Compact Electric Construction Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

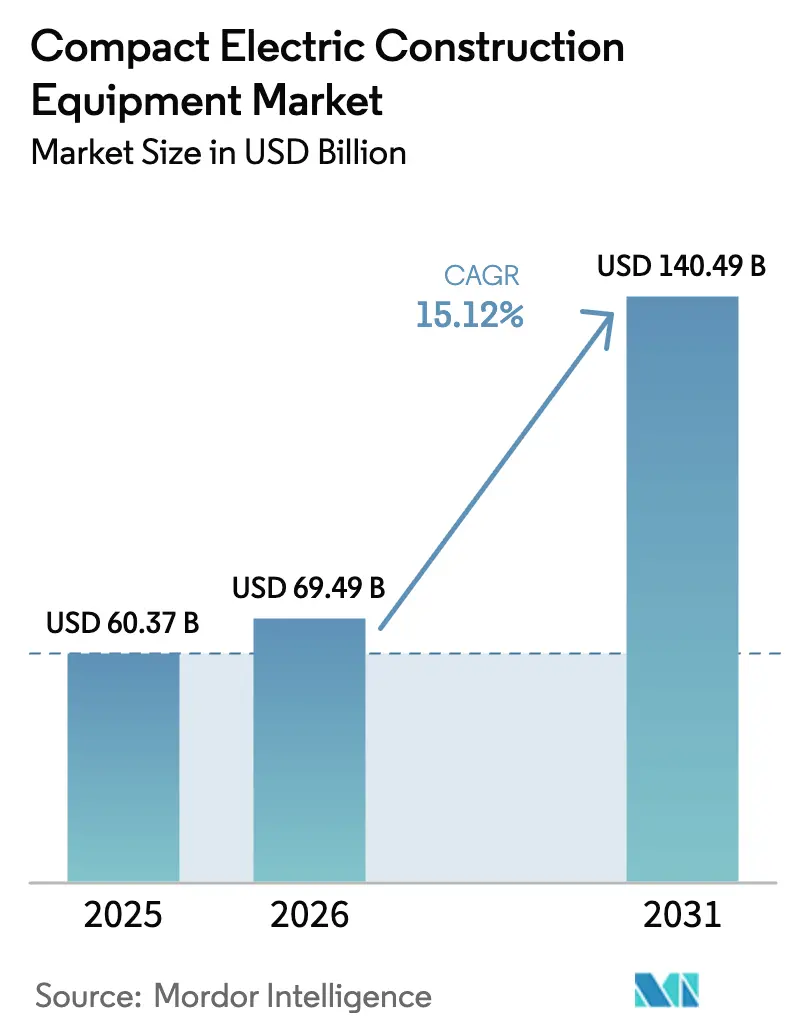

| Market Size (2026) | USD 69.49 Billion |

| Market Size (2031) | USD 140.49 Billion |

| Growth Rate (2026 - 2031) | 15.12% CAGR |

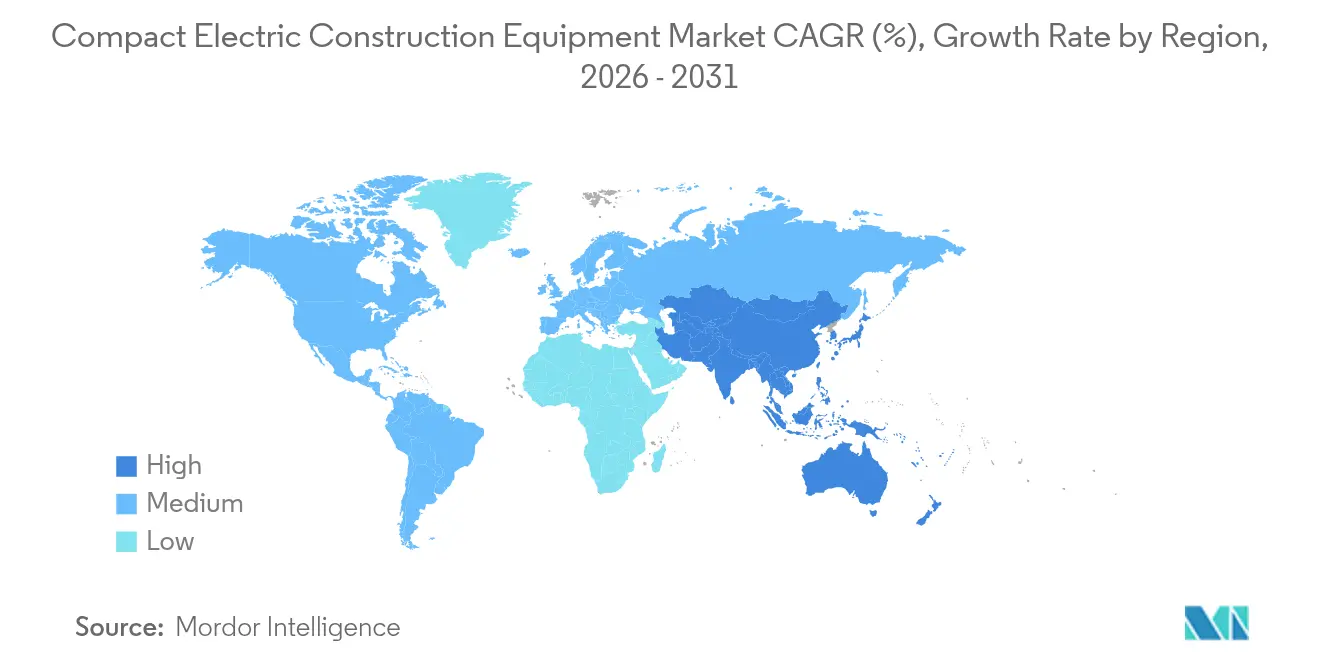

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compact Electric Construction Equipment Market Analysis by Mordor Intelligence

The compact electric construction equipment market size is expected to grow from USD 60.37 billion in 2025 to USD 69.49 billion in 2026 and is forecast to reach USD 140.49 billion by 2031 at 15.12% CAGR over 2026-2031. The sharp expansion reflects a pivotal shift from diesel machines to zero-emission alternatives as battery costs fall, charging speeds rise, and regulators tighten tail-pipe limits globally.[1]California Air Resources Board, “Potential Amendments to the Off-Road New Diesel Engine Emission Standards: Tier 5 Criteria Pollutants and CO₂ Standards,” arb.ca.gov Operators increasingly view battery-electric models as economically viable because fuel savings and lower maintenance offset higher purchase prices within three to four years in high-utilization fleets.[2]David Gohlke et al., “Quantification of Commercially Planned Battery Component Supply in the United States through 2035,” Argonne National Laboratory, anl.gov Demand concentrates in urban projects, renewable-energy build-outs, and grid-modernization worksites where noise and emissions restrictions favor quiet, clean equipment. Competitive dynamics also intensify as incumbents extend electric portfolios while start-ups introduce purpose-built platforms that shorten development cycles and lower operating weight. Strategic partnerships around batteries, autonomy, and fast-charging are becoming decisive in preserving market leadership.

Key Report Takeaways

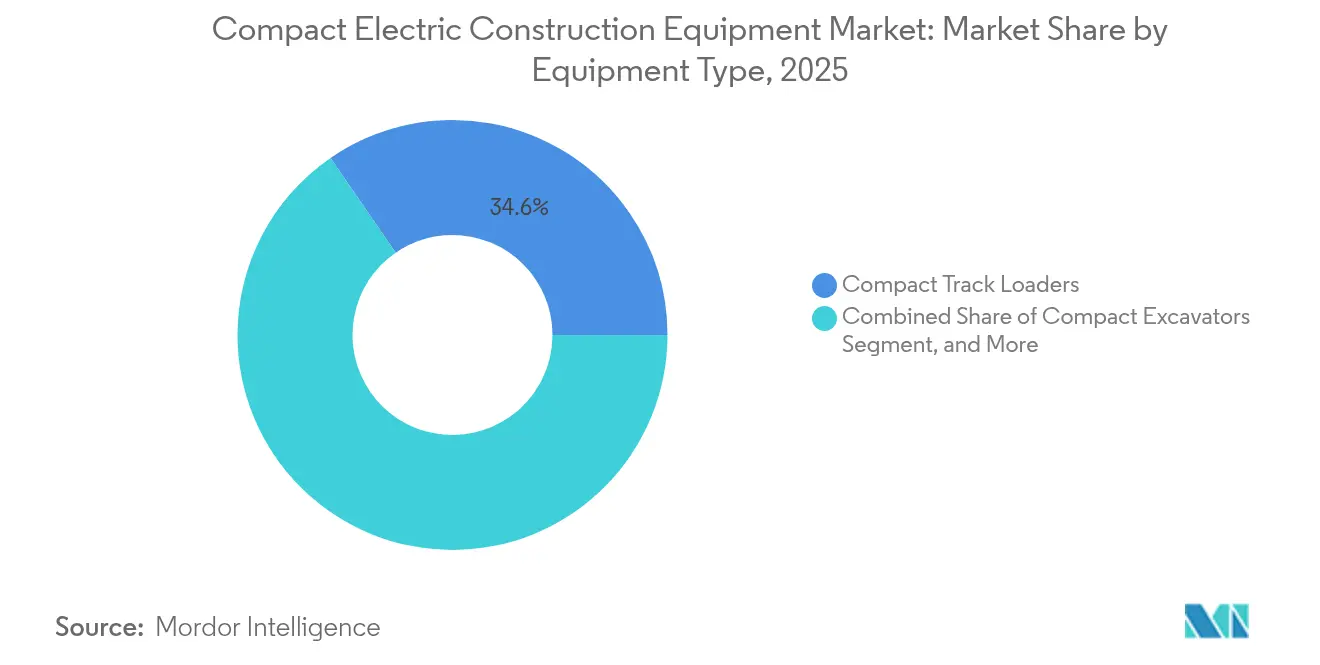

- By equipment type, compact track loaders held 34.60% of the electric compact construction equipment market share in 2025 while compact wheel loaders are projected to grow at 20.44% CAGR through 2031.

- By operating weight, the 2–5-ton class captured 41.30% share of the electric compact construction equipment market size in 2025; sub-2-ton machines are slated to expand at 19.81% CAGR to 2031.

- By propulsion, battery-electric systems commanded 74.20% share in 2025, whereas hybrid-electric solutions deliver the fastest CAGR of 17.95% through 2031.

- By end-user vertical, infrastructure projects led with 27.50% revenue share in 2025, while utilities and energy are forecast to accelerate at 22.05% CAGR, fueled by grid upgrades and renewable-energy installations.

- By geography, North America accounted for 31.70% of 2025 revenue, supported by the USD 1 billion EPA Clean Heavy-Duty Vehicles Program that subsidizes zero-emission machinery.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compact Electric Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent zero-emission regulations (Tier V, China VI, CARB, etc.) | +4.2% | Global, with early adoption in California, EU, China | Medium term (2-4 years) |

| Rapid battery-density & fast-charge breakthroughs | +3.8% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Total cost-of-ownership (TCO) savings on fuel & maintenance | +3.1% | Global, particularly in high fuel-cost regions | Long term (≥ 4 years) |

| Government purchase incentives & green-public-procurement rules | +2.7% | North America, EU, select APAC markets | Medium term (2-4 years) |

| Extended work-hours in noise-restricted urban zones | +1.9% | Urban centers globally, concentrated in developed markets | Short term (≤ 2 years) |

| Net-zero bid prerequisites in EPC / PPP tenders | +1.6% | Global, led by government infrastructure projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Zero-Emission Regulations Drive Market Transformation

California’s draft Tier 5 rules mandate 90% NOx cuts from 2029, introducing the first off-road CO₂ limits and pushing OEMs toward electrification to avoid costly after-treatment complexity. Similar momentum stems from Euro 7, which extends stringent standards to construction machinery across 2026-2034, and from China VI, reinforcing local demand and export competitiveness. Compliance costs tilt life-cycle economics in favor of battery systems, hastening the pivot in core product roadmaps.

Battery Technology Breakthroughs Enable Performance Parity

CATL’s 175 Wh/kg TECTRANS pack charges to 70% in 15 minutes and supports 15-year duty cycles, dismantling historic runtime and charging bottlenecks.[3]Contemporary Amperex Technology Co., “CATL Unveils Revolutionary TECTRANS Battery System,” catl.com Komatsu’s sodium-ion field trials and Tesla’s modular safety patents further diversify chemistry options that lengthen life, cut costs, and mitigate thermal risk. As a result, equipment selection increasingly rests on economic payback rather than performance trade-offs.

Total Cost of Ownership Advantages Accelerate Fleet Conversion

Operators report 70% operating-cost reductions through fuel and maintenance savings when switching to battery-electric units, shortening payback to under four years in intensive applications. Argonne forecasts battery pack prices sliding toward USD 86/kWh by 2035, with U.S. tax credits pushing effective cost as low as USD 56/kWh by 2029, locking in TCO advantages. Predictable OPEX and quieter operations elevate productivity on sensitive sites.

Government Incentives Create Adoption Momentum

The EPA’s USD 1 billion Clean Heavy-Duty Vehicles Program offers point-of-sale vouchers, while California’s CORE scheme has broadened eligible categories fourteen-fold since 2020, easing the upfront premium hurdle. Similar green-procurement rules in the U.K. and EU prioritize zero-emission fleets in public tenders, giving early movers a competitive edge in bidding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex of electric machines | -2.8% | Global, particularly in price-sensitive emerging markets | Medium term (2-4 years) |

| Limited fast-charging & swap infrastructure | -2.1% | Global, acute in rural and remote construction sites | Short term (≤ 2 years) |

| Residual-value uncertainty dampening leasing appetite | -1.7% | Developed markets with mature leasing sectors | Long term (≥ 4 years) |

| Battery-performance loss in extreme climates | -1.4% | Cold climate regions, high-temperature environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure Constrains Adoption

Price premiums of 40–60% over diesel equivalents deter small contractors despite lifecycle savings. Bobcat’s TL25.60e telehandler illustrates market hesitation where incentives are insufficient, even though performance matches diesel variants. Financing innovation, battery leasing, and broader voucher programs remain pivotal to unlock demand.

Infrastructure Limitations Constrain Operational Flexibility

Grid access and high-power charging remain scarce on remote sites. Volvo CE’s mobile charging partnership offers interim solutions, but long-haul deployment depends on wider NEVI-funded infrastructure that is still tailored to light vehicles. Battery-swap schemes could bridge gaps, yet lack of cross-OEM standards curbs scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Loaders Capture Urban Demand

Compact track loaders accounted for 34.60% of 2025 revenue and anchored the electric compact construction equipment market size leadership in urban material-handling applications. Compact wheel loaders post the highest 20.44% CAGR to 2031 as municipalities tighten noise ordinances and contractors demand versatile machines that maneuver in constrained spaces. CASE’s 580EV backhoe proves 8-hour runtime parity and signals expanding adoption across heavier tasks.

Demand for compact excavators persists where precision digging in tight footprints is essential, while electric forklifts gain traction inside warehouses mandated to maintain indoor air quality. Compact track loaders gain share in landscaping due to reduced ground pressure. Integration of telematics and over-the-air updates further lifts utilization by optimizing charging windows and predictive maintenance schedules, reinforcing operator confidence.

By Operating Weight: Mid-Range Platforms Dominate Utilization Sweet Spot

The 2–5-ton class retained 41.30% of 2025 volume, reinforcing its importance in the electric compact construction equipment market share mix. Liebherr’s modular battery offering on the L 507 E allows right-sizing packs to job duration and cost targets, illustrating how flexible energy architecture supports TCO optimization. Sub-2-ton machines, meanwhile, deliver a 19.81% CAGR through 2031 as residential infill projects and indoor renovations call for ultra-compact units.

At the high end, 5–8-ton models cater to mid-sized urban works requiring greater lift without compromising maneuverability, while 8–13-ton categories await next-generation high-density batteries and megawatt charging to displace diesel incumbents. Weight-class choice increasingly hinges on balancing battery mass with payload, pushing OEMs to pursue structural-lighting innovations and high-strength composites.

By Propulsion Type: Battery-Electric Sets the Benchmark

Battery-electric platforms captured 74.20% of 2025 shipments, anchoring the electric compact construction equipment market. Pack price declines, fast-charge improvements, and widening dealer service networks mitigate historic adoption risks. Hybrid-electric solutions grow fastest at an 17.95% CAGR, enabling contractors to hedge against infrastructure gaps while lowering emissions on partial duty cycles.

Tethered power and grid-connected variants fill stationary applications like industrial plants, whereas hydrogen fuel cell pilots remain exploratory amid supply chain immaturity. OEMs increasingly build propulsion-agnostic chassis that accept battery, hybrid, or fuel-cell modules, future-proofing capital investments.

By End-User Vertical: Infrastructure and Utilities Underpin Demand

Government-funded infrastructure projects led adoption with 27.50% market contribution in 2025, capitalizing on procurement clauses favoring zero-emission fleets. Utilities and energy customers spark the highest 22.05% CAGR as grid hardening, renewable installations, and substation upgrades require emission-free machinery around sensitive assets.

Commercial developers integrate electric fleets to meet LEED criteria, while residential builders favor low-noise models for neighborhood sites. Industrial plants deploy electric forklifts and loaders indoors to comply with occupational health standards. Landscaping firms value quiet operation for suburban contracts, indicating broadening end-market acceptance.

Geography Analysis

North America led with 31.70% revenue in 2025, propelled by federal and state vouchers that neutralize upfront premiums and by mature dealer ecosystems adept at servicing electric drivetrains. The United States anchors demand, while Canada and Mexico add incremental volume tied to infrastructure stimulus and near-shoring manufacturing investments. CNH Industrial’s expansion of electric loader production in Lecce, Italy, primarily serves rising North American orders, underscoring trans-Atlantic supply-chain integration.

Asia-Pacific records the fastest 17.55% CAGR to 2031, steered by China, which commanded 75% of global electric construction equipment sales in 2024 due to large-scale manufacturing capabilities and domestic procurement mandates. Japan’s equipment orders rebounded 14.1% in early 2025 on electrification investments, while India’s urbanization and agricultural mechanization spark demand for sub-2-ton models. Komatsu’s USD 65 million U.S. battery expansion illustrates APAC manufacturers’ global capacity positioning.

Europe remains a regulatory bellwether with staged Euro 7 deadlines and a 2035 zero-emission target for construction machinery. Germany, France, the U.K., and Italy feature robust incentive schemes and stringent urban noise limits that drive fleet turnover. Volvo’s EC230 Electric launch in France and Hitachi’s ZX55U-6EB mini excavator roll-out exemplify OEM confidence in regional demand. Economic variability and energy-price volatility temper purchasing in southern and eastern states, yet sustainability imperatives keep growth positive.

Competitive Landscape

The electric compact construction equipment market exhibits moderate concentration, with the top five participants controlling roughly 55% of global shipments in 2024. Caterpillar generated USD 67.060 billion in 2023 sales and is integrating Luminar lidar into autonomous systems to enhance job-site productivity and retain premium positioning in hybrid and battery domains. Volvo Group reported a 24% surge in compact electric orders, validating its multi-voltage platform strategy and early-mover advantage in mid-size classes.

Strategically, incumbents pursue dual tracks: expanding battery models while sustaining diesel lines in markets with limited infrastructure. Partnerships—such as Caterpillar-CRH for battery trucks and Liebherr-Fortescue for zero-emission mine fleets—signal integration of equipment, charging, and energy supply chains to deliver end-to-end decarbonization. Emerging challengers like Lumina and FIRSTGREEN adopt clean-sheet designs that reduce part counts and exploit high-torque electric drivetrains to create differentiated value. Intellectual-property races center on battery safety, modularity, and thermal management, with more than 120 patent filings in 2024 targeting pack mounting and cooling enhancements.

Dealer readiness and financing innovations become competitive levers. OEM-backed leasing with guaranteed residuals mitigates buyer risk tied to rapid technology cycles, while energy-as-a-service contracts bundle hardware, charging, and maintenance into predictable monthly fees, aligning with contractor cash-flow realities.

Compact Electric Construction Equipment Industry Leaders

Caterpillar Inc.

Bobcat Company

AB Volvo Construction Equipment

JCB Services Ltd.

Hyundai Doosan Infracore Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lumina revealed the ML6 Moonlander electric dozer prototype capable of 8–10-hour shifts and 300-kW charging, signaling a push into heavier duty classes. The strategy seeks to pre-empt incumbent dominance in large dozers while showcasing purpose-built electric architectures.

- March 2025: Fayat Group agreed to acquire Mecalac, adding multifunctional urban machines that strengthen Fayat’s position in compact, electric-ready platforms; the deal also expands cross-selling through BOMAG and Dynapac channels.

- March 2025: Caterpillar partnered with Luminar to integrate Iris lidar into autonomous quarry equipment, accelerating the Cat Command platform’s move toward full self-driving job-site ecosystems.

- January 2025: Volvo Group booked 766 fully electric compact units in Q4 2024, validating its modular battery strategy and reinforcing backlog visibility for 2025 deliveries.

Global Compact Electric Construction Equipment Market Report Scope

The compact electric construction equipment market focuses on smaller, electrically powered machines designed for construction, landscaping, and urban projects. These machines offer lower emissions, reduced noise, and increased efficiency compared to traditional equipment, making them ideal for sustainable construction practices. This market is driven by advancements in battery technology, stringent environmental regulations, and rising demand for eco-friendly construction solutions.

The Compact Electric Construction Equipment Market is segmented by equipment type (excavators, forklifts, loaders, aerial work platforms (AWP), and other equipment type), ton (below 5 ton, 5 to 8 ton, above 8 ton), end-user (residential construction, commercial construction, industrial construction, infrastructure development, landscaping, mining, and other end-users), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Compact Excavators |

| Compact Wheel Loaders |

| Compact Track Loaders |

| Electric Forklifts |

| Aerial Work Platforms – Scissor Lifts |

| Other Equipment Types |

| < 2 Ton |

| 2 – 5 Ton |

| 5 – 8 Ton |

| 8 – 13 Ton |

| Battery Electric (Li-ion) |

| Hybrid Electric |

| Tethered / Grid-Connected Electric |

| Hydrogen Fuel Cell (Pilot) |

| Solar-Assisted / Battery-Swap Ready |

| Residential Construction |

| Commercial Construction |

| Industrial Facilities and Plants |

| Infrastructure Development |

| Utilities and Energy |

| Landscaping and Agriculture |

| Other End-user Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| Equipment Type | Compact Excavators | |

| Compact Wheel Loaders | ||

| Compact Track Loaders | ||

| Electric Forklifts | ||

| Aerial Work Platforms – Scissor Lifts | ||

| Other Equipment Types | ||

| Operating Weight (Ton) | < 2 Ton | |

| 2 – 5 Ton | ||

| 5 – 8 Ton | ||

| 8 – 13 Ton | ||

| Propulsion Type | Battery Electric (Li-ion) | |

| Hybrid Electric | ||

| Tethered / Grid-Connected Electric | ||

| Hydrogen Fuel Cell (Pilot) | ||

| Solar-Assisted / Battery-Swap Ready | ||

| End-User Vertical | Residential Construction | |

| Commercial Construction | ||

| Industrial Facilities and Plants | ||

| Infrastructure Development | ||

| Utilities and Energy | ||

| Landscaping and Agriculture | ||

| Other End-user Verticals | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the electric compact construction equipment market?

The market is valued at USD 69.49 billion in 2026, with a forecast to reach USD 140.49 billion by 2031.

Which equipment category leads revenue today?

Battery-electric loaders hold 34.60% of global revenue due to versatility and strong urban demand.

How fast are battery prices falling?

Argonne projects pack costs dropping from USD 140/kWh in 2023 to USD 86/kWh by 2035, with U.S. tax credits potentially lowering the effective cost to USD 56/kWh by 2029.

Which region shows the highest growth rate?

Asia-Pacific posts a 17.55% CAGR, driven mainly by China’s dominant manufacturing scale and domestic incentives.

What policies accelerate adoption in North America?

The EPA’s USD 1 billion Clean Heavy-Duty Vehicles Program and California’s CORE vouchers directly cut purchase costs for zero-emission equipment.

Are hybrid machines still relevant?

Yes; hybrid-electric systems grow at 17.95% CAGR as they provide a transition path for contractors lacking robust charging infrastructure.

Page last updated on: