Commercial Vehicle Remote Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.07 Billion |

| Market Size (2031) | USD 12.12 Billion |

| Growth Rate (2026 - 2031) | 11.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Commercial Vehicle Remote Diagnostics Market Analysis by Mordor Intelligence

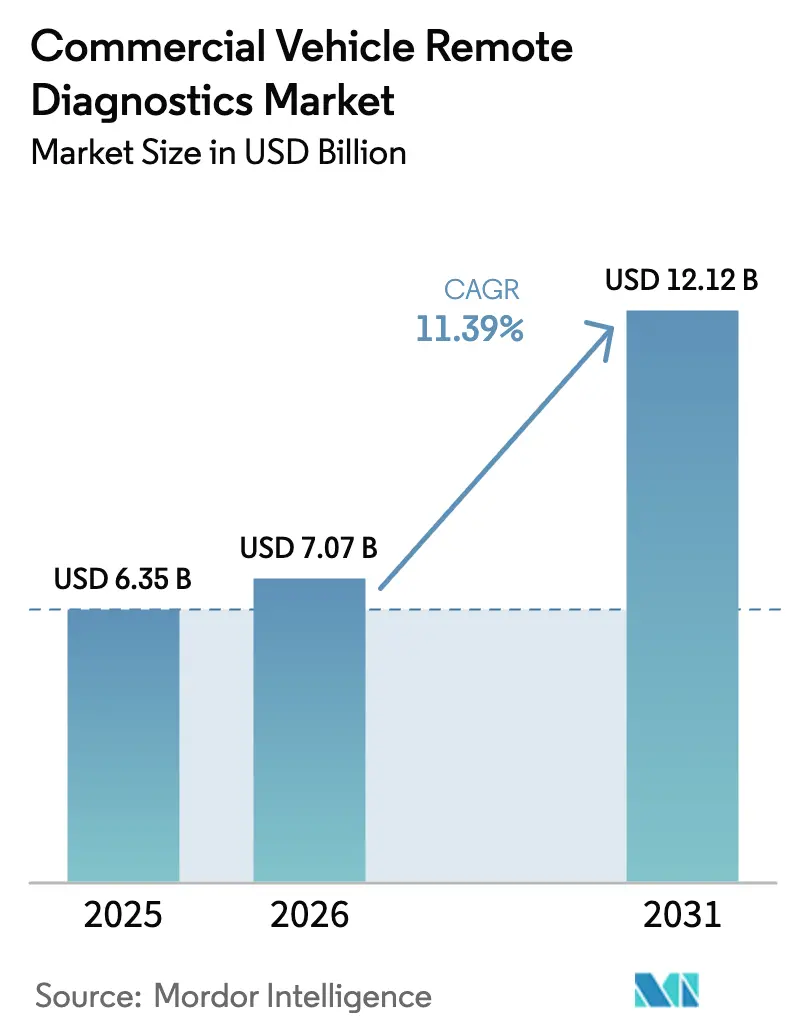

The Commercial Vehicle Remote Diagnostics Market size was valued at USD 6.35 billion in 2025 and estimated to grow from USD 7.07 billion in 2026 to reach USD 12.12 billion by 2031, at a CAGR of 11.39% during the forecast period (2026-2031).

Fleet operators worldwide view real-time health monitoring as indispensable because tighter emissions regulations, 5 G-enabled edge analytics, and persistent driver shortages reward uptime-centric operations. Regulatory deadlines such as EPA Phase 3 and Euro VII steer powertrain design toward always-on data streams. At the same time, OEMs and tier-one suppliers now integrate diagnostics at the factory rather than treating them as add-ons. Cloud-native analytics reduces false alarms, accelerates root-cause analysis, and frees scarce maintenance staff for higher-value tasks. Partnerships between truck makers and software specialists are intensifying as companies race to deliver unified, over-the-air-updatable platforms that shorten development cycles and expand revenue from post-sale services. Investors and insurers also signal confidence by linking financing terms to demonstrated reductions in unplanned downtime.

Key Report Takeaways

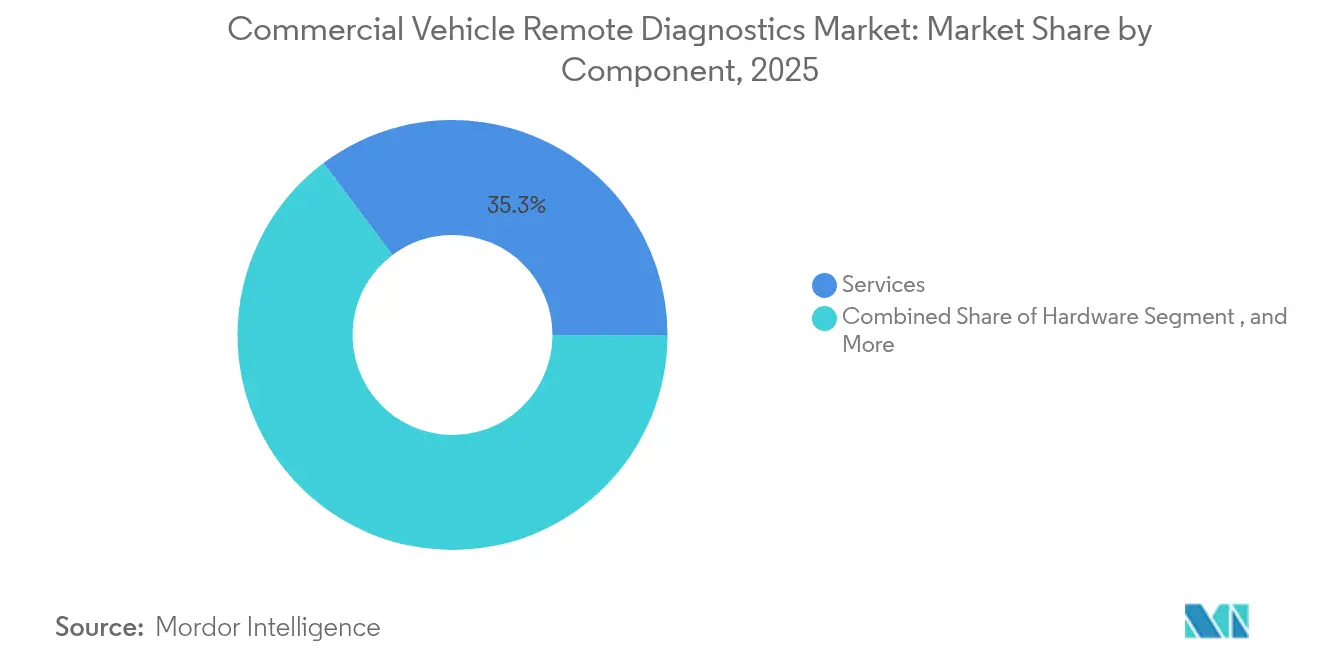

- By component, services accounted for 35.25% of the commercial vehicle remote diagnostics market revenue share in 2025, whereas software is projected to expand at an 18.25% CAGR to 2031.

- By vehicle type, medium and heavy trucks led with 56.60% of the commercial vehicle remote diagnostics market share in 2025; electric light commercial vehicles are forecast to grow at a 23.10% CAGR through 2031.

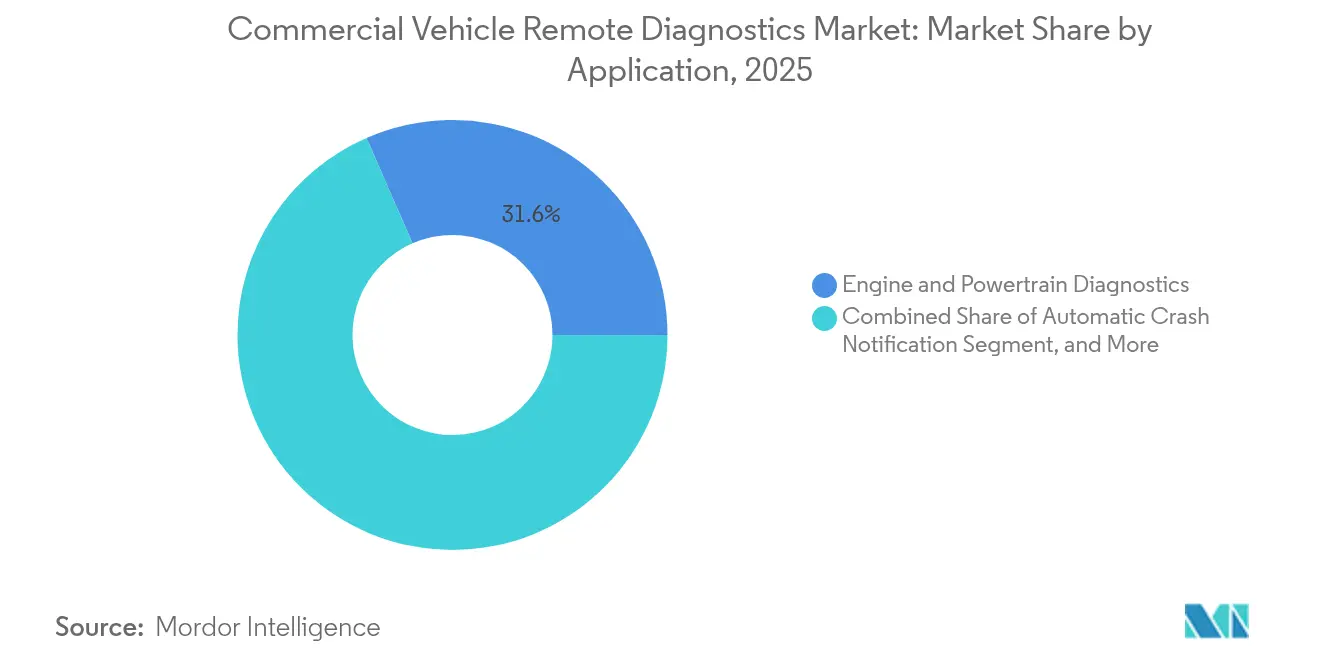

- By application, engine and powertrain diagnostics captured 31.55% of the commercial vehicle remote diagnostics market size in 2025 and remain essential, while battery and thermal management systems are advancing at a 24.40% CAGR.

- By end-use, OEM platforms controlled 54.50% of the commercial vehicle remote diagnostics market revenue share in 2025, yet leasing and rental companies record the fastest uptake at a 16.85% CAGR as uptime-guaranteed contracts proliferate.

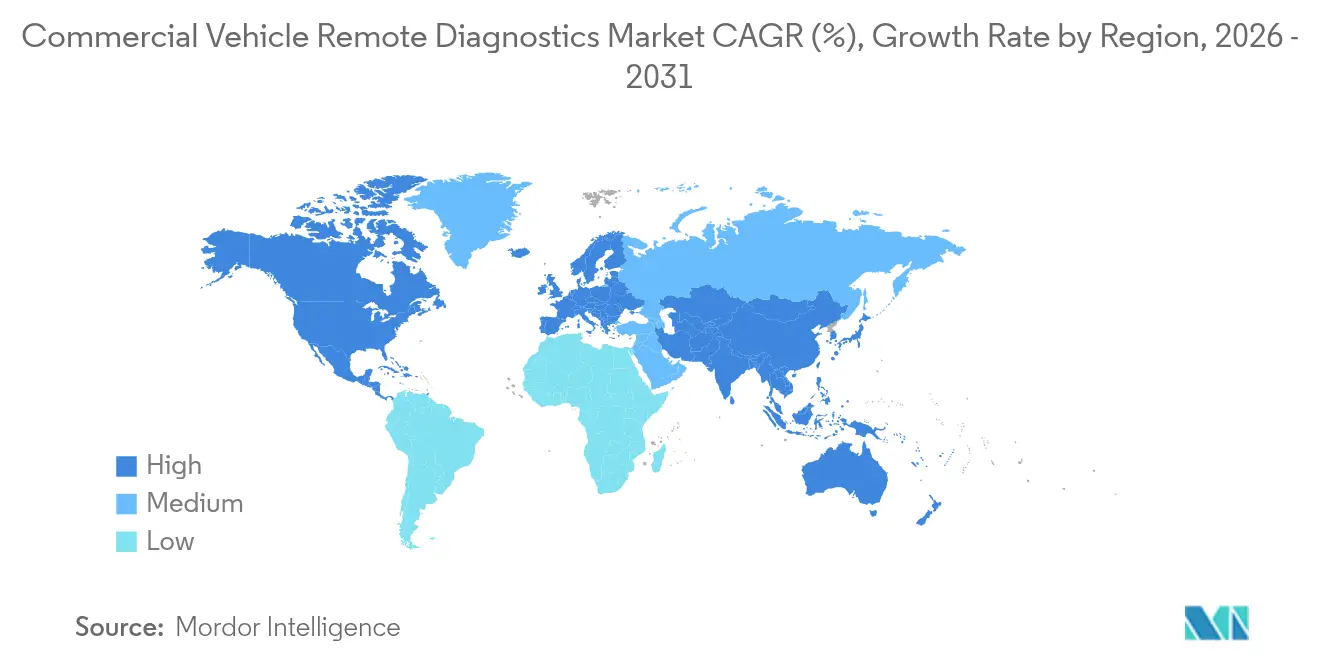

- By geography, North America represented a 33.80% of the commercial vehicle remote diagnostics market revenue share in 2025; Asia-Pacific is the fastest-growing region with a 14.55% CAGR projected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Vehicle Remote Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G-Enabled Edge Analytics for Heavy Trucks | +3.2% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| OEM-Installed Telematics Standardization in EU and US | +2.8% | North America and EU | Medium term (2–4 years) |

| Tightening GHG Rules (Euro VII, EPA Phase 3) | +2.5% | North America and EU | Medium term (2–4 years) |

| Fleet Uptime-Linked Leasing Contracts | +2.1% | Global, with concentration in North America | Short term (≤ 2 years) |

| Lithium-Ion Battery Prognostics for Electric CVs | +1.9% | Global, early gains in China, EU, California | Long term (≥ 4 years) |

| SaaS Migration of Legacy Diagnostics Suites | +1.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G-Enabled Edge Analytics for Heavy Trucks

The deployment of 5G infrastructure specifically designed for vehicular applications is enabling unprecedented real-time processing capabilities at the vehicle edge, transforming diagnostic systems from reactive monitoring tools into proactive operational intelligence platforms. MAN Truck & Bus projects that data exchange will increase from current levels of 5-50 MB to over 100 MB daily by 2025, with potential growth to 2 terabytes per day per truck by 2027 as 5G enables more sophisticated diagnostic algorithms. Beijing's vehicle-road-cloud integration pilot project, supported by China Mobile and featuring over 7,000 5G-A base stations, demonstrates how network slicing can prioritize critical diagnostic data transmission while supporting autonomous driving functions. The 5GCroCo project's successful cross-border trials between France, Germany, and Luxembourg validate that 5G networks can maintain service continuity for diagnostic applications as vehicles traverse international boundaries, addressing a key concern for long-haul operators. Ericsson's collaboration with Scania on network slicing for autonomous vehicle testing shows how 5G can create dedicated communication channels for safety-critical diagnostic data, ensuring reliable transmission even under heavy network loads. This infrastructure investment is particularly significant for the heavy truck segment, where high-value assets and complex powertrains generate substantial diagnostic data volumes that require low-latency processing for effective predictive maintenance.

OEM-Installed Telematics Standardization in EU and US

Regulatory harmonization across major markets accelerates OEM adoption of standardized telematics architectures, fundamentally reshaping how commercial vehicle data flows through the supply chain. The California Air Resources Board's transition to SAE J1979-2 protocol starting with 2027 engine model years represents a critical inflection point, requiring heavy-duty vehicle manufacturers to implement unified diagnostic communication standards[1]"Guidance for Engines Using the SAE J1979-2 (OBDonUDS) Protocol", California Air Resources Board, ww2.arb.ca.gov.. This standardization enables seamless integration between OEM systems and third-party fleet management platforms, reducing the technical barriers that have historically fragmented the aftermarket. Geotab's recent expansion to support 157 OEMs and nearly 15,000 vehicle models demonstrates how standardization creates economies of scale for telematics providers. The emergence of open-source initiatives like Cummins' Eclipse CANought platform, developed with Bosch and KPIT, signals a broader industry shift toward interoperable diagnostic ecosystems that reduce customization costs and accelerate time-to-market for new applications. This standardization trend is particularly significant for mixed-fleet operators who previously faced integration challenges when managing vehicles from multiple manufacturers.

Tightening GHG Rules (Euro VII, EPA Phase 3)

Stringent emissions regulations mandate sophisticated diagnostic capabilities that extend far beyond traditional fault code reporting, requiring real-time monitoring of emissions control system performance and battery state-of-health for electric vehicles. The EPA's Phase 3 greenhouse gas standards, finalized in March 2024 for model years 2027-2032, include specific battery and electric powertrain warranties requiring continuous state-of-health monitoring for plug-in hybrid and battery electric vehicles. The new NOx emission standards, dropping from 200 mg/hp-hr to 35 mg/hp-hr by 2027, require advanced aftertreatment systems with electric heating capabilities that must be continuously monitored to ensure optimal performance at low engine loads. California's Clean Truck Check program exemplifies how regulatory compliance drives diagnostic adoption, requiring semi-annual emissions testing that includes OBD data scans for newer vehicles and establishing penalties for non-compliance. The extension of warranty periods from 100,000 to 450,000 miles under the new regulations creates additional incentives for manufacturers to implement robust diagnostic systems that can predict component failures before they occur. These regulatory changes are particularly impactful for the engine and powertrain diagnostics segment, which maintains the largest application share at 32.1%, as traditional diagnostic approaches prove insufficient for meeting the new compliance requirements.

Fleet Uptime-Linked Leasing Contracts

Commercial vehicle leasing models' evolution toward uptime guarantees creates powerful incentives for diagnostic system adoption, as lessors increasingly assume maintenance risk and require real-time vehicle health monitoring to protect their investments. United Road's implementation of Uptake Fleet achieved a 4x return on investment by transitioning from reactive to predictive maintenance strategies, demonstrating how diagnostic-enabled contracts can simultaneously reduce costs for lessors and improve service levels for lessees. This model shift is particularly pronounced in the leasing and rental segment, which shows the fastest growth at 17.30% CAGR as companies like Hogan Truck Leasing leverage telematics to achieve a 62% reduction in credited miles, saving millions in operational costs. Integrating diagnostic data into lease pricing algorithms enables more accurate risk assessment and customized contract terms based on vehicle utilization patterns. Mack Trucks' Premium Service Contract exemplifies this trend by using AI to dynamically adjust maintenance intervals based on real-time operational data, optimizing service schedules for individual customer operations. This convergence of financial and operational incentives accelerates diagnostic adoption across fleet segments that previously viewed such systems as optional rather than essential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CAN-FD Cyber-Security Vulnerabilities | -1.8% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Fragmented Aftermarket Data Standards | -1.4% | Global, particularly affecting mixed fleets | Medium term (2-4 years) |

| ROI Uncertainty for Small Fleet Operators | -1.1% | Global, concentrated in emerging markets | Short term (≤ 2 years) |

| Sparse Truck-Specific 5G Highway Coverage | -0.9% | Rural corridors globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CAN-FD Cyber-Security Vulnerabilities

The inherent security weaknesses in Controller Area Network protocols create systemic risks that threaten to undermine fleet operators' confidence in connected diagnostic systems, particularly as attack vectors become more sophisticated and accessible. Research published in 2024 identified 14 attack scenarios against SAE J1939 communication protocols, with 11 scenarios confirmed as feasible through testing, including single-message injection attacks that are particularly difficult to detect. The lack of encryption and authentication in CAN-FD protocols exposes commercial vehicles to remote hijacking, data manipulation, and denial-of-service attacks that could compromise vehicle safety and sensitive operational data. ZF's cybersecurity initiatives highlight potential breaches' financial and safety implications, emphasizing the need for security-by-design approaches that comply with UNECE regulations UN R155 and UN R156. Developing secure CAN-FD architectures like EXT-TAURUM P2T demonstrates industry efforts to address these vulnerabilities through rolling secret key systems and hardware signature mechanisms, but widespread implementation remains limited. These security concerns are particularly acute for fleet operators in regulated industries where data breaches could result in significant compliance penalties and operational disruptions.

Fragmented Aftermarket Data Standards

The absence of unified data communication protocols across different vehicle manufacturers and diagnostic system providers creates integration challenges that increase implementation costs and limit the scalability of fleet management solutions. The Association of Equipment Management Professionals (AEMP) standard represents an attempt to normalize telematics data from various OEMs. Still, challenges persist in ensuring data availability, accuracy, and frequency across different platforms. McKinsey research indicates that many organizations struggle to realize expected performance improvements from telematics investments due to internal disconnects and the complexity of integrating data from multiple sources. The proliferation of proprietary diagnostic protocols creates vendor lock-in scenarios that limit fleet operators' ability to switch between service providers or integrate best-of-breed solutions from multiple vendors. European Union regulations requiring user consent for data collection and restricting third-party data access further complicate standardization efforts, particularly for international fleet operators. This fragmentation is especially problematic for mixed-fleet operators who manage vehicles from multiple manufacturers and require unified diagnostic platforms to achieve operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Drives Digital Transformation

Services maintain the largest market share at 35.25% of the commercial vehicle remote diagnostics market in 2025, and the rapid growth of software solutions indicates a fundamental transformation in how diagnostic capabilities are delivered and consumed. Software is the fastest-growing component segment with an 18.25% CAGR through 2031, reflecting the industry's accelerating shift toward cloud-based diagnostic platforms and AI-driven predictive analytics. Hardware components, including ECUs, sensors, and telematics control units, continue to provide the foundational infrastructure for data collection. Still, their growth is increasingly tied to software functionality rather than standalone device sales. Edge-AI gateways represent a particularly dynamic hardware subsegment, enabling real-time processing capabilities that reduce latency and bandwidth requirements for critical diagnostic functions.

The migration toward Software-as-a-Service models is exemplified by platforms like Navistar's OnCommand Connection, which processes over 70 telematics and sensor data feeds from more than 375,000 connected vehicles, demonstrating how cloud-based architectures can scale to handle massive data volumes. Managed uptime services are gaining traction as fleet operators seek to transfer maintenance risk to specialized providers who can leverage diagnostic data to optimize service intervals and prevent costly breakdowns. Integration and consulting services remain essential for complex implementations, particularly as organizations struggle to extract value from telematics investments without proper data interpretation capabilities and organizational alignment.

By Vehicle Type: Electric Light CVs Challenge Heavy Truck Dominance

Medium and heavy trucks command 56.60% of the commercial vehicle remote diagnostics market share in 2025, driven by their high-value assets and complex diagnostic requirements, but electric light commercial vehicles represent the fastest-growing segment at 23.10% CAGR as electrification accelerates across urban delivery fleets. The Class 8 and off-highway truck subsegment generates the highest diagnostic data volumes due to sophisticated emissions control systems and extended duty cycles that require continuous monitoring. Class 4-7 medium-duty vehicles benefit from increasing adoption of telematics-enabled fleet management solutions, particularly in last-mile delivery applications where route optimization and vehicle utilization directly impact profitability. Vans and pick-ups in the light commercial vehicle category are experiencing rapid growth in diagnostic adoption as e-commerce expansion drives demand for efficient urban logistics solutions.

The electric vehicle transition fundamentally reshapes diagnostic requirements, with battery thermal management systems becoming critical for vehicle performance and safety. Developing high-voltage insulation resistance detection systems for commercial vehicles operating at 800V highlights the specialized diagnostic requirements emerging in the electric vehicle segment. Advanced battery management systems incorporating Extended Kalman Filter and machine learning algorithms are becoming essential for accurate state-of-charge and state-of-health estimation in electric commercial vehicles.

By Application: Battery Management Emerges as Growth Driver

Engine and powertrain diagnostics maintain the largest application share at 31.55% of the commercial vehicle remote diagnostics market in 2025, reflecting the continued dominance of internal combustion engines in commercial vehicle fleets. Still, battery and thermal management systems are expanding rapidly at 24.40% CAGR as electrification gains momentum. Automatic crash notification systems provide essential safety functionality that is increasingly mandated by regulatory authorities. At the same time, roadside assistance applications leverage diagnostic data to enable proactive service dispatch and reduce vehicle downtime. Over-the-air software update validation represents an emerging application area that becomes critical as vehicles evolve into software-defined platforms requiring continuous security and functionality updates. Vehicle tracking and geofencing applications continue to provide fundamental fleet management capabilities, though their growth is increasingly tied to integration with more sophisticated diagnostic functions.

The sophistication of battery thermal management systems is advancing rapidly, with research demonstrating that heat pipe embedded cooling systems can maintain optimal battery temperatures and prevent thermal runaway in electric commercial vehicles. Predictive analytics platforms are becoming essential for processing the massive data volumes generated by modern commercial vehicles, with some systems achieving 98.70% accuracy in fault detection using ensemble machine learning methods. The AI-driven diagnostics integration enables new applications like adaptive maintenance scheduling, where service intervals are dynamically adjusted based on real-time operational data rather than fixed time or mileage thresholds. Advanced driver assistance systems are creating additional diagnostic requirements as vehicles become more automated, necessitating continuous monitoring of sensor performance and system calibration.

By End-Use: Leasing Companies Drive Innovation Adoption

OEMs control 54.50% of the commercial vehicle remote diagnostics market in 2025 through their integrated telematics offerings and direct customer relationships. Still, leasing and rental companies demonstrate the fastest growth at 16.85% CAGR as they leverage diagnostic data to optimize asset utilization and reduce maintenance costs. The aftermarket and fleet segment benefits from the flexibility to choose best-of-breed solutions from multiple vendors. However, this advantage diminishes as OEM platforms become more open and interoperable. Leasing companies increasingly position diagnostic capabilities as value-added services that differentiate their offerings and enable more sophisticated pricing models based on actual vehicle utilization and maintenance requirements.

The transformation of leasing models toward uptime guarantees creates powerful incentives for diagnostic adoption, as demonstrated by Hogan Truck Leasing's 62% reduction in credited miles through automated data collection and analysis. Small fleet operators are finding value in telematics solutions starting at under USD 20 per month, with companies like Frisch & Sons achieving over USD 1,000 in weekly savings through improved operational efficiency. The emergence of diagnostic-enabled service contracts blurs traditional boundaries between OEMs, aftermarket providers, and fleet operators, as seen in partnerships like Platform Science's acquisition of Trimble's telematics business units to create integrated fleet management ecosystems. OEM strategies are evolving toward platform-based approaches that enable third-party application development, as exemplified by International Truck's integration with over 30 telematics service providers through their OnCommand Connection platform.

Geography Analysis

North America commands 33.80% of the commercial vehicle remote diagnostics market in 2025 revenue, propelled by EPA Phase 3 rules that mandate advanced onboard diagnostics for 2027 model-year heavy trucks. The region’s robust service-dealer network speeds parts distribution once the platform flags impending failures. California’s Clean Truck Check program adds semi-annual OBD scans, cementing diagnostics as a compliance staple.

Asia-Pacific is the fastest-growing territory with a 14.55% CAGR forecast to 2031. China’s vehicle-road-cloud pilots, backed by 5 G-Advanced base stations, show how network slicing prioritizes truck telemetry even in dense urban corridors. Japan, South Korea, and India layer government incentives on smart-mobility roadmaps, prompting vendors to localize dashboards for non-Latin scripts and multi-SIM connectivity.

Europe stands at an inflection point as Euro VII negotiations conclude. Trials under the 5GCroCo consortium demonstrated flawless cross-border hand-offs, assuaging carrier concerns about roaming charges and session drops. Scandinavian countries pioneer battery-electric truck corridors, while Germany’s manufacturing clusters cultivate supplier ecosystems that blend cybersecurity modules with embedded diagnostics toolchains.

Competitive Landscape

The commercial vehicle remote diagnostics market features moderate fragmentation. Bosch, Continental, and ZF leverage ECU portfolios and deep OEM ties, bundling diagnostics with brake, steering, and ADAS subsystems. Cloud-native challengers such as Platform Science accelerate innovation cycles by running marketplace models that invite independent app developers onto the truck.

M&A activity reshapes boundaries: Platform Science purchased Trimble’s telematics arm for USD 300 million to gain 1.3 million connected assets, while Powerfleet absorbed Fleet Complete for USD 200 million to secure 2.6 million subscribers. Meanwhile, Volvo Group and Daimler Truck formed Coretura an equal-stake venture that will deliver a standardized software-defined platform by 2030.

Competitive focus shifts toward intellectual property in cybersecurity and AI prognostics. USPTO filings on secure CAN-FD handshakes rose 38% year-on-year, indicating that code-signing and anomaly-detection engines will differentiate offers. Vendors also court electrification niches, where battery-specific analytics remain immature yet lucrative.

Commercial Vehicle Remote Diagnostics Industry Leaders

-

Continental AG

-

ZF Friedrichshafen AG

-

Daimler Truck AG

-

Cummins Inc.

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Platform Science has finalized the acquisition of Trimble's global transportation telematics business units, establishing a cohesive fleet management ecosystem. This integration generates approximately USD 300 million in annual revenue, with USD 200 million derived from recurring sources. Through this transaction, customers gain access to an expanded portfolio of applications via Platform Science's Virtual Vehicle platform.

- October 2024: Bosch has bolstered its diagnostics and workshop services for trucks and heavy vehicles by introducing three new offerings: the 3rd Generation KTS Truck, OHW 3 tailored for Material Handling Equipment, and a comprehensive Heavy Vehicle Training Program.

- September 2024: Cummins Inc, in collaboration with Bosch Global Software and India's KPIT, has unveiled the launch of 'Eclipse CANought'. This new open-source project, tailored for commercial vehicle telematics, will be integrated into the Eclipse Software Defined Vehicle project. This initiative aligns with the larger 'Open Telematics' movement, aiming to curtail the expenses associated with developing telematics applications for commercial vehicles.

- June 2024: Schmitz Cargobull acquired a majority stake in Atlantis Global System, a Spanish telematics specialist for refrigerated logistics, integrating AGS's capabilities with the TrailerConnect® platform to enhance cold chain monitoring solutions.

Global Commercial Vehicle Remote Diagnostics Market Report Scope

Commercial vehicle remote diagnostics leverages telematics to monitor, diagnose, and assess a vehicle's performance and health, while also identifying potential issues. This technology aids in minimizing downtime, enhancing vehicle safety, and fine-tuning fleet maintenance schedules. By facilitating real-time monitoring and early issue detection, remote diagnostics pave the way for proactive maintenance and timely repairs.

Commercial vehicle remote diagnostics Market is segmented component, vehicle type, application, end use and geography. Based on Component, the market is segmneted into Hardware, Software and Services. Based on Vehicle Type, the market is segmented into Light Commerical Vehicle and Heavy Commercial Vehicle. Based on Application, the market is segmented into Automatic crash notification, Vehicle tracking, Roadside assistance, Engine diagnostics and Others. Based on End use, the market is segmented into OEM and Aftermarket. Based on the geography, the market is segmented into the North America, Europe, Asia Pacific and Rest of the World. For each segment, market sizing and forecast have been done on the basis of value (USD).

| Hardware | ECUs and Sensors |

| Telematics Control Units | |

| Edge-AI Gateways | |

| Software | Diagnostic Protocol Stacks |

| Predictive Analytics Platforms | |

| Services | Managed Uptime Services |

| Integration and Consulting |

| Light Commercial Vehicles | Vans |

| Pick-ups | |

| Medium and Heavy Trucks | Class 4 to7 |

| Class 8 and Off-Highway Trucks |

| Automatic Crash Notification |

| Engine and Powertrain Diagnostics |

| Battery and Thermal Management (e-CV) |

| Roadside Assistance |

| OTA Software-Update Validation |

| Vehicle Tracking and Geofencing |

| OEM |

| Aftermarket / Fleet |

| Leasing and Rental Companies |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Hardware | ECUs and Sensors |

| Telematics Control Units | ||

| Edge-AI Gateways | ||

| Software | Diagnostic Protocol Stacks | |

| Predictive Analytics Platforms | ||

| Services | Managed Uptime Services | |

| Integration and Consulting | ||

| By Vehicle Type | Light Commercial Vehicles | Vans |

| Pick-ups | ||

| Medium and Heavy Trucks | Class 4 to7 | |

| Class 8 and Off-Highway Trucks | ||

| By Application | Automatic Crash Notification | |

| Engine and Powertrain Diagnostics | ||

| Battery and Thermal Management (e-CV) | ||

| Roadside Assistance | ||

| OTA Software-Update Validation | ||

| Vehicle Tracking and Geofencing | ||

| By End-use | OEM | |

| Aftermarket / Fleet | ||

| Leasing and Rental Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the commercial vehicle remote diagnostics market?

It stands at USD 7.07 billion in 2026 with an 11.39% CAGR outlook to 2031.

Which region leads the commercial vehicle remote diagnostics market?

North America leads with a 33.80% revenue share thanks to stringent EPA rules and early technology uptake.

How do 5G networks influence remote diagnostics?

5G slicing supplies reliable low-latency bandwidth that lets heavy trucks process diagnostic AI at the edge and transmit only prioritized alerts.

Why are leasing companies adopting remote diagnostics so quickly?

Uptime-linked contracts transfer maintenance risk to lessors, so predictive diagnostics reduce unplanned downtime and protect residual values.

Page last updated on: