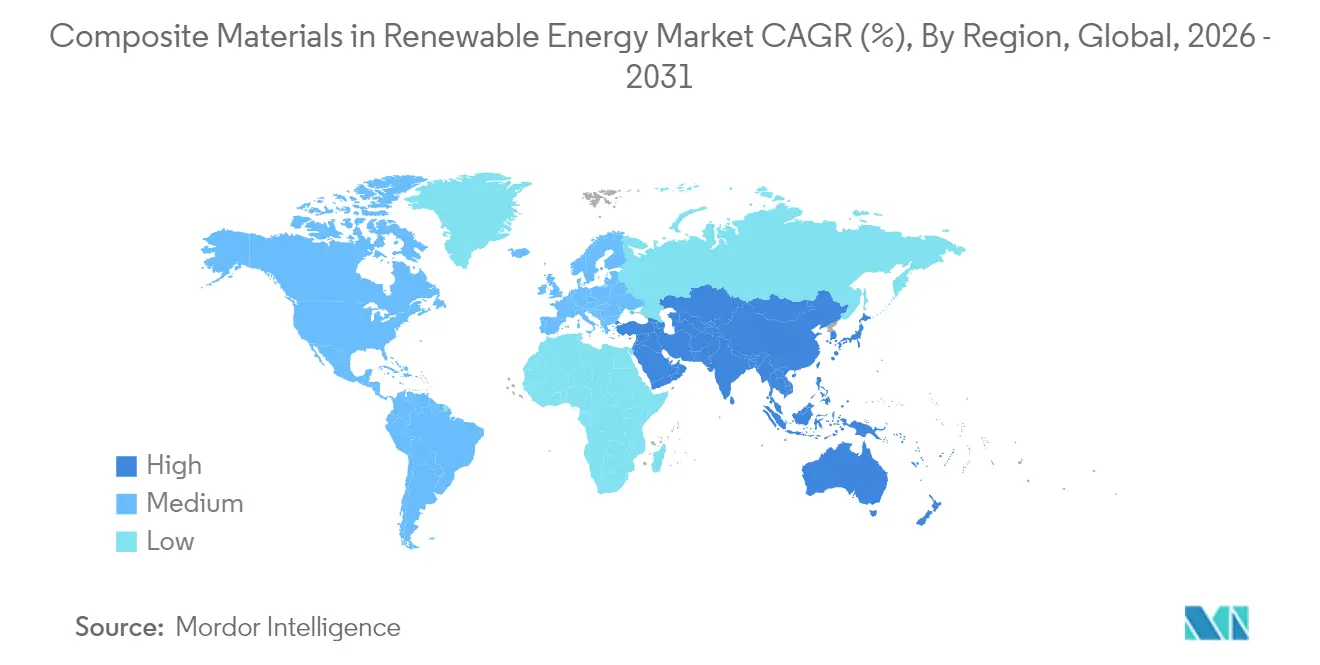

- By geography, Asia-Pacific accounted for 44.30% of the composite materials in the renewable energy market size in 2025 and is forecast to post an 8.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Composite Materials In Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reduced weight versus metallic structures | +1.8% | Global, with strongest impact in offshore wind markets | Medium term (2-4 years) |

| Growing demand for longer wind-turbine blades | +2.1% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Government inclination towards adoption of renewable energy | +1.5% | Global, with early gains in US (IRA), China, and India | Short term (≤ 2 years) |

| Commercialization of thermoplastic recyclable blade platforms | +0.9% | Europe and North America leading, APAC following | Medium term (2-4 years) |

| Rising adoption of 3D printed composite parts in floating solar & tidal devices | +0.7% | APAC coastal regions, expanding to MEA and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reduced Weight Versus Metallic Structures

Composite substitution cuts structural mass in offshore wind, hydrogen tanks, and tidal devices, boosting payload efficiency and easing transport logistics. Weight savings of 13.76% on tidal blades have lifted power output by 46.1% versus steel alternatives. In aerospace, the development of liner-less Type V carbon-composite tanks supports the transition to liquid-hydrogen propulsion, indirectly increasing demand for renewable-grade fibres. Mitsubishi Chemical’s C/SiC ceramic matrix composite endures 1,500 °C, opening paths for heliostat receivers and fusion-reactor hardware. These advances underline why the composite materials in the renewable energy market continue to displace aluminum and steel in high-temperature, corrosive environments.

Growing Demand for Longer Wind-Turbine Blades

Siemens Energy’s 21 MW prototype with a 276 m rotor diameter illustrates how blade lengths nearing 150 m require carbon-fibre spar caps for stiffness-to-weight targets unattainable with glass fibre alone. Segmented blade architectures, enabled by high-toughness epoxy joints, ease transport while maintaining aeroelastic integrity. The ZEBRA consortium completed the world’s largest fully recyclable thermoplastic blade using Arkema’s Elium resin, signalling industrial readiness for closed-loop platforms. Hybrid lay-ups that mix natural and synthetic fibres improve impact resistance and lower embodied carbon, aligning with EU offshore wind targets of 150 GW by 2050 that could double global carbon-fibre demand.

Government Inclination Towards Adoption of Renewable Energy

Policy momentum accelerates procurement. The U.S. Inflation Reduction Act grants a 10% bonus tax credit for domestically sourced components, spurring nearly USD 600 million of new GE Vernova factories and 1,500 jobs in 2025. China’s 2024 green-manufacturing rules call for 40% of all industrial output from certified “green factories” by 2030, fostering investment in blade-recycling capacity[1]Government of China, “Green Manufacturing Policy Framework 2024,” gov.cn. India’s National Hydrogen Mission allots USD 2.4 billion to reach 5 million t annual green-hydrogen output by 2030, priming demand for 700-bar composite vessels. Japan’s perovskite roadmap, spearheaded by a public-private council, targets 38.3 GW by 2040 via flexible composite substrates. Such statutes propel the composite materials in the renewable energy market toward localization and rapid capacity buildout.

Commercialization of Thermoplastic Recyclable Blade Platforms

Arkema’s Elium chemistry enables 100% recyclability through depolymerization without fibre property loss, achieving 90% recovery rates in pilot lines at the University of Sydney[2]University of Sydney, “Closed-Loop Recycling of Thermoplastic Wind Turbine Blades,” sydney.edu.au. Westlake Corporation’s rotor concept similarly separates matrix and fibre for reuse, lowering life-cycle emissions. Advances in APA-6 and CBT resin systems permit room-temperature infusion and faster cure cycles, trimming energy demand. Nonetheless, scaling thermoplastics for 100-m-plus structures necessitates press systems with tighter temperature uniformity and higher tonnage, sustaining capex hurdles that slow widespread adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High research and development and tooling CAPEX | -1.2% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Recycling & landfill-ban compliance costs | -0.8% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Concerns regarding the durability and fire resistance of some composite materials | -0.6% | Global, with particular focus on offshore wind and marine applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Research and Development and Tooling CAPEX

Automated fibre-placement lines cost USD 5–10 million each, while molds for >100 m blades exceed USD 2 million per set, tying up capital for years before payback. Certification programs often run 5-7 years, stretching working-capital needs for mid-tier innovators. Hexcel’s USD 300 million bond issue in 2025 exemplifies the financial firepower required to retain process-technology leadership. Thermoplastic adoption compounds costs, since ovens, presses, and welding equipment differ from thermoset lines, creating parallel asset footprints that hamper small manufacturers’ competitiveness.

Recycling & Landfill-Ban Compliance Costs

EU directives and China’s 2024 recycling mandate make producers responsible for end-of-life blades, lifting operating costs by 2-3 times relative to landfill fees, where disposal remains legal. Pyrolysis and solvolysis plants need multimillion-dollar investments, yet feedstock purity varies, undermining predictable returns. Carbon Rivers’ glass-fibre reclamation route shows industrial viability but requires steady blade-supply contracts to reach scale. Divergent regional rules complicate compliance strategies for global OEMs and add uncertainty to long-range budgeting across the composite materials in the renewable energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fibre Type: Carbon Fibre Expands Premium Niches

The segment generated the largest revenue contribution in 2025, when GFRP held 54.70% of composite materials in the renewable energy market share. Carbon fibre’s 8.39% CAGR reflects rotor diameters that eclipse 120 m, where stiffness and fatigue performance justify its 5-10× cost premium. SGL Carbon’s supply agreements for 80 m-plus blades illustrate vertical moves into energy from aerospace. Fibre-hybrid lay-ups blending basalt and natural fibre reduce embodied carbon yet maintain required modulus, expanding options for mid-range turbine classes. Bio-based lignin fibre research in Germany offers a future cost-reduction lever, although commercial volumes remain limited. Recycled carbon fibre is steadily integrating into secondary structures as mechanical recycling preserves 60-70% original tensile strength, further diversifying feedstocks and tempering raw material price swings.

By Resin Matrix: Bio-Resins Gain Momentum

Epoxy maintained a 45.20% revenue share in 2025 thanks to mature supply chains and high fatigue resistance. Yet bio-resins and recycled resins are expanding at an 7.88% CAGR as OEMs race to satisfy circular-economy mandates. Dow and Vestas have qualified polyurethane spar-cap chemistries that enable rapid pultrusion while elevating interlaminar toughness. Sicomin’s SGi 128 bio-epoxy gel coat demonstrates fire-safe solutions with 35% renewable content. Thermoplastic matrices such as Elium offer the added benefit of repairability and melt recycling, pivoting the composite materials in the renewable energy market toward closed-loop economics.

By Manufacturing Process: Automation Redefines Cost Curves

Vacuum infusion delivered 33.75% of 2025 revenue, retaining primacy for 50-plus-meter blades due to favorable glass-volume fraction and low volatile-organic emissions. Automated fibre placement, robotic filament winding, and 3D printing represent the fastest-growing cluster at a 7.75% CAGR. National Renewable Energy Laboratory prototypes show that additive nacelle covers reduce waste by 20% and cycle time by 35% versus hand lay-up. Solvay’s robotic winding cell achieves 100 m/min deposition, eliminating manual defects. AI-driven cure-cycle control lowers scrap rates, supporting stable throughput despite material batch variability. These shifts recalibrate cost bases and reinforce the competitive edge of well-capitalized plants across the composite materials in the renewable energy market.

By Application: Wind Dominates, Hydrogen Storage Surges

Wind turbines accounted for 55.40% of 2025 sales, yet green-hydrogen storage, tidal devices, and floating photovoltaics are growing at 7.60% CAGR. Composite type-IV and emerging type-V tanks permit 700-bar storage with gravimetric densities outperforming steel by nearly 65%, making them essential for distributed hydrogen refueling stations. AC Marine & Composites’ blade deal for Orbital Marine’s 2 MW tidal unit underscores marine adoption. Floating solar deployments in Southeast Asia and the Middle East demand lightweight, corrosion-proof pontoons that withstand biofouling and UV exposure, tilting procurement toward thermoplastic composites.

Geography Analysis

Asia-Pacific commanded 44.30% of the composite materials in the renewable energy market size in 2025 and is on track for an 8.03% CAGR through 2031. China anchors the region with end-to-end supply chains, yet its 2024 recycling standards raise compliance costs that favor integrated local champions. India’s USD 2.4 billion Hydrogen Mission and defense-sector carbon-fibre push reinforce domestic production incentives. Japan’s perovskite roadmap aims for 38.3 GW by 2040 via flexible composite substrates, a pivot that may recalibrate global solar module architectures. South Korea leverages shipbuilding know-how to enter offshore wind composites, while Australia tests floating solar on inland reservoirs, showcasing regional diversity in end-use cases.

North America benefits from USD 369 billion of Inflation Reduction Act funding, with domestic-content bonuses catalyzing plant expansion in Texas, New York, and Ontario. GE Vernova’s USD 600 million manufacturing buildout exemplifies reshoring moves that cut trans-Pacific logistics risk. Canada’s aerospace-composite cluster supports the transfer of out-of-autoclave methods to tidal-turbine shells, while Mexico’s cost-competitive labor pool draws pultruders for solar-rack exports. The region’s challenge is scaling fibre production to prevent over-dependence on imports, a gap several joint ventures aim to close by 2027.

Europe wields regulatory clout, steering global norms on recyclability and embodied carbon. The ZEBRA project’s thermoplastic blade success positions the continent as a technology frontrunner. Germany’s lignin-fibre pilot lines symbolize R&D leadership, whereas France leverages aerospace heritage to refine high-modulus prepregs. The UK National Composites Centre’s SusWIND program validates multiple recycling routes, giving OEMs design flexibility. Offshore wind buildout in the North Sea and Baltic drives sustained fibre demand, though high energy costs compel automation to defend margins.

Regulatory Landscape

Policy and standards increasingly link circularity, chemical compliance, and turbine integrity requirements to composite selection and end-of-life planning. In the European Union, the European Commission is progressing circular economy policy and is drafting a Circular Economy Act targeted for adoption in 2026, with stated intent to strengthen the single market for secondary raw materials. This direction is likely to raise the emphasis on recyclability and traceability for composite components used in wind and other renewable assets.

For chemicals and technical standards, ECHA committees (RAC/SEAC) have evaluated a proposed broad REACH restriction on PFAS, pointing to potential impacts on multiple technologies, including green energy applications, while discussing use-specific derogations. On the performance side, IEC 61400-5:2020+AMD1:2025 tightens blade integrity and material selection expectations for wind turbines, reinforcing certification-driven qualification cycles. China also implemented GB/T 33630-2025 effective May 1, 2026, updating corrosion protection specifications for offshore wind turbine components, including composite structures exposed to aggressive marine environments.

Value Chain Analysis

The value chain covers (i) upstream fibre and chemical inputs, (ii) intermediate reinforcements and resin systems, (iii) conversion into semi-finished forms (prepregs, fabrics, pultruded profiles), and (iv) fabrication of renewable-energy components such as wind blades and nacelle structures, solar frames and trackers, hydro runner assemblies, and composite pressure vessels for hydrogen and energy storage. Upstream dependencies include glass fibre precursors, PAN-based carbon fibre precursors, and resin chemistries, including epoxy, vinyl ester, polyurethane, and emerging thermoplastic and bio-based systems, with supply risk amplified when production is geographically concentrated.

Component manufacturing and logistics tend to favor regionalized footprints because of blade size and the cost of moving large composite structures. As a result, suppliers often locate fabrication closer to OEM assembly and wind farm installation corridors. For example, TPI Composites operates blade manufacturing capacity across the United States, Mexico, Turkiye, and India, while Lianyungang Zhongfu Lianzhong Composites Group (LZ Blades) maintains operations in China and Germany. Policy discussions around local content and trade defense in Europe also influence where reinforcement, core materials, and finished composite kits are sourced and converted, raising the value of vertically integrated players that can secure fibres, resin supply, and certified processing capability.

Competitive Landscape

The composite materials in the renewable energy market exhibit moderate fragmentation. Sustainability remains a key driver, accelerating R&D in bio-resins and blade recyclability. Strategic moves, such as Toray’s acquisition of a Dutch prepreg line and Owens Corning’s investment in thermoplastic recycling, emphasize vertical integration and alignment with circular-economy mandates. Established leaders maintain a competitive edge through scale in raw-fibre procurement and global qualification data sets, despite potential disruption from new technologies like rapid-cure thermoplastics and AI-enabled process control.

Composite Materials In Renewable Energy Industry Leaders

TEIJIN LIMITED

TORAY INDUSTRIES, INC.

Owens Corning

Gurit Services AG

Hexcel Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circularity-driven redesign and recycling infrastructure are creating whitespace across wind-blade materials, processing, and downstream reuse pathways. The EU push toward clearer waste codes for end-of-life composites, supported by industry bodies such as EuCIA and Glass Fibre Europe, highlights the operational need for auditable collection, classification, and recycling routes. That, in turn, supports demand for resin systems and blade architectures compatible with mechanical or chemical recycling.

Industrialization signals are strengthening. Stena Recycling moved a wind turbine blade chemical recycling system from lab work to an industrial-scale testbed in Halmstad, Sweden (May 2026). Separately, NREL disclosed prototype validation of a plant-derived chemically recyclable resin concept for wind turbine blades (July 2026), pointing to more options beyond landfill and basic mechanical size reduction. Upstream capacity additions and localization programs are also reshaping procurement strategies for large structures, particularly as blade lengths increase and carbon fibre content rises in spar caps and other high-stiffness elements. China-based expansions in large-tow carbon fibre capacity include Sinopec Shanghai Petrochemical starting production on two 3,000-ton carbon fibre lines in Ordos, Inner Mongolia (May 2026), and Zhongfu Shenying bringing additional carbon fibre lines into operation with a 31,000-ton design capacity at Lianyungang, Jiangsu (June 2026). On the component side, Kineco Exel Composites India reaching volume production for carbon fibre wind energy components reinforces momentum toward regional supply chains aligned with domestic-content incentives and transport constraints for large composite parts.

Recent Industry Developments

- April 2026: Teijin Limited commenced full-scale operation of a new natural gas-fired cogeneration system at its Matsuyama plant, targeting an estimated 200,000 tons per year reduction in CO2 emissions. The move supports lower-carbon manufacturing for advanced materials, aligning supplier footprints with renewable OEM requirements around embodied emissions and factory sustainability credentials.

- March 2025: Toray Carbon Fibers Europe announced the operational startup of a new carbon fiber production facility in South-West France producing T300 and high modulus fibers, increasing annual capacity to 6,000 tonnes. Additional European production improves regional availability for wind blade and other renewable-energy composite applications while reducing exposure to long intercontinental logistics for qualified fibre grades.

- September 2024: Kineco Exel Composites India secured a contract to manufacture pultruded carbon fibre planks for Vestas Wind Systems. The award signals deeper localization of wind-component composite supply in India, expanding qualified conversion capacity for carbon fibre profiles used in structural blade elements and related assemblies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is measured as the annual factory-gate value of composite material systems used in renewable energy equipment, where demand follows new build and replacement cycles for key components across wind, solar, hydro, and adjacent storage uses.

Scope exclusions: refurbishment-only parts, legacy fiberglass insulation, and composites used mainly in electric vehicles or civil infrastructure are excluded from the totals.

Segmentation Overview

- By Fibre Type

- Glass-Fibre-Reinforced Plastics (GFRP)

- Carbon-Fibre-Reinforced Plastics (CFRP)

- Fibre-Reinforced Polymers (FRP)

- Other Fibre Types (Hybrid and Other Fibres, etc.)

- By Resin Matrix

- Epoxy

- Polyester

- Polyurethane

- Thermoplastic

- Bio-resins and Recycled Resins

- By Manufacturing Process

- Vacuum Infusion

- Prepreg/Autoclave

- Pultrusion

- Automated Fibre Placement / 3-D Printing

- Compression Moulding (SMC, BMC)

- By Application

- Wind Power

- Solar Power

- Hydroelectricity

- Other Applications (Green-Hydrogen & Energy-Storage Vessels)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean view of renewable energy build-out and identifying where composite materials are used in practice, then linking those usage points to materials intensity. We refer to public sources such as the International Energy Agency for capacity additions, the International Renewable Energy Agency for deployment trends, and U.S. Energy Information Administration releases for generation and capacity context. For trade and production signals, we also review customs and trade statistics agencies where relevant, along with national statistics offices for manufacturing output and industrial price indices.

To keep assumptions realistic, we cross-check against company annual reports and investor presentations, and we incorporate technical standards and guidance that industry associations publish. Where available, we also use peer-reviewed materials engineering journals that describe blade and component design changes over time. In a few places, paid subscriptions that consolidate company financials, patent activity, and shipment-level import-export records are used to speed up checks on volume direction and technology change. These desk sources are illustrative only, and many other public references were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm how composite usage per unit is changing and how pricing is being set as resin systems, fiber mixes, and manufacturing yields shift. We speak with stakeholders across material suppliers, component makers, and renewable equipment supply chains, and we cover major demand regions so the model reflects real ordering patterns rather than announced capacity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 21% | APAC: 45% |

| Mid tier: 41% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 21% | Managers: 42% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where renewable capacity additions and equipment production trends are reconstructed into a demand pool for composite-intensive components, and then converted into value using realistic material intensity and pricing. We corroborate the totals with selective bottom-up approximations, including sampled bill-of-material checks for blades and structural parts, channel inputs on typical order mixes, and sanity checks on composite ASP ranges by fiber and resin type.

A few practical inputs used in the model include annual wind installations and repowering activity, average rotor diameter and blade length trends, composite content per MW for blades and nacelle covers, solar tracker and frame adoption rates, and the glass fiber versus carbon fiber mix (including hybrid designs). Where public data is thin, gaps are handled by using ranges from interviews and narrowing them through consistency checks against trade flows, capacity utilization signals, and observed price movements.

For forecasting, scenario analysis is used around installation pipelines and policy-driven build rates. The main case is supported by time-series smoothing on key indicators such as annual additions and materials pricing, and it is reviewed with expert feedback before being locked into the model.

Data Validation & Update Cycle

Outputs are checked against independent signals, including renewable capacity additions, component production cues, and the direction of fiber and resin pricing, so the final values stay anchored to observable market movement. When a number looks off, we trace it back to the driver, test alternative assumptions, and re-contact sources when the variance is material.

Before sign-off, the workbook goes through step-by-step analyst review so unit conversions, currency timing, and inflation handling remain consistent across regions and years. The report is refreshed annually, and interim updates are made when major policy shifts, large project delays, or sudden materials price changes can alter near-term demand, followed by a final pre-delivery pass to keep the view current.

Mordor Intelligence's Renewable Energy Composite Materials Market Sizing Compared With Other Published Estimates

Published market sizes for this topic can look far apart because the same words are used for different things, and because some studies tie their values to energy asset spending instead of materials sold. Currency timing, the year chosen as the starting point, and how fast prices are assumed to rise also tend to move totals up or down.

The main gap comes from whether non-material items and broad green energy composites are counted. Mordor Intelligence limits the value to factory-gate composite systems used in defined renewable equipment parts, and it keeps refurbishment-only demand out of scope. Some external figures also assume higher composite intensity per unit as rotor sizes grow, or they mix in adjacent sectors like electric mobility, which pushes the number above what renewable hardware build alone would support.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.97 B (2026) | |

| Industry Research House A | USD 18.90 B (2024) | Uses an earlier base year and appears to include a wider renewable composites scope with less clarity on factory-gate material-only treatment, which can pull in non-composite system value and adjacent component spend. |

| Syndicated Publisher B | USD 12.10 B (2025) | Starts from a different base year and applies a higher growth path through 2034, and it may blend broader application definitions and intensity assumptions that do not separate new-build materials from refurbishment demand. |

Seen together, the spread is mainly explained by scope choices and how intensity and pricing are carried forward from the base year. Our approach stays traceable because each step is tied back to renewable build indicators, component-level composite use, and practical price checks that can be repeated as new data comes in.

Key Questions Answered in the Report

What is the current Composite Materials in Renewable Energy Market size?

The Composite Materials in Renewable Energy Market size is USD 10.97 billion in 2026 and is on course to hit USD 16.12 billion by 2031 at an 7.99% CAGR.

Which application has the biggest share in Composite Materials in Renewable Energy Market?

Wind power accounts for 55.40% of current sales, reflecting the sheer scale of global onshore and offshore installations.

Which is the fastest growing region in Composite Materials in Renewable Energy Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

How are governments influencing the market’s trajectory?

Policies such as the U.S. Inflation Reduction Act, China’s green-factory rules, and India’s Hydrogen Mission provide financial incentives and domestic-content requirements that spur regional composite production.

Page last updated on: