Commercial Combi Ovens Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

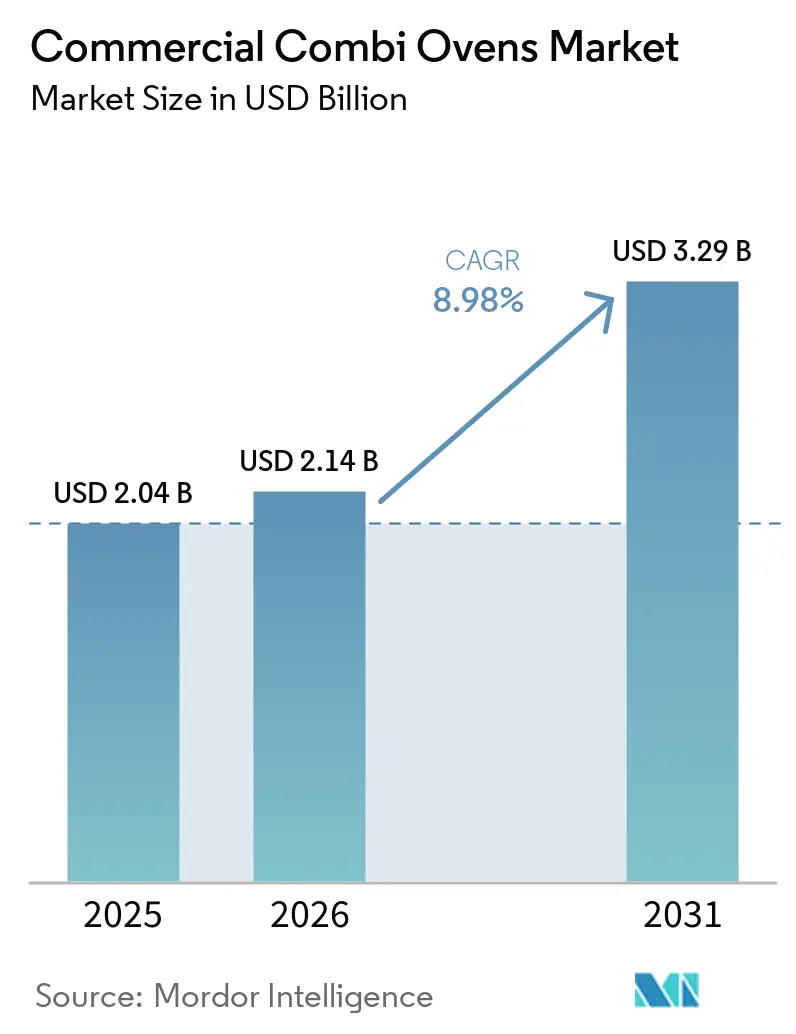

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.29 Billion |

| Growth Rate (2026 - 2031) | 8.98% CAGR |

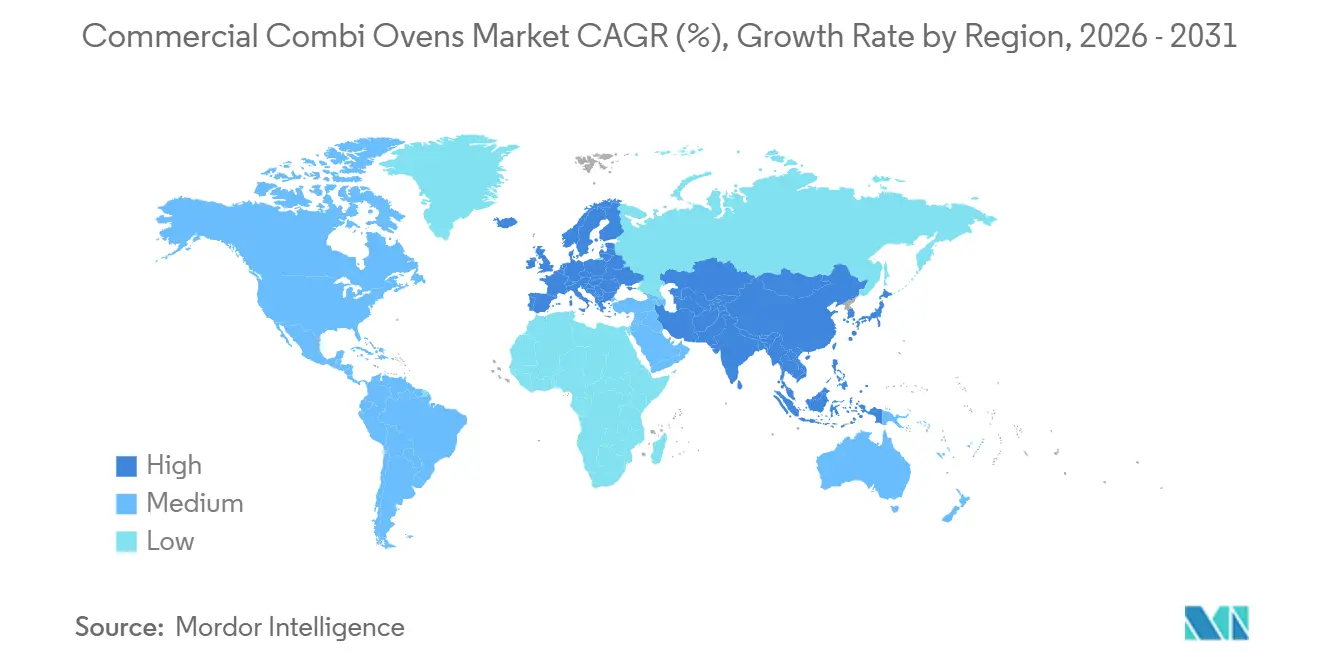

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

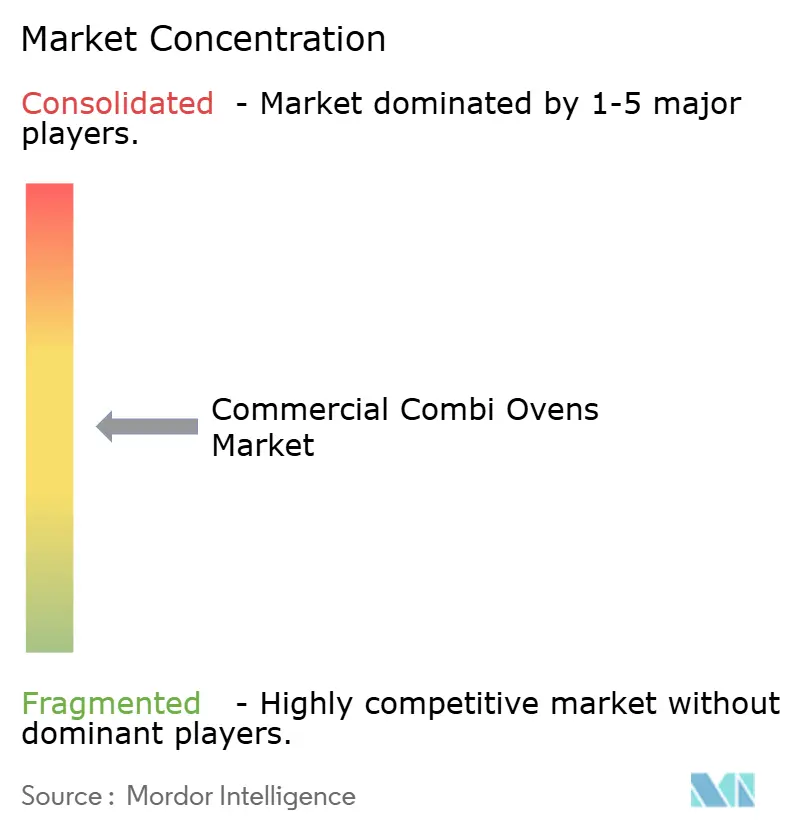

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Combi Ovens Market Analysis by Mordor Intelligence

The commercial combi ovens market size is projected to be USD 2.04 billion in 2025, USD 2.14 billion in 2026, and reach USD 3.29 billion by 2031, growing at a CAGR of 8.98% from 2026 to 2031. Structural shifts in how operators buy back-of-house equipment continue to accelerate adoption, as buyers respond to labor scarcity, stricter limits on fossil-fuel combustion in new builds, and the rapid growth of delivery-first kitchen formats. The commercial combi ovens market links energy efficiency with workflow gains, which helps operators compress payback windows when electrification replaces multiple single-function appliances. Technology adoption continues to shape competitive differentiation through IoT connectivity, cloud recipe management, and AI-assisted controls that simplify training and improve output consistency. Procurement models are also evolving, with equipment-as-a-service and manufacturer-backed leasing offering predictable monthly costs and vendor-managed maintenance, which appeals to public-sector buyers and multi-site operators. Regulatory actions in major cities and national associations’ advocacy for electric kitchens reinforce a multi-year shift toward electric, high-efficiency platforms that define the next phase of growth in the commercial combi ovens market.

Key Report Takeaways

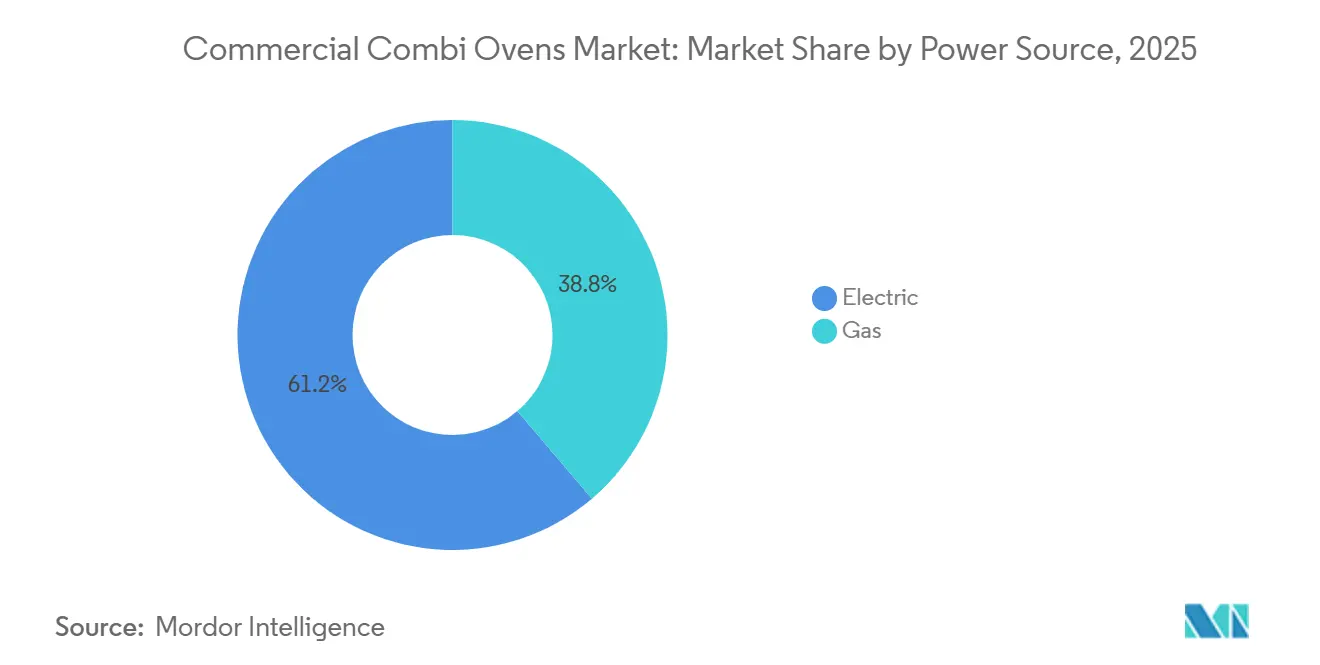

- By power source, electric models captured 61.23% of the revenue in 2025 and are projected to grow at an 8.65% CAGR between 2026 and 2031.

- By steam generation, boiler-based systems captured 56.62% of the revenue in 2025, and injector systems are projected to grow at a 9.15% CAGR between 2026 and 2031.

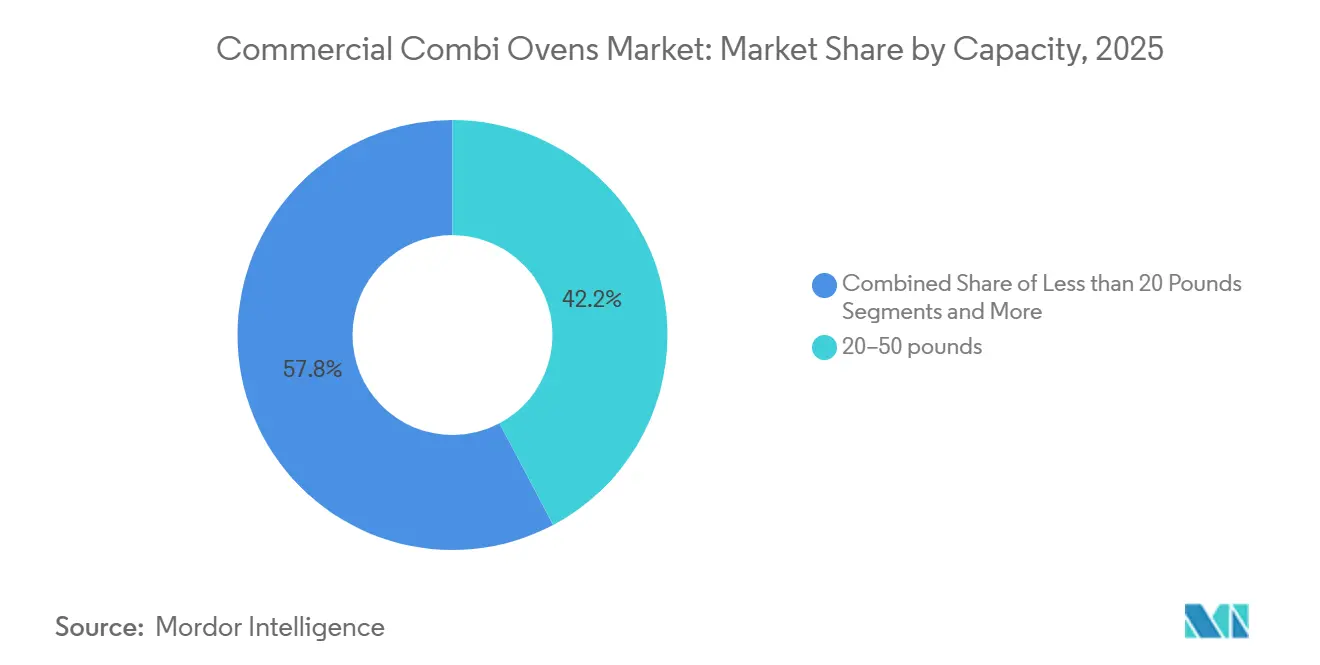

- By capacity, the 20-50 pound bracket captured 42.23% of the revenue in 2025, and sub-20 pound units are projected to grow at a 9.46% CAGR between 2026 and 2031.

- By installation type, floor-standing units captured 64.58% of the revenue in 2025, and counter-top configurations are projected to grow at a 10.21% CAGR between 2026 and 2031.

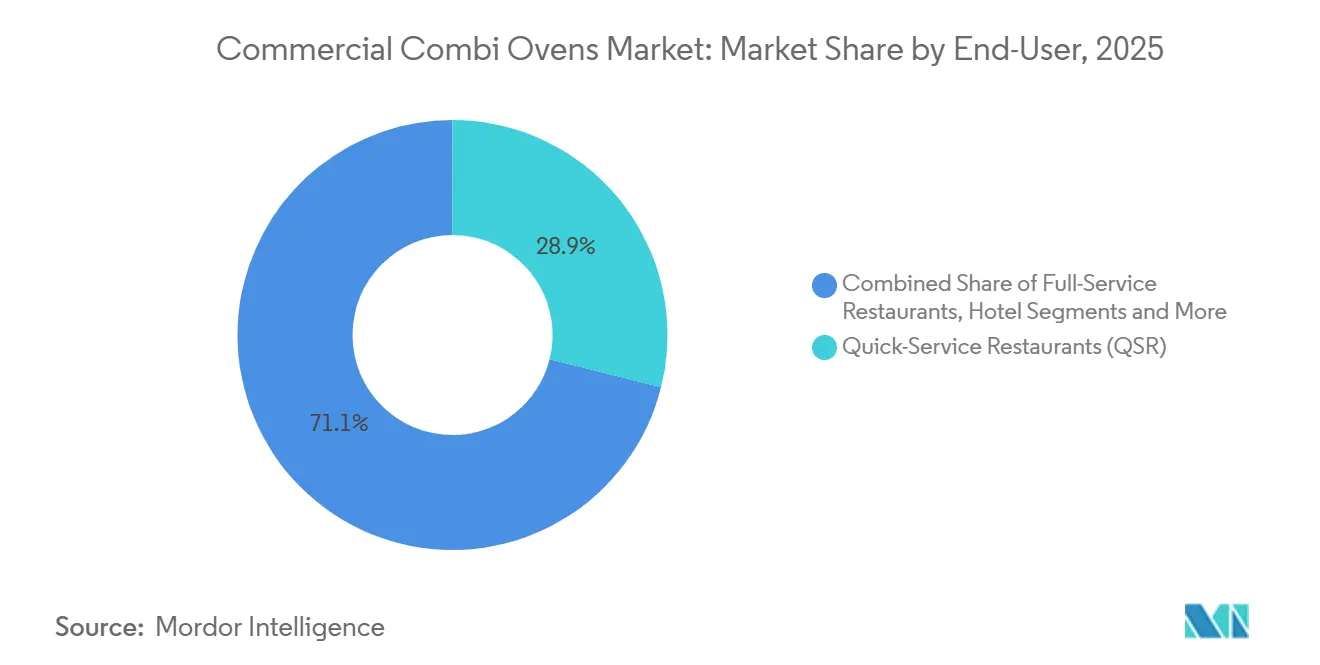

- By end-user, quick-service restaurants captured 28.95% of the revenue in 2025, and institutional catering is projected to grow at an 8.99% CAGR between 2026 and 2031.

- By geography, Europe captured 34.41% of the revenue in 2025 and Asia-Pacific is projected to grow at a 9.79% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Combi Ovens Market Trends and Insights

Drivers Impact Analysis*

| DRIVERS | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-driven kitchen retrofits | +2.1% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Growing ghost-kitchen and dark-store footprints | +1.8% | Asia-Pacific core with spill-over to North America | Short term (≤ 2 years) |

| Post-COVID labor shortage accelerating back-of-house automation | +2.3% | Global, acute in high-wage markets | Short term (≤ 2 years) |

| AI-enabled recipe optimization lowering skill barriers | +1.4% | Early adoption in North America and Europe | Medium term (2-4 years) |

| Regulations on gas cooking emissions | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Micro-financing apps for independent QSR equipment leasing | +0.9% | North America and Europe, emerging in India and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Driven Kitchen Retrofits Propel Electrification and Lifecycle-Cost Focus

Electrification momentum is building as operators integrate high-efficiency equipment to reduce energy use and meet building performance targets. In 2025, a UK hospitality organization study highlighted that electric cooking equipment can reach around 90% energy-use efficiency compared to 40-60% for gas, a differential that supports both operating-cost reduction and lower heat in work areas[1]UKHospitality, “Why the Future of Hospitality Kitchens Is Electric,” UKHospitality, ukhospitality.org.uk . The Sustainable Restaurant Association (SRA), the Global Cooksafe Coalition (GCC), and Hospitality Energy Saving and Sustainability (HESS) combined study found that all-electric kitchens in real-world sites delivered annual energy-cost savings between GBP 2,610 and GBP 8,839, energy-consumption cuts of 49-64%, and carbon-emissions reductions of 50-65%, with a payback of around three years and 10-year savings above GBP 65,000 for a modeled gastropub, reinforcing the total-cost-of-ownership case for integrated electric platforms. These outcomes align with the core value proposition of the commercial combi ovens market, as single multi-mode systems can replace multiple appliances, lighten hood loads, and support demand-controlled exhaust strategies. Public- and private-sector procurement frameworks increasingly emphasize lifecycle-managed contracts, preventive maintenance, and remote monitoring to preserve performance and energy savings over time, which syncs with connected combi systems and manufacturer service programs. In regions prioritizing net-zero pathways and green-building standards, high-efficiency combi platforms enable electrification without sacrificing menu range, which is a key decision factor for multi-site chains and institutional buyers.

Ghost-Kitchen Expansion Accelerates Demand for Compact, Multi-Brand-Capable Units

Delivery-first business models require equipment that supports high throughput in small footprints, consistent yields for packaging and holding, and fast changeovers across multiple virtual brands. Asia-Pacific shows the strongest momentum, with the dark-kitchen business expanding in China and India as platforms and operators scale delivery logistics and multi-brand operating models at speed[2]SIAL Network, “From App to Plate: The Global Business of Cloud Kitchens,” SIAL Network, sial-network.com. These kitchens prioritize flexible equipment that supports programmable cooking, cloud-managed recipes, and compact or stackable footprints that work in sites with limited hood positions, which aligns with new-generation counter-top combi configurations. Reduced front-of-house investment in delivery-only sites can shift more budget to automation and connected back-of-house systems, which shortens menu iteration cycles and promotes standardization across multiple brands. As the commercial combi ovens market evolves, compact designs with efficient clean cycles and quick pre-heats allow operators to reconfigure production between dayparts and to run diverse menus from a constrained line-up. Continuous expansion of delivery ecosystems in dense urban areas favors programmable, networked combi ovens that enable multi-brand execution with repeatability at scale.

Labor Scarcity and Wage Inflation Drive Automation and Skill-Agnostic Equipment

Operators in many high-wage regions are investing in connected systems that reduce the training burden and free staff for hospitality roles. A 2026 survey of U.S. operators shows a rise in technology adoption plans, with a significant share aiming to implement new systems to improve consistency across sites, coordinate labor, and integrate with analytics[3]Toast POS, “The State of the Restaurant Industry in 2026,” Toast, pos.toasttab.com . Combi ovens that manage temperature, humidity, and cook sequencing with programmable profiles reduce hands-on time and can integrate with predictive maintenance to avoid downtime shocks that disrupt revenue. For multi-location brands, the ability to distribute recipes remotely, log HACCP data, and update software across fleets supports standardized execution and higher asset availability, which aligns with ConnectedCooking and similar OEM platforms in the commercial combi ovens market. Automation spending has also benefited from vendor-backed financing and subscription models that align with operating budgets, allowing operators to upgrade without high upfront costs while maintaining service-level agreements for uptime. Adoption is most pronounced where labor costs and turnover pressures are greatest, which sustains demand for appliances that simplify tasks and deliver repeatable outcomes.

AI-Driven Recipe Optimization and Predictive Maintenance Lower Operational Complexity

Peer-reviewed research from early 2026 indicates that AI-driven adaptive control in thermal processing can reduce energy consumption meaningfully by replacing conservative setpoints with dynamic optimization, and that digital twins and physics-informed models help test load patterns and airflow movements virtually before implementation. As these techniques move into production settings, the commercial combi ovens market benefits from cloud-connected ecosystems that coordinate recipes, monitor asset health, and provide updates across fleets to preserve output consistency and reduce service incidents. Computer vision and spectroscopy are also being integrated to improve color and moisture detection, which supports uniform results in variable loading and packaging conditions, though field performance can vary with steam and lighting. Predictive maintenance using time-series models can reduce unplanned downtime, which is critical for multi-site operators that need to protect peak-time throughput. As connectivity expands, operators also weigh cybersecurity best practices, where sector guidance encourages network segmentation and anomaly detection to keep cooking controls resilient in connected kitchens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex vs. traditional convection ovens | -1.6% | Global, price-sensitive SMEs and emerging markets | Short term (≤ 2 years) |

| Persistent gas price volatility influencing OPEX planning | -0.7% | Europe, North America, Asia | Medium term (2-4 years) |

| Limited three-phase power availability in emerging markets | -1.1% | APAC excluding Japan and South Korea, Sub-Saharan Africa, parts of Latin America and MEA | Long term (≥ 4 years) |

| Data-security concerns around IoT-connected ovens | -0.4% | North America and Europe, with growing awareness in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital Cost Premium Versus Traditional Convection Platforms Constrains SME Adoption

Upfront prices for commercial combi ovens exceed those of traditional gas convection platforms, which pressures budgets for independent operators and smaller chains. Equipment financing can spread acquisition costs over 12-84 months, with terms and rates linked to credit profiles, and this can include Section 179 deductions and bonus depreciation mechanics that influence purchase timing in 2026 and 2027[4]Equinox Funding, “Equipment Financing Equinox Funding,” Equinox Funding, equinox-funding.com . Manufacturer-backed leasing and bundled connectivity subscriptions demonstrate new routes to adoption that wrap hardware, maintenance, and service into fixed monthly fees, and these programs are seeing early traction with public-sector and multi-site buyers that value predictability. UNOX has brought an all-inclusive leasing model to UK public-sector caterers that packages delivery, installation, scheduled maintenance, and warranty within a monthly payment, which highlights how the commercial combi ovens market is adapting procurement to budget cycles. For cost-sensitive operators, certified pre-owned supply offers a lower entry price with warranty coverage, although availability and performance consistency can vary by source and vintage, which continues to limit scale in some regions.

Three-Phase Electrical Infrastructure Gaps in Emerging Markets Delay Electrification Timelines

Grid-readiness issues in many fast-growing regions present practical barriers to full-electric kitchens, as sites face connection queues, limited amperage in older buildings, and upgrade costs that add time and capital to projects. Global analysis in 2026 points to the need for higher annual grid investment to support electrification, with greater emphasis on anticipatory planning horizons and network storage in order to keep pace with rising loads from buildings and transportation. In the commercial combi ovens market, the required dedicated circuits and breaker sizing for electric units can be difficult to accommodate without panel and service upgrades in certain geographies, which pushes some operators to retain gas models while they plan phased transitions. Where three-phase service is uncertain, or grid reliability is uneven, operators may prioritize models that can run within current constraints, adopt ventless or integrated-hood solutions, or schedule electrical work to align with lease renewals and remodel cycles. Harmonized specifications and programmatic procurement can help reduce connection and installation times, although execution varies by utility and jurisdiction. As policymakers and utilities implement targeted programs that accelerate commercial connections, the commercial combi ovens market is well-positioned to expand electrified footprints over multi-year timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Electrification Mandates and Efficiency Gains Tilt the Balance

Electric combi ovens accounted for 61.23% of 2025 revenue and are projected to expand at an 8.65% CAGR to 2031, supported by regulatory momentum and lifecycle-cost improvements that strengthen the value case in high-wage regions. The commercial combi ovens market is benefiting from city-level restrictions on new gas connections in several jurisdictions, which is concentrating new-build demand on electric platforms with advanced controls and cloud connectivity for fleet-wide standardization. Electric cooking is recognized for higher energy-use efficiency compared with gas, which reduces ambient kitchen heat and supports a better working environment that can improve staff retention in tight labor markets. As the commercial combi ovens market evolves, the ecosystem of connected services and remote monitoring supports uptime, compliance logging, and software updates, which aligns with the priorities of multi-location buyers that emphasize uniform execution.

Gas combi ovens retain a role in markets with low gas prices, established infrastructure, and culinary requirements that prefer flame or specific moisture dynamics, yet long-term regulatory uncertainty and cost variability are pushing many chains to plan for electrification. Product advances also show a pathway for future-proofing gas investments as energy systems evolve, including units that are designed to run on gas blends with hydrogen content in order to reduce emissions intensity in step with infrastructure changes. Maintenance profiles also differ, as gas units require flue management and periodic combustion checks, while electric platforms avoid flues and reduce indoor air pollutants, which can simplify compliance and operational routines in sensitive sites. In the commercial combi ovens market, the decision between electric and gas is increasingly grounded in lifecycle economics, local code requirements, and staffing priorities, with electric seeing broader preference in new-build and high-traffic chain locations. Where electrification remains phased, operators combine portable induction with compact combi ovens to reach targeted efficiency gains before a complete line conversion.

By Steam Generation: Injector Systems Gain Ground in Hard-Water Geographies and Efficiency-Focused Segments

Boiler-based steam generation held 56.62% of 2025 revenue based on a legacy preference for precise humidity control and strong steam output. The commercial combi ovens market has seen injector-based systems close the performance gap as manufacturers improve preheating, atomization, and steam modulation to enable precise setpoint control and faster responsiveness for varied cooking tasks. Injector systems generate steam on demand by spraying water onto hot surfaces, which reduces standby energy draw and lowers water use because there is no tank to maintain at a temperature. Operators in hard-water areas often favor injector designs because they avoid reverse-osmosis infrastructure, save space, and simplify upkeep by reducing scale formation, which can lower maintenance costs over time. Growth expectations reflect these usage advantages and a technology curve that is maturing at scale, supporting a 9.15% CAGR for injector systems through 2031 in the commercial combi ovens market.

Menu and site conditions still shape architecture choices. Seafood and shellfish production can expose injector components to corrosive residues that require adherence to cleaning routines, while high-volume batch work for precision applications may continue to lean on boiler-based systems in specific contexts. Across both architectures, site water testing and filtration guidance remain essential, with attention to chlorine or chloramine tolerances and deliming protocols. OEMs are also enhancing variable-speed fans and self-clean coverage to reduce downtime and extend intervals between service cycles, which supports throughput and asset availability across large fleets. The commercial combi ovens market continues to educate buyers on aligning steam architecture with menu mix, water quality, and maintenance capacity in order to sustain expected performance across the equipment lifecycle.

By Capacity: Sub-20 Pound Units Surge as Ghost Kitchens and Convenience Stores Prioritize Agility

The 20-50 pound capacity bracket led with 42.23% of 2025 revenue, reflecting the fit with standard QSR batch sizes and sheet-pan production. The commercial combi ovens market size for compact segments is set to expand as sub-20-pound systems post a projected 9.46% CAGR to 2031, supported by delivery-first operations, micro-format convenience sites, and multi-brand operators that value quick changeovers and small footprints. Counter-top models, such as 6-half-size configurations, allow 20-100 meals per day with flexible stacking, which supports throughput in tight kitchens without adding new hood positions or extensive upgrades. This agility lets ghost kitchens host multiple virtual brands and handle frequent menu changes without maintaining a large suite of single-function appliances. As a result, compact combi units with fast clean cycles and consistent yields see growing preference within the commercial combi ovens market.

Larger footprints retain importance in banqueting and institutional settings. Capacity bands of 50-100 pounds and above 100 pounds support large meal counts and multi-chamber processing, allowing high-throughput workflows that coordinate bulk retherming and finishing in constrained service windows. These units usually require dedicated three-phase electrical service or high-BTU gas connections, which limits adoption to sites designed for heavy production or to facilities undergoing major refurbishments. Software-enabled sequencing tools are also raising utilization in larger combi systems by synchronizing mixed loads to finish at the same time, which reduces idle time and energy waste across production cycles. In the commercial combi ovens market, capacity selection is now a holistic decision that balances menu diversity, packaging, and holding needs for delivery, installation constraints, and cleaning cycles to preserve uptime.

By End-User: Institutional Catering and QSR Lead Divergent Demand Trajectories

Quick-service restaurants accounted for 28.95% of 2025 demand, reflecting the large installed base and the need for standardized platforms that support multi-site rollout schedules. QSR kitchens use programmable profiles, fast heat-up times, telemetry, and automated cleaning to deliver consistent results while reducing training and manual intervention across shifts. The commercial combi ovens market is also benefiting from public-sector shifts, with institutional catering in hospitals, schools, and defense set to grow at an 8.99% CAGR to 2031 as procurement leans into lifecycle-managed leasing and high-efficiency specifications. UNOX’s fleX program offers all-inclusive monthly fees that bundle installation, scheduled maintenance, warranty coverage, and optional digital upgrades, which align with public-sector budgeting practices and service expectations. These models reduce upfront costs and align service responsibilities, which improves adoption prospects across distributed facilities.

Full-service restaurants, hotels, and resorts look for versatile systems that handle à la carte and banquet demands with humidity control, multi-sensor probes, and extensive recipe libraries. Bakeries and confectioneries emphasize even steam-proofing and dry-finish profiles for consistent viennoiserie and pastry outputs. Catering services and central kitchens require bulk preparation, flexible diet compliance, and coordinated staging that syncs with delivery time windows. In 2025, a leading commercial equipment supplier reported dealer-channel strength and broadening demand among independents, institutional customers, and fast-casual chains, which matches the adoption patterns observed across the commercial combi ovens market. With connected platforms and performance analytics now common in new rollouts, end-user groups are converging on similar requirements for standardization, uptime, and labor-light workflows.

By Installation Type: Counter-Top Configurations Accelerate as Space and Hood Constraints Intensify

Floor-standing units captured 64.58% of 2025 revenue due to their central role in full-service restaurants, hotels, institutional kitchens, and high-volume QSR locations. The commercial combi ovens market is now seeing counter-top configurations grow at a projected 10.21% CAGR to 2031, a trend tied to ghost kitchens, convenience formats, and operators planning around limited hood positions and electrical capacity. Compact designs with integrated or compatible venting reduce installation complexity and make it easier to maintain throughput in kitchens of 800-1,200 square feet, where reconfiguration can be expensive. Single-phase models broaden feasibility for older buildings while giving operators a path to electrification that aligns with lease schedules and cash flow. As the commercial combi ovens market expands, flexible installation options and ventless solutions enable phased deployment without full remodels.

Design advances are improving productivity in small footprints with dual-chamber and stackable countertop units that allow multi-processing without additional hood positions. Operators gain menu flexibility and can stage production to reduce bottlenecks, while integrated connectivity supports fleet standardization and remote diagnostics across dispersed sites. Differences in local code and hood requirements matter, so buyers coordinate early with electricians and HVAC contractors to avoid delays. Manufacturers are also refining accessories and condensation management to fit more use cases and to meet institutional procurement standards that emphasize safety, serviceability, and clear lifecycle costs. Together, these factors are expanding the role of counter-top systems and sharpening how the commercial combi ovens market addresses space and compliance constraints.

Geography Analysis

Europe led with 34.41% of global revenue in 2025, supported by sustainability mandates, structured public procurement, and strong multi-brand catering networks. The region’s associations actively track regulatory changes and product standards, helping manufacturers and buyers align on energy performance, materials, and compliance, which increases confidence in electrification investments across the commercial combi ovens market. UK Hospitality has highlighted the efficiency and work-environment gains from electric equipment, and 2026 guidance on electric kitchen savings has reinforced the case for transitions with tangible operational results. European OEMs continue to advance repairability and hydrogen readiness in gas-capable models, providing a bridge as infrastructure evolves and helping future-proof purchases under tightening emissions standards. The commercial combi ovens market size in Europe also benefits from tourism recovery and refurbishment cycles in hotels and foodservice chains that are standardizing on connected, multi-function platforms.

Asia-Pacific is set to post the fastest regional growth at a projected 9.79% CAGR through 2031, propelled by delivery ecosystems and urban density that demand compact, connected equipment. China remains a core market with technology-forward consumers and strong delivery penetration, while India’s young, mobile-first population is driving smart, multi-brand kitchen models that value space efficiency and standardized execution. Southeast Asian markets are seeing gains driven by urbanization and tourism, and demand for remote monitoring and predictive maintenance is rising as operators scale their footprints across cities and countries. Some near-term softness in parts of the region has not changed the longer-term pattern, where labor constraints and delivery growth continue to push fleets toward intelligent, multi-function ovens that use space and energy more effectively. As the commercial combi ovens market expands, regional tailoring of cost and feature sets provides a path to penetration in SME-heavy segments.

North America shows steady momentum in dealer channels and among independents, institutions, and fast-casual operators, with large QSRs pacing investments amid mixed macro signals in 2025-2026. Associations representing a large base of manufacturers engage with energy, environmental, and regulatory topics that shape training, product qualification, and operator confidence in adoption. At the city level, the acceleration of New York City’s Local Law 154 tightened exemptions for gas appliances in new buildings, which will concentrate upcoming projects on electric solutions and support a multi-year adoption curve for connected combi platforms in the commercial combi ovens market. In Canada, restaurant sales data and operator ROI guidance from equipment distributors indicate interest in high-efficiency ovens that compress payback windows and deliver quantifiable water and energy savings. Across Latin America, the Middle East, and Africa, adoption depends on electrical infrastructure and access to financing, with microfinance and leasing models emerging in some countries to support independent operators, while grid constraints in parts of MEA and APAC slow full electrification timelines. As the global commercial combi ovens market matures, regional differences in codes, infrastructure, and financing shape the pace and path of transitions.

Competitive Landscape

The commercial combi ovens market has moderate concentration with a leading European manufacturer reporting record global sales in 2025 and continued growth in combi and multifunctional lines, while still citing a large addressable base that uses traditional equipment. These dynamics leave room for regional specialists, equipment-as-a-service providers, and cost-optimized platforms aimed at small and medium operators in emerging markets. Strategic moves in early 2026 included a global OEM introducing a hydrogen-ready combi model with a top-tier repairability rating, showing a dual focus on future fuel blends and circular-economy design principles. Financing and leasing innovation is also notable, with manufacturer-backed programs that wrap connectivity subscriptions, preventive maintenance, and service under single monthly fees to remove upfront barriers for public-sector and multi-site adopters. These models align with the growing demand for predictable operating costs in the commercial combi ovens market.

In February 2026, a major U.S. equipment group sold a controlling stake in its residential kitchen business to refocus on commercial foodservice automation and related platforms, with proceeds earmarked for repurchases and capital structure optimization, and a planned separation of food processing to advance its pure-play strategy. The company’s 2025 financials showed solid performance in commercial foodservice with improved dealer-channel dynamics and resilience in independents and institutional customers, indicating healthy demand for connected, labor-saving equipment. Another OEM continued to scale connected-cloud ecosystems for fleet management, recipe distribution, HACCP logging, and software updates, creating recurring service revenue while helping operators manage consistency and compliance across large networks. In parallel, a complementary brand promoted AI-enabled optical sensing to automate load recognition and cooking, while integrating with cloud-based asset and menu management tools for portfolios ranging from single sites to large fleets. These developments illustrate how product and service differentiation are evolving in the commercial combi ovens market.

Smaller challengers are using regional manufacturing and nearshoring to reduce tariff risk and speed delivery, while building local service networks that compete on response times and total cost. Certification remains essential, including Energy Star qualification and adherence to performance standards that underpin many institutional procurement lists and chain specifications. As the commercial combi ovens market grows, product roadmaps emphasize connectivity, predictive maintenance, and AI-assisted cooking profiles, while service strategies prioritize uptime guarantees and clear lifecycle economics. This blend of technology and service supports buyer priorities across QSR, institutional, and hospitality segments where consistent output, compliance, and staff efficiency are core to return on investment. Leasing and subscription approaches are likely to deepen, particularly where public procurement or multi-site governance frameworks prefer predictable operating expenses to large capital allocations. Taken together, the competitive field is active, with incumbents and new entrants shifting from hardware-only propositions to integrated equipment-plus-services portfolios.

Commercial Combi Ovens Industry Leaders

Rational AG

Electrolux Professional AB

Welbilt (Convotherm)

Alto-Shaam Inc.

Unox S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Merrychef (Welbilt brand) launched a manufacturer-backed leasing solution for its conneX high-speed commercial ovens, offering fixed monthly payments for 3-5 year terms with no upfront deposit via Latitude Leasing, bundling equipment, service, preventative maintenance and Welbilt KitchenConnect connectivity subscription under a single agreement delivered by Merrychef's factory-trained engineer network.

- February 2026: Electrolux Professional launched the SkyLine Combi Oven with Platinum UL Solutions Repairability Rating, becoming the first foodservice company to participate in that accreditation process, and introduced 20% hydrogen-ready capability enabling operation with gas blends containing up to 20% hydrogen to future-proof kitchens against regulatory and infrastructure shifts away from natural gas.

- September 2025: UNOX launched fleX, an equipment leasing solution for UK public-sector caterers to access CHEFTOP-X, MIND.Maps PLUS and EVEREO commercial combi ovens via all-inclusive monthly fees starting at GBP 252.68 per month (USD 320) for 3-year terms, including delivery, installation, scheduled maintenance, comprehensive parts and labor warranty, technical assistance and optional Digital.ID Premium upgrades, distributed via partnership with Latitude Leasing.

Global Commercial Combi Ovens Market Report Scope

| Electric |

| Gas |

| Boiler |

| Injector |

| Less than 20 lbs |

| 20–50 lbs |

| 50–100 lbs |

| More than 100 lbs |

| Counter-top |

| Floor-standing |

| Quick-Service Restaurants (QSR) |

| Full-Service Restaurants |

| Hotels & Resorts |

| Bakeries & Confectioneries |

| Institutional Catering |

| Catering Services & Central Kitchens |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Power Source | Electric | |

| Gas | ||

| By Steam Generation | Boiler | |

| Injector | ||

| By Capacity | Less than 20 lbs | |

| 20–50 lbs | ||

| 50–100 lbs | ||

| More than 100 lbs | ||

| By Installation Type | Counter-top | |

| Floor-standing | ||

| By End-User | Quick-Service Restaurants (QSR) | |

| Full-Service Restaurants | ||

| Hotels & Resorts | ||

| Bakeries & Confectioneries | ||

| Institutional Catering | ||

| Catering Services & Central Kitchens | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the commercial combi ovens market?

The commercial combi ovens market size stands at USD 2.14 billion in 2026 and is forecast to reach USD 3.29 billion by 2031, registering an 8.98% CAGR over 2026-2031.

Which power source is leading adoption in commercial combi ovens and why?

Electric models led with 61.23% of 2025 revenue and are projected to grow at 8.65% CAGR (2026-2031) due to higher energy-use efficiency, better kitchen conditions, and alignment with electrification mandates and lifecycle-cost priorities.

Which installation type is growing fastest and in what settings?

Counter-top configurations are the fastest growing at a projected 10.21% CAGR (2026-2031) as ghost kitchens, convenience formats, and sites with limited hood capacity prioritize compact, vent-compatible designs.

Which end-user segments are most important for near-term demand?

Quick-service restaurants held 28.95% of 2025 demand, while institutional catering is set to grow at 8.99% CAGR due to lifecycle-managed leasing and energy-efficiency requirements in hospitals, schools, and defense facilities.

What regions are driving future growth in the commercial combi ovens market?

Asia-Pacific is projected to lead growth at 9.79% CAGR through 2031, supported by delivery ecosystems and urbanization, while Europe remains the largest region by 2025 share due to sustainability mandates and mature procurement frameworks.

How are OEMs competing in the commercial combi ovens industry beyond hardware?

Leading OEMs are bundling connectivity, recipe libraries, predictive maintenance, and leasing into integrated offerings that deliver predictable operating costs and reduce downtime, which supports multi-site standardization and compliance.

Page last updated on: