Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

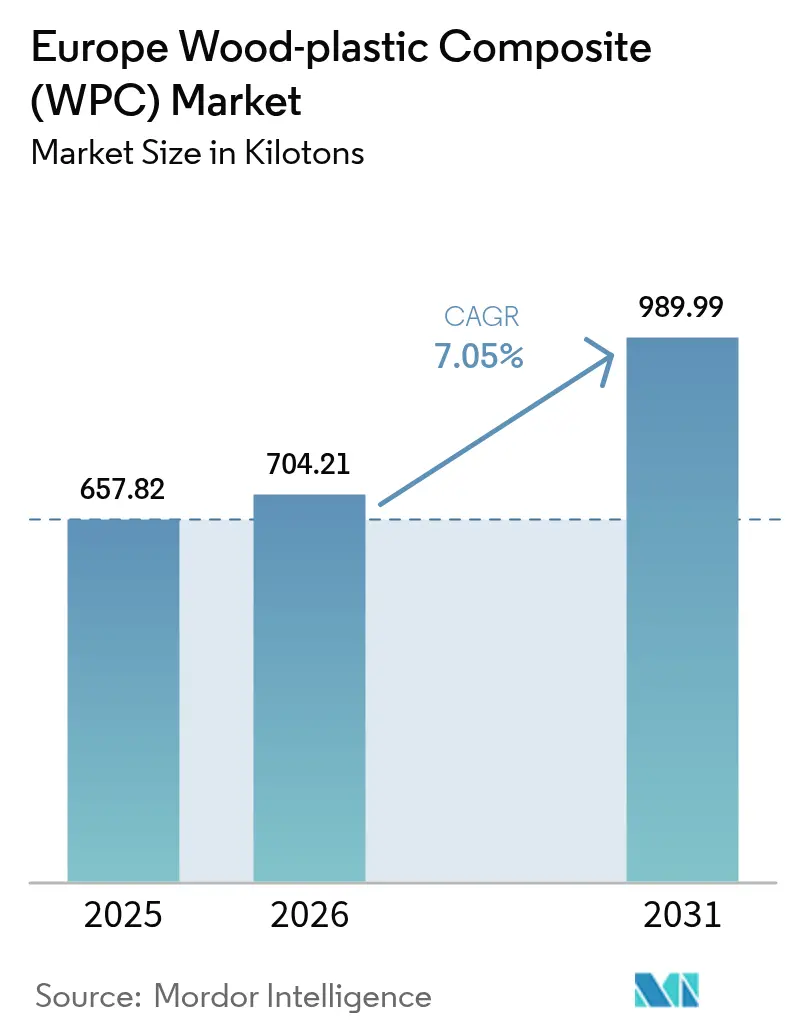

| Base Year Market Size (2025) | 657.82 kilotons |

| Market Volume (2026) | 704.21 kilotons |

| Market Volume (2031) | 989.99 kilotons |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

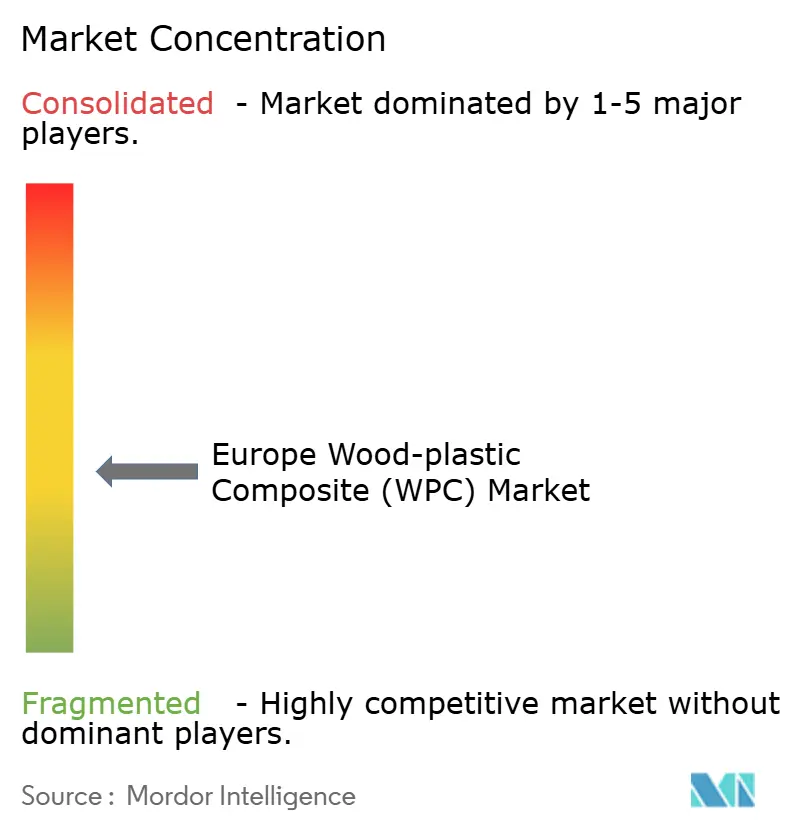

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wood-plastic Composite (WPC) Market Analysis by Mordor Intelligence

The Europe Wood-plastic Composite market size is expected to grow from 657.82 kilotons in 2025 to 704.21 kilotons in 2026 and is forecast to reach 989.99 kilotons by 2031 at 7.05% CAGR over 2026-2031. Adoption accelerates because regulators, builders, and OEMs view the material as a direct pathway to decarbonize products without sacrificing performance. Demand gains trace to the EU-wide plywood anti-dumping duties that tilt price dynamics in favor of composites, to the recovery of Europe’s construction spending, and to automotive lightweighting imperatives that spotlight natural-fiber–reinforced plastics. Competitive intensity is rising as recyclate-friendly silicone coupling chemistry unlocks higher post-consumer content, and as corporate acquisitions consolidate technology, distribution, and brand power. Manufacturers able to verify feedstock origin under the EU Deforestation Regulation and to match regional design aesthetics with fade-resistant formulations are positioned to capture incremental share within the expanding Europe Wood Plastic Composite market.

Key Report Takeaways

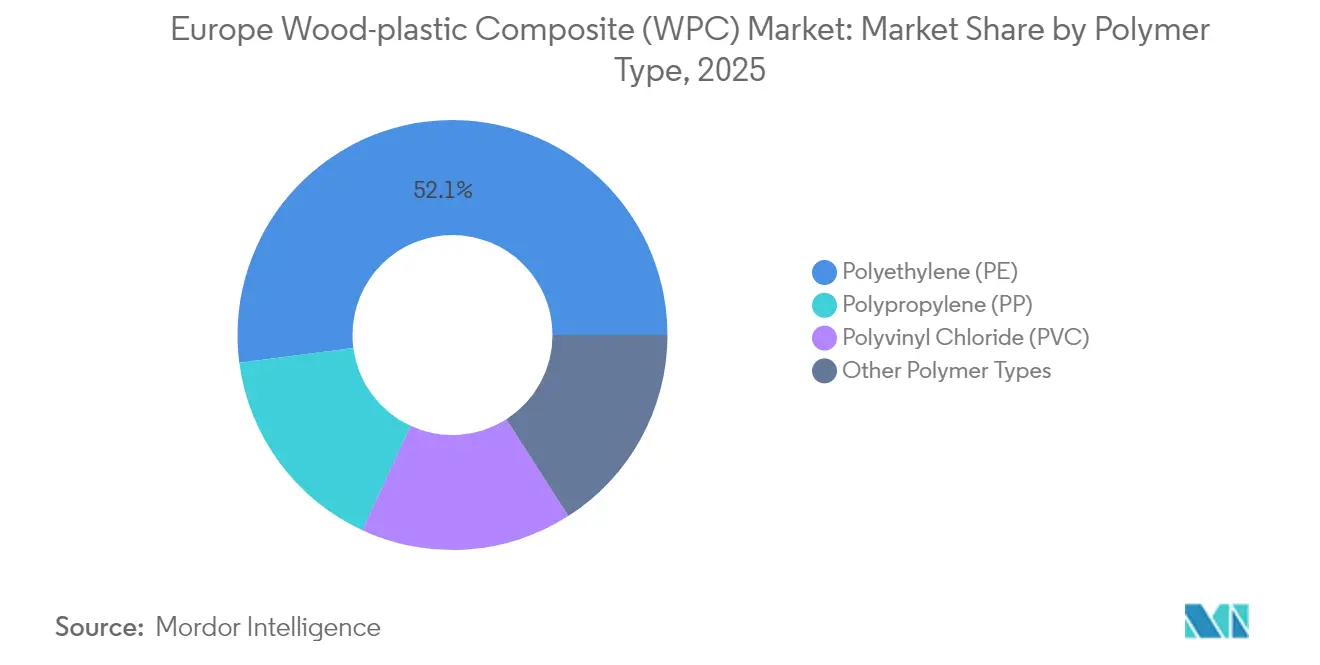

- By polymer type, polyethylene led with 52.06% of the Europe Wood Plastic Composite market share in 2025, while polypropylene is projected to expand at an 7.75% CAGR to 2031.

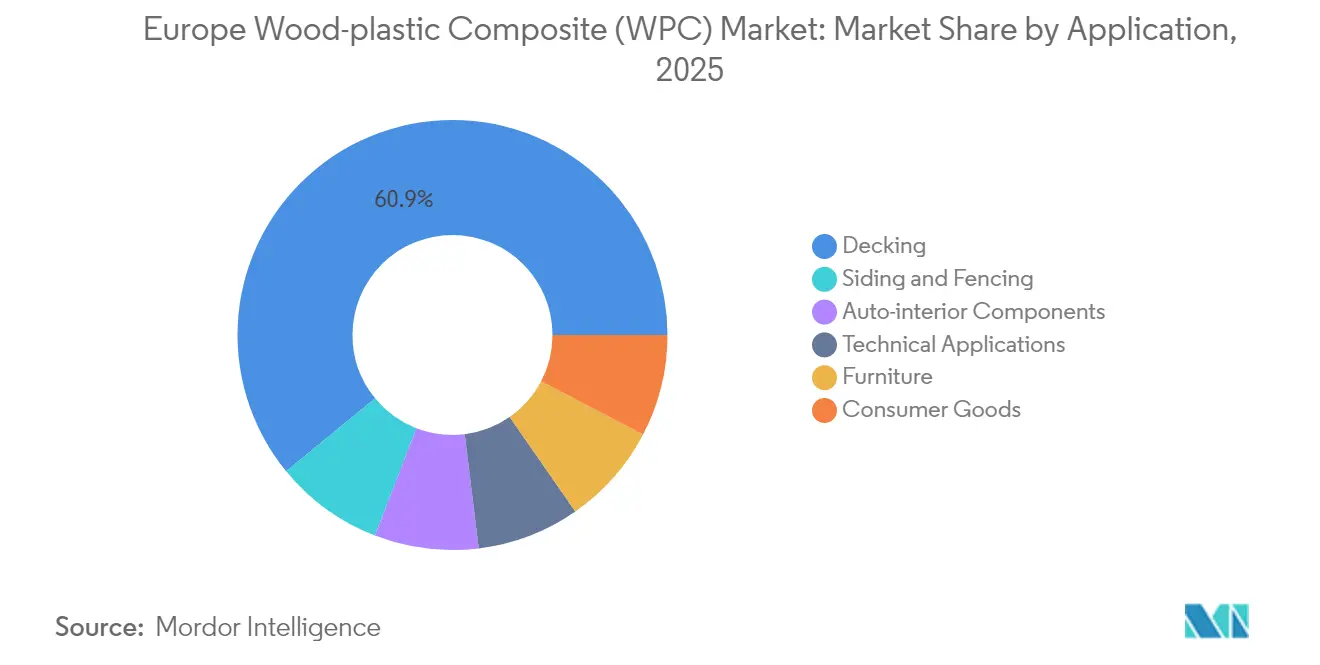

- By application, decking accounted for 60.92% share of the Europe Wood Plastic Composite market size in 2025 and siding and fencing is advancing at a 8.79% CAGR through 2031.

- By geography, Germany held 38.31% revenue share in 2025; Denmark is forecast to register the highest CAGR at 7.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Wood-plastic Composite (WPC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable Characteristics of WPC Drive Circular Economy Adoption | +1.8% | Global, with strongest impact in Germany, Nordic countries | Long term (≥ 4 years) |

| Construction-Sector Demand Resurgence Accelerates Infrastructure Investment | +2.1% | Germany, France, UK core markets with spillover to Eastern Europe | Medium term (2-4 years) |

| Lightweighting Push in European Automotive Interiors Creates Niche Opportunities | +1.2% | Germany, France, Italy automotive manufacturing hubs | Medium term (2-4 years) |

| EU Anti-Dumping Duties on Asian Plywood Spur WPC Substitution | +1.5% | EU-wide, particularly Germany, Belgium, Netherlands import centres | Short term (≤ 2 years) |

| EUDR Traceability Boosts Demand for Certified-Origin WPC | +0.8% | EU-wide regulatory compliance requirement | Long term (≥ 4 years) |

| Low-Temperature Silicone-Coupling Tech Enables High-Recycled-Content WPC | +0.6% | Advanced manufacturing regions: Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainable Characteristics of WPC Drive Circular Economy Adoption

European brands position Europe Wood Plastic Composite market offerings as carbon-smarter substitutes that can lock up to half of their polymer matrix in recyclate while still clearing VinylPlus audits[1]Deceuninck, “Annual Report 2023,” deceuninck.com . Mechanical recyclers feed sorted film and rigids into twin-screw extruders, and coupling agents restore fiber–matrix adhesion so decking boards retain flexural strength. The integration of municipal solid-waste streams diverts landfill tonnage and shields processors from virgin polymer volatility. Germany’s take-back schemes now certify geo-tracked wood fiber streams, a regulatory advantage that increases buyer confidence. Even with polymer chain scission after multiple melt cycles, compounders maintain dimensional stability by blending virgin pellets at calibrated thresholds. As a result, the Europe Wood Plastic Composite market secures environmental credits that translate into specification wins with public-sector contractors.

Construction-Sector Demand Resurgence Accelerates Infrastructure Investment

ING’s 2025 outlook confirmed that Europe’s building output returns to positive territory, converting EU Recovery Fund disbursements into renovation outlays that favor low-maintenance cladding. Nordic developers retrofit schools and municipal offices with insulated composite façades that withstand freeze-thaw cycles. Capital projects in France bundle WPC walkways with flood-resilient flood-barrier systems for coastal towns. Suppliers embed hidden-clip systems to reduce onsite labor, an advantage in high-wage Western Europe. Re-roofing and balcony revamps fuel inventory turnover in specialty merchant channels, while public procurement frameworks increasingly score bids on life-cycle emissions. Consequently, the construction rebound supplies a durable volume baseline for the Europe Wood Plastic Composite market.

Lightweighting Push in European Automotive Interiors Creates Niche Opportunities

Original equipment manufacturers replace talc-filled PP panels with 30 wt % wood-fiber-reinforced PP to shave 12% mass and improve acoustic damping in hatchback door trim. Tier-1 molders qualify new material cards under VDA 276 emissions testing, addressing in-cabin volatile organic compound limits. Processors exploit the higher heat-deflection temperature of PP versus PE to survive paint oven bake cycles. Additive packages tailor odor, scratch, and color to meet brand interiors. Audi, Renault, and Stellantis pilot olive-pit or wheat-straw fibers, yet eucalyptus and spruce remain dominant in compound recipes due to uniform morphology. As lightweight norms tighten under the EU fleet emissions cap, automotive pull-through volumes, while modest against decking, provide a high-margin adjunct that elevates the Europe Wood Plastic Composite market profile.

EU Anti-Dumping Duties on Asian Plywood Spur WPC Substitution

On 11 June 2025 the European Commission imposed provisional duties of 62.4% on imported Chinese hardwood plywood, instantly widening the cost delta in favor of domestically extruded composite sheets. Builders that relied on bonded birch panels for temporary formwork pivot to WPC alternatives that can be reused multiple cycles. Importers redirect supply contracts toward regional compounders, unlocking roughly EUR 2.8 billion worth of demand displacement across under-roof decking and crate skids. Manufacturers with short lead times secure framework contracts from DIY chains facing seasonal surges. The tariff window lasts six months but is widely expected to convert into definitive measures, cementing an enduring addressable gain for the Europe Wood Plastic Composite market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Upfront Cost vs. Pressure-Treated Timber Limits Mass-Market Penetration | -1.4% | Price-sensitive markets: Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| UV / Weathering and Color-Fade Challenges Require Advanced Stabilization Systems | -0.9% | High UV exposure regions: Southern Europe, outdoor applications | Medium term (2-4 years) |

| Fire-Performance Compliance Costs Under EU Building Codes | -0.7% | EU-wide, particularly high-rise construction applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost vs. Pressure-Treated Timber Limits Mass-Market Penetration

Price comparisons in Romania and Bulgaria show WPC decking retailing at 40-60% premiums versus impregnated spruce boards, keeping cash-constrained homeowners on traditional lumber. Labor savings only accrue over years, whereas purchase decisions remain dominated by invoice totals. Builders face certification fees for CE marking under EN 15534, inflating entry barriers for small lot sizes. Subsidy programs rarely target composite materials, leaving processors to craft own-brand financing schemes. Until production economies of scale or recycled-content credits compress cost curves, this restraint moderates unit uptake in peripheral economies, tempering volume expansion for the Europe Wood Plastic Composite market.

UV / Weathering and Color-Fade Challenges Require Advanced Stabilization Systems

Accelerated xenon-arc testing confirms PP-based composites can lose up to 35% tensile strength after 1,000 hours when unprotected, while color ΔE values exceed homeowner acceptability thresholds in Mediterranean climates. Carbon-black masterbatches enhance stability but yield darker hues that limit architectural freedom. Cap-stock co-extrusion adds bill-of-material cost, and organic-pigment packages suffer photobleaching. Heat-treated fibers improve matrix adhesion yet introduce variability in moisture uptake. Suppliers experiment with nano-TiO₂ and HALS stabilizers but must verify recyclability impacts under DIN EN 13430. The net effect is a technical challenge that restrains exterior-cladding growth potential within the Europe Wood Plastic Composite market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Polyethylene Holds Lead but Polypropylene Gains Momentum

Polyethylene recorded a 52.06% share of the Europe Wood Plastic Composite market in 2025, underscoring the entrenched processing infrastructure and its compatibility with softwood fibers. Un-foamed PE profiles exhibit low melt viscosity, enabling high line speeds that translate into cost-per-linear-meter advantages. The segment benefits from widespread availability of post-consumer high-density polyethylene streams sourced from bottle reclaimers, which plug easily into extrusion recipes. Compounders leverage maleic-anhydride-grafted compatibilizers to stabilize the interface, allowing boards to pass EN 310 flexural testing with modest virgin polymer additions. Despite these strengths, PE’s comparatively low heat-deflection temperature curtails its use in automotive or technical panels that encounter service temperatures above 90 °C.

Polypropylene, although trailing in volume, is projected to register the segment-leading 7.75% CAGR as OEMs seek higher heat performance and stiffness for interior modules. Researchers at European institutes demonstrate that PP-based composites deliver 15% higher flexural modulus than PE analogues at equal fiber loadings, while absorbing 25% less moisture. Mold-in-color capability aligns with carmaker demands for class-A surfaces that avoid paint. However, PP processing necessitates tighter thermal windows to avert oxidative degradation, compelling processors to invest in nitrogen-blanketed gravimetric feeders. PVC maintains smaller niches in window profiles and marine decking where inherent UV and flame behavior outweigh cost. Emerging bio-resins such as PLA and PHA remain below 1% share due to price, yet pilot lines in the Netherlands explore their integration, signaling future possibilities for diversifying the Europe Wood Plastic Composite market.

By Application: Decking Continues to Dominate as Siding Outpaces Growth

Decking retained a commanding 60.92% share of the Europe Wood Plastic Composite market size in 2025, supported by mature DIY segments and standardized clip-lock installation systems. Promotional financing at big-box retailers encourages homeowners to trade up from softwood planks based on lifetime maintenance savings. Slip-resistance ratings under EN 15534-1 classify grooved surfaces for poolside use, expanding hospitality demand across Mediterranean resorts. Nonetheless, growth is moderating because replacement cycles elongate and penetration is already deep in Belgium, Germany, and the Netherlands. To maintain velocity, brands introduce embossed cap-stocks that emulate exotic hardwood grain, combining visual differentiation with scratch resistance.

Siding and fencing, although smaller, accelerate at a 8.79% CAGR as façade designers prioritize materials that integrate insulation layers while resisting UV chalking. Cladding installers appreciate light weight, which simplifies scaffolding logistics on retrofit jobs. Regulatory triggers, notably France’s RE2020 energy code and Germany’s BEG subsidy, elevate demand for exterior rainscreen systems that deliver both thermal and moisture management. Boards pre-drilled for hidden fasteners cut labor hours, while color-through cores reduce on-site touch-up. Fire-performance challenges remain, but ammonium-polyphosphate additives enable C-s3, d0 classifications under EN 13501, widening acceptance in mid-rise projects. The convergence of building-physics requirements and aesthetic preferences expands end-market diversity, reinforcing medium-term scalability for the Europe Wood Plastic Composite market.

Geography Analysis

Germany’s 38.31% share anchors the regional landscape due to its co-located automotive and building-materials value chains. Compounders benefit from access to more than 15 000 installed twin-screw extruders that permit quick recipe iteration. Municipalities demand certified recyclate content in public tenders, lifting average selling prices and margins. Dual-use lines switch from decking to interior trim, balancing seasonal order patterns and smoothing revenue. The domestic fire code pushes suppliers to certify each profile segment, increasing entry barriers that favor incumbents within the Europe Wood Plastic Composite market.

Nordic countries represent the fastest-growing cluster, led by Denmark’s 7.88% CAGR, thanks to aggressive carbon-neutrality schedules that incentivize low-maintenance façades across social housing. Finland institutionalizes procurement of circular products, channeling sawmill residues into composite extrusion. Sweden’s timber-house producers pair WPC terraces with cross-laminated-timber structures to simplify on-site logistics during short construction windows. Norway’s offshore infrastructure orders salt-spray-resistant gangways, leveraging WPC’s corrosion immunity. Across the bloc, life-cycle-assessment tools standardize environmental declarations, enabling specifiers to benchmark composite offerings and boosting transparency in the Europe Wood Plastic Composite market.

Western Europe, encompassing the United Kingdom, France, Belgium, Italy, and Spain, delivers steady but differentiated growth paths. The United Kingdom’s retrofit push drives demand for cladding kits that integrate fire-barrier layers post-Grenfell. France aligns cladding choices with its NF DTU standards, prompting suppliers to localize testing. Belgium’s status as a polymer import gateway supplies compounders with competitive feedstock, encouraging export-oriented production. Italy and Spain draw on tourism infrastructure upgrades—boardwalks, hotel terraces, marina docks—to specify WPC. Across all sub-regions, EUDR compliance and evolving fire classifications create baselines that professionalize the supplier base and help the Europe Wood Plastic Composite market scale beyond early-adopter niches.

Competitive Landscape

Consolidation reshapes the field after James Hardie’s USD 8.75 billion acquisition of AZEK in 2024, which pairs AZEK’s capped-decking know-how with James Hardie’s fiber-cement channel to broaden European distribution. Large players wield portfolio breadth and marketing budgets to lock shelf space at builders’ merchants. Deceuninck’s vertical integration embeds in-house PVC recycling that lifted reclaimed content to 18% in 2024, supporting VinylPlus accreditation and price premiums. Regional specialists in Poland and the Czech Republic concentrate on private-label production for Northern European brands, while Italian processors exploit design-centric expertise to sell premium terrace kits into luxury hospitality.

Technology partnerships differentiate competitors. Dow supplies silicone-coupling pellets that allow higher recyclate loads without downgrading mechanicals, helping processors meet circular-content quotas. Coperion and Bausano market turnkey extrusion lines that integrate melt filtration and pelletizing, reducing contamination risks associated with post-consumer streams. German toolmakers refine die geometries to combat plate-out and ensure embossing fidelity at high line speeds. Patents cluster around cap-stock UV packages, hollow-core profile geometries, and adhesive-free click-systems.

Competitive emphasis shifts toward validated traceability. Companies deploy blockchain-enabled platforms that furnish geolocation data and lab testing certificates to satisfy EUDR auditors. Those lacking verification capabilities risk exclusion from municipal contracts. Fire-performance remains another moat; proprietary formulations that achieve C-s3, d0 without halogens unlock high-rise façade jobsites. Overall, strategic moves in M&A, recycling, and compliance are intensifying market concentration, yet more than 200 active extruders keep the Europe Wood Plastic Composite market moderately fragmented.

Europe Wood-plastic Composite (WPC) Industry Leaders

NOVO-TECH GmbH & Co. KG

Silvadec

UPM

Fiberdeck

Deceuninck

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Deceuninck invested EUR 45 million to upgrade recycling infrastructure in Belgium and France. This investment strengthened Wood Plastic Composite production capabilities by improving material recycling efficiency and product quality.

- June 2025: The European Commission announced provisional duties of up to 62.4% on Chinese hardwood plywood imports following its anti-dumping investigation on hardwood-faced plywood. The increased duties have compelled European WPC manufacturers to seek alternative suppliers and explore domestic sourcing options, while adjusting their production processes to maintain competitive pricing despite higher raw material costs and supply chain modifications.

Europe Wood-plastic Composite (WPC) Market Report Scope

Wood-plastic composite (WPC) is a composite material made of wood fibers, such as sawdust, pulp, peanut hulls, bamboo, and plastic materials, including polypropylene (PP) and polyethylene (PE). The WPC granulates can be further processed through extrusion, injection molding, blow molding, compression molding, and other methods to produce different products for various end-user industries, including construction and automotive. The European wood plastic composite (WPC) market is segmented by application and geography. By application, the market is segmented into decking, auto-interior parts, siding and fencing, technical applications, furniture, and consumer goods. The report also covers the market size and forecasts for the wood-plastic composite market in 8 countries across Europe. For each segment, the market sizing and forecasts have been done based on volume (kilo tons).

By Polymer Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyvinyl Chloride (PVC) |

| Other Polymer Types |

By Application

| Decking |

| Auto-interior Components |

| Siding and Fencing |

| Technical Applications |

| Furniture |

| Consumer Goods |

By Geography

| Germany |

| United Kingdom |

| France |

| Belgium |

| Italy |

| Spain |

| Finland |

| Norway |

| Denmark |

| Sweden |

| Rest of Europe |

| By Polymer Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyvinyl Chloride (PVC) | |

| Other Polymer Types | |

| By Application | Decking |

| Auto-interior Components | |

| Siding and Fencing | |

| Technical Applications | |

| Furniture | |

| Consumer Goods | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Belgium | |

| Italy | |

| Spain | |

| Finland | |

| Norway | |

| Denmark | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected volume for Europe’s WPC demand in 2031?

The market is forecast to reach 989.99 kilo tons by 2031, reflecting a 7.05% CAGR from 2026.

Which polymer dominates European WPC formulations?

Polyethylene currently leads with 52.06% share, though polypropylene is growing faster due to higher heat-resistance needs.

Which end use is expanding the quickest?

Siding and fencing applications are advancing at a 8.79% CAGR as builders look for low-maintenance exterior cladding.

Why is Germany the largest national market?

Germany combines advanced extrusion infrastructure with strong automotive and construction activity, yielding 38.31% share in 2025.

Page last updated on: