Market Overview

| Study Period | 2020 - 2031 |

|---|---|

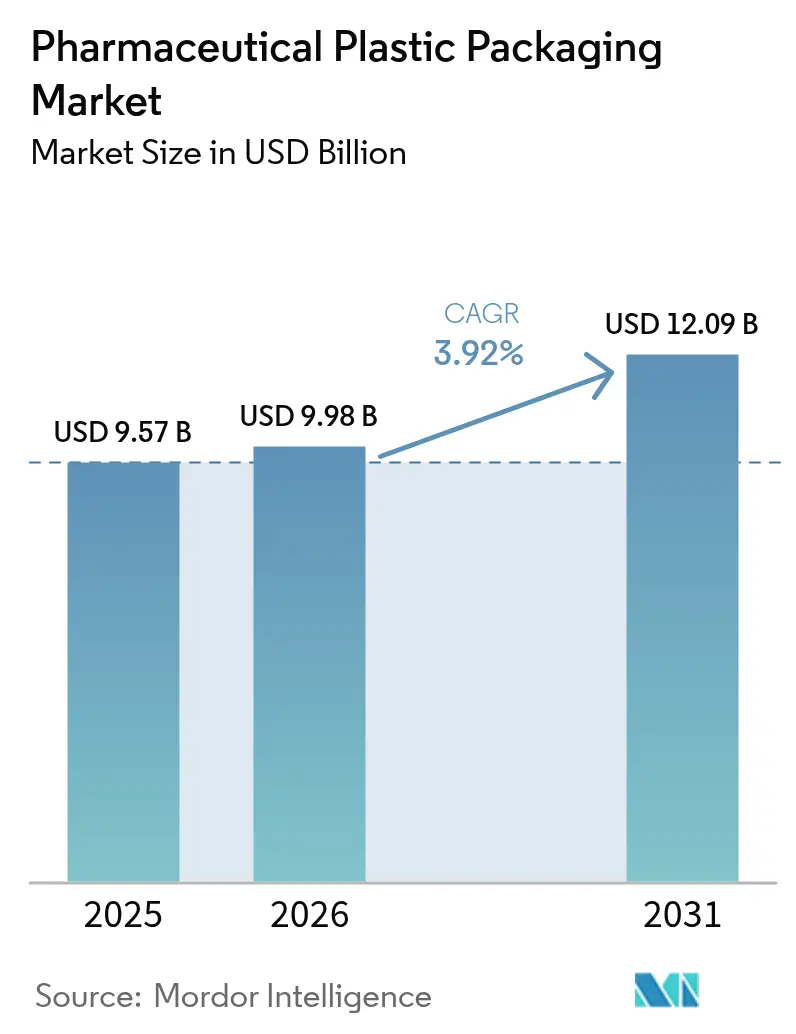

| Market Size (2026) | USD 9.98 Billion |

| Market Size (2031) | USD 12.09 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

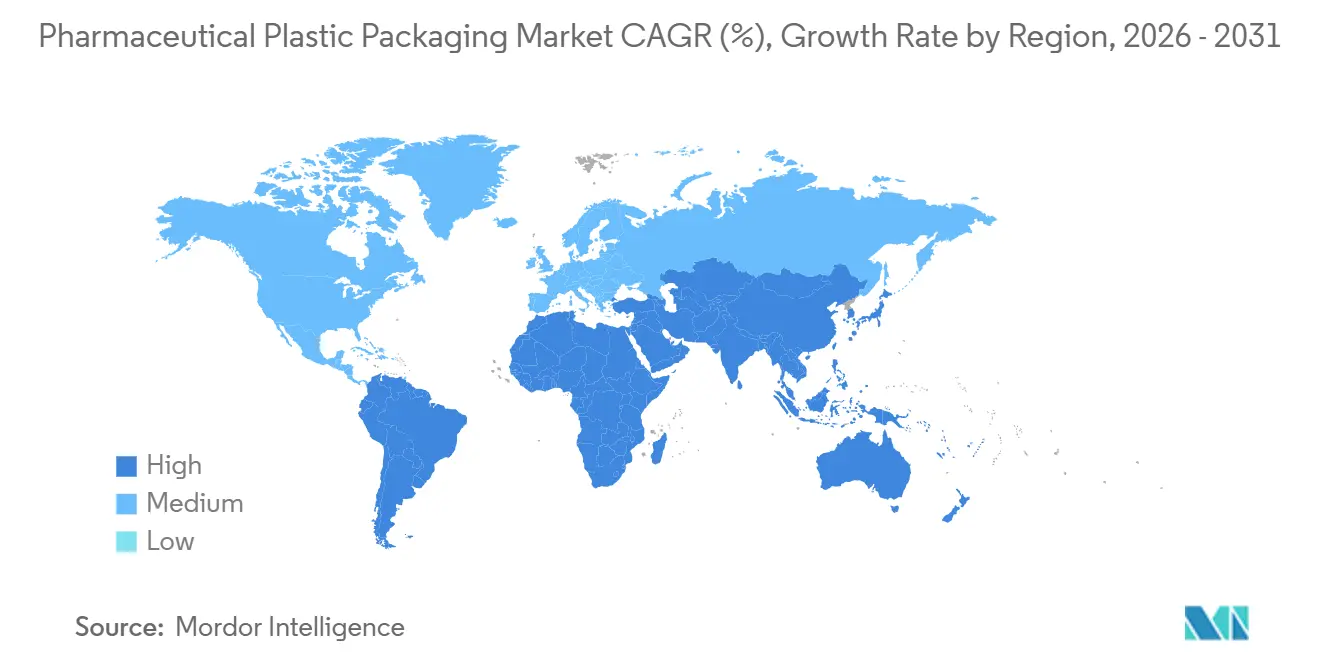

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Plastic Packaging Market Analysis by Mordor Intelligence

The pharmaceutical plastic packaging market size is projected to expand from USD 9.57 billion in 2025 and USD 9.98 billion in 2026 to USD 12.09 billion by 2031, registering a 3.92% CAGR between 2026 to 2031. Sustained uptake of biologics and specialty injectables, tightening circular-economy regulations, and the proliferation of home-health therapies continue to shape competitive priorities. Larger buyers increasingly demand tamper-evident, traceable, and recyclable packs that safeguard complex drug chemistries without compromising speed to market. Suppliers are responding by integrating blow-fill-seal, multilayer barrier films, and AI-enabled inline inspection, moves that shorten qualification cycles and reduce scrap. Interlinked regulatory and sustainability mandates are steering investments toward certified recycled resin and bio-based feedstock, while e-commerce distribution keeps fueling lightweight, unit-dose format adoption.

Key Report Takeaways

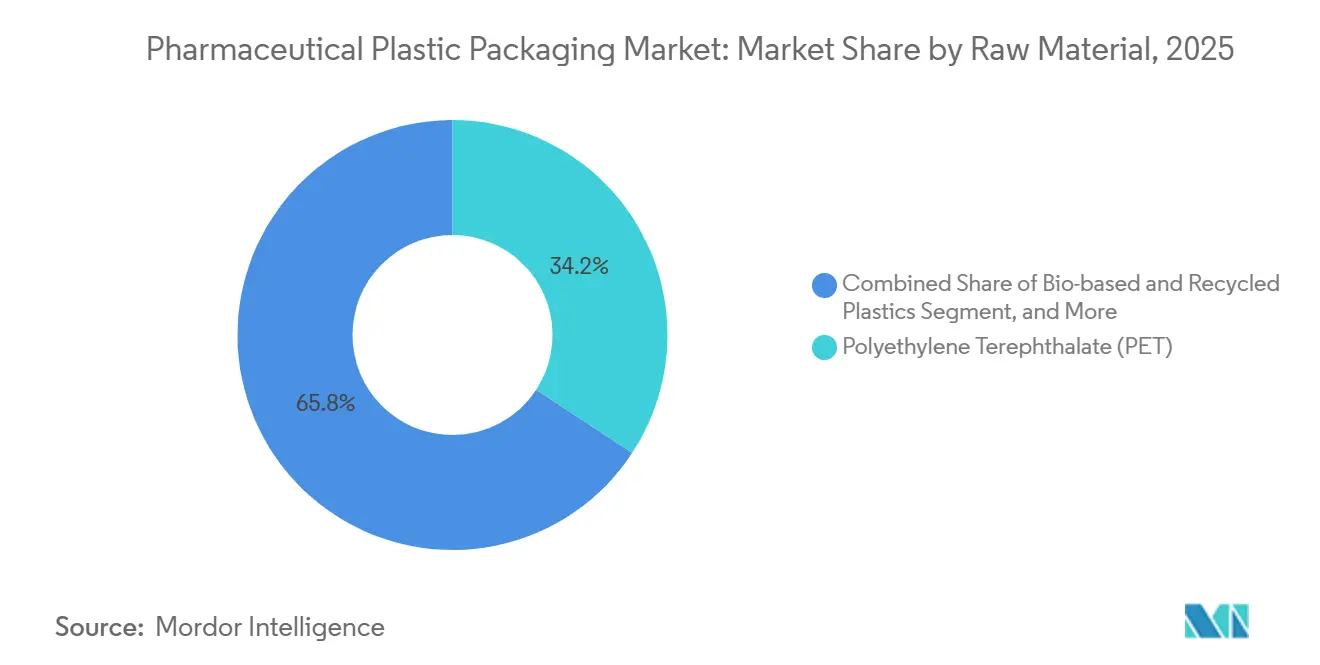

- By raw material, Polyethylene terephthalate captured 34.23% of pharmaceutical plastic packaging market share in 2025, and high-density polyethylene is set to advance at a 5.09% CAGR through 2031.

- By product type, Vials and ampoules delivered 17.32% revenue share in 2025, whereas prefillable syringes and cartridges are forecast to grow at a 5.27% CAGR over 2026-2031.

- By packaging format, Rigid formats accounted for 56.23% of the 2025 base, yet flexible packs are on track for a 4.31% CAGR to 2031.

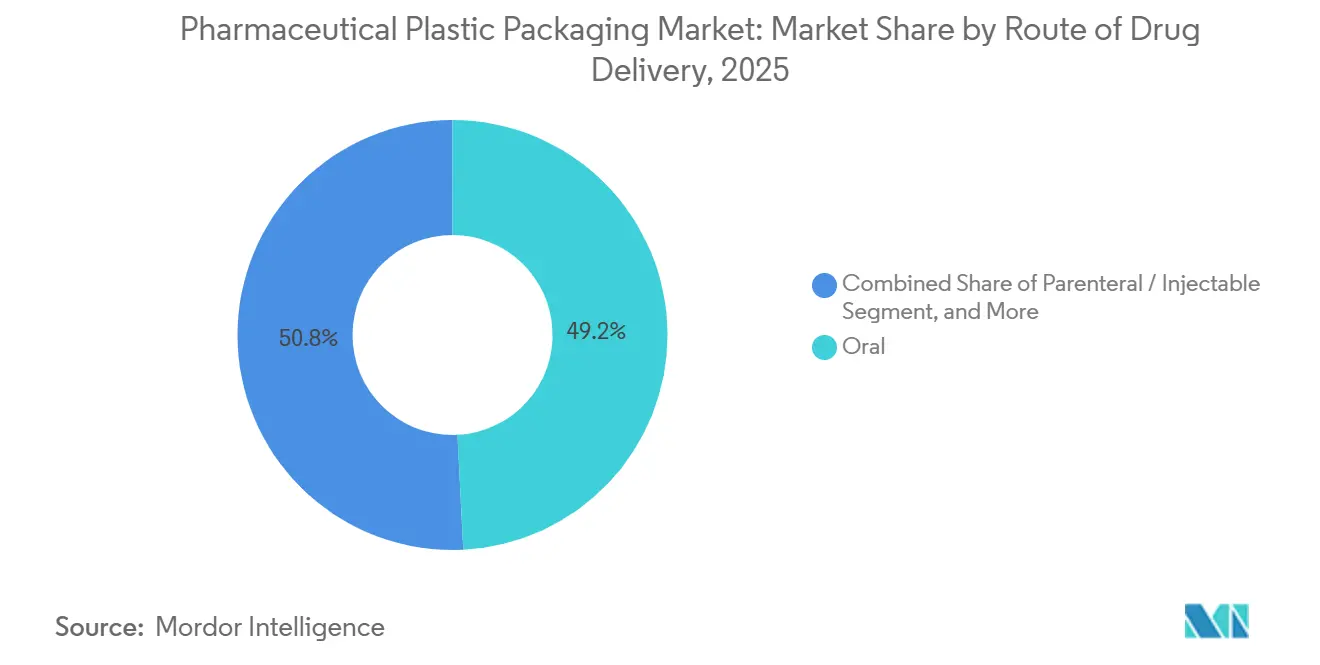

- By route of drug delivery, Oral drug delivery held 49.20% of the 2025 total, while parenteral and injectable formats are projected to expand at a 4.69% CAGR over the same horizon.

- By end-user, Pharmaceutical manufacturers commanded 47.12% of 2025 demand, but contract development and manufacturing organizations are expected to rise at a 4.78% CAGR to 2031.

- By geography, North America led with a 29.32% slice in 2025, and Asia-Pacific is anticipated to post a 4.91% CAGR, the fastest regional trajectory to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for plastic packs for biologics and injectables | +1.2% | Global | Medium term (2-4 years) |

| Expansion of generic drug production in emerging markets | +0.8% | Asia-Pacific, South America, Africa | Long term (≥ 4 years) |

| Lightweight and shatter-proof logistics advantage | +0.7% | Global | Short term (≤ 2 years) |

| Home-health and e-commerce unit-dose adoption | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| AI-enabled predictive maintenance for BFS sterility | +0.4% | North America, Europe | Short term (≤ 2 years) |

| Circularity mandates and pharmaceutical-grade PCR supply | +0.3% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Plastic Packs for Biologics and Injectables

A rising biologics pipeline is shifting container selection away from glass toward cyclic olefin polymer vials, prefillable syringes, and high clarity PET, options that reduce breakage and lower extractables. Recent FDA and EMA endorsements of COP and COC have shortened validation timelines, encouraging Big Pharma to retrofit filling suites with blow-fill-seal and syringe nesting stations.[1]U.S. Food and Drug Administration, “Container Closure Systems for Packaging Human Drugs and Biologics,” fda.gov Contract packers now quote sub-15-day changeovers, a speed essential for mRNA and cell-therapy launches. The sharper focus on compatibility also extends to low-adsorption silicone coatings that preserve protein integrity during cold-chain transit.[2]European Medicines Agency, “Guideline on Plastic Immediate Packaging Materials,” ema.europa.eu Collectively, these shifts reinforce plastics as the preferred primary barrier for next-generation parenterals.

Expansion of Generic Drug Production in Emerging Markets

China and India continue to scale WHO-aligned manufacturing campuses, using cost-effective HDPE and PP bottles to accelerate abbreviated new-drug application approvals.[3]Central Drugs Standard Control Organization, “Revised GMP Schedule M,” cdsco.gov.in Regional CDMOs bundle automated filling, serialization, and tamper-evident banding to win multinational contracts targeting price-sensitive therapies for Africa and South America. Government incentives, such as India’s production-linked subsidies, further catalyze upstream resin polymerization projects that de-risk supply continuity. This capacity build-out enables faster substitution of off-patent biologics, sustaining long-term demand for versatile, regulatory-compliant plastic packs.

Lightweight and Shatter-Proof Logistics Advantage

Airfreight providers report a measurable drop in temperature-excursion claims when PET or HDPE containers replace glass for narcotics and specialty injectables. Lower tare weight trims freight costs, while shatter-proof resilience reduces spoilage across last-mile delivery in regions where road infrastructure remains fragmented. Packaging converters collaborate with carriers to pre-qualify high-barrier monolayer bottles that withstand −20 °C to +40 °C excursions, supporting global vaccine distribution programs. This combination of cost savings and risk mitigation positions plastics as the default for high-velocity supply chains.

Home-Health and E-Commerce Unit-Dose Adoption

Telehealth platforms and specialty pharmacies now ship biologics directly to patients, necessitating tamper-evident blister strips, connected inhalers, and insulated pouches that fit through standard mail slots. The FDA’s draft guidance on mail-order drug stability has prompted brands to integrate NFC tags for real-time temperature logging. In Europe, the updated Medical Device Regulation classifies smart auto-injectors as combination products, accelerating alliances between device start-ups and packaging majors. As adherence tracking becomes standard for high-cost therapies, data-enabled plastic formats gain an edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended plastics-waste regulation, EU SUP and EPR compliance costs | −1.1% | Europe, North America, Global | Medium term (2-4 years) |

| Volatile polymer feedstock pricing linked to crude-oil and naphtha swings | −0.7% | Global | Short term (≤ 2 years) |

| Biologic-glass policy shift toward COP vials | −0.4% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Scarcity of pharma-grade PCR certification | −0.3% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extended Plastics-Waste Regulation, EU SUP and EPR Compliance Costs

The EU Single-Use Plastics directive now obliges pharmaceutical packers to finance collection, sorting, and recycling, even though medical packaging faces partial derogations. Parallel EPR schemes in France and Germany levy eco-modulated fees that reward monomaterial designs but penalize multilayer laminates. U.S. states such as Washington and Oregon have proposed analogous take-back laws, signaling broader spillover. Compliance demands investment in traceability printing, life-cycle assessments, and recycled-content verification, eroding margins for converters that already operate under GMP constraints. Suppliers lacking closed-loop partnerships may defer innovation programs to cover mounting regulatory overhead.

Volatile Polymer Feedstock Pricing Linked to Crude-Oil and Naphtha Swings

Geopolitical uncertainty and refinery outages caused HDPE spot prices to swing more than 30% during 2025-2026. Pharmaceutical converters countered by dual-sourcing resins and negotiating quarterly indexation with drugmakers, yet price pass-throughs lag feedstock spikes. Although bio-based ethylene projects in Brazil and the United States promise diversification, their medical-grade output remains limited, and qualification cycles can exceed 18 months. Such volatility disrupts capital budgeting for new syringe lines and forces some buyers to maintain larger safety stocks, temporarily inflating working capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: PET Sets the Pace While HDPE Widens Application Scope

PET secured 34.23% of pharmaceutical plastic packaging market share in 2025, reflecting its transparency, barrier performance, and recyclability credentials. The material dominates high-turnover cough syrups, oral suspensions, and increasingly, parenteral diluents that benefit from its low-extractable profile. Widespread acceptance across the United States Pharmacopeia, European Pharmacopoeia, and Japanese Pharmacopoeia accelerates line changeovers, keeping throughput high. Over the outlook period, brand owners are piloting recycled-content PET with 30% post-consumer resin, contingent on FDA non-objection letters that certify purity levels.

High-density polyethylene is forecast as the fastest-rising resin, with a 5.09% CAGR. Drugmakers value HDPE’s chemical resistance for aggressive antiseptics, ophthalmic washes, and inhalation solutions. Blow-molding advancements now deliver <0.1 µm particulate levels, matching sterility demands for ventricular catheter flushes. Regional suppliers in Asia-Pacific are scaling multimodal polymer reactors that integrate bimodal HDPE grades, enabling lighter bottle designs without compromising top-load. The result is a progressive down-gauging trend that optimizes freight efficiency while meeting tight moisture-vapor-transmission targets.

By Product Type: Vials Hold Scale as Prefillable Syringes Accelerate Patient Convenience

Vials and ampoules retained the top slot with a 17.32% 2025 slice of the pharmaceutical plastic packaging market. Biologic-glass delamination concerns are redirecting fill-finish managers to COP vials that withstand cryogenic storage to −80 °C. Complex oncology regimens often require multi-dose formats, and multilayer vial walls balance oxygen barrier with gamma-sterilization compatibility. Automated vision systems detect injection-mold flash defects under 50 µm, lifting batch release confidence.

Prefillable syringes and cartridges are projected to register the segment-leading 5.27% CAGR. The surge stems from self-administration trends in diabetes, rheumatoid arthritis, and emerging weight-management biologics. Integrated plungers with baked-on silicone minimize siliconization particles, enhancing patient safety. Device-packaging convergence is intensifying, with auto-injector platforms embedding RFID chips for dose logging that meets payer reimbursement conditions. As national health systems tie reimbursements to adherence data, suppliers that bundle primary container, plunger, and smart cap gain a procurement edge.

By Packaging Format: Rigid Dominates Volume, Yet Flexible Leads Agility

Rigid formats comprised 56.23% of sales in 2025, anchored by molding scale economies in bottles, vials, and multidose syringes. Serialization requirements drive demand for flat sidewalls that accommodate two-dimensional barcodes, and label-free laser etching is gathering pace. Yet producers face cost escalation from rising ethylene prices, spurring interest in format flexibility.

Flexible packs are on a 4.31% growth path and increasingly target high-barrier pouches for antibiotic dry-powders, stick packs for electrolyte rehydration salts, and cold-form blister webs for high-potency oncology pills. New PE-PP monomaterial laminates meet EU recycle-readiness criteria, and in-line blown-film extrusion enables rapid custom sizing, a decisive advantage for small-batch orphan drugs. Coupled with lightweight attributes, flexible packs now feature desiccant-integrated layers, extending product beyond-use dating without secondary cartons.

By Route of Drug Delivery: Oral Retains Scale, Injectables Propel Innovation

Oral dosage maintained 49.20% of the 2025 tally, with HDPE and PP bottles prevailing due to childhood safety closures and cost efficiency. However, patient adherence challenges persist, and brands embed humidity indicators plus audible click rings that confirm cap torque, reducing medication errors. Parenteral and injectable delivery is poised for a 4.69% CAGR, reflecting the biologic wave.

BFS vials, polymer-based dual-chamber syringes, and collapsible infusion bags support cold-chain integrity and eliminate rubber stoppers, mitigating particulate risk. Sterile barrier validation leverages advanced helium leak-testing down to 1 × 10⁻⁶ mbar·L/s, ensuring container closure integrity for immunotherapies.

By End-User: Manufacturers Dominate Installed Base while CDMOs Expand Share

Pharmaceutical manufacturers controlled 47.12% of demand in 2025, backed by vertically integrated fill-finish lines that favor long-run efficiencies. Investments in robotic nested tub loading and AI-driven inspection help operators sustain >99.9% first-pass yield for high-value biologics. CDMOs, projected for a 4.78% CAGR, attract emerging biotech firms that prefer asset-light commercialization.

Their modular cleanrooms accommodate rapid format changes between PET oral liquids in the morning and cyclic olefin syringes in the evening, a flexibility that large incumbents cannot match easily. Hospitals and home-care ecosystems also influence specification, advocating for color-coded ports and tactile markings that aid visually impaired patients.

Geography Analysis

North America represented 29.32% of 2025 global value, underlining its advanced regulatory environment and strong biologics pipeline. The United States alone operates more than 50 commercial blow-fill-seal lines certified for high-potency drugs, while Canada aligns formulation pack standards through Health Canada monographs. Mexico’s border industrial corridor upgrades extrusion-blow-molding clusters to support regional vaccine filling, deepening near-shoring resilience. Widespread serialization mandates prompted early adoption of machine-readable 2D codes, and digital traceability now underpins narcotic diversion control.

Europe remains a bellwether for sustainability policy. Germany and France pilot circular-economy hubs where PET pharmaceutical bottles reenter feedstock loops within 30 days. The EU SUP directive and eco-modulated EPR fees accelerate monomaterial conversion, and real-world clinical trials measure patient acceptance of lighter packs. Central and Eastern European converters catch up by licensing barrier film chemistries that pass EP rigid-container extractables testing, narrowing performance gaps with Western peers. Brexit-aligned United Kingdom maintains MHRA recognition of EMA container standards, preserving cross-border equivalence.

Asia-Pacific is assessed to clock the fastest 4.91% CAGR from 2026 onward. China’s Hainan Free Trade Port offers zero-tariff import of resin compounding equipment, fast-tracking multinationals that co-locate packaging with biologic fill-finish. India’s revised Schedule M compels plants to adopt Class 100 laminar flow during bottle filling, upgrading quality baselines. Japan deploys smart blister packs for dementia medications, capturing electronic adherence data reimbursed by public insurers. South Korea’s CDMOs, leveraging K-Bio health incentives, integrate cloud-linked cleanrooms that stream data to EMA regulators, expediting batch release for European exports.

The Middle East undertakes localization drives anchored by sovereign health strategies. Saudi Arabia’s Vision 2030 funds polymer tube lines for topical creams, while United Arab Emirates free zones entice global converters through 50-year corporate tax exemptions. Africa’s incremental build-out concentrates in South Africa’s Gauteng province, where PET preform molding supports antiretroviral programs. Nigeria and Egypt court overseas joint ventures that bundle resin supply with GMP training, narrowing capability gaps.

South America targets import substitution to improve drug affordability. Brazil’s ANVISA fast-tracks prefillable syringe projects that include local content requirements, and Argentina extends tax credits for pharmaceutical pouch lines producing orphan-drug sachets for neighboring markets. Continental harmonization via Mercosur eases pack artwork and language compliance, incentivizing multinational launches.

Competitive Landscape

The top five suppliers, Amcor, Gerresheimer, AptarGroup, West Pharmaceutical Services, and Berry Global, collectively represent well over half of installed capacity, underscoring moderate consolidation. Recent shifts emphasize capacity localization: Gerresheimer’s USD 120 million Indian syringe plant brings production within one-day trucking of major vaccine hubs, slashing lead times for domestic demand. Amcor’s Brazilian acquisition adds flexible and rigid assets, reinforcing its one-stop offering for biologics across South America.

Innovation pipelines reveal strategic pivots toward smart and circular designs. West’s 2025 launch of an RFID-enabled self-injection system combines tamper evidence and adherence data capture, and AptarGroup’s barrier-enhanced nasal systems cater to preservative-free formulations demanded by European allergen therapy specialists. Berry Global’s investment in United States HDPE clean-room molding extends supply redundancy for high-potency applications. Patent analytics show a surge in low-extractable cyclic olefin structures and micro-taggant anticounterfeit coatings filed during 2025-2026.

Competitive heat intensifies as Asia-Pacific challengers harness cost advantage and government subsidies to supply CDMOs serving Western drug sponsors. Digital manufacturing techniques—computer vision for defect mapping, automated tool-change robots, and cloud MES integration—compress lead times and allow rapid iteration on geometry. Sustainability credentials increasingly influence procurement scoring, and converters with closed-loop PET or HDPE partnerships secure multiyear offtake agreements from Big Pharma sustainability councils. Despite margin pressures from raw-material price swings, established incumbents retain leverage through GMP pedigree, multi-regional audit readiness, and broad SKU portfolios.

Pharmaceutical Plastic Packaging Industry Leaders

Aptar Group Inc.

Plastipak Holdings

Amcor PLC

Klöckner Pentaplast Group

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AptarGroup unveiled an inline-sensor cap that records humidity exposure for high-potency oral solids, targeting oncology supply chains.

- February 2026: Gerresheimer inaugurated a USD 120 million prefillable syringe facility in India equipped with AI-based vision inspection, doubling local capacity by 2027.

- January 2026: Amcor completed the acquisition of a Brazilian specialty converter, adding biologics-oriented flexible and rigid lines to its South American footprint.

- December 2025: Berry Global announced a USD 45 million United States plant focused on medical-grade HDPE and PET containers for injectables and oral solids.

Global Pharmaceutical Plastic Packaging Market Report Scope

Pharmaceutical plastic packaging involves using plastic materials to package pharmaceutical drugs. Pharmaceutical plastic bottles, tailored for storing and distributing pharmaceutical products, are pivotal in upholding the safety, efficacy, and integrity of medications and pharmaceutical items. Pharmaceutical plastic packaging products are designed to protect the contents from contamination, moisture, and light, ensuring the drugs remain effective throughout their shelf life. Additionally, plastic packaging offers lightweight, durability, and cost-effectiveness benefits, making it a preferred choice in the pharmaceutical industry.

The Pharmaceutical Plastic Packaging Market Report is segmented by Raw Material (Polypropylene, Polyethylene Terephthalate, High-Density Polyethylene, Low-Density Polyethylene, Cyclic Olefin Polymer/Copolymer, Bio-Based and Recycled Plastics), Product Type (Bottles and Solid Containers, Vials and Ampoules, Pre-Fillable Syringes and Cartridges, Blister Packs and Strip Packs, Pouches/Stick Packs/Sachets, Closures, Caps and Lids, IV Bags and Flexible Bags), Packaging Format (Rigid, Flexible), Route of Drug Delivery (Oral, Parenteral/Injectable, Ophthalmic/Nasal, Topical/Transdermal), End-User (Pharma Manufacturers, CDMOs, Hospitals and Clinics, Home-Care Settings), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

By Raw Material

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) |

| Cyclic Olefin Polymer / Copolymer (COP/COC) |

| Bio-Based and Recycled Plastics |

By Product Type

| Bottles and Solid Containers |

| Vials and Ampoules |

| Pre-Fillable Syringes and Cartridges |

| Blister Packs and Strip Packs |

| Pouches / Stick Packs / Sachets |

| Closures, Caps and Lids |

| IV Bags and Flexible Bags |

By Packaging Format

| Rigid |

| Flexible |

By Route of Drug Delivery

| Oral |

| Parenteral / Injectable |

| Ophthalmic / Nasal |

| Topical / Transdermal |

By End-User

| Pharma Manufacturers |

| Contract Development and Manufacturing Orgs (CDMOs) |

| Hospitals and Clinics |

| Home-Care Settings |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Raw Material | Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | ||

| High-Density Polyethylene (HDPE) | ||

| Low-Density Polyethylene (LDPE) | ||

| Cyclic Olefin Polymer / Copolymer (COP/COC) | ||

| Bio-Based and Recycled Plastics | ||

| By Product Type | Bottles and Solid Containers | |

| Vials and Ampoules | ||

| Pre-Fillable Syringes and Cartridges | ||

| Blister Packs and Strip Packs | ||

| Pouches / Stick Packs / Sachets | ||

| Closures, Caps and Lids | ||

| IV Bags and Flexible Bags | ||

| By Packaging Format | Rigid | |

| Flexible | ||

| By Route of Drug Delivery | Oral | |

| Parenteral / Injectable | ||

| Ophthalmic / Nasal | ||

| Topical / Transdermal | ||

| By End-User | Pharma Manufacturers | |

| Contract Development and Manufacturing Orgs (CDMOs) | ||

| Hospitals and Clinics | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the pharmaceutical plastic packaging market be by 2031?

It is projected to reach USD 12.09 billion by 2031, based on a 3.92% CAGR from 2026 to 2031.

Which raw material leads current demand?

Polyethylene terephthalate held 34.23% of 2025 demand, topping all other resins.

What packaging format is growing fastest?

Flexible packs are expected to grow at a 4.31% CAGR, outpacing rigid alternatives.

Why are prefillable syringes gaining traction?

Self-administration trends and biologic therapies are driving a 5.27% CAGR for prefillable syringes and cartridges.

Which region is set to expand quickest?

Asia-Pacific is forecast to post a 4.91% CAGR because of manufacturing expansion in China and India.

How are regulations influencing material choices?

EU SUP, EPR fees, and FDA guidance push converters toward recyclable monomaterial packs and certified recycled resin to balance compliance and sustainability.

Page last updated on: