Cloud AI Market Size and Share

Market Overview

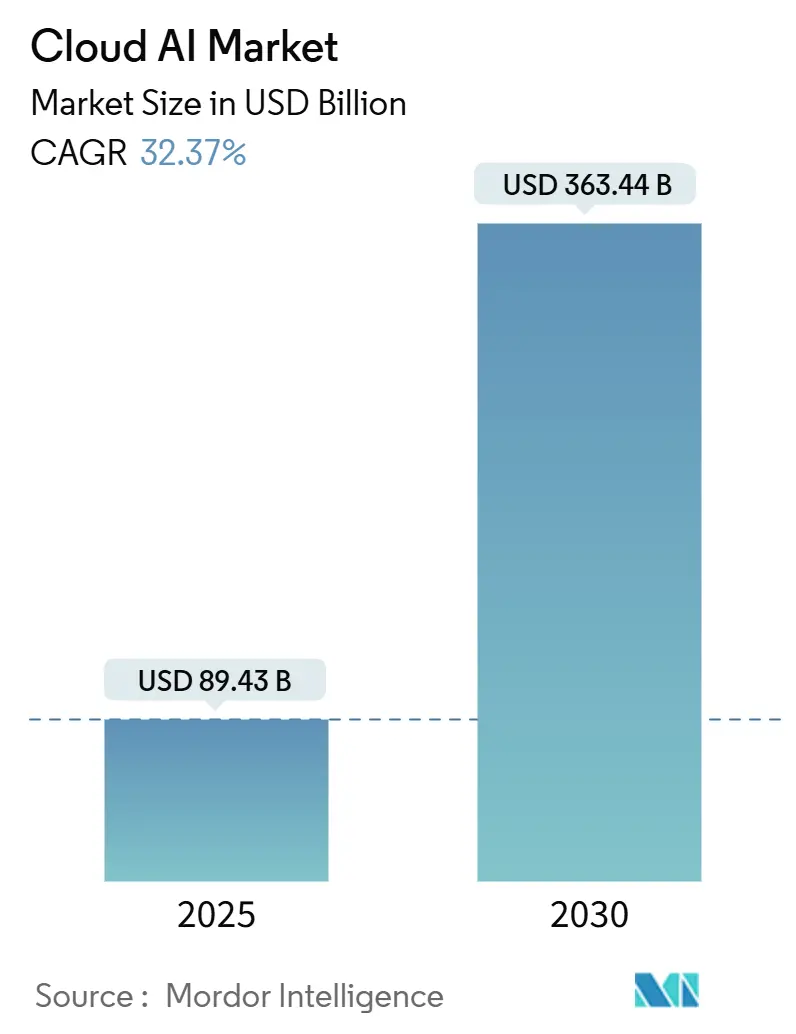

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 89.43 Billion |

| Market Size (2030) | USD 363.44 Billion |

| Growth Rate (2025 - 2030) | 32.37% CAGR |

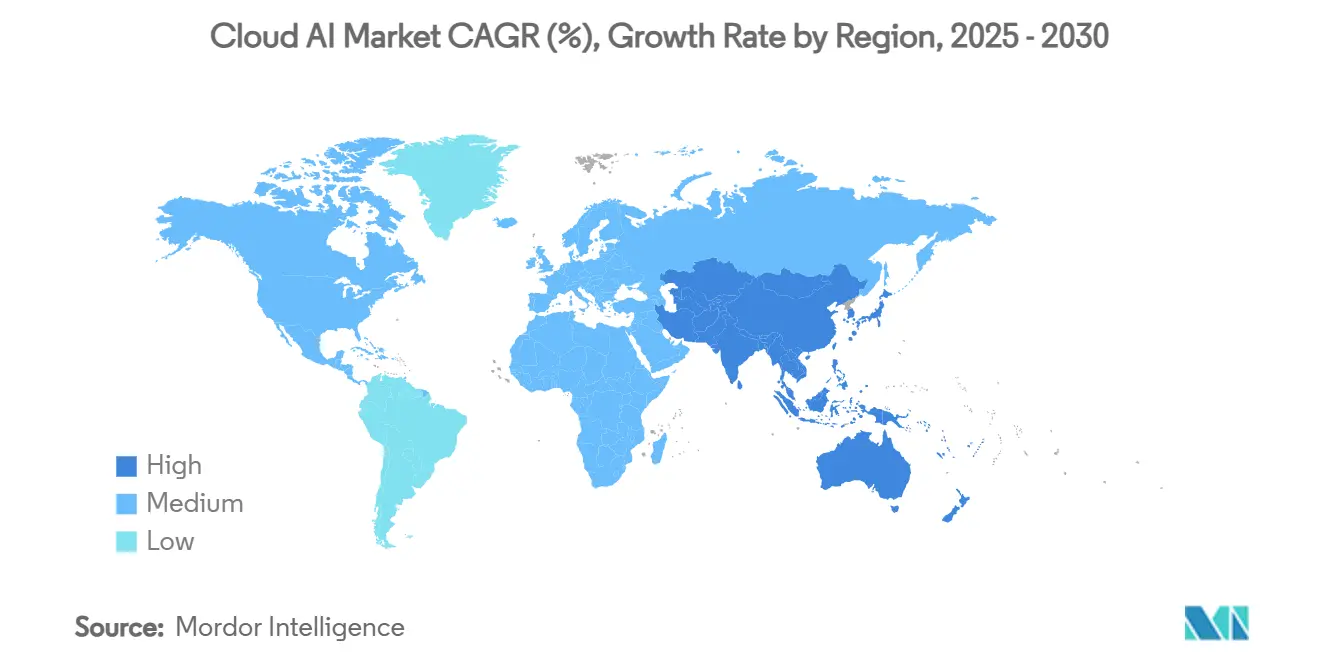

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cloud AI Market Analysis by Mordor Intelligence

The Cloud AI market reached USD 89.43 billion in 2025 and is forecast to advance to USD 363.44 billion by 2030, reflecting a 32.37% CAGR.[1]Microsoft, “Microsoft 2024 Annual Report,” Microsoft.com Generative AI partnerships, such as Microsoft’s USD 13 billion commitment to OpenAI and Amazon’s USD 8 billion investment in Anthropic, are expanding capacity, lowering entry barriers, and accelerating time-to-value for enterprises.[2]Amazon Web Services, “AWS plans to invest 2.26 trillion yen into its Japanese cloud infrastructure by 2027,” Amazonaws.com Mid-market adoption is rising as GPU-fractionalization technologies reduce infrastructure costs, while sector-specific regulations in healthcare and financial services favor providers that can demonstrate robust governance. Supply-chain dynamics, notably in high-bandwidth memory, spur chip diversification strategies among hyperscalers, and carbon-aware workload orchestration begins to influence data-center siting decisions.

Key Report Takeaways

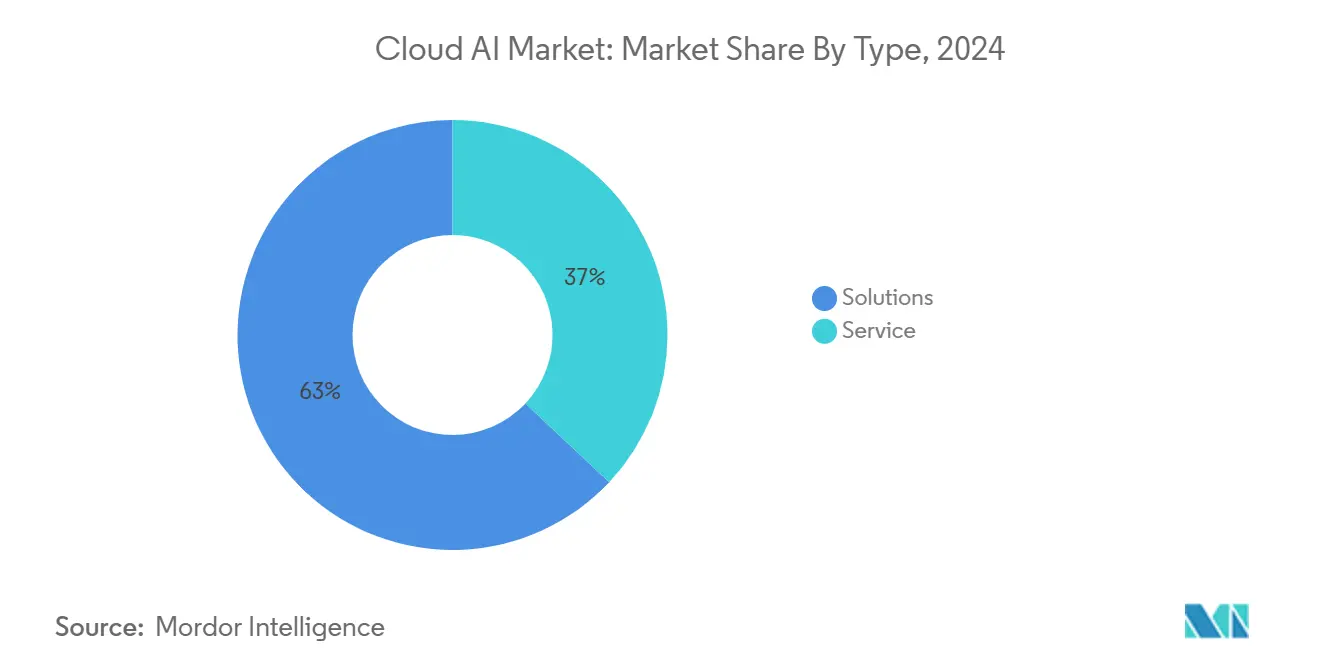

- By type, Solutions held 63% of the Cloud AI market share in 2024, while Services are projected to expand at 33.98% CAGR to 2030.

- By end-user vertical, BFSI led with 29% revenue share in 2024; Healthcare is forecast to rise at a 35.61% CAGR through 2030.

- By deployment model, Public Cloud dominated with 71% share of the Cloud AI market size in 2024, whereas Hybrid/Multi-cloud is advancing at 33.11% CAGR.

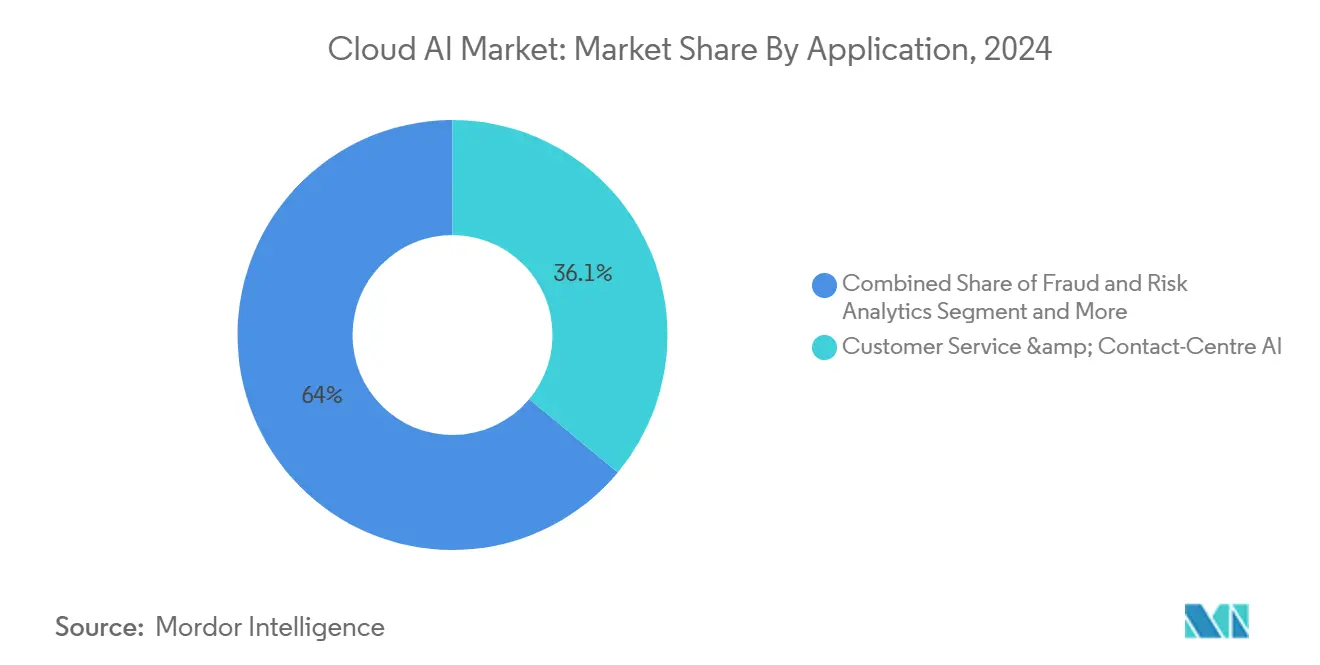

- By application, Customer Service and Contact-Centre AI accounted for 36.05% share of the Cloud AI market size in 2024; Marketing and Personalisation is growing at 32.53% CAGR to 2030.

- By technology, Machine Learning commanded 34.60% Cloud AI market share in 2024, and Natural Language Processing is set to climb at 38.71% CAGR.

- By region, North America held 41% of revenue in 2024, while Asia Pacific is expected to register a 32.41% CAGR through 2030.

Global Cloud AI Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising big-data volume | +8.2% | Global, led by North America and APAC | Medium term (2–4 years) |

| Growing adoption of AI-as-a-Service | +9.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Increasing demand for virtual assistants and GenAI chatbots | +6.8% | Global, early uptake in North America and APAC | Short term (≤ 2 years) |

| GenAI GPU-fractionalization expanding SME access | +4.3% | Global, strong in emerging markets | Medium term (2–4 years) |

| Edge–cloud AI interoperability standards | +2.9% | Global, manufacturing hubs | Long term (≥ 4 years) |

| Carbon-aware workload orchestration incentives | +1.4% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

Source: Mordor Intelligence

Growing Adoption of AI-as-a-Service (AIaaS)

Enterprises are shifting from capital-heavy on-premises deployments to pay-as-you-go AI services. Microsoft’s AI business reached a USD 13 billion annual run rate in Q2 FY 2025, contributing 16 percentage points to Azure growth. Custom silicon such as AWS Trainium2 delivers 30-40% price-performance gains, broadening AI accessibility for mid-market firms that must meet regional data-sovereignty rules. Uptake is evident across Europe and Asia, where 60% of mid-size enterprises expect regionally trained language models by 2025.

Rising Big-Data Volume

Unstructured data exceeds 80% of enterprise information assets, driving demand for real-time AI analytics. Healthcare use cases include Mayo Clinic processing genomic records from 100,000 patients to improve early disease detection. Financial services apply cloud AI to reduce false positives in anti-money-laundering screening by 95%. Edge-cloud convergence allows manufacturers to perform predictive maintenance on IoT data streams with millisecond response times.

Increasing Demand for Virtual Assistants and GenAI Chatbots

Conversational AI is scaling from simple chatbots to multimodal agents that complete complex workflows. Goldman Sachs deployed its GS AI Assistant to 10,000 staff, cutting document-creation time from hours to minutes. Microsoft’s Copilot Wave 2 introduces Researcher and Analyst agents capable of multi-step data analysis across Microsoft 365 applications.[3]World Wide Technology, “Microsoft 365 Copilot Wave 2: Spring 2025 Release Overview,” Wwt.com Healthcare providers employ ambient listening systems that chart patient records without manual entry, freeing nursing time for direct care.

GenAI GPU-Fractionalization Expanding SME Access

Fractional GPU consumption models reduce experimentation costs by up to 70% compared with dedicated hardware. Oracle Cloud Infrastructure now supports fractional access to clusters of up to 64,000 NVIDIA Blackwell GPUs, enabling startups to train advanced models without marquee budgets. Manufacturing surveys show 93% of firms launched new AI projects in 2024, though only 20% completed rollouts owing to integration complexity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of skilled workforce and data-security concerns | −6.4% | Global, acute in APAC and emerging markets | Medium term (2–4 years) |

| Persistent GPU/HBM supply-chain shortages | −4.7% | Global, concentrated in Asian manufacturing | Short term (≤ 2 years) |

| AI datacenter energy constraints and carbon regulations | −3.2% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Geopolitical GPU export-control frameworks | −2.8% | China, Russia, select emerging markets | Medium term (2–4 years) |

Source: Mordor Intelligence

Persistent GPU/HBM Supply-Chain Shortages

SK Hynix controls 70% of the HBM market and reports full allocation through 2025, creating cost pressures for cloud providers.[4]South China Morning Post, “Nvidia supplier SK Hynix says 2025 HBM chips for AI processors nearly sold out,” Scmp.com AWS counters with Trainium custom chips, while Oracle procures thousands of NVIDIA Blackwell GPUs to sustain training capacity. Tight memory supply has triggered price spikes in DDR5 and VRAM, with Samsung inking a USD 3 billion HBM3E supply deal with AMD.

Lack of Skilled Workforce and Data-Security Concerns

A global talent deficit inflates AI engineer salaries by up to 50%, and regulated sectors face shortages in model-governance expertise. JPMorgan Chase employs more than 2,000 AI specialists yet still cites gaps in explainability skills. The EU AI Act classifies most healthcare AI tools as high-risk, intensifying compliance burdens that demand scarce legal and technical knowledge.

Segment Analysis

By Type: Services Scale on Advisory Demand

Solutions represented 63% of the Cloud AI market in 2024. Enterprises gravitated to packaged platforms that integrate with existing DevOps pipelines, ensuring quick deployment and consistent performance. As adoption deepens, professional guidance becomes essential for migration roadmaps and governance, pushing the Services segment to a forecast 33.98% CAGR.

Services growth reflects multi-year transformation programs that include strategy, model tuning, and managed operations. Firms such as Accenture have retrained 1,400 engineers for Anthropic-on-AWS implementations, directly addressing enterprise skills gaps. Combined solution-service offerings are growing in popularity, enabling organizations to onboard AI quickly while building internal competencies.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Healthcare Surges

BFSI held 29% Cloud AI market share in 2024 due to fraud analytics and robo-advisory use cases. However, Healthcare is set to grow at 35.61% CAGR, buoyed by AI-enabled diagnostics and ambient clinical documentation.

Hospitals deploy large language models for radiology triage and personalized treatment recommendations. The FDA’s January 2025 guidance provides a clear regulatory path, encouraging capital investment. Manufacturing and retail follow, leveraging AI for defect detection and inventory optimization, respectively.

By Deployment Model: Hybrid Rises for Flexibility

Public Cloud controlled 71% of the Cloud AI market size in 2024 thanks to hyperscale economies and a broad services catalog. Yet, Hybrid/Multi-cloud is projected to grow 33.11% CAGR as firms balance cost, sovereignty, and resilience.

Oracle’s MultiCloud database revenue more than doubled year-over-year, illustrating customer appetite for distributing workloads across vendors. Providers are enhancing direct interconnects and policy-based data controls to smooth hybrid operations and minimize egress fees.

By Application: Personalised Marketing Gains SpeeD

Customer Service and Contact-Centre AI accounted for 36.05% of the Cloud AI market size in 2024, driven by conversational agents that shorten handling times and boost satisfaction. Marketing and Personalisation will expand 32.53% CAGR as brands deploy recommendation models to tailor offers in real time.

Retailers embed AI in campaign orchestration systems that analyze click-stream data within seconds, improving conversion rates. Manufacturing and energy sectors continue to expand predictive-maintenance deployments, capturing gains in uptime and safety.

Note: Segment shares of all individual segments available upon report purchase

By Technology: NLP Outpaces for GenAI

Machine Learning secured 34.60% Cloud AI market share in 2024, underpinning classic forecasting and optimization. Natural Language Processing is set to grow 38.71% CAGR on the back of generative models that create, summarize, and translate content at scale.

Multimodal architectures weave NLP with computer vision and speech to deliver richer interactions, while reinforcement learning optimizes sequential decision tasks in logistics and finance. Vendors differentiate with domain-tuned language models that embed privacy and bias-mitigation techniques.

Geography Analysis

North America retained 41% Cloud AI market share in 2024, anchored by hyperscaler footprints and venture funding. Regulatory clarity, exemplified by the FDA’s AI device guidelines, encourages adoption across life-sciences and finance. Capital outlays include Amazon’s USD 8 billion Anthropic investment and Microsoft’s continued OpenAI integration, reinforcing regional dominance.

Asia Pacific is the fastest-growing territory with 32.41% CAGR. China’s projected USD 46 billion cloud spend for 2025, along with Alibaba’s multi-year capex commitment, fuels infrastructure expansion. Japan accelerates with Oracle’s USD 8 billion pledge and Tokyo’s selection for OpenAI’s first Indo-Pacific branch. India and Southeast Asia benefit from digital public-infrastructure programs and rising developer communities.

Europe shows steady growth amid complex regulation. The EU AI Act provides a harmonized framework that advantages providers with certified governance. Sovereign cloud initiatives and carbon-reduction mandates encourage hybrid architectures. Emerging markets in the Middle East and Africa witness early uptake, backed by sovereign-wealth investments in data centers.

Competitive Landscape

Competition centers on hyperscalers racing to integrate proprietary silicon, large models, and vertical solutions. AWS leverages its Trainium/Inferentia roadmap to drive cost efficiency, complemented by a USD 8 billion Anthropic pact. Microsoft embeds OpenAI capabilities across Azure and Microsoft 365, delivering a USD 13 billion annual run rate for AI services. Google Cloud counters with Trillium TPUs that quadruple training throughput

Oracle positions on high-performance clusters, procuring thousands of NVIDIA Blackwell GPUs, and announcing a USD 40 billion chip spend for OpenAI’s Texas installation. Supply-chain fragility in HBM memory pressures all players, prompting multi-vendor agreements and in-house chip projects.

Specialist providers exploit white spaces in regulated verticals, edge-cloud orchestration, and compliance automation. Consolidation continues through strategic investments and ecosystem alliances that marry infrastructure with model innovation.

Cloud AI Industry Leaders

-

Amazon Web Services Inc.

-

Microsoft Corporation

-

Google LLC

-

IBM Corporation

-

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Oracle will invest over USD 40 billion in NVIDIA chips for OpenAI’s Texas data center

- June 2025: OpenAI signed a cloud partnership with Google Cloud to diversify compute sources

- May 2025: Microsoft released Copilot Wave 2 with Researcher and Analyst agents

- April 2025: SK Hynix posted record quarterly profit on HBM demand, holding 70% share

Global Cloud AI Market Report Scope

An AI cloud comprises a shared infrastructure for AI use cases, simultaneously supporting several projects and AI workloads. The AI cloud pools various hardware and software resources to deliver AI software-as-a-service (SaaS) on cloud infrastructure, providing enterprises access to key AI capabilities. As such, the study tracks revenues accrued from off-the-shelf AI tools that are offered through cloud technologies. The study also considers revenues accrued from training, consulting, and system integration services for Cloud AI.

The study is segmented by type (Solution, Services), end-user industry (BFSI, Healthcare, Automotive, Retail, Government, and Education, among others), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided regarding value (USD billion) for all the above segments.

| By Type | Solution | |||

| Service | ||||

| By End-user Vertical | BFSI | |||

| Healthcare | ||||

| Automotive and Mobility | ||||

| Retail and E-commerce | ||||

| Government and Public Sector | ||||

| Education | ||||

| Manufacturing | ||||

| By Deployment Model | Public Cloud | |||

| Private Cloud | ||||

| Hybrid / Multi-cloud | ||||

| By Application | Customer Service and Contact-Centre AI | |||

| Predictive Maintenance and Asset Ops | ||||

| Fraud and Risk Analytics | ||||

| Marketing and Personalisation | ||||

| Computer-Vision-as-a-Service | ||||

| By Technology | Machine Learning | |||

| Natural Language Processing | ||||

| Computer Vision | ||||

| Generative AI | ||||

| Reinforcement and Edge AI | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Chile | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Netherlands | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| ASEAN | ||||

| Rest of Asia Pacific | ||||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) | ||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Kenya | ||||

| Rest of Africa | ||||

| Solution |

| Service |

| BFSI |

| Healthcare |

| Automotive and Mobility |

| Retail and E-commerce |

| Government and Public Sector |

| Education |

| Manufacturing |

| Public Cloud |

| Private Cloud |

| Hybrid / Multi-cloud |

| Customer Service and Contact-Centre AI |

| Predictive Maintenance and Asset Ops |

| Fraud and Risk Analytics |

| Marketing and Personalisation |

| Computer-Vision-as-a-Service |

| Machine Learning |

| Natural Language Processing |

| Computer Vision |

| Generative AI |

| Reinforcement and Edge AI |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Cloud AI market?

The Cloud AI market stands at USD 89.43 billion in 2025 and is projected to reach USD 363.44 billion by 2030.

Which sector is growing fastest within the Cloud AI market?

Healthcare leads growth with a 35.61% CAGR through 2030, propelled by diagnostic, ambient listening, and personalized-medicine applications.

Why are hybrid deployments gaining traction?

Hybrid architectures let organizations balance cost control, data-sovereignty compliance, and resilience, driving a 33.11% CAGR for Hybrid/Multi-cloud deployments.

How are supply-chain constraints affecting Cloud AI?

Limited HBM memory capacity raises infrastructure costs and spurs hyperscalers to develop custom chips and long-term vendor agreements.

What technologies are advancing fastest?

Natural Language Processing, closely tied to generative AI, is expected to expand at 38.71% CAGR as enterprises embed conversational agents across workflows.

Which regions will contribute most to future growth?

Asia Pacific, led by China, Japan, and India, is forecast to record a 32.41% CAGR on the strength of sovereign AI initiatives and large-scale infrastructure investments.

Page last updated on: July 7, 2025