Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

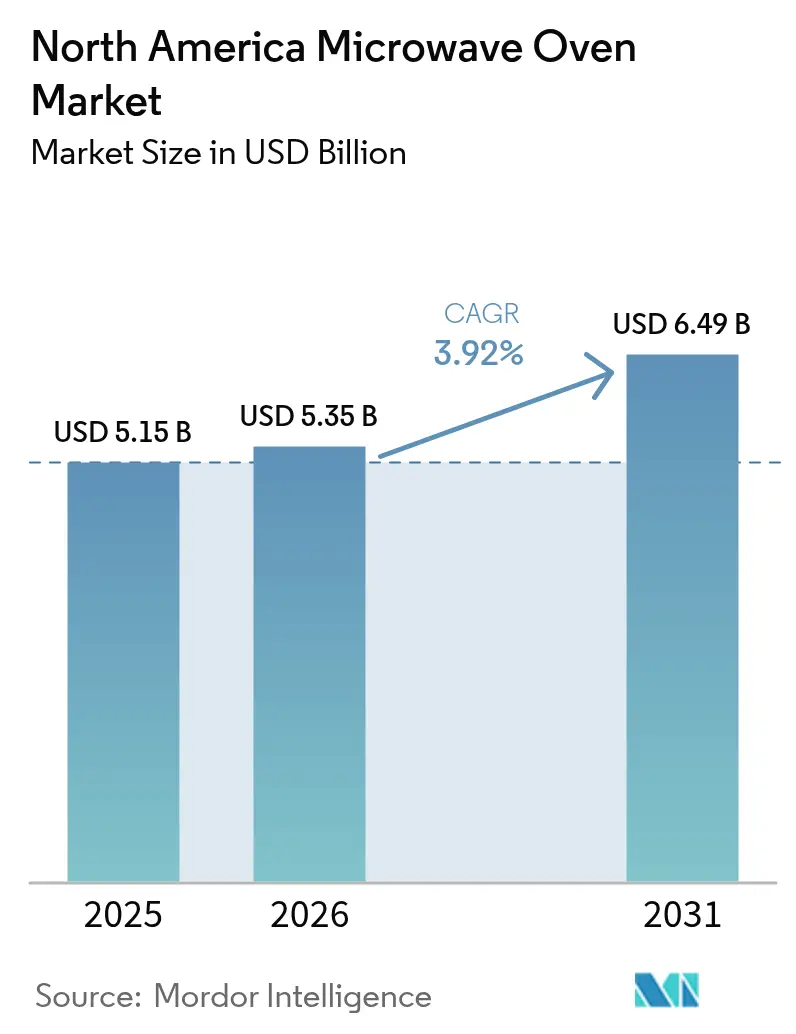

| Base Year Market Size (2025) | USD 5.15 Billion |

| Market Size (2026) | USD 5.35 Billion |

| Market Size (2031) | USD 6.49 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Microwave Oven Market Analysis by Mordor Intelligence

The North America microwave oven market size was valued at USD 5.15 billion in 2025 and estimated to grow from USD 5.35 billion in 2026 to reach USD 6.49 billion by 2031, at a CAGR of 3.92% during the forecast period (2026-2031). Replacement purchases now outweigh first-time sales as households approach full penetration, yet upgrade appetite stays healthy thanks to multifunctional designs, smart connectivity, and stricter energy-efficiency rules. Premium built-in units benefit from renovation spending, while countertop models remain dominant in rental housing and smaller kitchens. Manufacturers are defending relevance against air-fryer ovens by integrating convection, grill, and air-fry modes inside a single cavity. Competitive rivalry has intensified as LG, Samsung, Whirlpool, and GE race to embed AI-driven cooking guidance, voice control, and IoT services that lift average selling prices while locking customers into proprietary ecosystems.

Key Report Takeaways

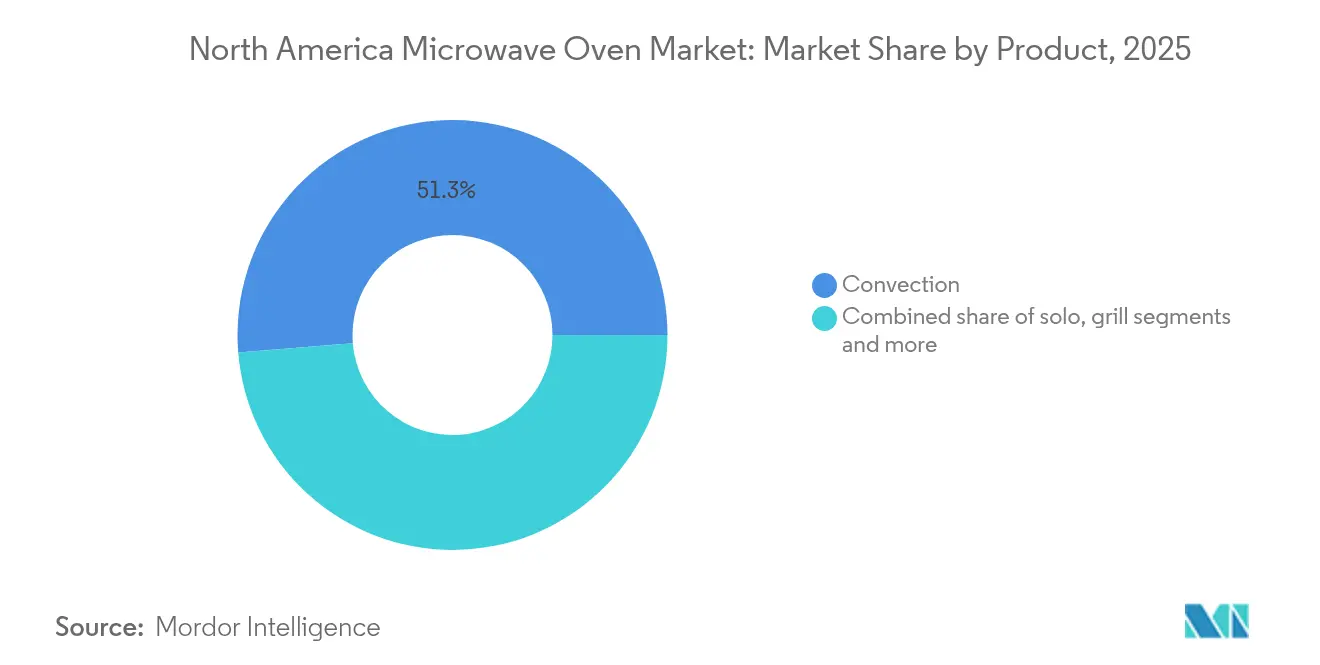

- By product, convection microwaves led with 51.30% revenue share in 2025, while grill variants are projected to expand at a 4.52% CAGR through 2031.

- By structure, countertop units held 64.55% of the North America microwave oven market share in 2025; built-in models are expected to grow at a 5.33% CAGR to 2031.

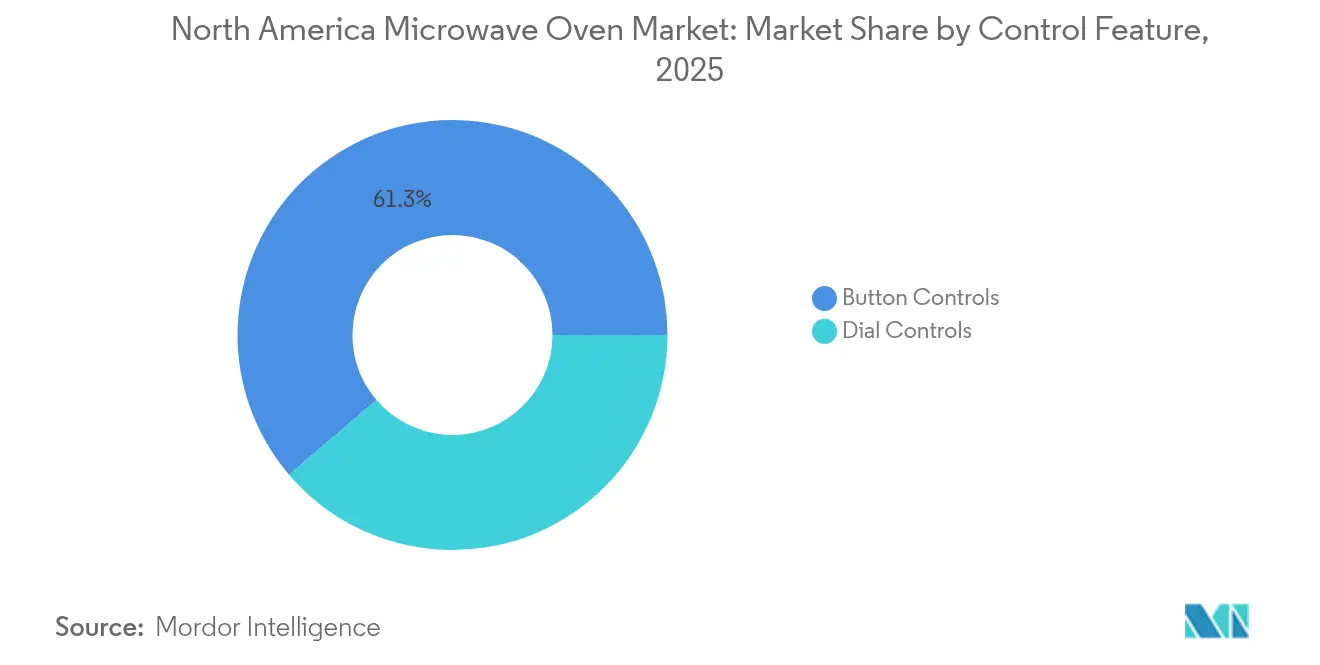

- By control feature, button interfaces captured 61.25% of the North America microwave oven market share in 2025 and are advancing at a 5.5% CAGR through 2031.

- By capacity, the 25-29 liter class held 35.60% of the North America microwave oven market size in 2025, while 30 liter-plus models are projected to expand at a 5.28% CAGR between 2026 and 2031

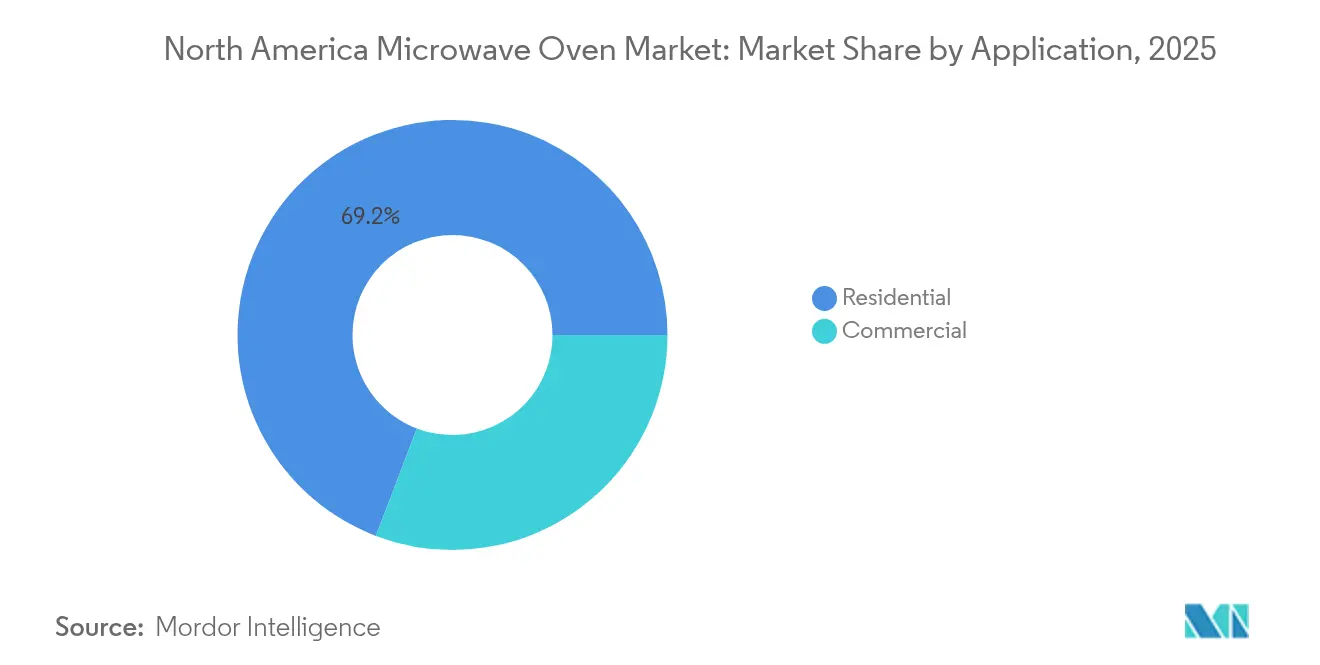

- By application, residential usage accounted for 69.20% of the North America microwave oven market size in 2025, while commercial demand is advancing at a 5.05% CAGR.

- By distribution channel, multi-brand stores captured 39.10% revenue in 2025; online sales are climbing at a 5.82% CAGR through 2031.

- By geography, the United States commanded 70.50% of the North America microwave oven market size in 2025, whereas Canada posts the fastest 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Microwave Oven Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income and Kitchen Renovations | +1.2% | United States and Canada | Medium term (2-4 years) |

| Growth of E-Commerce Appliance Sales | +0.8% | North America (strongest in Canada) | Short term (≤ 2 years) |

| Energy-Efficiency Regulations Driving Replacements | +0.9% | United States and Canada | Long term (≥ 4 years) |

| Dark-kitchen and Meal-Kit Expansion | +0.6% | Urban centers across North America | Medium term (2-4 years) |

| Aging-in-Place Demand for Easy-to-Use Appliances | +0.5% | United States and Canada suburban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Kitchen Renovations

Kitchen upgrade budgets have increased, shortening replacement cycles for built-in microwaves as homeowners seek seamless cabinetry alignment and premium finishes. Flush-mount and drawer-style models, such as Whirlpool’s 1.1 cu ft turntable-free design launched at KBIS 2024, cater to this demand [1]Whirlpool, “1.1 Cu Ft Flush Mount Microwave,” whirlpool.com . Higher-income households often replace an entire suite of cooking appliances during renovations, boosting cross-category sales. Smart connectivity and capacitive touch controls appeal to design-conscious buyers, lifting average selling prices. Mortgage rate volatility may briefly temper renovation outlays, yet pent-up remodeling projects continue to support medium-term growth.

Growth of E-Commerce Appliance Sales

Online channels are reshaping distribution economics. Direct-to-consumer storefronts allow manufacturers to upsell extended warranties and recipe subscriptions while harvesting first-party data. Canada shows the sharpest shift as long travel distances make click-to-deliver appliances attractive. Lower store overhead enables sharper pricing but elevates logistic costs for heavy built-in units requiring professional installation. The North America microwave oven market, therefore, sees hybrid fulfilment, where countertop models ship parcel while built-in units route through local installers.

Energy-Efficiency Regulations Driving Replacements

The U.S. Department of Energy finalized stricter standby-power limits for residential cooking products in January 2024, with compliance mandatory from January 31, 2028. Anticipation of costlier compliant models prompts early replacements of legacy units, lifting short-term volumes. Makers are switching to inverter power supplies and solid-state magnetrons to meet the sub-1-watt targets. The North America microwave oven market benefits from the rule’s signaling effect on household utility savings and greenhouse gas reduction.

Dark-Kitchen & Meal-Kit Expansion

Ghost kitchens and meal-kit assemblers require high-duty microwaves to finish dishes rapidly and consistently. Units above 1,200 watts now serve as essential line equipment. Five-to-seven-year commercial lifespans create predictable replacement rhythms that smooth manufacturer revenues. Price sensitivity caps feature proliferation, but programmable multi-stage cooking and durable stainless-steel interiors remain must-have specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Household penetration near saturation | -1.8% | United States & Canada mature markets | Long term (≥ 4 years) |

| Health concerns over radiation & nutrient loss | -0.7% | Health-conscious segments across North America | Medium term (2-4 years) |

| Competitive pressure from countertop air-fryer ovens | -1.1% | United States & Canada urban markets | Short term (≤ 2 years) |

| Supply-chain volatility for magnetron components | -0.6% | Global, concentrated in North America, manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Household Penetration Near Saturation

Microwaves sit in more than 90% of North American kitchens, shifting demand toward later-cycle replacements rather than new installs. With proper maintenance and regular use, most microwaves have a lifespan of 7 to 10 years. However, premium models can extend that duration, lasting anywhere from 10 to 15 years, or even beyond. Brands counter by bundling convection, air-fry, and smart capabilities to tempt earlier trade-ins, but consumer price sensitivity constrains uptake. Consequently, producers pursue incremental revenues in commercial and export channels.

Health Concerns Over Radiation & Nutrient loss

Public scrutiny of 2.45 GHz exposure has risen after 2024 studies linked prolonged microwave radiation to cellular oxidative stress and cochlear changes. Although FDA leakage limits remain unchanged at 1 mW/cm² at 5 cm, perception issues influence purchase decisions among families with children [2]U.S. Department of Energy, “DOE Finalizes Cost-Saving Efficiency Standards for New Cooking Products,” energy.gov. Manufacturers now highlight reinforced door interlocks, PFAS-free interiors, and even-heat inverter technology to reassure buyers and protect brand trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Convection Dominance Amid Grill Innovation

Convection units captured 51.30% of the North America microwave oven market in 2025, reflecting consumer desire for browning and crisping that traditional solo models lack. Grill hybrids, though smaller in volume, are growing at 4.52% CAGR as they double as countertop air fryers. Panasonic’s HomeCHEF Connect 4-in-1, introduced in March 2025, epitomizes this trend with microwave, convection, air-fry, and broil modes. Manufacturers blur boundaries between quick reheating and primary cooking, reshaping competitive sets. Continued innovation in magnetron-free solid-state heating may unlock higher energy savings, further boosting the North America microwave oven market.

The product mix also mirrors evolving dietary habits. Health-focused users prefer grill or combi units that achieve crisp textures without deep-frying oil, while convenience-driven households stick with solo models for fast reheats. Premium drawer-style convection designs appeal to luxury renovations, even though they command a higher price. The drive toward multifunctionality positions microwaves as central rather than auxiliary appliances, sustaining replacement demand despite unit saturation.

By Structure: Countertop Convenience Versus Built-in Aesthetics

Countertop models dominated with 64.55% share in 2025, bolstered by renters and urban dwellers who favor portability and lower up-front cost. Built-in formats, including flush-mount and drawer variants, are rising 5.33% annually as renovation projects prioritize cohesive sight lines and decluttered counters. Whirlpool’s flush-mount series demonstrates how slim trim kits deliver zero-gap installation without custom millwork. Over-the-range options straddle both segments by combining ventilation with microwave functionality.

The North America microwave oven market size for built-in units is projected to expand faster than overall demand, enabled by higher average selling prices and retailer attachment rates for professional installation. Yet countertop units still account for the bulk of e-commerce orders because parcel shippers can handle them without carpentry services. Space-efficient low-profile over-the-range models address smaller kitchens, while luxury drawer formats target premium cabinetry builds. Structural preference thus tracks housing tenure, household income, and renovation activity.

By Control Feature: Button Interfaces Lead Digital Transition

Button interfaces, ranging from membrane pads to capacitive touch surfaces, represented 61.25% share in 2025 and are also the fastest-growing segment at 5.5% CAGR. The shift away from rotary dials reflects consumer familiarity with smartphone-like haptics and the need for complex multi-stage cooking programs. LG previewed a 27-inch LCD-touchscreen microwave in December 2024, underscoring the push toward large-format displays. Dial controls retain a niche among budget buyers and heavy-duty commercial installations that favor mechanical longevity.

Intuitive interfaces deliver tangible value for aging users who require legible fonts and simplified menus, supporting inclusive-design mandates. NFC and voice integration allow hands-free operation via smart-home speakers, while over-the-air firmware updates add new cooking presets long after purchase. Button control innovation therefore sustains differentiation as raw magnetron technology approaches commoditization, reinforcing brand ecosystems within the North America microwave oven market.

By Capacity: Mid-Range Dominance with Large-Capacity Growth

Ovens sized 25-29 liters led with 35.60% share in 2025, balancing footprint and volume for typical family meals. Units above 30 liters are expanding at 5.28% CAGR as more households batch-cook or substitute microwaves for conventional ovens to save energy. Commercial operators often specify 0.6 cu ft stainless chambers paired with 1,700–2,100 watts for maximum throughput across standard plate sizes. Conversely, units below 19 liters cater to dorms, break rooms, and tiny homes where counter space remains scarce.

The North America microwave oven market size for larger cavities benefits from consumer substitution of full-size ranges with multi-ovens capable of convection bake and air-fry. Shelf-ready refrigerated meals also come in larger trays that demand wider turntables or flatbed designs, nudging households toward bigger footprints. Energy codes encourage inverter power scales that adapt output to load weight, improving efficiency in larger chambers without sacrificing speed.

By Application: Residential Stability Amid Commercial Acceleration

Residential buyers contributed 69.20% revenue in 2025, underpinning the mature core of the North America microwave oven market. Household demand now arises chiefly from technological refresh cycles rather than first ownership. Conversely, the commercial segment is gaining momentum at 5.05% CAGR, driven by food-delivery infrastructure, hospital cafeterias, and convenience stores that require reliable reheating at high duty factors. Panasonic’s NE-series 2,100-watt commercial models illustrate how ruggedized components and multi-stage programming command premium margins.

Commercial buyers evaluate the total cost of ownership, factoring service life, menu flexibility, and NSF sanitation compliance. Manufacturers responding with modular parts and field-diagnostic software win repeat contracts. Residential lines emphasize aesthetics, child-safety locks, and smartphone integration to keep pace with connected-kitchen expectations.

By Distribution Channel: Online Growth Challenges Traditional Retail

Multi-brand brick-and-mortar stores held a 39.10% share in 2025 but face sales cannibalization as pure-play online and manufacturer webshops post a 5.82% CAGR. Countertop models ship via standard parcel; built-ins still rely on showrooms and installer networks, preserving retail relevance. Manufacturers pursuing a dual path offer online exclusive colors or bundles to entice direct traffic. Canada leads the channel shift because remote communities lack large appliance outlets, making doorstep delivery compelling.

Financing, assembly, and haul-away services influence consumer channel choice. Online retailers partner with service aggregators to replicate in-store support, while physical stores deploy interactive displays and live cooking demos to showcase new features such as sensor-driven air fry. Channel convergence will likely stabilize as omnichannel logistics mature across the North America microwave oven market.

Geography Analysis

The United States constituted 70.50% of 2025 revenue thanks to its sizeable installed base, active renovation pipeline, and early adoption of smart appliances that command premium prices. Regulatory certainty from DOE standards also accelerates turnover as consumers pre-empt impending efficiency mandates. American dark-kitchen growth clusters around metropolitan hubs, reinforcing commercial demand and raising the North America microwave oven market density.

Canada, while smaller, is the fastest-growing locale at 5.12% CAGR because new-household formation and provincial energy rebates encourage replacement of legacy units. E-commerce penetration surpasses U.S. levels, driven by vast geography and fewer big-box stores per capita. Provincial building codes that favor ENERGY STAR appliances further stimulate high-efficiency model sales, expanding the North America microwave oven market footprint north of the border.

Mexico remains the production workhorse of the region, leveraging nearshoring momentum that brought appliance investment from Whirlpool, Electrolux, Samsung, and Mabe. Domestic demand is smaller but rising alongside middle-class purchasing power. Currency volatility and tariff policy could affect local affordability, yet proximity advantages keep Mexico integral to continental supply resilience.

Competitive Landscape

Market leadership is fragmented. Whirlpool, LG Electronics, Samsung, and GE Appliances, each leveraging deep R&D, brand equity, and multi-channel distribution. GE’s IoT Breakthrough Award as 2025 “Smart Appliance Company of the Year” underscores the strategic shift toward connected features like CookCam AI that personalize cooking cycles. LG and Samsung integrate microwaves into wider smart-home ecosystems that bundle refrigerators and dishwashers, reinforcing lock-in.

Product differentiation pivots on design, connectivity, and multifunctionality rather than core microwave output. Sharp’s Celerity High-Speed Oven introduces inverter-assisted convection that roasts a chicken three times faster than a conventional oven, illustrating performance rivalry. Niche disruptors such as Brava exploit gaps with light-based rapid cookers targeting wellness-minded seniors. Established brands respond by adding non-toxic interiors and PFAS-free coatings to safeguard health credentials.

Price competition intensifies online, yet premium segments command higher margins thanks to flush-mount aesthetics and integrated recipe platforms. Warranty extensions and subscription-based cooking apps become new revenue layers.

North America Microwave Oven Industry Leaders

Whirlpool Corporation

LG Electronics Inc.

Samsung Electronics Co., Ltd.

GE Appliances (Haier)

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Panasonic launched the HomeCHEF Connect 4-in-1 Multi-Oven with Kitchen+ app guidance.

- February 2025: Sharp showcased the Celerity High-Speed Oven with inverter-based microwave and True European Convection at KBIS 2025.

- January 2025: GE Appliances won “Smart Appliance Company of the Year” in the 2025 IoT Breakthrough Awards.

- December 2024: LG Electronics revealed a microwave with a 27-inch LCD touchscreen and speakers, pushing interface boundaries.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the North America microwave oven market as the value of new residential and light-commercial ovens that heat food primarily by dielectric microwave energy, sold through B2C retail and B2B project channels across the United States, Canada, and Mexico.

Scope Exclusions: We intentionally leave out industrial microwave drying systems, laboratory units, and aftermarket parts so the numbers reflect only finished ovens purchased by households, food-service outlets, and small offices.

Segmentation Overview

- By Product

- Solo

- Grill

- Convection

- Other Products

- By Structure

- Countertop

- Built-in / Wall

- Over-the-Range

- By Control Feature

- Button Controls

- Dial Controls

- By Capacity

- Up to 19 litres

- 20 to 24 litres

- 25 to 29 litres

- 30 litres & above

- By Application

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Multi-brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- B2B/Directly from the Manufacturers

- B2C/Retail

- By Geography

- Canada

- United States

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts supplemented desk work with interviews and structured questionnaires involving regional appliance distributors, kitchen designers, mass-merchandise buyers, and service technicians across the Sun Belt, Great Lakes, and major Canadian metros. These conversations clarified replacement cycles, builder pull-through demand, and the real-world share of convection-enabled units, letting us refine penetration assumptions and validate preliminary model outputs.

Desk Research

We began with public datasets that anchor ownership and flow variables, such as household counts from the US Census and Statistics Canada, appliance shipment tallies from AHAM, and import records pulled from USITC and Mexico's SAT customs portal. Trade association white papers on smart-appliance adoption, Energy Star efficiency certifications, and Consumer Technology Association retail surveys offered directional trend lines on connected models and price band shifts. To profile corporate footprints and gauge average selling prices, analysts tapped D&B Hoovers and Dow Jones Factiva. The sources cited above are illustrative; many additional documents, databases, and press releases were consulted to cross-check figures and definitions.

Market-Sizing & Forecasting

A top-down construct begins with household stock, new housing completions, and commercial food-service outlet counts, which are then multiplied by observed penetration or replacement rates to recreate yearly demand pools. Select bottom-up tests, channel checks on unit shipments, and sampled average selling price times volume roll-ups act as reasonableness gates. Key variables include: 1) average replacement cycle length, 2) smart-connected model penetration, 3) retail average selling price migration between specified bands, 4) import duty changes on components, and 5) new housing starts. Forecasts rely on multivariate regression supported by smoothing techniques to project each driver before aggregating totals. Gaps in shipment data are bridged with moving averages anchored to import disclosures and verified with expert calls.

Data Validation & Update Cycle

Outputs pass a two-step peer review, followed by variance checks against historical shipment ratios and energy-efficiency certification issuances. Material anomalies trigger re-contact of sources. Reports refresh every twelve months, with interim updates whenever tariffs, major recalls, or regulatory shifts materially alter the baseline.

Why Mordor's North America Microwave Oven Baseline Commands Stakeholder Confidence

Published estimates frequently diverge because firms pick different product mixes, apply varying ASP ladders, or refresh at uneven intervals.

Key gap drivers here include competitor inclusion of heavy-duty industrial ovens, omission of over-the-range channel splits, and use of retail mark-ups without customs reconciliation. Mordor's disciplined scope, annual refresh cadence, and dual-path validation deliver a figure decision-makers can trace and reproduce with publicly accessible inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.15 B (2025) | Mordor Intelligence | - |

| USD 6.79 B (2024) | Regional Consultancy A | Counts all microwave appliances, including high-power industrial units; silent on channel breakdowns |

| USD 5.32 B (2024) | Global Consultancy B | Uses shipment data layered with retail mark-ups; limited geographic granularity beyond the U.S. |

In sum, the modest delta between our baseline and external figures stems mainly from tighter product definition and rigorous cross-checks. That discipline gives clients a balanced, transparent reference they can rely on when sizing opportunities or benchmarking performance.

Key Questions Answered in the Report

What is the current value of the North America microwave oven market?

It is USD 5.35 billion in 2026 and is forecast to reach USD 6.49 billion by 2031.

How fast is the market growing?

The market is expected to expand at a 3.92% CAGR between 2026 and 2031.

Which product type holds the largest share today?

Convection microwaves lead with 51.30% of regional revenue.

Why are built-in models gaining traction?

Kitchen renovations and flush-mount designs are driving built-in units to grow 5.33% annually.

What is the biggest restraint on future unit growth?

Household penetration above 90% in the United States and Canada shifts demand to slower, replacement-only cycles.

Page last updated on: