Commercial Microwave Ovens Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

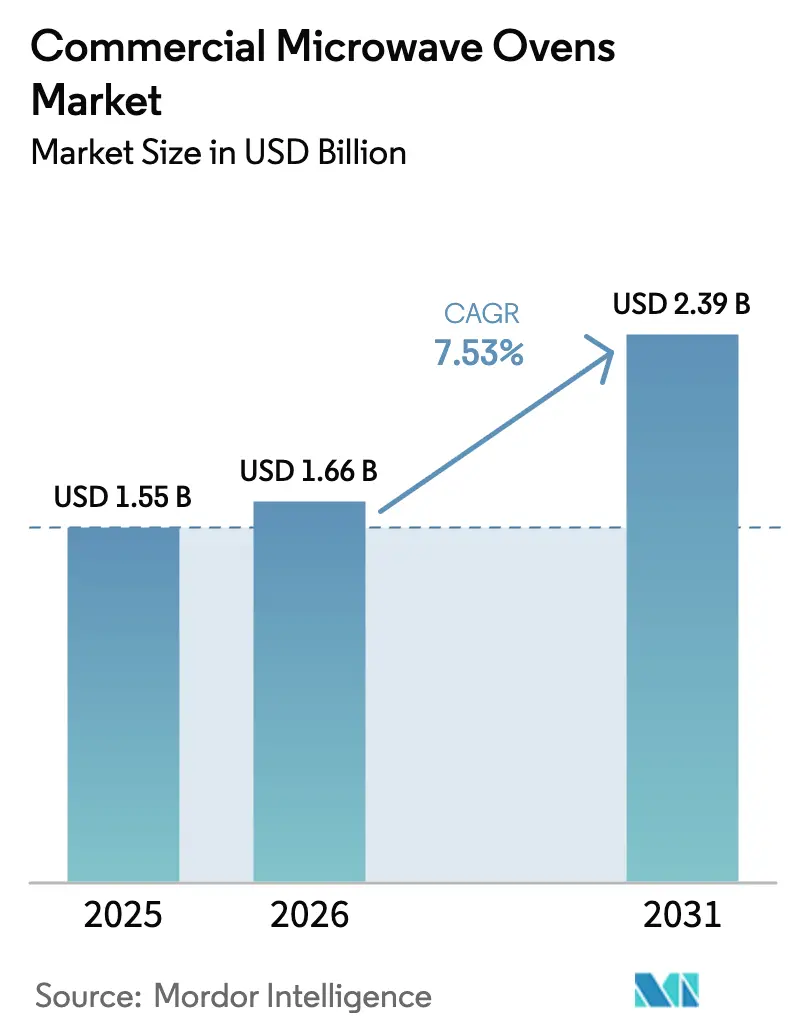

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

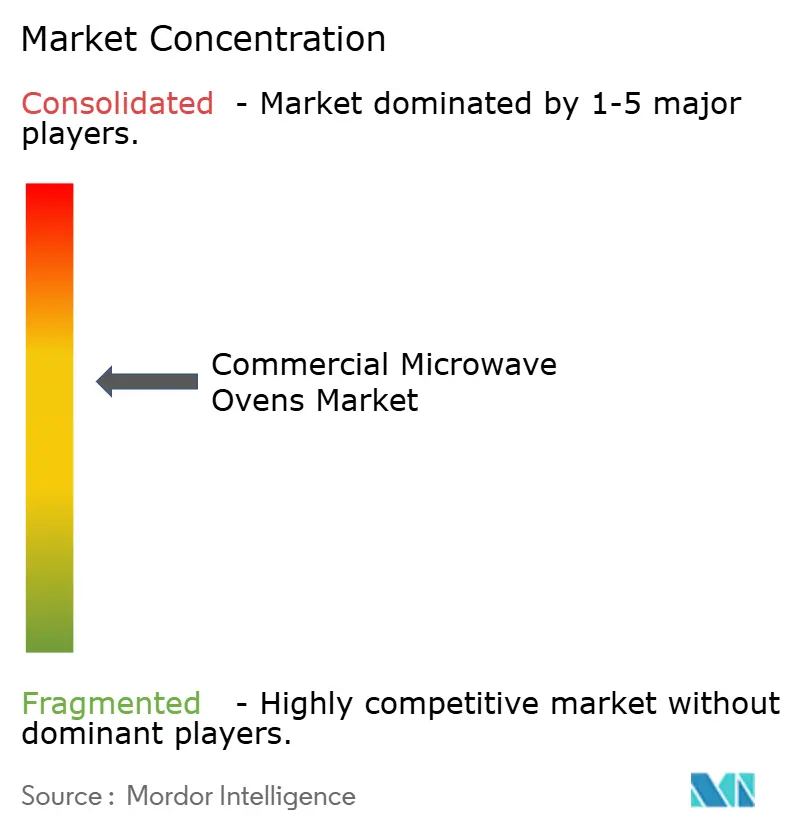

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Commercial Microwave Ovens Market Analysis by Mordor Intelligence

The commercial microwave ovens market size is expected to grow from USD 1.56 billion in 2025 to USD 1.66 billion in 2026 and is forecast to reach USD 2.39 billion by 2031 at 7.53% CAGR over 2026–2031. The growth profile aligns with kitchen modernization cycles and a shift toward programmable, connected equipment that compresses training time and stabilizes output quality during labor shortages. Operators favor ventless high-speed formats that add hot food without ventilation retrofits, which helps maximize throughput within small footprints. Heavy-duty models above 2 kilowatts have led near-term purchasing, while high-speed combinations integrating microwave, convection, and impingement have become the technology to watch due to cycle time reductions and menu versatility. Quick service chains continue to anchor demand as they scale delivery and pickup heavy formats that depend on consistent reheating and rapid service speed.

Key Report Takeaways

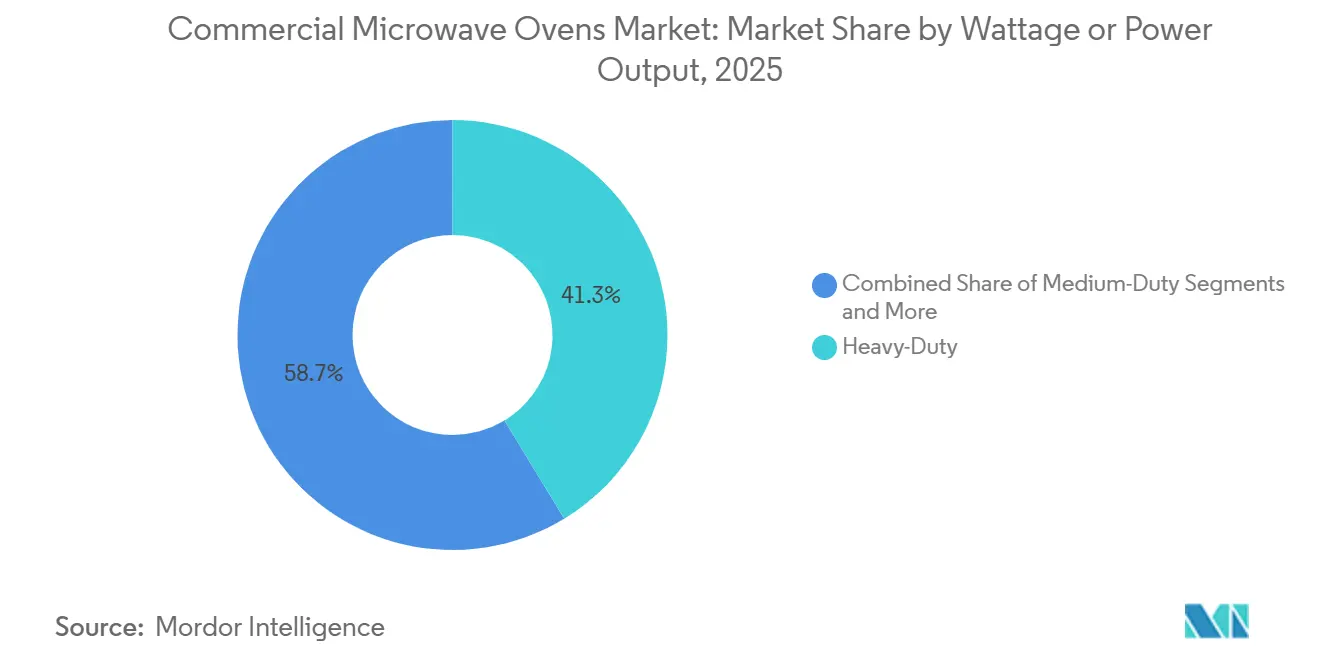

- By wattage or power output, heavy-duty models above 2 kilowatts held 41.26% of the commercial microwave ovens market size in 2025 and are expected to grow at 9.37% annually through 2031.

- By product type, countertop or freestanding units led with 49.35% of the commercial microwave ovens market share in 2025, while high-speed or combination ovens are projected to expand at an 11.72% CAGR through 2031.

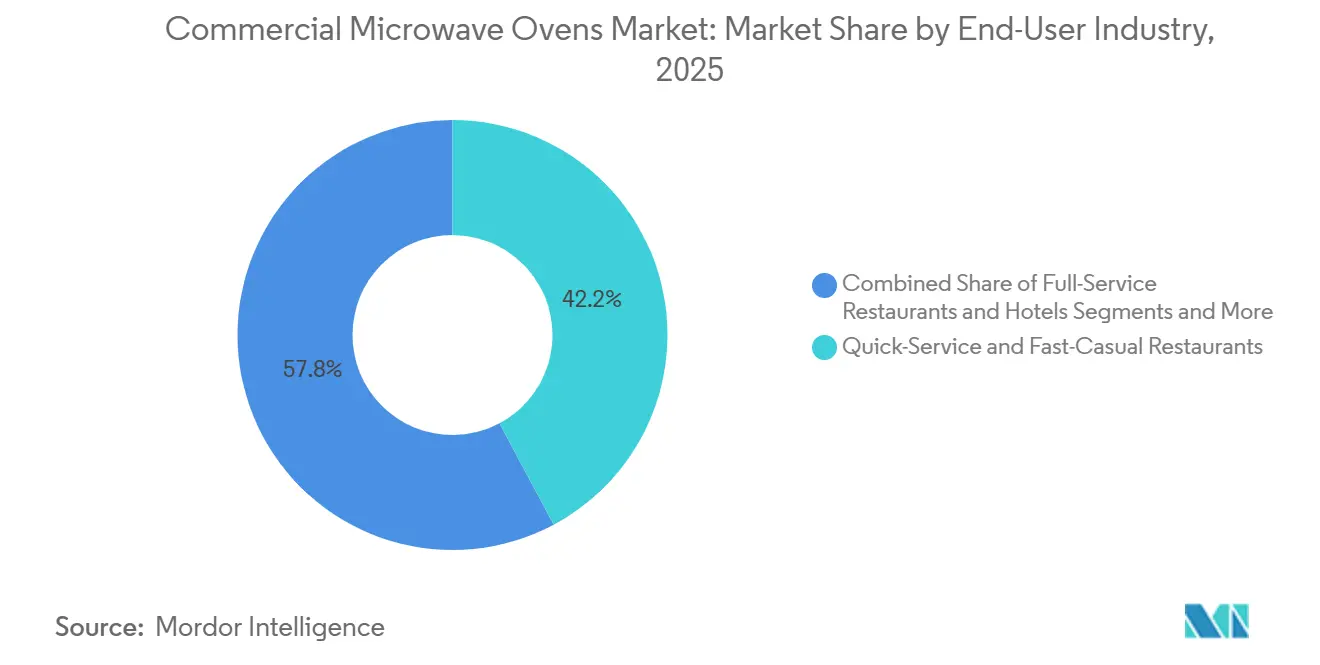

- By end user industry, quick service restaurants accounted for 42.24% of the commercial microwave ovens market share in 2025, and convenience and grocery stores are set to grow at 9.33% annually through 2031.

- By distribution channel, B2C or retail captured 53.35% of the commercial microwave ovens market in 2025, and B2B or direct sales are projected to post a 10.24% CAGR through 2031.

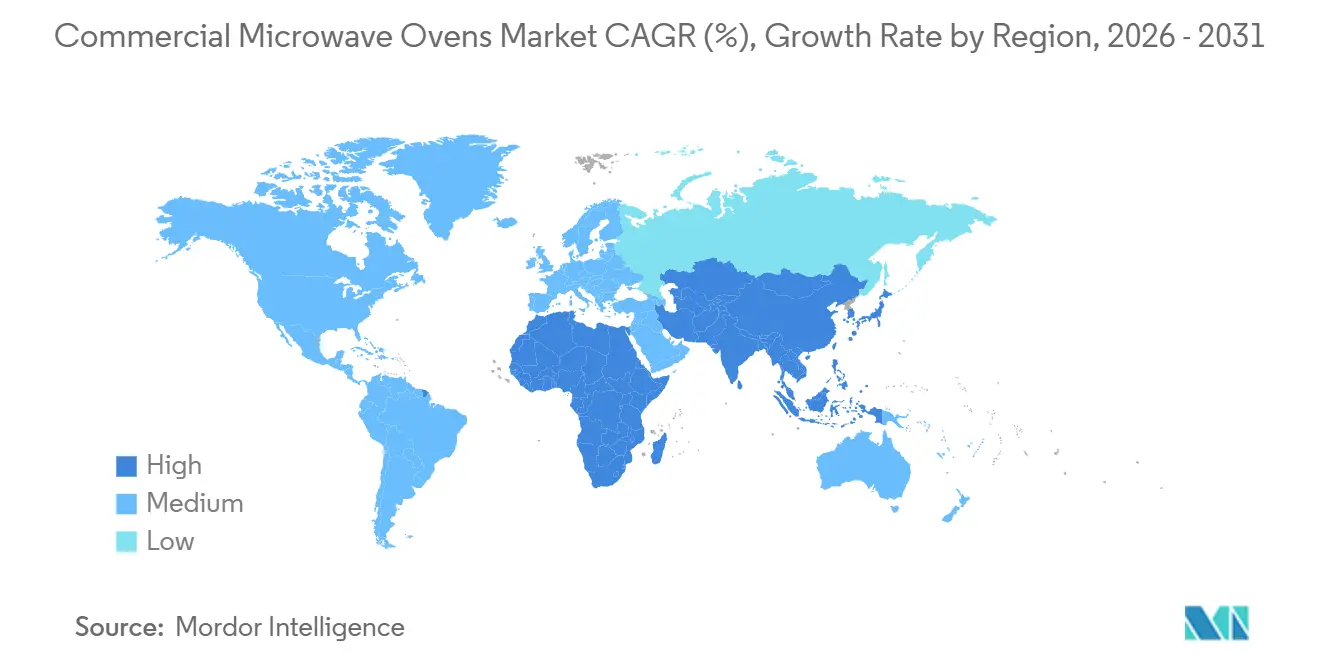

- By geography, North America secured 36.65% of the commercial microwave ovens market in 2025, and the Asia-Pacific is forecast to record an 11.32% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Microwave Ovens Market Trends and Insights

Drivers Impact Analysis*

| Driver | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| QSRs Expand, and Meal-Delivery Kitchens Thrive | +2.1% | Global, with early gains in North America, China, India | Medium term (2-4 years) |

| Magnetron and Inverter Technologies Become More Energy-Efficient | +0.9% | Europe, high‑utility‑rate U.S. metropolitan areas, Japan | Long term (≥ 4 years) |

| Kitchen Automation Rises Due To Post-Covid Labor Shortages | +1.8% | North America core, spill‑over to Western Europe | Short term (≤ 2 years) |

| Programmable Ovens Benefit from Stricter Food-Safety Audits | +0.7% | North America, EU | Medium term (2-4 years) |

| Ventless High-Speed Combo Ovens see Increased Popularity | +1.3% | Urban markets globally, especially <1,000 sq ft footprints | Medium term (2-4 years) |

| AI-Driven Self-Diagnostics Cut Down on Downtime | +0.6% | Early adopters: Japan, South Korea, U.S. QSR chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

QSRs Expand, and Meal-Delivery Kitchens Thrive

Quick service restaurant locations in the United States are continuing to expand, supported by steady year-over-year growth and strong overall economic contribution. Ordering patterns are increasingly skewed toward off-premises consumption, raising expectations for consistent reheating performance and strict timing control during peak periods. Operators are prioritizing programmable cooking cycles that preserve texture, eliminate cold spots, and improve delivery satisfaction. Rapid-cook and high-speed oven formats that dramatically reduce preparation time without compromising quality align well with these operational demands and help manage volume surges tied to digital ordering. As the commercial microwave oven market emphasizes fast deployment in high-growth regions, vertically integrated manufacturers offering AI-enabled systems with short lead times are well positioned to support chain expansion, especially where compact footprints and throughput efficiency are critical.

Magnetron and Inverter Technologies Become More Energy-Efficient

Inverter-based systems deliver a continuous energy stream instead of traditional on-off pulsing, which reduces power draw and supports repeatable results for sensitive items that can scorch under peak cycling. European operators that face high retail electricity rates have accelerated payback modeling and are favoring inverter platforms that also extend component life versus pulsed legacy designs. Established electronics players that generate cash from adjacent high-efficiency components are directing funding to inverter R&D, and that roadmap is starting to influence commercial platforms in the field. Solid state RF generators, which replace magnetrons with semiconductor power modules that deliver finer control and zero warm-up lag, remain premium due to higher capital cost but represent the next step in precision cooking. As the commercial microwave ovens market matures in energy-sensitive regions, technology selection increasingly tracks total cost of ownership rather than first price alone, a shift that is reinforced by power efficiency mandates and lifecycle savings targets. Corporate financial disclosures also show how profit growth in energy and semiconductor lines supports innovation that can filter into professional kitchen platforms.

Kitchen Automation Rises Due To Post-Covid Labor Shortages

Restaurant labor vacancy rates in the United States remained near 12% through 2024 and continued to pressure staffing ratios in 2025, which kept automation on the near-term roadmap for many chains. A large share of restaurants added technology in 2024 and plan to continue in 2025, citing the need to de-skill prep work and standardize output with simple push-button routines. Programmable rapid cook cycles reduce training time by storing multi-stage steps that any staff member can execute during the rush while maintaining consistent quality. Front-of-house engagement benefits when repetitive back-of-house tasks shift to automated routines, and that helps maintain service speed at peak hours. Adoption patterns suggest the commercial microwave ovens market will continue to integrate features like cloud recipes and connected service diagnostics that lower the support burden and stabilize uptime in busy venues. Industry communications also highlight robotics pilots and other automation projects that complement connected ovens and help close staffing gaps without sacrificing safety or throughput.

Programmable Ovens Benefit from Stricter Food-Safety Audits

Auditors are increasing the emphasis on digitally verifiable cook records in larger venues and within institutional catering, which makes integrated HACCP data logging a practical requirement. Programmable commercial microwave ovens provide tagged time temperature profiles that remove the need for paper logs, and cloud dashboards present real-time status and history across fleets. Multi-mode platforms that pair microwave with steam and hot air support diverse menus while still capturing complete cook cycle records that are auditor-friendly. The policy agenda also includes food labeling and nutrition measures with publication targets in 2026, which keeps compliance on the agenda for large multi-site operators and their equipment partners. As the commercial microwave ovens market aligns with data-driven audits, connected platforms that make compliance automatic provide a clear return by lowering risk and reducing manual tracking tasks[1]U.S. Food and Drug Administration, “Foods Program Regulations Under Development,” U.S. Food and Drug Administration, fda.gov. Connectivity suites from category leaders, which include energy reporting and remote monitoring, are already standard in many installations and continue to evolve with new cybersecurity and data sharing requirements across regions.

Restraints Impact Analysis*

| Restraint | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Costs of Raw Materials, Including Steel And Semiconductors | -1.1% | Global supply chains | Short term (≤ 2 years) |

| Intensifying Competition Posed by Rapid-Cook Convection Ovens | -0.9% | North America, Europe | Medium term (2-4 years) |

| Heightened Cyber-Security Concerns Associated With IoT-Connected Models | -0.4% | Enterprise segments in North America, EU | Long term (≥ 4 years) |

| Uncertain Regulations Surrounding RF Emissions in Emerging Markets | -0.3% | Middle East, Africa, select Southeast Asian markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Costs of Raw Materials, Including Steel And Semiconductors

Input cost inflation in steel and electronic components influences price quotes and delivery schedules, which can defer planned purchases in value-sensitive segments. Manufacturers have partially mitigated exposure through scale purchasing, multi-sourcing strategies, and design standardization to improve component interchangeability. Some chains respond by extending replacement cycles or prioritizing refurbishments, which redistributes order flow toward service contracts and parts. Price visibility improves under direct enterprise agreements, but small independent buyers still face list price changes and delivery variability. The commercial microwave ovens market balances these headwinds by emphasizing energy savings, uptime guarantees, and performance features that justify payback under constrained capital budgets, with connectivity features and remote monitoring framed as additional cost avoidance levers in service agreements. Purchasing guidance from large chains also now weighs vendor lead times and parts availability on equal footing with headline features to reduce disruption risk during peak periods.

Intensifying Competition Posed by Rapid-Cook Convection Ovens

Rapid cook convection platforms that rely on high velocity air and smart airflow controls compete at similar speed tiers, which can slow adoption among operators that prefer to minimize microwave use in front-of-house environments. These systems promote browning and crisping qualities and have cultivated loyalty in bakeries and cafes where texture is a central attribute. Competitive positioning, therefore, hinges on cycle flexibility, footprint, and electrical load, with multi-mode designs that include microwave often beating pure convection when speed is the primary constraint. Product trainers and culinary teams frame pilot tests to show side-by-side cycle output, which supports head-to-head evaluations in chain specifications. As the commercial microwave ovens market increasingly features high-speed hybrid designs, the overlap with rapid cook convection is turning into a feature race where integrated microwave inputs tip outcomes when seconds matter in queue time metrics[2]Merrychef Product Team, “Products,” Merrychef, merrychef.com. Ongoing energy efficiency work and cloud recipe governance add separation on operating cost and standardization, which matters in multi-site operations that rely on centralized updates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wattage/Power Output: Heavy-Duty Dominance Reflects Volume Demands

Heavy-duty commercial microwave ovens exceeding 2.0 kilowatts held 41.26% of the 2025 market size, reflecting the needs of high-throughput locations that require speed and consistency during peak periods. The segment is projected to grow at 9.37% annually through 2031, supported by drive-through formats that must maintain queue times under two minutes while handling a broader menu. Medium-duty models in the 1.2 to 2.0 kilowatt range align with mid-volume cafeterias and offices where peak loads are predictable, and budgets target durable entry-level commercial designs. Light-duty ovens below 1.2 kilowatts serve compact venues that prioritize small footprints and simple cycles over multi-item simultaneous reheats. As the commercial microwave ovens market adapts to higher off-premises sales, power tiers are being specified to match expected order surge profiles rather than legacy back-of-house archetypes.

Engineering roadmaps continue to emphasize power density and uniformity, with dual magnetron designs balancing speed and cavity coverage to reduce cold spots at heavy-duty power levels. Product launches that push faster warm-up and more even airflow show how the category is crossing into high-speed hybrid terrain with better browning while preserving microwave speed. A notable focus is stackability and vertical clearance, which influences how many units can fit on a line without air intake compromises. Platform durability and cooling design also remain central since higher power cycles drive thermal loads that affect component life across long opening hours. These refinements help the commercial microwave ovens market sustain heavy-duty leadership at scale and preserve consistency in chain kitchens where peak period stability matters most.

By Product Type: Flexibility Drives Countertop Leadership, Innovation Fuels High Speed Ascent

Countertop and freestanding units captured 49.35% of the 2025 market size due to plug-and-play installation and compatibility with legacy layouts that lack built-in cutouts. High-speed or combination ovens that integrate microwave, convection, and impingement are forecast to expand at an 11.72% CAGR through 2031, which reflects rising demand for shorter cycles and versatile menus without hood retrofits. Built-in formats retain a place in full-service kitchens with planned renovations, but decision cycles and installation complexity slow share gains relative to countertop growth. Product development showcases larger cavities within compact frames so that standard plates and half-size pans fit, which improves utilization per square foot. This variety keeps the commercial microwave ovens market responsive to the layout realities of QSR, convenience, and small-format retail.

Innovation within the countertop category focuses on stackable designs with small footprints that still deliver high airflow speeds and multi-mode flexibility. Connectivity and cloud recipe management are becoming standard asks in multi-site deployments, which reduces retraining time and stabilizes outcomes across shifts. High-speed ranges continue to improve cavity-to-footprint ratios and cycle controls to hit speed targets for pizzas, sandwiches, and baked items. Vendor communications highlight 80% faster cycles relative to conventional methods, which supports peak readiness and raises the ceiling on menu innovation in space-constrained sites. These design and software advances sustain the commercial microwave ovens market momentum in countertop and hybrid models that balance speed, quality, and footprint in urban venues.

By End User Industry: QSRs Lead Share, Convenience Stores Race Ahead

Quick service and fast casual restaurants accounted for 42.24% market share of 2025 end-user revenue, supported by unit count growth and expanded menus that require precise reheating under time pressure. Convenience and grocery stores are projected to grow at 9.33% annually through 2031 as hot grab-and-go programs spread and help monetize underutilized space in breakfast and lunch dayparts. Full-service restaurants and hotels contribute steady replacement demand and continue to add connectivity features to centralize control and record-keeping. Institutional venues such as hospitals, schools, and airports lean toward HACCP-ready ovens and fleet dashboards that support audits and policy compliance. The commercial microwave ovens market continues to consolidate around use cases that pair fast cycles with repeatable quality and documented cook profiles.

Off-premises sales now represent a larger share of revenue. Kitchen planners respond with line designs that distribute load across multiple microwave or high-speed cavities to handle surges without queue slippage. Packaging and cycle coordination also matter since temperature retention and texture drive repeat orders and broader menu adoption. These factors keep reheating performance central to equipment selection and raise the premium on programmable cycles that maintain taste and structure across items. The commercial microwave ovens market is, therefore, closely tied to how chains standardize digital production flows and integrate connected ovens into broader automation stacks.

By Distribution Channel: Retail Breadth Meets Direct Efficiency

B2C or retail routes, including multi-brand stores, exclusive brand outlets, online platforms, and other points of sale, held 53.35% of the 2025 distribution market size due to broad geographic coverage and accessory cross-selling. B2B or direct manufacturer sales are projected to post a 10.24% CAGR through 2031 as large chains negotiate volume contracts that include training and dedicated support service levels. Multi-brand stores support side-by-side comparisons for independent buyers, while brand showrooms leverage immersive demonstrations that shorten decision cycles. Online sales continue to grow for small ticket and replenishment items, though high ticket ovens still benefit from live consultations for installation planning and financing terms. With more enterprise agreements embedding connectivity, recipe governance, and service packages, the commercial microwave ovens market is seeing direct channels take a larger role in chain standardization programs.

Direct channel performance also reflects manufacturer innovation centers that bring specifiers into controlled test kitchens to pilot menu items and collect timing data. Platform integration with cloud dashboards and service portals can be demonstrated in these settings, which raises confidence among central kitchen teams and franchisee networks. Retail still plays a critical role for independent operators that need immediate replacement units or entry-level options with basic programmability. Digital discovery through online catalogs and configurators feeds both direct and retail paths and creates a more informed buyer before the final consultation. This blended approach allows the commercial microwave ovens market to serve both enterprise and independent customers without eroding the benefits that come with standardization and contracted support.

Geography Analysis

North America commanded a 36.65% market share in 2025 as a large installed base and labor headwinds maintained demand for programmable ovens that stabilize output with fewer skilled hands. The region’s vacancy rates held near 12% during 2024 and into 2025, which aligned with plans to invest in automation and connected equipment that cut training time and improve consistency. Urban stores benefit from ventless high-speed designs that eliminate hood costs and enable hot menus in sites below 1,000 square feet, especially in dense retail corridors. Canadian chains continue to adopt IoT-enabled equipment to streamline multi-site governance with cloud recipes and service dashboards. Cross-border supply coordination within USMCA supports component flow, while tariff discussions since early 2025 have increased emphasis on supplier diversification to manage exposure in complex assemblies.

Asia-Pacific is forecast to grow at an 11.32% CAGR from 2026 to 2031, driven by rising chain penetration and investment in compact automated equipment for small format stores. China’s growth in limited service formats and regional manufacturers’ ability to shorten lead times support faster rollouts in Tier 2 cities and beyond. India’s expansion in quick service outlets through 2026 elevates demand for robust countertop and high-speed ovens that perform under variable grids, and franchise networks are writing cloud recipe requirements into specifications to coordinate menus across regions. Japan and South Korea continue to lead on connected diagnostics and remote recipe management, which shortens support cycles and makes cross-site optimization more practical. The commercial microwave ovens market benefits from vertically integrated production footprints that can ship AI-enabled units with short lead times into Southeast Asian store pipelines.

Europe’s market size is shaped by eco design measures and energy priorities that nudge operators toward efficient inverter platforms and connected oversight for fleets. The European Union’s eco design agenda for small appliances includes tighter idle power expectations in 2026, which aligns with operator efforts to trim electricity bills under higher retail rates in several member states. Lifecycle carbon and total cost of ownership feature in evaluations, and listings such as Energy Star and the United Kingdom’s Energy Technology List remain useful signals in product selection processes. Network-capable combi and high-speed platforms with published compliance to the EU Radio Equipment Directive help reduce procurement friction for enterprise buyers with strict cybersecurity baselines. Outside Europe, South American demand centers in Brazil, Argentina, Chile, and Peru upgrade legacy equipment in urban foodservice, and the Middle East and Africa continue to benefit from hospitality growth in the Gulf Cooperation Council countries with premium hotel and travel venues specifying international standards. The commercial microwave ovens market in these regions emphasizes durability, repairability, and compliance documentation to serve multinational buyers and to work within local service ecosystems.

Competitive Landscape

The commercial microwave ovens market is moderately concentrated, with the top five companies controlling about half of the global share, leaving opportunities for specialists focused on specific technologies or end-use needs. Panasonic, Midea Group with Galanz, Sharp, Ali Group’s portfolio including Merrychef and Amana Commercial, and Whirlpool form the core global players, supported by scale manufacturing and strong brand recognition. Samsung and LG extend their connected-appliance expertise into professional kitchens by integrating cameras, AI-based cooking logic, and Wi-Fi connectivity for chain-wide recipe consistency. The Middleby Corporation continues to advance its TurboChef and Merrychef high-speed oven lines within a broader commercial foodservice ecosystem centered on speed, uptime, and system integration. Multi-mode competitors such as Rational strengthen demand for ovens that combine microwave, steam, and hot air, appealing to operators seeking multifunctionality in a compact footprint.

Strategic initiatives across the sector emphasize vertical integration, connected service platforms, and faster expansion in Asia-Pacific markets. Middleby announced plans to spin off its food processing segment into a standalone public company by 2026, enabling its commercial foodservice division to pursue acquisitions with a more focused capital structure. The company’s Commercial Foodservice platform generated USD 2.38 billion in revenue in 2024 with adjusted EBITDA margins above 27%, reflecting strong performance in high-speed ovens and connected services. Panasonic highlighted its financial resilience in 2025 while expanding partnerships around AI-enabled cooking assistants that help standardize output across restaurant chains. Samsung also introduced AI-driven camera systems that automatically recognize food and optimize settings, reducing training requirements and simplifying kitchen workflows.

Manufacturing scale and component access are increasingly used to shorten lead times and stabilize supply chains. Midea invested RMB 8.8 billion (USD 1.21 billion) in R&D during the first half of 2025 and reached RMB 43 billion (USD 5.89 billion) over three years, while expanding overseas manufacturing to improve regional responsiveness and reduce logistics risk[3]Midea Global Communications, “Midea Wins Forbes China Flagship Brand Again,” Midea Group, midea.com. Whirlpool committed USD 300 million to U.S. facilities in 2025 to enhance automation, energy efficiency, and domestic production of connected appliances[4]Whirlpool Investor Relations, “Q3 2025 Earnings Presentation,” Whirlpool Corporation, whirlpoolcorporation.com. Alto-Shaam showcased new school nutrition ovens and marked a milestone anniversary with Energy Star-certified combi models designed for institutional reliability and efficiency. Across the industry, vendors are strengthening cybersecurity documentation to meet evolving EU requirements, while solid-state RF technology remains a premium but promising pathway toward more precise energy control in future connected platforms.

Commercial Microwave Ovens Industry Leaders

-

Panasonic Corporation

-

Midea Group (Galanz)

-

Sharp Corporation

-

Ali Group (Amana / Menumaster)

-

Whirlpool Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Sharp Electronics of Canada unveiled expanded commercial microwave offerings for Canadian foodservice, adding medium-duty R 21LCFS and R 21LVF and heavy-duty TwinTouch R CD1200M and R CD1800M units with dual control panels.

- February 2025: Sharp launched the Celerity high-speed oven at the Kitchen & Bath Industry Show in Las Vegas, featuring an industry-first Golden Heater designed for faster high-temperature performance, with U.S. availability expected in fall 2025.

- February 2025: Samsung announced the Bespoke AI Oven with a built in camera and AI Pro Cooking that recognizes 80 dishes and optimizes settings for automated preparation across light commercial and residential use cases.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the commercial microwave ovens market as all newly manufactured, plug-in or built-in microwave units rated above 1 kW that are purpose-built for foodservice, hospitality, institutional catering, or retail snack preparation environments. These ovens include light, medium, and heavy-duty classes and high-speed combination models that integrate convection or impingement cooking.

Scope exclusion: household microwave ovens sold to consumers for domestic use are not counted.

Segmentation Overview

-

By Wattage / Power Output

- Light-Duty ( Less than 1.2 kW)

- Medium-Duty (1.2–2.0 kW)

- Heavy-Duty (More than 2.0 kW)

-

By Product Type

- Countertop / Freestanding

- Built-in / Over-the-Range

- High-speed / Combination

-

By End-user Industry

- Quick-Service & Fast-Casual Restaurants

- Full-Service Restaurants & Hotels

- Convenience & Grocery Stores

- Institutional Catering (Hospitals, Schools, Airports)

-

By Distribution Channel

-

B2C/Retail

- Multi-brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- B2B/Directly from the Manufacturers

-

B2C/Retail

-

By Geography

-

North America

- Canada

- United States

- Mexico

-

South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

-

Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

-

Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews with chain-restaurant equipment buyers, independent kitchen designers, and regional distributor managers across North America, Europe, and Asia Pacific. Respondents validate duty-cycle assumptions, replacement intervals, and the shift toward ventless high-speed models, while short online polls of caterers and convenience-store operators benchmark unit throughput expectations.

Desk Research

Our analysts first pull shipment and trade volumes coded under HS 851650 from national customs dashboards such as UN Comtrade, the US International Trade Commission DataWeb, and China Customs, which show global traffic by wattage band. Next, we review restaurateur demand indicators from the National Restaurant Association, Eurostat tourism accommodation nights, and Technomic menu-cycle audits to gauge install bases and replacement rates. Energy-efficiency standards from the US Department of Energy and EU Ecodesign files help us bound price dispersion by power class. Company filings accessed through D&B Hoovers and news flows on Dow Jones Factiva supply average selling prices and corporate unit sales. These sources are illustrative; many additional public records and industry bulletins are consulted for triangulation.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model is applied. Import-export reconciliations and national foodservice outlet counts create the demand pool, which is then cross-checked against sampled supplier roll-ups (ASP × volume) to refine totals. Key variables include 1) quick-service restaurant outlet growth, 2) average oven lifespan, 3) magnetron cost trend, 4) share of heavy-duty units in new installs, and 5) online equipment sales penetration. Multivariate regression projects each driver through 2030, after which scenario analysis adjusts for energy-efficiency mandates or commodity shock events. Gaps in channel data are bridged by applying proven replacement-cycle ratios gathered during interviews.

Data Validation & Update Cycle

Outputs pass two analyst reviews, where anomalies versus external shipment trends or sudden ASP swings trigger re-checks. Reports refresh yearly, and material events such as tariff shifts prompt mid-cycle updates; a final validation pass occurs before client delivery.

Why Our Commercial Microwave Ovens Baseline Earns Trust

Published estimates often diverge because firms pick different wattage cut-offs, bundle household units, or apply flat growth curves.

Key gap drivers include varying inclusion of combo high-speed ovens, currency conversion at spot versus average annual rates, and lighter refresh cadences that miss rapid post-pandemic demand rebounds. Mordor's quarterly trade-flow monitoring and interview-verified duty-cycle filters narrow these spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.54 B (2025) | Mordor Intelligence | - |

| USD 4.83 B (2024) | Global Consultancy A | Combines residential units and uses installed-base value rather than new sales |

| USD 3.27 B (2024) | Trade Journal B | Applies list prices without channel discounts; limited geographic coverage for Africa |

| USD 2.80 B (2024) | Industry Association C | Excludes light-duty ovens below 1.2 kW and lacks replacement-cycle adjustment |

These contrasts show that our disciplined scope selection, variable tracking, and annual refresh give decision-makers a balanced, transparent baseline they can confidently reference.

Key Questions Answered in the Report

What is the current size and outlook for the commercial microwave ovens market through 2031?

The commercial microwave ovens market size is USD 1.66 billion in 2026 and is projected to reach USD 2.39 billion by 2031 at a 7.53% CAGR, reflecting sustained demand for programmable and ventless high‑speed formats in multi‑site foodservice.

Which product types are growing fastest in commercial microwave ovens?

High‑speed or combination ovens integrating microwave, convection, and impingement are projected to expand at 11.72% annually through 2031 as operators pursue cycle‑time reductions and menu versatility without hoods.

Which end‑users account for the largest demand in commercial microwave ovens?

Quick‑service restaurants led with 42.24% share in 2025 due to their high throughput needs, while convenience and grocery stores are the fastest growing with a 9.33% CAGR as hot grab‑and‑go expands.

What region leads and which region will grow fastest in commercial microwave ovens?

North America led with 36.65% share in 2025, while Asia‑Pacific is forecast as the fastest growing at 11.32% CAGR from 2026 to 2031 on the back of chain rollouts and compact, automated formats.

Which wattage class dominates the commercial microwave ovens landscape?

Heavy‑duty ovens above 2.0 kilowatts held 41.26% of revenue in 2025 and are projected to grow at 9.37% annually through 2031 as drive‑through and delivery‑heavy formats concentrate on speed and consistency.

How is connectivity influencing purchasing decisions in commercial microwave ovens?

Buyers are prioritizing ovens with Wi‑Fi, cloud recipe management, and predictive maintenance since these features reduce training time, improve compliance, and cut unplanned downtime across large fleets.

Page last updated on: