Cloud-Based Email Security Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

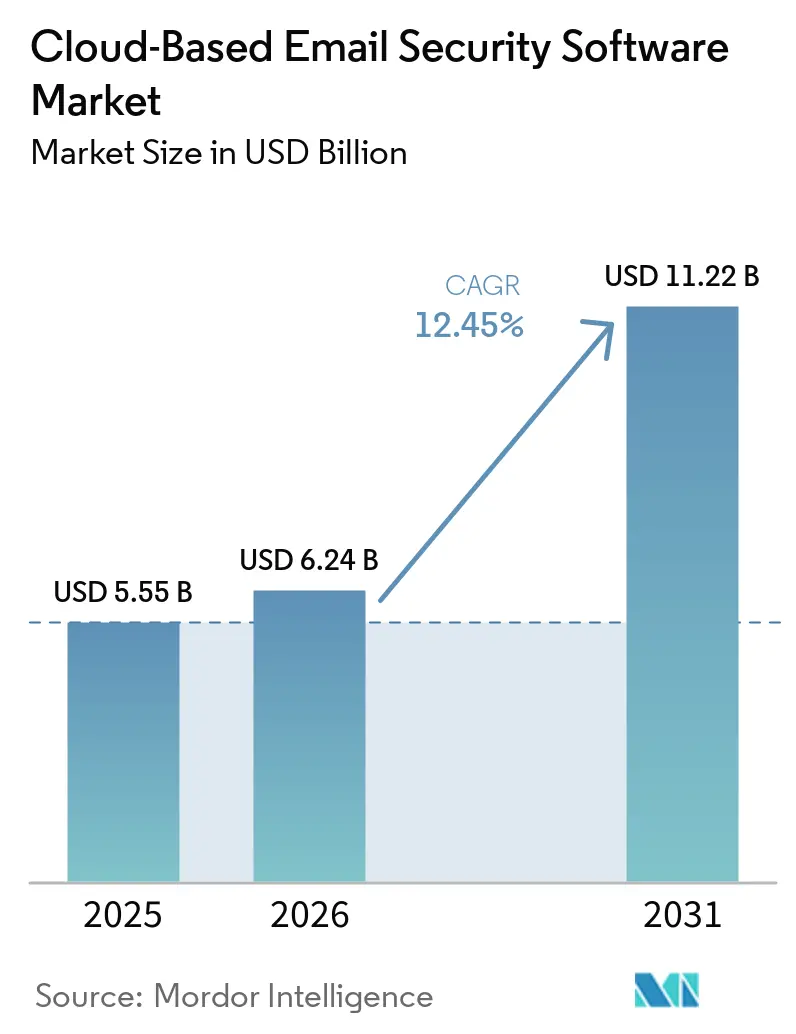

| Market Size (2026) | USD 6.24 Billion |

| Market Size (2031) | USD 11.22 Billion |

| Growth Rate (2026 - 2031) | 12.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-Based Email Security Software Market Analysis by Mordor Intelligence

Cloud-based email security software market size in 2026 is estimated at USD 6.24 billion, growing from 2025 value of USD 5.55 billion with 2031 projections showing USD 11.22 billion, growing at 12.45% CAGR over 2026-2031. A rapid pivot from secure email gateways to API-integrated, cloud-native platforms underpins this growth as enterprises confront AI-powered phishing campaigns that post 24% higher success rates than human-crafted attacks. Quantum-resilient encryption requirements and regionally tighter mandates such as the NIS 2 Directive are pushing organizations to direct 9% of IT budgets to information security[1]European Union Agency for Cybersecurity, “NIS 2 Directive Explained,” enisa.europa.eu. Enterprises also prioritize behavioral analytics to counter generative-AI deepfake emails, while cost-efficient cloud delivery models accelerate adoption among small and mid-sized businesses. Finally, strategic vendor consolidation—exemplified by Proofpoint’s USD 1 billion agreement for Hornetsecurity—signals a race to deliver integrated, human-centric protection that fills the 4.8 million global cybersecurity workforce gap.

Key Report Takeaways

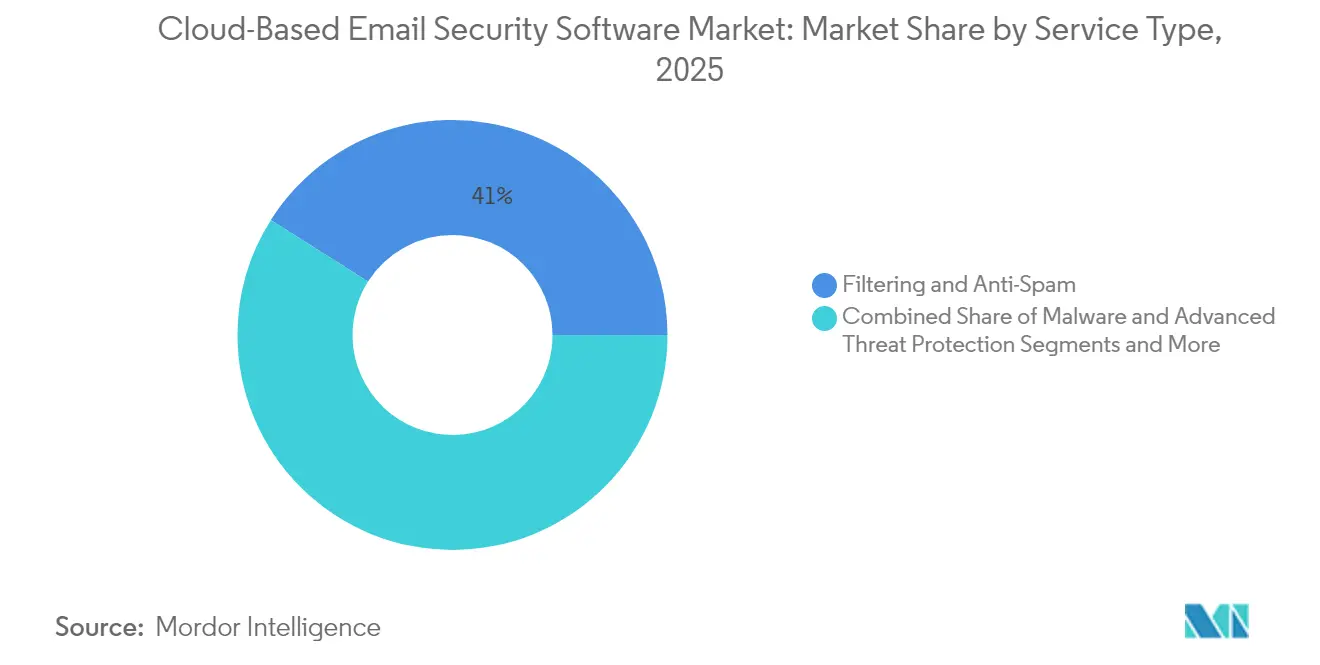

- By service type, Filtering and Anti-Spam held 41.02% of the cloud-based email security software market share in 2025, whereas Data Loss Prevention is projected to advance at a 13.22% CAGR through 2031.

- By platform integration, Secure Email Gateways retained 54.95% revenue share in 2025, but Integrated Cloud Email Security software solutions are poised for a 13.55% CAGR to 2031.

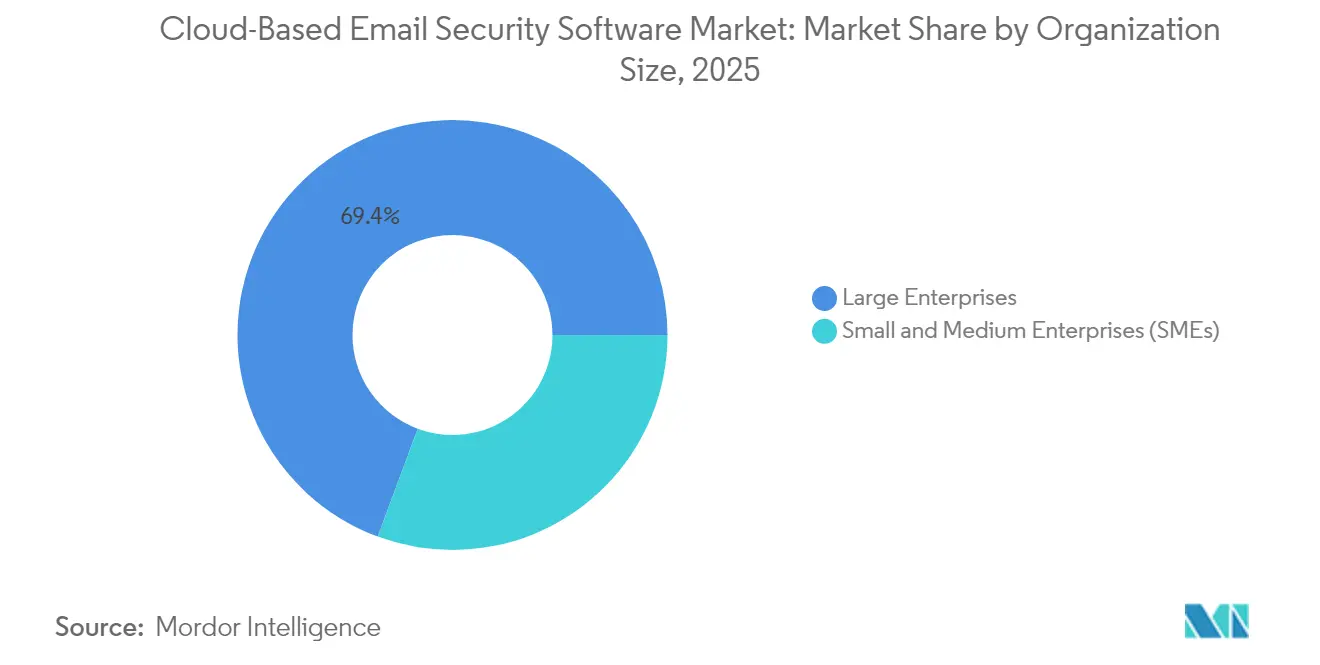

- By organization size, large enterprises commanded 69.35% of the cloud-based email security software market in 2025, yet small and medium enterprises show a 13.98% CAGR as managed services remove deployment barriers.

- By industry vertical, IT and Telecommunications led with 31.05% revenue in 2025; Banking, Financial Services and Insurance is forecast for a 12.58% CAGR through 2031.

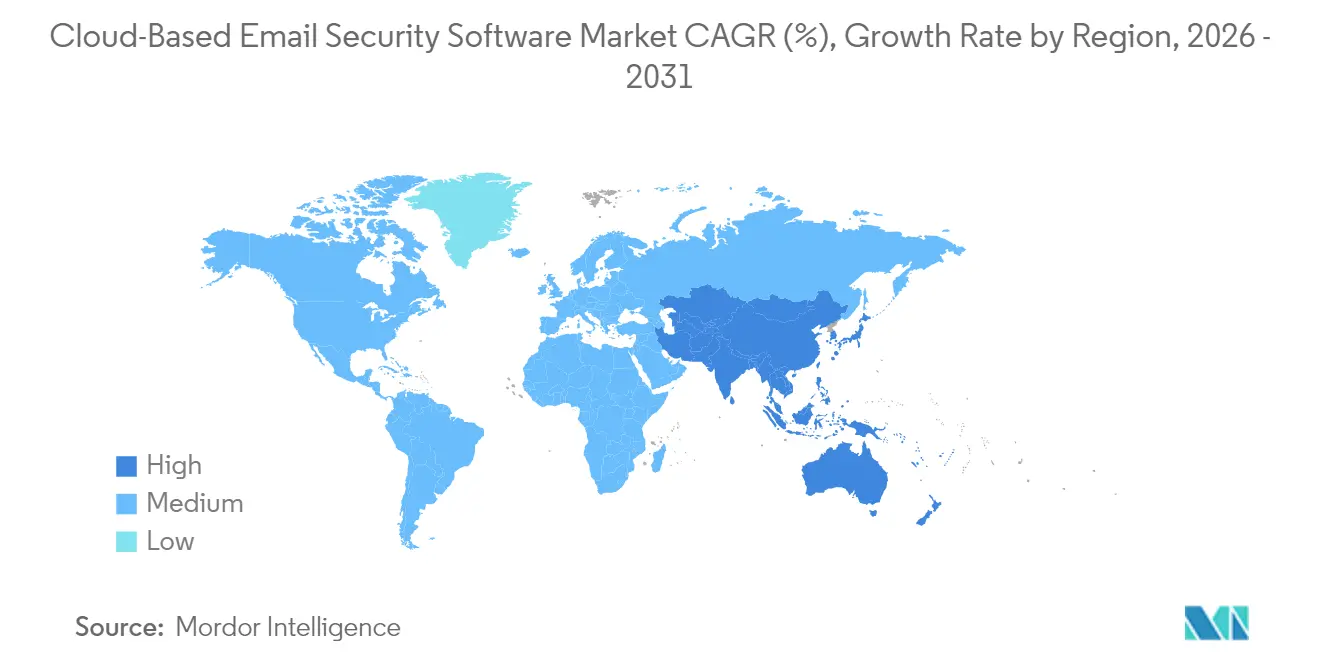

- By geography, North America contributed 38.10% of 2025 revenue, while Asia-Pacific is expected to climb at a 12.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud-Based Email Security Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in AI-driven phishing and BEC attacks | +2.8% | Global; peak influence in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rapid migration from SEG to API-based ICES | +2.1% | North America and Europe; Asia-Pacific following | Medium term (2–4 years) |

| Cost and agility benefits of cloud delivery | +1.7% | Global, especially SMEs in emerging markets | Medium term (2–4 years) |

| Generative-AI deepfake emails | +1.4% | Global; high impact in finance and government | Short term (≤ 2 years) |

| Urgency around quantum-resilient encryption | +1.2% | North America and Europe regulatory-driven | Long term (≥ 4 years) |

| ESG demand for carbon-light email security | +0.9% | Europe leading; wider adoption globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in AI-driven phishing and BEC attacks

Generative-AI tooling now allows adversaries to craft tailored emails that mimic executive tone and timing, driving phishing success rates to 60% and pushing 2024 business email compromise losses to USD 2.9 billion[2]United States Cybersecurity and Infrastructure Security Agency, “BEC Loss Reports,” cisa.gov . Seventy-five percent of phishing kits marketed on the dark web advertise AI functionality, underscoring an industrialized threat economy. Healthcare recorded a 279% jump in AI-enabled BEC incidents with average losses of USD 125,000 per case. Organizations therefore deploy natural-language processing engines that baseline communication patterns and flag linguistic anomalies. Behavioral awareness programs complement technology as employees remain the final checkpoint against well-crafted lures.

Rapid migration from SEG to API-based ICES

Seventy percent of enterprises are actively replacing secure email gateways with Integrated Cloud Email Security platforms that connect directly into Microsoft 365 or Google Workspace via APIs. API integration brings visibility into internal traffic and user behavior without mail-flow rerouting, improving detection efficacy by 30% in customer environments. Real-time telemetry from cloud suites feeds machine-learning models that isolate compromised accounts within minutes. Vendor alliances—such as Proofpoint’s integration with Azure security APIs—lower deployment timelines from months to days, hastening the architectural shift.

Cost and agility benefits of cloud delivery

Cloud-delivered email security consumes 4.1 times less energy than on-premises gateways and can cut carbon emissions by 99% when optimized for hyperscale infrastructure. Subscription pricing removes capital-expenditure barriers, while multi-tenant designs let managed service providers deliver enterprise-grade protection to SMEs. Typical API-based deployments finish in three months, compared with year-long gateway rollouts that require data center redesigns. Unified administration consoles fold email threat telemetry into broader XDR views, reducing operational overhead for stretched security teams.

Generative-AI deepfake emails

Attackers now embed voice or video deepfakes inside email chains to bypass biometric checks, imitating executives and authorizing fraudulent payments. The United Kingdom’s National Cyber Security Centre warns that consumer-grade AI lowers barriers for sophisticated social engineering. Security vendors respond with multi-modal detectors that correlate language, metadata timing, and communication context. Financial institutions are early adopters, calibrating payment approval workflows to flag anomalies and introducing mandatory call-back verification for high-value transfers. Behavioral training modules coach staff to verify unusual requests despite sender familiarity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent skills gap in cloud-security operations | −1.8% | Global; acute in Asia-Pacific and emerging economies | Medium term (2–4 years) |

| Latency and data-sovereignty compliance hurdles | −1.3% | Europe and Asia-Pacific regulatory-driven | Long term (≥ 4 years) |

| Exploitable misconfigurations in multi-cloud | −1.1% | Global; notable in hybrid deployments | Medium term (2–4 years) |

| AI-based evasion of sandboxing | −0.8% | Global; prevalent in advanced threat landscapes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent skills gap in cloud-security operations

The global workforce counts 5.5 million cybersecurity professionals, yet faces a 4.8 million shortfall, and 90% of companies cite cloud and AI security expertise as the hardest to hire. ENISA confirms that 99% of cloud security failures originate from customer misconfigurations rather than provider flaws. Financial services and technology firms hold vacancy rates around 28%, slowing the rollout of behavioral analytics tools that demand specialized tuning. Many organizations therefore shift to managed security services and AI-assisted tooling to offset human shortages, though automation still requires oversight for policy governance.

Latency and data-sovereignty compliance hurdles

Divergent regulations, from GDPR in Europe to the US CLOUD Act, complicate cross-border email routing, especially when encryption keys must remain in specific jurisdictions. Nations including China and Saudi Arabia enforce strict data-localization mandates that fragment global security architectures. Enterprises deploy regional instances to meet residency rules, but added network hops raise latency and entail higher operational cost. Adaptive key-management frameworks and policy-based routing attempt to balance sovereignty with performance, yet legal complexity persists as new localization rules emerge annually.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Proactive data protection surges

Filtering and Anti-Spam retained 41.02% of the cloud-based email security software market in 2025. Data Loss Prevention, however, is projected to grow fastest at 13.22% CAGR because remote work accelerates unstructured data exposure in email workflows. Organizations now value context-aware DLP that tracks content, user, and location metadata in real time, replacing legacy regex pattern matching. Malware and Advanced Threat Protection services integrate large language models that scan attachments for behavioral indicators rather than static signatures. Encryption and Tokenization offerings expand as early movers embed post-quantum algorithms, preparing customers for National Institute of Standards and Technology transition timelines. Collectively, these shifts mark a pivot from perimeter defense to data-centric controls.

Expanding regulatory frameworks such as HIPAA and PCI-DSS compel enterprises to log and audit email-borne data flows. Google’s delivery of end-to-end encryption for Gmail enterprise users illustrates how vendors package compliance inside default settings. The cloud-based email security software market size for DLP-driven offerings is expected to capture a rising share of total spend as organizations tackle insider risk alongside external threat vectors. Vendors also bundle security-awareness training modules that reinforce policy adherence, creating unified platforms that reduce alert fatigue and compliance overhead.

By Platform Integration: API revolution accelerates

Secure Email Gateways still controlled 54.95% revenue in 2025, yet API-enabled Integrated Cloud Email Security solutions are forecast to rise at 13.55% CAGR, reflecting architectural limitations of gateway proxies in cloud-native suites. ICES connects directly into Microsoft 365 and Google Workspace to analyze internal traffic, delivering 30% uplift in social-engineering detection rates. Cloud-native email security platforms also auto-scale, making them attractive for burst workloads and geographically distributed teams. Hybrid approaches persist where heavily regulated sectors maintain on-prem gateways for compliance logging but wrap APIs for behavioral analytics.

As partnerships deepen—Microsoft recently extended Azure-based threat-signal sharing with Proofpoint—customers gain unified telemetry that feeds downstream XDR platforms. Resulting efficiencies shorten mean-time-to-detect incidents by up to 40%. The cloud-based email security software market size attached to API-first deployments is projected to overtake SEG allocations before 2029 as refresh cycles retire appliance footprints.

By Organization Size: SME adoption surge

Large enterprises contributed 69.35% of 2025 revenue, yet small and medium enterprises are accelerating at 13.98% CAGR. Managed service providers leverage multi-tenant platforms that let SMEs subscribe to the same behavioral engines used by Fortune 500 firms without capital expense. Microsoft surveys show that 94% of SMEs rate cybersecurity as critical following at least one attack experience in the past year. Proofpoint’s channel ecosystem reaches 125,000 SMBs through 12,000 partners, evidencing scalable go-to-market models.

Automation is pivotal: policy templates and guided onboarding shrink configuration steps from hundreds to single-digit prompts, countering skills shortages. As a result, the cloud-based email security software market sees convergence in capability parity, where SMEs can procure advanced features such as automated phishing triage or end-user remediation workflows previously reserved for large enterprises. Collaborative intelligence feeds also enable community-wide defense as attacks detected in one tenant inoculate peers within minutes.

By Industry Vertical: BFSI compliance acceleration

IT and Telecommunications retained 31.05% revenue in 2025 owing to high email volume and early cloud adoption. Banking, Financial Services and Insurance follows closely, projected to grow at 12.58% CAGR under stronger encryption, audit, and fraud-mitigation mandates. Healthcare faces heightened urgency after a sharp rise in AI-enhanced BEC attacks, adopting HIPAA-aligned encryption and anomaly detection to protect personal health information. Government and Defense prioritize quantum-resilient key management to secure classified communications.

Retail and E-Commerce lag in DMARC deployment, leaving customer data vulnerable to spoofing. Sector-specific modules therefore bundle compliance checklists and reporting templates that reduce audit effort. The cloud-based email security software market size for BFSI is predicted to reach USD 3.48 billion by 2031 as institutions modernize legacy message archives and integrate secure omnichannel communications. Vendor roadmaps increasingly include blockchain-based tamper-evident audit trails tailored for regulators, further cementing vertical customization as a competitive lever.

Geography Analysis

North America led the cloud-based email security software market with 38.10% revenue in 2025. Widespread Microsoft 365 adoption and high incident disclosure rates drive investment, while tight breach-notification windows compel rapid deployment of automated response tooling. Vendor consolidation in the region accelerates platform breadth, offering bundled email, endpoint, and identity security under single contracts. Government directives such as the US Cybersecurity Strategy promote zero-trust email architectures, underpinning continued demand.

Asia-Pacific is forecast for the highest 12.74% CAGR through 2031 amid rapid digital transformation and the region’s 31% share of global cyberattacks. China and Japan together are projected to expand at 16.9% CAGR through 2028 as data-localization requirements fuel demand for sovereign cloud instances that embed email security controls in country-specific data centers. India emerges as a growth hotspot, buoyed by its expanding IT services sector and government-led “Digital India” program that offers tax incentives for cybersecurity investment.

Europe’s momentum rests on stringent regulations: GDPR fines for data-exfiltration via email and the new NIS 2 Directive have elevated security spending to 9% of IT budgets on average. Organizations in Germany and France push suppliers for quantum-resilient encryption and ESG-validated data centers. Elsewhere, South America and the Middle East and Africa remain nascent markets, yet cloud vendor region launches combined with rising ransomware incidents foster gradual uptake. As hyperscalers open local availability zones, latency barriers fall, and email security services become compliant with emerging data-residency laws.

Competitive Landscape

The cloud-based email security software industry features moderate consolidation. Vendors pursue adjacent acquisitions to deliver integrated, human-centric protection as customers favor one-stop security suites. Proofpoint’s USD 1 billion agreement for Hornetsecurity extends European reach and injects SMB-focused distribution expertise. Microsoft’s Security Copilot adds 11 generative-AI agents that automate phishing classification, intent analysis, and incident response tasks, addressing the workforce gap through guided remediation.

Technology differentiation centers on three pillars. First, API extensibility unlocks granular telemetry from SaaS suites, with early movers offering 400-plus policy hooks for automation workflows. Second, behavioral analytics at scale leverages large language models fine-tuned on billions of enterprise emails to detect nuanced social-engineering tactics. Third, quantum-resilient encryption now enters commercial roadmaps as enterprises future-proof sensitive archives.

White-space opportunities arise in sovereign-cloud deployments where regional regulations demand in-country processing. Vendors also chase ESG-aligned solutions that measure carbon savings tied to email security offload. Disruptors such as IRONSCALES embed GPT-powered copilots directly within Outlook clients, reducing false-positive fatigue through conversational threat explanations. Incumbents counter by opening threat-intelligence exchanges that democratize detection signals across partner ecosystems. Competitive intensity is expected to heighten as hyperscalers embed native email protection that could commoditize baseline features, forcing specialized vendors to innovate on analytics and compliance depth.

Cloud-Based Email Security Software Industry Leaders

Cisco Systems Inc.

Proofpoint Inc.

Trend Micro Inc.

Fortinet Inc.

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Google enabled end-to-end encryption for Gmail enterprise users, granting customer-controlled encryption keys.

- March 2025: Proofpoint signed a definitive agreement to acquire Hornetsecurity for more than USD 1 billion, expanding Microsoft 365 defenses and SMB reach.

- March 2025: Microsoft launched 11 AI-powered security agents for Security Copilot to automate phishing detection and incident response.

- March 2025: Trend Micro released the Cybertron AI platform built on open-source components for proactive cloud threat detection.

Global Cloud-Based Email Security Software Market Report Scope

Cloud email security solutions provide robust protection against cyber threats transmitted via email. A key feature of these systems is their Anti-Phishing capability: As phishing attempts grow increasingly sophisticated, recognizing and countering them becomes ever more challenging.

The cloud-based email security software market is segmented by deployment model (public, private, and hybrid), by end-user industry (BFSI, government, IT and telecommunications, retail, and other end-user industries), and by geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Italy, Spain, and Rest of Europe], Asia Pacific [India, China, Japan, Australia, South Korea, and Rest of Asia Pacific], Latin America [Brazil, Mexico, Argentina and Rest of Latin America], and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Filtering and Anti-Spam |

| Malware and Advanced Threat Protection |

| Data Loss Prevention |

| Encryption and Tokenization |

| Others |

| Secure Email Gateway (SEG) |

| Integrated Cloud Email Security (ICES/API) |

| Cloud-Native Email Security Platform |

| Hybrid Gateway and API |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Government and Defense |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Filtering and Anti-Spam | ||

| Malware and Advanced Threat Protection | |||

| Data Loss Prevention | |||

| Encryption and Tokenization | |||

| Others | |||

| By Platform Integration | Secure Email Gateway (SEG) | ||

| Integrated Cloud Email Security (ICES/API) | |||

| Cloud-Native Email Security Platform | |||

| Hybrid Gateway and API | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | BFSI | ||

| Government and Defense | |||

| IT and Telecommunications | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the cloud-based email security software market?

The market stands at USD 6.24 billion in 2026 and is projected to reach USD 11.22 billion by 2031 at a 12.45% CAGR.

Which service segment is growing fastest?

Data Loss Prevention leads growth with a 13.22% CAGR through 2031, reflecting a shift toward proactive data-centric controls.

Why are API-based Integrated Cloud Email Security platforms gaining traction?

API integration lets solutions ingest real-time telemetry from Microsoft 365 and Google Workspace, improving detection accuracy by 30% and reducing deployment timelines.

How large is the skills gap affecting cloud-based email security software?

The industry faces a shortfall of 4.8 million cybersecurity professionals worldwide, with 90% of organizations citing cloud-security expertise as the hardest to recruit.

Which region is forecast for the highest growth?

Asia-Pacific is expected to post a 12.74% CAGR to 2031 due to rapid digital transformation, stringent data-localization rules, and rising cybercrime rates.

How are vendors addressing quantum-resilient encryption?

Suppliers are embedding lattice-based algorithms and crypto-agility frameworks so enterprises can rotate to post-quantum keys without disrupting email workflows.

Page last updated on: