Cloud Services Brokerage (CSB) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

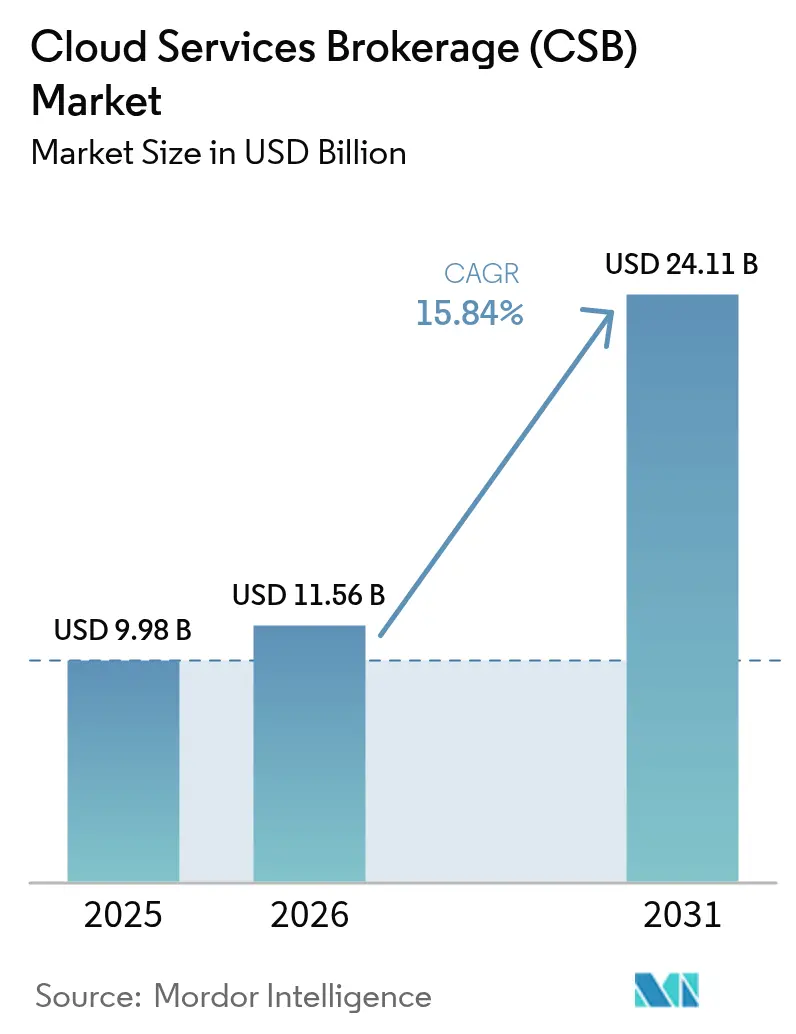

| Market Size (2026) | USD 11.56 Billion |

| Market Size (2031) | USD 24.11 Billion |

| Growth Rate (2026 - 2031) | 15.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Services Brokerage (CSB) Market Analysis by Mordor Intelligence

Cloud Services Brokerage Market size in 2026 is estimated at USD 11.56 billion, growing from 2025 value of USD 9.98 billion with 2031 projections showing USD 24.11 billion, growing at 15.84% CAGR over 2026-2031.

This growth reflects enterprises’ need for a single pane of glass to govern increasingly complex multi-cloud estates, where the typical organization now juggles 2.6 public clouds alongside private resources. Regulatory mandates add further momentum, especially in Europe, where the Digital Services Act and Data Act enforce strict portability and sovereignty rules that amplify demand for brokerage controls[1]Osborne Clarke, “EU Digital Services Act Key Implications,” osborneclarke.com. Supplier consolidation, highlighted by Broadcom’s VMware takeover, has nudged many IT leaders toward independent platforms to preserve negotiating power and avoid lock-in. Meanwhile, hyperscaler marketplaces have exploded, creating lucrative co-sell avenues for brokers tied into Amazon Web Services, Microsoft Azure, and Google Cloud ecosystems. Supply-chain headwinds persist, with semiconductor constraints lifting regional infrastructure costs by 15-20%, yet the cloud service brokerage market continues to absorb this pressure as cost governance tools prove indispensable.

Key Report Takeaways

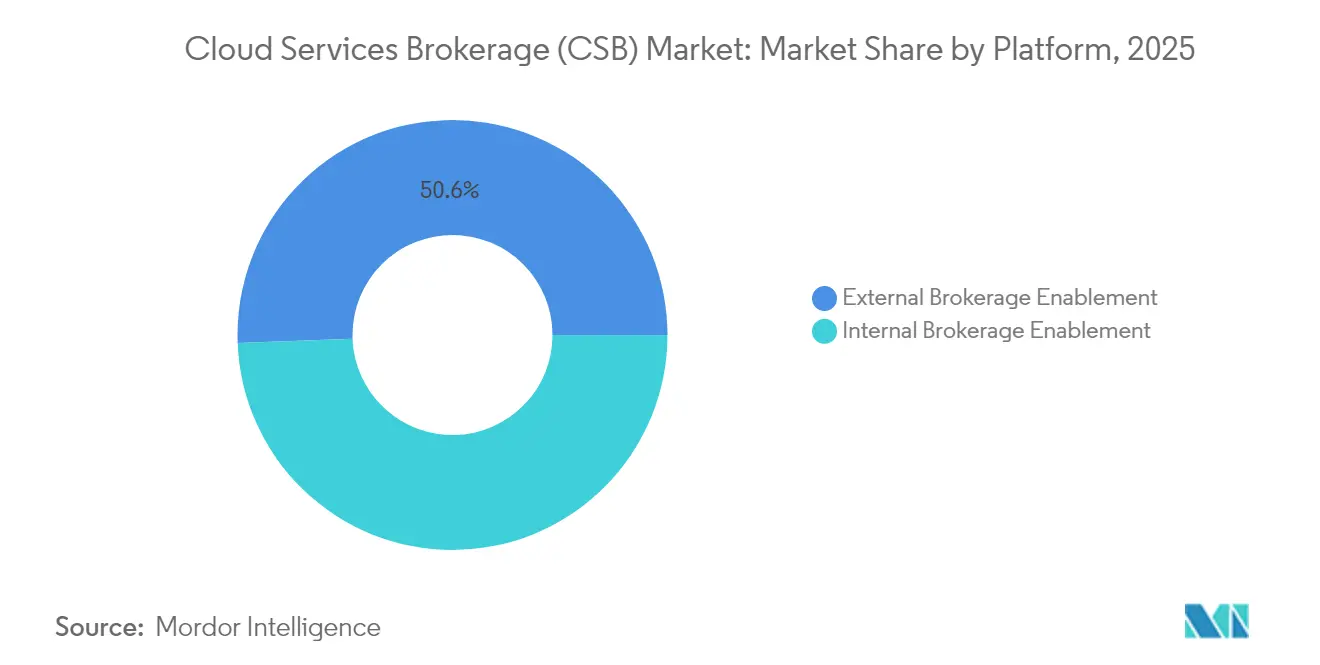

- By platform, External Brokerage Enablement led with 50.60% revenue share in 2025; Internal Brokerage Enablement is projected to post an 18.45% CAGR to 2031.

- By deployment model, Public Cloud retained 53.20% of the cloud service brokerage market share in 2025, while Hybrid Cloud is set to expand at a 20.05% CAGR through 2031.

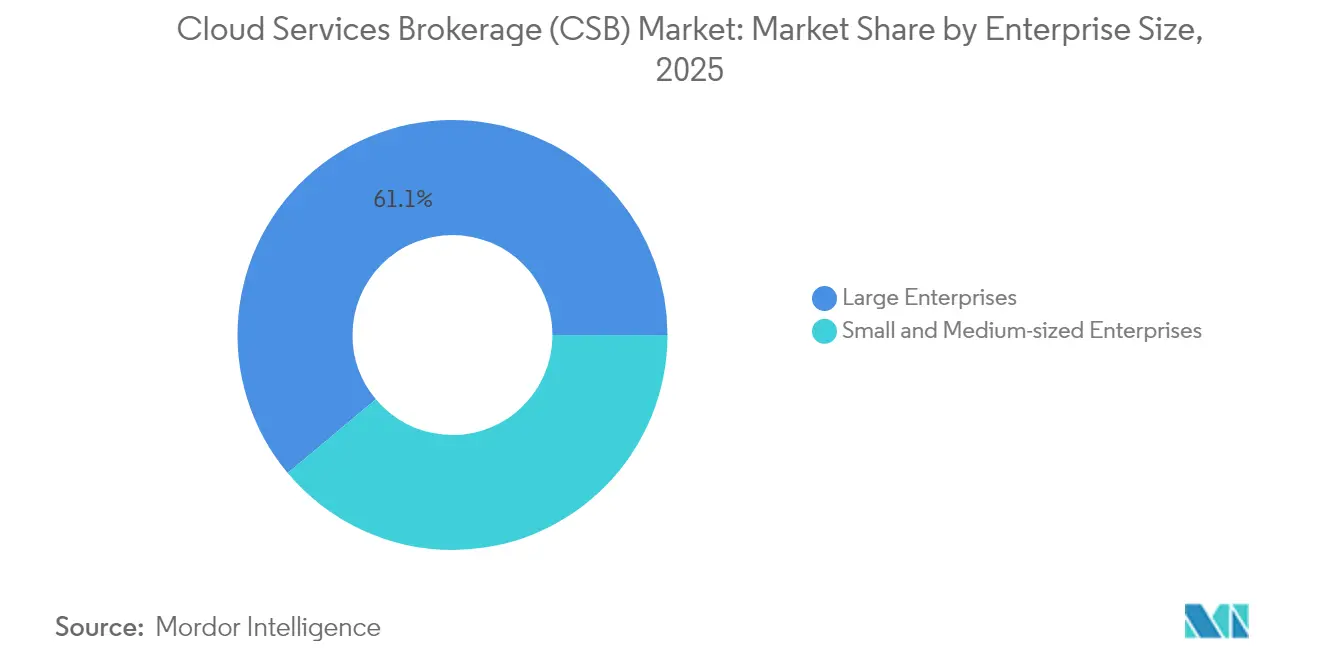

- By enterprise size, Large Enterprises held 61.10% share of the cloud service brokerage market size in 2025, yet the SME segment is forecast to grow 19.22% annually to 2031.

- By end-user industry, IT & Telecommunications captured 27.60% share of the cloud service brokerage market size in 2025; Healthcare & Life Sciences is advancing at a 16.98% CAGR through 2031.

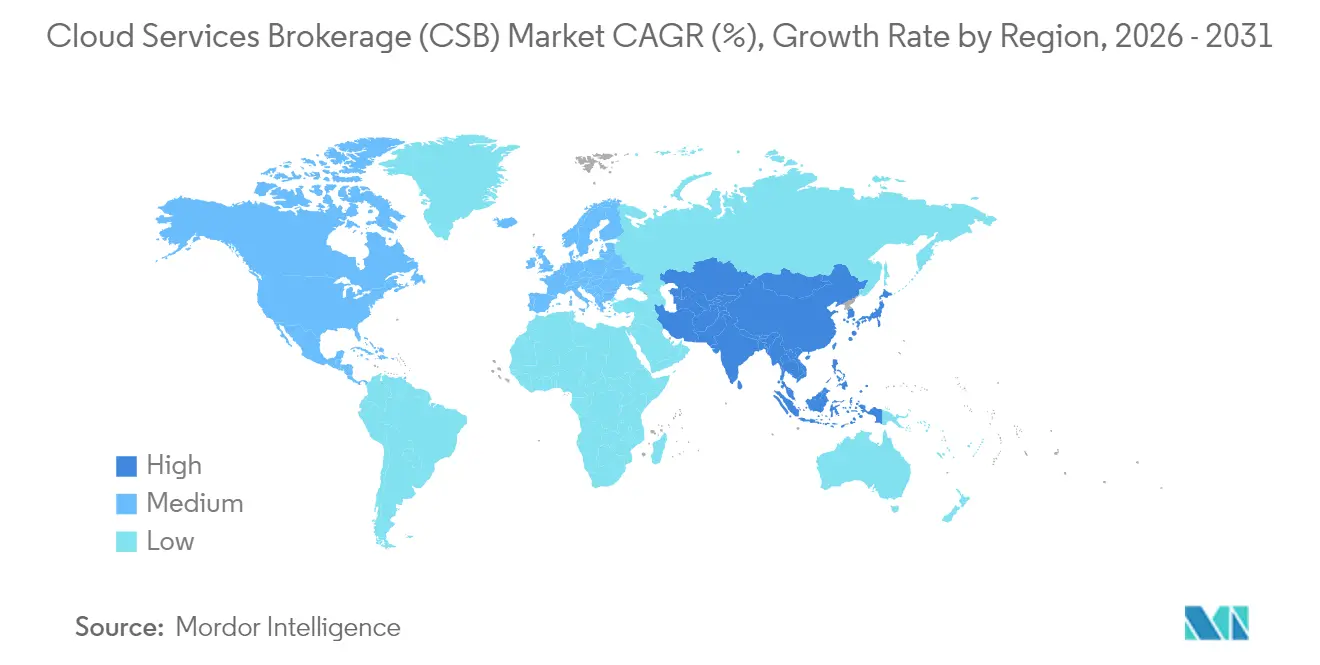

- By region, North America commanded a 43.30% share in 2025; Asia Pacific is forecast to accelerate at an 18.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Services Brokerage (CSB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid and multi-cloud adoption surge | +3.20% | Global (North America, EU lead) | Medium term (2–4 years) |

| Enterprise cloud-spend acceleration | +2.80% | Global (North America, Asia Pacific) | Short term (≤ 2 years) |

| Need for centralized cost and governance | +2.10% | Global, regulated industries | Medium term (2–4 years) |

| Hyperscaler marketplace co-sell boom | +1.90% | Global, strongest in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hybrid and Multi-Cloud Adoption Surge

Hybrid and multi-cloud strategies now dominate CIO roadmaps, with 92% of enterprises expected to pursue multi-cloud architectures by 2025. The resulting sprawl demands brokerage platforms that stitch disparate environments into unified policy domains while shielding organizations from vendor lock-in. Financial services firms stand at the forefront because data-residency mandates bar outright public-cloud migration. Oracle’s direct interconnect with Google Cloud demonstrates how service brokers enable low-latency cross-cloud data flows without traversing the open internet. Container proliferation compounds complexity, pushing CSBs to deliver deep Kubernetes orchestration so DevOps teams avoid juggling console-specific scripts. With edge workloads entering the mix, a broker offers one governance fabric spanning on-prem, public, and edge nodes, minimizing skills gaps and operational risk.

Enterprise Cloud-Spend Acceleration

End-user cloud spending is on track to hit USD 723.4 billion in 2025, a 21.20% jump over 2024 levels. Bigger invoices expose finance leaders to budget overruns, turning FinOps insight into a board-level mandate. CSB platforms now embed machine-learning algorithms that forecast consumption spikes and trigger automated right-sizing. Banks showcase the urgency: despite using only 49% of their committed cloud outlays, they plan to boost allocations further to run AI models requiring premium GPUs[2]Infosys, “Financial Services Cloud Spend Survey 2025,” infosys.com. Without broker-led guardrails, many CFOs fear “bill shock,” where a single poorly scoped data-science project can wipe out annual spend thresholds within months.

Need for Centralized Cost and Governance

The EU Data Act, effective September 2025, forces providers to erase switching fees and simplify cross-cloud data moves, making auditable governance frameworks indispensable. Hospitals already leverage CSB dashboards to police Protected Health Information flows across supply-chain apps and analytics sandboxes. Beyond compliance, finance departments demand real-time visibility to allocate spend by business unit. Brokers meet that need with chargeback engines that align consumption to cost centers, curbing shadow-IT risk and demonstrating ROI in weeks.

Hyperscaler Marketplace Co-Sell Boom

Marketplace transactions have scaled into multi-billion-dollar deals. Google Cloud’s USD 2.5 billion agreement with Salesforce underscores how CSB vendors ride co-sell programs to gain global reach while piggybacking on hyperscaler billing rails. Brokers integrated natively with AWS, Microsoft, or Google can auto-provision third-party SaaS and instantly apply negotiated discounts, appealing to SMEs that prefer click-to-buy simplicity over classic enterprise tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security and compliance concerns | -1.80% | Global, regulated industries | Medium term (2–4 years) |

| Low SME awareness of CSB value | -1.20% | Global, emerging markets acute | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Security and Compliance Concerns

Shared-responsibility models confuse many risk officers, especially when the Digital Services Act imposes fresh notice-and-action rules on cloud operators. Brokers must therefore support granular access controls, geo-fencing, and tamper-proof audit logs across every connected provider. Implementing such depth raises R&D costs and lengthens sales cycles as buyers demand exhaustive penetration-test evidence. Identity management remains the hardest element: CSBs must federate credentials across Azure AD, AWS IAM, and Google Identity while preserving least-privilege defaults.

Low SME Awareness of CSB Value

SMEs grow fastest, yet many founders still equate “brokerage” with unnecessary middle layers. Surveys show smaller firms place user friendliness above cost savings when picking cloud tools. Vendors have responded with template-driven consoles and guided setup flows that deliver value in under an hour. Government voucher schemes in Asia and Europe that subsidize cloud adoption can further improve awareness, but marketing messages must pivot toward simplicity rather than complex FinOps jargon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: External Dominance Faces Internal Innovation

External Brokerage Enablement platforms accounted for 50.60% of the cloud service brokerage market share in 2025, thanks to their vendor-neutral appeal and mature feature sets. Internal Brokerage Enablement, however, is forecast to compound at 18.45% CAGR, reflecting management’s push to embed cloud governance natively into enterprise DevOps pipelines. The cloud service brokerage market size tied to internal platforms is set to more than double by 2031 as Fortune 500 banks and telecoms spin up bespoke portals linked to ServiceNow, Jira, and CI/CD stacks.

This internal surge rides on rising platform-engineering headcount and strategic acquisitions such as IBM’s USD 6.4 billion purchase of HashiCorp, which delivers Terraform and Vault automation under one roof. Internal CSBs also cut license spend over time and let security teams inject organization-specific controls at the code level. External vendors still hold ground by offering faster time-to-value and evergreen marketplace integrations, positioning themselves as “broker of brokers” layers that manage legacy, internal, and SaaS estates together.

By Deployment Model: Hybrid Acceleration Challenges Public Dominance

Public Cloud services retained 53.20% of the cloud service brokerage market in 2025, propelled by ever-expanding hyperscaler availability zones. Yet, Hybrid Cloud deployments are sprinting ahead at 20.05% CAGR as CFOs weigh egress fees against compliance mandates. EU sovereign initiatives have nudged buyers toward architectures where regulated data stays on-prem while analytics elastically burst to public capacity, a pattern Microsoft’s EU Sovereign Cloud expressly targets.

Edge computing further boosts hybrid adoption because manufacturers want latency-critical workloads processed on factory floors. Brokers now knit local Kubernetes clusters with cloud back-ends, granting one-click workload mobility. As 5G private networks spread, expect CSB consoles to manage on-prem MEC nodes alongside classic IaaS resources, a capability public-only brokers cannot match.

By Enterprise Size: SME Growth Disrupts Large-Enterprise Dominance

Large Enterprises controlled 61.10% revenue in 2025 because they hold multi-cloud estates vast enough to justify sophisticated cost-governance layers. The cloud service brokerage market size tied to SMEs, however, is expanding at a 19.22% CAGR, narrowing the gap quickly. Consumption-based pricing and simplified onboarding let a 50-person software startup use the same optimization engines once reserved for Fortune-500 peers.

Arrow Electronics and other distributors now white-label AI-assisted brokerage portals that channel partners can resell to microbusinesses. SME buyers prioritize rapid deployment, so vendors emphasize wizard-driven interfaces and pre-built policy packs that cover common compliance baselines without consultant engagement. Once usage tops certain thresholds, they can graduate seamlessly to premium tiers, ensuring lifetime customer value.

By End-User Industry: Healthcare Innovation Accelerates Beyond IT Leadership

IT & Telecommunications held 27.60% of the 2025 spend due to deep cloud-native heritage and always-on service demands. Healthcare & Life Sciences is projected to grow 16.98% annually as AI-assisted diagnostics and clinical-data exchanges surge. The cloud service brokerage market share for healthcare will therefore widen, with platforms layering HIPAA, GDPR-health, and regional data-sovereignty policies into turnkey blueprints.

Hospitals leverage brokers to orchestrate imaging workloads that spin up GPU clusters only during analysis windows, slashing idle compute spend. Pharma firms embrace brokers to track research data lineage across contract research organizations, satisfying FDA audit trails. Other verticals, manufacturing, retail, and public sector, follow similar patterns, each demanding industry-specific policy libraries that general-purpose cloud consoles seldom provide.

Geography Analysis

North America retained 43.30% of global revenue in 2025, owing to early cloud maturity and dense partner ecosystems. Financial services and healthcare providers dominate adoption, drawn to brokers that streamline Sarbanes-Oxley and HIPAA reporting. Semiconductor shortages continue to inflate regional rack costs, yet brokers mitigate the impact by optimizing workload placement across lower-cost zones. Sovereign-cloud conversations are growing louder as federal agencies and defense contractors seek domestic data-residency assurances, nudging brokers to certify FedRAMP High controls.

Asia Pacific is the fastest-growing territory at an 18.22% CAGR through 2031. Governments from India to Japan run “cloud-first” directives, while regional GDP uplift from cloud computing is estimated at 0.25%–2.23%. Japanese providers such as Sakura Internet now bundle brokerage functions with domestic clouds, appealing to firms wary of trans-border data transfer rules. Meanwhile, semiconductor manufacturing clusters in Taiwan and South Korea secure component supply for local data-center rollout, counterbalancing geopolitical risks.

Europe stands out for regulatory pull: the EU Data Act and GAIA-X lay down stringent portability and sovereignty targets. Microsoft’s sovereign-cloud roadmap and Oracle’s EU Regulated Cloud hint at a service landscape tailor-made for broker overlays. The Middle East and Africa, plus South America, remain emergent but promising; national digital-economy programs in the UAE, Saudi Arabia, and Brazil are funding hyperscaler region launches, planting fertile ground for broker uptake once connectivity gaps close.

Regulatory Landscape

Cloud service brokerage is increasingly shaped by Europe-led requirements that formalize portability, outsourcing controls, and sovereignty assurance. The EU Data Act becoming effective in September 2025 tightened switching and data-mobility obligations, which increases demand for broker-delivered governance, auditability, and chargeback capabilities that can be evidenced across multiple cloud providers.

Financial services and critical infrastructure oversight also raises expectations for compliance in cloud brokered services through third-party ICT risk governance aligned with frameworks such as DORA and NIS2. These frameworks require clearer documentation and ongoing monitoring of outsourced cloud arrangements. In June 2026, the European Commission published a proposal for a Cloud and AI Development Act, introducing a Union assurance concept for cloud sovereignty that can influence procurement requirements and increase the need for brokers to map services and workloads to explicit assurance levels. Alongside that, recognized standards and guidance such as ISO/IEC TR 23187:2020 and the EU Cloud Code of Conduct provide reference points for broker interactions, controls, and data-protection accountability.

Value Chain Analysis

The CSB value chain begins with upstream cloud infrastructure and platform providers, including public cloud, private cloud stack vendors, and SaaS publishers. Brokerage platforms then add aggregation (catalogs, unified billing, identity and access guardrails), integration (connectors, orchestration, automation, and service management tie-ins), and arbitrage/intermediation (marketplace operations, discounting, and service lifecycle management).

Delivery typically combines direct enterprise sales, hyperscaler marketplaces and co-sell motions, and channel partners such as distributors and managed service providers that bundle brokerage with migration, security, and managed operations. The main pinch points lie in integration complexity (legacy apps, heterogeneous IAM, and policy reconciliation across clouds) and the economics of running brokerage capabilities on top of volatile infrastructure costs, including the report-noted semiconductor-driven pressure that raised regional infrastructure costs by 15-20%. Supplier consolidation in adjacent layers, such as the VMware ownership change referenced in the report context, also shifts bargaining power and encourages some buyers to move toward vendor-neutral brokers. At the same time, native management tooling from hyperscalers increases competitive substitution pressure, pushing CSB providers to differentiate through deeper governance, stronger security evidence, and regulated-industry policy libraries.

Competitive Landscape

The cloud service brokerage market displays moderate consolidation. Broadcom’s USD 69 billion VMware purchase slashed the number of accredited resellers and left many clients scrambling for neutral alternatives. IBM’s HashiCorp deal shows platform vendors racing to embed automation IP natively rather than relying on partners. Three strategic clusters have emerged:

- Hyperscaler-integrated brokers are tightly coupled with AWS, Azure, or Google Cloud billing APIs.

- Independent multi-cloud orchestrators positioning as “Switzerland” to avoid lock-in fears.

- Vertical-specific solutions tuned for healthcare, public sector, or manufacturing compliance nuances.

Innovation centers on AI-enabled autonomy. Start-ups tout “self-optimizing cloud” claims, promising 50% cost cuts via predictive scaling. Midsize players respond through mergers. SoftwareOne and Crayon pursue a CHF 1.6 billion tie-up to match scale advantages. Intellectual-property filings around automated rightsizing, policy inference, and edge-node governance hint at intensifying R&D rivalry. Yet differentiation increasingly hinges on partner ecosystems: brokers with deep marketplace catalogs win deals by bundling third-party SaaS, DRM, and observability add-ons in one invoice.

Cloud Services Brokerage (CSB) Industry Leaders

Accenture PLC

Capgemini SE

NEC Corporation

DXC Technology Company

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardization and audit-ready brokerage architectures create whitespace for platforms and service providers that can demonstrate consistent controls across clouds. ITU-T Recommendations Y.3536 (functional architecture) and Y.3506 (functional requirements) outline how brokerage functions such as aggregation, integration, and intermediation should be structured, while the NIST Cloud Computing Reference Architecture explicitly positions the Cloud Broker as a core actor. These anchors support procurement discussions where buyers want a defined broker role for negotiating, integrating, and governing multi-provider services.

FinOps-led governance is also narrowing the entry point for CSB expansion from cost visibility into policy-enforced optimization, SaaS governance, and AI workload management. The FinOps Foundation State of FinOps 2026 report, released April 2026, shows multi-cloud as a mainstream operating model (76% among surveyed practitioners) and highlights organizational focus on AI management and SaaS governance use cases. That profile supports brokerage workflows that can allocate costs, enforce tagging and access policies, and apply consistent guardrails across clouds and SaaS. Europe-focused sovereignty and outsourcing requirements, including the EU Data Act effective September 2025 and the European Commission Cloud and AI Development Act proposal published in June 2026, further strengthen demand for brokers that package attestations, geo-fencing, and auditable logs as repeatable compliance overlays for regulated industries and public-sector procurement.

Recent Industry Developments

- July 2026: Accenture signed a EUR 200 million contract with the NATO Communications and Information Agency to design, implement, and operate the Protected Business Network platform, a secure multi-cloud environment, over seven years. The award elevates demand for broker-style governance, identity controls, and compliance evidence in defense-grade multi-cloud programs. It also reinforces the role of large integrators in setting reference architectures for secure multi-cloud service delivery.

- April 2026: Accenture and Google Cloud expanded their partnership with the launch of the Gemini Enterprise Acceleration Program, introducing a catalog of industry-specific AI agents designed for enterprise operations. The move increases pressure on brokers and managed service providers to add agent governance, workload placement controls, and cost attribution across multi-cloud estates. It also accelerates bundling of AI enablement into cloud brokerage and optimization engagements.

- March 2026: Accenture expanded its strategic partnership with Google Cloud to integrate Google Security Operations with Accenture cybersecurity services to address AI-driven threats. The integration strengthens broker-led security posture management by aligning detection and response workflows with cloud consumption and policy controls across providers. It also supports more standardized security operating models for enterprises managing hybrid and multi-cloud environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as third party and in house brokerage services that help enterprises select, integrate, govern, and manage cloud services across one or more cloud environments, and the value is measured as annual revenue earned for these brokerage activities.

Scope exclusions: We exclude the underlying cloud spend itself (IaaS, PaaS, and SaaS subscription revenue) when it is not billed and recognized as brokerage revenue.

Segmentation Overview

- By Platform

- Internal Brokerage Enablement

- External Brokerage Enablement

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Enterprise Size

- Small and Medium-sized Enterprises

- Large Enterprises

- By End-user Industry

- IT and Telecommunications

- Banking, Financial Services and Insurance

- Retail and Consumer Goods

- Healthcare and Life Sciences

- Government and Public Sector

- Manufacturing

- Media and Entertainment

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of the South America

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Rest of Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for how cloud brokerage is procured and reported, and to build a consistent set of demand signals across regions. We referenced public sources such as the National Institute of Standards and Technology (NIST) cloud guidance, OECD digital economy statistics, the US Bureau of Labor Statistics for IT services employment trends, the International Telecommunication Union (ITU) ICT indicators, and standards material from ISO/IEC where it clarifies governance and security terms.

On the market side, we also reviewed cloud adoption and governance publications from major regulators and trade bodies, along with company annual reports, investor presentations, and reputable press coverage to capture changes in service packaging and pricing language. Where a data point was not consistently available in public disclosures, we used approved paid subscriptions for company financials and intelligence, news and financials screening, and patent databases to confirm product direction and timing. The specific desk research sources listed here are illustrative and many other references were also used for data collection, validation, and clarification checks.

Primary Interviews and Surveys

Primary work was conducted through expert interviews and structured surveys with CSB platform teams, managed service providers, systems integration focused practices, cloud governance specialists, and enterprise buyers responsible for cloud operations and vendor management. For a global view, inputs were balanced across Americas, EMEA, and APAC so assumptions on adoption pace, typical contract structure, and attach rates were not driven by a single region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 44% |

| Mid tier: 57% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 15% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was started with a top-down demand reconstruction, where enterprise cloud adoption and multi cloud complexity indicators were translated into an addressable pool for brokerage engagement and then converted into revenue using observed packaging and pricing norms. The totals were then checked with selective bottom-up approximations such as sampled provider revenue disclosures where available, channel checks on typical deal sizes, and volume by average selling price builds for common brokerage bundles, which helped us adjust outliers before finalizing.

Key inputs that shaped the model included the share of enterprises using hybrid or multi cloud setups, the typical percentage of cloud programs that use a service catalog or marketplace workflow, the penetration of automation and orchestration for provisioning, and the intensity of security and compliance management attached to cloud governance. We also tracked indicators like IT services spend direction, cloud migration activity signals, and the mix shift toward managed governance, since these move brokerage revenue differently than raw cloud consumption. Forecasting was run using scenario analysis anchored to expert consensus on adoption pace and pricing progression, and the scenarios were blended into a single base case after variance checks across regions and enterprise sizes.

Data Validation & Update Cycle

Model outputs were validated by comparing results against independent signals such as cloud governance adoption patterns, managed services activity, and the implied revenue per customer for typical brokerage contracts. When a regional total or a vertical level value moved outside expected ranges, the assumptions were revisited and, if needed, respondents were re-contacted to confirm whether the change came from definition, pricing, or timing.

Before sign-off, the numbers pass through multi-step analyst reviews that look for math consistency, year over year movements that need explanation, and alignment between qualitative trends and quantified outputs. Reports are refreshed annually, with interim updates triggered by material events such as major regulation changes or visible shifts in enterprise cloud operating models. Right before delivery, a fresh final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Cloud Services Brokerage Csb Market Size Versus Other Published Estimates

Published market values for cloud services brokerage often vary because the word brokerage is applied differently across studies, and because some figures mix platform enablement, managed governance, and adjacent cloud professional services. Timing differences also matter since fast growth years can look very different depending on the chosen base year and currency conversion point.

In this study, the main gap driver is scope treatment, where some estimates count a wider set of cloud managed services and broader integration work as brokerage revenue, and others apply more aggressive uplift on average selling prices as automation features expand, which is then carried into the forecast curve by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.56 B (2026) | |

| Global Consultancy A | USD 15.36 B (2026) | Uses a broader service taxonomy that can pull in more aggregation, intermediation, and arbitrage activities across cloud models, which can raise the counted revenue beyond brokerage-only billing. |

| Industry Research House B | USD 11.51 B (2025) | Uses a different base year and a longer forecast window, and the scope description is less explicit on separating brokerage revenue from underlying cloud subscription and adjacent services, which can shift year-to-year comparability. |

Overall, the spread is largely explained by what each publisher counts as brokerage and how base years are chosen for a fast-growing service market. By keeping the counted value tied to brokerage revenue signals and then cross-checking it against adoption and contract realities, the estimate stays easier to reconcile and repeat in future refreshes.

Key Questions Answered in the Report

What is the projected value of the cloud service brokerage market by 2031?

The cloud service brokerage market is forecast to reach USD 24.11 billion by 2031.

Which deployment model is growing fastest?

Hybrid Cloud is advancing at a 20.05% CAGR as firms balance sovereignty with scalability.

Why are SMEs adopting brokerage platforms quickly?

Simplified onboarding and consumption-based pricing let smaller firms access enterprise-grade governance without large IT teams.

How do brokers help manage cloud costs?

Modern brokers embed AI algorithms that predict usage spikes and automatically right-size resources, preventing budget overruns.

Which region offers the strongest growth outlook?

Asia Pacific leads growth with an 18.22% CAGR, driven by cloud-first government policies and expanding infrastructure.

What is the chief restraint facing market expansion?

Security and compliance concerns, especially in regulated sectors, can slow adoption until brokers prove robust controls.

Page last updated on: