Glass Tiles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

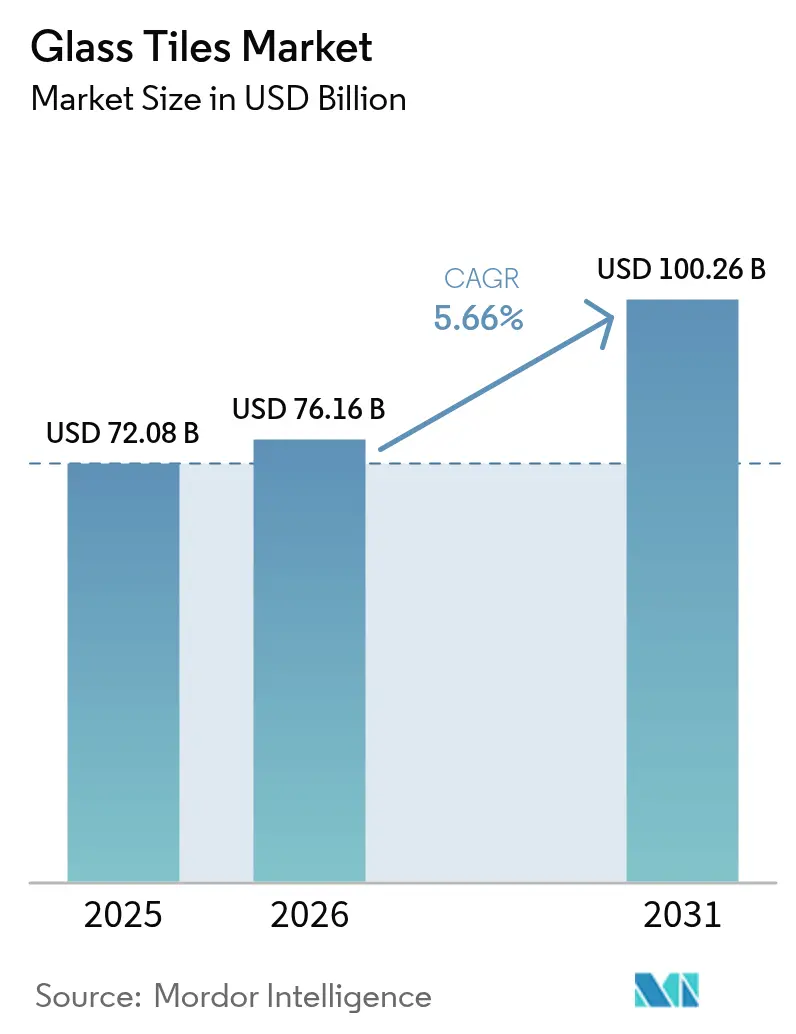

| Market Size (2026) | USD 76.16 Billion |

| Market Size (2031) | USD 100.26 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Tiles Market Analysis by Mordor Intelligence

The glass tiles market size was valued at USD 72.08 billion in 2025 and estimated to grow from USD 76.16 billion in 2026 to reach USD 100.26 billion by 2031, at a CAGR of 5.66% during the forecast period (2026-2031). Rising urbanization, premium renovation spending, and stricter green-building codes favor lightweight, low-carbon cladding materials, positioning the glass tiles market as a preferred solution in residential, commercial, and infrastructure projects. Sintered technology gains momentum because it trims firing temperatures and cuts energy use, while design trends toward matte finishes widen aesthetic options for architects. Asia-Pacific leads both production and consumption thanks to large-scale infrastructure programs, integrated supply chains, and growing disposable incomes.

Key Report Takeaways

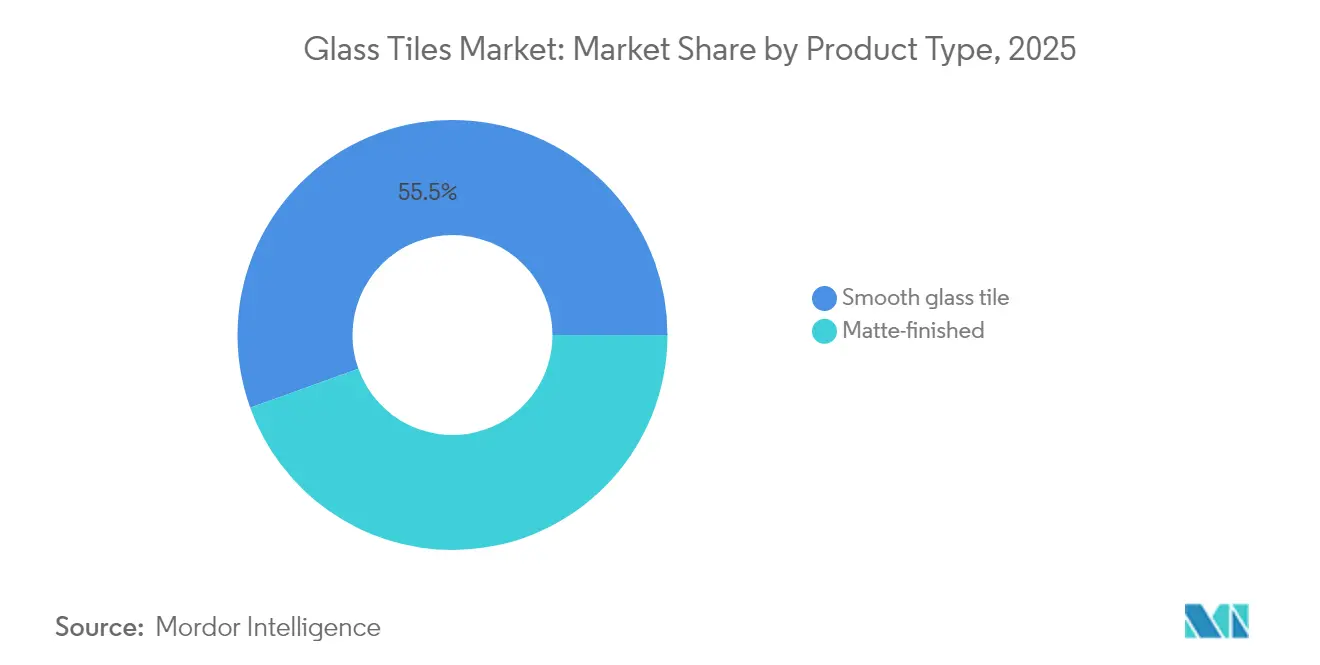

- By product type, smooth/glossy finishes accounted for 55.49% share of the glass tiles market size in 2025; matte finishes are projected to expand at 6.88% CAGR between 2026-2031.

- By manufacturing process, fused tiles led with 37.58% of the glass tiles market share in 2025, while sintered tiles are forecast to grow at a 6.97% CAGR through 2031.

- By application, wall cladding commanded 40.12% share of the glass tiles market size in 2025, while outdoor and landscape installations are set to rise at 6.55% CAGR through 2031.

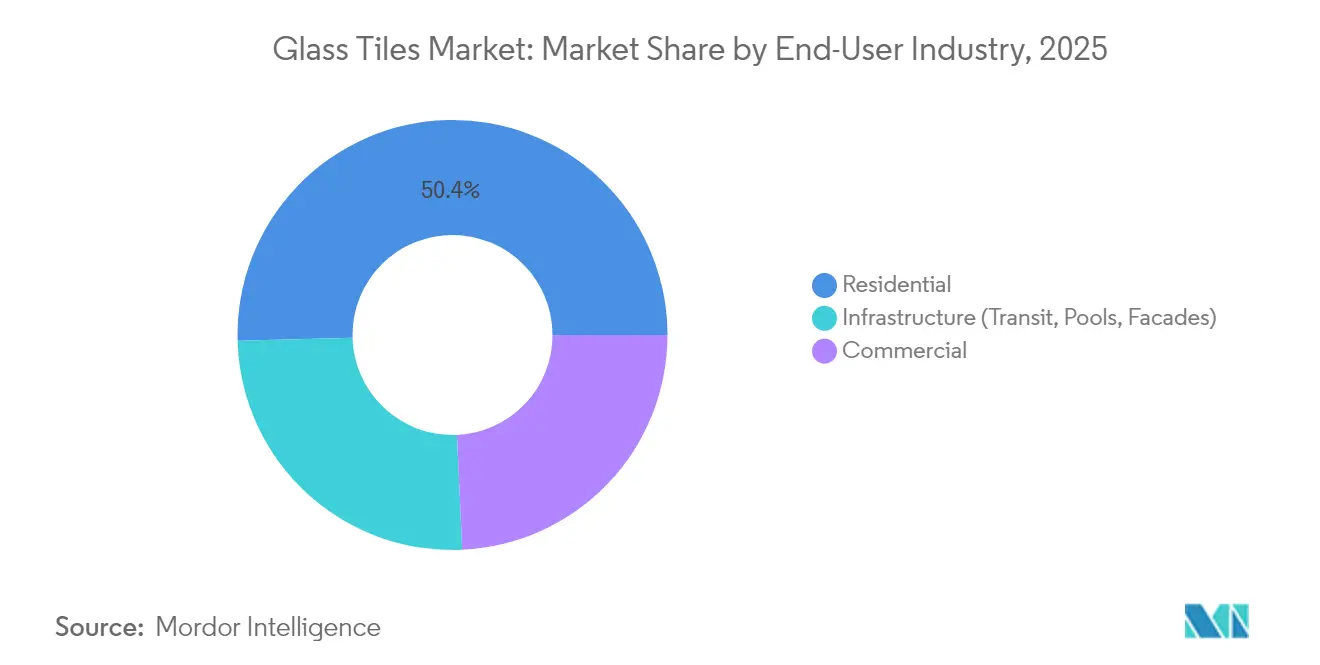

- By end-user industry, the residential segment held 50.43% revenue share in 2025, whereas infrastructure applications are advancing at a 6.74% CAGR to 2031.

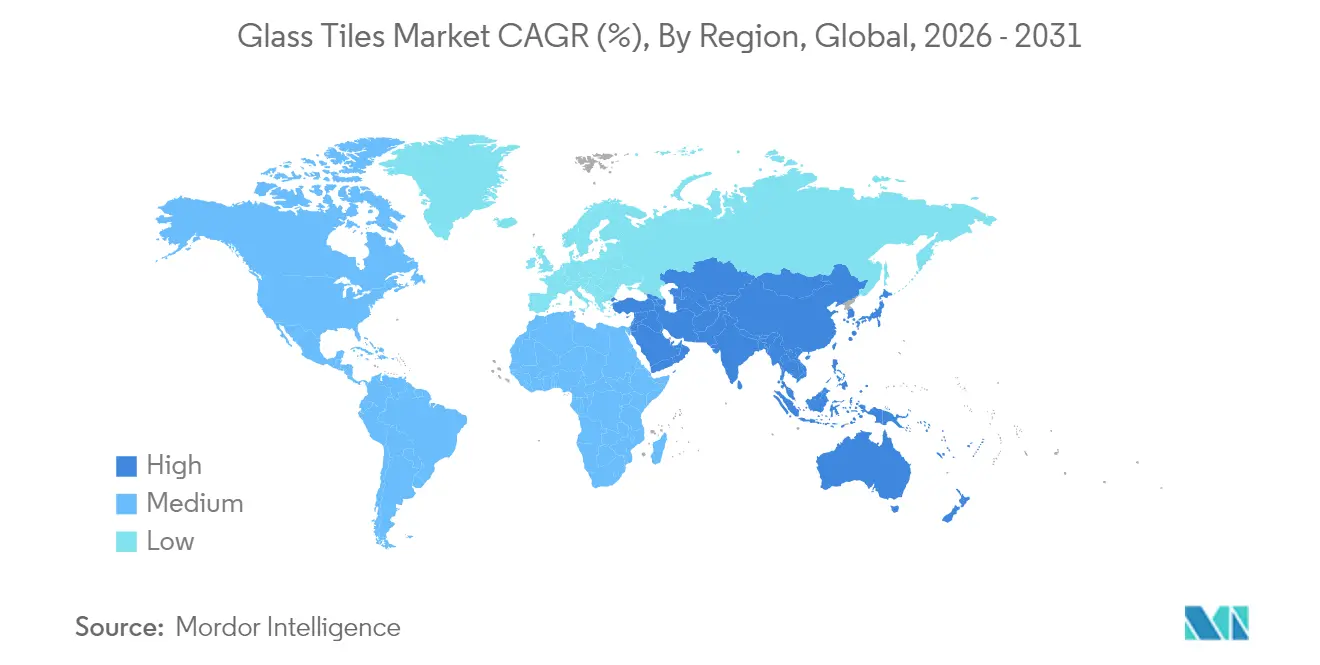

- By geography, Asia-Pacific dominated with 51.84% of the glass tiles market share in 2025 and is growing at a 6.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glass Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand in residential construction | +1.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Eco-friendly manufacturing processes | +1.2% | Europe and North America leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growing usage in luxury and high-end architectural projects | +1.0% | North America, Europe, and select Asia-Pacific markets | Medium term (2-4 years) |

| Increasing demand for lightweight glass tiles for high-rise retrofits | +0.8% | Global urban centers, particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Growing popularity in renovation and DIY market | +0.7% | North America and Europe, with emerging growth in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand in Residential Construction

Renovation activity fuels premium material uptake as homeowners target kitchens and bathrooms where durability and aesthetics justify higher budgets. Canada’s building construction investment reached CAD 22.2 billion in March 2025, and year-over-year growth of 5.4% underscores resilient housing demand [1]Statistics Canada, “Building Construction Investment, March 2025,” www150.statcan.gc.ca. The residential share of 51.04% reflects this preference for higher-value finishes over commodity ceramic alternatives. Glass tiles’ stain resistance and color permanence add long-term value in moisture-prone rooms, aligning with buyer expectations for low lifecycle costs. Consequently, the glass tiles market benefits from steady replacement cycles in mature housing stock and upscale condominium projects in Asia-Pacific and North America.

Eco-Friendly Manufacturing Processes

Regulators and building-rating schemes favor low-carbon materials, prompting manufacturers to increase cullet content and switch to renewable power. AGC Glass Europe recycled 700,000 tonnes of cullet in 2024 and targets a 50% cullet ratio by 2030, cutting 490,000 tonnes of CO₂ emissions. NSG Group plans to reach 50% renewable electricity in 2024 and achieve carbon neutrality by 2050, supported by new green-hydrogen furnaces in the United Kingdom[2]NSG Group, “2024 Integrated Report,” nsg.com. These initiatives create brand differentiation and meet specification criteria in Europe and North America, where architects select products that contribute to LEED and BREEAM credits. Sintered processes that lower kiln temperatures amplify these environmental gains, steering procurement toward suppliers with verifiable decarbonization roadmaps.

Growing Usage in Luxury and High-End Architectural Projects

Designers specify glass tiles for their depth, translucence, and light-reflecting qualities that ceramic rivals cannot replicate. Guardian Glass developed ClimaGuard and SunGuard coatings to enhance solar control without sacrificing clarity, demonstrating how performance upgrades support contemporary facades. Luxury resorts in Southeast Asia adopt matte-etched glass mosaics for spa interiors to convey bespoke aesthetics, while premium office towers in North America incorporate back-lit glass walls for visual impact. Rising disposable incomes in China and India boost upscale residential demand, further bolstering the glass tiles market. The synergy of aesthetics and energy performance secures a premium price point, protecting margins against cheaper substitutes.

Increasing Demand for Lightweight Glass Tiles for High-Rise Retrofits

Urban densification drives retrofits of aging high-rise stock, where structural load limits dictate material choice. Research on foamed glass aggregates containing 90% recycled waste shows potential to lighten structural concrete while maintaining strength. Lightweight glass tiles reduce dead load on curtain walls and simplify seismic anchoring in earthquake-prone regions. Municipal incentive programs that subsidize energy-efficient facade upgrades in Tokyo, New York, and Shanghai further enhance adoption. Short installation cycles appeal to property owners seeking minimal tenant disruption, accelerating specification of sintered thin-panel formats. Consequently, the glass tiles market secures share in retrofit budgets previously dominated by aluminum composite and stone slabs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material & energy cost volatility | -1.5% | Global, with acute impact in energy-intensive manufacturing regions | Short term (≤ 2 years) |

| Cheaper ceramic & porcelain substitutes | -0.9% | Price-sensitive markets globally, particularly emerging economies | Medium term (2-4 years) |

| Micro-cracking risk in seismic zones | -0.6% | Seismic-prone regions including California, Japan, Chile, and Turkey | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material & Energy Cost Volatility

Glass production is energy-intensive, making manufacturers vulnerable to fuel spikes and electricity shortages. Engineering News-Record reported a 3% increase in its Materials Cost Index by end-2024, with glass prices expected to climb 6-11% in 2025 due to tariffs and energy levies. Steel price inflation of 11.2% compounded furnace maintenance costs, squeezing margins. Spot natural-gas rates in Europe surged during 2024, temporarily forcing capacity curtailments and elongating lead times. Such volatility prompts developers to switch to ceramic tiles when budgets tighten, especially in emerging markets lacking green-building incentives. Hedging strategies and on-site renewable power become critical for glass tile producers to stabilize operating expenses.

Cheaper Ceramic & Porcelain Substitutes

Ceramic producers leverage scale and low-cost clay inputs to challenge the glass tiles market in mass segments. The United States consumed 264.5 million m² of ceramic tiles in 2023, with average factory prices of USD 19.06 per m², far below glass equivalents. Distributor consolidation, illustrated by Louisville Tile’s acquisition of American Olean Midwest, enhances purchasing power and marketing reach. Wider retail networks improve ceramic availability and shorten delivery times. In price-sensitive housing projects across Latin America and Southeast Asia, contractors often downgrade from glass to ceramic backsplashes to protect profit margins, limiting glass penetration outside premium tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Matte Finishes Gain Premium Positioning

Smooth/glossy products held 55.49% share in 2025, yet matte finishes expand fastest at 6.88% CAGR. Designers appreciate low-glare surfaces that provide subtle depth and modern aesthetics. Anti-fingerprint treatments now preserve matte purity in high-traffic hotel lobbies, widening use cases beyond bathrooms. Advances in nano-etching allow manufacturers to retain the easy-clean surface of glossy glass while delivering a satin appearance. Matte variants often command price premiums of 10-15%, encouraging producers to allocate incremental capacity to these SKUs. Hybrid digital-print systems apply metallic accents onto matte backgrounds, satisfying luxury commercial interiors. The glass tiles market size for matte finishes is projected to exceed USD 44.62 billion by 2031, underpinned by upscale condominium demand in Asia-Pacific.

Smooth tiles remain essential in clinical settings, foodservice areas, and swimming pools because their impervious glaze simplifies sanitation. Public health codes in the United States mandate non-porous wall surfaces behind commercial kitchen prep lines, securing baseline demand for glossy glass. Producers bundle anti-microbial silver ions into clear glazes, differentiating from ceramic rivals. Although matte popularity rises, balanced production portfolios help mitigate style swings. Integrated facilities dedicate sequential furnace zones to alternate between gloss and matte runs without stopping the line, maintaining throughput. Overall, product-type diversification anchors the glass tiles market against fashion-cycle volatility while giving distributors a broader palette.

By Manufacturing Process: Sintered Technology Drives Innovation

Sintered products register the highest 6.97% CAGR through 2031 while fused tiles retain 37.58% share in 2025. The glass tiles market rewards sintering because the process fires at lower temperatures, cutting gas consumption and CO₂ emissions. Manufacturers embed recycled cullet into sintered blends without compromising strength, aligning with LEED scoring. Fused formats still dominate large-run production due to mature kiln infrastructure, but rising carbon taxes elevate operating costs. Cast and smalti tiles serve artisanal mosaics and heritage restorations where hand-crafted textures justify premium pricing. Research at the Saitama Institute of Technology shows low-temperature recycling routes that could transfer to glass tile furnaces and further reduce energy bills. As architects demand environmental product declarations, sintered suppliers gain preferred-vendor status in publicly funded projects. The glass tiles industry thus pivots capital expenditure toward continuous sinter lines equipped with waste-heat recovery, reinforcing the shift away from traditional fusion.

Lower thermal budgets extend kiln life, freeing maintenance outlays for surface-coating R&D. Automated pressing and calendaring equipment boosts dimensional accuracy, easing site installation and trimming labor spend for contractors. The glass tiles market sees sintered planks entering ventilated facade systems where lighter weight and tight tolerances are critical. Producers co-fire iridescent glazes in a single pass, reducing cycle time compared with separate fusing stages. Lifecycle analyses demonstrate up to 25% embodied-carbon savings relative to fused equivalents, supporting procurement under green-public-procurement rules in Europe. Consequently, sintered technology is forecast to narrow the glass tiles market share gap with fused formats before 2030.

By Application: Outdoor Installations Drive Premium Growth

Wall cladding dominated at 40.12% share in 2025, yet outdoor and landscape installations rise fastest at 6.55% CAGR. UV-stable glazes and frost-resistant bodies now permit glass mosaics in exterior pools, plazas, and terrace planters. Luxury resorts commission iridescent lagoon pools that leverage sunlight refraction for dramatic visuals. Glass pavers with anti-slip texture replace stone on rooftop walkways where weight limits favor thin profiles. Landscape architects specify recycled-glass aggregates in permeable pathways, tying hardscape design to circular-economy goals. As a result, the glass tiles market harvests premium margins in boutique outdoor projects.

Interior flooring, backsplash, and countertop applications remain stable niches. Slip-rated glass floor tiles line spa shower areas where hygiene and aesthetics converge. Commercial kitchens adopt heat-resistant glass countertops that withstand thermal shock better than engineered stone. Backsplashes in quick-service restaurants favor glossy glass for ease of wipe-down during service peaks. Despite these steady volumes, growth concentrates on exterior segments that exploit glass’s resilience to weather cycles and algae staining. Manufacturers supplying pre-mounted mesh sheets streamline installation, reducing field labor and reinforcing the cost case versus porcelain alternatives.

By End-User Industry: Infrastructure Modernization Accelerates Growth

The residential category accounted for 50.43% of revenue in 2025 because households prioritize premium kitchen backsplashes and bathroom mosaics. However, infrastructure projects such as metro stations, airports, and civic centers offer the fastest 6.74% CAGR. Governments in China and India budget record sums for transit corridors that specify vandal-resistant, low-maintenance finishes, fueling bulk orders of textured glass panels. Glass tiles meet stringent fire-safety and smoke-toxicity requirements, securing approval in mass-transit design codes. Commercial refurbishments also gain traction as landlords upgrade lobbies with luminous glass feature walls to attract tenants.

Infrastructure growth benefits suppliers with seismic-certified anchoring systems. ASCE guidelines for non-structural glazing in seismic Zone 4 demand flexible, high-displacement mounting hardware. Manufacturers offering pre-tested assemblies reduce engineering costs for design firms. The glass tiles market size serving public works is expected to surpass USD 25.35 billion by 2031, providing a defensive revenue stream amid cyclical housing swings. Residential demand still underpins volume, but infrastructure and commercial verticals diversify risk, ensuring balanced industry expansion.

Geography Analysis

Asia-Pacific held 51.84% share of the glass tiles market in 2025 and continues to grow at a 6.61% CAGR through 2031. China’s metro-station construction pipeline, India’s Smart Cities Mission, and Japan’s hotel boom ahead of global events sustain robust regional purchasing. Integrated supply chains in Guangdong and Shandong provinces let producers source float glass, colorants, and packaging locally, cutting logistics costs and enabling aggressive export pricing. Governments promote recycled-content mandates, giving sintered producers a domestic advantage and bolstering regional leadership. Rapid urban household formation also supports steady residential renovation demand, making Asia-Pacific the strategic priority for multinational tile brands.

North America represents a mature yet resilient market. United States renovation outlays stay strong as aging housing stock needs updates, while Canada’s CAD 22.2 billion construction investment in March 2025 signals healthy activity. High rise retrofits in New York, Chicago, and Toronto prefer lightweight glass panels to minimize structural reinforcement costs. Mexico’s commercial real-estate growth underpins demand for back-painted glass murals in shopping centers. Stringent energy-codes catalyze adoption of low-emissivity coated glass cladding, offering a functional edge over ceramic alternatives. Consequently, the glass tiles market maintains premium positioning despite economic headwinds.

Europe commands significant share, anchored by strict decarbonization policies that align with cullet-rich, low-carbon glass. AGC’s target of 50% cullet usage by 2030, together with hybrid-furnace pilots cutting emissions 75%, meets EU taxonomy requirements. Public authorities in Germany and France tender transit-hub refurbishments demanding environmental product declarations, accelerating procurement from certified suppliers. United Kingdom and Italy focus on heritage building upgrades, where glass mosaics complement restoration aesthetics without compromising authenticity. Although growth lags Asia-Pacific, stable public-sector spending and regulatory certainty underpin Europe’s contribution to global revenue.

South America and Middle East and Africa offer early-stage potential. Brazil’s hotel and resort construction along coastal corridors spurs niche demand for iridescent pool mosaics. Saudi Arabia’s giga-projects specify large-format back-lit glass walls in retail districts, yet supply-chain gaps and price sensitivity limit widespread adoption. Distributors invest in regional warehouses to shorten lead times, positioning the glass tiles market for faster uptake as economic conditions stabilize.

Competitive Landscape

The glass tiles market is moderately fragmented, with major conglomerates leveraging integrated manufacturing and omnichannel distribution to dominate, creating barriers for smaller producers. European players such as Saint-Gobain and Arizona Tile focus on R&D for sustainability, securing institutional projects emphasizing carbon disclosure. Strategic acquisitions enhance distribution and competitiveness against low-cost imports. Technological advancements, including AI-driven designs and renewable energy integration, drive innovation, shifting competition from volume to value-based differentiation.

Glass Tiles Industry Leaders

Arizona Tile

Daltile

Emser Tile

Saint-Gobain

Iris Ceramica Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Artaic, a mosaic manufacturer leveraging robotic technology, has reduced the price of its sustainable Sintered Glass Tile by 40% and expanded its color palette to enhance design flexibility. The tiles are made from 100% post-consumer recycled car windshields and exemplify eco-friendly circular design.

- March 2024: Fireclay Tile reintroduced its Glass Tile product line, now manufactured in its advanced Glass Factory in Spokane, Washington. As a Certified B Corp, the company ensures all products are responsibly made in the USA, reinforcing its commitment to sustainability and craftsmanship.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the glass tiles market as all sintered, fused, cast, or smalti tiles whose visible body is >=90 % glass and that are sold for interior or exterior walls, floors, backsplashes, pool linings, and decorative facades in residential, commercial, and infrastructure projects worldwide. These values are expressed in USD retail-equivalent revenue.

Scope exclusion: flat architectural glazing, fiber-glass panels, and ceramic or composite tiles with glass coatings are kept outside the model.

Segmentation Overview

- By Product Type

- Matte-finished

- Smooth glass tile

- By Manufacturing Process

- Smalti Tiles

- Fused Tiles

- Sintered Tiles

- Cast Tiles

- Other Manufacturing Processes (Slumped / Etched Tiles)

- By Application

- Wall Cladding

- Flooring

- Backsplashes and Countertops

- Outdoor and Landscape

- By End-User Industry

- Residential

- Commercial

- Infrastructure (Transit, Pools, Facades)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Asian tile exporters, North American distributors, Middle-East project specifiers, and European mosaic artisans to validate average selling prices, installation ratios per square meter, and emerging finishes such as photoluminescent glass. Rapid e-mail polls of renovation contractors helped us test renovation-driven volume swings and channel mix assumptions.

Desk Research

We began with public statistics such as UN Comtrade HS 7016 trade flows, U.S. Census construction-spending tables, Eurostat building-permit data, and World Bank housing-starts series. Industry associations, including the Tile Council of North America, China Building Ceramics Association, and the European Tile & Sanitaryware Federation, offered shipment, price, and capacity insights. Company filings accessed through D&B Hoovers, press releases captured on Dow Jones Factiva, and patent counts drawn from Questel rounded out trend signals. These inputs built the historical demand curve and anchored price corridors. The sources named illustrate our desk work; many additional references informed fact-checks and nuance.

Market-Sizing & Forecasting

A top-down "production + imports - exports" construct derived apparent consumption by country, which we then converted to retail value using region-specific ASPs gathered above. Supplier revenue roll-ups and sampled ASP × area checks supplied a bottom-up reasonableness screen before figures were locked. Key variables feeding the multivariate regression forecast include new residential floor area completions, renovation outlays, glass-cullet price index, global kiln-fuel costs, and average tile coverage per dwelling. Scenario analysis adjusts for energy-price shocks or rapid green-building adoption.

Data Validation & Update Cycle

Outputs run through variance flags versus independent trade totals and price series, after which senior reviewers sign off. We refresh every twelve months, with mid-cycle updates triggered by material events so clients get our latest view.

Why Mordor's Glass Tiles Baseline Earns Trust

Published values often diverge because firms choose different product mixes, revenue definitions, and refresh cadences. By capturing every major installation area and converting to retail value in constant 2024 dollars, Mordor's base year is directly comparable across regions.

Key gap drivers include rivals excluding floor tiles, bundling glass with broader ceramics, using factory-gate pricing, or applying static currency rates. Our annual refresh and two-step validation narrow these gaps, giving decision-makers a stable, defensible anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 72.08 B (2025) | Mordor Intelligence | - |

| USD 74.97 B (2025) | Global Consultancy A | Uses broader decorative-surfaces scope; limited primary validation |

| USD 89.5 B (2030) | Industry Research House B | Longer horizon and bundles glass mosaics with recycled panels |

| USD 2.0 B (2024) | Trade Journal C | Focuses on premium handmade tiles; omits mass-produced volume |

In sum, our disciplined mix of public data, field insight, and scheduled audits lets stakeholders rely on Mordor's numbers as the most transparent baseline available today.

Key Questions Answered in the Report

What is the current Glass Tiles Market size?

The glass tiles market size is valued at USD 76.16 billion in 2026 and is forecast to reach USD 100.26 billion by 2031.

Which region contributes the most revenue to the glass tiles market?

Asia-Pacific leads with 51.84% share in 2025 and is also the fastest-growing region at a 6.61% CAGR through 2031.

Why are sintered glass tiles gaining popularity?

Sintered tiles fire at lower temperatures, lower energy costs, and deliver superior mechanical properties, driving a 6.97% CAGR that outpaces other manufacturing methods.

What applications are expanding fastest within the glass tiles market?

Outdoor and landscape installations are advancing at a 6.55% CAGR as UV-stable, frost-resistant glass tiles gain favor in pools, facades, and premium exterior features.

Page last updated on: