Pharmaceutical Blister Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

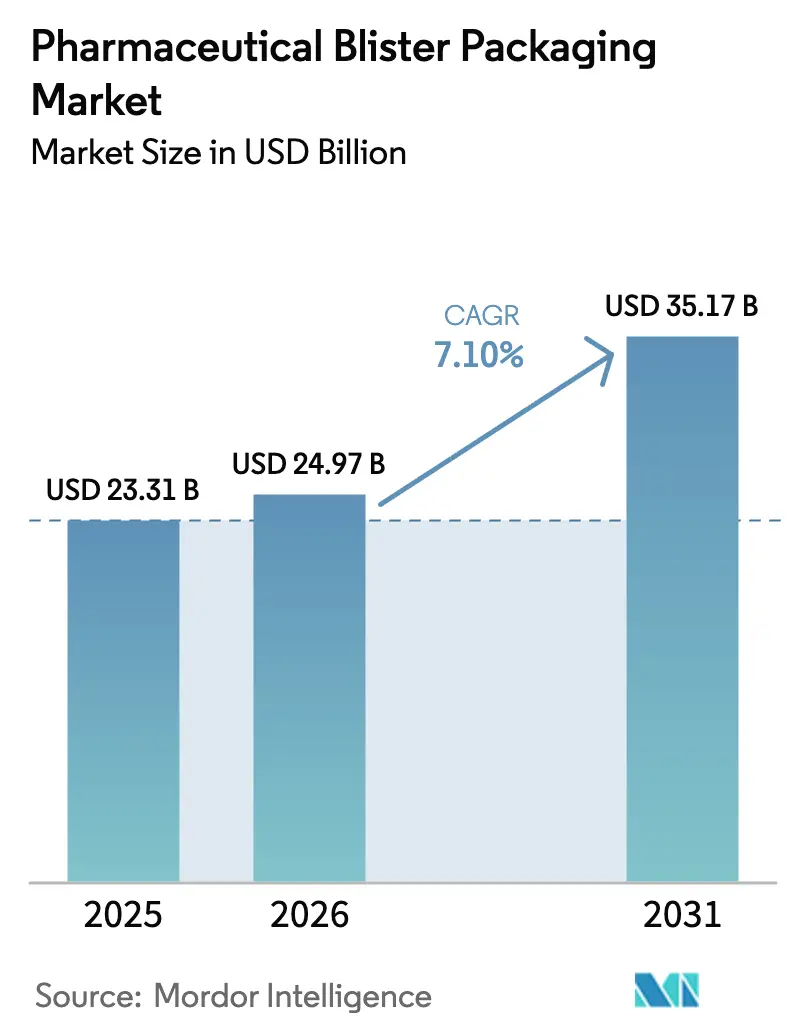

| Market Size (2026) | USD 24.97 Billion |

| Market Size (2031) | USD 35.17 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Blister Packaging Market Analysis by Mordor Intelligence

Pharmaceutical blister packaging market size in 2026 is estimated at USD 24.97 billion, growing from 2025 value of USD 23.31 billion with 2031 projections showing USD 35.17 billion, growing at 7.10% CAGR over 2026-2031. Demand is rising because solid-dose drugs remain the dominant oral therapy, regulators favor unit-dose formats for accuracy, and smart sensors now fit seamlessly into standard blisters. Firms are also working around aluminum price swings by qualifying recyclable high-barrier plastics and by reshoring foil supply. Asia-Pacific is the largest production hub and accounts for more than one-third of global output thanks to competitive labor costs and strong local demand; growth momentum there is reinforced by state incentives for continuous-manufacturing lines and expanding CDMO capacity. Capacity additions in the United States and the European Union signal that global players want network resilience as well as proximity to high-value biologics pipelines. Digital adherence packs launched by Aardex Group and sensor-ready closures from Gerresheimer show how packaging is now part of connected-health strategies, which opens new revenue streams for data analytics services.

Key Report Takeaways

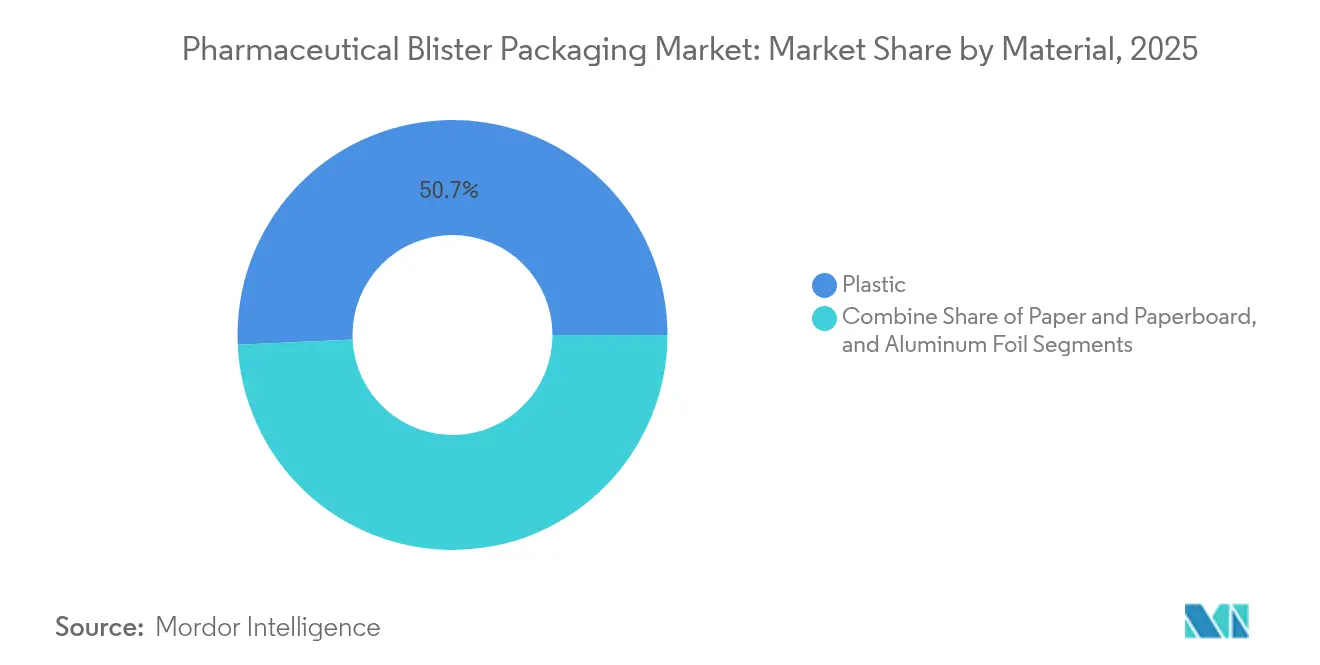

- By material, plastic films led with 50.72% revenue share in 2025, while paper and paperboard are expanding at a 9.12% CAGR through 2031.

- By technology, thermoforming accounted for 72.45% of the pharmaceutical blister packaging market share in 2025; cold-form solutions post the fastest 10.63% CAGR.

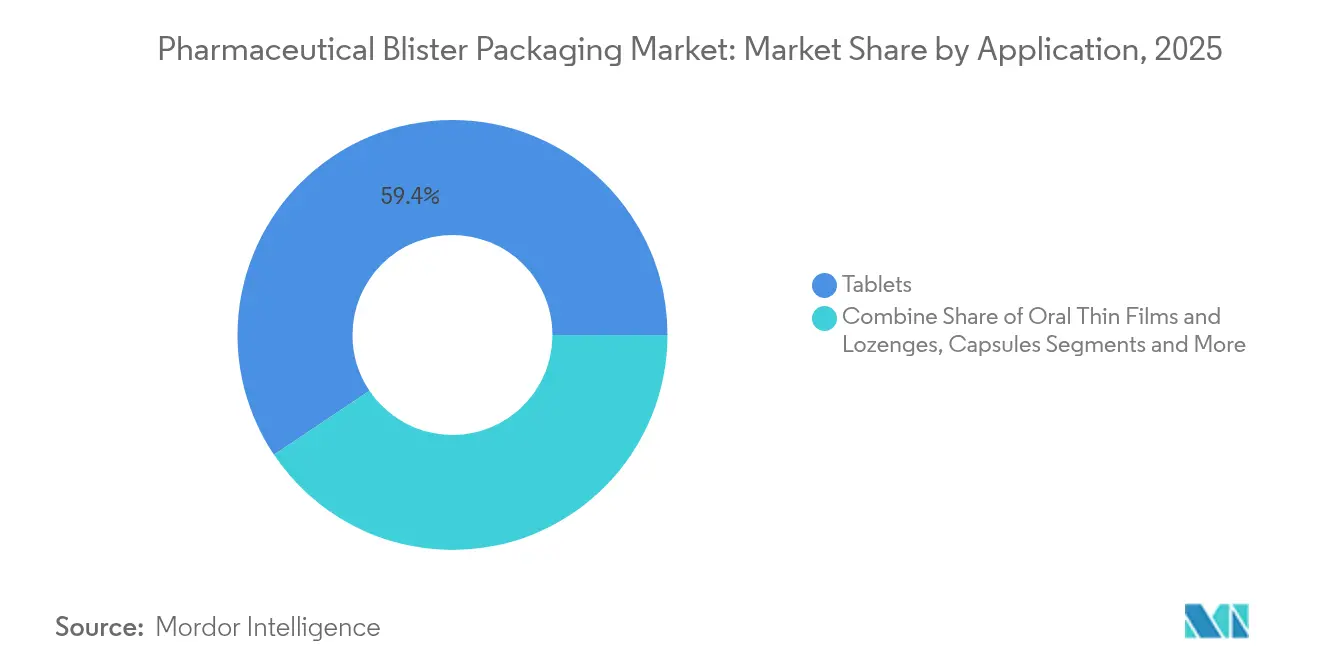

- By application, tablets dominated with 59.41% share in 2025; oral thin films and lozenges advance at an 10.79% CAGR.

- By end-user, conventional pharma manufacturers held 64.38% share, whereas CDMOs record a 9.05% CAGR through 2031.

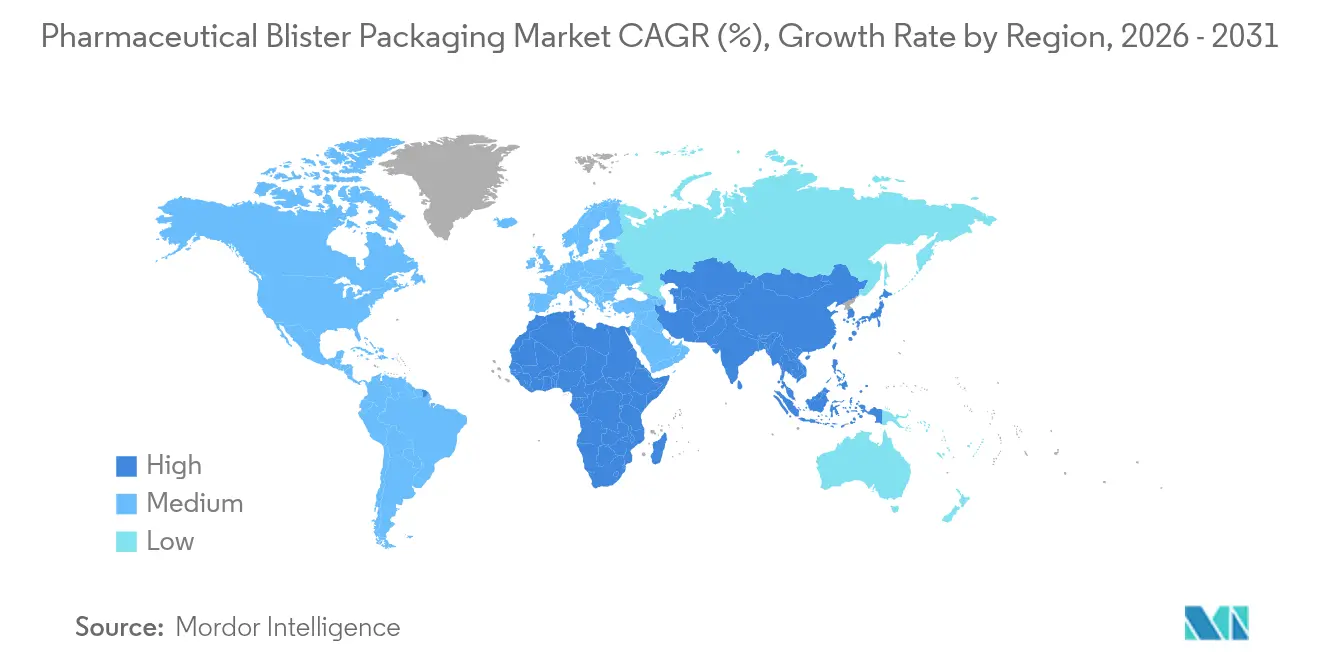

- By geography, Asia-Pacific commanded 33.97% of global revenue in 2025 and remains the fastest-growing region with a 8.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Blister Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in demand for unit-dose adherence packs | +1.2% | North America, EU, expanding globally | Medium term (2-4 years) |

| Growing adoption of recyclable high-barrier plastics | +0.8% | EU leading, uptake in North America and Asia-Pacific | Long term (≥ 4 years) |

| Expansion of chronic-disease oral therapies | +1.5% | Global, highest therapy growth in Asia-Pacific | Long term (≥ 4 years) |

| Aging population boosting OTC solid-dose demand | +1.1% | North America and EU core, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Emergence of smart, sensor-enabled blister packs | +0.9% | Early adoption in North America and EU | Medium term (2-4 years) |

| Continuous-manufacturing lines with inline blistering | +0.6% | Global pharma hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in demand for unit-dose adherence packs

Regulators see unit-dose formats as an effective way to lower dosing errors, so proposed FDA rules would require over-the-counter orally disintegrating tablets and films to ship only in single-unit packaging. Hospital and retail pharmacists confirm that visual dose cues reduce skipped administrations among seniors. Payers also welcome lower readmission risk, which anchors reimbursement incentives. Contract packers respond by adding multi-product blister lines that let one card hold an entire daily regimen. The effect is quickest in North America, but Europe follows as e-prescription platforms integrate adherence data.

Growing adoption of recyclable high-barrier plastics

The EU Packaging and Packaging Waste Regulation mandates that all healthcare packs placed on the market after 2030 must be designed for recycling. Suppliers such as TekniPlex now commercialize mid-barrier blister films containing 30% post-consumer resin without sacrificing moisture protection. Borealis’ Bornewables grades, produced from renewable feedstock, give origin-controlled polymer options to manufacturers seeking carbon-footprint cuts. Japanese converters add closed-loop systems that collect foil scrap and re-smelt it into pellets, cutting CO₂ emissions nearly 20% versus virgin routes.

Expansion of chronic-disease oral therapies worldwide

Rising incidence of diabetes, cardiovascular disease, and central-nervous-system disorders keeps oral solids in high demand. Formulators use Quality-by-Design tools to engineer controlled-release tablets that improve therapeutic windows. [1]MDPI, “Advances in Oral Solid Drug Delivery Systems,” mdpi.com Combination-therapy films that dissolve on the tongue shorten time to effect and bypass swallow challenges, which heightens the need for moisture-tight packs able to preserve volatile actives. Roquette’s multipart ODT platform extends shelf life while ensuring fast breakup, reinforcing the market’s pivot to patient-centric formats.

Aging population boosting OTC solid-dose demand

About one in six US residents is already above 65 years, and similar ratios appear in Germany, Italy, and Japan. This demographic shift increases self-medication with vitamins, pain relievers, and antacids. Push-through blisters offer tamper evidence plus a moisture barrier prized for hygroscopic actives. Brand owners like Berry Global now supply clarified-polypropylene jars for large counts, but they still rely on blister cards for travel packs that remind users to take daily doses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans or taxes on single-use plastics | -0.7% | EU leading, expanding worldwide | Short term (≤ 2 years) |

| Volatility in aluminum and polymer feed-stock prices | -1.0% | Global, most acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Heightened scrutiny on novel-film extractables | -0.5% | North America and EU | Medium term (2-4 years) |

| Geopolitical disruption of aluminum-foil supply | -0.8% | Regions dependent on imported foil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in aluminum and polymer feed-stock prices

Aluminum foil is the classic blister barrier but faces price spikes linked to geopolitical tariffs and Chinese export policy shifts. Europe’s foil mills reported almost 724 thousand tonnes of nine-month output in 2024, yet supply still tightened after energy-price shocks. [2]European Aluminium Foil Association, “European Foil Rollers Maintain Production,” alufoil.org Resin makers also pass higher naphtha costs into PVC and PET grades. Brand owners diversify sourcing toward Southeast Asia and Latin America and test polypropylene-based laminates that cut foil gauge without hurting barrier performance.

Heightened scrutiny on novel-film extractables and leachables

The FDA and EMA now expect full toxicological risk assessments for any new polymer in direct drug contact. USP is drafting fresh chapters that spell out reference standards and analytical protocols United States Pharmacopeia. [3]United States Pharmacopeia, “Extractables and Leachables,” usp.org Contract labs such as Intertek report growing demand for ICP-MS and UPLC-HRMS screening of small molecules that can migrate at parts-per-billion levels Intertek. The cost and time for such studies slow material changeovers, especially for startups bringing niche dosage forms to market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material – sustainability drives diversification

supported by mature PVC-PVDC supply chains and proven thermoforming behavior. The pharmaceutical blister packaging market size for plastics aligns with high-volume generic production that values low forming temperatures and predictable seal integrity. Yet paper-based structures are gaining momentum because brand owners want curbside recyclability and lower Scope 3 emissions. Paperboard laminates coated with thin polymer or aluminum layers now approach nine-month shelf-life performance, expanding their use beyond vitamins into prescription gastroenterology drugs.

Demand for aluminum-plastic cold-form foil remains solid because deep-draw cavities shield moisture-sensitive compounds. However, foil gauges are trending lower as converters add nanolayer coatings that deliver equal barrier with less metal. Cold-seal cards from Ecobliss illustrate how pressure-activated adhesive eliminates heat while cutting energy consumption in pack rooms. TekniPlex’s 30% PCR blister films demonstrate the direction of resin circularity and keep clarity that pharmacists prefer for visual inspection.

By Technology – cold-form innovation accelerates

Thermoforming owned 72.45% of the pharmaceutical blister packaging market share in 2025 because it offers high line speeds and clear cavities that support visual confirmation. Form-fill-seal lines routinely cross 600 packs per minute, matching blockbuster tablet volumes. Even so, moisture-sensitive APIs push manufacturers toward cold-forming where aluminum foil delivers near-zero water vapor transmission rates. The pharmaceutical blister packaging market size for cold-form lines grows as specialty generics and orphan-drug volumes climb, despite higher material costs.

Cold-form equipment vendors now integrate servo-driven indexers that improve foil usage, trimming scrap by up to 15%. Aptar CSP Technologies expanded its Active Blister production into Europe to meet regional demand for built-in desiccant channels that prevent hydrolysis without extra sachets. Continuous-manufacturing advocates link powder-to-pack trains where tablets exit compression, pass through weight checks, and reach blister sealing within minutes, minimizing hold-time validation.

By Application – oral thin films reshape format mix

Tablets accounted for 59.41% of the pharmaceutical blister packaging market in 2025 as patients and prescribers still favor familiar swallow pills for chronic therapy. Capsules offer taste-masking and multipart filling flexibility, yet they trail tablets in volume. Oral thin films and medicated lozenges now record the swiftest 10.79% CAGR because they dissolve without water and simplify pediatric or geriatric dosing. ZIM Labs’ Thinoral platform loads poorly soluble molecules onto fast-disintegrating polymer matrices, which requires high-barrier packs to guard humidity.

Film strips sit in narrow, perforated cavities to prevent curl and mechanical damage. Developers also explore push-pocket designs that allow one-hand dispensing, improving adherence for Parkinson’s patients. Diagnostic kits packaged in blisters emerge as adjacent growth because home-testing swabs use the same thermoforming lines, offering CDMOs an additional revenue stream during off-peak pharma cycles.

By End-User – CDMOs capture outsourcing wave

Originator and generic drug companies consumed 64.38% of blister volumes in 2025 since most run legacy packaging centers close to tablet presses. Yet the pharmaceutical blister packaging industry sees the strongest 9.05% CAGR among CDMOs as innovators prioritize core R&D and outsource variable-demand packaging. PCI Pharma Services invests USD 365 million in US and EU campuses that house high-speed blistering and sterile fill-finish suites. Jabil’s acquisition of Pharmaceutics International gives it 70+ classified rooms able to blister solid doses and insert smart components.

Contract packers without drug-product manufacturing also gain traction. They specialise in late-stage customization, printing regional languages and affixing serialized codes just before market release, which reduces inventory obsolescence for multinational brands.

Geography Analysis

Asia-Pacific led with 33.97% of global revenue in 2025 and shows a 8.87% CAGR through 2031. Governments in India, China, and Singapore offer tax credits for automated packaging lines, while local CDMOs win supply contracts for Europe’s generics. Japanese suppliers spotlight transparent barrier films and AI inspection at Interphex Tokyo, revealing how digital tools shrink defect rates. Regional harmonization with PIC/S GMP accelerates cross-border distribution, so multinationals can validate a single pack across several ASEAN markets.

North America ranks second due to high-value biologic pipelines and the early rollout of smart adherence packs. The United States also benefits from reshoring moves that shorten supply chains and hedge geopolitical risk. Aluminum tariff reinstatements push converters to secure domestic foil rolling capacity or switch to polymer-based lidding, limiting exposure to import price swings. Canadian facilities integrate renewable electricity, enabling carbon-neutral pack claims that resonate with public payers. Europe maintains significant share thanks to strict quality norms and investment in sustainable materials. TekniPlex’s new Modena plant adds mid-barrier PCR film, while Faller Packaging expands folding-carton space in Germany to handle leaflet demand. The region’s circular-economy directives drive trials of mono-material blisters that qualify for blue-bin collection schemes. Eastern European contract packers provide cost relief for small and mid-sized innovators seeking EU Qualified Person release.

Mordor Intelligence provides coverage of the pharmaceutical blister packaging market across other key regional markets, including Asia, Europe, North America, Latin America, and Middle East and Africa, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Pharmaceutical blister packaging sits under pharmaceutical GMP and labeling controls, alongside packaging-specific requirements for safety features and standards. In the European Union, Regulation (EU) 2016/161 on safety features for medicinal products shapes pack design and production through unique identifiers and anti-tampering features, which raises the operational focus on controlled artwork, coding, and line verification for blister cards and lidding. EMA guidance for centrally authorized medicinal products also formalizes the review of packaging mock-ups and specimens, including submission of the smallest pack-size layouts and multilingual labeling and package leaflet elements as part of marketing authorization workflows.

Quality management and material compliance further tighten across primary packaging supply chains through international standards. ISO 15378:2017/Amd 1:2024, effective 12-Feb-2026, updates the GMP-based quality management standard for primary packaging materials by incorporating climate action considerations, lifting the compliance bar for converters and material suppliers supporting blister formats. Broader container-closure standards such as ISO 15747:2026 (published 12-May-2026), while focused on plastic containers for parenterals, reinforce the wider regulatory direction toward more structured physical, chemical, and biological verification for polymer systems in direct drug contact and adjacent packaging applications.

Competitive Landscape

The pharmaceutical blister packaging market features a moderate level of fragmentation, with a long tail of regional converters operating beside diversified multinationals. Uhlmann, Marchesini, and Körber supply turnkey lines, yet local integrators customize end-of-line coding and aggregation. Patent filings cover child-resistant one-piece packs that eliminate secondary cartons and integrate authentication microtext.

Mergers and acquisitions expand scale and technology portfolios. Jabil moved into healthcare by buying Pharmaceutics International, while Blue Wolf Capital stitched together three facilities to form a mid-tier CDMO. Sustainability remains a differentiator; Aptar’s N-Sorb absorber targets nitrosamine prevention, earning a place in the FDA Emerging Technology Program and enhancing the firm’s credibility with oncology drug sponsors.

Digital convergence spurs collaboration between packaging converters and software firms. Aardex licenses cloud dashboards to blister suppliers so hospitals can track adherence without adding hardware. BD embeds RFID tags in prefillable syringes, signaling similar connectivity will migrate to oral-dose packs. As connected formats scale, data-privacy compliance and cybersecurity become new competitive dimensions.

Pharmaceutical Blister Packaging Industry Leaders

Constantia Flexibles

Huhtamäki Oyj

Amcor PLC

Sonoco Products Company

Smurfit Westrock

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sustainability-led redesign creates a visible whitespace in blister structures where converters can offer recycle-ready formats without compromising barrier performance or line speed. The EU Packaging and Packaging Waste Regulation (EU) 2025/40 sets recycled-content direction through 2030, while maintaining an exemption timeline for primary pharmaceutical packaging until Jan 1, 2035. That window supports near-term work on qualified mono-material or PVC-free blister alternatives that still meet GMP and stability needs, aligning with supplier activity already underway, including TekniPlex commercializing blister films with 30% post-consumer resin alongside European capacity investments. For brand owners and CDMOs, this creates practical pathways to test circular materials within validated blister platforms.

Capacity localization and automation at contract partners are also widening addressable demand for blistering services, especially for multi-SKU, late-stage customization, and adherence-oriented formats. Aenova’s new blister packaging line commissioning at Bad Aibling, Germany, under a EUR 20 million program reflects the capital shift toward flexible packaging campuses that can support serialized, multilingual, and short-run requirements. On materials and converting, Amcor opening a USD 35 million healthcare packaging coating facility in Subang Jaya, Malaysia, and announcing expansion investment in Sira, Karnataka, India, further anchors Asia-Pacific as a manufacturing and innovation hub for high-performance films and coatings feeding blister applications, while improving resilience for global pharmaceutical networks.

Recent Industry Developments

- June 2026: Constantia Flexibles published results from a real-life sorting test in which used REGULA CIRC PVC-free cold-forming blister packs were detected and sorted as rigid non-ferrous aluminum at a 100% rate. The outcome supports recycling-compatibility claims for PVC-free cold-form designs and helps brand owners defend material-change decisions under tightening packaging sustainability requirements.

- April 2025: Amcor completed its all-stock combination with Berry Global, expanding its scale across consumer and healthcare packaging. The deal strengthens Amcor's global footprint and can accelerate investment in high-barrier materials, coating capacity, and patient-centric formats used in pharmaceutical blister packaging supply chains.

- October 2024: Aptar CSP Technologies began European output of Active Blister moisture-control packs. Regional manufacturing of desiccant-integrated blister solutions shortens qualification lead times for European pharmaceutical customers and supports stability-sensitive oral solids without adding secondary components like sachets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers blister packs used to package pharmaceutical products, measured in value terms, and includes the main blister materials and the common forming technologies used to make those packs.

Scope exclusions: We exclude non-blister pharmaceutical packaging formats (such as bottles, sachets, and vials) and secondary packaging items unless they are integral to the blister pack itself.

Segmentation Overview

- By Material

- Plastic

- Aluminum Foil

- Paper and Paperboard

- By Technology

- Thermoforming

- Cold-form

- Heat-seal / Heat-shrink

- By Application

- Tablets

- Capsules

- Oral Thin Films and Lozenges

- Diagnostic Kits and Others

- By End-User

- Branded / Generic Pharma Manufacturers

- Contract Development and Manufacturing Organizations (CDMOs)

- Contract Packaging Organizations (CPOs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the initial demand map, and collect anchor indicators that move blister demand up or down. We leaned on public packaging and pharma production signals, then cross-checked them with policy and safety documentation that influences material choices and pack formats.

Sources included non-paywalled and official references such as U.S. FDA guidance and recalls, EMA public information, UN Comtrade trade statistics, OECD industrial indicators, and peer reviewed packaging and materials journals, along with annual reports, investor presentations, and reputable press coverage from major pack and material suppliers. For added consistency checks, we also used paid subscriptions focused on company financials and intelligence, patent databases, and shipment-level import and export records where available. These are illustrative examples, and many other public sources were also reviewed to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on structured interviews and surveys with packaging converters, material suppliers, pharma manufacturing and packaging teams, and channel experts who track pack-format shifts. We used these conversations to confirm pack-mix by therapy type, validate regional demand patterns, and pressure-test assumptions like material substitution and average pricing (especially for cold-form versus thermoformed packs).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 37% | EMEA: 32% |

| Smaller Players: 18% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where pharma manufacturing output and pack-format penetration are used to reconstruct the value pool for blister packs, which is then converted into dollars using regionally relevant price points. Once that total was formed, we corroborated it with selective bottom-up approximations, such as sampled converter revenue splits, channel checks on pack consumption, and a limited ASP times volume sanity check for key material and process combinations.

Key inputs we tracked included the mix between thermoforming and cold forming, typical material structure choices (for example PVC based structures versus higher barrier aluminum formats), regional pharma production and export intensity, serialization and tamper evidence adoption pressure, and observed material cost movements that influence conversion pricing. Forecasts were built using scenario analysis with a simple driver stack, where assumptions on pharma output growth, generic volumes, and pack-format shifts were reviewed with interviewees before finalizing the trajectory. Where direct bottom-up detail was missing for smaller countries, we filled gaps using proxy indicators like pharma output share and trade intensity, and then normalized results back to interview grounded pricing ranges.

Data Validation & Update Cycle

Validation is done in multiple passes so the final numbers remain explainable and consistent with real market signals. We compare outputs against independent indicators like packaging material trade flows, reported capacity additions, and directional movement in pharma production, and then we re-check any large variances by revisiting assumptions and re-contacting sources when needed.

Before sign-off, the model and narrative go through analyst reviews that look for unit errors, currency timing issues, and unusual year-over-year jumps by region or technology. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory shifts, large capacity changes, or sudden raw-material price moves. Right before delivery, a final pass is performed so clients receive the most current view available at that time.

Mordor Intelligence's Pharmaceutical Blister Packaging Market Size Measured Against Other Published Estimates

Published market values for pharmaceutical blister packaging can differ even when the topic name looks identical, because the scope and the unit of measure are not always handled the same way. In practice, differences usually come from whether adjacent healthcare blister uses are blended in, what years are treated as the current baseline, and how pricing is carried forward over the forecast window.

The main gap comes from whether the estimate stays strictly within pharmaceutical blister packs by material and forming process, or whether it also folds in broader healthcare blister packaging and related formats, and Mordor Intelligence keeps the count tied to pharma-specific blister materials and cold-form or thermoform processes only. A second driver is the timing of price assumptions, since some publications apply a single global price curve, while others adjust ASPs by region and by process based on conversion mix and material pass-through.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.97 B (2026) | |

| Trade Journal A | USD 23.90 B (2025) | Uses a different base year and may blend end uses beyond pharmaceuticals, which can pull the starting value down even if the long-term growth rate is similar. |

| Industry Report B | USD 21.12 B (2024) | Covers healthcare blister packaging at large, so the included demand pool is wider, and the year and scope mismatch makes direct comparison to a pharma-only blister definition uneven. |

The table shows that most of the spread is explained by scope alignment and year selection, followed by how pricing is carried forward by region and process. When the included pack formats, geography coverage, and ASP logic are made explicit, the market total becomes easier to trace back to observable demand drivers and to repeat over time.

Key Questions Answered in the Report

What is the current value of the pharmaceutical blister packaging market?

The pharmaceutical blister packaging market size reached USD 24.97 billion in 2026 and is projected to hit USD 35.17 billion by 2031.

Which material holds the largest share in blister packaging?

Plastic films, mainly PVC-based structures, commanded 50.72% revenue share in 2025.

Why are oral thin films gaining popularity?

They dissolve quickly without water, improve patient compliance, and post the fastest 10.79% CAGR, prompting specialized high-barrier blister designs.

How are sustainability regulations affecting packaging choices?

EU rules require all packs sold after 2030 to be recyclable, so converters now use PCR plastics and ultra-thin barrier coatings to meet future compliance.

What role do CDMOs play in this market?

CDMOs show a 9.05% CAGR because pharmaceutical firms outsource packaging to access advanced blister lines and serialization without large capital expenditure.

How are smart blister packs changing patient care?

Sensor-enabled packs record each dose removal and transmit data to care teams, which can improve adherence and support value-based reimbursement models.

Page last updated on: