Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

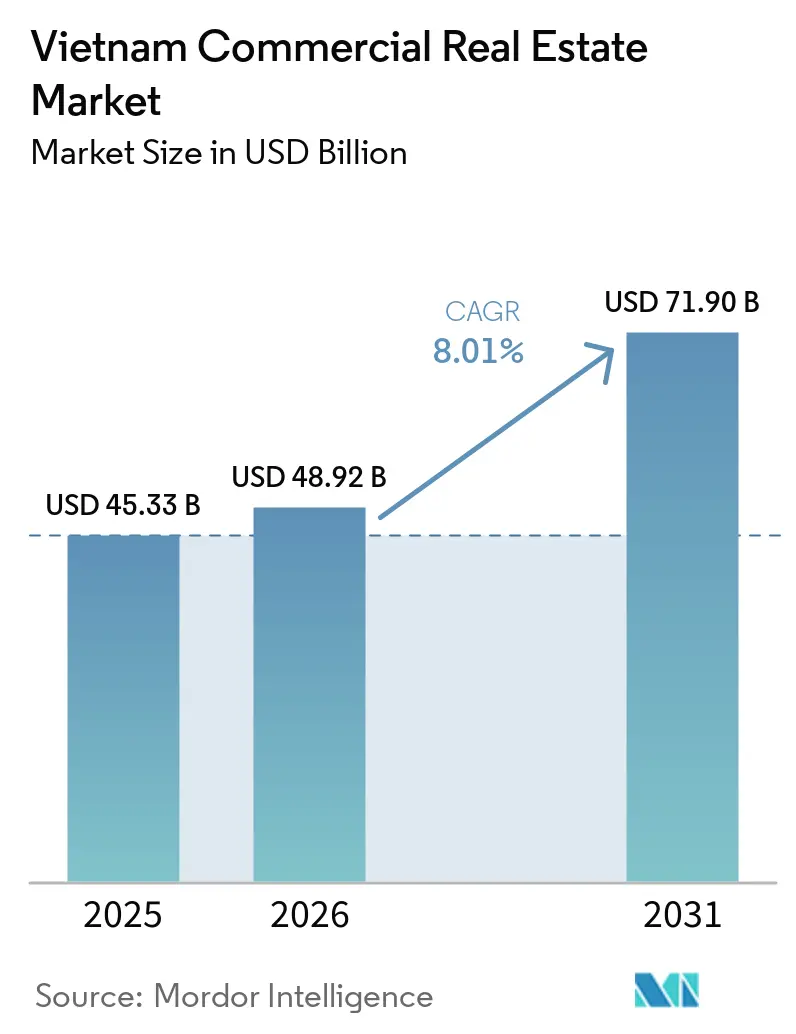

| Base Year Market Size (2025) | USD 45.33 Billion |

| Market Size (2026) | USD 48.92 Billion |

| Market Size (2031) | USD 71.90 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

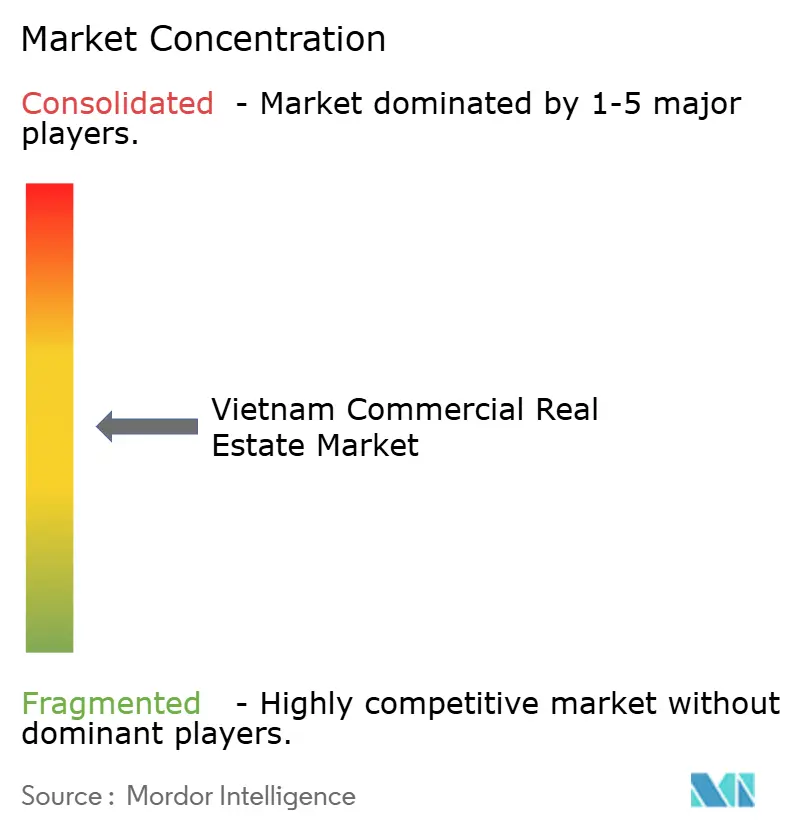

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Commercial Real Estate Market Analysis by Mordor Intelligence

The Vietnam commercial real estate market size is projected to be USD 45.33 billion in 2025, USD 48.92 billion in 2026, and reach USD 71.9 billion by 2031, growing at a CAGR of 8.01% from 2026 to 2031. Robust e-commerce growth, expressway and metro build-outs, and a steady rotation of institutional capital into core and decentralized office nodes are reinforcing demand for modern offices, data-center campuses, and Grade-A logistics parks.[1]Nguyen Pham, “Vietnam CRE 2025 Snapshot,” Bloomberg, bloomberg.com ESG regulations have become a mainstream catalyst, with LEED or LOTUS-certified assets collecting rental premiums of 8–12%. Meanwhile, hybrid work keeps CBD vacancy elevated, and construction-cost inflation is elongating project timelines, forcing developers to adopt forward-purchase strategies and modular methods to protect returns.

Key Report Takeaways

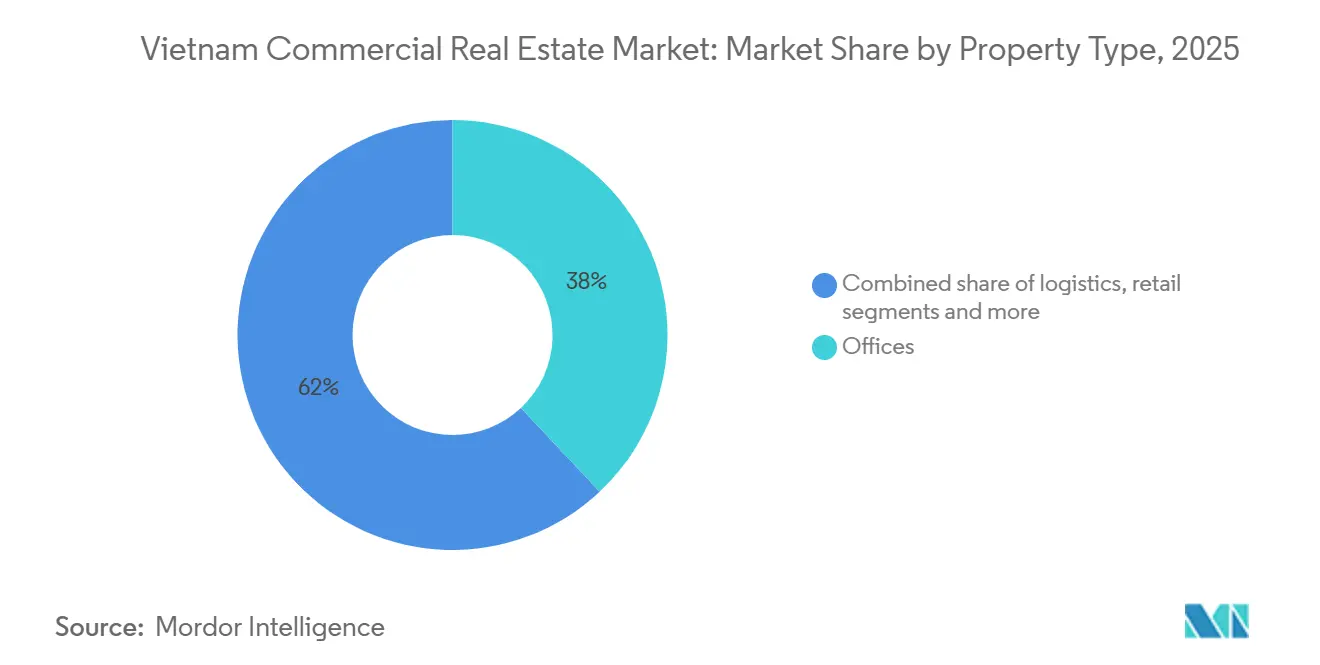

- By property type, offices held 38% of the commercial real estate market share in 2025, while hospitality is forecast to expand at a 9.1% CAGR through 2031.

- By business model, the rental segment controlled 61% of the commercial real estate market size in 2025; in contrast, the sales channel is projected to rise at a 10.33% CAGR over 2026–2031.

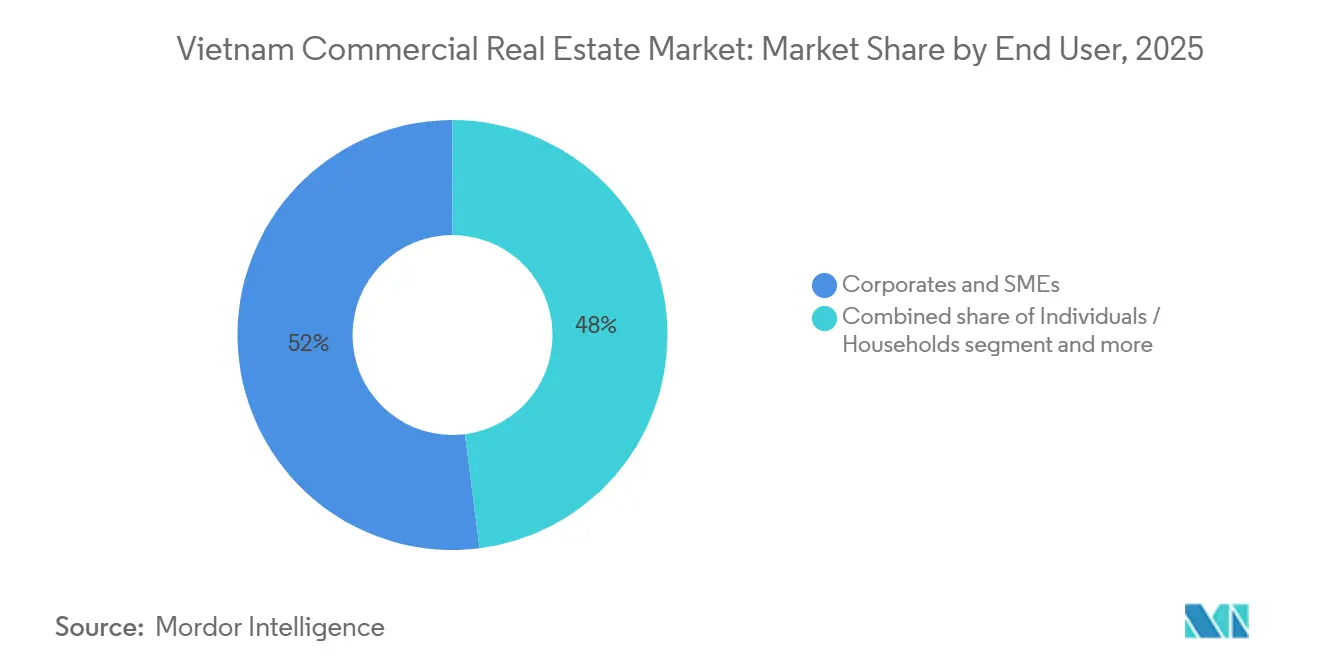

- By end-user, corporates and SMEs accounted for 52% of demand in 2025, whereas institutions and government entities represent the fastest-growing segment at a 9.1% CAGR through 2031.

- By geography, Ho Chi Minh City led with a 47% commercial real estate market share in 2025, but the rest of Vietnam is advancing at an 8.9% CAGR on the back of port-linked logistics investments

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-led surge for Grade-A industrial & logistics parks | +2.1% | Hai Phong, Binh Duong, Dong Nai, HCMC periphery | Short term (≤ 2 years) |

| Institutional capital rotation into core CBD & decentralized offices | +1.8% | Ho Chi Minh City, Hanoi, Binh Duong | Medium term (2–4 years) |

| Government expressway & metro pipeline uplifting corridor land values | +1.5% | National; early gains in HCMC Metro Line 1, North-South Expressway nodes | Long term (≥ 4 years) |

| ESG-compliant green buildings commanding premium rents | +1.2% | HCMC, Hanoi core districts | Medium term (2–4 years) |

| Tourism rebound revitalizing CBD hotel RevPAR | +0.9% | HCMC, Hanoi, Da Nang, Nha Trang | Short term (≤ 2 years) |

| Edge data-center campus rollout driven by data-localization laws | +0.6% | HCMC, Hanoi, Da Nang | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

E-commerce-Led Surge for Grade-A Industrial & Logistics Parks

Vietnam’s e-commerce gross merchandise value topped USD 20 billion in 2025, spurring demand for automated warehouses minutes from urban cores[2]Tran Dao, “E-Commerce Warehousing Boom,” Financial Times, ft.com. Frasers Property Industrial and Mapletree Logistics Trust pledged USD 600 million for 1.2 million sq m of Grade-A space across Hai Phong and Binh Duong, with pre-lease ratios above 70%. The North-South Expressway cuts Hanoi–HCMC transit times by 40%, enabling just-in-time inventory. Cold-chain mandates and fire-safety certifications from the Ministry of Industry and Trade are pushing landlords toward global standards.

Institutional Capital Rotation into Core CBD & Decentralized Offices

Japanese pension funds and Singaporean REITs have shifted from high-rise condos to Grade-A towers in Ho Chi Minh City’s District 1 and Hanoi’s Ba Dinh, chasing 6.8% yields despite hybrid-work drag. Vietnam Infrastructure Finance Company deployed USD 320 million across three office assets within its first year, validating newfound liquidity. Decentralized zones like Thu Dau Mot and Cau Giay attract back-office hubs that value lower rents and expressway proximity. This bifurcation has compressed CBD cap rates to 5.5% versus 7.2% in outer nodes, opening arbitrage for value-add plays. Institutional mandates now require ISO 50001 energy-management compliance before acquisition.

Government Expressway & Metro Pipeline Uplifting Corridor Land Values

The USD 12 billion North-South Expressway, on track for 2028 completion, has lifted land prices within 5 km of interchanges by up to 50% since 2024. Metro Line 1 in Ho Chi Minh City is triggering transit-oriented developments, while Ring Road 4 in Hanoi and Long Thanh Airport in Dong Nai are driving speculative industrial buys. Local governments fast-track land-use conversions for projects that promise LEED or LOTUS certification and job creation.

ESG-Compliant Green Buildings Commanding Premium Rents

LEED Gold or LOTUS-qualified towers earn 8–12% rent premiums and boast 98% occupancy. Saigon Centre Phase 2’s LEED Platinum rating illustrates early success, achieving USD 52 per m² monthly, well above sub-market averages. New codes effective 2025 require energy-performance certificates for buildings over 10,000 m², steering developers toward solar PV and smart HVAC. Institutional investors insist on ISO 14001 and ISO 50001 verification before closing deals.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-cost inflation & labor shortages delaying handovers | -1.1% | National; acute in HCMC and Hanoi | Short term (≤ 2 years) |

| Monetary tightening elevating cap rates & compressing deal volumes | -0.8% | National; large-ticket transactions | Short term (≤ 2 years) |

| Hybrid-work persistence curbing CBD office absorption | -0.7% | HCMC, Hanoi CBD districts | Medium term (2–4 years) |

| Rising climate-risk insurance premia for coastal assets | -0.3% | Da Nang, Nha Trang, Hai Phong coast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction-Cost Inflation & Labor Shortages Delaying Handovers

Steel and cement prices jumped 18% and 12% respectively in 2025, inflating budgets by nearly 20%. Skilled-labor migration to higher-wage markets has postponed large projects by up to nine months. Novaland reported penalties after two District 7 towers slipped schedules, underscoring delivery risk. Developers lock in materials through forward contracts and shift to modular techniques to contain overruns.

Monetary Tightening Elevating Cap Rates & Compressing Deal Volumes

Since early 2024, policy hikes have lifted borrowing costs by roughly 175 bps, widening spreads and pushing cap rates up 40–60 bps. Deal volumes for USD 100 million-plus assets fell 22% in 2025 as buyers reassessed hurdle rates. Sale-leasebacks provide liquidity to developers, but pricing power clearly favors cash-rich investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Data Centers Outpace Traditional Office Stock

Offices captured 38% of the commercial real estate market in Vietnam in 2025, reflecting entrenched corporate demand in District 1 and Ba Dinh[3]Dinh Hoang, “Data Centers Race Ahead,” Reuters, reuters.com. In contrast, data-center campuses are projected to grow at a 9.1% CAGR, the highest among all property types, buoyed by data-localization mandates and cloud uptake. CMC and Viettel IDC together pledged USD 800 million to hyperscale and edge facilities, targeting Tier III resilience and sub-10-ms latency benchmarks.

Occupiers value resilient power, neutrality, and ESG credentials, which justifies pre-leasing commitments above 70%. Retail malls pivot to experiential formats to combat e-commerce pressures, while logistics parks maintain 95% occupancy in zones like Deep C and VSIP III. Green retrofits, smart-building tech, and solar arrays are now standard features for core-grade office and logistics supply, underscoring the broadening sustainability imperative in the commercial real estate market in Vietnam.

By Business Model: Sales Channel Accelerates Amid Cap-Rate Volatility

Rentals dominated 61% of the commercial real estate market in Vietnam in 2025, anchored by REITs seeking stable yields. Yet the sales channel, led by strata-title offices and industrial land parcels, is expected to post a 10.33% CAGR through 2031. SMEs in districts like Cau Giap and District 7 favor asset ownership to hedge against rental escalation and interest-rate risk.

Sale-leasebacks worth USD 180 million by Becamex IDC and Nam Long exemplify hybrid financing, giving developers liquidity while preserving operational control. Institutional buyers secure long leases from credit-worthy tenants, insulating cash flows even as cap rates drift upward. The commercial real estate market in Vietnam thus balances rental annuities with ownership-led value-accretion strategies, dampening systemic risk.

By End-User: Institutions & Government Accelerate Infrastructure Mandates

Corporates and SMEs represented 52% of market value in 2025, but institutions and government entities are expanding at a 9.1% CAGR, the fastest among end-users. Ministries are pre-committing to logistics parks along the North-South Expressway, while state-owned enterprises anchor green office towers that fulfill ESG mandates. The commercial real estate market in Vietnam therefore benefits from sovereign balance-sheets that de-risk speculative supply.

SMEs prioritize flexible workspaces and suburban nodes for affordability and commute ease. Multinational tenants embed ESG clauses into leases, steering landlords toward LEED Gold or higher. These parallel demands compel diversified offerings—from CBD flagship towers to edge data centers—broadening absorption sources and cushioning cyclical volatility.

Geography Analysis

Ho Chi Minh City held 47% of the commercial real estate market in Vietnam in 2025, yet a 12.3% CBD vacancy shows that hybrid work and abundant Grade-B stock temper rent growth. New supply is gravitating to Thu Thiem, where metro connectivity and land availability enable smart, mixed-use districts and unlock incremental commercial real estate market size.

Hanoi combines government, diplomatic, and technology tenants, sustaining occupancy above 88% in Ba Dinh and Hoan Kiem. Peripheral districts such as Cau Giap attract shared-service centers, incentivized by expressway interchanges and lower rent. Meanwhile, Hai Phong is posting the fastest regional CAGR of 8.9%, supported by a deep-water port that handled 8.2 million TEUs in 2025 and extended expressway links that compress travel to Hanoi to under 90 minutes.

Binh Duong remains an industrial powerhouse; land prices have climbed 35% since 2024, and rental yields approach 8.5%. Da Nang diversifies from leisure into IT parks, though higher climate-risk insurance premia pressure margins. Secondary clusters across Can Tho, Nha Trang, and Vinh attract early movers who can navigate approvals, promising upside once expressway and airport extensions unlock accessibility.

Competitive Landscape

Competition is moderate, with the five largest developers controlling roughly 35% of new gross floor area, leaving headroom for niche and foreign players. Singaporean REITs such as Mapletree Logistics Trust and Frasers Property leverage low funding costs to acquire stabilized logistics assets; their scale and governance give them an edge in trophy bidding.

Japanese groups, including Mitsubishi Estate and Sumitomo Realty, co-develop metro-adjacent projects with Vietnamese partners, melding construction rigor with local land-bank access. Domestic champions like Vingroup and Sun Group exploit political ties and captive land banks to initiate large, mixed-use schemes near expressway nodes, accelerating pre-sales and raising entry barriers.

White-space segments—edge data centers, cold-chain logistics, self-storage—draw venture and private-equity interest. PropTech platforms digitize listings and transactions, while IoT-enabled smart-building systems enhance tenant experience and operational efficiency. Developers with diversified funding—bonds, REITs, and sale-leasebacks—are better positioned to navigate cap-rate expansion and construction-cost inflation.

Vietnam Commercial Real Estate Industry Leaders

Vingroup JSC

CapitaLand (Vietnam) Holdings

Keppel Land Vietnam

Sun Group

Novaland Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CapitaLand Investment and Vingroup formed a USD 420 million JV for a 45-story LEED Platinum complex in Thu Thiem, Ho Chi Minh City, with 60% of office space pre-let to tech and finance multinationals.

- December 2025: Frasers Property Industrial Vietnam bought 50 ha in Hai Phong’s Deep C Zone for USD 85 million to develop 250,000 m² of Grade-A logistics and cold-chain facilities, 70% pre-leased to DHL and Kerry Logistics.

- November 2025: Viettel IDC opened a 20 MW Tier III edge data-center campus in Da Nang to serve cloud and co-location clients needing sub-10-ms latency.

- October 2025: Mapletree Logistics Trust acquired a 180,000 m² park in Binh Duong’s VSIP III for USD 95 million, increasing its Vietnam footprint to 2 million m².

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we treat Vietnam's commercial real estate market as the yearly gross value of completed, income-producing properties, including offices, retail venues, logistics and industrial parks, hospitality assets, and purpose-built mixed-use complexes, sold or leased anywhere in the country.

Scope exclusion: raw land trades without approved construction plans and purely residential transactions remain outside this study.

Segmentation Overview

- By Property Type

- Office

- Retail

- Logistics/Industrial

- Hospitality

- By Business Model

- Sales

- Rental

- By End-User

- Individuals / Households

- Corporates & SMEs

- Institutions & Government

- By Region

- Ho Chi Minh City

- Hanoi

- Rest of Vietnam

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with commercial brokers, REIT portfolio managers, fit-out contractors, and municipal planning officers across Ho Chi Minh City, Hanoi, and emerging hubs such as Hai Phong. Their insights validated vacancy assumptions, typical rental yields, and pipeline schedules, filling gaps that desk sources leave.

Desk Research

Our analysts began with publicly available cornerstones such as the General Statistics Office of Vietnam, Ministry of Construction bulletins, customs import files for steel and cement, and the Vietnam Real Estate Association's quarterly trackers. Company 10-Ks, prospectuses, and capital-raising decks supplied transactional price ranges, while news archives in Dow Jones Factiva captured off-cycle deals and policy moves.

Macro drivers, including FDI inflows, industrial production, urban disposable income, and inbound tourism, were compiled from the World Bank, UNCTAD, and Civil Aviation Authority, then reconciled with province-level land bank disclosures and Questel patent trends on modular building systems. This list is illustrative; many other secondary inputs supported cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down production and trade reconstruction converts gross fixed capital formation in non-residential buildings into market value, while selective bottom-up roll-ups of Grade-A office towers and logistics parks stress-test totals. Key fingerprints, such as average rent per square meter, absorption rates, FDI-linked industrial land take-up, tourism room nights, and e-commerce parcel volumes, feed a multivariate regression that projects demand to 2030. Where sub-sector data are sparse, guided ranges from broker interviews bridge the gap before final triangulation.

Data Validation & Update Cycle

Outputs pass three-layer variance checks, peer review, and scenario testing. Reports refresh each year, with interim updates when material events trigger re-contact with experts, ensuring clients receive the latest view.

Why Mordor's Vietnam Commercial Real Estate Baseline Commands Reliability

Published figures often diverge because firms choose different asset mixes, rental multipliers, or refresh cadences, and we've observed such gaps widen after volatile years. We anchor our baseline on observed transactions and verified pipeline data, avoiding over-reliance on modeled asset inflation.

Key gap drivers include the exclusion of hospitality assets by some publishers, static exchange rates, or growth extrapolated from a narrow window, all of which inflate or suppress later-year totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 45.33 B (2025) | Mordor Intelligence | - |

| USD 19.83 B (2024) | Global Consultancy A | Narrow asset basket and conservative rent multiplier |

| USD 16.61 B (2024) | Industry Data Service B | Excludes hospitality assets and uses static 2019 exchange rate |

The comparison shows that by covering the full income-producing asset universe and updating annually, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

How large is the commercial real estate market in Vietnam in 2026?

The commercial real estate market size is expected to reach USD 48.92 billion in 2026.

Which property type is growing fastest through 2031?

Data-center campuses lead growth with a projected 9.1% CAGR, supported by data-localization rules and cloud demand.

Why is Hai Phong attracting more logistics investment?

Deep-water port upgrades and expressway links that cut Hanoi transit to under 90 minutes are driving an 8.9% CAGR in Hai Phong.

What premium do ESG-compliant buildings command?

LEED Gold or LOTUS-certified offices earn 8–12% higher rents than conventional stock.

How are developers coping with construction-cost inflation?

Firms pre-purchase steel and cement, adopt modular methods, and form joint ventures to share risk and ensure timely delivery.

What is the outlook for the sales versus rental business model?

Rentals remain dominant, yet the sales channel is forecast to grow at 10.33% CAGR as occupiers lock in long-term ownership amid cap-rate volatility.

Page last updated on: