Clinical Trial Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

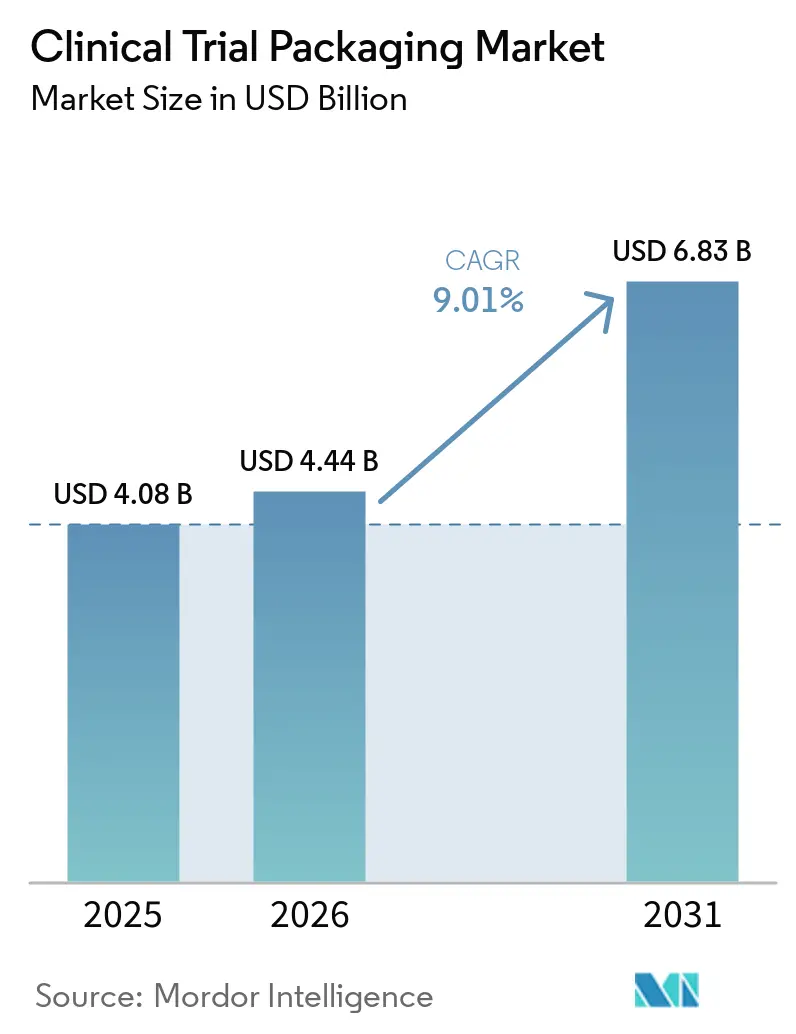

| Market Size (2026) | USD 4.44 Billion |

| Market Size (2031) | USD 6.83 Billion |

| Growth Rate (2026 - 2031) | 9.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

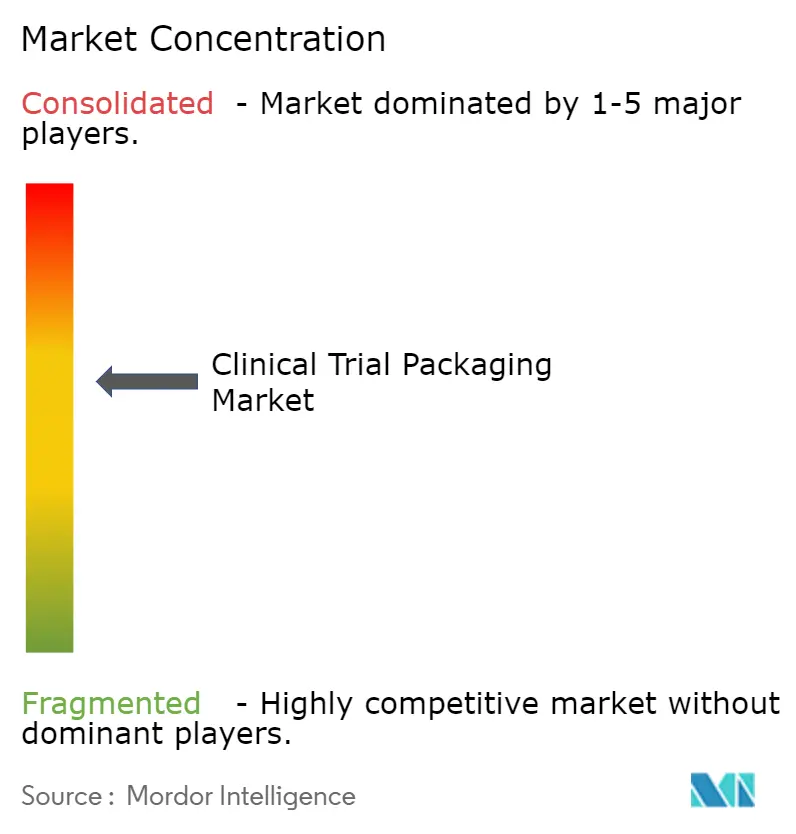

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Packaging Market Analysis by Mordor Intelligence

The clinical trial packaging market size is projected to be USD 4.08 billion in 2025, USD 4.44 billion in 2026, and reach USD 6.83 billion by 2031, growing at a CAGR of 9.01% from 2026 to 2031. This expansion reflects a deeper change in how investigational medicinal products are packed, labeled, and moved across increasingly complex trial networks. The clinical trial packaging market is also supported by the growing share of biologic and injectable drug candidates, which require tighter control over container performance, barrier properties, and stability than conventional small-molecule drugs. At the same time, decentralized and direct-to-patient study models now influence more than half of global trials, driving demand for patient-ready kits, stronger chain-of-custody controls, and more flexible secondary packaging workflows. The clinical trial packaging market is further supported by outsourcing, because sponsors often find it difficult to manage small-batch runs, traceability rules, and cold-chain handling internally. Cost pressure, dangerous goods handling, and detailed documentation still weigh on margins for smaller providers, yet those same barriers continue to strengthen the case for integrated clinical supply partners.

Key Report Takeaways

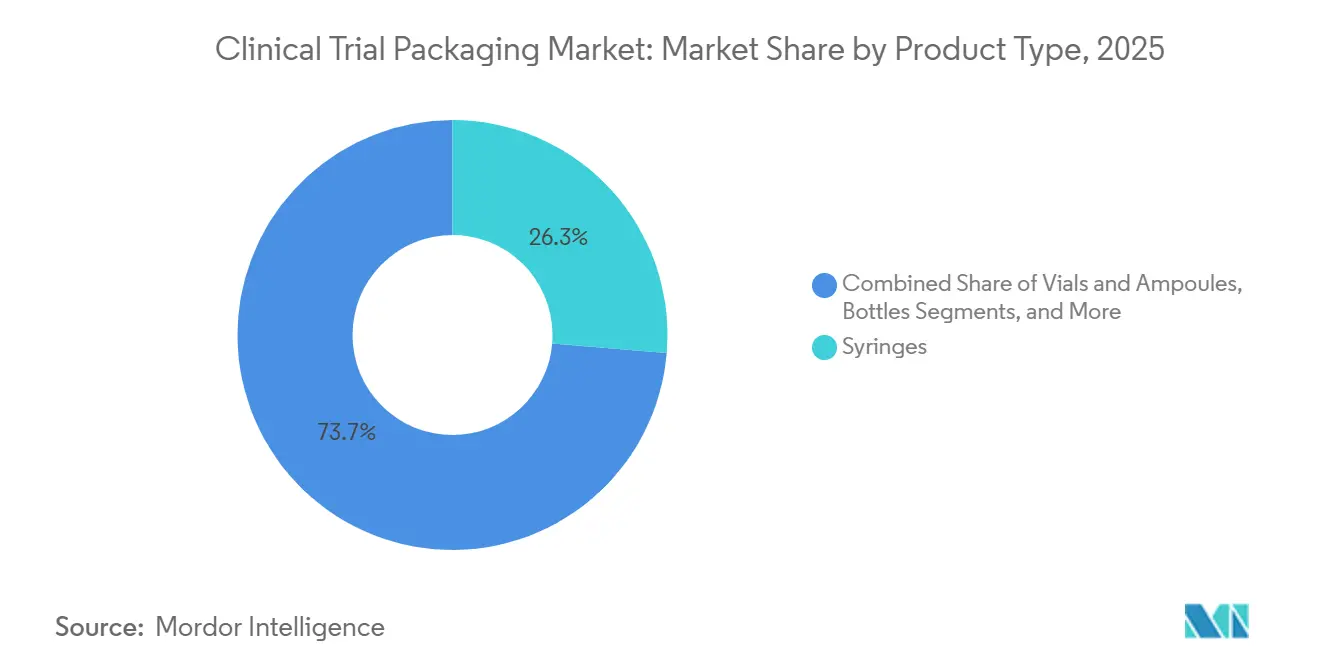

- By product type, syringes captured 26.34% of the clinical trial packaging market share in 2025.

- By material type, the clinical trial packaging market size for metal is projected to expand at a 10.28% CAGR through 2031.

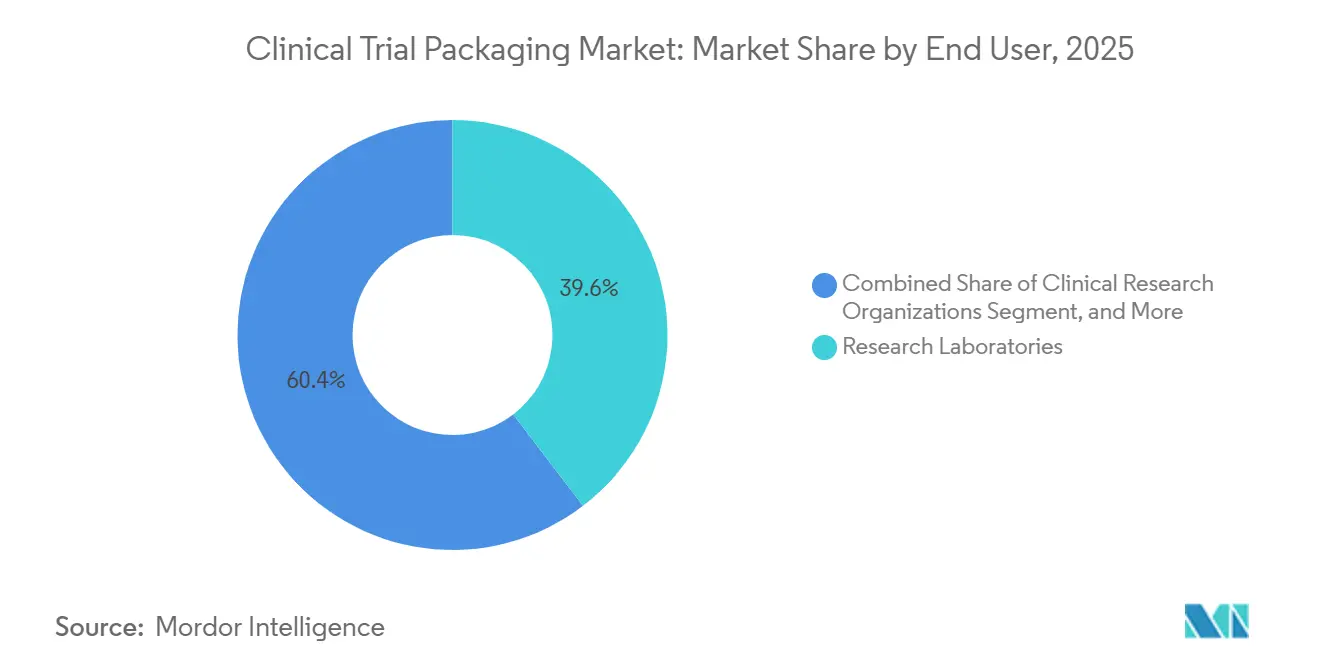

- By end user, research laboratories accounted for 39.61% of the clinical trial packaging market share in 2025.

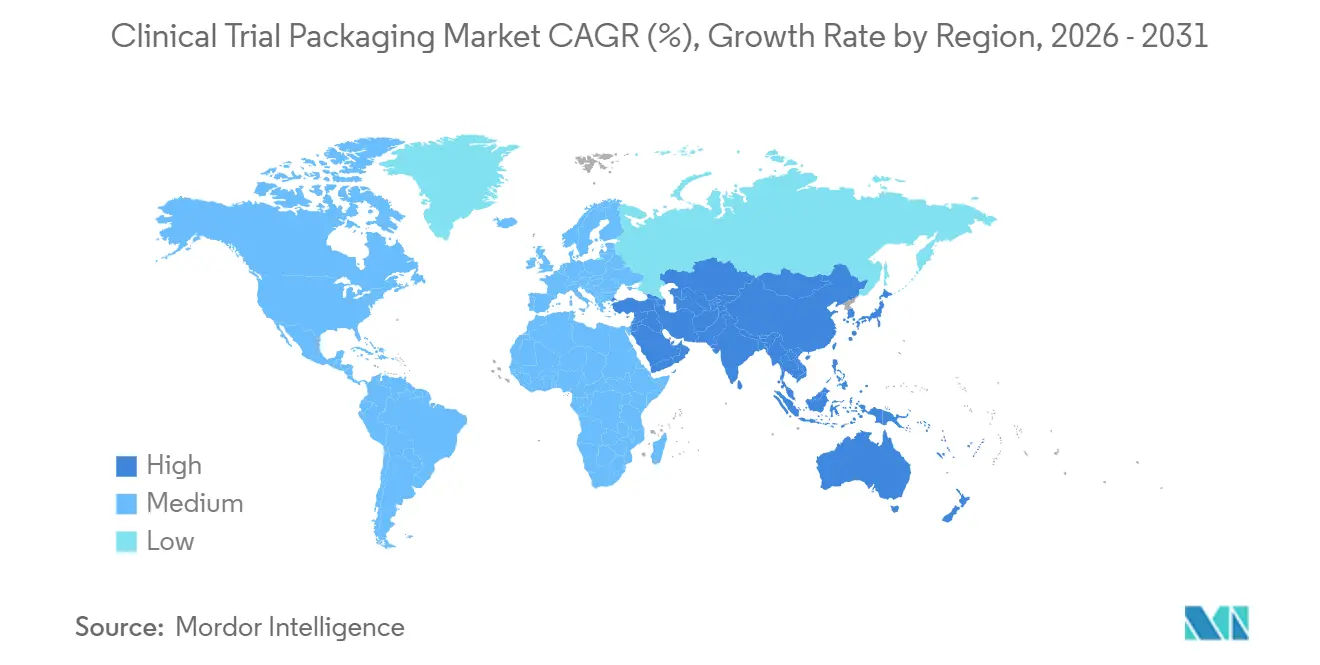

- By geography, the clinical trial packaging market size for Asia-Pacific is projected to advance at a 10.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trial Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Clinical Trial Volumes and R&D Intensity | +2.5% | Global | Short term (≤ 2 years) |

| Rising Biologics and Injectable Drug Development | +2.1% | North America and Europe, spill over to the Asia-Pacific | Medium term (2-4 years) |

| Expansion of Decentralized and Direct-To-Patient Trial Models | +1.4% | North America, Europe, and the Asia-Pacific, with gains in | Medium term (2-4 years) |

| Increasing Outsourcing to Integrated Clinical Supply Partners | +1.1% | Global | Short term (≤ 2 years) |

| ICH E6(R3) Traceability and Blinding Requirements | +0.8% | Global, with early compliance gains in North America and the EU | Short term (≤ 2 years) |

| Acceleration of Cell and Gene Therapy Trials | +0.5% | North America, Europe, Asia-Pacific core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Clinical Trial Volumes and R&D Intensity

Sponsor R&D budgets stayed elevated across 2023 to 2025 as companies refilled pipelines, responded to biosimilar pressure, and funded first-in-human work in newer modalities. That rise in trial activity directly affects the clinical trial packaging market, as each study phase requires its own labeling, blinding, accountability, and release process. Trial amendments add another layer of demand, since mid-study protocol changes can force relabeling or repackaging of inventory that has already been produced. Clinigen reported that its on-demand packaging model ships within 48 hours from U.S. facilities and within 72 hours from EU facilities, which shows how speed has become a standard service expectation rather than a niche premium offering.[1]Clinigen, “Packaging and Labelling,” Clinigen Group, clinigengroup.com The UK also saw a 5% rise in first-in-human trial applications in 2025 compared with the prior year, suggesting a broader study base entering packaging workflows.

Rising Biologics and Injectable Drug Development

More than half of Phase I to Phase III clinical trials now focus on parenteral formulations, and that mix has been moving upward as biologics, biosimilars, and complex antibody programs take a larger share of development pipelines. The clinical trial packaging market benefits from that shift because injectable therapies need more control over extractables, leachables, moisture protection, and dose presentation than many oral drugs. VuRoyal highlighted the growing use of cyclic olefin polymer syringe formats for high-pH biologics, as these systems help avoid glass delamination and silicone-oil interaction issues. SCHOTT Pharma reported H1 2026 Drug Delivery Systems revenue of EUR 201.8 million (USD 228 million), supported by demand for prefillable glass syringes used in injectable biologics. Comparator management adds further complexity because placebo and active products often require custom masking and secondary packaging to appear identical during blinded biologic studies.

Expansion of Decentralized and Direct-To-Patient Trial Models

Decentralized elements were present in 43% of global studies before 2020, reached 55% by 2025, and are projected to rise to 66% within 5 years. This change matters for the clinical trial packaging market because site-dispensed formats are giving way to patient-ready assemblies that combine the drug product, instructions, administration components, tamper-evidence, and return materials in a single shipment. That need is evident in kits and packs, which are the fastest-growing product type, growing at a 9.73% CAGR from 2026 to 2031, and in the rising use of extended-content labels that fit multilingual instructions into limited pack space. The European Medicines Agency and the Heads of Medicines Agencies updated their recommendation paper in October 2025, formalizing expectations for the delivery of investigational medicinal products, the chain of custody, and data handling in decentralized settings. Sponsors also face uneven handling of personally identifiable information across IRT and RTSM platforms, which shifts more documentation work onto packaging and supply partners.

Increasing Outsourcing to Integrated Clinical Supply Partners

Small and mid-sized biotechs increasingly treat outsourcing as a permanent operating model because internal packaging lines rarely match the demands of multi-country trials, adaptive protocols, and temperature-sensitive products. Experic stated in 2025 that combining drug product manufacturing, quality control testing, clinical packaging, and distribution within a single network eliminates redundant audits and shortens time to clinic. VuRoyal also noted that traditional fill-finish queues can run from 4 to 8 months for early-phase programs, while integrated models with late-stage customization and just-in-time workflows can reduce first-patient dosing timelines to under 3 weeks. Cryoport Systems said it had supported 766 clinical trials and 21 approved therapies by 2025 through a model that links transportation, biostorage, GMP secondary packaging, and compliance services. In the clinical trial packaging market, that integrated model is widening the gap between full-service supply partners and smaller providers that compete mainly on local speed or single-step packaging work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Small-Batch Customized Packaging | -1.3% | Global, most acute for early-phase sponsors in North America and Europe | Short term (≤ 2 years) |

| Fragmented Country-Level Labeling and Import Rules | -0.9% | Global, with the highest friction in South America, the Middle East, Africa, and the Asia-Pacific | Medium term (2-4 years) |

| Dangerous Goods and Reverse-Logistics Constraints | -0.6% | Global, with an elevated impact in regions with limited IATA cargo infrastructure | Medium term (2-4 years) |

| EU Transport-Pack Compliance and Packaging Data Burden | -0.4% | Europe, with a secondary impact on sponsors running EU-anchored global trials | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Small-Batch Customized Packaging

Small-batch packaging campaigns incur fixed quality and release costs that do not scale with volume, making unit economics difficult for early-stage sponsors. Contract Pharma noted in April 2025 that regulations built around large commercial output create disproportionate burdens for small-batch operations, especially for companies that lack modular cleanrooms, robotic filling, or single-use systems. The challenge becomes sharper in advanced therapies because validation, stability packaging, and qualified person release can consume a large share of total campaign cost, even when only dozens of patients are being served. This pressure can delay study activation and also lead some sponsors to narrow the packaging scope, increasing the risk of protocol deviation later. The clinical trial packaging market, therefore, continues to grow, but providers without efficient small-batch systems face a tougher margin environment than headline demand numbers suggest.

Fragmented Country-Level Labeling and Import Rules

Sponsors running global studies must still navigate a patchwork of language rules, import licenses, approval timelines, and labeling conventions across many jurisdictions. The EU Clinical Trial Regulation amendment to Annex VI allows omission of expiry dates on immediate packaging under certain conditions, which eases one part of relabeling, but it does not remove the broader country-by-country burden. The European Medicines Agency and Heads of Medicines Agencies also stated in their decentralized trial recommendation paper that direct delivery of investigational medicinal products to trial participants may still face national restrictions and case-specific approvals, which often force separate workflows for site-dispensed and home-delivered arms of the same trial. In South America and parts of the Middle East and Africa, local import licensing often requires country-specific overprints that split inventory into smaller pools, thereby increasing waste. This issue weighs most heavily on early-phase, multi-country studies where packaging volumes are too low to spread setup costs efficiently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Injectables Lead While Convenience Kits Accelerate

Syringes held 26.34% of the clinical trial packaging market share in 2025, reflecting the strong presence of parenteral biologics and the wider use of prefilled formats that reduce dosing errors in both site-based and home-use settings. The clinical trials packaging market continues to rely heavily on syringe formats because they support ready-to-administer dosing, controlled presentation, and easier accountability in blinded studies. Vials and ampoules formed the second-largest product group, especially in lyophilized biologics, vaccines, and oncology studies, where reconstitution at the point of care remains standard. Blister packs also remained relevant for oral oncology and central nervous system programs because their unit-dose structure helps site teams manage tamper evidence and patient-level accountability.

Kits and packs are projected to record the fastest growth at a 9.73% CAGR from 2026 to 2031, indicating that the clinical trials packaging market is moving beyond individual primary containers toward complete study-ready assemblies. These formats combine the drug product, administration device, instructions for use, and return materials into a single patient-facing unit and often require validated transit performance for home delivery routes. VuRoyal stated that decentralized supply programs increasingly require ISTA 7D or equivalent testing for such shipments, which raises the technical value of secondary packaging design. Thermo Fisher Scientific said its clinical trials innovation lab in Center Valley, Pennsylvania has been developing smart packaging with real-time temperature and GPS monitoring for decentralized kit formats, which shows how providers are adding data capture into packaging workflows.

By Material Type: Polymer Dominance Challenged by Metal's Specialty Surge

Plastic held 41.58% share of the clinical trial packaging market size in 2025 because it offered low cost, design flexibility, and broad use across oral solids, liquids, and many secondary packaging formats. The clinical trials packaging industry still depends on glass for a large part of primary containment in biologics, particularly in vials and prefillable syringes, where extractables and leachables profiles are familiar to regulators and sponsors. Paper and corrugated fiber also played an important role in tertiary packaging and shippers, especially as sponsors pursue simpler mono-material approaches in procurement and logistics. This means material selection in the clinical trials packaging market is no longer based only on cost, because product integrity, handling risk, and trial design increasingly shape the final format.

Metal packaging is projected to grow at a 10.28% CAGR through 2031, driven by high containment requirements in high-potency oncology, antibody-drug conjugate, and selected gene therapy applications. The Alliance for RTU, formed by SCHOTT Pharma, Gerresheimer, and Stevanato Group in September 2024, has been promoting ready-to-use sterile glass containers that reduce contamination risk and simplify clinical fill-finish workflows. At the same time, cyclic olefin polymer and cyclic olefin copolymer syringe barrels are gaining attention for biologic candidates that are vulnerable to glass delamination, which is putting pressure on traditional material choices in the clinical trials packaging market. VuRoyal identified these polymer formats as a response to stability concerns in sensitive injectable programs.[2]VuRoyal, “Clinical Supply Packaging, Key Considerations and Best Practices for Clinical Trial Materials,” VuRoyal, vuroyal.com The result is a market where plastic still leads by volume, while metal and specialty polymers are gaining value in narrower but more demanding applications.

By End User: Research Laboratories Anchor Demand While CROs Gain Influence

Research laboratories accounted for 39.61% of demand in 2025, reflecting the large number of early-phase and translational studies that require primary containers, blinded kits, and sample storage packaging. That base kept research settings central to the clinical trial packaging market because protocol changes, exploratory dosing, and small lot sizes create frequent relabeling and repackaging work. Drug manufacturing companies ranked as the second-largest end-user group and relied on packaging as part of their investigational new drug campaign operations, especially when label runs changed with protocol revisions. As studies that entered the clinic in 2023 and 2024 moved into later phases, those manufacturers generated fresh demand for updated secondary packaging and comparator handling.

Clinical research organizations are projected to grow at a 10.05% CAGR from 2026 to 2031, which signals a shift in procurement influence within the clinical trials packaging market. Samsung Biologics expanded its service offering in June 2025 with the launch of Samsung Organoids for drug screening, demonstrating how CRO-related providers are broadening their roles across earlier and later stages of study support. Medpace states that its clinical packaging and supplies function combines qualified person release, IRT collaboration, and depot management, which illustrates how CROs are bundling packaging inside wider clinical supply platforms. For packaging suppliers, that changes the commercial path to market because multi-year platform relationships with CROs can be more durable than individual sponsor purchase orders. The clinical trials packaging industry is therefore seeing a gradual transfer of buying power from sponsors alone toward service intermediaries that control wider study execution.

Geography Analysis

North America held 38.56% of the clinical trial packaging market share in 2025, supported by a dense sponsor base, established cGMP clinical packaging capacity, and strong cold-chain infrastructure. The clinical trials packaging market in the region also benefited from clearer U.S. regulatory treatment of direct-to-patient investigational product dispensing, which widened the addressable use cases for home-delivery formats. Almac Group completed phase one of its Pennsylvania expansion in September 2025, adding 36,100 sq. ft. of warehouse space and ultra-low temperature storage for 76 freezers at -60°C to -80°C. PCI Pharma Services also announced investment commitments totaling above USD 1 billion in U.S. sterile fill-finish and drug-device capabilities, including a GMP-ready vial and lyophilization line in Bedford, New Hampshire, commissioned in May 2026.

Europe held the second-largest share of the clinical trials packaging market in 2025, with Germany, France, and the UK as the main centers for packaging, labeling, and blinding activities. The UK introduced reformed clinical trial regulations effective April 28, 2026, including a 14-day assessment route for Phase I studies, while the European Medicines Agency implemented ICH E6(R3) from July 23, 2025. EU GMP Annex 13 and the EU Clinical Trial Regulation continue to support demand for specialized labeling and blinding services because sponsors must limit mislabeling risk in blinded products. SCHOTT Pharma launched EVERIC lyo and amber vials in January 2026 for light-sensitive lyophilized antibody-drug conjugates, and the product was designed to meet light transmission requirements in the EU, the U.S., and Japan.

Asia-Pacific is projected to expand at a 10.54% CAGR through 2031 in the clinical trials packaging market, making it the fastest-growing regional cluster in the forecast period. Growth is being driven by China's larger domestic CDMO base, India's expanding CRO footprint, South Korea's role in biologic and antibody-drug conjugate manufacturing, and Japan's demand for self-injection and home-care packaging. TPC Marketing Research reported through Chem-Station that Japan's pharmaceutical container and packaging material market reached JPY 223.9 billion (USD 1.5 billion) in 2024 and was projected to reach JPY 227.65 billion (USD 1.53 billion) in 2025, with prefilled syringes and autoinjectors posting the strongest gains.[3]TPC Marketing Research, “Survey Results Announced on Pharmaceutical Container and Packaging Material Market,” Chem-Station, chem-station.com China is projected to account for more than 30% of global cell and gene therapy clinical trials, which is lifting demand for local cryogenic packaging and validated cold-chain kit assembly. Samsung Biologics used Bio Japan 2025 to deepen partnerships with Japanese pharmaceutical companies, which points to tighter links between Asia-Pacific manufacturing and global clinical supply chains. South America and the Middle East and Africa remained the smallest regional pool, with Brazil and South Africa acting as the main trial locations while import-license friction and weaker cold-chain infrastructure limited broader scale.

Competitive Landscape

The clinical trials packaging market is moderately consolidated among integrated clinical supply providers, but it remains fragmented across primary container manufacturers and regional packaging specialists. No single company holds more than a mid-teens share, which means scale matters, yet breadth of service matters even more. The strongest positions belong to suppliers that can combine primary packaging, GMP secondary packaging, labeling, cold-chain logistics, and qualified person oversight within a single quality system. That model raises entry barriers because it needs capital, validated infrastructure, and deep regulatory discipline. As a result, the clinical trials packaging market is separating into a smaller group of full-platform providers and a wider field of niche container and regional service companies.

Almac Group reported revenue growth of 7% to GBP 1.1 billion (USD 1.41 billion) for the year ending September 2025, with pre-tax profit up 16%, supported by continued investment in clinical packaging, cold-chain infrastructure, and analytical services. PCI Pharma Services reinforced the capacity-led strategy through investment commitments above USD 1 billion in U.S. sterile fill-finish and drug-device combination capacity. Thermo Fisher Scientific has followed a platform-led route through its clinical trials innovation lab and its broader pharma services network, where smart packaging, digital connectivity, and integrated assembly are being developed with sponsors. The collaboration between Thermo Fisher Scientific and SHL Medical in March 2026 also showed how end-to-end drug-device assembly, packaging, and distribution are becoming a competitive differentiator. In the clinical trialspackaging market, these moves are making long-duration contracts more likely for providers that can offer both physical capacity and digital process control.

Open opportunities remain strongest in late-stage customization for faster-growing Asia-Pacific programs, in blinding and masking for comparator-heavy cell and gene therapy studies, and in more sustainable clinical packaging formats. Amcor achieved ISO 13485:2016 certification at its Winterbourne, UK site in March 2026, which strengthened its position in medical-grade packaging opportunities that require formal quality assurance.[4]Amcor, “Amcor Winterbourne Achieves ISO 13485:2016 Certification, Strengthening Its Commitment to Healthcare Packaging,” Amcor, amcor.com The Alliance for RTU, backed by SCHOTT Pharma, Gerresheimer, and Stevanato Group, also points to a gradual technical shift toward ready-to-use nest-and-tub formats in fill-finish and downstream packaging. Emerging disruption is likely to come from CDMO-CRO hybrids that place packaging inside broader study execution workflows and reduce the handoffs that often create accountability gaps in traditional models. That keeps the clinical trials packaging market competitive, but not dominated by a single structural winner.

Clinical Trial Packaging Industry Leaders

Almac Group Limited

Sharp Services, LLC

Gerresheimer AG

Amcor plc

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Parexel published a white paper on ICH E6 (R3) operationalization, highlighting that at least half of critical trial data may be captured outside EDC and underlining the traceability requirements that affect clinical packaging serialization and accountability documentation.

- April 2026: MM Group published guidance on Clinical Trial Technology, including PS 9000:2011-accredited cold-chain label solutions and just-in-time models for decentralized trial kits, reflecting growing European demand for integrated packaging and labeling under a single GMP-certified partner.

- March 2026: Almac Group reported phase one completion of its USD 93.5 million Pennsylvania campus expansion, adding 79,000 sq. ft. of warehouse, ULT storage, and distribution space, with phase two targeted for 2026.

- December 2025: SCHOTT Pharma, Gerresheimer, and Stevanato Group launched the "Alliance for RTU," an open industry expert platform to accelerate the adoption of ready-to-use vials and cartridges, targeting pharmaceutical companies, CMOs, and CDMOs transitioning from conventional bulk packaging to RTU configurations compliant with EU GMP Annex 1.

Global Clinical Trial Packaging Market Report Scope

The scope of the report covers the clinical trials packaging market, including packaging solutions specifically designed for clinical trial materials. These materials include investigational drugs, placebos, and comparator drugs, among others, ensuring their safety, stability, and compliance with regulatory standards throughout the clinical trial process.

The Clinical TrialsPackaging Report is Segmented by Product Type (Vials and Ampoules, Syringes, Blister Packs, Bottles, Bags and Pouches, Tubes, Sachets, and More), Material Type (Plastic, Glass, Metal, and Paper and Corrugated Fiber), End User (Research Laboratories, Clinical Research Organizations, and Drug Manufacturers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Vials and Ampoules |

| Syringes |

| Blister Packs |

| Bottles |

| Bags and Pouches |

| Tubes |

| Sachets |

| Other Product Types |

| Plastic |

| Glass |

| Metal |

| Paper and Corrugated Fiber |

| Research Laboratories |

| Clinical Research Organizations |

| Drug Manufacturing Companies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Vials and Ampoules | ||

| Syringes | |||

| Blister Packs | |||

| Bottles | |||

| Bags and Pouches | |||

| Tubes | |||

| Sachets | |||

| Other Product Types | |||

| By Material Type | Plastic | ||

| Glass | |||

| Metal | |||

| Paper and Corrugated Fiber | |||

| By End User | Research Laboratories | ||

| Clinical Research Organizations | |||

| Drug Manufacturing Companies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the clinical trial packaging market?

The clinical trial packaging market reached USD 4.08 billion in 2025, stands at USD 4.44 billion in 2026, and is projected to reach USD 6.83 billion by 2031 at a 9.01% CAGR.

Which product type leads clinical trials packaging demand?

Syringes led the market with a 26.34% share in 2025, supported by the large number of biologic and injectable studies moving through clinical pipelines.

Which material category is growing the fastest?

Metal packaging is projected to record the fastest growth at 10.28% CAGR through 2031, mainly in high-containment and advanced therapy applications.

Why are decentralized trials changing packaging requirements?

Home-delivery studies need patient-ready kits with instructions, administration supplies, tamper evidence, and return packaging, which adds more work than site-dispensed formats.

Which region is leading, and which one is growing fastest?

North America held the largest share at 38.56% in 2025, while Asia-Pacific is expected to post the fastest growth at a 10.54% CAGR through 2031.

Why are CROs becoming more important in this space?

CROs are projected to grow at a 10.05% CAGR because sponsors increasingly outsource packaging, labeling, depot management, and supply oversight to integrated service partners.

Page last updated on: