Metallic Stearate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

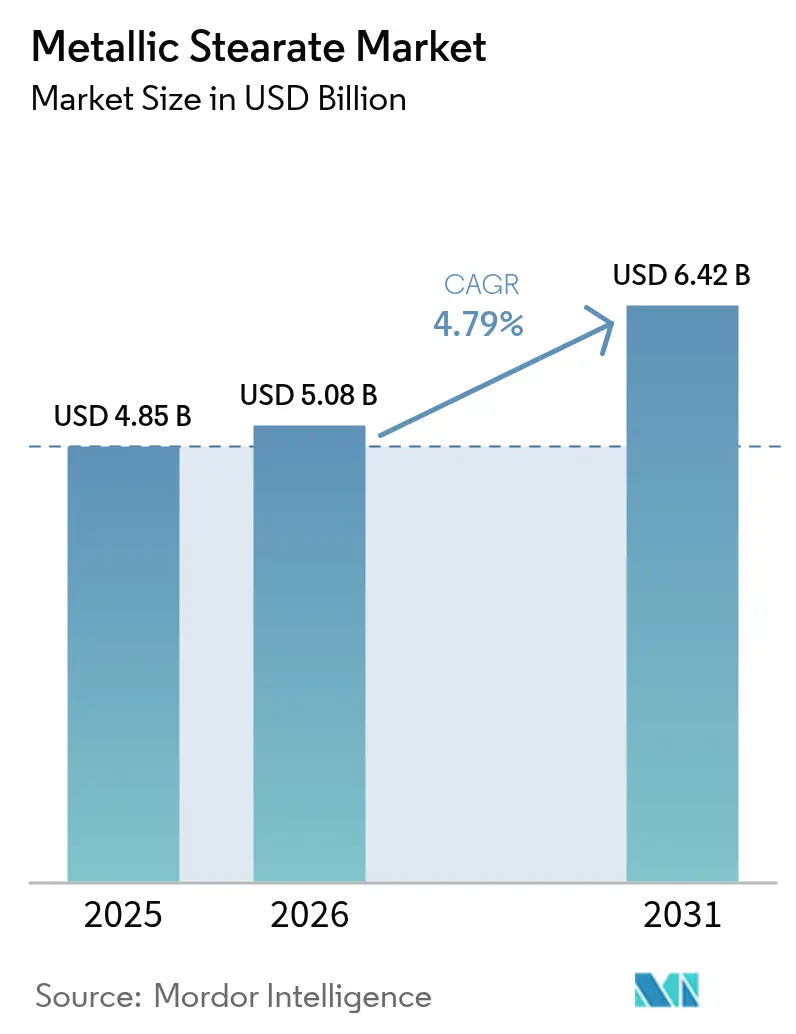

| Market Size (2026) | USD 5.08 Billion |

| Market Size (2031) | USD 6.42 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metallic Stearate Market Analysis by Mordor Intelligence

The Metallic Stearate Market size was valued at USD 4.85 billion in 2025 and estimated to grow from USD 5.08 billion in 2026 to reach USD 6.42 billion by 2031, at a CAGR of 4.79% during the forecast period (2026-2031). Combining polymer production growth, regulatory shifts favoring calcium-zinc stabilizer systems, and rising pharmaceutical tablet output reinforce demand stability. Steady appetite for lightweight plastics in automotive and packaging, coupled with robust Asian manufacturing capacity, underpins near-term momentum. At the same time, stricter limits on lead in PVC and improvements in drug-formulation technology are steering end users toward higher-purity products that comply with emerging quality norms. Feedstock price swings tied to palm-oil markets present cost headwinds, yet the metallic stearate market continues to expand as producers adopt vertical integration, diversify sourcing, and invest in low-dust dispersion technologies.

Key Report Takeaways

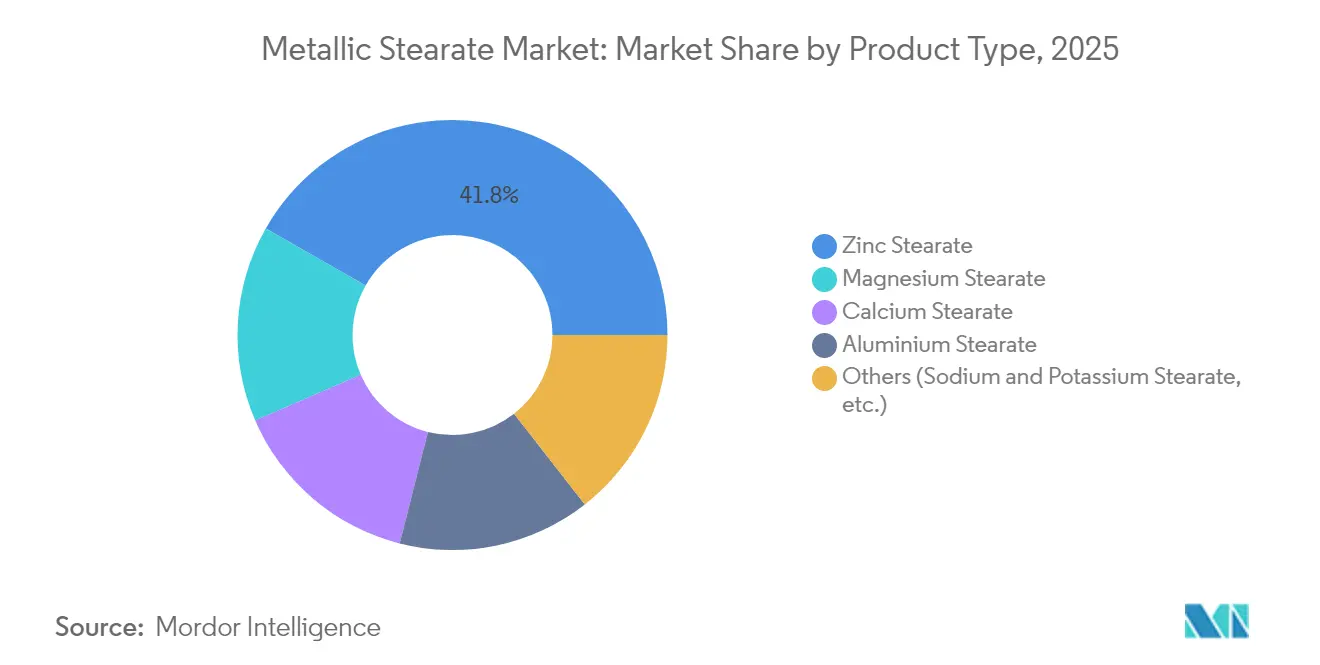

- By product type, zinc stearate led with 41.75% metallic stearate market share in 2025; magnesium stearate is projected to advance at a 6.15% CAGR through 2031.

- By form, powder held 46.90% share of the metallic stearate market size in 2025, whereas aqueous dispersions are set to grow at 6.78% CAGR by 2031.

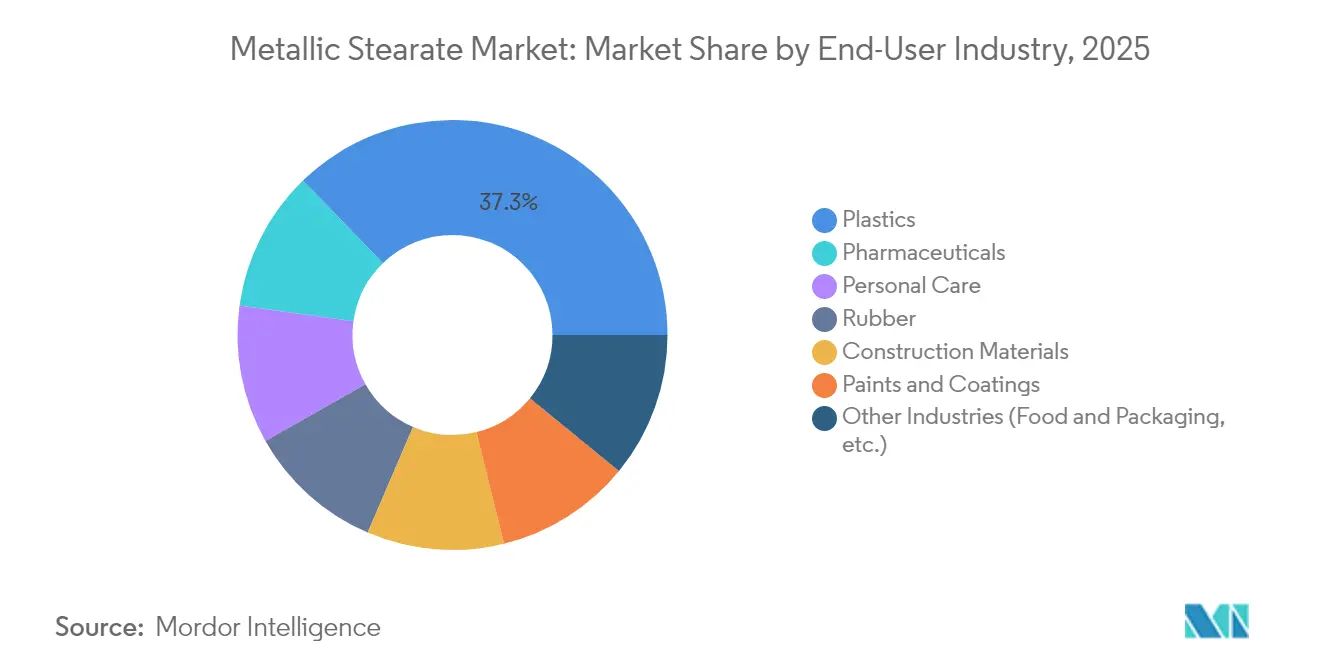

- By end-use industry, plastics and polymers accounted for 37.25% of the metallic stearate market size in 2025, while pharmaceuticals are forecast to post the highest 5.92% CAGR to 2031.

- By geography, Asia-Pacific commanded 50.85% metallic stearate market share in 2025 and is forecast to expand at 5.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metallic Stearate Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of global plastics production | +1.8% | Global, with APAC leading | Medium term (2-4 years) |

| Pharmaceutical tablet output surge | +1.2% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Rising cosmetics consumption | +0.9% | Global, with strong growth in emerging markets | Medium term (2-4 years) |

| Shift to lead-free PVC stabilizers | +1.1% | Europe & North America, spreading globally | Short term (≤ 2 years) |

| Rising Demand from Rubber Segment | +0.8% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Global Plastics Production

Escalating polyethylene and polypropylene output boosts additive demand as processors rely on metallic stearates to shorten cycle times and improve surface finish. Lightweight vehicle design and recycled-content packaging intensify the need for stable formulations that resist discoloration and thermal degradation. China’s polymer capacity leadership ensures regional consumption remains strong, while Southeast Asia’s integrated supply chains offer both feedstock availability and cost advantages. Emerging applications in battery casings and photovoltaic back-sheets extend growth beyond legacy sectors. This diversified pull across automotive, building-products, and flexible-packaging segments underlies a resilient outlook for the metallic stearate market[1]PMC Biogenix, “Metallic stearates in polymer processing,” pmcbiogenix.com.

Pharmaceutical Tablet Output Surge

Higher life-expectancy and biologic drug innovation push global solid-dosage production upward, elevating the role of magnesium stearate as a proven lubricant. Between 2012 and 2023, the United States Food and Drug Administration cleared 48 new drug approvals that rely on amorphous solid dispersions, a formulation class in which metallic stearates enhance stability and compressibility. Continuous-manufacturing platforms favor aqueous dispersions that reduce dust and speed cleaning cycles, further stimulating liquid-form uptake. Expansion of generics in India and injectable-to-oral switches in Latin America widen the demand base. Consequently, pharmaceutical preferences shift toward high-purity grades with strict endotoxin limits that support competitiveness in regulated markets[2]Roquette Frères, “Magnesium stearate excipient applications,” roquette.com.

Rising Cosmetics Consumption

Demand for long-lasting makeup, sunscreens, and men’s grooming products lifts usage of aluminum and zinc stearates that act as rheology modifiers and water-repellents. Emerging-market consumers are trading up to premium brands, increasing formulation complexity and requiring ingredients that maintain texture under humid conditions. Plant-based feedstocks resonate with sustainability-minded buyers, and suppliers now highlight palm-kernel-derived stearic acid traceability. Regulatory scrutiny of talc drives brand owners to favor metallic stearates as alternative slip agents in pressed powders. Digital commerce accelerates product-launch cadence, raising the need for multipurpose raw materials that streamline formulation libraries.

Shift to Lead-Free PVC Stabilizers

European Union Regulation 923/2023 caps lead in PVC below 0.1% by weight, which speeds adoption of calcium-zinc systems that depend on calcium stearate as a co-stabilizer. Building-material makers in cables, pipes, and siding have validated performance equivalency at similar dosage levels. Market leaders have introduced proprietary blends that lower plate-out and odor, meeting both technical and environmental targets. United States construction specifications are also moving toward lead-free content, broadening worldwide uptake. Producers with in-house calcium stearate capacity therefore secure early-mover benefits and strengthen customer lock-in.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter occupational exposure limits | -0.7% | Global, with stricter enforcement in developed markets | Short term (≤ 2 years) |

| Stearic-acid feedstock price volatility | -0.5% | Global, with higher impact in import-dependent regions | Medium term (2-4 years) |

| Substitution by montan-wax slip agents | -0.3% | Europe & North America, limited APAC impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Occupational Exposure Limits

The National Institute for Occupational Safety and Health sets a time-weighted average of 10 mg/m³ total particulate and 5 mg/m³ respirable particulate for zinc stearate dust. Updated Hazard Communication Standard alignment with the Globally Harmonized System obliges manufacturers to upgrade safety-data sheets, alter labels, and invest in dust-collection equipment. Workplaces shift toward granules and liquid dispersions that minimize airborne particles, adding conversion costs yet opening premium pricing opportunities. Smaller compounders may defer capital upgrades, temporarily damping demand for traditional powder grades. However, sustained enforcement is expected to push the metallic stearate market toward safer delivery formats by 2027.

Stearic-Acid Feedstock Price Volatility

Palm-oil production shortfalls linked to El Niño weather patterns and biodiesel mandates in Indonesia and Malaysia tighten stearic-acid supply, raising input prices for stearate manufacturers. Import-dependent regions face amplified cost swings because freight and currency movements compound raw-material volatility. Substitution with tallow-derived fatty acids or synthetic routes remains limited by higher purification costs and regulatory hurdles in pharmaceutical and food-contact uses. Forward-buying and hedging strategies lessen exposure yet tie up working capital. Overall, raw-material instability erodes margins for producers that lack backward integration into fatty-acid refining.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Zinc Strength Maintains Position, Magnesium Picks Up Pace

Zinc stearate captured 41.75% metallic stearate market share in 2025 as its versatility across PVC, rubber, and cosmetic formulations made it an indispensable additive. Demand remains steady because compounders value its balance of lubrication, mold-release, and heat-stability properties. Incremental gains arise from recyclate-rich polyolefin blends that need efficient internal lubricants to achieve uniform melt flow. In contrast, magnesium stearate is forecast at 6.15% CAGR through 2031 thanks to surging pharmaceutical tablet volumes that rely on concentrations between 0.25% and 5% weight for proper compressibility. Regulatory familiarity and low toxicity underpin this sustained lift. Calcium stearate absorbs stable growth from waterproofing admixtures in concrete and efflorescence mitigation in cementitious products, while aluminum stearate serves niche coatings and lubricating-grease uses where high gel strength is critical. Academic collaborations targeting hybrid zinc-calcium grades illustrate a broader trend toward tailored functionality, signaling renewed innovation despite zinc stearate’s mature status in the metallic stearate market.

A secondary tier comprising sodium and potassium stearates addresses personal-care cleansers and industrial detergents that seek biodegradable profiles. Potassium stearate’s high solubility gains traction in sulfate-free shampoos, while sodium stearate supports soap bar transparency. Market leaders differentiate by offering kosher and halal certifications to meet fast-growing consumer-goods regulatory requirements. Across all chemistries, buyers demand tighter metal content specifications and traceability to sustainably sourced fatty acids. Those attributes increasingly influence contract awards, reinforcing the competitive advantage of fully integrated suppliers that control both fatty-acid and metal-salt processing under one roof.

By Form: Powder Dominance Faces Rising Liquid Preference

Powder held 46.90% share of the metallic stearate market size in 2025 because it aligns with traditional batch mixing and extrusion processes in plastics and rubber. Users appreciate its free-flowing characteristics and wide compatibility with standard feeding systems. However, workplace exposure concerns prompt many multinational pharmaceutical firms to pivot toward aqueous dispersions that are growing at a 6.78% CAGR. Liquid formats integrate easily into continuous tablet presses, eliminate dust screens, and shorten change-over times, providing total cost benefits that offset their higher purchase price. Large compounders invest in closed-loop delivery tanks that minimize spills and further support adoption.

Flakes and prills remain relevant in rubber calendering where controlled dissolution is essential to process consistency. Producers fine-tune bulk density, particle size, and moisture profile to achieve reliable feeding within high-throughput internal mixers. Innovation in dispersion technology focuses on polymer-predispersed masterbatches that offer customers dosage accuracy and improved film clarity. Several leading suppliers have launched water-based systems free of volatile amines, which broadens appeal among environmentally conscious PE and PVC processors. Collectively, these shifts underline a gradual migration away from powder dominance toward higher-value, low-dust alternatives across the metallic stearate market.

By End-User Industry: Plastics Lead, Pharmaceuticals Accelerate

Plastics and polymers consumed 37.25% of global volume in 2025, driven by large-scale packaging, automotive, and pipe applications that benefit from metallic stearates’ melt-lubricating and heat-stabilizing roles. Additive functionality will remain essential as recycled resin content rises and processors face tighter thermal windows. Meanwhile, pharmaceuticals are expected to grow at a 5.92% CAGR through 2031 as multinationals expand capacity for continuous manufacturing and biologic therapeutics. Regulatory agencies increasingly prescribe data-rich excipient documentation, which positions established grades such as NF-compliant magnesium stearate for ongoing preference.

The rubber industry recovers alongside vehicle production, using zinc stearate as an anti-tack agent in styrene-butadiene and butyl rubber formulations. Personal care exhibits robust mid-single-digit growth because premium skin-care and color-cosmetics lines call for water-repellent aluminum and zinc stearates that improve product feel and pigment dispersion. Construction materials gain visibility through calcium stearate admixtures that guard against capillary water ingress in concrete façades, supporting the longevity of high-value building envelopes. Each segment’s distinct technical and regulatory demands lead suppliers to broaden their technical-service teams and invest in application-specific pilot lines that reinforce customer intimacy throughout the metallic stearate market.

Geography Analysis

Asia-Pacific dominated with a 50.85% revenue contribution in 2025 and is projected to expand at 5.61% CAGR through 2031. China commands the bulk of resin and rubber output, reinforcing local consumption of both zinc and calcium stearates, while India’s chemical sector is on track to rise from USD 220 billion in 2022 to USD 300 billion in 2025, deepening regional specialty-additive requirement. Southeast Asian economies provide integrated palm-oil based fatty acids that feed export-oriented metallic stearate plants, thereby anchoring supply chain efficiency and competitive pricing.

North America ranks second in market size because its pharmaceutical manufacturing footprint concentrates large excipient buyers that insist on current Good Manufacturing Practice accreditation. The transition toward lead-free PVC compounds in wire, cable, and vinyl siding supplies incremental pull. Canada’s infrastructure stimulus directs calcium stearate-treated concrete additives into highway and bridge projects, supporting modest growth. Europe positions itself at the forefront of eco-design and circularity, hosting early adopters of calcium-zinc stabilizer systems for PVC and ramping up regulatory compliance investments that favor high-purity stearate grades. Germany and Italy house major masterbatch producers that serve the broader European plastics network.

South America records stable but lower base volumes, mainly in Brazil’s PVC pipe and footwear industries, while emerging pharmaceutical clusters in Mexico and Colombia create pockets of faster uptake. The Middle East and Africa currently consume a small share yet show long-term promise as refinery and polymer-conversion capacity grows. Gulf Cooperation Council investments in polyolefin derivatives spur additive demand, whereas African urbanization drives PVC pipe and cosmetic needs, positioning the metallic stearate market for gradual penetration as regional manufacturing deepens.

Competitive Landscape

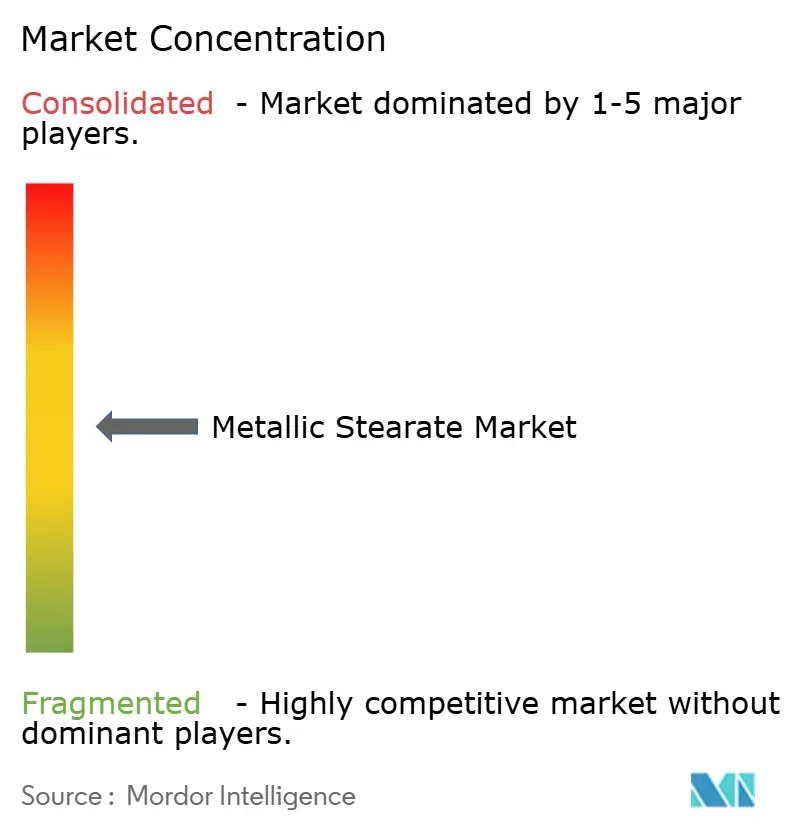

The metallic stearate market exhibits moderate fragmentation. Baerlocher remains a reference point through multi-continent plants and an extensive calcium-based stabilizer portfolio that aligns with the global shift to lead-free PVC. A new 10,000 tons per year expansion completed in May 2025 at its Cincinnati site underscores confidence in long-term additive demand. PMC Group leverages vertically integrated fatty-acid refining, offering pharma-grade magnesium stearate certified under US Pharmacopeia, while Dover Chemical maintains a niche in specialty zinc stearates used in flame retardants and wire enamels.

Strategic positioning centers on purity, dispersion technology, and compliance credentials such as ISO 9001, ICH Q7, and halal certification. Asian manufacturers like Mittal Dhatu and Shandong Heji benefit from domestic palm-oil derivative streams, providing cost advantages on commodity zinc and calcium grades. Western competitors counter by introducing solvent-free aqueous dispersions that cut facility dust load and fast-track Environmental Health and Safety approvals. Recent alliances link additive suppliers with polymer compounders to codevelop bespoke masterbatches that ease customer inventory complexity. Capital commitments have focused on energy-efficient reactor upgrades and automated packaging lines that preserve product integrity and minimize contamination risk.

Metallic Stearate Industry Leaders

Baerlocher GmbH

Faci Asia Pacific Pte Ltd

Peter Greven GmbH and Co. KG

PMC Group, Inc.

Valtris Specialty Chemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Baerlocher plans to construct a metallic stearate manufacturing plant in Malaysia. The MYR 220 million facility is projected to produce 30 kta of calcium-zinc (Ca-Zn) stearates, catering to growing regional demand. Operations are expected to begin in 2027.

- April 2025: Peter Greven has unveiled a new range of bio-based magnesium stearate grades. These products, derived from RSPO-certified palm oil, are tailored to meet the stringent requirements of pharmaceutical tablet formulations, emphasizing sustainability and quality.

Global Metallic Stearate Market Report Scope

The metallic stearate market report is segmented by product, application, and geography. By product, the market is segmented into Aluminum Stearate, Zinc Stearate, Calcium Stearate, Magnesium Stearate, and Others. By application, the market is segmented into Plastic, Rubber, Pharmaceutical, Personal Care, Construction Material, Paints and Coatings, and Others. The report also covers the market size and forecasts for the metallic stearate market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Zinc Stearate |

| Calcium Stearate |

| Magnesium Stearate |

| Aluminium Stearate |

| Others (Sodium and Potassium Stearate, etc.) |

| Powder |

| Flakes |

| Granules |

| Aqueous Dispersion |

| Plastics |

| Rubber |

| Pharmaceuticals |

| Personal Care |

| Construction Materials |

| Paints and Coatings |

| Other Industries (Food and Packaging, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Zinc Stearate | |

| Calcium Stearate | ||

| Magnesium Stearate | ||

| Aluminium Stearate | ||

| Others (Sodium and Potassium Stearate, etc.) | ||

| By Form | Powder | |

| Flakes | ||

| Granules | ||

| Aqueous Dispersion | ||

| By End-User Industry | Plastics | |

| Rubber | ||

| Pharmaceuticals | ||

| Personal Care | ||

| Construction Materials | ||

| Paints and Coatings | ||

| Other Industries (Food and Packaging, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current Metallic Stearate Market size?

The metallic stearate market was valued at USD 5.08 billion in 2026.

How fast is the metallic stearate market expected to grow?

The market is projected to rise at a 4.79% CAGR, reaching USD 6.42 billion by 2031.

Which product type leads the metallic stearate market?

Zinc stearate holds the top position with 41.75% share in 2025, supported by its broad use in PVC, rubber, and cosmetics.

Why is magnesium stearate demand increasing?

Growth in pharmaceutical tablet production and the shift to continuous-manufacturing platforms are driving a 6.15% CAGR for magnesium stearate through 2031.

Page last updated on: