Civil Aerospace Training And Simulation Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.9 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

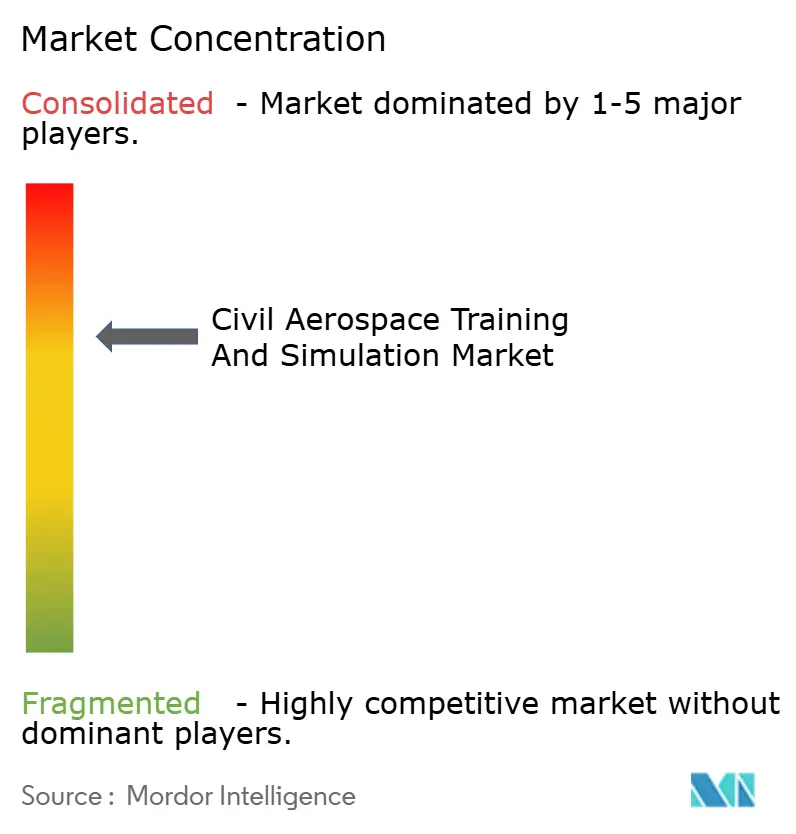

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Civil Aerospace Training And Simulation Market Analysis by Mordor Intelligence

The civil aerospace simulation and training market size is expected to grow from USD 1.93 billion in 2025 to USD 2.07 billion in 2026 and is forecasted to reach USD 2.9 billion by 2031 at a 6.98% CAGR over 2026-2031. Steady growth reflects airlines’ need to qualify record numbers of flight-deck and maintenance personnel while keeping revenue aircraft in service. This balance favors high-fidelity synthetic environments over fuel-intensive live flying. Regulatory authorities in the United States and Europe continue to expand the proportion of recurrent checks that can be completed in simulators, further enhancing the economics of the civil aerospace simulation and training market. At the same time, rapid adoption of digital-twin software and portable VR trainers compresses learning cycles and broadens access in secondary cities where full-flight devices were previously unaffordable. Rising cybersecurity expenditures and a deepening shortage of certified instructors temper momentum, but have not altered the upward trajectory, especially in the Asia-Pacific region, where China and India have set ambitious pilot-production targets.

Key Report Takeaways

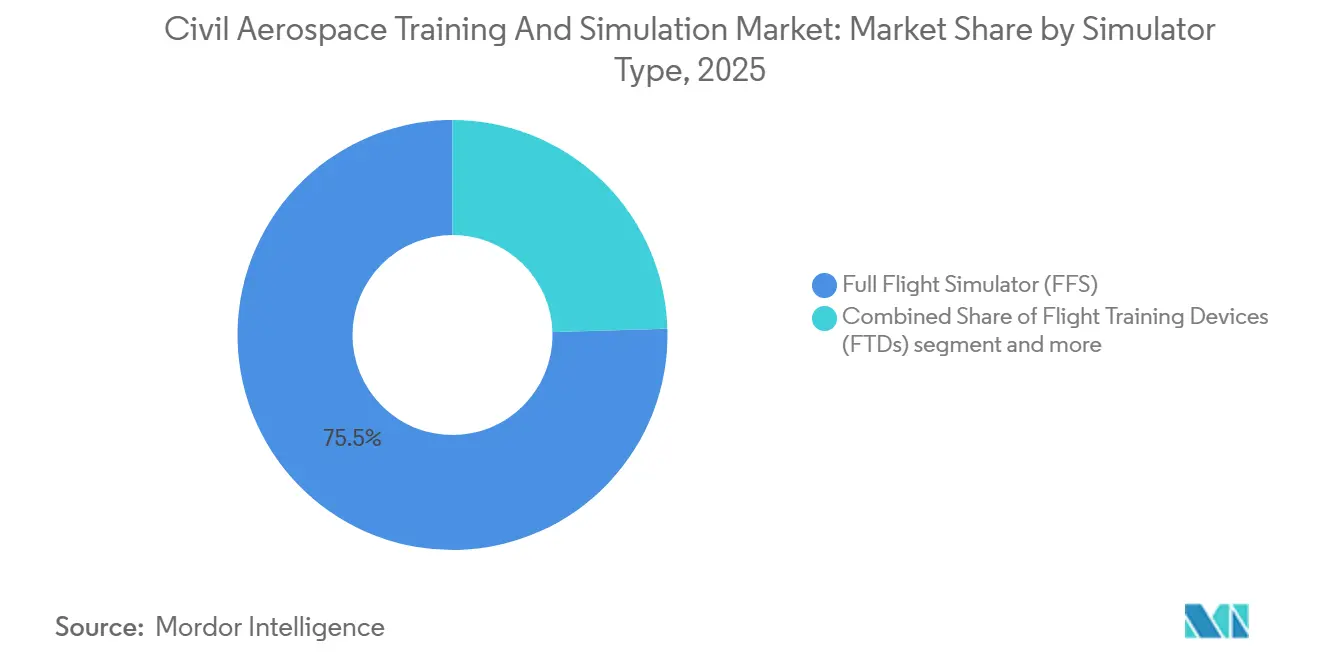

- By simulator type, full flight simulators captured 75.47% of the civil aerospace simulation and training market share in 2025; other simulator types, led by VR and fixed-base trainers, are forecast to expand at a 7.24% CAGR through 2031.

- By application, commercial aviation accounted for 72.13% of the revenue in 2025, while the space segment is poised for a 7.11% CAGR on the back of Artemis and commercial astronaut programs.

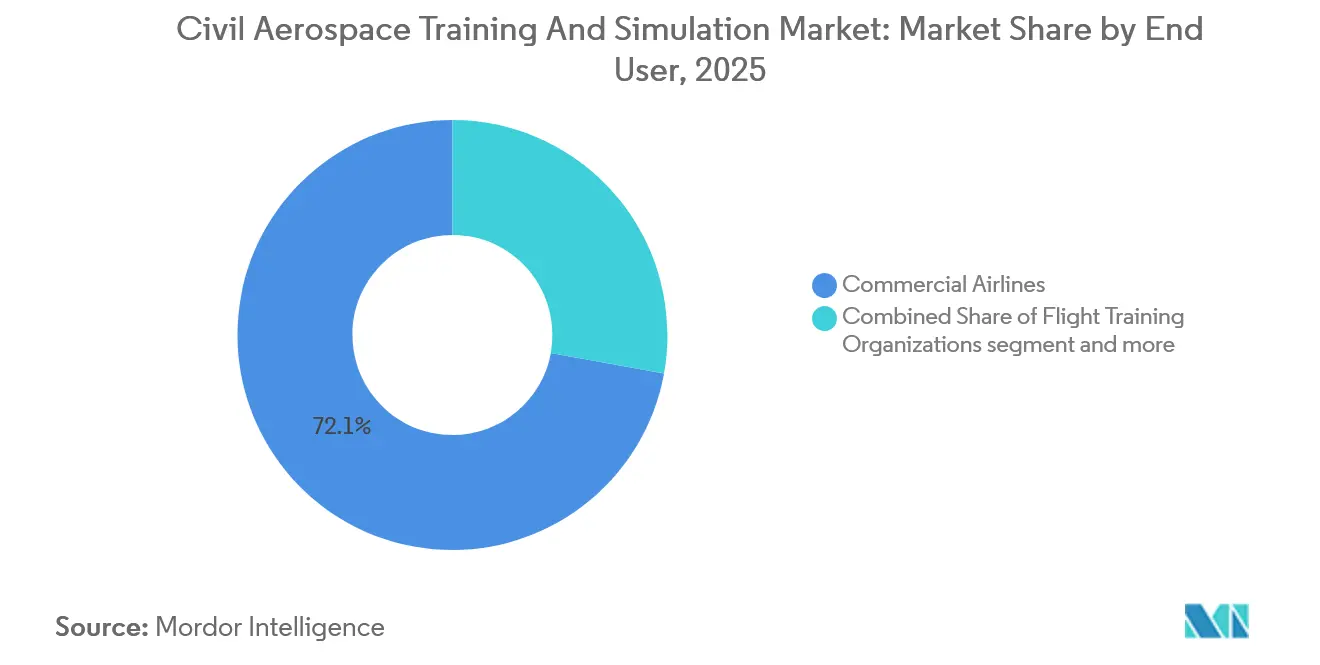

- By end user, commercial airlines accounted for 57.24% of spending in 2025; space agencies represented 7.82% and are the fastest-growing cohort through 2031.

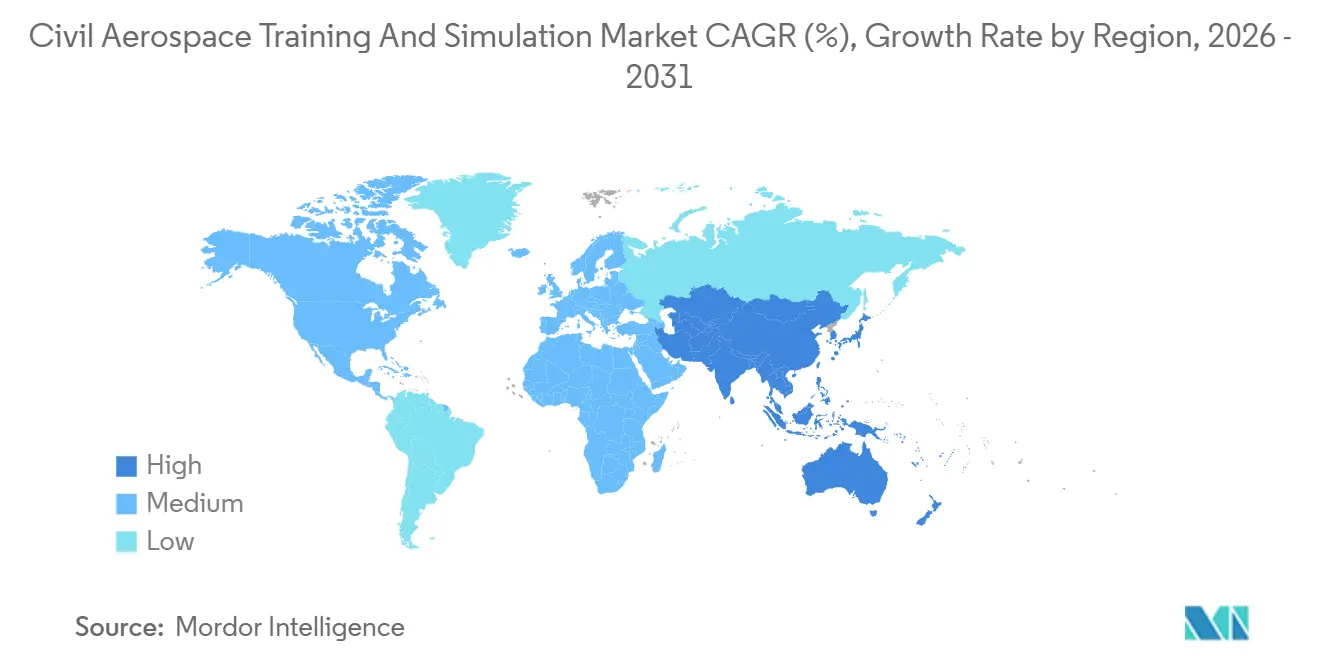

- By geography, North America dominated the market with 47.17% in 2025; however, the Asia-Pacific region is expected to record a brisk 7.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Civil Aerospace Training And Simulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global demand for trained pilots, technicians, and cabin crew | +2.1% | Asia-Pacific, Middle East, spill-over to Africa | Medium term (2–4 years) |

| Increasingly stringent safety and regulatory training requirements | +1.2% | North America, European Union, cascading to Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Cost advantages of simulation-based training compared to live aircraft operations | +1.6% | Europe, Japan, Africa, South America | Short term (≤ 2 years) |

| Growing adoption of VR- and AR-based portable simulators for early stage training | +1.5% | North America, European Union, China, India, South Korea | Short term (≤ 2 years) |

| Use of digital twin technologies to personalize and optimize training outcomes | +1.3% | North America, Western Europe, Singapore, Japan, Australia | Medium term (2–4 years) |

| Expansion of airline fleets and introduction of new aircraft types increasing transition training needs | +1.8% | Asia-Pacific, Middle East, global fleet operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for Trained Pilots, Technicians, and Cabin Crew

The worldwide fleet expansion has outpaced the talent pipelines. Boeing’s 2025 outlook indicated a need for 649,000 new commercial pilots by 2043, with 42% of them located in the Asia-Pacific region. China aims to recruit an additional 100,000 pilots by 2035 to operate nearly 4,930 transport aircraft. India’s airlines ordered more than 1,000 narrowbody jets between 2023 and 2025, forcing carriers to reserve simulator slots years in advance.[1]Directorate General of Civil Aviation India, “Annual Report 2024-2025,” dgca.gov.in Maintenance technicians also require recurrent composite repair and avionics updates for new-generation airframes, while cabin crews must certify in high-density evacuation procedures. These combined needs funnel students into the civil aerospace simulation and training market far more quickly than legacy training centers can scale, fueling demand for both fixed-site Level-D devices and mobile VR units that alleviate peak load.

Growing Adoption of VR- and AR-Based Portable Simulators for Early Stage Training

Head-mounted displays are shifting ab-initio curricula from brick-and-mortar schools to modular spaces. Loft Dynamics gained EASA approval in 2024 for an untethered VR helicopter simulator that operators can deploy aboard offshore platforms or in temporary classrooms. CAE’s 2025 rollout of the CAE Rise augmented-reality suite overlays checklists onto cockpit mock-ups, thereby reducing cognitive load during the first 50 hours of training. The US Air Force’s Pilot Training Next project cut time-to-wings by 30%, a metric that civilian schools emulate to accelerate throughput. VR devices cost barely 2% of a Level-D simulator, enabling smaller academies to tap into the civil aerospace simulation and training market without incurring heavy debt. Airlines in secondary cities now lease such equipment to pre-screen cadets, freeing full-motion bays for high-stakes checks.

Use of Digital Twin Technologies to Personalize and Optimize Training Outcomes

FlightSafety integrated Honeywell’s Forge engine into its A320 simulators in 2025 to capture eye-tracking and stress biomarkers, allowing difficulty levels to adapt in real time. Thales deployed a similar machine-learning feedback system for Air France, forcing the repetition of recurrent errors until pilots reached proficiency thresholds.[2]Thales Group, “TopSky Training Suite Deployment,” thalesgroup.com NASA’s Artemis simulators replicate real-time spacecraft telemetry, allowing astronauts to rehearse abort scenarios under authentic fault conditions. Airlines report that competency-based progress reduces type-rating hours to 32 from 40, allowing pilots to return to revenue flying sooner. These efficiencies strengthen the civil aerospace simulation and training market by converting fixed training budgets into higher student volume without raising capital expenditures.

Expansion of Airline Fleets and Introduction of New Aircraft Types Increasing Transition Training Needs

Boeing delivered 528 jets in 2025, including the first BB777-9, which features touchscreen avionics that differ markedly from the legacy widebody layouts. Airbus shipped 735 aircraft and debuted the A321XLR, whose extended-range fuel-management protocols require new certification modules. Each new cockpit architecture obliges airlines to order a dedicated full-flight simulator, generating steady replacement demand in the civil aerospace simulation and training market. Regional carriers adopting Embraer E2 and Comac C919 variants face the same constraint, often relying on manufacturer-run centers that bundle training with aircraft purchase. Consequently, simulator OEMs book multi-year backlogs, locking in revenue visibility through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs associated with full flight and Level-D simulators | -0.9% | Emerging markets in Africa, South America, Southeast Asia | Long term (≥ 4 years) |

| Regulatory certification and approval backlogs delaying simulator deployment | -0.8% | European Union, United States, dual-certification seekers in Asia-Pacific | Medium term (2–4 years) |

| Rising cybersecurity and data-protection costs for cloud-connected training systems | -0.6% | European Union, North America, growing scrutiny in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Limited availability of qualified simulator instructors and examiners constraining training capacity | -0.7% | Asia-Pacific (India, China, Indonesia), Africa, secondary markets in North America and EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs Associated with Full-Flight and Level-D Simulators

A Level-D simulator for aircraft such as the B737 MAX or A320neo involves significant capital investment and recurring maintenance costs, reflecting the advanced technical requirements of these aircraft. Banks in Southeast Asia and Africa demand pre-sold hours as collateral, yet airlines hesitate to sign lengthy contracts without proof of availability, trapping small schools in a financing loop. Leasing eases capital expenditures but carries rate premiums that erode thin margins. For widebody simulators, utilization below 4,000 hours turns the asset uneconomic, concentrating capacity in megahubs and leaving outlying regions underserved.

Limited Availability of Qualified Simulator Instructors and Examiners

Global examiner numbers rose only 2% in 2025 against a 6% jump in pilot candidates.[3]International Civil Aviation Organization, “Global Aviation Training Report 2025,” icao.int India alone had a 3,200-pilot waitlist for type rating check-ride slots despite open simulator slots. US instructors earn significantly less than airline first officers, which limits their ability to move laterally into teaching. FlightSafety’s 2024 equity-linked hiring plan will take 18 months to lift capacity. During peak hiring periods, airlines retain seasoned captains for line flying, thereby compounding the bottleneck and restraining the expansion of the civil aerospace simulation and training market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Simulator Type: Full-Flight Dominance Meets Portable Disruption

Full-flight simulators accounted for 75.47% of the civil aerospace simulation and training market in 2025. Regulatory frameworks, such as FAA 14 CFR Part 60, compel their use for type ratings and recurrent checks, ensuring baseline demand even during traffic downturns. Yet, the civil aerospace simulation and training market size for other simulator types is projected to expand at a 7.24% CAGR, reflecting airlines' shifting of ab-initio and refresher tasks to VR headsets and fixed-base devices.[4]Loft Dynamics, “EASA Certification Press Release,” loftdynamics.com

Growth in portable systems reduces capital intensity while widening geographic reach. Loft Dynamics' untethered platform eliminates hydraulic motion and fits inside shipping containers for pop-up classrooms. Redbird Flight Simulations logged a 40% rise in fixed-training-device orders among US Part 141 schools in 2025. As regulators gradually credit more synthetic hours, the civil aerospace simulation and training market gains a two-tier structure: high-fidelity bays for high-stakes checks and scalable VR labs for volume throughput.

By Application: Commercial Scale Versus Space Velocity

Commercial aviation generated 72.13% of 2025 revenue, supported by active airframes that require more than 10,000 simulator hours annually. Airlines replace motion systems every 10-12 years to keep pace with cockpit software baselines, cushioning OEM order books. The civil aerospace simulation and training market size for space applications, while much smaller, is expanding at a 7.11% CAGR as NASA, SpaceX, and Blue Origin commission bespoke lunar, docking, and microgravity trainers.

Space simulators differ fundamentally from aircraft simulators, modeling one-sixth gravity dynamics and several-second communication latency. ESA’s Columbus module upgrade in 2025 incorporated fluid-dynamics emulation, allowing astronauts to rehearse capillary-action experiments. Commercial providers see early opportunity in sub-orbital tourist briefings, where fixed-base cabins run high-volume familiarization loops. Over the decade, space could represent a meaningful share of civil aerospace simulation and training market growth if funding for Artemis follow-on missions and private stations stays intact.

By End User: Airlines’ Volume Versus Space Agencies’ Urgency

Commercial airlines accounted for 57.24% of spending in 2025, reflecting their fleet size and the legally mandated six- to twelve-month proficiency cycles. A simulator, operating extensively at a defined hourly rate, amortizes within a standard four-year period, reinforcing internal procurement strategies for major carriers such as Emirates and United. Flight training organizations occupy the middle ground, capturing cadets and regional pilots but suffering a margin squeeze when airlines insource capacity.

Space agencies, though only 7.82% of 2025 dollars, post the fastest rise as Artemis and Gaganyaan compress development timelines. ISRO’s contract with Thales for a Gaganyaan crew-module simulator highlights the premium agencies pay for mission-specific fidelity. As more governments fund lunar surface and Mars flyby concepts, the civil aerospace simulation and training market is poised to gain high-value, low-volume orders that balance commercial cyclicality.

Geography Analysis

North America retained 47.17% of the 2025 revenue, driven by OEM clusters, a dense network of over 200 training centers, and FAA rules that allow up to 50% of recurrent checks to be credited to simulators. Utilization frequently exceeds 5,000 hours per device per year, ensuring swift payback and steady aftermarket demand for software refreshes. Growth moderates toward replacement of aging bays rather than greenfield builds, with incremental upside tied to 777X and eVTOL simulator launches.

The Asia-Pacific is the locomotive of the civil aerospace simulation and training market, forecasted to grow at a 7.75% annual rate to 2031, as China, India, Indonesia, and Vietnam embark on historic fleet expansions. Beijing funds concessional loans that cut interest costs for training academies, while India’s 100% FDI allowance spurred a CAE-InterGlobe joint venture in 2024 with eight simulators online in Delhi and Bangalore. Indonesia’s Lion Air ordered six 737 MAX devices in 2025, citing the logistical advantage of localizing type-rating capacity.

Europe, under EASA, exhibits lower headline growth but steady revenue from the five-year revalidation cycle, which compels upgrades to match aircraft software baselines. Middle East mega-carriers operate captive centers that also serve as third-party hubs for African and South Asian pilots, leveraging geographic centrality to achieve high-yield utilization. Africa remains under-penetrated after South African Airways shuttered its Johannesburg center, forcing trainees to travel abroad, an expense that dampens demand. South America is concentrated in Brazil, where Azul sustains a small but profitable cluster of A320 and 737 simulators in São Paulo.

Regulatory Landscape

Regulatory requirements continue to anchor demand for qualified flight simulation training devices (FSTDs) while pushing providers toward more performance-based device validation. In the United States, FAA 14 CFR Part 60 governs initial and continuing qualification and use of FSTDs, setting the compliance baseline for type rating and recurrent training programs in a market where full flight simulators represented 75.47% of 2025 revenue.

In Europe, the regulatory framework moved in April 2026 with Commission Implementing Regulation (EU) 2026/781, which amended key aircrew and air operations rules (Regulations (EU) No 1178/2011 and (EU) No 965/2012) to update FSTD requirements and introduce an FSTD Capability Signature (FCS) approach. This shift supports a task-to-tool methodology, requiring training organizations and simulator OEMs to document objective evidence that device capabilities align with specific training and checking tasks, rather than relying only on legacy device-type or level labels. At the global level, ICAO discussions, including the May 2026 NACC/DCA meeting, on updates to Doc 9625 underscore that harmonization across national CAAs still depends on sequential domestic rulemaking and implementation support workflows.

Value Chain Analysis

The value chain spans aircraft and simulator OEMs, sub-system and software suppliers (visual systems, image generators, avionics and flight models, instructor operating stations), qualification and compliance services, and end users that monetize utilization through internal training and third-party hour sales. OEMs and large integrators such as CAE, Thales, RTX, and FlightSafety typically bundle hardware delivery with long-term services (maintenance, software baseline updates, spares, and instructor resources), while airlines and training organizations secure capacity via multi-year training service agreements. Cebu Pacific extending its training service agreements with CAE in February 2026, and Boeing licensing its Virtual Airplane training platform to Alaska Airlines in May 2026, illustrate how the model supports both hardware delivery and software-led training elements upstream of full-motion sessions.

Downstream, the chain is increasingly shaped by localized training-center build-outs and programmatic procurement that locks in demand visibility for suppliers. CAE and InterGlobe inaugurated a Mumbai pilot training center in April 2026 with an initial A320 full-flight simulator and planned capacity for additional devices. CAE also won a July 2026 contract to supply Boeing 737 MAX and 787 full-flight simulators to Royal Air Maroc's CasaAero facility, reinforcing the equipment-to-services lifecycle (delivery, qualification, sustainment, and instructor staffing). Alongside these civil dynamics, large training-system sustainment awards, for example Boeing's June 2026 IDIQ award for P-8A training systems, continue to pull simulator technology, visuals, and data management capabilities through adjacent procurement channels that many suppliers also serve.

Competitive Landscape

The civil aerospace simulation and training market remains moderately concentrated, with CAE Inc., FlightSafety International Inc., RTX Corporation, Thales Group, and TRU Simulation + Training Inc. collectively accounting for the majority of market share. These incumbents anchor long-term service contracts that bundle hardware sales with maintenance, updates, and instructor staffing, yielding sticky cash flows; the majority of CAE’s 2024 civil revenue is derived from services rather than product sales.

Challengers exploit software innovation. Loft Dynamics offers an EASA-approved VR platform that bypasses motion systems, slashing capital outlay by 80% and opening up white space in remote locations. Collins Aerospace filed a 2025 patent for a holographic-display hybrid simulator that preserves tactile feedback while halving the floor space needed. Cybersecurity compliance becomes a competitive lever; large providers absorb thousands of annual costs to satisfy NIST and prospective EASA Part-IS rules, cost levels that smaller firms struggle to meet.

Airlines are also entering the fray. Emirates invested USD 200 million in an 11-bay Dubai center that sells surplus hours to third parties, while United Airlines added 12 devices in 2024 to accommodate a 500-aircraft backlog. Such insourcing limits addressable hardware sales for OEMs but expands aftermarket opportunities in parts and software, keeping overall civil aerospace simulation and training market revenue on an upward slope.

Civil Aerospace Training And Simulation Industry Leaders

CAE Inc.

FlightSafety International Inc.

Thales Group

RTX Corporation

TRU Simulation + Training Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace remains in expanding training capacity outside traditional megahubs while preserving access to qualified devices and certified instructors. India is a clear focal point for localized infrastructure: CAE and InterGlobe added a fourth pilot training center in Mumbai in April 2026 with an initial A320 full-flight simulator and planned capacity expansion, and Airports Authority of India initiated an RFP in July 2026 to appoint a consultant to develop a strategy for establishing Full Flight Simulator (FFS) and Type Rating Training Organisation (TRTO) facilities across its airport network. In parallel, Simaero announced in July 2026 a 200 million euro, ten-year investment plan for its India operations to scale simulator footprint at its Gurugram facility, signaling continuing openings for OEMs, independent training centers, and financing and leasing partners as new devices are placed closer to demand.

The shift in qualification philosophy also creates opportunity for software-defined and modular training architectures that optimize expensive full-flight simulator utilization. EASA's move toward an FSTD Capability Signature (FCS) and task-to-tool methodology, together with airline adoption of digital training tools, supports hybrid curricula where cloud-based procedural trainers and immersive systems handle early and recurrent task blocks before pilots enter full-motion sessions. Airbus reinforced this direction by opening a new flight operations and training campus in Toulouse in February 2026 with seven full-flight simulators and a stated 50% increase in trainee capacity, and by highlighting in June 2026 the role of digital tools such as the Virtual Procedure Trainer to bridge procedural learning and high-fidelity simulator time. As standards and operating models evolve, dedicated technical forums such as APATS adding a specialized FSTD Operators Regulatory Stream for 2026 further indicate sustained demand for compliance, device-qualification expertise, and cybersecurity-ready, connected training environments.

Recent Industry Developments

- July 2026: CAE announced a contract to supply Boeing 737 MAX and 787 full-flight simulators to Royal Air Maroc's CasaAero training facility. The win strengthens CAE's footprint in airline-operated centers and extends the services tail tied to qualification, spares, and software baseline support around new devices.

- June 2026: Thales partnered with Airbus Helicopters and HELISIM to achieve FAA Level D certification for an upgraded H145 D3 full-flight simulator with enhanced night vision goggle (NVG) training capability. The certification expands the addressable training syllabus that can be delivered in-simulator and reinforces the role of regulator-approved upgrades as a lever for utilization and revenue per device.

- December 2025: HAVELSAN signed an agreement with Boeing to integrate the B737 MAX-8 full-flight simulator into its production line using a Boeing simulation data package procured directly. The move enhances HAVELSAN's technical capability and highlights how access to OEM data packages influences simulator development timelines and certification readiness.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending linked to civil aerospace simulation and training used to prepare and maintain proficiency for civil aviation and related civil space operations. It includes simulator equipment and training delivery where that activity is part of the supplier offering.

Scope exclusions: We exclude military-only training programs and defense simulators that are procured and used strictly for military missions.

Segmentation Overview

- By Simulator Type

- Full Flight Simulator (FFS)

- Flight Training Devices (FTDs)

- Other Simulator Types

- By Application

- Commercial Aviation

- Space

- By End User

- Commercial Airlines

- Flight Training Organizations

- Space Agencies

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, align definitions across regions, and build a starting view of demand drivers and constraints. We relied on public aviation and labor outlooks, such as those published by global civil aviation bodies, along with air transport statistics and safety and training guidance issued by regulators.

To make the sizing inputs practical, we also reviewed sources such as aircraft fleet and delivery disclosures, airline annual reports and investor presentations, airport and airline traffic releases, and training organization updates. Where needed, a paid subscription for company financials and intelligence was used to understand revenue mix patterns, and a separate patent database subscription was referenced to sanity-check adoption direction for training technologies. These desk sources are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with airline training leaders, flight training organizations, simulator operations teams, and supporting ecosystem roles that influence simulator procurement and training throughput. We covered demand signals across APAC, EMEA, and the Americas, so assumptions like simulator utilization, training hour mix, and replacement timing could be checked against how programs run in each market.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 46% |

| Mid tier: 45% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 18% | Managers: 58% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts from a top-down rebuild of the addressable training demand pool, where fleet growth and aircraft deliveries are connected to training cycles and required training hours, then translated into simulator capacity needs and related spending. The totals are corroborated with selective bottom-up approximations, such as sampled simulator pricing ranges and delivery cadence, plus channel checks on training hour pricing and simulator utilization. This supports adjustments when any single data stream under-represents the real operating constraint.

In the model, a few variables are treated as the main dials, including active commercial fleet, new aircraft inductions by region, pilot and crew hiring needs, recurrent training frequency, simulator utilization rates, and mix shifts between full flight simulators and other devices. When a bottom-up input is missing for a smaller geography, a proxy is applied using nearby fleet and training intensity, then pressure-tested through primary responses.

For forecasting, scenario analysis is used so the base case reflects expected fleet and traffic recovery paths, training capacity expansion plans, and technology adoption timing (such as more simulator-based checks). Expert feedback is used to select realistic ranges for utilization and pricing progression, and the final path is kept consistent with observable aviation cycle indicators.

Data Validation & Update Cycle

Outputs are triangulated against independent signals, such as changes in fleet size, training capacity announcements, and public hiring and traffic indicators, so the model does not drift away from real operating constraints. Variance checks are run at region and segment levels, followed by analyst review steps where outliers are investigated, and assumptions are either tightened or revalidated.

When large mismatches appear, we re-contact relevant respondents to understand whether it is timing, scope interpretation, or a one-off event causing the shift. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery check is done so the client view reflects the latest available market context.

Mordor Intelligence's Civil Aerospace Simulation and Training Market Size Compared With Other Published Estimates

Published market values for civil aerospace simulation and training can look far apart because analysts do not always count the same spend buckets, and timing choices around the base year can change the number being compared. Differences also come from how much of training services gets counted versus only simulator equipment, and whether civil space related training is included in the same pool.

The table shows a wide spread mainly because some estimates expand the scope to adjacent training spend categories and apply higher blended price assumptions across devices and services. Under Mordor Intelligence's model, the value is aligned to civil aerospace simulation and training with simulator types and related training devices, and it is reported with a 2026 base year that is validated against utilization and training cycle realities rather than assuming uniform growth across all training spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.07 B (2026) | |

| Industry Research Publisher A | USD 1.94 B (2025) | Uses a different base year and can shift totals by counting 2025 as the anchor, which changes how fleet cycle and training recovery timing are reflected in the starting value. |

| Global Consultancy B | USD 6.80 B (2024) | Appears to use a broader spend scope and a higher blended value pool, which can happen when wider civil training services and adjacent categories are rolled up beyond simulator and training device focused definitions. |

Looking across the three figures, the largest driver is scope, followed by the chosen base year and the implied pricing and utilization assumptions behind each estimate. By keeping inputs tied to fleet, training cycles, and simulator capacity signals, the resulting number stays traceable and easier to repeat when new demand data becomes available.

Key Questions Answered in the Report

What is the current value of the civil aerospace simulation and training market?

It is valued at USD 2.07 billion in 2026 and is projected to hit USD 2.90 billion by 2031.

How fast is the market expected to grow?

The forecast CAGR is 6.98% between 2026 and 2031.

Which simulator category dominates spending?

Full flight simulators hold 75.47% of 2025 revenue due to regulatory mandates.

Which region will add the newest simulator capacity?

Asia-Pacific, driven by China’s and India’s pilot-production targets, is forecast to grow at 7.75% a year through 2031.

What is the biggest restraint on market expansion?

High capital costs for Level D devices restrict adoption in emerging markets.

Which technology is cutting training hours the most?

Digital-twin analytics embedded in simulators are reducing type-rating time by up to 20%.

Page last updated on: