Market Overview

| Study Period | 2021 - 2031 |

|---|---|

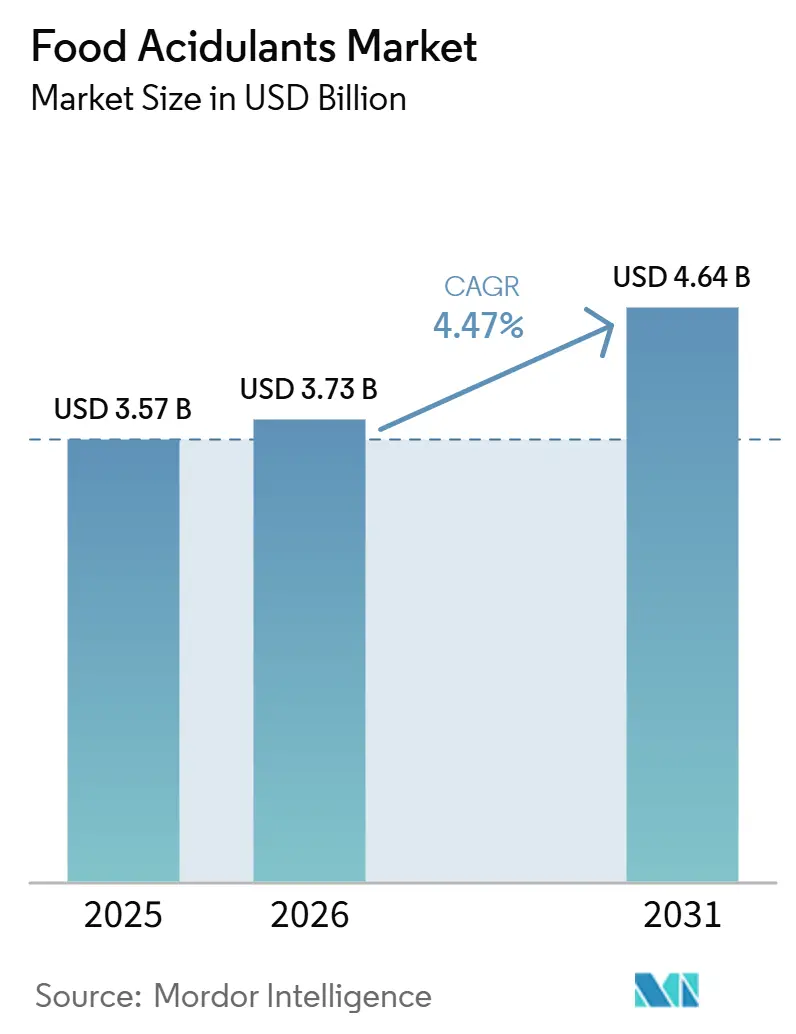

| Market Size (2026) | USD 3.73 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Acidulants Market Analysis by Mordor Intelligence

The food acidulants market size was valued at USD 3.57 billion in 2025 and estimated to grow from USD 3.73 billion in 2026 to reach USD 4.64 billion by 2031, at a CAGR of 4.47% during the forecast period (2026-2031). This growth is primarily driven by the implementation of stricter global food-safety regulations, increasing consumer preference for clean-label formulations, and the expanding adoption of processed foods in emerging economies. Regulatory developments in key regions, including China, the European Union, and Canada, present both challenges and opportunities for the adoption of naturally derived acidulants. Concurrently, innovations in bio-based production technologies are playing a pivotal role in reducing the carbon footprint associated with the production of citric, lactic, and succinic acids. Supply-chain vulnerabilities, particularly fluctuations in corn prices, are prompting manufacturers to diversify raw material sources, with a growing focus on cassava, sugarcane, and biowaste substrates. The competitive landscape is characterized by significant consolidation, exemplified by Tate and Lyle’s acquisition of CP Kelco. Additionally, strategic investments in fermentation-based production assets are enhancing the industry’s application-development capabilities, particularly in high-demand segments such as beverages, bakery products, and plant-based meat alternatives.

Key Report Takeaways

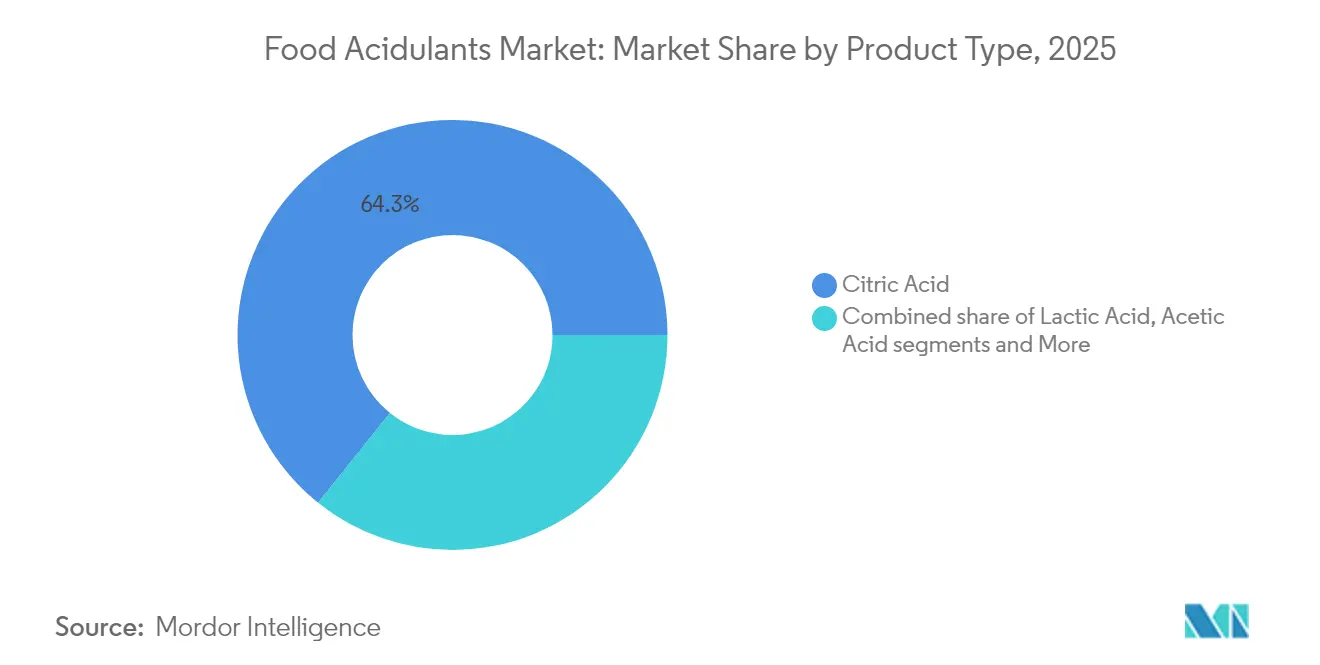

- By type, citric acid led with 64.25% of food acidulants market share in 2025; succinic acid is projected to grow at 9.93% CAGR through 2031.

- By source, the synthetic segment accounted for 71.05% of the food acidulants market size in 2025, while bio-based alternatives are set to expand at 9.23% CAGR to 2031.

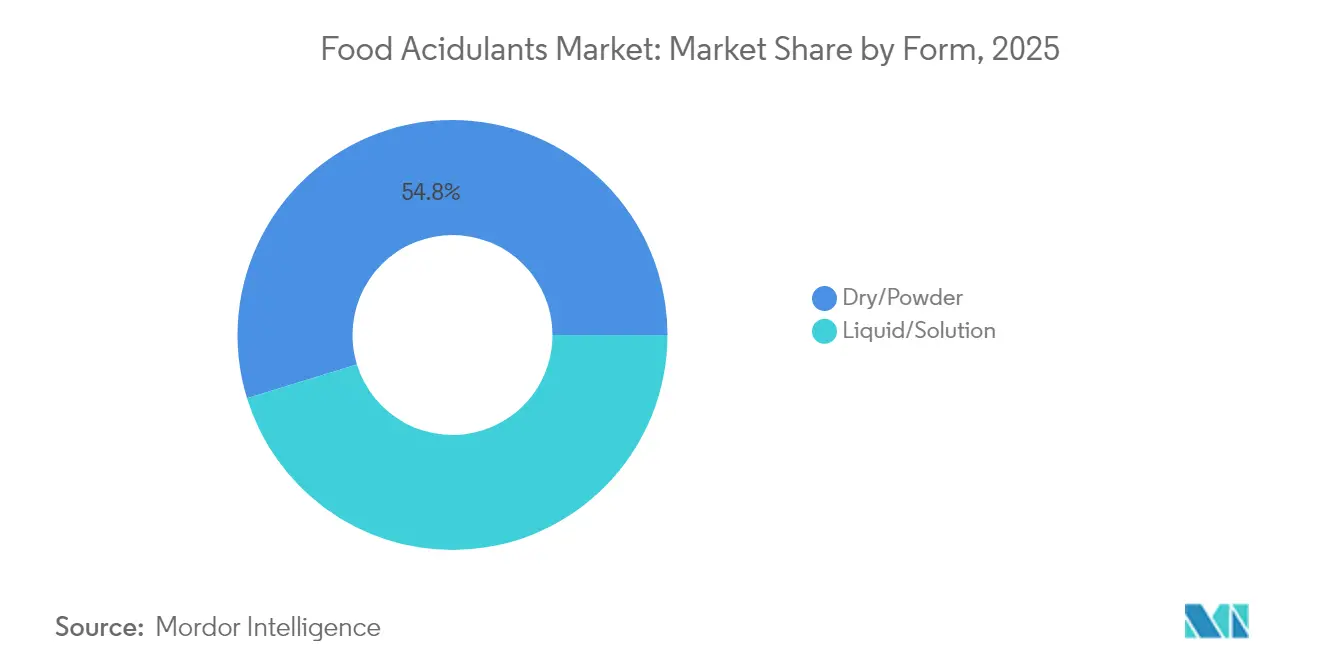

- By form, dry/powder products held 54.75% revenue share in 2025; liquid/solution formats are progressing at a 6.69% CAGR.

- By application, beverages captured 34.25% of the food acidulants market share in 2025, whereas plant-based meat and seafood applications are advancing at 11.78% CAGR through 2031.

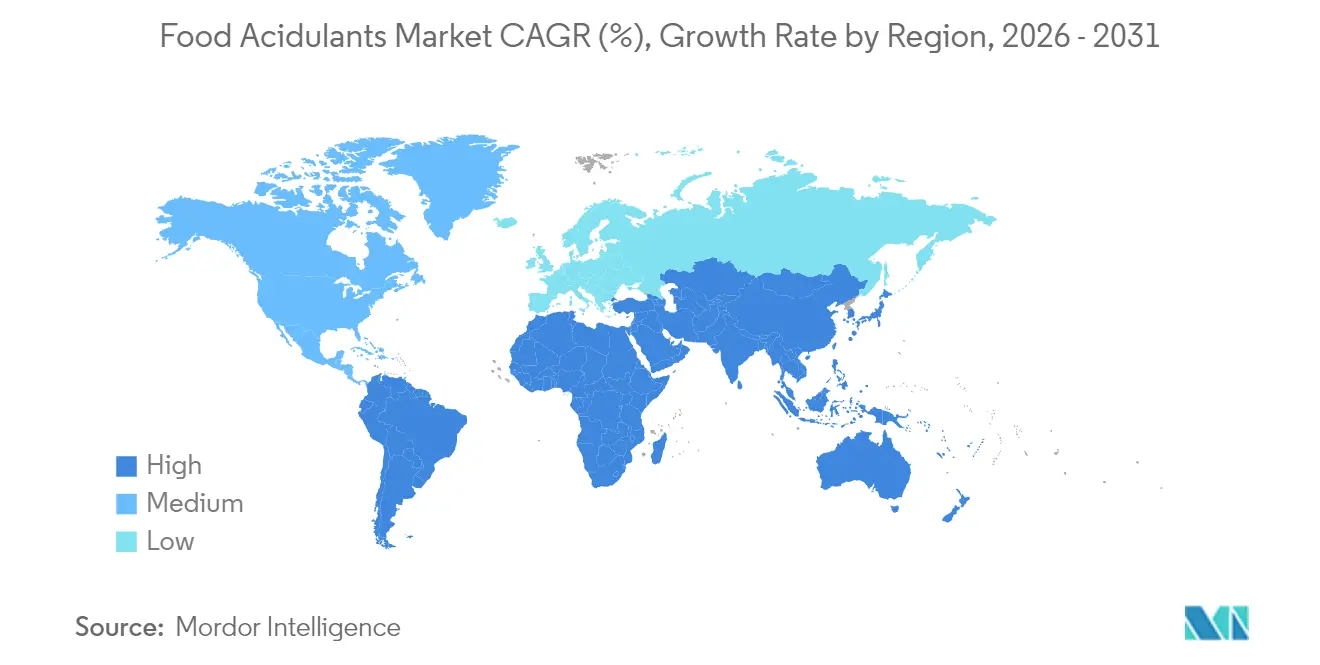

- By geography, Asia-Pacific commanded 39.35% share of the food acidulants market in 2025; the Middle East and Africa are forecast to record an 8.21% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Acidulants Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing interest in natural and clean-label ingredients | +1.2% | North America and Europe strongest | Medium term (2-4 years) |

| High demand for processed and convenience foods. | +0.8% | Asia-Pacific core; Middle East and Africa spill-over | Long term (≥ 4 years) |

| Shelf-stable plant-based meat demand boosting lactic and fumaric usage | +0.6% | North America and Europe expanding to Asia-Pacific | Short term (≤ 2 years) |

| Cola brand investments in low-sugar CSDs increasing phosphoric/malic uptake | +0.4% | Global urban markets | Medium term (2-4 years) |

| Emphasis on food safety and regulatory compliance. | +0.3% | Global | Long term (≥ 4 years) |

| Rising consumer preference for enhanced flavor profiles is driving the demand for food acidulants. | +0.2% | Global premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing interest in natural and clean-label ingredients

With a growing emphasis on ingredient transparency, bio-based citric, malic, and lactic acids are increasingly securing premium-priced contracts. The European Food Safety Authority (EFSA) has introduced revised guidance on novel foods, which will come into effect in February 2025. This updated framework is streamlining the approval process for fermentation-derived acids, thereby accelerating their path to commercialization. Jungbunzlauer, a key player in the market, has strategically prioritized naturally fermented citric acid, enabling the company to establish supply agreements with European beverage manufacturers that require GRAS-certified ingredients. The demand for clean-label products is particularly strong in categories such as sparkling water, functional shots, and premium juices, where apple-derived malic acid plays a pivotal role in enhancing flavor profiles. Although scaling up fermentation capacity remains a capital-intensive endeavor, companies with robust biobased portfolios are successfully capturing higher margins, which help mitigate the impact of rising raw material costs.

High demand for processed and convenience foods

Urbanization and evolving lifestyles in the Asia-Pacific and Middle East regions are driving a significant increase in the demand for shelf-stable food products, including noodles, sauces, and ready-to-eat rice bowls. This sustained demand has resulted in consistently high baseline consumption of citric and acetic acids. In China, the implementation of GB 2760-2024 has introduced stricter regulations on synthetic preservatives while simultaneously expanding the permissible applications for organic acids. This regulatory shift has led to a notable rise in orders from domestic food processors. Furthermore, the lactic-acid bacteria can effectively mitigate off-flavors in plant-based dairy products, thereby unlocking new opportunities for value creation in this segment. Additionally, regional taste preferences, such as the tamarind-associated tartness popular in South Asia, are driving the development of customized acidulant blends tailored to local palates. To address the challenges posed by raw material price volatility, multinational corporations are implementing hedging strategies and diversifying their sourcing approaches by utilizing multiple feedstocks.

Shelf-stable plant-based meat demand boosting lactic and fumaric usage

Precision fermentation is driving innovation in acidulant applications within alternative protein production. Lactic and fumaric acids have become essential for developing texture and ensuring preservation in plant-based meat substitutes. A demographic shift is occurring, characterized by changes in dietary preferences and lifestyle choices influenced by health awareness, environmental sustainability, and ethical considerations. According to the Good Food Institute, in 2024, approximately 40% of adults in Germany and the UK plan to increase their consumption of plant-based foods. Health-related factors account for 48% of this shift, while environmental concerns represent 29%, and animal welfare considerations make up 25%[1]Source: Good Food Institute, "State of the Industry 2024", www.gfi.org. Lactic and fumaric acids are critical for pH control, texture enhancement, and microbial stability in ambient vegan jerky and canned meat substitutes. Findings from Novonesis indicate that these acids enhance umami and kokumi flavors, effectively narrowing the taste gap with animal proteins. To maintain label claims, brands are prioritizing organic-certified acids and favoring suppliers with audited fermentation practices.

Cola-brand investments in low-sugar CSDs increasing phosphoric/malic uptake

Beverage giants are reformulating their core SKUs to align with sugar-reduction taxes. They're adding phosphoric or malic acid to counterbalance the reduced sweetness. As awareness of enamel erosion grows, there's increasing pressure on the use of phosphoric acid. This has led to a trend of partially substituting it with malic acid, especially in premium sodas. While the FDA still recognizes phosphoric acid as GRAS, shifting sentiments on social media are nudging corporations towards fruit-derived acids. Citric acid, in particular, is gaining prominence in organic carbonated soft drinks (CSDs), where it plays a dual role in maintaining pH balance and supporting clean-label initiatives, which are increasingly valued by health-conscious consumers. In response to these evolving market dynamics, suppliers are prioritizing innovation by developing acidulant solutions with low-impurity profiles and offering customized blends tailored to the specific needs of beverage manufacturers. These advancements aim to address both functional requirements and the growing demand for cleaner, more natural ingredient options in the beverage industry.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Corn price volatility post Black-Sea disruptions squeezing citric margins | -0.7% | Global corn-dependent regions | Short term (≤ 2 years) |

| Sub-Saharan cold-chain gaps limiting acidulants in chilled dairy drinks | -0.3% | Sub-Saharan Africa; rural Asia-Pacific | Long term (≥ 4 years) |

| U.S. consumer enamel-erosion concerns curbing phosphoric acid in CSDs | -0.4% | North America spreading to Europe | Medium term (2-4 years) |

| Stringent regulatory frameworks on food additives are posing challenges to the growth of the food acidulant market | -0.2% | Europe, with global spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corn price volatility post Black-Sea disruptions squeezing citric margins

Citric-acid fermenters primarily rely on corn steep liquor as a key input; however, disruptions in supply chains caused by war-related events have significantly increased corn prices. In the United States, domestic production capacity fulfills only one-third of the total demand, thereby intensifying the country's dependence on imports to bridge the gap. Smaller processors, particularly those without hedging mechanisms in place, are disproportionately affected by these cost escalations, leaving them vulnerable to operational shutdowns or potential acquisitions by larger entities. Although alternative substrates, such as cassava, present a possible solution, their adoption necessitates re-validation processes and substantial capital expenditure, further straining short-term profitability. The persistent price pressures in the market are driving larger firms to pursue vertical-integration strategies, enabling them to secure upstream feedstock acreage and mitigate supply chain risks effectively.

Stringent regulatory frameworks on food additives posing challenges

As food safety authorities tighten approval processes and post-market surveillance for acidulants, global regulatory complexity is on the rise. These heightened measures lead to compliance costs that weigh heavily on smaller manufacturers. The European Commission, under Regulation (EU) 2024/2597, has updated purity criteria for sorbates, mandating fresh product testing and documentation. In a notable move, China has decided to ban dehydroacetic acid across several categories starting in 2025, highlighting the suddenness of regulatory shifts. Meanwhile, the FDA’s Human Foods Program is pledging to continuously re-evaluate legacy GRAS substances, further inflating compliance costs. Such regulatory disparities compel multinational corporations to juggle multiple SKUs, while smaller enterprises grapple with funding analytical verifications, hindering their pace in launching new products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Citric Acid Dominance Faces Bio-Based Disruption

In 2025, citric acid led the food acidulants market with a 64.25% share, supported by well-established supply chains and GRAS approvals across various jurisdictions. Succinic acid, though a niche segment, is experiencing a 9.93% CAGR (2026-2031), driven by fermentative processes that lower greenhouse gas emissions and facilitate its application in compostable packaging resins. Lactic acid, traditionally used for yogurt preservation, is expanding its applications to include vegan cheese and growth media for cultured meats. Phosphoric acid, despite facing regulatory challenges in cola formulations, remains functionally relevant.

Declining fermentation costs are enabling the emergence of alternatives. Bio-derived malic and fumaric acids are gaining traction in beverage and protein powder applications. The market for organic acids associated with plant-based meats is expected to grow significantly as precision fermentation capacity increases. Producers with expertise in metabolic engineering are diversifying their acid portfolios to reduce dependency on a single acid.

By Source: Synthetic Dominance Challenged by Sustainability Mandates

In 2025, synthetic routes accounted for 71.05% of the food acidulants market, reflecting the industry's long-standing dependence on petrochemical infrastructure. However, bio-based alternatives are experiencing significant growth, with a strong 9.23% CAGR (2026-2031), as brands increasingly aim to reduce their Scope 3 emissions. Corbion’s circular lactic-acid plant in Thailand serves as a prime example, utilizing renewable feedstocks and closed-loop wastewater recycling to support clients in meeting ESG disclosure requirements.

Bio-based suppliers are not only delivering environmentally friendly solutions but also providing carbon-footprint declarations, enabling them to secure contracts in premium segments such as beverages and baby foods. Although these bio-based options carry an average price premium of 20%, buyers justify the additional cost through improved eco-label positioning. Over time, economies of scale and the implementation of regulatory carbon taxes are expected to reduce pricing disparities, gradually shifting the food acidulants market toward fermentation-based solutions.

By Form: Liquid Solutions Gain Operational Efficiency

Dry powders retained a 54.75% share in 2025, prized for shelf stability in bakery mixes and powdered beverages. Despite this dominance, liquid solutions are experiencing notable growth, with a 6.69% CAGR (2026-2031), driven by their compatibility with automated dosing systems in high-throughput beverage production facilities. Jungbunzlauer’s LIQUINAT stands out in this segment, offering instant dissolution that not only reduces cleaning time but also minimizes the risk of inhalation during handling, making it a safer and more efficient option for manufacturers.

The bulk tanker delivery of liquid citric or lactic acid substantially reduces secondary packaging waste, aligning with corporate sustainability objectives. With the growth of continuous-processing lines in snacks and sauces, processors are increasingly adopting pre-blended liquid acid systems that integrate efficiently with CIP regimes. This transition enhances traceability through closed pipelines and strengthens quality control measures.

By Application: Beverages Lead While Plant-Based Segments Surge

In 2025, beverage producers accounted for 34.25% of the food acidulants market share, employing citric and phosphoric acids to balance sweetness and inhibit microbial growth. Energy drinks and sparkling waters utilize malic acid to enhance tartness. Although shelf-stable plant-based meats and seafoods represent a smaller market volume, they are growing rapidly at a 11.78% CAGR (2026-2031), with fumaric and lactic acids playing a critical role in stabilizing protein matrices. The beverage segment's dominance is further supported by the Union of European Beverage Associations' commitment to reducing sugar content by 10% by 2025, addressing both consumer health concerns and regulatory requirements.

In 2023, soft drink consumption in the European Union (EU) reached 51,905.7 million liters, according to UNESDA - the Union of European Soft Drinks Associations. Formulators leveraging lactic-acid fermentation create the characteristic tang in dairy-free yogurts, while fumaric acid prevents caking in high-protein powders. Increasing consumer interest in global cuisines continues to drive demand for acetic and tartaric acids in condiments. As a result, suppliers are developing multi-acid blends tailored to regional taste preferences and shelf-life requirements, strengthening customer relationships.

Geography Analysis

In 2025, Asia-Pacific held a leading 39.35% share of the food acidulants market, supported by China's extensive beverage and snack industries and India's rapidly growing packaged food sector. The Indian food processing industry plays a crucial role in the nation's economy, characterized by a strong export orientation and substantial growth opportunities. During 2023-24, the sector attracted USD 608 million in foreign direct investment. According to the Ministry of Commerce and Industry, processed food exports accounted for 23.4% of the country's total agricultural exports. Additionally, Southeast Asian processors benefit from regional trade agreements, driving increased intra-ASEAN beverage exports and boosting acidulant demand.

North America, though a mature market, continues to innovate, with clean-label carbonated soft drinks (CSDs) and plant-based meats driving incremental growth. The FDA's intensified oversight through its Human Foods Program has raised documentation requirements, favoring established players with comprehensive toxicological data. Meanwhile, domestic citric acid producers face margin pressures due to corn-price volatility, prompting diversification into alternative carbohydrate sources. In Europe, stringent additive regulations create a compliance barrier that supports premium pricing. While the European Food Safety Authority (EFSA) has streamlined approvals for naturally fermented acids, enabling easier market entry for bio-based suppliers, the purity standards outlined in Regulation (EU) 2024/2597 necessitate advanced analytical capabilities. Eastern European beverage manufacturers leverage lower operational costs and import acidulants from western facilities to meet EU harmonized standards. The Middle East and Africa region is experiencing the fastest growth, with a robust CAGR of 8.21% (2026-2031), driven by urbanization, the expansion of quick-service restaurants (QSRs), and rising disposable incomes. Although acidulant usage in fruit-based beverages and shelf-stable dairy products is increasing, cold-chain infrastructure gaps in Sub-Saharan Africa limit growth potential. However, government investments in cold storage infrastructure could unlock additional demand, particularly for lactic-acid-based stabilizers. In South America, regional soft-drink manufacturers are reformulating products in response to sugar taxes, replacing phosphoric acid with malic acid to align with health-conscious consumer preferences. Additionally, Brazil's thriving citrus industry strengthens domestic citric acid production, reducing reliance on imports and enabling competitive pricing across Mercosur markets.

Competitive Landscape

Globally, the food acidulants market faces moderate competition, with the presence of both global and local players. Several giant companies are investing huge amounts in research and development and also focusing extensively on providing consumers with innovative offerings while including functional benefits in each of their products. There are several local companies in each region that are intensely competitive with global players (as these manufacturers price their products lower than most global players). The major players, such as Jungbunzlauer Suisse AG, Cargill Incorporated, Adavancein Organics LLP, Archer Daniels Midland Company, and Corbion NV, are actively increasing production capacities to meet the rising demand of global consumers and to establish their presence in the market studied.

Additionally, regional companies adopted various strategies. For example, in November 2024, Tate and Lyle completed the acquisition of CP Kelco for USD 1.8 billion, expanding its portfolio of mouthfeel and acidulant solutions tailored for beverage clients. The post-merger integration focuses on fostering research and development collaboration, exemplified by the launch of a new automated laboratory in Singapore designed to accelerate prototype development. Corbion has commenced operations at a new circular lactic-acid facility in Thailand, utilizing renewable sugarcane feedstock to reduce Scope 3 emissions for global dairy and meat-alternative brands. At the same time, ADM faces reputational challenges due to ongoing accounting investigations, which may shift specialty-acid contracts toward competitors.

Technological innovation is centered on metabolic-engineering platforms that enhance the production yields of succinic and malic acids from non-food biomass. Companies adopting AI-driven process analytics are achieving superior impurity control, securing contracts in the infant-nutrition market. Additionally, strategic partnerships, such as Tate and Lyle’s collaboration with BioHarvest Sciences in botanical synthesis, are advancing hybrid ingredient systems that integrate sweeteners with acidulants to improve flavor modulation efficiency.

Food Acidulants Industry Leaders

-

Jungbunzlauer Suisse AG

-

Archer Daniels Midland Company

-

Corbion N.V.

-

Cargill Incorporated

-

Adavancein Organics LLP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Caitlyn India Pvt Ltd (CIPL) unveiled plans for a Rs 400 crore investment to set up a phosphoric acid plant in India, targeting an annual output of 50,000 tonnes. This initiative seeks to curtail import reliance and enhance the nation's fertiliser self-sufficiency. Strategically located in a port-accessible industrial zone in southern India, the plant will harness hemihydrate–dihydrate (HH-DH) technology, ensuring high-purity phosphoric acid and cleaner gypsum by-products.

- December 2024: Tate and Lyle have entered into a partnership with BioHarvest Sciences to leverage Botanical Synthesis technology for the development of next-generation plant-based ingredients, focusing on sustainable sweeteners and acidulants that optimize land and water usage.

- November 2024: Tate and Lyle has completed its USD 1.8 billion acquisition of CP Kelco, significantly enhancing its portfolio of nature-based ingredients. These include pectin and citrus fiber, which are essential for applications such as food preservation and texture modification. This strategic acquisition strengthens Tate and Lyle's ability to address the growing demand in the clean-label market and highlights the industry's focus on bio-based ingredient solutions.

- November 2024: INEOS Acetyls and Gujarat Narmada Valley Fertilizers & Chemicals Ltd (GNFC) inked an MoU, eyeing the feasibility of establishing a 600kt acetic acid plant at GNFC's Bharuch site in Gujarat, India.

Global Food Acidulants Market Report Scope

Acidulants are chemical elements that are being utilized to provide a tart flavor or a sharp taste to food and beverage items. The global food acidulants market is segmented based on type, application, and geography. By type, the food acidulants market is segmented into citric acid, lactic acid, acetic acid, phosphoric acid, malic acid, and other types. The application segment involves beverages, dairy and frozen products, bakery, meat industry, confectionery, and other applications. By geography, the market covers the major countries in North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. The report offers market size and forecasts for the food acidulants market in value (USD million) for all the above segments.

By Product Type

| Citric Acid |

| Lactic Acid |

| Acetic Acid |

| Phosphoric Acid |

| Malic Acid |

| Fumaric Acid |

| Succinic Acid |

| Tartaric Acid |

| Others (GDL, Gluconic, etc.) |

By Source

| Bio-based/Natural |

| Synthetic (Petro-/Corn-derived) |

By Form

| Dry/Powder |

| Liquid/Solution |

By Application

| Beverages |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Meat and Seafood |

| Sauces, Dressings and Condiments |

| Infant and Clinical Nutrition |

| Other Processed Foods |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pcific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Citric Acid | |

| Lactic Acid | ||

| Acetic Acid | ||

| Phosphoric Acid | ||

| Malic Acid | ||

| Fumaric Acid | ||

| Succinic Acid | ||

| Tartaric Acid | ||

| Others (GDL, Gluconic, etc.) | ||

| By Source | Bio-based/Natural | |

| Synthetic (Petro-/Corn-derived) | ||

| By Form | Dry/Powder | |

| Liquid/Solution | ||

| By Application | Beverages | |

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Meat and Seafood | ||

| Sauces, Dressings and Condiments | ||

| Infant and Clinical Nutrition | ||

| Other Processed Foods | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pcific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the food acidulants market?

The market is valued at USD 3.73 billion in 2026 and is projected to reach USD 4.64 billion by 2031.

Which segment holds the largest share of the food acidulants market?

Citric acid leads by type, accounting for 64.25% of market revenue in 2025.

What is driving the rapid growth of bio-based acidulants?

Clean-label demand and corporate sustainability mandates are encouraging food manufacturers to switch to fermentation-derived acids despite higher costs.

Why is Middle East & Africa the fastest-growing region?

Urbanization and rising processed-food consumption boost acidulant usage, delivering an 8.21% regional CAGR through 2031.

Page last updated on: