Circulating Fluidized Bed Boiler Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 0.99 Billion |

| Market Size (2030) | USD 1.17 Billion |

| Growth Rate (2025 - 2030) | 4.26% CAGR |

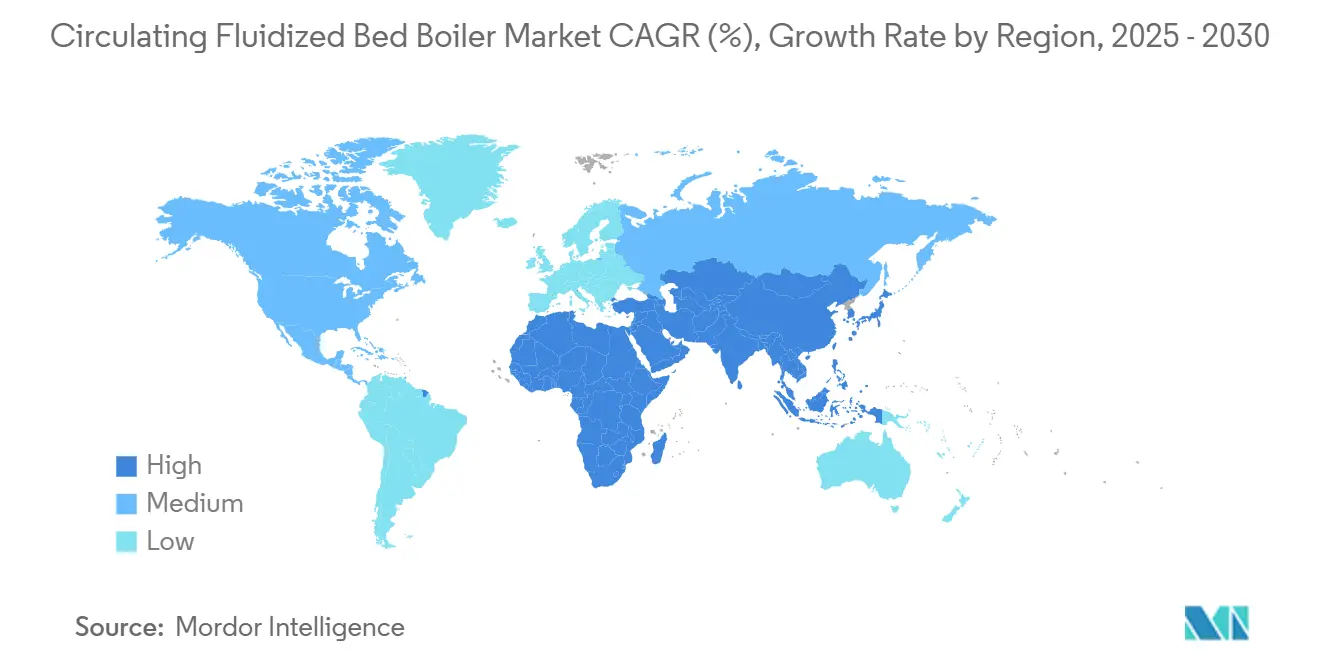

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

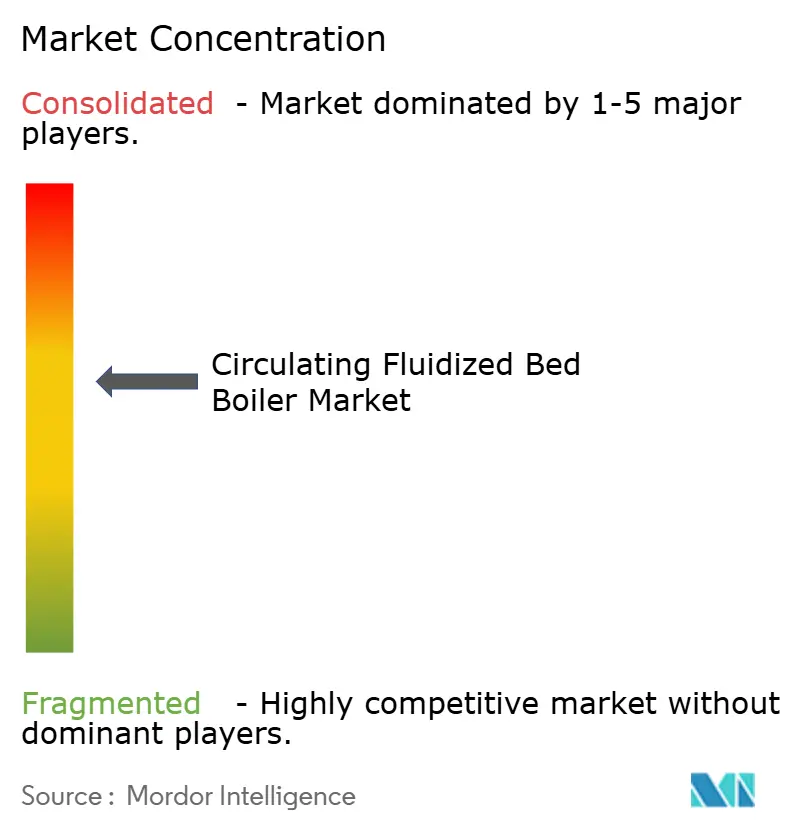

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Circulating Fluidized Bed Boiler Market Analysis by Mordor Intelligence

The Circulating Fluidized Bed Boiler Market size is estimated at USD 0.99 billion in 2025, and is expected to reach USD 1.17 billion by 2030, at a CAGR of 4.26% during the forecast period (2025-2030).

This steady expansion reflects the technology’s fit with stricter global air-quality rules, its capability to burn a wide range of fuels, and its rising adoption in power generation and industrial steam duties. Asia Pacific remains the demand anchor as utilities in China and India modernize coal fleets while adding super-critical and ultra-super-critical units that curb emissions and improve heat rates. Technology providers continue to prioritize material science advances that enable higher steam parameters, while industrial customers value circulating fluidized bed boiler market solutions that co-fire biomass, waste, and low-grade coal without costly downstream controls. Competitive positioning now hinges on in-house design depth, regional manufacturing footprints, and the breadth of after-sales service networks, with large contracts in India, Poland, and Canada underscoring the healthy project pipeline.

Key Report Takeaways

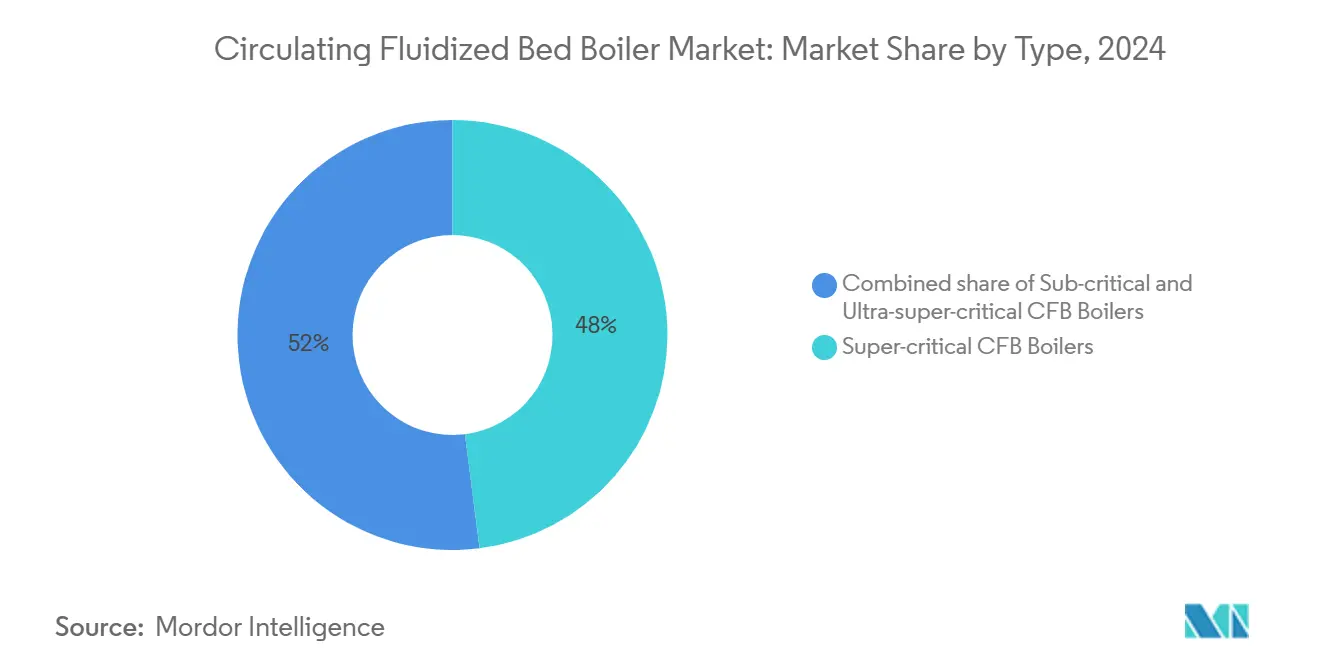

- By type, super-critical units held 48% of the circulating fluidized bed boiler market share in 2024. ultra-super-critical units are forecast to register the fastest 4.85% CAGR through 2030.

- By fuel, ecoal/ignite accounted for a 63.2% share of the circulating fluidized bed boiler market size in 2024, and biomass and agricultural residue id projected to post a 5.42% CAGR over 2025-2030.

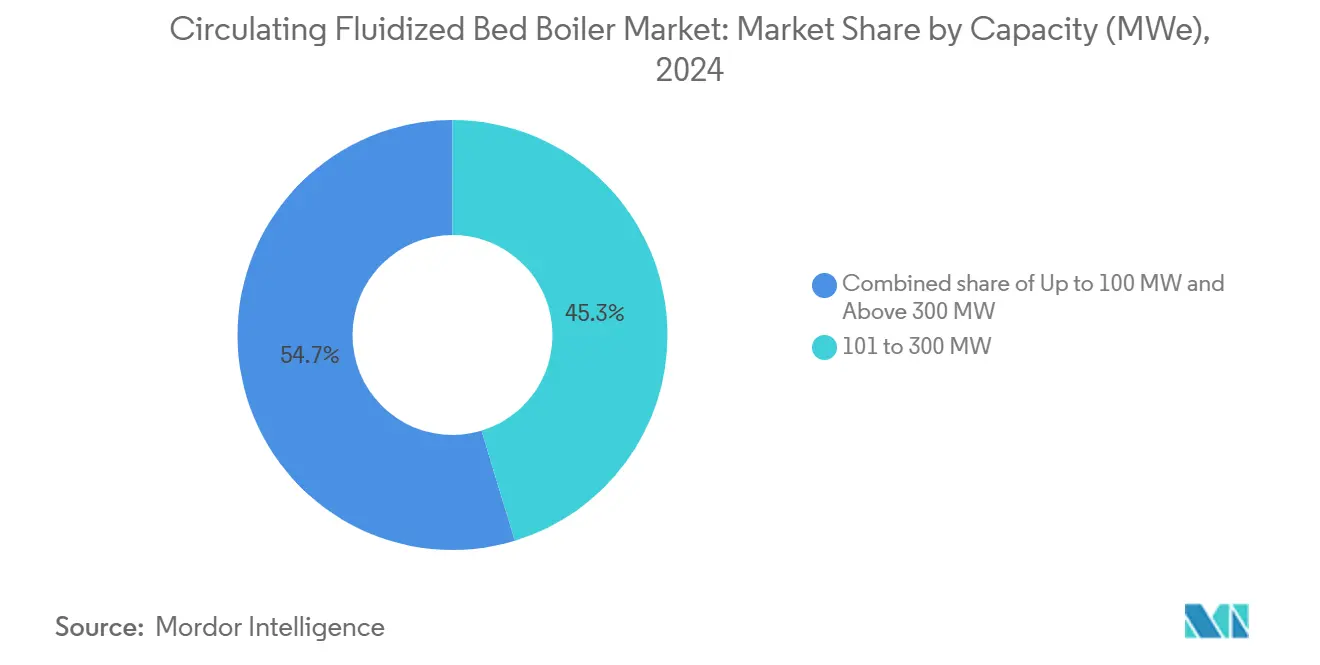

- By capacity, the 101 to 300 MW segment represented a 45.3% share of the circulating fluidized bed boiler market size in 2024, and the same is also forecasted to climb at 4.52% CAGR through 2030.

- By application, Power generation dominated 71.2% of the circulating fluidized bed boiler market size in 2024. Industrial process heat is set to rise at a 4.63% CAGR between 2025-2030.

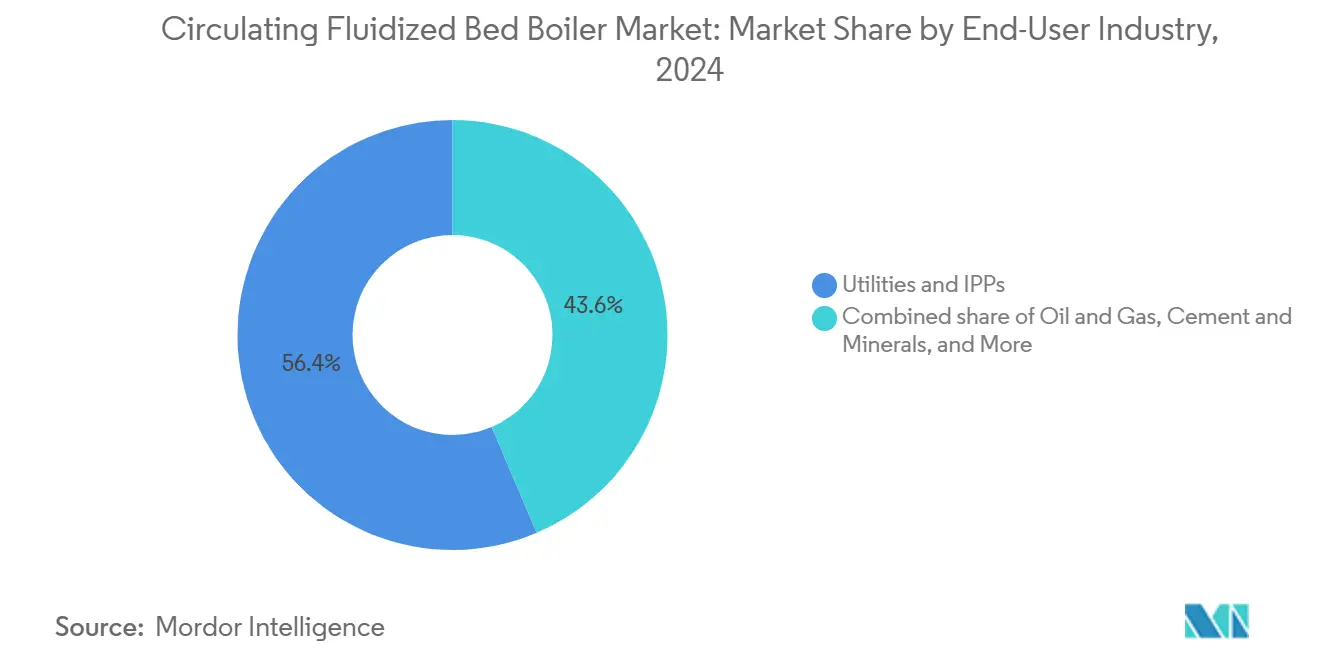

- By end-user industry, utilities and IPPs held 56.4% of the circulating fluidized bed boiler market share in 2024. while the cement and minerals segment is forecasted to register the fastest 5.02% CAGR through 2030.

- By geography, the Asia Pacific commanded 41.43% revenue share in 2024 and is expected to expand at a 4.86% CAGR to 2030.

Global Circulating Fluidized Bed Boiler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter SOx/NOx emission norms worldwide | +1.2% | EU, China, global adoption | Medium term (2-4 years) |

| Efficient combustion of low-grade solid fuels | +0.8% | Asia Pacific core, MEA spill-over | Long term (≥4 years) |

| Retirement of aging sub-critical coal plants | +0.9% | North America, EU, emerging in Asia Pacific | Medium term (2-4 years) |

| Industrial heat demand from chemicals & O&G | +0.6% | Global, petrochemical hubs | Long term (≥4 years) |

| Waste-to-energy mandates enabling co-firing | +0.5% | EU core, North America expansion | Short term (≤2 years) |

| Incentives for decentralized biomass CFB | +0.4% | Southeast Asia, pilot schemes in India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter SOx/NOx emission norms worldwide

Tightening air-pollution standards accelerate the circulating fluidized bed boiler market technology adoption because its low-temperature combustion curbs NOx and its in-situ limestone injection captures SO₂. The European Union reported 92% cuts in SO₂ and dust, plus 70% NOx reduction from large plants between 2004-2022.[1]European Environment Agency, “Emissions and energy use in large combustion plants in Europe,” eea.europa.eu China’s updated national rules require bed temperatures below 900 °C and optimized limestone sizing, reinforcing domestic demand. In the United States, the EPA’s May 2025 revision limits NOx to 0.40 lb/mmBtu, a target readily met by CFB firing.[2]U.S. Environmental Protection Agency, “40 CFR 76.7—Revised NOx Emission Limitations,” ecfr.gov

Efficient combustion of low-grade solid fuels

Fuel-flexible design lets operators burn lignite, washery rejects, petroleum coke and agricultural waste while still achieving up to 99% combustion efficiency. India’s coal-gasification initiative and China’s installed base of over 3,000 units exceeding 90 GW highlight large-scale deployment. Industrial users exploit the same versatility to co-fire bagasse, rice husk, and refuse-derived fuel, cutting disposal costs while meeting steam needs.

Retirement & replacement of aging sub-critical coal plants

Modernization programs in Poland, India, and the United States favor CFB retrofits or green-field additions that lift unit efficiencies above 41% and slash NOx by more than 70%. Ultra-super-critical trials in India target 46% gross efficiency, setting new performance benchmarks.

Industrial heat demand from chemicals & O&G sectors

Petrochemical, refinery, and fertilizer complexes value the steady steam supply and in-furnace emission control of circulating fluidized bed boiler market installations. Process-tailored CO boilers handle catalyst-regenerator off-gases, recover heat, and comply with sulfur caps. EU research under the SUSHEAT program identified almost 135 TWh per year of industrial heat demand between 150 °C-250 °C that could migrate to high-efficiency boilers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX versus conventional PC boilers | -0.7% | Global, particularly in cost-sensitive markets | Short term (≤ 2 years) |

| Design complexity leading to longer EPC lead-times | -0.5% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Rising competition from renewables & gas-fired capacity | -0.9% | EU and North America primarily | Long term (≥ 4 years) |

| Refractory-supply bottlenecks for large-scale units | -0.4% | Global, concentrated in mega-project markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX versus conventional PC boilers

Typical turnkey costs average USD 1,153 per kW, roughly 8-10% above comparable pulverized-coal projects owing to cyclones, refractory linings, and larger furnace footprints. Standardized modular designs and local fabrication are gradually cutting the premium, while lifecycle savings from built-in SO₂ capture offset part of the initial gap.

Rising competition from renewables & gas-fired capacity

Rapid solar, wind, and combined-cycle build-outs in Europe and North America erode coal plant load factors, squeezing investment appetite for new CFB units. Fuel-switching to biomass or waste and integration with carbon capture improve the technology’s resilience, as shown by a USD 246 million gas-conversion project in the United States that retained CFB architecture for future multi-fuel flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ultra-Super-Critical Technology Drives Efficiency Gains

Super-critical designs held 48% circulating fluidized bed boiler market share in 2024 on the strength of proven 600 MW Chinese references and multiple 800 MW awards in India.[3]Ministry of Heavy Industries, “Advanced Ultra Supercritical Technology for Thermal Power Plants,” heavyindustries.gov.in Ultra-super-critical variants are projected to log a 4.85% CAGR, benefiting from alloy breakthroughs that withstand steam at >25 MPa and 600 °C. Efficiency rises of up to 8 percentage points trim fuel bills and cut CO₂, justifying higher capital outlays. Sub-critical units persist in captive and retrofit roles where budget and space rule decisions.

Wider uptake underpins a healthy pipeline of demonstration projects in China, India, and Poland, with R&D focused on tube corrosion control and advanced controls that stabilize bed temperature. OEMs market reference plants aggressively as utilities weigh lifecycle economics rather than first cost alone. The circulating fluidized bed boiler market size for ultra-super-critical systems will expand notably after 2027 once material supply chains mature.

By Fuel: Biomass Adoption Accelerates Amid Sustainability Push

Coal and lignite supplied 63.23% of feedstock demand in 2024; however, dedicated biomass and residue firing is forecast for the quickest 5.42% CAGR. Nordic utilities have demonstrated 10-16% CO₂ cuts when co-firing pine chips with waste coal.[4]Bhoi & Sarkar, “Co-Firing of Pine Biomass and Waste Coal,” mdpi.com Municipal and industrial solid-waste projects in Kuwait and Alberta illustrate the growing waste-to-energy niche.

Multi-fuel flexibility is a de-risking feature for buyers concerned about future carbon costs and price swings. Pelletization of sugarcane by-products in Southeast Asia widens local biomass supply, while petroleum coke continues in select refinery-adjacent sites. Collectively, fuel diversification supports a broader circulating fluidized bed boiler market penetration across regions and industries.

By Capacity: Mid-Scale Units Dominate Utility Applications

Systems rated 101-300 MW accounted for 45.34% of global installations in 2024 and are projected to rise at a 4.52% CAGR. The size balances grid-support capability with moderate construction risk; typical Asian projects bundle two or three units for 300-900 MW. Units ≤100 MW cater to captive industrial steam and power, whereas >300 MW units, such as Poland’s 460 MW Lagisza plant, showcase the upper technical frontier.

Ongoing awards in India—for example, three 800 MW blocks at Telangana—suggest that large-scale interest remains, especially where domestic manufacturing lowers delivered cost. OEMs leverage modular furnace sections and shop-assembled cyclones to shorten schedules and standardize quality, keeping the circulating fluidized bed boiler market size growing in the utility segment.

By Application: Industrial Heat Segment Accelerates

Power generation contributed 71.2% of the circulating fluidized bed boiler market size in 2024, yet industrial steam duties are projected to expand at a 4.63% CAGR. EU research estimates 135 TWh/y of medium-temperature industrial heat is technically suitable for efficient boilers.

Petrochemical complexes, cement kilns, and pulp mills deploy CFB systems for on-site energy and waste fuel disposal. Combined heat-and-power schemes increase overall plant efficiency and enhance decarbonization credentials, keeping industrial adoption rising steadily.

By End-User Industry: Cement Sector Drives Growth

Electric utilities and IPPs retained 56.4% of demand in 2024, but cement and minerals processing are projected to have the quickest 5.02% CAGR through 2030. Kilns require large volumes of 800-1,000 °C process heat; CFB firing of alternative fuels such as bottom ash and refuse-derived fuel aligns with cost and sustainability goals.

Oil, gas, and chemicals continue to specify CFB units for reliable steam and off-gas combustion. Pulp-and-paper mills, food processors, and textile plants form an additional tail of adopters that keeps the circulating fluidized bed boiler industry diversified.

Geography Analysis

Asia Pacific retained 41.43% of the circulating fluidized bed boiler market revenue in 2024 and is forecast to advance at a 4.86% CAGR to 2030. China operates more than 3,000 units aggregating 90 GW, while India’s coal output surpassed 1 billion t in FY 2024-25 and underpins large super-critical awards to domestic OEMs. Government backing for advanced ultra-super-critical research further cements regional leadership.

Europe provides a strong regulatory pull, with SO₂, dust and NOx cuts encouraging plant owners to retrofit or replace aging assets with cleaner combustion. Poland’s 460 MW Lagisza CFB plant remains a flagship reference, and waste-to-energy directives widen prospects across the continent.

North America focuses on life-extension and fuel-switching. A Michigan plant conversion will couple biomass firing with carbon capture, while another multistate utility is shifting over 1 GW of coal capacity to gas, yet keeping CFB core components for potential future multi-fuel flexibility. South America and the Middle East & Africa show emerging opportunity, especially in urban waste management and cement production where secure baseload steam is mandatory.

Competitive Landscape

The global circulating fluidized bed boiler market is moderately concentrated. Sumitomo SHI Foster Wheeler, GE Steam Power and Babcock & Wilcox dominate high-parameter designs, while Asian groups such as BHEL, Harbin Boiler and Shanghai Electric leverage cost-effective fabrication and local supply chains. Babcock & Wilcox posted USD 181.2 million Q1 2025 revenue, up 10%, with a backlog of USD 526.8 million. BHEL secured orders worth more than INR 25,000 crore for super-critical projects, reinforcing its 55% share of India’s installed thermal capacity.

Competitive levers include proprietary cyclone geometry, in-house alloy production and digital monitoring platforms that optimize bed temperature and limestone feed. M&A activity, typified by Miura’s purchase of Cleaver-Brooks, signals a quest for scale and product diversity in industrial boilers. Service revenues tied to maintenance contracts, parts and retrofits now form a rising share of OEM income, reflecting the aging installed base.

Circulating Fluidized Bed Boiler Industry Leaders

Sumitomo SHI Foster Wheeler

GE Steam Power

Doosan Lentjes

Babcock & Wilcox Enterprises

Bharat Heavy Electricals Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Swedish utility Kraftringen Energi has chosen technology provider Valmet to supply a biomass-fired boiler and an advanced flue gas treatment system for its new combined heat and power (CHP) facility in Örtofta, Skåne.

- February 2025: Haryana Power Generation Corporation Ltd. awarded BHEL a substantial INR 5,500 crore contract. The contract mandates BHEL to establish a 1x800 MW ultra-supercritical unit at the Deen Bandhu Chhotu Ram Thermal Power Plant.

- November 2024: NTPC granted a Letter of Intent (LoI) to BHEL for the main plant package of the 3x800 MW Telangana Stage-II supercritical thermal power plant (STPP).

- September 2024: Babcock & Wilcox awarded front-end design for Canada’s first waste-to-energy plant with carbon capture.

Global Circulating Fluidized Bed Boiler Market Report Scope

| Sub-critical CFB Boilers |

| Super-critical CFB Boilers |

| Ultra-super-critical CFB Boilers |

| Coal/Lignite |

| Biomass and Agricultural Residue |

| Petroleum Coke |

| Municipal/Industrial Solid Waste |

| Multi-fuel (switchable) |

| Up to 100 MW |

| 101 to 300 MW |

| Above 300 MW |

| Power Generation |

| Industrial Process Heat |

| Utilities and IPPs |

| Oil and Gas (Up/Mid/Downstream) |

| Chemicals and Petrochemicals |

| Pulp and Paper |

| Cement and Minerals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Sub-critical CFB Boilers | |

| Super-critical CFB Boilers | ||

| Ultra-super-critical CFB Boilers | ||

| By Fuel | Coal/Lignite | |

| Biomass and Agricultural Residue | ||

| Petroleum Coke | ||

| Municipal/Industrial Solid Waste | ||

| Multi-fuel (switchable) | ||

| By Capacity (MWe) | Up to 100 MW | |

| 101 to 300 MW | ||

| Above 300 MW | ||

| By Application | Power Generation | |

| Industrial Process Heat | ||

| By End-user Industry | Utilities and IPPs | |

| Oil and Gas (Up/Mid/Downstream) | ||

| Chemicals and Petrochemicals | ||

| Pulp and Paper | ||

| Cement and Minerals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current circulating fluidized bed boiler market size?

The market stood at USD 994.27 million in 2025 and is forecast to reach USD 1,174.83 million by 2030.

Which region leads demand?

Asia Pacific holds 41.43% of global revenue thanks to large-scale projects in China and India.

Which type of CFB boiler is growing fastest?

Ultra-super-critical designs are projected to post a 4.85% CAGR through 2030 due to higher efficiency.

How are emission rules influencing adoption?

Stricter SOx/NOx caps in the EU, China and the U.S. push operators toward CFB units that meet limits without costly scrubbing.

Which industry beyond utilities is adopting CFB technology quickly?

Cement and minerals processing is forecast for a 5.02% CAGR as plants seek low-carbon heat and alternative-fuel capability.

Page last updated on: