Cloud MFT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

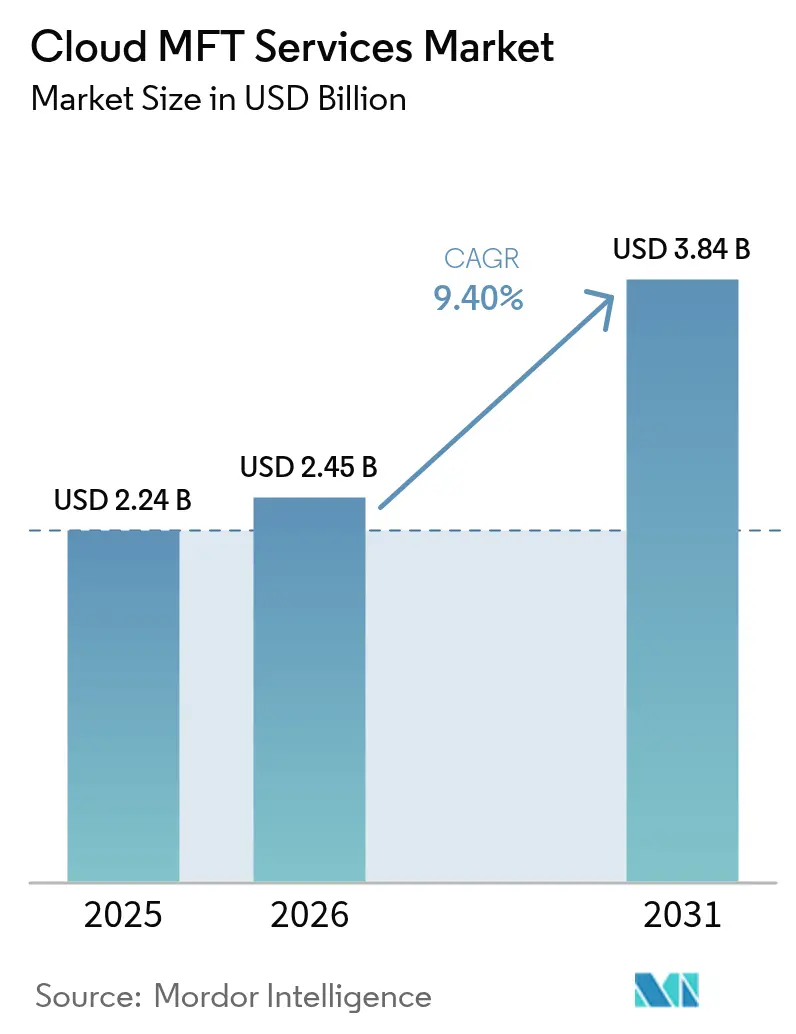

| Market Size (2026) | USD 2.45 Billion |

| Market Size (2031) | USD 3.84 Billion |

| Growth Rate (2026 - 2031) | 9.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud MFT Services Market Analysis by Mordor Intelligence

The Cloud MFT Services market size is expected to grow from USD 2.24 billion in 2025 to USD 2.45 billion in 2026 and is forecast to reach USD 3.84 billion by 2031 at 9.40% CAGR over 2026-2031. Rapid migration from on-premises gateways toward fully managed, cloud-native platforms that automate encryption, audit logging, and multi-cloud orchestration is the primary engine of expansion. Hybrid adoption is scaling faster than public or private deployments as enterprises reconcile local data-residency mandates with the need for operational elasticity. Tighter data-protection statutes, escalating ransomware campaigns, and an expanding edge-computing footprint are driving the replacement of legacy FTPS scripts with API-driven managed file transfer microservices. Vendors are responding with tiered subscription models, AI-powered routing, and containerized agents that extend secure exchange to 5G and industrial Internet of Things nodes. Competitive intensity remains high as incumbents defend share against cloud-native newcomers offering lightweight, event-streaming gateways.

Key Report Takeaways

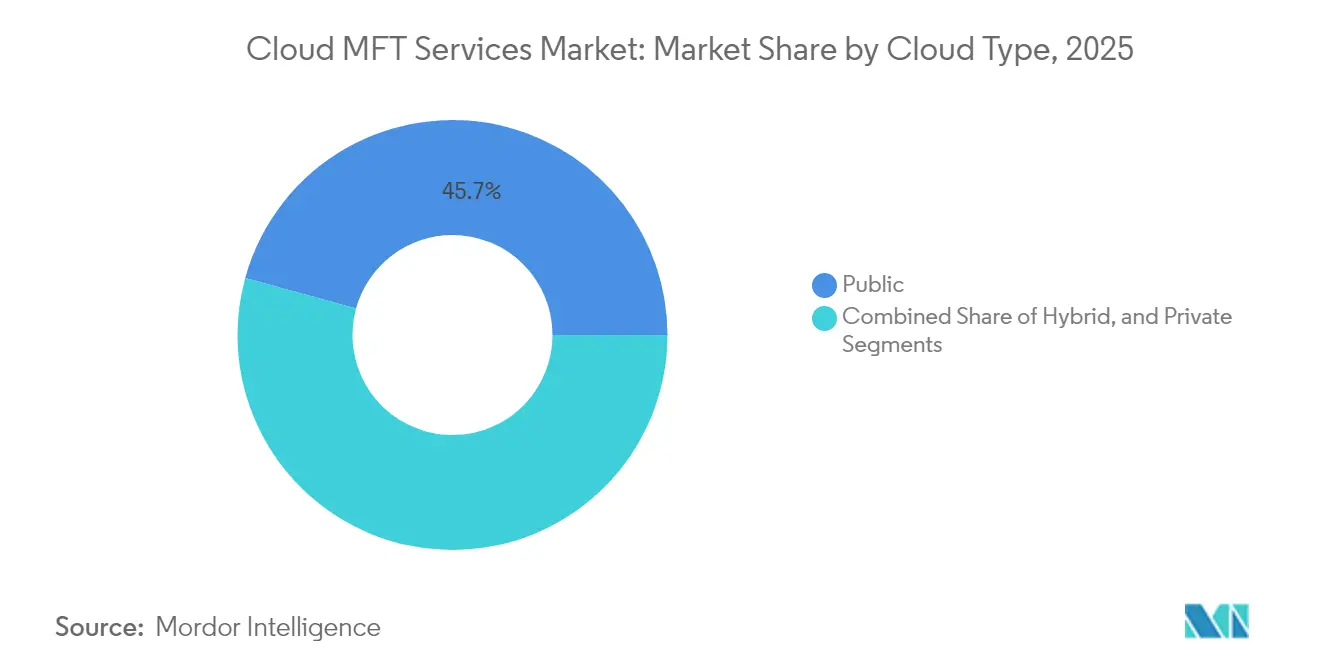

- By cloud type, public deployments led with a 45.72% market share in Cloud MFT Services in 2025, while hybrid models are forecast to grow at a 13.92% CAGR through 2031.

- By end-user industry, BFSI accounted for a 23.74% share of the Cloud MFT Services market size in 2025, whereas healthcare is expected to advance at a 12.95% CAGR through 2031.

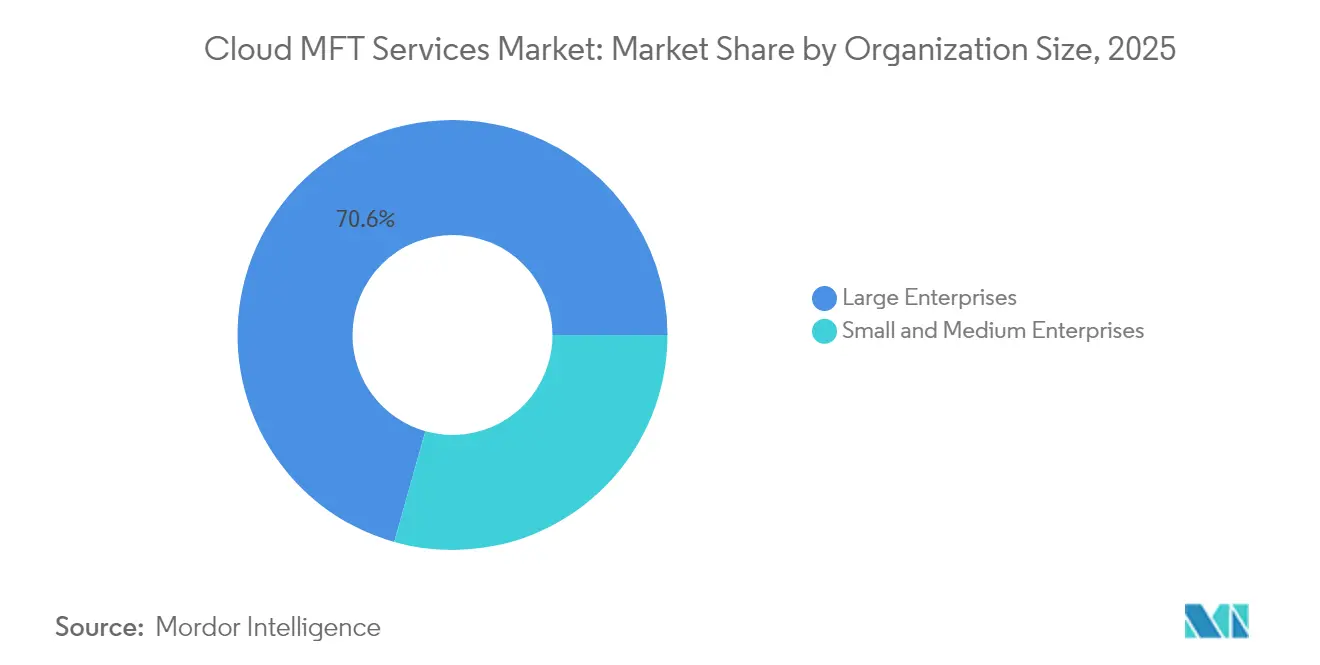

- By organization size, large enterprises held a 70.63% share in 2025, while small and medium enterprises are poised for the fastest growth, with a 11.98% CAGR through 2031.

- By transfer type, system-to-system exchanges captured a 47.66% share of the Cloud MFT Services market size in 2025, and mobile-to-mobile transfers are expected to expand at a 14.88% CAGR through 2031.

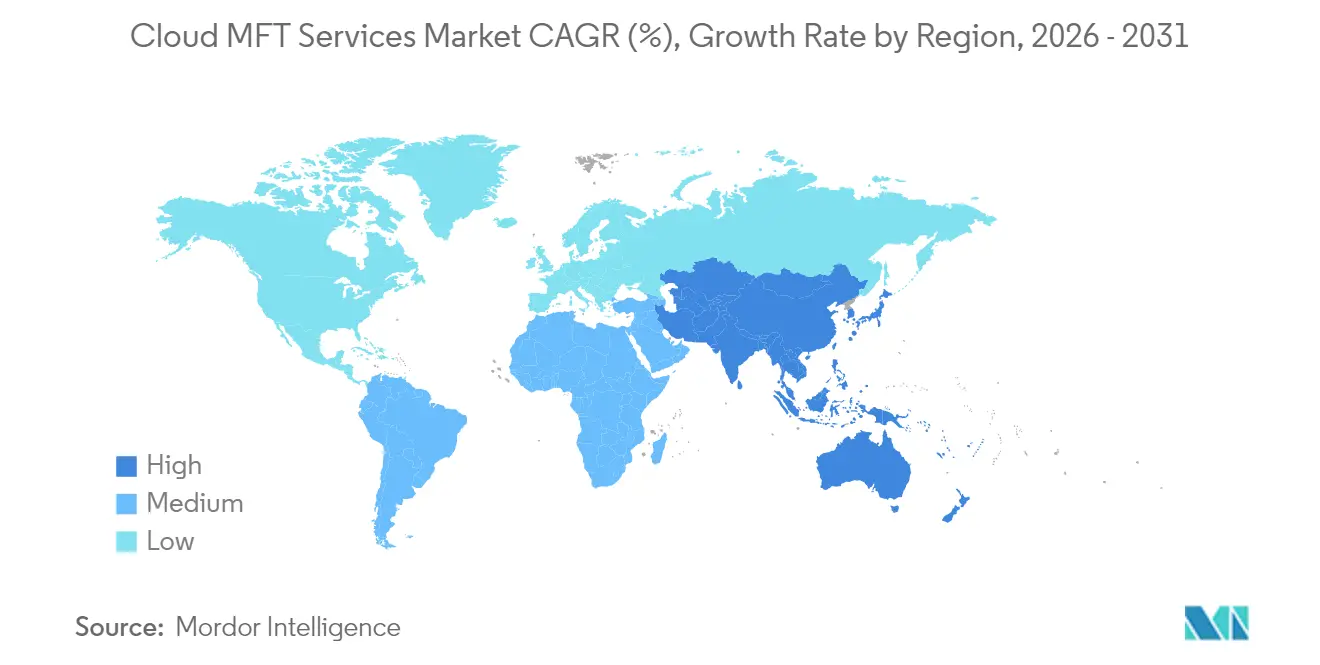

- By geography, North America dominated with a 36.68% share in 2025, whereas the Asia Pacific is projected to register the highest CAGR of 13.55% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud MFT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Need for Secure File Transfer | +2.1% | Global, with elevated demand in North America and Europe | Short term (≤ 2 years) |

| Proliferation of Hybrid Cloud Architectures | +1.8% | Global, concentrated in North America, Europe, and the Asia Pacific | Medium term (2-4 years) |

| Regulatory Compliance Requirements for Data Protection | +1.5% | Global, particularly Europe (GDPR), North America (HIPAA, SOC 2), and Asia Pacific (emerging frameworks) | Long term (≥ 4 years) |

| AI-Powered Adaptive Routing Optimizing Bandwidth Utilization | +1.2% | North America and the Asia Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Expansion of Edge Computing Creating Micro-Transfer Hubs | +1.0% | Global, with early adoption in North America and the Asia Pacific manufacturing corridors | Long term (≥ 4 years) |

| Rising Adoption of Event-Driven Architectures Requiring Real-Time File Streaming | +0.9% | North America and Europe, expanding to the Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Need for Secure File Transfer

Ransomware incidents targeting insecure file-transfer endpoints climbed 38% year-over-year in 2024, according to the FBI’s Internet Crime Complaint Center.[1]Federal Bureau of Investigation, “2024 Internet Crime Report,” ic3.gov Enterprises are therefore hardening exchange workflows with end-to-end encryption, multi-factor authentication, and policy-based quarantines. The Cybersecurity and Infrastructure Security Agency’s directive 23-01 compels U.S. federal agencies to embed zero-trust principles in every file movement. Parallel momentum is evident in payment ecosystems following the tightening of PCI DSS v4.0 requirements for encrypted data-in-motion, which has catalyzed the procurement of certified MFT services by processors and merchant acquirers. Healthcare adoption accelerated when the Department of Health and Human Services imposed USD 4.75 million in HIPAA fines for unencrypted transmissions during 2024.

Proliferation of Hybrid Cloud Architectures

A 2024 Cloud Security Alliance survey found that 67% of enterprises already operate workloads across at least three cloud environments.[2]Cloud Security Alliance, “Cloud Adoption Survey 2024,” cloudsecurityalliance.org Hybrid MFT deployments enable firms to retain sensitive files on-premises for residency compliance while leveraging public cloud scalability for burst workloads. European banks are adopting hybrid models to comply with the European Banking Authority's outsourcing rules, which mandate that critical payment files be hosted on EU-domiciled infrastructure. Manufacturers synchronize large CAD files between private PLM systems and supplier portals, reducing iteration cycles. Telecom operators are injecting MFT micro-services into 5G edge nodes to serve latency-sensitive use cases such as autonomous vehicles.

Regulatory Compliance Requirements for Data Protection

GDPR Article 32 obliges data controllers to encrypt personal data in transit, and EU regulators levied EUR 2.1 billion (USD 2.3 billion) in fines during 2024 for inadequate safeguards.[3]European Data Protection Board, “GDPR Enforcement Tracker 2024,” edpb.europa.eu In the United States, HIPAA continues to require covered entities to protect electronic protected health information, prompting the procurement of FIPS-validated MFT platforms. Asia Pacific policies are intensifying as India’s Digital Personal Data Protection Act and China’s Cybersecurity Law restrict cross-border data flows, forcing in-country MFT deployments. ISO 27001 certification is becoming a more common vendor prerequisite in regulated industries.

AI-Powered Adaptive Routing Optimizing Bandwidth Utilization

AI is moving from proof-of-concept to production inside MFT platforms. IEEE research shows that telecom carriers can cut backbone costs by up to 30% after adopting machine-learning-based routing, which diverts large payloads to underutilized paths. Cloud providers now offer rules that shift non-urgent transfers to off-peak hours, which appeals to media companies moving multi-terabyte video assets. Predictive analytics forecast link degradation and reroute transfers in advance of failure. AI-driven compression further reduces payload sizes, enabling enterprises to meet aggressive backup windows without increasing bandwidth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Legacy FTPS Infrastructure | -1.3% | Global, particularly acute in North America and Europe, with aging enterprise IT estates | Short term (≤ 2 years) |

| High Switching Costs for Large Enterprises | -1.1% | Global, concentrated in North America and Europe, where large enterprise density is highest | Medium term (2-4 years) |

| Limited IPv6 Support in MFT Protocol Implementations | -0.8% | The Asia Pacific and Europe are leading the way in IPv6 adoption, while North America is lagging. | Medium term (2-4 years) |

| ESG Scrutiny Elevating Data Center Energy Audit Costs | -0.6% | Europe and North America, expanding to the Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dependence on Legacy FTPS Infrastructure

International Data Corporation research indicates 54% of large enterprises still rely on FTPS for at least half of their external exchanges.[4]International Data Corporation, “Legacy Infrastructure Study 2024,” idc.com Hard-coded IPs, custom scripts, and proprietary authentication loom as migration hurdles. Mainframe-centric financial institutions bear the heaviest burden, as FTPS gateways are intricately integrated with core banking systems. Re-engineering workflows to support REST APIs and OAuth can exceed USD 5 million for global firms, delaying projects. The absence of native S3 or Azure Blob connectors in legacy stacks forces middleware deployments that add latency and risk.

High Switching Costs for Large Enterprises

Deloitte estimates the average three-year total cost of an MFT migration for a Fortune 500 firm to be USD 8 million, which includes license termination charges, professional services, and parallel runs. Proprietary metadata and partner configurations deepen vendor lock-in. External ecosystems must retest every endpoint, thereby increasing the risk of disruption in regulated industries such as aerospace, where delayed submissions incur penalties. Chief information officers often postpone replacement, opting for continuity over modernization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cloud Type: Hybrid Strategies Accelerate Multicloud Orchestration

Hybrid deployments contributed the fastest 13.92% CAGR from 2026 to 2031, as organizations blended regulatory assurance with elastic capacity. Public cloud retained 45.72% of the Cloud MFT Services market share in 2025, as banks and telecom operators prized pay-as-you-go scaling during seasonal transaction peaks. Private cloud remained essential for agencies bound by FedRAMP High and similar sovereignty requirements.

Hybrid adoption intensifies as enterprises adopt multicloud playbooks to avoid single-vendor dependence. The Cloud MFT Services market size tied to hybrid models will expand steadily as low-latency edge nodes connect factory floors and branch offices to centralized compliance engines. Vendors now bundle containerized gateways and software-defined connectors that expose uniform policies across AWS, Azure, Google Cloud, and on-premises clusters. This capability is vital for manufacturers distributing CAD updates through supplier networks and logistics platforms, while safeguarding intellectual property in accordance with export control rules.

By End-User Industry: Healthcare Momentum Outpaces Early BFSI Leadership

BFSI captured a 23.74% share in 2025, driven by early regulatory triggers, including PCI DSS and SWIFT CSP audits. The Cloud MFT Services market size linked to BFSI will continue to grow, yet healthcare’s 12.95% forecast CAGR positions the sector as the prime accelerator. Electronic health record interoperability mandates and the growth of telehealth raise the volume of protected health information (PHI) circulating among providers, payers, and patients.

The 21st Century Cures Act compels U.S. providers to expose standardized APIs by 2025, driving investment in connectors that translate HL7 streams to FHIR while preserving encryption. Pharmacies and clinical research organizations similarly need validated transfer logs for regulatory audits. Other verticals are maturing at varying speeds: the government is embracing MFT for tax filings and license renewals, manufacturing relies on the secure exchange of design and inspection files, and the media sector secures high-resolution content transfers for streaming distribution.

By Organization Size: SMEs Close the Functionality Gap

Large enterprises held a 70.63% share of the Cloud MFT Services market in 2025, primarily due to their sprawling partner ecosystems and stringent audit obligations. However, SME adoption is projected to post a robust 11.98% CAGR through 2031 as pay-per-use pricing and low-code onboarding lower entry barriers. Consumption-based models enable smaller firms to align their spending with actual volumes, rather than capital outlay.

Templates for QuickBooks, Salesforce, and Shopify enable rapid integration with partners, significantly reducing setup timelines. PwC research noted a 45% drop in file-transfer error rates and a 60% acceleration in partner onboarding among SME adopters. As vendors integrate AI-driven automation into mid-tier plans, SMEs gain features such as predictive routing and self-service compliance dashboards, which were once reserved for large enterprises. The Cloud MFT Services market size attached to SMEs is expected to expand as digital supply chains become increasingly globalized.

By Transfer Type: Mobile-First Exchanges Surge Amid Remote Work

System-to-system traffic dominated with a 47.66% share in 2025 because automated B2B and EDI workflows anchor enterprise operations. Yet mobile-to-mobile transfers register the quickest 14.88% CAGR as remote employees exchange sensitive files via smartphones and tablets.

Bring-your-own-device policies require containerized MFT apps that feature biometric login and remote wipe capabilities. Citrix, Box, and Dropbox have enhanced enterprise suites to meet this requirement, reflecting broader convergence between collaboration and managed file transfer. System-to-system exchanges continue to evolve through event-driven triggers that initiate transfers when inventory thresholds, regulatory deadlines, or payment clearing events are met. Ad-hoc transfers complement both modes by offering controlled human collaboration with version control and expiry timers, ensuring policy uniformity across disparate exchange scenarios.

Geography Analysis

North America controlled 36.68% of the Cloud MFT Services market in 2025, driven by the Health Insurance Portability and Accountability Act (HIPAA), Sarbanes-Oxley rules, and stringent state breach-notification laws that mandate the encryption of data in motion. Enterprises lead global zero-trust adoption, extending verification policies to every file exchange endpoint. The U.S. Securities and Exchange Commission amended Regulation S-P in 2024, obliging financial institutions to integrate secure transfer protocols into incident response plans. Canadian organizations face similar imperatives under PIPEDA, boosting demand for certified platforms with blockchain audit trails.

Asia Pacific is forecast to deliver a 13.55% CAGR through 2031, the highest regional pace. India’s Digital Personal Data Protection Act mandates the local processing of sensitive personal information, whereas China’s Cybersecurity Law and supporting measures stipulate in-country storage and regulatory approval for outbound transfers. Japan and South Korea both tightened personal data statutes in 2024, prompting enterprises to adopt MFT services with granular permission controls. The region’s vast manufacturing base relies on secure exchange for just-in-time supply chains, intensifying adoption among automotive and electronics clusters.

Europe’s trajectory is shaped by the GDPR, with supervisory authorities imposing significant penalties for lapses in data transfer security. The European Banking Authority’s 2024 update insists that banks retain oversight of outsourced file-transfer operations. Germany’s BSI cloud guidelines and the United Kingdom’s Data Protection Act add sector nuances. Middle Eastern regulators mandate sovereign cloud architectures, exemplified by Saudi Arabia’s National Cybersecurity Authority, which requires locally hosted MFT. In Africa, South Africa and Nigeria spearhead uptake through financial inclusion programs that hinge on secure mobile transfers, while Brazil’s LGPD drives similar modernization in South America.

Regulatory Landscape

Cloud MFT procurement increasingly relies on auditable security controls and sector rules covering data-in-motion, identity, and third-party oversight. In the United States, federal use cases map to FISMA and NIST SP 800-53 Rev. 5 for information exchange and continuous assessment, with deployments often requiring FIPS-validated cryptography. In Europe, DORA has applied since January 2025 for financial entities and raises the bar for ICT risk management and oversight of critical third-party providers that handle file transfer workflows, while PCI DSS v4.0 reached full enforcement on March 31, 2025, reinforcing encryption and monitoring expectations for payment-related transfers.

Data access, portability, and sovereignty rules are also reshaping architecture choices across cloud, private, and hybrid MFT. The EU Data Act (Regulation (EU) 2023/2854) entered into force on January 11, 2024 and began general application from September 12, 2025, increasing requirements for governed sharing, standardized formats, and robust logging. For defense contractors handling CUI, CMMC 2.0 Level 2 assessment requirements starting November 10, 2026 further elevate secure transfer, traceability, and third-party risk controls across partner ecosystems.

Value Chain Analysis

The cloud MFT services value chain begins with foundational infrastructure from hyperscalers (compute, storage, networking, and regional availability zones) and secure connectivity options that bridge enterprise environments to cloud regions. Key inputs include cryptographic components and security controls (encryption, key management, MFA, and WAF/zero-trust patterns), along with private connectivity links such as AWS Direct Connect and Azure ExpressRoute for regulated and latency-sensitive transfers. On top of this layer, MFT platform vendors provide protocol support, policy engines, audit logging, and integrations, then deliver via SaaS or managed service operations that include monitoring, incident response, and compliance reporting.

Downstream, systems integrators and managed security providers handle partner onboarding, workflow automation (including B2B/EDI patterns), and hybrid orchestration across public cloud, private environments, and edge agents. End users in BFSI, manufacturing, healthcare, and government push for residency-aware routing, immutable logs, and standardized controls aligned to ISO 27001 and sector mandates. The main frictions are multicloud policy consistency and reliance on a limited set of high-availability cloud regions that fit both performance and regulatory needs, which drives differentiation through governance tooling, connectors, and deployable agents for hybrid environments.

Competitive Landscape

The Cloud MFT Services market displays moderate concentration. IBM, Axway, and Progress Software leverage their longstanding enterprise footprints and extensive protocol libraries to hold a significant share. New entrants differentiate themselves through cloud-native design, event streaming, and frictionless API gateways that resonate with DevOps teams. Product roadmaps are increasingly emphasizing vertical templates that encapsulate sector-specific compliance tasks, thereby shrinking deployment timelines for healthcare, banking, and government users.

Technology rivalry centers on AI-assisted automation. Progress MOVEit 2025.1 now quarantines anomalous transfers in real time, addressing the security spotlight following the 2023 exploit incident. IBM expanded Sterling File Gateway to edge devices, targeting industrial settings where intermittent connectivity demands local decision-making. Axway’s partnership with Microsoft Azure Arc underscores the strategic value of unified governance across multicloud estates.

Hyperscalers add pressure by bundling native file-transfer functions directly into storage services, compelling independent vendors to prove added value through analytics, compliance reporting, and protocol breadth. Price competition is fierce in the SME segment, where serverless architectural models allow challengers to undercut subscription fees. Opportunities remain in underserved niches such as edge-native orchestration, integrated ESG reporting, and IPv6-first stacks.

Cloud MFT Services Industry Leaders

IBM Corporation

Oracle Corporation

Axway Software SA

Progress Software Corporation (Ipswitch)

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led modernization is creating whitespace for cloud-native MFT platforms that combine encryption, tenant isolation, and continuous evidence generation for audits. DORA (effective January 2025) and PCI DSS v4.0 enforcement (March 31, 2025) have tightened expectations around monitoring, access control, and secure transmission in financial and payment flows, while U.S. federal-aligned programs tied to NIST SP 800-53 controls reinforce control mapping and continuous assessment requirements. This setup supports opportunities for vendors that can package pre-mapped control sets, tamper-evident audit trails, and third-party risk reporting features that simplify procurement in regulated industries.

A second opportunity area is hybrid and multicloud orchestration with first-class connectors to dominant enterprise content and cloud storage endpoints, because migrations often stall at the integration layer rather than the transfer protocol itself. Product activity, such as Progress expanding Automate MFT endpoint support (Google Cloud Storage, Microsoft OneDrive, and SharePoint connectors), points to demand for secure, policy-governed connectivity into common cloud repositories and collaboration stacks. As the EU Data Act moves into broader application from September 12, 2025, governed sharing and portability capabilities for product-generated data increase the value of standardized, machine-readable exchange workflows, especially when paired with residency controls for cross-border constraints.

Recent Industry Developments

- June 2026: Coviant Software released Diplomat MFT 9.5 with a secure, browser-based file transfer portal. The update broadens secure ad-hoc and partner-facing transfer options without forcing client software installation, supporting organizations that are tightening control over external sharing endpoints.

- April 2026: Progress Software published Automate MFT updates that expanded native endpoint support to Google Cloud Storage and Microsoft OneDrive. The added connectivity supports hybrid workflows where sensitive data movement is governed centrally while files land in widely used cloud repositories for downstream processing.

- May 2025: Boomi signed a definitive agreement to acquire Thru, Inc. to strengthen secure managed file transfer within the Boomi Enterprise Platform. The deal connects file-based data exchange with application and API integration use cases, enabling consolidation of governance and monitoring across integration patterns.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cloud MFT services market is defined as paid cloud-delivered services used to securely move files and data sets between people, apps, and systems, with policy controls, encryption, logging, and compliance reporting built into the transfer workflows.

Scope exclusions: We exclude generic cloud storage, unmanaged FTP tools, and in-house file transfer built only for internal use without an external service revenue component.

Segmentation Overview

- By Cloud Type

- Public

- Private

- Hybrid

- By End-User Industry

- Government

- Retail

- Manufacturing

- Energy and Utilities

- Telecommunications

- BFSI

- Healthcare

- Other Industries

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Transfer Type

- Ad-Hoc Transfer

- System-to-System Transfer

- Mobile-to-Mobile Transfer

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping what secure file transfer in the cloud means in real buying terms, then aligning it to observable signals like cloud adoption, cybersecurity spend, and compliance intensity in regulated industries. We relied on public sources such as NIST guidance and the NIST National Vulnerability Database, U.S. SEC filings, U.S. Bureau of Labor Statistics data for IT roles, and International Telecommunication Union (ITU) connectivity statistics to ground the demand context and constraints.

To shape assumptions, we also reviewed company annual reports and investor presentations, trade association materials, product documentation, and business press coverage of incidents, regulations, and cloud migration. For cross-checking revenue scale and coverage, we used paid subscriptions for company financials and intelligence, plus news and financial databases, and patent databases where applicable. The sources listed here are illustrative, and we also used other public references to collect data, validate patterns, and resolve open questions.

Primary Interviews and Surveys

Primary interviews and survey inputs focused on how cloud MFT is purchased and priced, where it sits versus adjacent secure file sharing tools, and what volumes typically look like (number of transfers, data size bands, and active endpoints). We spoke with a mix of service providers, system integrators, and enterprise buyers across major regions, so our assumptions on adoption, subscription structures, and compliance-driven upgrades could be tested and adjusted when respondent descriptions differed from desk research.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 43% |

| Mid tier: 51% | Functional/Unit leaders: 43% | EMEA: 30% |

| Smaller Players: 19% | Managers: 44% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up logic. For the top-down view, we reconstructed addressable spend by starting with cloud security and integration budgets, then applying penetration and attach-rate assumptions for managed file transfer use cases. To keep the calculations grounded, we used market fingerprints such as cloud workload migration pace, regulated data transfer needs in BFSI and healthcare, policy and audit logging requirements, typical subscription packaging (users, endpoints, and throughput), and the share of system-to-system transfers versus ad-hoc transfers.

We then used selective bottom-up approximations to sanity-check totals. This included sampled price points multiplied by estimated customer counts in key industries, plus channel checks on how often hybrid deployments are selected due to data residency rules. Where bottom-up views showed gaps, for example bundled pricing where MFT is packaged with other integration tools, we separated the MFT portion using interview-led allocation keys and stress-tested the result across regions.

For forecasting, we used scenario analysis with a base case aligned to expected cloud adoption and security compliance trends, then higher and lower cases that adjust ransomware pressure, regulatory enforcement intensity, and IT budget growth. Assumptions were reviewed with primary respondents to keep the growth path tied to realistic upgrade cycles and procurement behavior.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as enterprise cloud spending direction, security software growth patterns, and reported pipeline commentary in public filings, and then any variances were investigated before sign-off. If an output appeared as an outlier by region or end-user mix, we re-checked inputs, reran sensitivity ranges, and re-contacted respondents when the gap could not be explained by a clear market development.

Each report goes through multi-step analyst reviews, including a final logic check of assumptions, units, and currency conversion timing. Reports are refreshed annually, and interim updates are used when material events occur, such as major regulatory changes or sharp shifts in cloud security spending. Before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Cloud Mft Services Market Size Versus Other Published Estimates

Published market sizes for cloud MFT services can differ substantially because the scope line is drawn differently, and then the same label is used for revenues that are not always comparable. Differences also come from how firms treat hybrid deployments, whether software licenses are counted with services, and how currency timing and base years are handled.

In this study, the key gaps usually come from whether revenues are limited to cloud-delivered MFT services tied to secure transfer workflows, or whether adjacent secure file sharing and broader integration revenues are included. Forecast curves can spread further when ASPs are pushed up without a clear usage metric check. Here the count is kept centered on subscription and service revenues linked to managed transfer activity, with checks on endpoints, throughput bands, and compliance features. This is also why the baseline can differ from sources that blend in license-heavy or wider file exchange spend, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.45 B (2026) | |

| Industry Research Publisher A | USD 3.32 B (2026) | Uses a broader revenue definition that explicitly includes sales of file transfer software and related compliance or governance tools alongside services, which can lift totals versus a services-only view. |

| Industry Research Publisher B | USD 3.78 B (2024) | Uses an earlier base year and a wider segmentation frame that can fold in adjacent cloud file transfer offerings and application use cases, which can expand the demand pool compared with a narrower managed transfer workflow scope. |

The spread across the three numbers is mainly explained by scope boundaries and what is counted as service revenue versus bundled software and adjacent file exchange tools. By keeping inputs traceable to practical demand signals and repeating the same checks across regions and end users, we end up with a value that is easier to reconcile and update as pricing and adoption shift.

Key Questions Answered in the Report

What is the current value of the Cloud MFT Services market?

The Cloud MFT Services market is projected to be worth USD 2.45 billion by 2026.

What is the market's expected growth rate by 2031?

It is forecast to reach USD 3.84 billion by 2031, reflecting a 9.40% CAGR over 2026-2031.

Which deployment model is expanding the quickest?

Hybrid cloud managed file transfer is growing at a 13.92% CAGR as firms balance compliance with scalability.

Why are healthcare organizations accelerating the adoption of MFT?

Electronic health record mandates and HIPAA penalties are driving healthcare’s 12.95% CAGR in MFT spending.

Which transfer type shows the highest growth rate?

Mobile-to-mobile exchanges lead with a 14.88% CAGR due to remote work and bring-your-own-device policies.

Which region is expected to record the fastest market expansion?

The Asia Pacific is projected to grow at a 13.55% CAGR, led by the implementation of new data-protection laws in India and China.

Page last updated on: