Home and Property Improvement

9th JuneA Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

The Pizza Ovens Market Report is Segmented by Product Type (Brick Ovens, Clay Ovens, Deck/Stone Ovens, Conveyor Ovens, and More), Fuel Type (Wood-Fired, Gas-Fired, Electric, and More), End-User (Residential, Commercial), Distribution Channel (Offline, Online), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

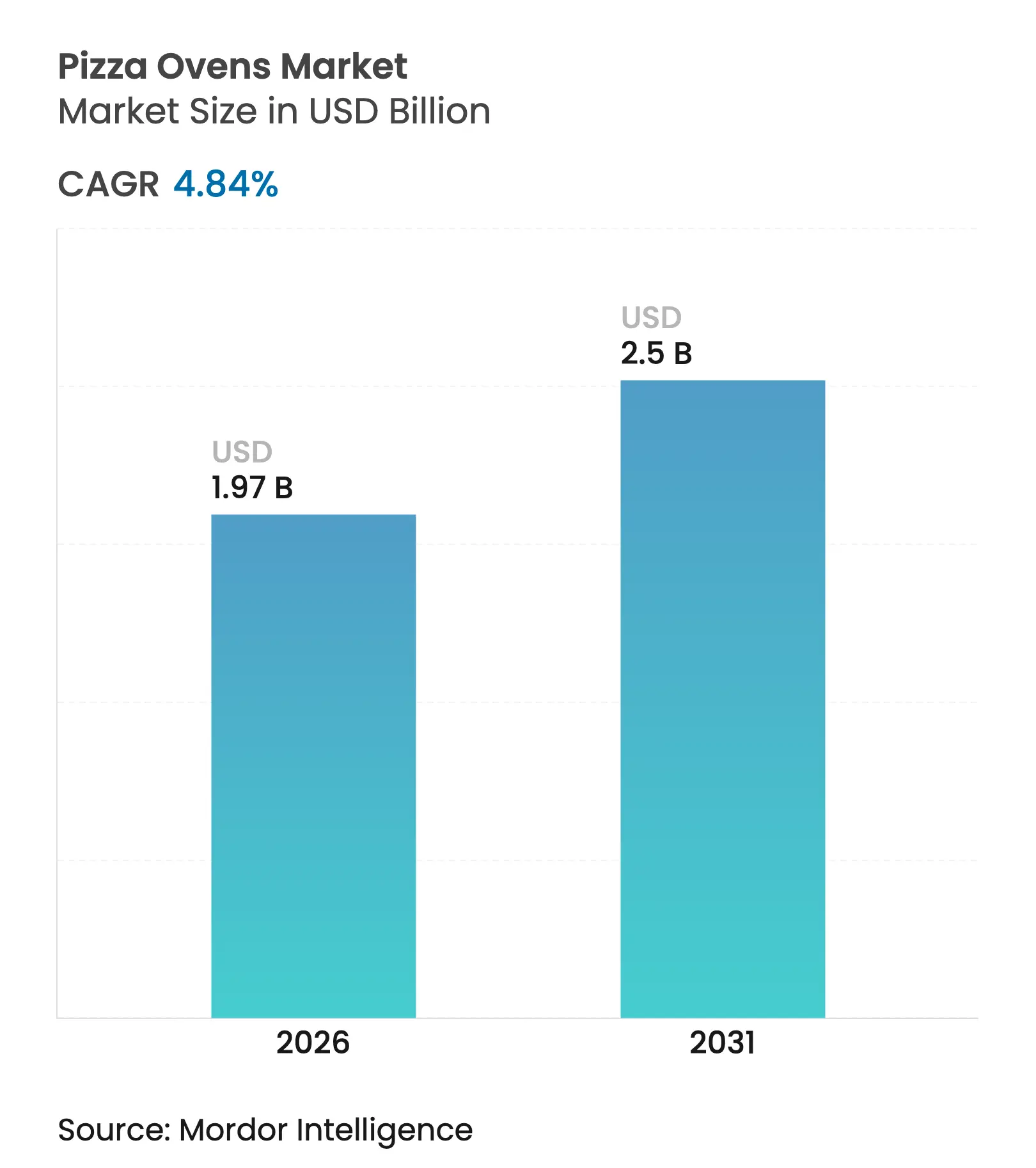

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.5 Billion |

| Growth Rate (2026 - 2031) | 4.84 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The pizza ovens market size was valued at USD 1.88 billion in 2025 and estimated to grow from USD 1.97 billion in 2026 to reach USD 2.5 billion by 2031, at a CAGR of 4.84% during the forecast period (2026-2031). Consumer appetite for at-home gourmet cooking, the rebound in food-service openings, and steady upgrades to energy-efficient equipment collectively underpin this expansion. Demand also benefits from outdoor living investments that boost property resale values, while city-level incentives for low-emission appliances accelerate electric-oven adoption. On the supply side, scale players are integrating Internet-of-Things (IoT) controls, predictive maintenance features, and hybrid fuel systems to differentiate offerings. Raw-material volatility for refractory components remains a watch item, yet larger manufacturers are partially insulating margins through multi-year supply contracts and regional sourcing strategies.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growth of the food-service sector

Growth of the food-service sector

| +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% |

Geographic Relevance

:

Global, with concentration in North America and

Asia-Pacific

|

Impact Timeline

:

Medium term (2-4 years)

|

Technological innovation in oven design and energy

efficiency

Technological innovation in oven design and energy

efficiency

| +0.8% | Global, led by North America and Europe | Long term (≥ 4 years) | |||

Expansion of fast-casual pizza chains and QSR formats

Expansion of fast-casual pizza chains and QSR formats

| +1.0% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) | |||

Residential demand for outdoor/portable ovens

Residential demand for outdoor/portable ovens

| +1.3% | North America, Europe, and emerging Asia-Pacific markets | Short term (≤ 2 years) | |||

Ghost-kitchen adoption of compact high-speed deck ovens

Ghost-kitchen adoption of compact high-speed deck ovens

| +0.7% | Urban centers globally, concentrated in North America and Asia-Pacific | Medium term (2-4 years) | |||

City-level incentives for switching to low-emission

electric ovens

City-level incentives for switching to low-emission

electric ovens

| +0.6% | North America and Europe, with selective Asian cities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growth of the Food-Service Sector

Restaurant construction pipelines and reopening programs are lifting equipment‐replacement cycles, creating a direct pull-on commercial pizza oven. Fiscal-year 2024 filings from Williams-Sonoma show robust demand for premium cooking appliances even as broader retail sales cooled, illustrating how operators and consumers prioritize high-quality equipment to offset labor constraints and energy costs[1]Source: Investor Relations, “Williams-Sonoma Fiscal 2024 Results,” Williams-Sonoma, williams-sonomainc.com.

Technological Innovation in Oven Design and Energy Efficiency

Manufacturers are embedding Wi-Fi modules, Bluetooth sensors, and cloud analytics to automate temperature profiles and remote diagnostics. The U.S. Environmental Protection Agency has established alternative control technologies for bakery oven emissions, including pizza ovens, which drive innovation in cleaner-burning systems[2]Source: Environmental Protection Agency, “Alternative Control Techniques for Bakery Oven Emissions,” epa.gov . Advanced insulation materials and heat recovery systems are becoming standard features, enabling operators to reduce energy consumption while maintaining cooking performance.

Expansion of Fast-Casual Pizza Chains and QSR Formats

Franchise rollouts emphasize speed, unit economics, and standardized output. BurgerFi's acquisition of Anthony's Coal Fired Pizza for USD 161.3 million in June 2024 demonstrates the sector's consolidation and the value placed on specialized cooking equipment, with Anthony's signature 900-degree coal-fired ovens being a key asset. The segment's growth creates demand for compact, high-speed deck ovens for ghost kitchen applications, where space efficiency and throughput optimization are critical success factors[3]Source: Investor Relations, “BurgerFi Holdings Inc. Investor Presentation 2025,” burgerfi.com. Conveyor ovens dominate this segment due to their ability to produce consistent results with minimal operator skill requirements.

Residential Demand for Outdoor/Portable Ovens

Post-pandemic lifestyle patterns cemented pizza ovens as a status kitchen amenity. Zillow-linked data show listings mentioning pizza ovens command a 3.7% premium, incentivizing homeowners to add outdoor cooking spaces. Portable models satisfy urban dwellers who seek restaurant-quality crusts without permanent masonry builds.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High upfront cost of commercial pizza ovens

High upfront cost of commercial pizza ovens

| -0.9% | Global, particularly affecting small operators | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Global, particularly affecting small operators

|

Impact Timeline

:

Short term (≤ 2 years)

|

Competition from multifunction combi and convection ovens

Competition from multifunction combi and convection ovens

| -0.6% | Global, strongest in cost-sensitive markets | Medium term (2-4 years) | |||

Stricter particulate-emission rules for wood-/coal-fired

ovens

Stricter particulate-emission rules for wood-/coal-fired

ovens

| -0.4% | North America and Europe, selective Asian cities | Long term (≥ 4 years) | |||

Supply-chain tightness for refractory bricks and

cordierite stone

Supply-chain tightness for refractory bricks and

cordierite stone

| -0.3% | Global, with China supply concentration risks | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Cost of Commercial Pizza Ovens

Independent restaurateurs often defer purchases that exceed USD 15,000 per unit, tightening access to premium models. Leasing plans and revenue-share agreements have emerged as hedges, although elevated credit costs in 2025 curtail finance uptake. The cost barrier creates opportunities for refurbished equipment markets and drives demand for multi-functional units that can justify higher upfront investments through expanded menu capabilities.

Competition from Multifunction Combi and Convection Ovens

Operators in emerging markets opt for combi ovens that cover baking, steaming, and roasting, eroding potential share for specialized pizza equipment. Manufacturers counter by promoting deck-oven versatility for flatbreads, roasted vegetables, and desserts. Manufacturers are responding by developing cleaner-burning technologies and emission control systems, while operators are evaluating transitions to electric and gas-fired alternatives that meet regulatory requirements without compromising cooking performance.

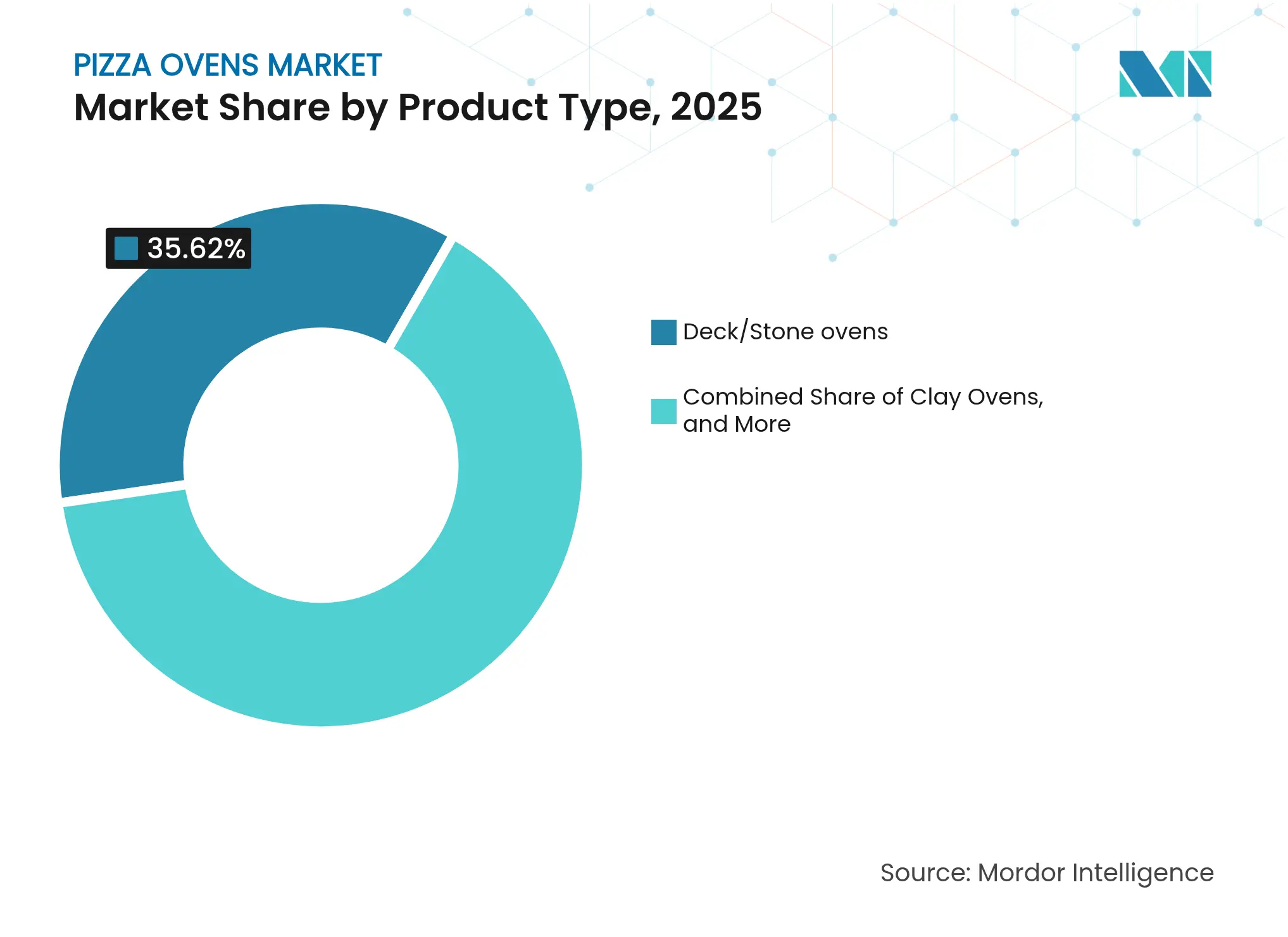

By Product Type: Deck Ovens Hold Sway Amid Portable-Oven Uptick

Deck/stone units retained 35.62% of the pizza ovens market in 2025, favored for their even thermal mass and ability to replicate artisanal wood-fired crusts. Many models now include digital thermostats and self-diagnostic kits to cut downtime. Counter-top and portable designs clock a 8.92% CAGR through 2031, reflecting urban kitchens’ need for compact, quick-heat solutions. Hybrid-kit variants let homeowners assemble brick-look finishes around factory-built cores, marrying aesthetics with regulated combustion chambers. Conveyor systems dominate high-volume, fast-casual chains thanks to continuous belts that deliver 200-plus pies per hour.

High-speed smart ovens remain niche yet influential: their infrared elements and algorithm-driven airflow finish Neapolitan pies in under two minutes, offering ghost kitchens a means to expand pizza menus without dedicated staff. Brick ovens, priced at a premium, retain prestige appeal in fine-dining venues, although stricter smoke codes in metro zones could cap their future growth.

Note: Segment shares of all individual segments available upon report purchase

By Fuel Type: Gas Leads While Electric Gains Momentum

Gas-fired models occupied 46.27% of the pizza ovens market size in 2025, buoyed by existing pipeline infrastructure and operators’ familiarity with gas burners. The Associazione Verace Pizza Napoletana certifies both gas and wood-burning ovens for authentic Neapolitan pizza production, with gas systems operating at approximately 900°F and requiring specific equipment specifications. Electric systems, expanding at 11.05% CAGR, leverage rapid coil response and precise PID controls to slash warm-up times by up to 30%. Utilities highlight off-peak tariffs that lower operating expenditure, and carbon-credit programs in California provide incremental savings that nudge purchasing decisions.

Wood-fired units retain premium cachet, but operators must now integrate insulated flues and real-time particulate monitors. Dual-fuel hybrids merge gas convenience with occasional wood-smoke infusion; interest is particularly high among suburban homeowners. Pellet-burning models straddle regulatory and flavor demands, logistics of pellet supply can limit adoption in remote geographies.

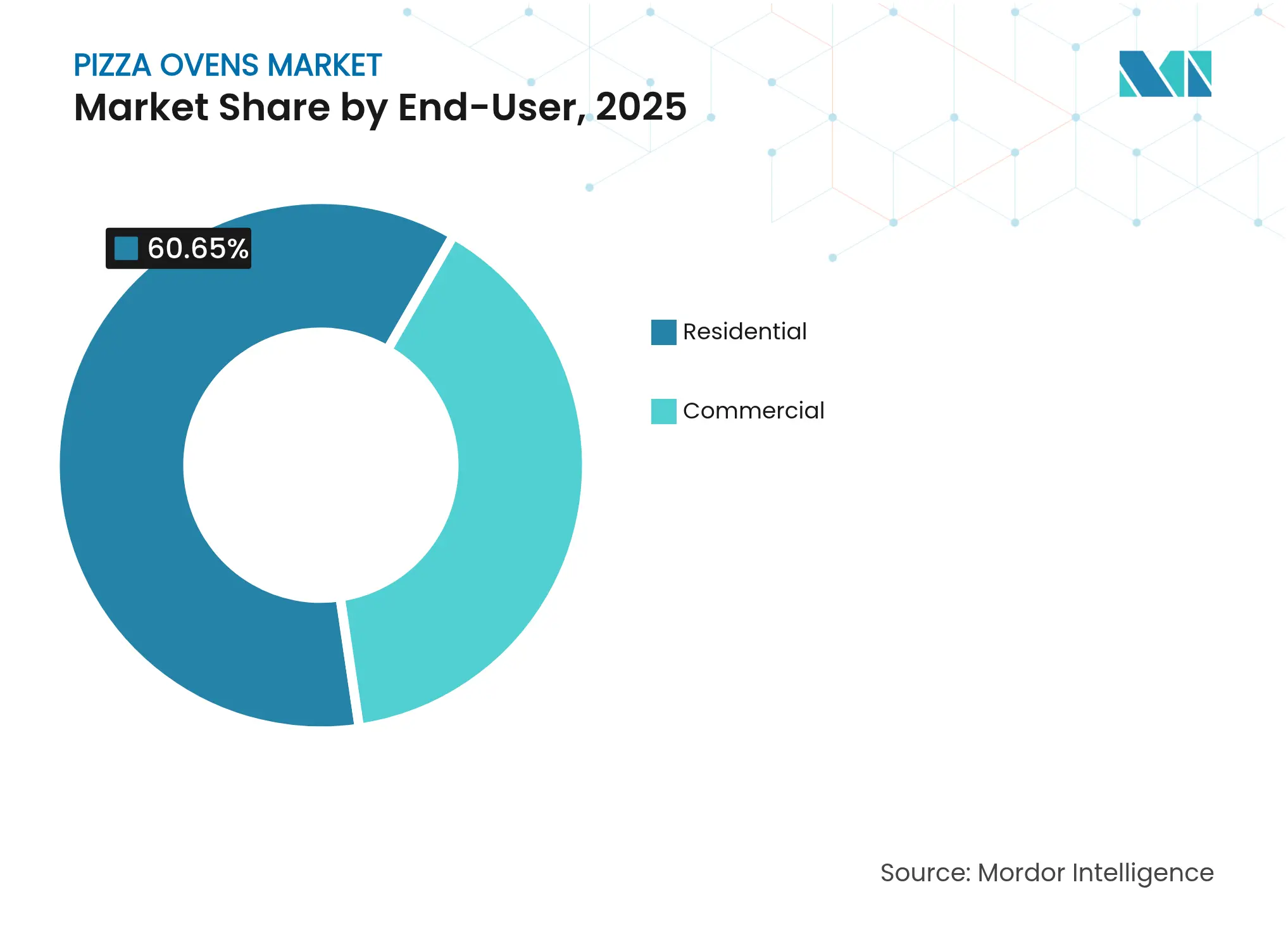

By End User: Residential Dominance With Commercial Acceleration

Residential buyers represented 60.65% of the pizza ovens market in 2025, an outcome of pandemic-era cooking enthusiasm and outdoor kitchen upgrades. Interior models with integrated ventilation allow apartment dwellers to enjoy high-heat baking without rooftop ducts. Commercial demand is growing faster at 9.92% CAGR, catalyzed by fast-casual outlets and ghost kitchens that prize modular, stackable decks. Food trucks favor 16-inch gas or dual-fuel portables weighing under 80 lb to meet mobility codes. Hospitality venues such as resorts are commissioning showcase ovens clad in mosaic tiles to elevate guest experiences and live-cooking theatrics.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Offline Advisory Strength Meets Digital Surge

Specialty brick-and-mortar retailers held a 53.88% share in 2025, offering live-fire demos that aid big-ticket conversions. Professional HoReCa dealers bundle after-sales maintenance, an important factor for operators subject to health department inspections. Online sales, advancing at 10.58% CAGR, draw strength from detailed comparison grids and user-generated recipe libraries.

Manufacturer-direct e-commerce bypasses traditional markups, although last-mile logistics for 400-lb units remain a hurdle. Big-box chains leverage omnichannel inventories, enabling click-and-collect for mid-range models. Channel evolution reflects changing consumer behavior and manufacturers' strategies to optimize reach and profitability across diverse market segments. Distributor e-stores represent a hybrid approach that combines online convenience with specialized expertise, appealing to professional buyers who value both digital efficiency and technical support capabilities.

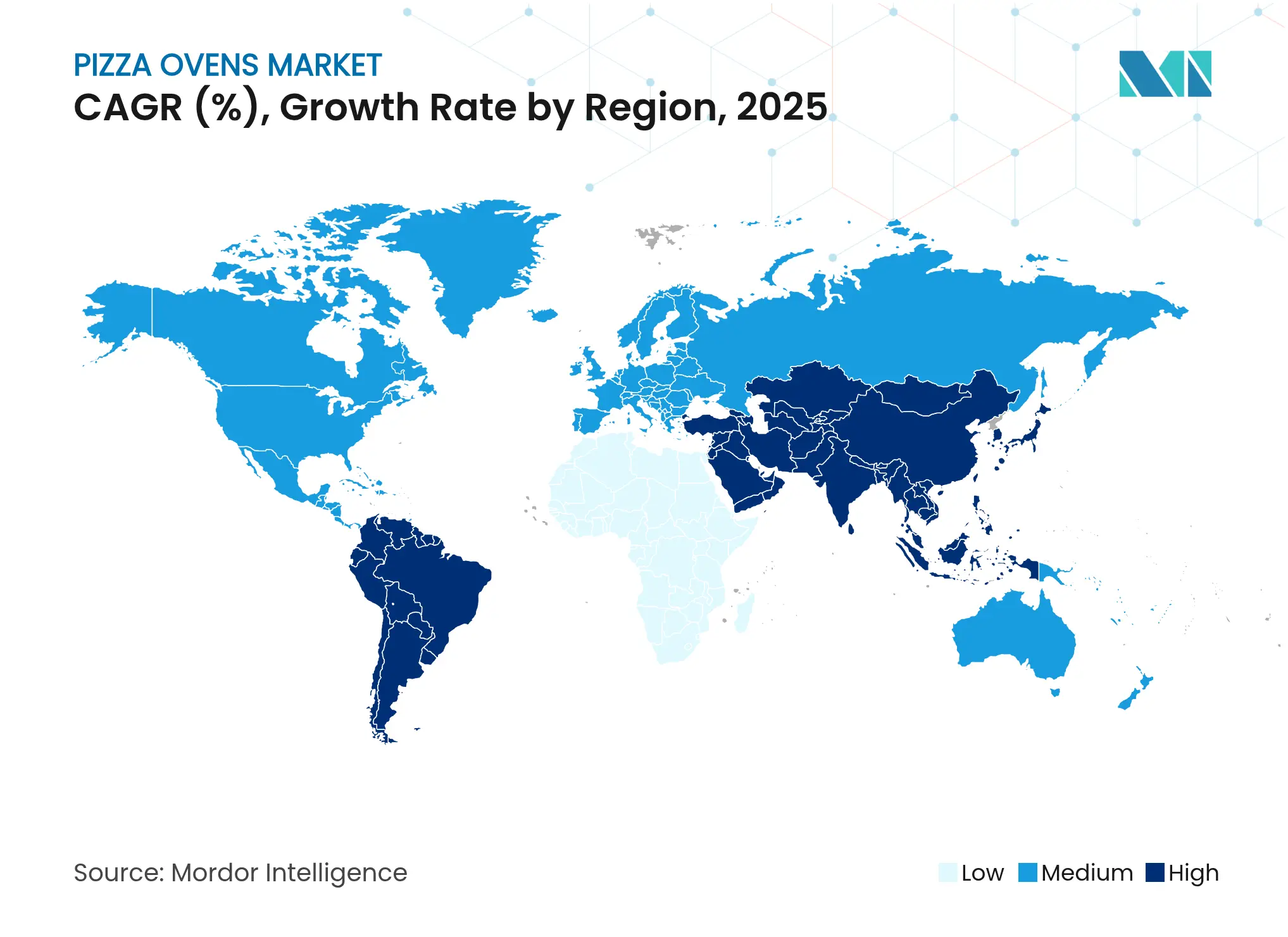

North America accounted for 42.05% of the pizza ovens market in 2025 and continues to benefit from mature replacement cycles, high disposable incomes, and a well-established outdoor cooking culture. State rebates for energy-efficient appliances and rigorous safety codes also favor sales of next-generation electric and hybrid units. The region’s pizza ovens market size is expected to progress steadily at 3.92% CAGR as suburban remodeling activity underpins residential installs.

Asia-Pacific, projected to expand at 11.01% CAGR, is reshaping the competitive order. Rapid urbanization, growing middle-class spending, and aggressive quick-service restaurant additions generate sizable volume demand. Commercial operators in Japan and South Korea lean toward compact deck ovens with automated conveyor loaders to compensate for high wage costs, while Indian households gravitate to dual-fuel models that accommodate tandoor-style flatbreads alongside pizzas. Supply-chain proximity to refractory plants in Shandong Province offers cost advantages but exposes OEMs to export-control shifts.

Europe remains a regulation-driven market where energy-labeling rules nudge commercial kitchens toward high-efficiency electric decks. Italy’s culinary heritage sustains demand for traditional dome brick ovens, whereas Scandinavian countries prioritize pellet-burning systems paired with catalytic converters to meet particulate thresholds. Middle East & Africa and South America collectively account for less than 10% of current value but present upside through tourism‐led hotel projects and rising urban fast-food concepts.

Market Concentration

Market leadership is moderately fragmented, with the top five suppliers holding a significant share of the market. These firms increasingly package ovens with digital controls, recipe databases, and predictive-maintenance dashboards to lock in service contracts and elevate switching costs. In February 2024, Middleby Corporation broadened its European footprint by acquiring GBT GmbH Bakery Technology, adding tunnel-oven and conveyor expertise that complements its commercial pizza range.

Private-equity interest continues: Brynwood Partners’ 2024 purchase of Miracapo Pizza Company expanded its vertically integrated network to 19 facilities, underscoring the strategic value of upstream dough-production capabilities. Product-led disruptors, notably outdoor-focused Ooni, rely on direct-to-consumer channels and influencer campaigns to scale rapidly in the premium residential space. Larger incumbents respond by launching quick-build modular kits and forming joint R&D hubs with refractory suppliers to accelerate time-to-market for low-emission designs.

Supply-side bargaining power remains balanced. OEMs must navigate input inflation for steel and fire-clay bricks yet benefit from multi-year service contracts that secure recurring revenue. End users hold sway in highly competitive commercial tenders, whereas residential consumers exhibit brand loyalty once post-purchase satisfaction is established through recipe communities and warranty support.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Pizza ovens are designed to evenly bake pizzas, ensuring both the top and bottom achieve the perfect texture. These ovens harness and retain high heat, resulting in a crispy crust. This method also ensures that vegetable and meat toppings are cooked optimally, minimizing the risk of burning.

The pizza oven market is segmented into product type, fuel type, end-user, distribution channel, and region. By product type, the market is segmented into brick ovens, clay ovens, conveyor ovens, and others. By fuel type, the market is segmented into wood-fired pizza ovens, gas-powered pizza ovens, electric pizza ovens, and dual-fuel pizza ovens. By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into online and offline channels, and by geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report offers market size and forecasts in terms of value (USD) for all the above segments.

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.