Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.23 Billion |

| Market Size (2026) | USD 4.37 Billion |

| Market Size (2031) | USD 5.45 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

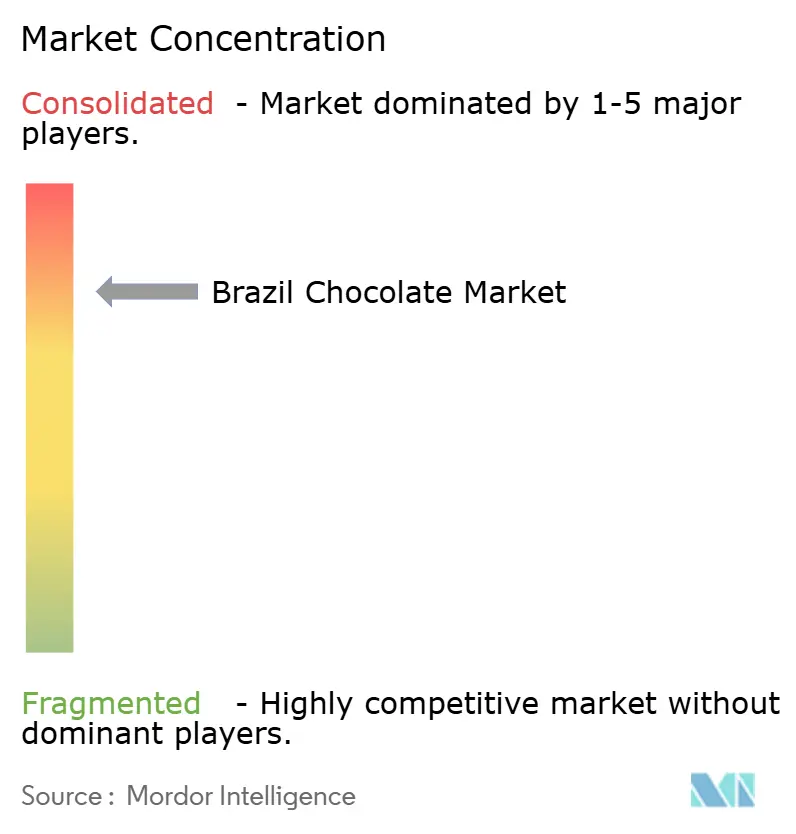

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Chocolate Market Analysis by Mordor Intelligence

The Brazil chocolate market size is expected to increase from USD 4.23 billion in 2025 to USD 4.37 billion in 2026 and reach USD 5.45 billion by 2031, growing at a compound annual growth rate (CAGR) of 4.51% over 2026-2031. This growth is occurring amidst volatile cocoa prices, increasing household penetration, and the continued influence of gifting traditions on demand. Despite inflation prompting consumers to opt for smaller pack sizes instead of switching to private labels, the consumption gap compared to Europe highlights significant potential for volume growth. Oligopolistic consolidation, as demonstrated by Nestlé’s USD 900 million acquisition of Grupo CRM, has strengthened the bargaining power of leading suppliers and intensified competition for shelf space. The premium segment, driven by bean-to-bar artisans, is expanding at a faster rate than the mass market, while rising health-consciousness and stricter front-of-pack labeling regulations are boosting demand for dark chocolate. Furthermore, online retail, driven by trends on social media platforms, has emerged as the fastest-growing channel, transforming route-to-market strategies through direct-to-consumer models and last-mile delivery partnerships.

Key Report Takeaways

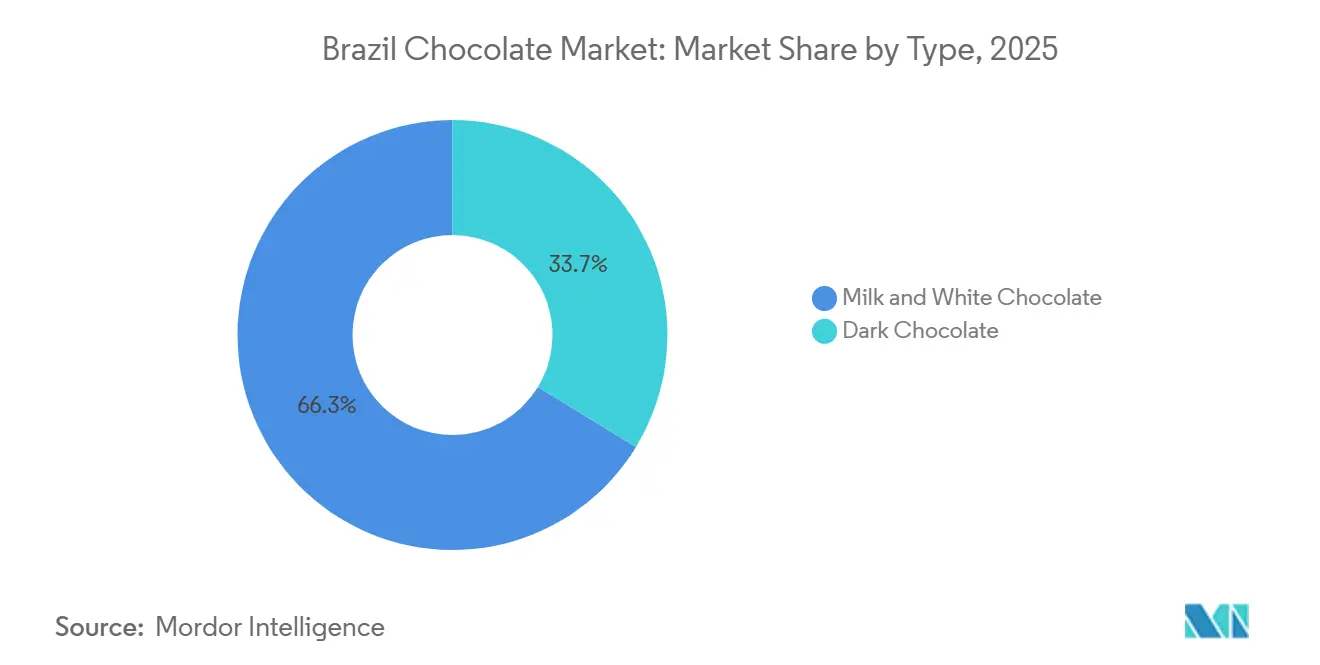

- By type, milk and white chocolate led with 66.29% of the Brazil chocolate market share in 2025, whereas dark chocolate is advancing at a 5.18% CAGR through 2031.

- By category, sugar-based chocolate accounted for 80.13% share of the Brazil chocolate market size in 2025 and sugar-free chocolate is forecast to expand at a 5.08% CAGR through 2031.

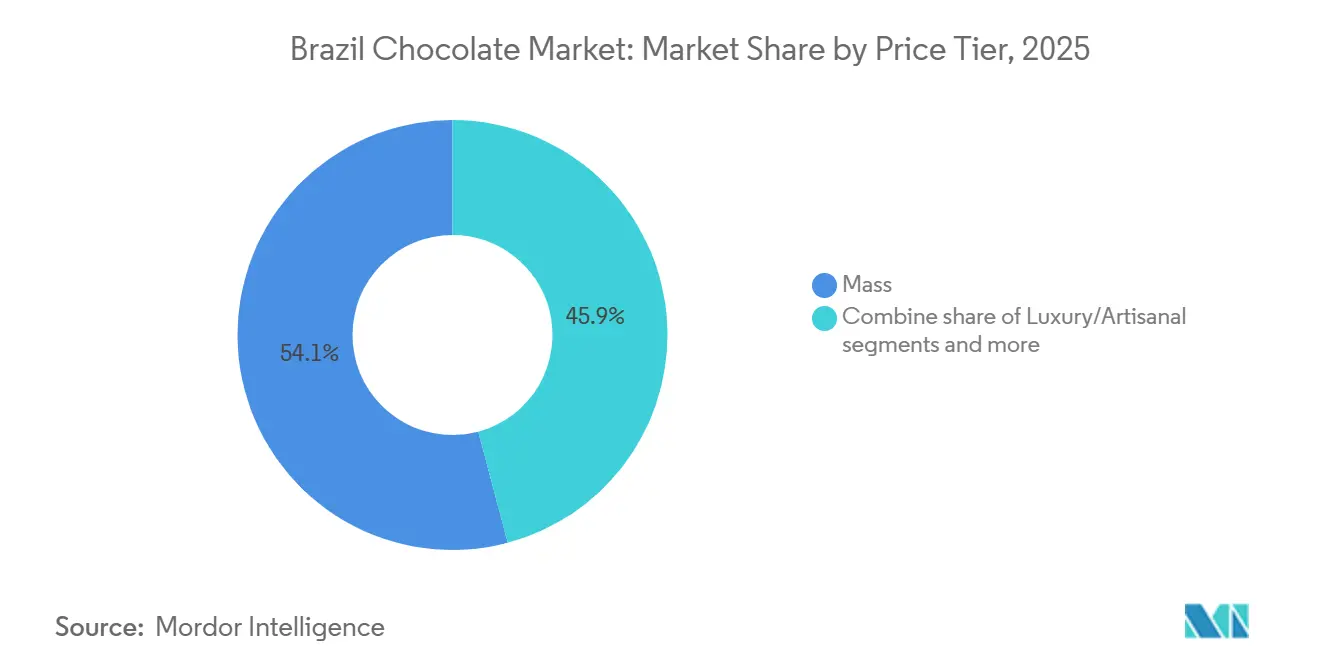

- By price tier, mass chocolate offerings held 54.13% of the Brazil chocolate market size in 2025 and luxury/artisanal chocolate is projected to register the fastest 5.25% CAGR through 2031.

- By distribution channel, online retail captured the highest 5.47% CAGR between 2026-2031, while supermarkets and hypermarkets retained 46.52% of 2025 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban snacking culture and on-the-go consumption | +0.9% | National, with concentration in São Paulo, Rio de Janeiro, Brasília metropolitan areas | Medium term (2-4 years) |

| Gifting and seasonal consumption traditions | +1.2% | National, with Easter peak in Southeast and South regions | Short term (≤ 2 years) |

| Premiumization and artisanal chocolate appeal | +0.7% | Southeast urban centers (São Paulo, Rio de Janeiro), expanding to South | Long term (≥ 4 years) |

| Rising preference for dark and high-cocoa chocolate | +0.6% | Southeast and South regions, affluent urban demographics | Medium term (2-4 years) |

| Influence of social media and digital marketing | +0.8% | National, strongest among Gen Z and millennial cohorts in urban areas | Short term (≤ 2 years) |

| Localization of flavors and formats | +0.4% | Regional variations- Northeast (tropical fruits), Southeast (brigadeiro), South (European styles) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban snacking culture and on-the-go consumption

Urbanization in Brazil has played a key role in integrating chocolate into daily snacking routines, especially among commuters and office professionals who seek convenient options. The increasing demand for single-serve formats and impulse purchases at convenience stores and cash-and-carry outlets has reshaped consumer buying behavior, with these channels capturing a larger share of category sales. Nestlé responded to this trend by introducing Choco Trio, a combination of chocolate and biscuits, while Hershey’s Eaternet campaign targeted younger consumers by promoting confectionery as a way to alleviate digital fatigue. Furthermore, the growing presence of major cash-and-carry retailers such as Assaí Atacadista and Atacadão has improved access to mid-tier chocolate brands in suburban and peripheral urban areas. These changing snacking preferences have also influenced seasonal consumption patterns. For instance, chocolate bars outperformed traditional boxed assortments during the Easter season as consumers opted for more accessible, grab-and-go options instead of formal gifting choices.

Gifting and seasonal consumption traditions

Easter, Valentine’s Day in Brazil, and Christmas contribute significantly to annual chocolate revenue. During Easter, production volumes were deliberately reduced to address the rising costs of cocoa. Cacau Show, a prominent chocolate manufacturer, focused on driving revenue growth through higher pricing and increased investments in marketing, particularly targeting children’s products, which have become a more important category compared to a decade ago. For Valentine’s Day, retail performance was strong, with chocolates remaining one of the most preferred gift options. Mobile electronic commerce (e-commerce) played a crucial role in enabling last-minute purchases, especially among male consumers. During the Christmas season in Rio Grande do Sul, the market experienced steady growth as consumers preferred smaller, boxed chocolate assortments for affordable gifting amid economic recovery. The consistent seasonal demand allows manufacturers to plan production and secure cocoa futures in advance. However, inflationary pressures from both domestic and import price increases continue to challenge consumer affordability and pricing strategies.

Premiumization and artisanal chocolate appeal

The bean-to-bar chocolate movement in Brazil is witnessing notable growth, supported by the Bean to Bar Brasil association, which plays a key role in promoting artisanal producers such as Nugali, Mestiço Chocolates, and Labarr Chocolate. These brands have achieved international recognition through prestigious competitions. Dengo Chocolates has shown its commitment to the premium and artisanal chocolate segment by announcing a significant investment plan to establish a new manufacturing facility in Southeast Brazil. The luxury chocolate category is currently the fastest-growing segment in the market. Nestlé has strengthened its presence with the KitKat Chocolatory in Brazil, which offers a wide variety of flavors designed to appeal to Generation Z consumers who value customization and visually appealing, shareable products. This strategy has contributed to strong retail performance in recent months. São Paulo has become a hub for specialty chocolate boutiques, while Cacau Show bridges the gap between mass-market and premium consumers by offering artisanal-inspired products at more accessible price points. The trend toward premiumization is further supported by Brazil’s status as a net importer of cocoa, primarily sourced from West Africa. This dynamic enhances the perception of quality, as brands increasingly highlight single-origin sourcing and ethical certifications to attract discerning consumers.

Rising preference for dark and high-cocoa chocolate

Dark chocolate is expected to grow at a compound annual growth rate (CAGR) of 5.18% through 2031, outpacing the growth of milk and white chocolate. This growth is driven by health-conscious consumers who are increasingly seeking products with lower sugar content and higher levels of polyphenols. In Brazil, the National Health Surveillance Agency's (ANVISA) Resolução da Diretoria Colegiada (RDC) 264/2005 mandates that products labeled as "chocolate" must contain a minimum of 25% cocoa solids. Products that do not meet this requirement must carry a "sabor chocolate" (chocolate-flavored) disclaimer, creating a regulatory standard that supports the credibility of dark chocolate variants [1]Source: Agência Nacional de Vigilância Sanitária, “RDC 429/2020,” gov.br/anvisa. Furthermore, the front-of-pack labeling regulation (RDC 429/2020) requires a magnifying-glass symbol on products containing more than 15 grams of added sugar per 100 grams [2]Source: World Trade Organization, “Guidelines on Front-of-Pack Nutrition Labelling,” wto.org. This regulation has resulted in 100% of surveyed chocolates being categorized under the high-warning label, inadvertently strengthening dark chocolate's image as a "better for you" indulgence. Brands are aligning with this trend. For example, Cacau Show has expanded its product range to include bars with higher cocoa content, while Dengo highlights the unique characteristics of Brazilian cacao. Mondelez has also adapted by introducing its 5Star candy bar, utilizing Aquto's sponsored-data mechanics to engage health-conscious millennials through digital platforms instead of traditional sugar-focused messaging. Beyond its health benefits, dark chocolate also acts as a gateway for premiumization, allowing brands to justify higher price points through functional claims and artisanal storytelling.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -0.3% | National, enforced by ANVISA | Short term (≤ 2 years) |

| Emerging sugar and health policy pressures | -0.5% | National, with potential regional variations | Medium term (2-4 years) |

| Negative perception of chocolate as unhealthy | -0.4% | Urban centers with higher health awareness (Southeast, South) | Medium term (2-4 years) |

| Rising consumer scrutiny of ingredients and additives | -0.3% | National, strongest among educated urban demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety and labeling regulations

The Brazilian Health Regulatory Agency (ANVISA), through its Resolução da Diretoria Colegiada (RDC) 429/2020, introduced front-of-pack nutrition labeling requiring magnifying-glass warnings on products exceeding thresholds for added sugar, saturated fat, or sodium. Implemented in October 2022, this regulation has significantly impacted confectionery manufacturers, with all surveyed Easter chocolate products surpassing the permissible limits for sugar and saturated fat. Compliance involves substantial costs per stock-keeping unit (SKU), including packaging redesign, laboratory testing, and regulatory submissions, which are particularly burdensome for small-scale producers. ANVISA’s Resolução da Diretoria Colegiada (RDC) 264/2005 also mandates minimum cocoa solid and cocoa butter content for chocolate and white chocolate, respectively, with non-compliant products labeled as "chocolate flavor," reducing their premium positioning. Enforcement varies regionally, with states like São Paulo and Rio de Janeiro conducting regular audits, while northern and central-western regions experience less oversight. The regulatory burden intensifies during peak periods like Easter, leading to supply chain disruptions, product recalls, and financial penalties for non-compliance, complicating operations for manufacturers.

Emerging sugar and health policy pressures

Brazil’s National Health Surveillance Agency (Agência Nacional de Vigilância Sanitária) implemented front-of-pack labeling regulations under RDC 429/2020, which became effective in October 2022. These regulations require magnifying-glass warnings on packaged foods that exceed specified limits for added sugar, saturated fat, or sodium content. In 2023, a survey conducted by the Brazilian Institute of Consumer Protection found that while most Easter chocolate products complied with the labeling requirements, nearly all exceeded the nutrient thresholds for saturated fat and added sugar, categorizing much of the segment as ultra-processed. In contrast to Chile, where products displaying high-warning labels are subject to strict marketing restrictions aimed at children, Brazil’s framework does not impose advertising limitations. This has sparked ongoing debates and pressure from health advocates for stronger measures. At the same time, production costs have risen as manufacturers work to reformulate products and reduce sugar content, leading to noticeable price increases across the market. Furthermore, the sugar-free chocolate segment is experiencing steady growth; however, the higher cost of alternative sweeteners such as stevia and erythritol compared to traditional sugar continues to challenge profitability and pricing strategies for brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Health Narratives Propel Dark Chocolate

Milk and white chocolate accounted for 66.29% of the market share in 2025, driven by mass-market brands such as Lacta, Bis, and Garoto, which dominated supermarket shelves and traditional retail channels. In contrast, dark chocolate grew at a compound annual growth rate (CAGR) of 5.18% through 2031. This growth reflected a structural shift as health-conscious urban consumers increasingly favored products with higher cocoa content and lower sugar levels. This trend was further influenced by the Brazilian Health Regulatory Agency (ANVISA)'s front-of-pack warnings, which identified that 100% of surveyed chocolates contained excessive saturated fat or added sugar.

Nestlé’s KitKat Chocolatory has introduced a wide range of dark chocolate options designed to attract Generation Z consumers who value both indulgence and health-focused benefits. In a similar effort, Dengo Chocolates is making significant long-term investments to strengthen its focus on premium, single-origin dark chocolate bars, which are positioned at a higher price point compared to regular milk chocolate. While dark chocolate continues to gain popularity, milk and white chocolate remain in strong demand, supported by traditional gifting occasions such as Easter and Valentine’s Day in Brazil. At the same time, the increasing share of children’s products during festive seasons highlights a growing consumer preference for sweeter flavor profiles.

By Category: Sugar-Free Gains Despite Regulatory Headwinds

Sugar-based chocolate held 80.13% of the category share in 2025. However, sugar-free variants are projected to grow at a compound annual growth rate (CAGR) of 5.08% through 2031, marking the fastest growth rate within the segment. This growth is driven by the Brazilian Health Regulatory Agency (ANVISA) enforcing warning labels and the rising stigma associated with ultra-processed foods, prompting reformulation efforts. Artisanal brand Jupará Chocolates has launched zero-sugar options priced between USD 5.45 and USD 14.55, targeting diabetic and weight-conscious consumers who are willing to pay two to three times more than the price of conventional chocolate bars.

Although the market for sugar-free chocolate is experiencing growth, its adoption remains limited due to higher production costs associated with alternative sweeteners like stevia and erythritol, which are considerably more expensive than regular sugar. Additionally, taste-related challenges persist, as consumer taste panels often find sugar-free variants less appealing in terms of flavor and texture. Mondelez’s launch of the 5Star candy bar, supported by Aquto’s sponsored-data program, strategically shifted focus from the sugar content debate to digital engagement, emphasizing interactive brand experiences over nutritional claims. This strategy resonates particularly with millennial consumers, who prioritize engaging brand interactions over detailed ingredient information. The sustained popularity of traditional sugar-based chocolate highlights the influence of Brazil’s gifting culture, where occasions such as Easter and Valentine’s Day prioritize indulgence and enjoyment over health-conscious choices. Recent consumer spending trends during major festive seasons further indicate that shoppers preferred to absorb rising product prices rather than opt for sugar-free alternatives.

By Price Tier: Luxury Segment Defies Trade-Down Pressures

The mass segment accounted for 54.13% of the 2025 market share, driven by brands such as Lacta, Bis, and Garoto, which are priced between USD 0.55-1.45 per bar and dominate supermarket and atacarejo (cash-and-carry) channels. In comparison, luxury and artisanal chocolate, while holding 45.87% of the market, is projected to grow at a compound annual growth rate (CAGR) of 5.25% through 2031, the fastest among price tiers. The market growth is driven by affluent consumers who increasingly value the authenticity of bean-to-bar chocolates and the appeal of visually engaging brand experiences. Cacau Show, by leveraging its extensive retail network, effectively bridges the gap between the mass market and premium segments by offering artisanal-style chocolate products at accessible price points [3]Source: Bean to Bar Brasil, “Brazilian Chocolate Makers Win International Awards,” beantobarbrasil.org. Dengo Chocolates is expanding its presence in the luxury chocolate market with a substantial investment plan extending through the end of the decade, focusing on single-origin bars positioned at premium price points.

Nestlé has strengthened its position in the high-end gifting category by acquiring Grupo CRM, the owner of the Kopenhagen and Brasil Cacau brands. This acquisition has enhanced Nestlé's access to a segment characterized by significantly higher profit margins compared to mass-market products. While many Brazilian consumers displayed trade-down behavior in the subsequent year, this primarily involved adjustments in package sizes rather than a shift to lower-priced alternatives. Consumers continued to purchase their preferred brands, choosing smaller formats instead of switching to private labels. The premium chocolate segment remained resilient, particularly during key gifting occasions such as Easter, Valentine’s Day (Dia dos Namorados), and Christmas, when consumers are less price-sensitive and prioritize quality and brand experience. These trends highlight the importance of maintaining brand loyalty and delivering high-quality products in the premium chocolate market.

By Distribution Channel: E-Commerce Reshapes Retail Dynamics

In 2025, supermarkets and hypermarkets accounted for 46.52% of the distribution share, driven by impulse-buy placements and promotional bundles. However, their compound annual growth rate (CAGR) of 4.51% is lower than the 5.47% growth rate of online retail, which is the fastest-growing distribution channel. Mondelez's strategic goal to increase its Brazil sales through digital channels to 30% by 2030, up from 10% in 2023, highlights the structural benefits of e-commerce. These benefits include reduced overhead costs, algorithmic targeting, and subscription models that ensure recurring revenue.

During Dia dos Namorados (Brazilian Valentine's Day) in 2025, mobile devices accounted for the majority of online chocolate purchases, as last-minute male buyers prioritized convenience over in-store shopping. Online sales continue to grow annually, with chocolate representing an estimated 6% of supermarket revenue. This share is higher online, driven by gifting and subscription box models. While convenience stores and specialty stores hold smaller market shares, they play important strategic roles. Convenience stores address on-the-go snacking needs in urban areas, whereas specialty stores, such as Cacau Show with 5,000 locations and Kopenhagen with over 800 outlets, offer brand experiences that support premium pricing strategies.

Geography Analysis

Chocolate consumption in Brazil is predominantly concentrated in the Southeast region, particularly in the metropolitan areas of São Paulo and Rio de Janeiro. This concentration is attributed to dense urban populations, higher per capita incomes, and a well-developed retail infrastructure, including 15 specialty chocolate shops in São Paulo alone. The South region, led by Rio Grande do Sul’s robust manufacturing base and supported by established confectionery companies such as Florybal and Neugebauer, experienced notable growth in Christmas sales during December 2024. Demand for small boxed chocolates, locally known as bombons, rose significantly as consumers opted for more affordable gifting options, reflecting the positive effects of the region’s ongoing economic recovery.

Nestlé's Caçapava factory in São Paulo state, the largest chocolate production facility in Latin America, is set to expand to six exclusive production lines by 2028. This expansion reinforces the Southeast's dominance in manufacturing and supply chain efficiencies, which reduce logistics costs by 15-20% compared to production in the Northeast or North regions. Meanwhile, Barry Callebaut's establishment of a logistics hub in the Northeast in 2024 highlights the growing focus on regional demand dispersion. The Northeast region, with improving infrastructure and a rising middle class, offers untapped growth potential despite lower per capita consumption compared to the Southeast.

Urbanization in cities such as Recife, Fortaleza, and Salvador is contributing to narrowing consumption disparities in the Northeast and North regions. While these regions continue to face challenges related to income inequality and distribution, they present significant growth opportunities. Cash-and-carry outlets, including Assaí and Atacadão, have been more effective in reaching consumers in these areas compared to traditional supermarkets, as they provide bulk purchasing options tailored to lower-income households. Cocoa cultivation remains concentrated in Bahia, located in the Northeast; however, the region has experienced substantial production setbacks due to witches’ broom disease, which has significantly reduced yields over the years. Consequently, Brazil has become increasingly dependent on cocoa imports from major producers such as Ivory Coast and Ghana, heightening the vulnerability of its confectionery supply chain to external factors.

Competitive Landscape

Brazil's chocolate market operates within an oligopolistic structure dominated by multinational corporations, including Nestlé SA, Mondelez International Inc., Ferrero International SA, Mars Inc., and Hershey Co. These companies collectively account for the majority of retail value sales. The market has seen increasing consolidation as major players focus on acquisitions to strengthen their competitive positions. For instance, Nestlé's acquisition of Grupo CRM, which owns premium chocolate brands Kopenhagen and Brasil Cacau, expanded its presence through a large network of specialty stores and enhanced its vertical integration from manufacturing to branded retail. Similarly, Ferrero's acquisition of Dori Alimentos represented a strategic move into adjacent confectionery segments, diversifying its portfolio to include gummy and sugar confectionery products under brands such as Dori, Pettiz, and Jubes.

Market growth is being driven by strategies centered on premiumization and artisanal craftsmanship. Emerging local brands like Dengo and established players such as Cacau Show are expanding their presence and investing in brand experiences. Digital commerce is also becoming a significant growth driver, with companies like Mondelez International setting ambitious targets to increase online sales contributions in the coming years. Additionally, nostalgic brand revivals, such as Nestlé's renewed focus on its classic Caribe range, aim to reconnect with traditional consumers while broadening market reach.

Strong growth momentum is evident in the sugar-free, luxury, and artisanal chocolate segments, supported by evolving consumer preferences for healthier and more premium options. However, rising cocoa prices are tightening profit margins, particularly affecting larger manufacturers. Smaller bean-to-bar producers, which rely on direct sourcing, are better positioned to maintain quality and cost efficiency under these conditions. Boutique brands such as Nugali, Mestiço Chocolates, and Labarr Chocolate are gaining prominence by leveraging international recognition and social media engagement to command premium pricing. A notable example of digital and social platforms influencing consumer trends is Cacau Show's viral launch of its LaNut Pistache Dubai bar, which gained significant traction on TikTok. This underscores the growing role of social commerce in accelerating innovation cycles and benefiting agile market players.

Brazil Chocolate Industry Leaders

Mondelez International Inc.

Nestlé SA

Cacau Show

Ferrero International SA

Arcor S.A.I.C

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Brazil's largest conilon coffee cooperative, Cooabriel, launches a cocoa pilot project in Bahia state with Cargill's support, targeting 10,000 bags initially. This initiative aims to revive domestic cocoa production post-1980s disease losses, enhancing self-sufficiency for the chocolate market.

- December 2025: Barry Callebaut and Nestlé partner to accelerate net-zero cocoa production in Brazil, empowering farmers with seedlings, agroforestry, and financial support across three projects. Leveraging Barry Callebaut's 6 million seedling nursery expertise, the initiative fosters sustainable cocoa sector growth and climate-friendly expansion.

- July 2025: Nestlé Professional partnered with KitKat to launch a chocolate beverage maker using Nescafé Fusion pods, debuting in Brazil for out-of-home venues like convenience stores and bakeries. The machine delivers authentic KitKat-flavored hot chocolates, targeting professionals before global rollout.

Brazil Chocolate Market Report Scope

The Brazil chocolate market includes the consumption of various chocolate products and reflects evolving health trends that favor premium and functional variants. The market is experiencing robust growth driven by innovation in flavors, sustainable sourcing practices, and the expansion of retail networks.The Brazil chocolate market is segmented into chocolate types, dark chocolate, and milk and white chocolate. By category, the market is segmented into sugar and sugar-free. The market is segmented by price tier into mass, premium, and luxury/artisanal. By distribution channel the market is segmented into supermarkets/ hypermarkets, convenience stores, specialty stores, online retail, and others. The market sizing has been done in value terms in USD and volume in tonnes for all the abovementioned segments.

By Type

| Dark Chocolate |

| Milk and White Chocolate |

By Category

| Sugar |

| Sugar-free |

By Price Tier

| Mass |

| Premium |

| Luxury/Artisanal |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail |

| Others |

| By Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Category | Sugar |

| Sugar-free | |

| By Price Tier | Mass |

| Premium | |

| Luxury/Artisanal | |

| By Distribution Channel | Supermarkets/ Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Others |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms