Cleaning Robot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.98 Billion |

| Market Size (2031) | USD 38.52 Billion |

| Growth Rate (2026 - 2031) | 14.38% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

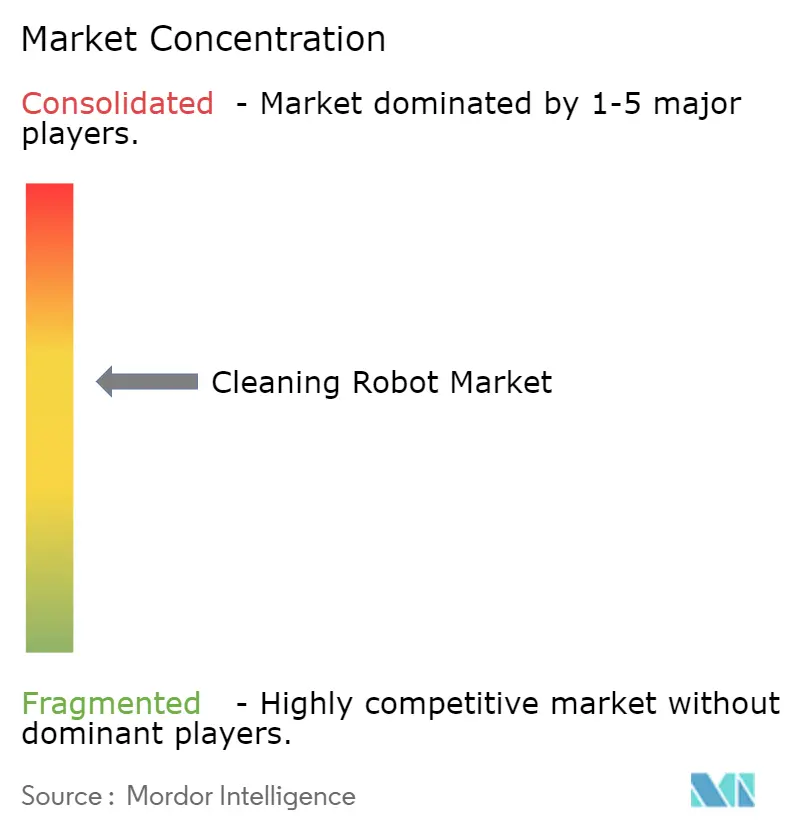

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cleaning Robot Market Analysis by Mordor Intelligence

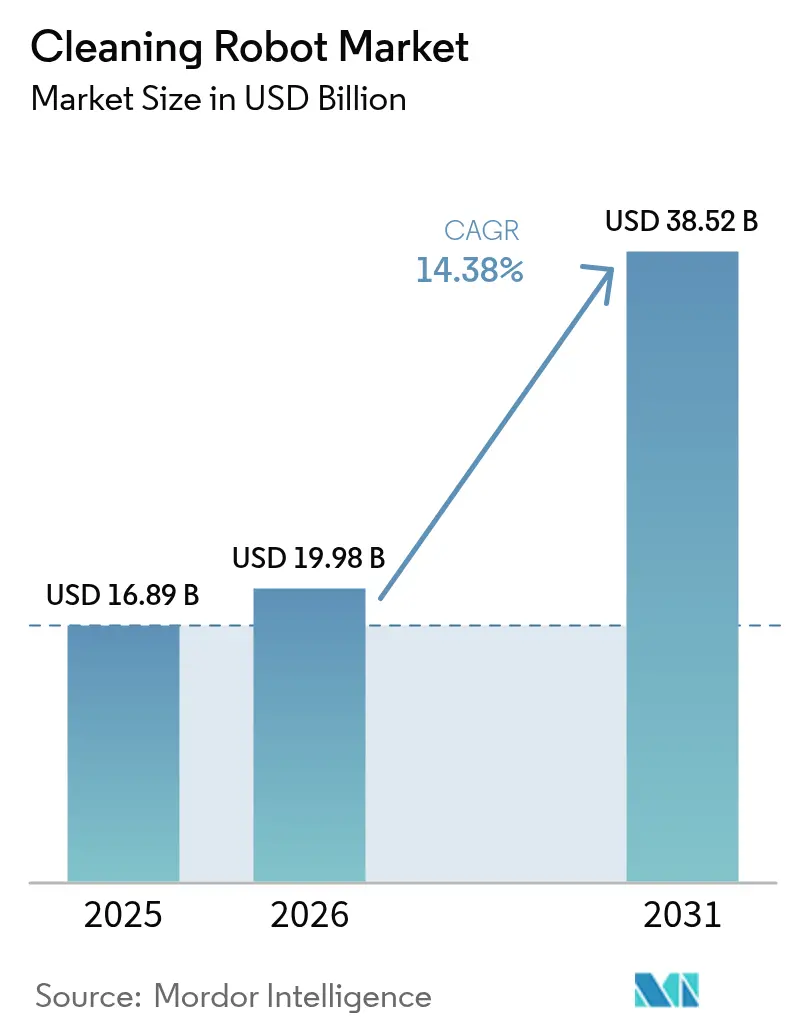

The cleaning robot market size is projected to be USD 16.89 billion in 2025, USD 19.68 billion in 2026, and reach USD 38.52 billion by 2031, growing at a CAGR of 14.38% from 2026 to 2031. Structural labor shortages, post-pandemic hygiene mandates, and rapid smart-home adoption keep demand elevated for both residential and professional robots. Falling LiDAR and vision-sensor average selling prices compress bill-of-materials costs, enabling mid-tier models to offer premium navigation features and drawing price-sensitive buyers into the cleaning robot market. Facility-management firms are turning to robots-as-a-service to reclassify janitorial spending as an operating lease, unlocking budget headroom for autonomous systems. Competitive intensity is increasing as vertically integrated Chinese manufacturers undercut incumbents on price while matching feature parity, placing sustained pressure on gross margins throughout the cleaning robot market.

Key Report Takeaways

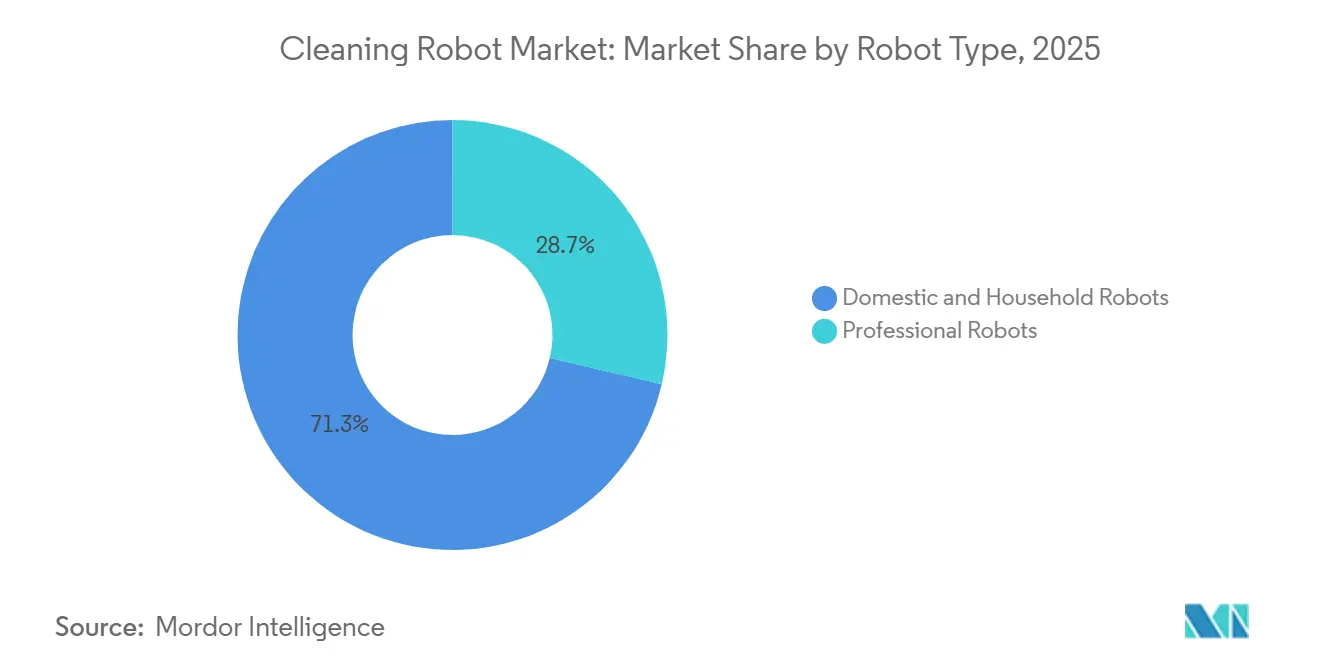

- By robot type, household units led with 71.32% of the cleaning robot market share in 2025, while professional robots are forecast to advance at a 15.23% CAGR through 2031.

- By end-user, the residential segment accounted for a 57.46% share of the cleaning robot market size in 2025, whereas the commercial segment is projected to expand at a 14.87% CAGR over 2026-2031.

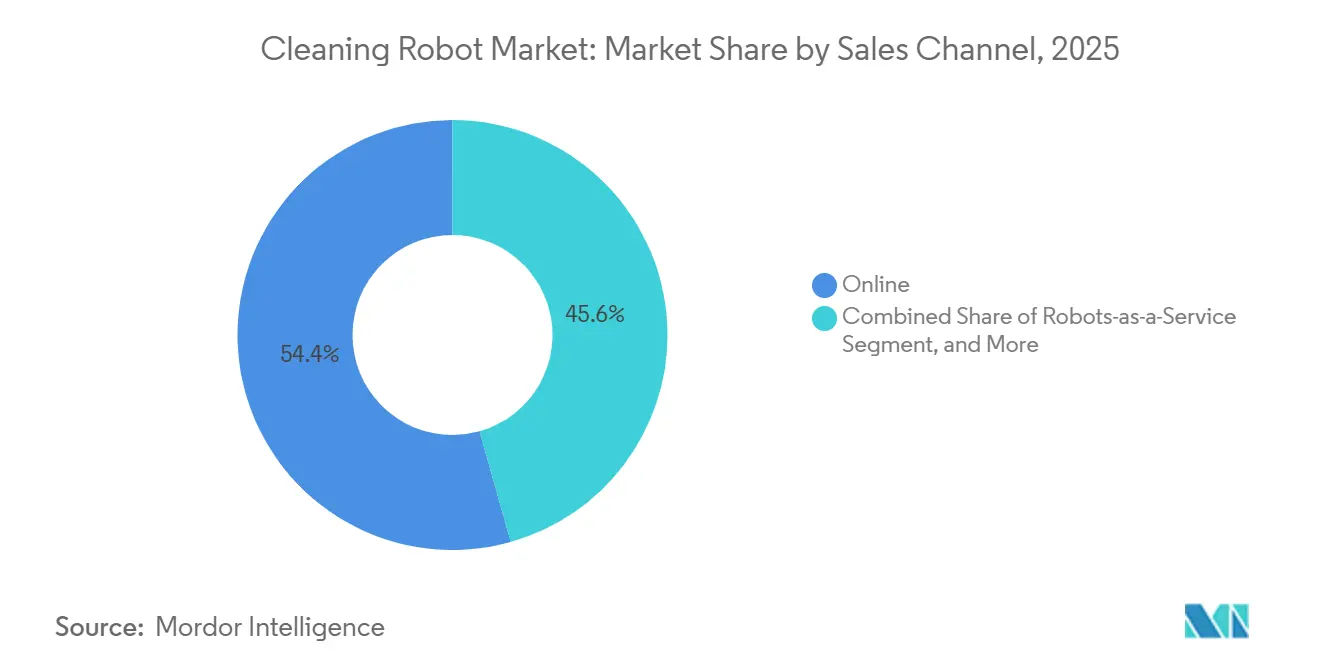

- By sales channel, online outlets captured 54.37% revenue share in 2025; robots-as-a-service is the fastest-growing channel at a 15.76% CAGR during the forecast period.

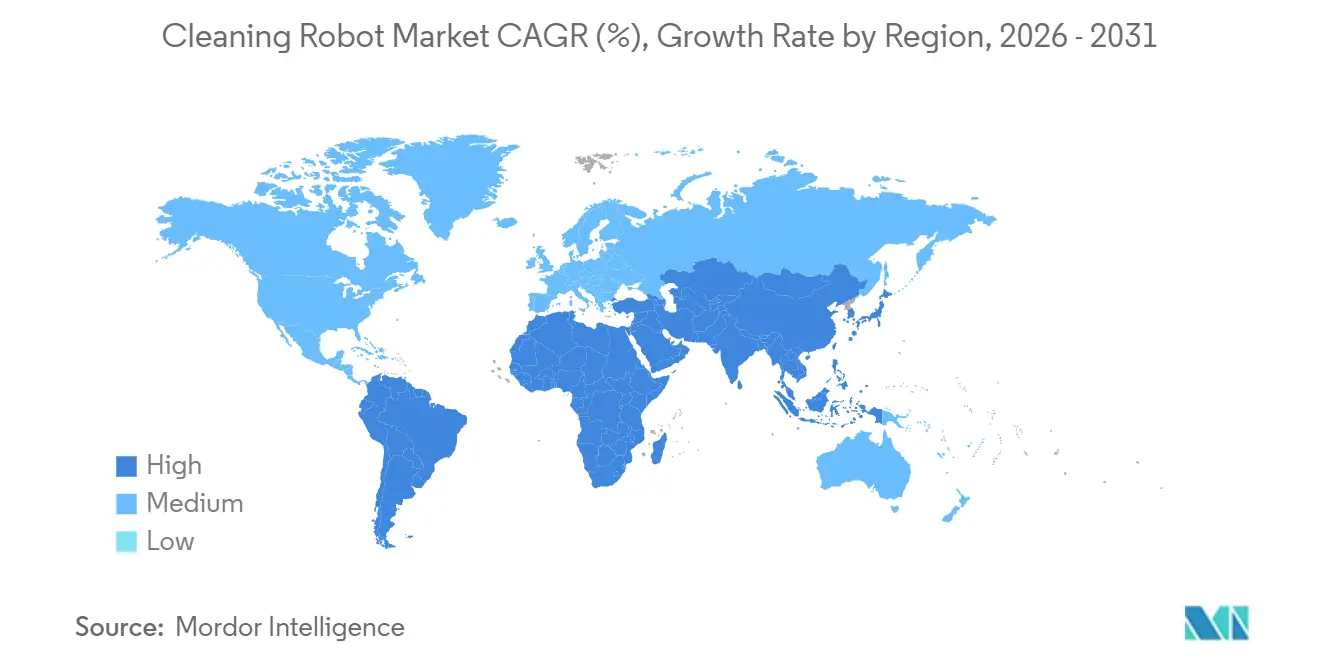

- By geography, North America held a 39.41% revenue share in 2025, yet Asia-Pacific is expected to post the highest regional CAGR at 15.07% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cleaning Robot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Post-Pandemic Hygiene Standards In Commercial Spaces | +3.2% | Global, most visible in North America, Europe, and Asia-Pacific healthcare and hospitality properties | Medium term (2-4 years) |

| Rapid Smart-Home Penetration And Disposable-Income Growth | +2.8% | North America and Europe mature markets, Asia-Pacific emerging middle class | Long term (≥ 4 years) |

| Falling LiDAR And Sensor-Suite ASPs Reduce BOM Cost | +2.5% | Global, with manufacturing concentration in China | Short term (≤ 2 years) |

| Facility-Management Contracts Shifting To Robots-As-A-Service | +2.1% | North America and Europe commercial real estate, extending to Middle East and Asia-Pacific | Medium term (2-4 years) |

| E-Commerce Channel Scaling Accelerates Global Reach | +1.9% | Global, highest penetration in urban North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Government Procurement Of UV-Disinfection Robots For Public Infrastructure | +1.3% | Asia-Pacific (Singapore, Japan, South Korea) and Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Post-Pandemic Hygiene Standards in Commercial Spaces

Airports, hotels, and hospitals now treat continuous, highly visible cleaning as a non-negotiable amenity. At London Heathrow Airport, 50 autonomous scrubbers deployed in 2025 delivered a 40% reduction in labor hours while enabling 24/7 floor sanitization.[1]Mitie Group, “Mitie Deploys Autonomous Cleaning Robots at Heathrow Airport,” mitie.com Facility managers view audit-ready disinfection logs and pathogen-removal metrics as differentiators when bidding for corporate tenants. The premium commanded by professional cleaning robots, typically priced between USD 30,000 and USD 120,000, is increasingly justified by payback periods of under 18 months in high-traffic venues. Heightened infection-control standards lock in recurring demand for UV-C and electrostatic-spray variants, ensuring sustained growth in the cleaning robot market. Vendors that integrate compliance reporting directly into the fleet-management dashboard strengthen their value proposition to risk-averse operators.

Rapid Smart-Home Penetration and Disposable-Income Growth

Robot vacuums have graduated from novelty to necessity in North American and Western European households, a shift mirrored by rising ownership in Chinese and Southeast Asian urban centers. At IFA 2025, 94% of new smart-home cleaning launches were robotic vacuums.[2]IFA Berlin, “IFA 2025 Smart Home Product Launches,” ifa-berlin.com Parks Associates reported that 42% of U.S. homes owned at least one smart-home device in 2024, with robot vacuums ranking third in adoption. Feature innovation, AI obstacle avoidance, self-emptying docks, and combined vacuum-mop capability, encourages replacement purchases every three to four years. Disposable-income gains in Asia-Pacific expand the buyer pool, with units priced between USD 300 and USD 800 now within reach of the growing middle class. This demographic tailwind sustains double-digit unit growth for the cleaning robot market even as mature regions plateau.

Falling LiDAR and Sensor ASPs Reduce Bill of Materials Cost

Automotive investment in solid-state LiDAR has collapsed component pricing for adjacent robotics applications. Hesai Technology cut LiDAR costs by 99.5% in eight years, targeting USD 200 per module by late 2025. IEEE research demonstrated low-cost LiDAR SLAM capable of sub-USD 50 bill-of-materials.[3]IEEE, “Low-Cost LiDAR SLAM for Mobile Robotics,” ieeexplore.ieee.org These savings allow sub-USD 500 home robots to incorporate mapping-grade sensors once reserved for premium SKUs, leveling the competitive playing field. For professional models, the same cost curve enables dual-LiDAR plus vision stacks that navigate large-format retail and warehouse spaces without costly infrastructure modifications. Reduced hardware differentials shift competition toward software intelligence and after-sales service, intensifying the race for proprietary AI navigation algorithms within the cleaning robot market.

Facility-Management Contracts Shifting to Robots-As-A-Service

Enterprises increasingly treat cleaning as a subscription rather than a capital purchase. In 2025, SoftBank Robotics and HITEK AI launched Middle East leasing packages starting at USD 1,200 per month, covering hardware, maintenance, and performance guarantees.[4]SoftBank Robotics, “Robots-as-a-Service Launch in UAE and Saudi Arabia,” softbankrobotics.com Australian provider Intelliclean disclosed that 35% of new contracts in 2024 included robots-as-a-service clauses, nearly triple the 2022 level.[5]Intelliclean, “RaaS Contract Growth in Australian Facilities,” intelliclean.com.au The model unlocks adoption among small and medium-sized enterprises that lack upfront budgets, thereby expanding the addressable cleaning robot market. Predictable operating expenses appeal to publicly traded real-estate investment trusts eager to shield EBITDA from wage inflation. Manufacturers benefit from recurring software fees, boosting lifetime customer value and smoothing revenue cyclicality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Versus Conventional Equipment | -1.8% | Global, particularly price-sensitive South America, Africa, and Southeast Asia | Short term (≤ 2 years) |

| Data-Privacy Concerns Over Camera/VSLAM Mapping | -0.9% | Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Supply-Chain Fragility For Solid-State LiDAR Components | -0.6% | Global, concentration in Taiwan and South Korea fabs | Short term (≤ 2 years) |

| Emerging Trade Tariffs On Chinese Robot Exports | -1.1% | North America and Europe import markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Equipment

Professional robots often carry price tags ten to forty times higher than manual scrubbers, creating sticker shock for budget-constrained operators. While robots-as-a-service spreads payments over time, hidden expenses, consumables, software subscriptions, and periodic recalibration, add up to 25% per year to total cost of ownership. The hurdle is most acute in South America and Africa, where household and enterprise purchasing power lags developed regions. Vendors bundle financing and predictive-maintenance guarantees to soften the blow, yet many facilities delay adoption until component costs fall further, tempering near-term growth in the cleaning robot market.

Data-Privacy Concerns Over Camera/VSLAM Mapping

Vision-based mapping raises regulatory red flags in jurisdictions with strict privacy regimes. Brain Corp’s 2024 whitepaper described edge anonymization to comply with GDPR, but many competitors still transmit raw video to the cloud.[6]Brain Corp, “GDPR Compliance for Autonomous Mobile Robots,” braincorp.com The U.K. Information Commissioner’s Office clarified in 2025 that camera-equipped robot vacuums fall under surveillance regulations, requiring explicit consent. A 2024 data breach involving leaked interior images eroded consumer trust and triggered a class-action settlement. Manufacturers now tout LiDAR-only designs or on-device processing as privacy-centric differentiators, yet added engineering complexity can raise bill-of-materials cost, constraining margins within the cleaning robot market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Household Dominance Masks Professional Surge

Domestic robots accounted for 71.32% of revenue in 2025, reflecting their entrenched status as smart-home staples, but professional units are forecast to outpace them at a 15.23% CAGR to 2031. The vacuum sub-segment remains the cornerstone, benefiting from self-emptying docks and AI obstacle avoidance that spur upgrade cycles. Pool cleaners form a high-margin niche as solar-powered designs slash electricity use by up to 80%. ECOVACS has sold 1.5 million window-cleaning units cumulatively and holds 278 patents in suction and edge detection. Lawn-mowing robots equipped with RTK-GPS are scaling in suburban markets, with commercial models such as Husqvarna CEORA priced at EUR 15,000-20,000 (USD 16,950-22,600).

Professional robots, though smaller in unit volume, deliver higher revenue per device and deeper workflow integration. Floor-scrubber fleets connect to facility dashboards, covering 20,000 square feet per charge and sending real-time utilization metrics. UV-C disinfection units, now routine in Japanese and South Korean hospitals, achieve 99.9% pathogen reduction in 15-minute cycles. Tank-cleaning robots priced between USD 50,000 and USD 200,000 minimize confined-space entry risks in oil, chemical, and water utilities. Subscription models are accelerating adoption: the International Federation of Robotics recorded a 31% jump in robots-as-a-service fleets in 2024, underscoring the structural shift toward pay-per-use economics.

By End-User: Commercial Velocity Challenges Residential Incumbency

Residential buyers held 57.46% of the cleaning robot market in 2025, buoyed by North American and European penetration, but commercial demand is set to climb quickly at a 14.87% CAGR through 2031. Hotels pilot corridor-cleaning robots that trimmed labor hours by 30% while boosting guest satisfaction, according to field trials by Marriott International. Retail malls deploy overnight scrubbers to maintain glossy surfaces linked to higher shopper dwell time. Healthcare facilities integrate UV-C robots into terminal-cleaning protocols, cutting hospital-acquired infections by 22% in controlled studies.

Airports such as Heathrow now run fleets around the clock, capitalizing on multi-sensor navigation that avoids passengers and trolleys. Corporate offices accelerated adoption as cleaning-staff vacancies reached 20-30% in major metro areas, compelling facilities to fill gaps with automation. Industrial plants deploy ruggedized units that integrate with warehouse-management systems to steer clear of forklifts and autonomous mobile robots, creating a cooperative multi-robot environment. On the residential side, next-generation products unveiled at CES 2026, Roborock Saros 20 with a retractable arm and Dreame X60 Max Ultra with stair-climbing ability, target specific pain points, sustaining replacement cycles even as first-time purchase growth moderates.

By Sales Channel: Online Supremacy Meets Robots-as-a-Service (RaaS)Disruption

E-commerce captured 54.37% of 2025 revenue as buyers gravitated toward price transparency and door-step fulfillment. Parks Associates found that 70% of U.S. robot vacuum purchases occurred online in 2024. Direct-to-consumer brands leverage video explainers and influencer reviews to compress the sales funnel, while Chinese platforms offer same-day delivery and installment plans that democratize access to mid-tier models. Offline big-box retailers still matter for hands-on demos but surrendered three percentage points of share between 2023 and 2025.

Robots-as-a-service is the fastest-growing channel, rising at a 15.76% CAGR as enterprises convert capex into opex. SoftBank Robotics and HITEK AI’s Middle East launch illustrates regional appetite for bundled performance guarantees. Intelliclean tripled its RaaS contract mix in two years, evidencing momentum in developed Asia-Pacific. Manufacturers monetize recurring software subscriptions for fleet management and predictive maintenance, elevating lifetime gross margin beyond one-time hardware sales. For professional buyers, distributors such as Tennant and Nilfisk continue to add value through on-site integration, operator training, and 24/7 technical support.

Geography Analysis

North America generated 39.41% of 2025 revenue, underpinned by early smart-home adoption and stringent workplace-safety codes. The United States leads, with 42% household smart-home penetration in 2024 and robot vacuums ranking third in ownership, while Canada’s infection-control building codes spur UV-robot uptake. Mexico’s export-oriented manufacturing sector installs autonomous scrubbers to meet ISO 14001 compliance. Yet escalating tariffs on Chinese robots inflate retail prices, pressuring elasticity and nudging some buyers toward refurbished units or subscription models.

Asia-Pacific is expected to record the fastest 15.07% CAGR, fueled by urbanization and rising disposable incomes. Chinese giants Ecovacs and Roborock posted combined 2024 revenue exceeding USD 1.09 billion at prevailing exchange rates, underscoring domestic scale. Japan earmarked JPY 5 billion (USD 45.5 million) in subsidies for hospital UV-robot purchases in 2025. India’s e-commerce growth opens tier-2 cities, while Singapore’s ROBIN program showed a 60% pathogen-count reduction in public transport hubs. South Korea and Australia boast high per-capita ownership, aided by compact living spaces and tech-savvy consumers.

Europe, South America, Middle East, and Africa round out the cleaning robot market. Europe’s GDPR drives demand for on-device mapping, a boon for hybrid LiDAR-plus-vision systems from regional leaders. The United Kingdom’s window-robot segment reached GBP 64.21 million (USD 73.2 million) in 2025. German and French automakers deploy shop-floor robots for occupational safety compliance. South America remains highly price-sensitive, leading distributors to import mid-tier Chinese models with installment financing. Middle Eastern sovereign funds finance public-space fleets, while Africa’s nascent adoption is visible in South African malls and Nigerian airports despite infrastructural challenges.

Competitive Landscape

The top five vendors, iRobot, Ecovacs, Roborock, Dreame, and SharkNinja, command roughly 60% of the domestic cleaning robot market, indicating moderate concentration. iRobot’s aborted sale to Amazon in 2024 triggered restructuring, workforce cuts, and a 20% revenue slide, highlighting exposure to mature Western demand. Chinese challengers exploit vertical integration, from LiDAR fabrication to AI chipset design, to compress price points and erode incumbent margins. Roborock’s Q3 2024 revenue grew 26% year-over-year as it diversified into lawn-mowing and window-cleaning categories.

Innovation is tilting toward software differentiation. Narwal’s Flow 2 rotates fresh water every 10 minutes, solving hygiene complaints about stagnant mop reservoirs. Dreame’s X60 Max Ultra adds stair-climbing to address multi-level residences. Friendly Robots introduced a USD 29-per-month subscription, swapping units every two years to keep features current, a model targeting price-sensitive consumers.

Enterprise clients increasingly demand ISO 27001 certification and GDPR compliance, narrowing the vendor shortlist to companies with robust cybersecurity. Regional specialists such as Avidbots and Gaussian Robotics capture vertical niches, airport concourses, large-format retail, by bundling site surveys and integration services. Mergers and partnerships are accelerating as players seek scale and data to refine navigation algorithms, setting the stage for further consolidation within the cleaning robot market.

Cleaning Robot Industry Leaders

iRobot Corporation

Ecovacs Robotics Co., Ltd.

Roborock Technology Co., Ltd.

Neato Robotics Inc.

SharkNinja Operating LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Roborock unveiled the Saros 20 and Qrevo Curv 2 Flow at CES 2026, adding retractable arms for baseboard wiping and AI fusion obstacle avoidance.

- January 2026: Dreame Technology launched the X60 Max Ultra and Cyber 10 Ultra at CES 2026, featuring 35,000 Pa suction and stair-climbing capability, priced between USD 1,299 and USD 1,799.

- January 2026: Narwal Robotics introduced the Flow 2 at CES 2026 with a self-cleaning mop reservoir that refreshes water every 10 minutes.

- January 2026: Eufy debuted the Omni S2 at CES 2026 for USD 549, targeting value buyers with 8,000 Pa suction and basic obstacle avoidance.

Global Cleaning Robot Market Report Scope

Cleaning robots are autonomous devices capable of cleaning the floor, pool, windows, and lawns with little or no human intervention. Cleaning robots, such as robot vacuum cleaners, are used for residential and industrial purposes. Industrial cleaning robots are typically mobile, application-specific robots that automate industrial cleaning processes. These robots automate routine, dangerous, or dirty work for safety and efficiency.

The Cleaning Robot Market Report is Segmented by Robot Type (Domestic and Household Robots [Vacuum Floor Cleaner, Pool Cleaning, Window Cleaning, Lawn Cleaning, and Other Domestic and Household Cleaning], and Professional Robots [Floor Cleaning, Tank, Tube and Pipe Cleaning, Disinfection Robots, and Other Professional Cleaning]), End-User (Residential, Commercial [Hospitality, Retail and Shopping Centres, Healthcare Facilities, Airports and Transportation Hubs, Office and Corporate Facilities and Other Commercial Facilities], and Industrial), Sales Channel (Online, Offline, and Robots-as-a-Service), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Domestic and Household Robots | Vacuum Floor Cleaner |

| Pool Cleaning | |

| Window Cleaning | |

| Lawn Cleaning | |

| Other Domestic and Household Cleaning | |

| Professional Robots | Floor Cleaning |

| Tank, Tube and Pipe Cleaning | |

| Disinfection Robots | |

| Other Professional Cleaning |

| Residential | |

| Commercial | Hospitality |

| Retail and Shopping Centres | |

| Healthcare Facilities | |

| Airports and Transportation Hubs | |

| Office and Corporate Facilities | |

| Other Commercial Facilities | |

| Industrial (Manufacturing and Warehousing) |

| Online |

| Offline |

| Robots-as-a-Service |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Singapore | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Robot Type | Domestic and Household Robots | Vacuum Floor Cleaner |

| Pool Cleaning | ||

| Window Cleaning | ||

| Lawn Cleaning | ||

| Other Domestic and Household Cleaning | ||

| Professional Robots | Floor Cleaning | |

| Tank, Tube and Pipe Cleaning | ||

| Disinfection Robots | ||

| Other Professional Cleaning | ||

| By End-User | Residential | |

| Commercial | Hospitality | |

| Retail and Shopping Centres | ||

| Healthcare Facilities | ||

| Airports and Transportation Hubs | ||

| Office and Corporate Facilities | ||

| Other Commercial Facilities | ||

| Industrial (Manufacturing and Warehousing) | ||

| By Sales Channel | Online | |

| Offline | ||

| Robots-as-a-Service | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the cleaning robot market be by 2031?

It is projected to reach USD 38.52 billion by 2031, reflecting a 14.38% CAGR from 2026-2031.

Which region is expected to grow the fastest?

Asia-Pacific is forecast to post the highest CAGR at 15.07% thanks to urbanization, income growth, and local manufacturing scale.

What drives commercial adoption of cleaning robots?

Tight labor markets, post-pandemic hygiene standards, and the shift toward robots-as-a-service subscriptions accelerate uptake in hotels, airports, and hospitals.

Why are LiDAR prices important to the cleaning robot sector?

A 99.5% cost decline in solid-state LiDAR enables advanced navigation features in sub-USD 500 units, broadening affordability and intensifying competition.

How significant is privacy regulation for camera-equipped robots?

GDPR and similar rules require explicit consent and data minimization, prompting many manufacturers to adopt LiDAR-only or edge-processing designs to avoid compliance risks.

What is robots-as-a-service and why is it growing?

Robots-as-a-service lets enterprises lease autonomous cleaners with bundled maintenance and software updates, converting capex into predictable opex and lowering adoption barriers.

Page last updated on: