Window Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

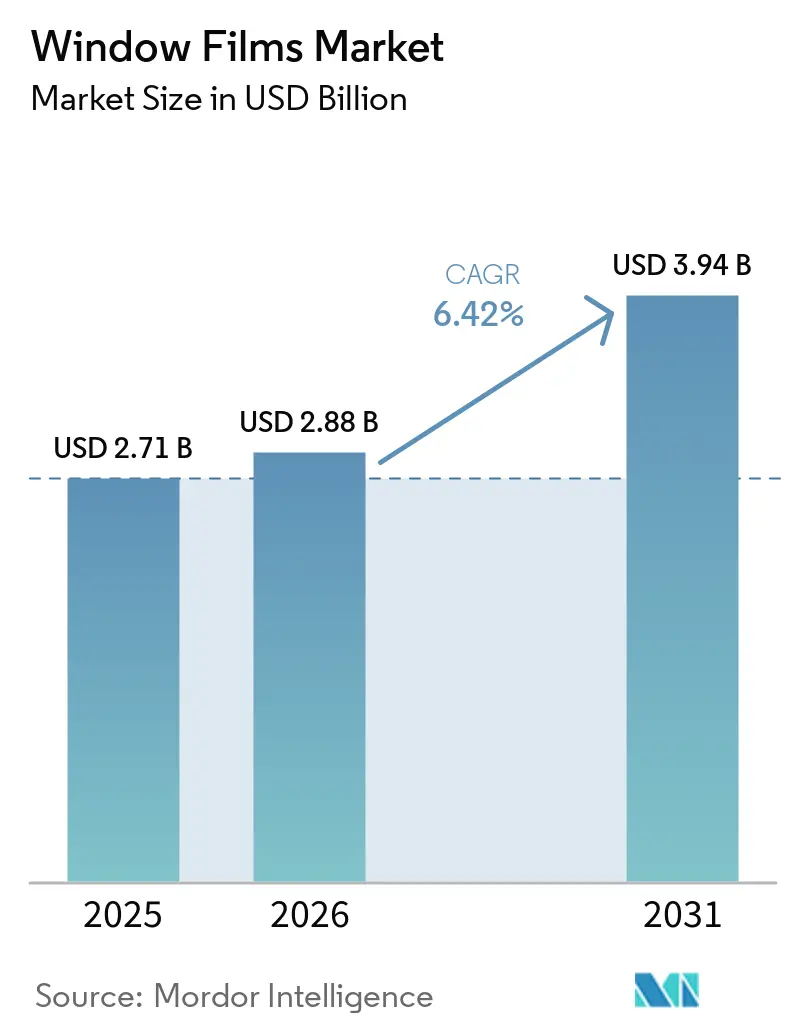

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Window Films Market Analysis by Mordor Intelligence

The Window Films Market size is expected to increase from USD 2.71 billion in 2025 to USD 2.88 billion in 2026 and reach USD 3.94 billion by 2031, growing at a CAGR of 6.42% over 2026-2031. Policy pressures aimed at reducing emissions in the building sector are shifting films from optional upgrades to essential compliance assets. This is particularly evident in regions where local codes mandate lower solar-heat-gain coefficients or enhanced insulation. In temperate zones, there is a noticeable shift in demand: owners are increasingly opting for insulating and low-E variants, not just for summer cooling, but also for winter energy savings. The automotive sector is gaining momentum, bolstered by uniform tint regulations. These regulations allow dealers to package ceramic films with new vehicle deliveries, all while maintaining manufacturer warranties. The Asia-Pacific region remains the dominant player, driven by China's stringent building-energy regulations and India's revised ECBC timelines. Yet, with market reforms in the Gulf Cooperation Council, growth in the Middle-East is rapidly catching up.

Key Report Takeaways

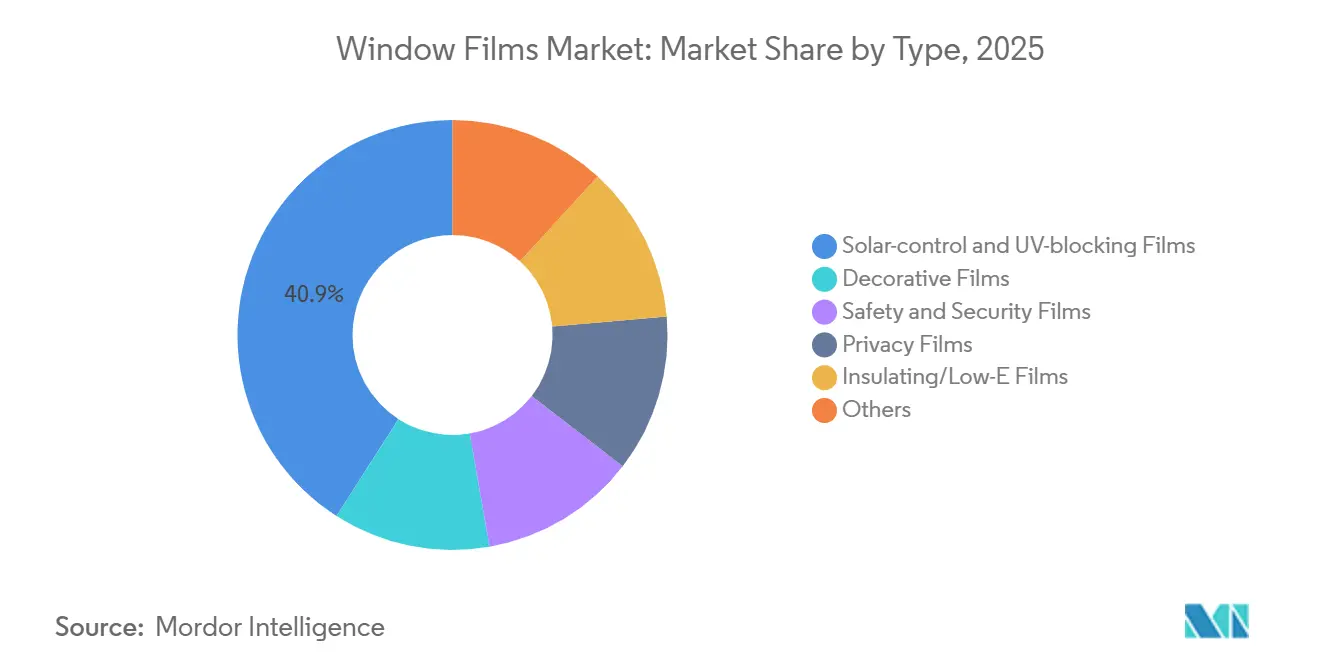

- By type, solar-control and UV-blocking films led with 40.93% revenue share of the window films market in 2025; insulating/low-E films are projected to expand at a 7.30% CAGR from 2026 to 2031.

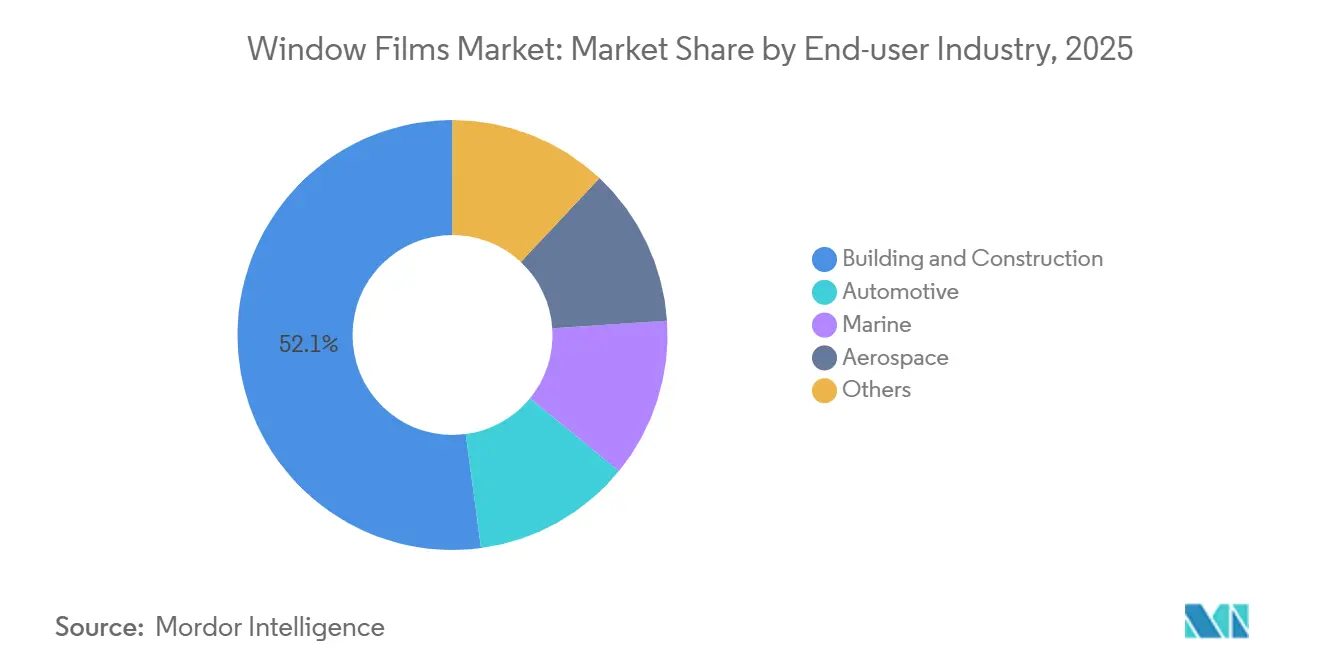

- By end-user industry, building and construction commanded 52.12% share of the window films market size in 2025; automotive applications register the highest forecast CAGR at 7.12% during 2026-2031.

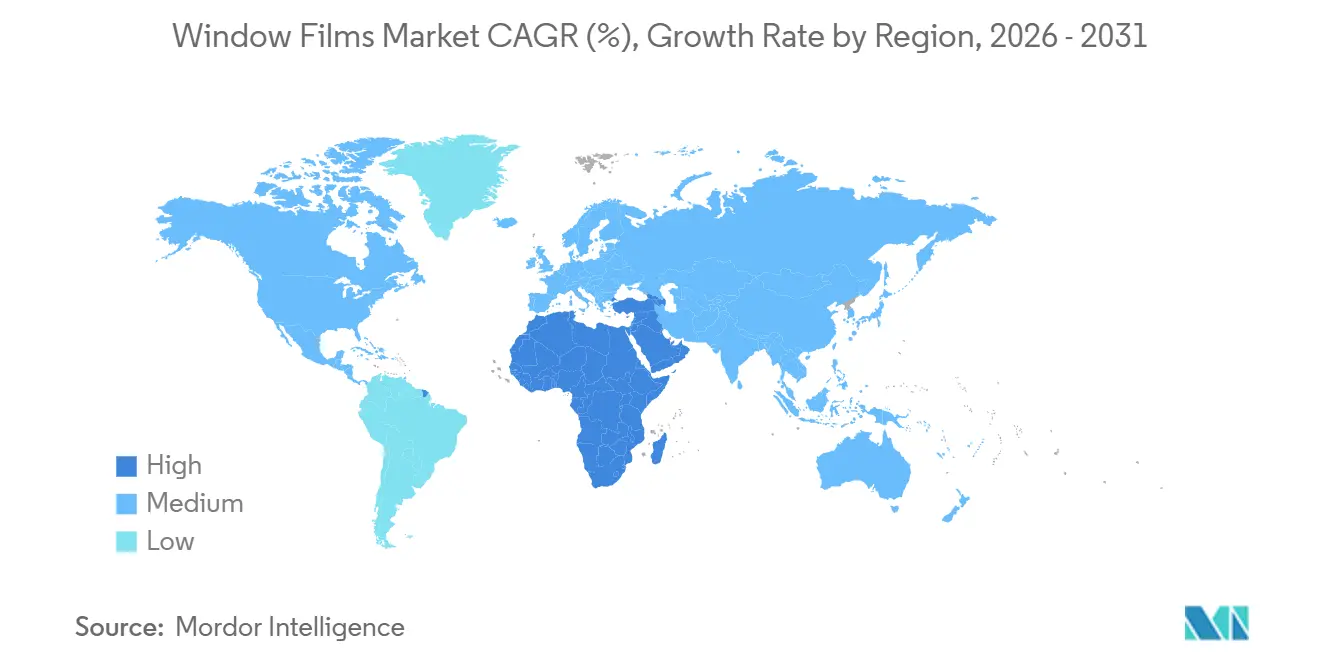

- By geography, Asia-Pacific captured 46.12% of the window films market share in 2025, while Middle-East and Africa are advancing at a 6.88% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Window Films Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Net-zero mandates spurring solar-control film retrofits | +1.8% | North America, EU, APAC (China, Japan, South Korea) | Medium term (2-4 years) |

| Accelerated glazing replacement in automotive aftermarket | +1.5% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Insurance rebates for hurricane-resistant films | +0.7% | North America (Florida, Texas, Gulf Coast states) | Short term (≤ 2 years) |

| IoT-ready films enabling HVAC load-balancing | +1.2% | Global, early adoption in smart-city projects (Singapore, UAE, select U.S. metros) | Long term (≥ 4 years) |

| 5G-friendly nano-ceramic multilayer films unlocking new building codes | +0.9% | Global, regulatory leads in North America, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Net-Zero Mandates Spurring Solar-Control Film Retrofits

Building-energy codes are now standardizing spectral-selective performance as a compliance measure. California’s Title 24 Part 6 requires nonresidential glazing on west façades to maintain a solar heat gain below 0.40[1]California Energy Commission, “Title 24 Building Standards,” Energy.ca.gov. Single-pane windows can only meet this standard with the addition of aftermarket films. Similarly, Toronto’s Green Standard and Germany’s GEG update have adopted this trend, mandating retrofit spending as a capital expense. This shift is providing a buffer for the Window Films market against broader economic fluctuations during the forecast period of 2026–2031. Property owners are increasingly opting for window films to avoid citations, as these films can be installed from the interior without displacing tenants. Energy-modeling firms highlight that a large office in Chicago can achieve a significant reduction in HVAC loads with high-performance films, allowing property owners to recover the investment within a short period. As more regions emphasize embodied-carbon scoring, window films are becoming even more appealing, as they introduce minimal structural weight compared to a complete glazing replacement.

Accelerated Glazing Replacement in Automotive Aftermarket

From 2023 to 2025, 15 U.S. states standardized statutes for visible-light transmission, resolving the inconsistent regulations that had previously hindered multi-state dealer programs. By 2025, ceramic-particle films emerged as the leading choice in the U.S. aftermarket. Customers prioritized the benefits of reduced cabin heat and enhanced signal reception over traditional metallized tints. This shift is particularly significant for electric vehicle owners, as cooler cabin temperatures contribute to an extended driving range. Additionally, fleet operators have begun entering into multi-year blanket purchase agreements, aligning tint installations with their preventive maintenance schedules. This approach not only increases revenue predictability for regional installers but also expands the Window Films market, transitioning it from retail transactions to a more integrated service offering.

Insurance Rebates for Hurricane-Resistant Films

Property insurers are now offering premium discounts for impact-mitigating laminates. In Florida, Citizens Property Insurance grants annual savings to buildings that meet the ASTM D3363 3H hardness standard. Similarly, the Texas FAIR Plan rolled out these incentives in 2025. As commercial owners face double-digit premium inflation, many are now viewing their investments in 7-mil security films as a strategic risk-transfer move rather than merely energy projects. Consequently, larger glazing contractors are training their teams for retrofit film installations, aiming for insurer verification, and driving increased volume in the Window Films market.

IoT-Ready Films Enabling HVAC Load Balancing

Smart-building pilots are showcasing notable operational savings. In Singapore, a trial spanning several towers reduced peak cooling demand by integrating IoT-ready films with building management systems. In Dubai, a large office avoided annual demand charges by employing dynamic tinting during specific hours. Manufacturers are now embedding NFC tags in every pane during commissioning, significantly reducing setup time. In the future, grid operators could leverage these film-enabled load reductions for demand-response markets, potentially creating new revenue streams for facilities that can validate performance data.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from electro-chromic smart glass | -1.1% | Global, concentrated in premium commercial real estate (North America, EU, select APAC cities) | Medium term (2-4 years) |

| Skilled-installer shortage causing project delays | -0.8% | North America, EU, with emerging pressure in APAC urban centers | Short term (≤ 2 years) |

| Tightening PVC-disposal rules squeezing low-cost vinyl films | -0.6% | EU, with regulatory spillover into APAC markets (Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Electro-Chromic Smart Glass

Electro-chromic glazing has secured a significant share of the high-end retrofit market, a space previously dominated by films. This shift is supported by a robust installation pipeline expected to be completed by 2024. Over time, unit costs have reduced the price gap. Building owners are evaluating the long-term controllability of electro-chromic glazing against the quick payback of films, with many opting for hybrid façades. These façades incorporate dynamic glass on prominent elevations and standard film on the remaining areas. In response, film suppliers are bundling daylight sensors and Bluetooth modules to replicate the functionality of active control.

Skilled-Installer Shortage Causing Project Delays

In 2024, a decline in the U.S. construction workforce has left developers struggling to secure certified film crews[2]U.S. Bureau of Labor Statistics, “Employment Situation,” BLS.gov. Since a misaligned edge can void warranties, major projects have adjusted their budgets, allocating several weeks for installations that previously required less time. This issue is not limited to the United States; In 2025, Germany also experienced a shortage of skilled workers, particularly in glazing roles. Although manufacturers have established training academies, only a few states in the United States require licensure, resulting in inconsistent quality standards. This labor shortage is constraining the Window Films Market, as property owners are postponing projects until labor firms stabilize. Apprenticeship programs linked to community colleges show potential for addressing this shortage by the forecast period of 2026–2031, but immediate challenges persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Insulating Films Propel Efficiency Over Aesthetics

Forecasts predict that insulating and low-E variants will grow at a 7.30% CAGR during the forecast period of 2026–2031, outpacing all other categories. Owners are realizing that the savings from winter heating can rival those from summer cooling. While solar-control and UV-blocking products accounted for 40.93% of the revenue in the base year 2025, their dominance is diminishing. This change is primarily driven by municipalities in temperate climates providing subsidies for R-value enhancements. The market for insulating window films is poised for significant growth, supported by municipal trials that have demonstrated notable reductions in heating costs. As open-plan offices prioritize privacy without structural partitions, decorative films are experiencing steady single-digit growth.

Safety and security films remain crucial in regions governed by blast-mitigation codes, creating a lucrative niche that is insulated from price competition. In the healthcare sector, privacy films are gaining traction, driven by the demand for one-way-vision glazing to comply with HIPAA regulations. The "Others" category, which includes anti-graffiti and EMI-shielding films, remains relatively small. However, it has attracted attention from defense contracts, particularly for RF-transparent and low-signature applications. With ISO 12543 emphasizing peel strength, manufacturers are re-evaluating adhesives under cyclic humidity. This not only increases research and development expenses but also enhances performance differentiation in the Window Films market.

By End-User Industry: Automotive Momentum Challenges Construction Dominance

In 2025, the building and construction sector led the Window Films market with a 52.12% share, driven by retrofit cycles aligning with energy-code upgrades. However, the automotive sector is rapidly gaining ground, boasting a projected 7.12% CAGR growth rate for the forecast period 2026–2031. This momentum is largely due to dealerships increasingly offering ceramic film packages with vehicle sales. The automotive segment's growth trajectory is further fueled by the rise of electric vehicles and uniform tint regulations. On a smaller scale, marine retrofits are expanding as yacht builders comply with IMO's UV-exposure standards.

Although aerospace adoption grapples with FAA certification delays, a 2025 memorandum on “minor alterations” hints at a brighter future. By reducing compliance costs, it paves the way for growth in regional-jet fleets. The “Others” segment includes retail storefronts, where luxury car makers are experimenting with factory-installed films to set apart trim levels. While varying standards - ANSI/SAE Z26.1 for vehicles and NFRC 200 for architecture - pose challenges for cross-channel integration, they also ensure premium pricing for specialized formulations, enhancing margins throughout the Window Films industry.

Geography Analysis

In 2025, the Asia-Pacific region, spurred by China's GB 50189 standard and India's ECBC update, accounted for 46.12% of the revenue, with both megacities and Tier 2 urban areas increasingly adopting films. Japan and South Korea introduced new policies, setting thermal-transmittance ceilings below 1.9 W/m²·K for retrofits, effectively mandating either triple glazing or high-performance films. The ASEAN region showcases a fragmented landscape: Singapore's Green Mark incentivizes sub-0.30 SHGC films with rebate points, while Malaysia's approach treats films as optional credits, leading to varied adoption rates.

Spanning the Middle-East and Africa, the region is witnessing the fastest growth at a 6.88% CAGR, projected for the forecast period of 2026–2031. The UAE's Estidama update mandates significant reductions in cooling loads from the baseline. With Saudi Arabia's Vision 2030 construction surge, there is a pronounced shift towards spectrally selective films, especially in thousands of hotel rooms aiming for SBC 601 compliance. In South Africa, a notable spike in electricity tariffs has shortened payback periods, prompting office parks in Johannesburg to retrofit their west façades. However, both Nigeria and Egypt grapple with price sensitivity, as import duties inflate landed costs significantly.

North America and Europe together constituted a significant portion of the 2025 demand, with a growing reliance on retrofitting. Revisions to California's Title 24 and Toronto's Green Standard ensure a steady demand by pushing existing stocks towards enhanced efficiency. Meanwhile, the EU's Energy Performance of Buildings Directive mandates a consistent annual renovation rate, often leaning towards films over complete replacements due to their reduced embodied carbon footprint. In South America, buoyed by a construction rebound in Brazil and GDP growth, commercial permits have seen an uptick. However, challenges such as currency fluctuations and delays in import licenses hinder film availability in secondary cities.

Competitive Landscape

The window films market is moderately consolidated. Regional specialists are enhancing their market presence by bundling installation services with compliance guidance. In a proactive response, multinational companies are rolling out turnkey training academies, aiming to upskill installers, address the labor gap, and uphold their premium pricing. While IoT-enabled films currently constitute a minor segment of unit volume - largely due to the lack of standardized data schemas in building-automation protocols - successful pilot projects hint at a promising shift ahead. Despite raw-material inflation being kept in check by stabilized polyester feedstock prices, companies are grappling with rising costs for vinyl-backed films. This uptick is largely due to adhesive reformulations necessitated by EU VOC regulations. Strategically, many companies are pivoting toward thermoplastic-polyurethane bases, even at a premium. As electro-chromic smart glass steadily carves out a niche in the high-end market, film manufacturers are pushing boundaries with innovations like aerogel inserts and phase-change microcapsules. These enhancements aim to boost R-values without adding thickness. Yet, with unit costs remaining elevated, achieving widespread commercial adoption poses a significant hurdle.

Window Films Industry Leaders

Eastman Chemical Company

3M

Saint-Gobain

Avery Dennison Corporation

Garware Hi-Tech Films

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Automotive care company Garware Hi-Tech Films (GHFL) expanded its product portfolio with the introduction of four new offerings. Within its window film segment, the company categorized its products into three tiers: Premium (Gold range), Medium (Silver range), and Economy (Bronze range).

- July 2025: Lintec launched the BR-50UH RECYCLE 100, a solar-control window film made entirely from recycled PET resin, reducing CO2 emissions by 17.5% compared to non-recycled alternatives. The product enhances Lintec's eco-friendly range while maintaining transparency and shatterproof properties.

Global Window Films Market Report Scope

Window films are a glass treatment put on windows and other glass surfaces to reduce the amount of solar heat transmitted through the glass. By minimizing heat, window film can reduce HVAC costs and increase comfort in cars, homes, offices, etc.

The window films market is segmented by type, end-user industry, and geography. By type, the market is segmented into solar-control and UV-blocking films, decorative films, safety and security films, privacy films, insulating/low-E films, and others. By end-user industry, the market is segmented into automotive, building and construction, marine, aerospace, and others. The report also covers the market size and forecasts for the market in 22 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Solar-control and UV-blocking Films |

| Decorative Films |

| Safety and Security Films |

| Privacy Films |

| Insulating/Low-E Films |

| Others |

| Automotive |

| Building and Construction |

| Marine |

| Aerospace |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Type | Solar-control and UV-blocking Films | |

| Decorative Films | ||

| Safety and Security Films | ||

| Privacy Films | ||

| Insulating/Low-E Films | ||

| Others | ||

| By End-user Industry | Automotive | |

| Building and Construction | ||

| Marine | ||

| Aerospace | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Window Films market in 2026?

The Window Films market size stands at USD 2.88 billion in 2026, on track to reach USD 3.94 billion by 2031, registering a 6.42% in the period.

Which product type is expanding fastest?

Insulating and low-E films are growing at a 7.30% CAGR (2026-2031) as owners target year-round energy savings.

Why is automotive demand rising so quickly?

Harmonized tint statutes and electric-vehicle growth let dealers bundle premium ceramic films at the point of sale, driving a 7.12% CAGR (2026-2031) in automotive applications.

Which region offers the highest growth potential?

The Middle-East and Africa lead with a projected 6.88% CAGR (2026-2031) because new codes mandate significant solar-gain reductions in commercial buildings.

How are insurers influencing adoption?

Gulf-state and U.S. insurers now offer premium discounts for ASTM-compliant security films, turning safety features into an immediate cost-saving lever.

What is the main competitive threat to traditional films?

Falling prices for electro-chromic smart glass are capturing premium retrofit projects, pressuring film makers to add IoT functionality and multifunctional coatings.

Page last updated on: